Project Report: Management Accounting

VerifiedAdded on 2023/06/15

|8

|1048

|261

AI Summary

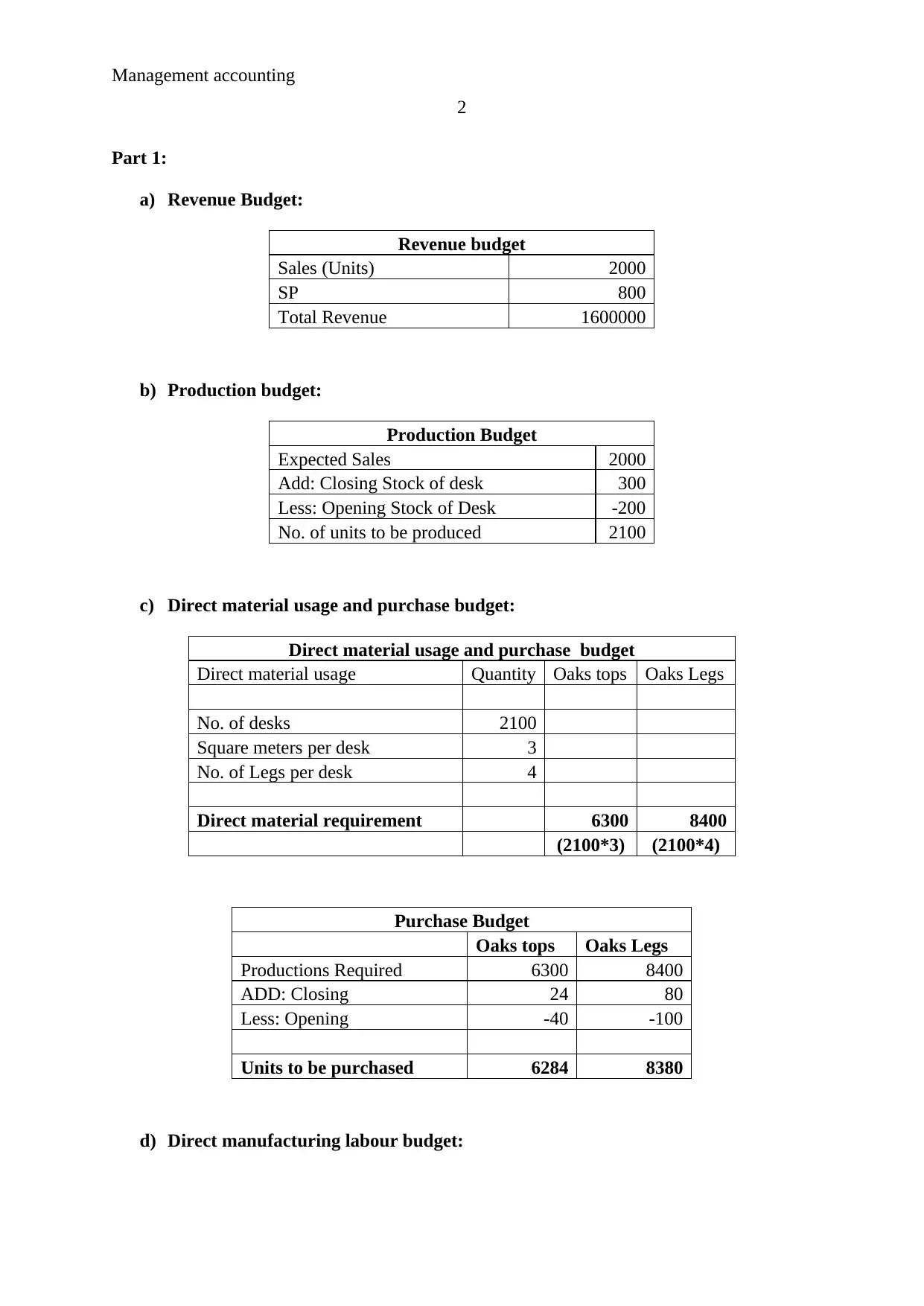

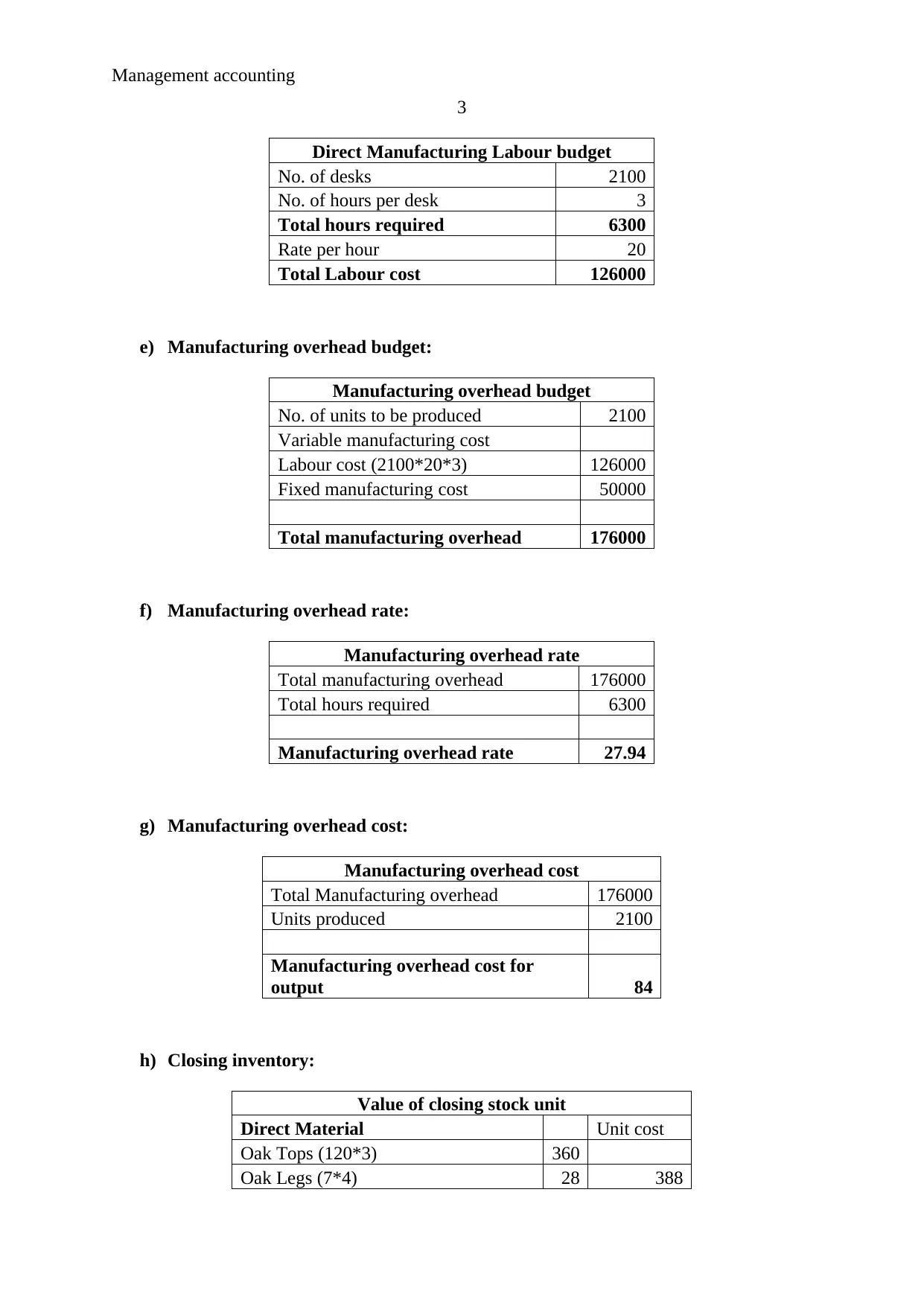

