Performance Analysis of Amana Ltd. with Recommendations Report

VerifiedAdded on 2023/06/06

|11

|3037

|310

Report

AI Summary

This report provides a comprehensive analysis of Amana Ltd.'s financial performance, focusing on management accounting principles. It includes a detailed examination of the company's original, flexed, and actual budgets, along with a variance analysis to identify areas of improvement. The report calculates and interprets material, labor, variable overhead, and fixed overhead variances, offering insights into the company's cost management. Based on these findings, the report offers specific recommendations to Amana's CEO, focusing on budgeting, process assessment, and variance analysis reporting. Furthermore, the report evaluates two strategic options for the company: establishing its own online platform versus utilizing Amazon's platform, comparing the associated costs per unit to inform a strategic decision. The analysis emphasizes cost considerations, the importance of a proper pricing strategy, and the overall ability to achieve organizational objectives.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

PART – A........................................................................................................................................3

Monthly Control Report Showing Original Budget, Flexed Budget, And Variances.................3

Report on the performance of Amana Ltd. for year 2020...........................................................4

Recommendations to Amana’s CEO On Areas of Improvement................................................6

PART B...........................................................................................................................................7

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

PART – A........................................................................................................................................3

Monthly Control Report Showing Original Budget, Flexed Budget, And Variances.................3

Report on the performance of Amana Ltd. for year 2020...........................................................4

Recommendations to Amana’s CEO On Areas of Improvement................................................6

PART B...........................................................................................................................................7

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting us related with having the significant formulation of reports and

statement so that help for making the strategic decision in order to incline the business

performance. In the current era, it is important for the organization to have effective management

accounting in turn attaining the effective level of growth & development to achieve competitive

performance. The current report is based on Amana Ltd which operates in tourist business by

offering the varied level of locations. It will pay attention on having the significant information

regarding the original and flexed budget and variances. This will help in gaining the corrective

information regarding evaluation of the options regarding going online by setting up own

platform or selling on Amazon so that depth understanding to make decision in effective pattern.

MAIN BODY

PART – A

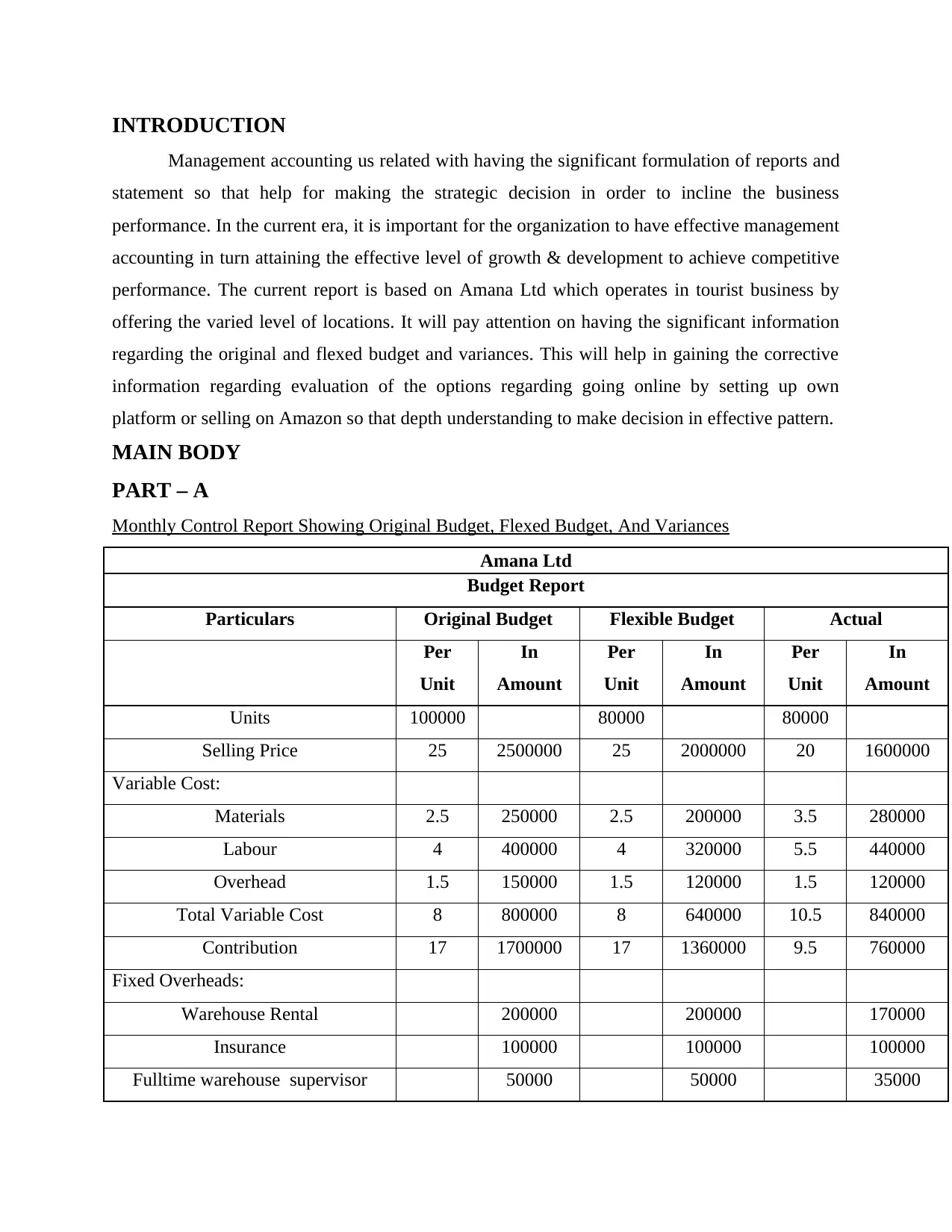

Monthly Control Report Showing Original Budget, Flexed Budget, And Variances

Amana Ltd

Budget Report

Particulars Original Budget Flexible Budget Actual

Per

Unit

In

Amount

Per

Unit

In

Amount

Per

Unit

In

Amount

Units 100000 80000 80000

Selling Price 25 2500000 25 2000000 20 1600000

Variable Cost:

Materials 2.5 250000 2.5 200000 3.5 280000

Labour 4 400000 4 320000 5.5 440000

Overhead 1.5 150000 1.5 120000 1.5 120000

Total Variable Cost 8 800000 8 640000 10.5 840000

Contribution 17 1700000 17 1360000 9.5 760000

Fixed Overheads:

Warehouse Rental 200000 200000 170000

Insurance 100000 100000 100000

Fulltime warehouse supervisor 50000 50000 35000

Management accounting us related with having the significant formulation of reports and

statement so that help for making the strategic decision in order to incline the business

performance. In the current era, it is important for the organization to have effective management

accounting in turn attaining the effective level of growth & development to achieve competitive

performance. The current report is based on Amana Ltd which operates in tourist business by

offering the varied level of locations. It will pay attention on having the significant information

regarding the original and flexed budget and variances. This will help in gaining the corrective

information regarding evaluation of the options regarding going online by setting up own

platform or selling on Amazon so that depth understanding to make decision in effective pattern.

MAIN BODY

PART – A

Monthly Control Report Showing Original Budget, Flexed Budget, And Variances

Amana Ltd

Budget Report

Particulars Original Budget Flexible Budget Actual

Per

Unit

In

Amount

Per

Unit

In

Amount

Per

Unit

In

Amount

Units 100000 80000 80000

Selling Price 25 2500000 25 2000000 20 1600000

Variable Cost:

Materials 2.5 250000 2.5 200000 3.5 280000

Labour 4 400000 4 320000 5.5 440000

Overhead 1.5 150000 1.5 120000 1.5 120000

Total Variable Cost 8 800000 8 640000 10.5 840000

Contribution 17 1700000 17 1360000 9.5 760000

Fixed Overheads:

Warehouse Rental 200000 200000 170000

Insurance 100000 100000 100000

Fulltime warehouse supervisor 50000 50000 35000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

salary

A AV RI NCES

Material o t arianceC s V -80000 n a ora le(u f v b )

tandard o t o Material edS C s f s Us (2.5 * 80000) 200000

Act al o t o Material edu C s f s Us (3.5 * 80000) 280000

Material Price arianceV -1 n a ora le(u f v b )

tandard Price o Material per nitS f u 2.5

Act al Price o Material per nitu f u 3.5

a or o t arianceL b C s V -120000 n a ora le(u f v b )

tandard a e or a or o r edS W g s f L b h u s us (4 * 80000) 320000

Act al a e or a or o r edu W g s f L b h u s us (5.5 * 80000) 440000

a or ate arianceL b R V -1.5 n a ora le(u f v b )

tandard ate o la or or prod cin one nitS R f b f u g u 4

Act al ate o la or or prod cin one nitu R f b f u g u 5.5

aria le er ead o t arianceV b Ov h C s V 0

tandard aria le er eadS V b Ov h (1.5 *80000) 120000

Act al aria le er eadu V b Ov h (1.5 *80000) 120000

aria le er ead ate arianceV b Ov h R V 0

tandard aria le er ead ateS V b Ov h R 1.5

Act al aria le er ead ateu V b Ov h R 1.5

i ed er ead o t arianceF x Ov h C s V 45000 (favorable)