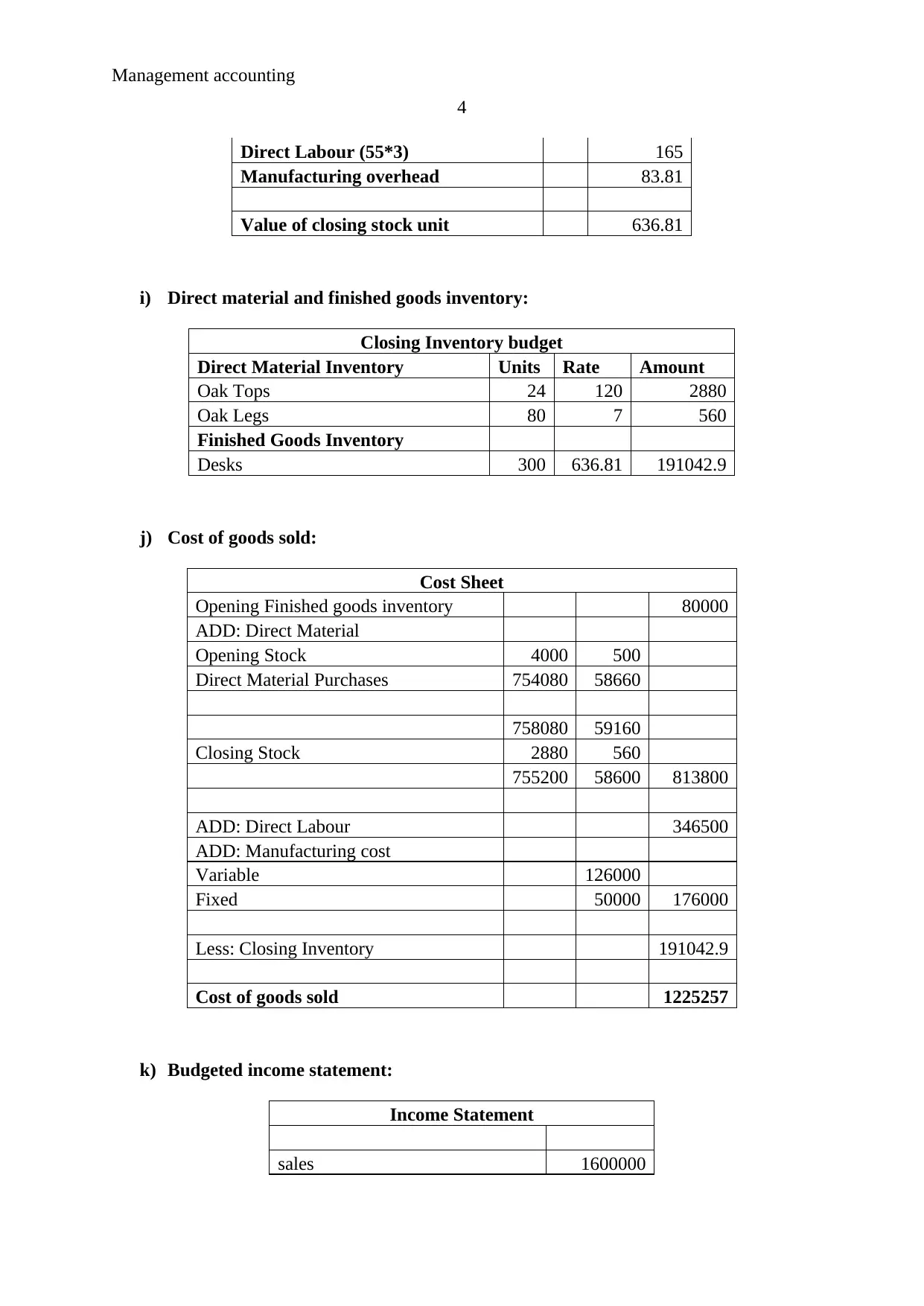

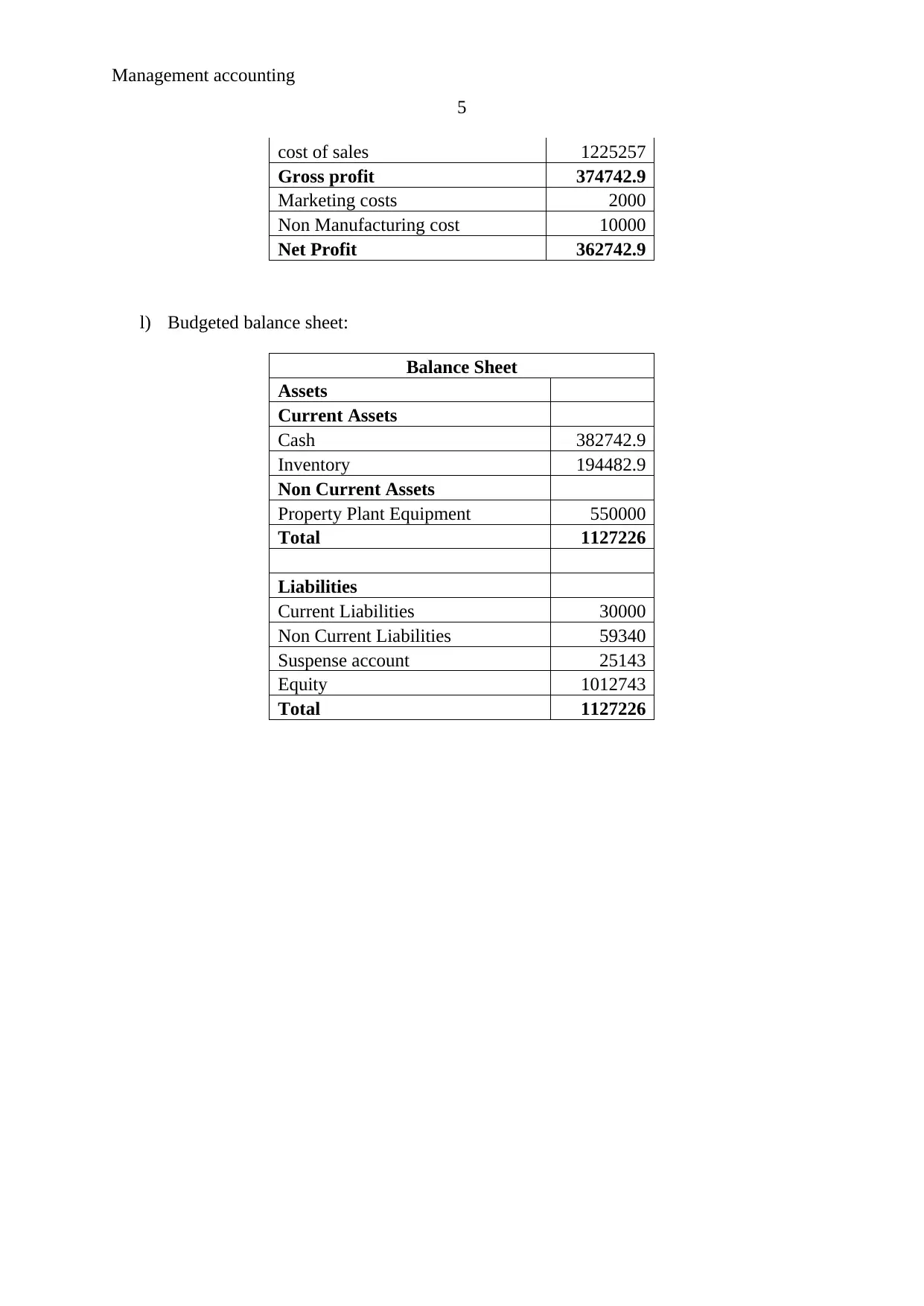

This project report covers revenue budget, production budget, direct material usage and purchase budget, direct manufacturing labour budget, manufacturing overhead budget, closing inventory, direct material and finished goods inventory, cost of goods sold, budgeted income statement, and budgeted balance sheet. It also suggests strategies for budgeting such as balance scorecard, JIT, activity-based costing, and treatment of non-manufacturing cost.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.