tandard i ed er eadS F x Ov h (200000 + 100000 + 50000) 350000

Act al i ed er eadu F x Ov h (170000 + 100000 + 35000) 305000

i ed er ead Per nit arianceF x Ov h U V -0.6 (favorable)

tandard i ed er ead Per nitS F x Ov h U (350000 / 80000) 4.4

Act al i ed er ead Per nitu F x Ov h U (305000 / 80000) 3.8

Report on the performance of Amana Ltd. for year 2020

On the basis of the control report the performance of the Amana Ltd. can be analysed.

The control report showing original, flexed and actual budgets is prepared on the basis of the

units. The original budget is prepared as per the production expectations of 100,000 units. The

actual expenditures for the month are for 80,000 units. The preparation of flexed budget is done

A AV RI NCES

Material o t arianceC s V -80000 n a ora le(u f v b )

tandard o t o Material edS C s f s Us (2.5 * 80000) 200000

Act al o t o Material edu C s f s Us (3.5 * 80000) 280000

Material Price arianceV -1 n a ora le(u f v b )

tandard Price o Material per nitS f u 2.5

Act al Price o Material per nitu f u 3.5

a or o t arianceL b C s V -120000 n a ora le(u f v b )

tandard a e or a or o r edS W g s f L b h u s us (4 * 80000) 320000

Act al a e or a or o r edu W g s f L b h u s us (5.5 * 80000) 440000

a or ate arianceL b R V -1.5 n a ora le(u f v b )

tandard ate o la or or prod cin one nitS R f b f u g u 4

Act al ate o la or or prod cin one nitu R f b f u g u 5.5

aria le er ead o t arianceV b Ov h C s V 0

tandard aria le er eadS V b Ov h (1.5 *80000) 120000

Act al aria le er eadu V b Ov h (1.5 *80000) 120000

aria le er ead ate arianceV b Ov h R V 0

tandard aria le er ead ateS V b Ov h R 1.5

Act al aria le er ead ateu V b Ov h R 1.5

i ed er ead o t arianceF x Ov h C s V 45000 (favorable)

tandard i ed er eadS F x Ov h (200000 + 100000 + 50000) 350000

Act al i ed er eadu F x Ov h (170000 + 100000 + 35000) 305000

i ed er ead Per nit arianceF x Ov h U V -0.6 (favorable)

tandard i ed er ead Per nitS F x Ov h U (350000 / 80000) 4.4

Act al i ed er ead Per nitu F x Ov h U (305000 / 80000) 3.8

Report on the performance of Amana Ltd. for year 2020

On the basis of the control report the performance of the Amana Ltd. can be analysed.

The control report showing original, flexed and actual budgets is prepared on the basis of the

units. The original budget is prepared as per the production expectations of 100,000 units. The

actual expenditures for the month are for 80,000 units. The preparation of flexed budget is done

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

for 80,000 units. Flexed budget is being compared with the actual expenditures that were

incurred during the year. On the basis of such comparison variances are calculated. Using the

calculated variances performance of the Amana Ltd. can be interpreted. Below is the assessment

of above calculated variances.

1. Material Variance: Material Variance is inclusion of material cost variance as well as the

material price variance. The material cost variance is computed from two values that are

standard cost that should be incurred by the company for the production of 80,000 units

and the actual cost that the company, Amana Ltd has incurred for producing such number

of units (Knardal and Bjørnenak, 2020). The standard cost is equals to 200,000 whereas the

actual expense that the company has beard is equals to 280000. It means that there is a

change of 80000 in both values. This difference between standard and actual values is

unfavourable for the company as the actual expense is higher than the standard expenses.

Further the Material Rate that was set as the standard rate for material to be used in per

unit is 2.5 and the actual rate incurred for per unit material is 3.5. the difference is of 1.

This difference is because of excess of actual rate over the standard rate. Hence such a

difference is undesirable for the performance of the company.

2. Labour Variance: There are types of labour variances whose calculation is depicted above

that are labour cost variance and the labour rate variance. The labour that was set as

standard rate accounts to be 4 and the actual rate at which the company was able to

arrange the labour is 5.5. So the actual is more than the standard by 1.5, again an

unfavourable variance for the company (Eldenburg and et.al., 2020). The total cost to the

company for producing 80000 units is 440000 and as per the standard set into the flexed

budget it should be 320000 for the such production volume. The variance is of 120000

indicating low performance of the company.

3. Variable Overhead Variance: The variable overhead variances that are computed for

Amana Ltd. are variable overhead cost variance and variable overhead rate variance.

Both of these variances are as per the standard predefined by the company. The standard

variable rate was predefined as 1.5 per unit and the actual is same. And also the variable

cost overhead as per the standard value and the actual expense is same that is 120000.

This indicates that on this criteria of variable overhead expense the company’s

performance is up to the mark.

incurred during the year. On the basis of such comparison variances are calculated. Using the

calculated variances performance of the Amana Ltd. can be interpreted. Below is the assessment

of above calculated variances.

1. Material Variance: Material Variance is inclusion of material cost variance as well as the

material price variance. The material cost variance is computed from two values that are

standard cost that should be incurred by the company for the production of 80,000 units

and the actual cost that the company, Amana Ltd has incurred for producing such number

of units (Knardal and Bjørnenak, 2020). The standard cost is equals to 200,000 whereas the

actual expense that the company has beard is equals to 280000. It means that there is a

change of 80000 in both values. This difference between standard and actual values is

unfavourable for the company as the actual expense is higher than the standard expenses.

Further the Material Rate that was set as the standard rate for material to be used in per

unit is 2.5 and the actual rate incurred for per unit material is 3.5. the difference is of 1.

This difference is because of excess of actual rate over the standard rate. Hence such a

difference is undesirable for the performance of the company.

2. Labour Variance: There are types of labour variances whose calculation is depicted above

that are labour cost variance and the labour rate variance. The labour that was set as

standard rate accounts to be 4 and the actual rate at which the company was able to

arrange the labour is 5.5. So the actual is more than the standard by 1.5, again an

unfavourable variance for the company (Eldenburg and et.al., 2020). The total cost to the

company for producing 80000 units is 440000 and as per the standard set into the flexed

budget it should be 320000 for the such production volume. The variance is of 120000

indicating low performance of the company.

3. Variable Overhead Variance: The variable overhead variances that are computed for

Amana Ltd. are variable overhead cost variance and variable overhead rate variance.

Both of these variances are as per the standard predefined by the company. The standard

variable rate was predefined as 1.5 per unit and the actual is same. And also the variable

cost overhead as per the standard value and the actual expense is same that is 120000.

This indicates that on this criteria of variable overhead expense the company’s

performance is up to the mark.

4. Fixed Overhead Variance: The next variance on the basis of which interpretations

regarding Amana Ltd.’s performance can be made is the fixed overhead variance. This is

again computed on two criteria Fixed overhead cost variance and Fixed overhead rate

variance (Maheshwari, Maheshwari and Maheshwari, 2021). The fixed overhead expenses of the

firm according to the flexed budget are 200000 for the warehouse rental, 100000 for

insurance and 500000 for the salary to be paid to supervisor of warehouse for the

fulltime. And for the period the actual expenses of the firm over such fixed overhead

expenses accounts to be 170000, 100000 and 35000 for warehouse rent, insurance and

fulltime warehouse supervisor salary respectively. The total of such expenses in the

actual expenditure is 305000 and standard total is 350000, a difference of 45,000. The

variance is favourable as the actual expense is lower than the standard expenses.

Computation of fixed overhead per unit variance is done by dividing the total of expenses

by the total of unit produced. This gives standard fixed overhead per unit as 4.4 and the

actual fixed overhead per unit comes to be 3.8. The variance that is actual minus standard

is – 0.6 per unit, favourable for the company as actual expenditure per unit is lower than

the standard expense per unit.

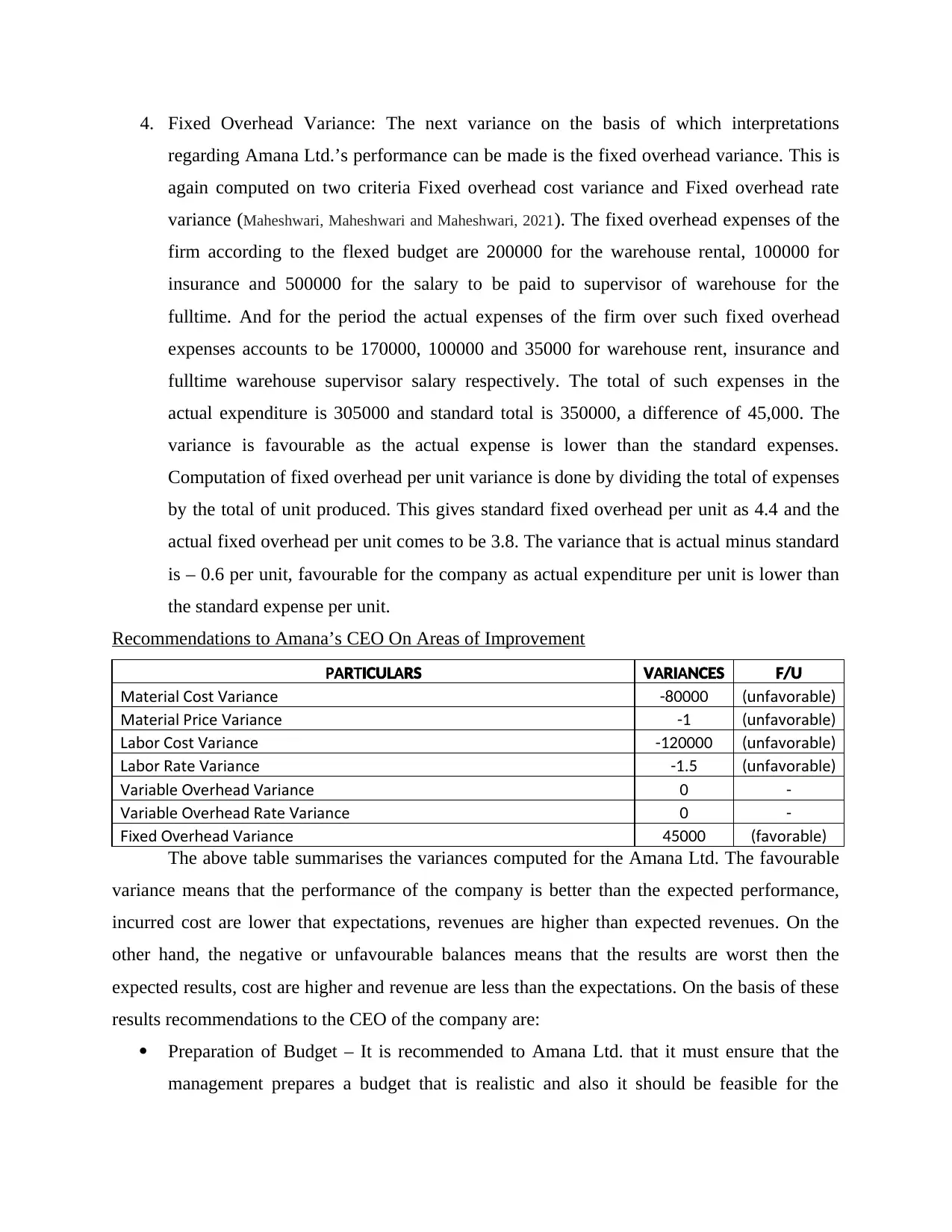

Recommendations to Amana’s CEO On Areas of Improvement

PA T AR ICUL RS A AV RI NCES F/U

Material o t arianceC s V -80000 n a ora le(u f v b )

Material Price arianceV -1 n a ora le(u f v b )

a or o t arianceL b C s V -120000 n a ora le(u f v b )

a or ate arianceL b R V -1.5 n a ora le(u f v b )

aria le er ead arianceV b Ov h V 0 -

aria le er ead ate arianceV b Ov h R V 0 -

i ed er ead arianceF x Ov h V 45000 a ora le(f v b )

The above table summarises the variances computed for the Amana Ltd. The favourable

variance means that the performance of the company is better than the expected performance,

incurred cost are lower that expectations, revenues are higher than expected revenues. On the

other hand, the negative or unfavourable balances means that the results are worst then the

expected results, cost are higher and revenue are less than the expectations. On the basis of these

results recommendations to the CEO of the company are:

Preparation of Budget – It is recommended to Amana Ltd. that it must ensure that the

management prepares a budget that is realistic and also it should be feasible for the

regarding Amana Ltd.’s performance can be made is the fixed overhead variance. This is

again computed on two criteria Fixed overhead cost variance and Fixed overhead rate

variance (Maheshwari, Maheshwari and Maheshwari, 2021). The fixed overhead expenses of the

firm according to the flexed budget are 200000 for the warehouse rental, 100000 for

insurance and 500000 for the salary to be paid to supervisor of warehouse for the

fulltime. And for the period the actual expenses of the firm over such fixed overhead

expenses accounts to be 170000, 100000 and 35000 for warehouse rent, insurance and

fulltime warehouse supervisor salary respectively. The total of such expenses in the

actual expenditure is 305000 and standard total is 350000, a difference of 45,000. The

variance is favourable as the actual expense is lower than the standard expenses.

Computation of fixed overhead per unit variance is done by dividing the total of expenses

by the total of unit produced. This gives standard fixed overhead per unit as 4.4 and the

actual fixed overhead per unit comes to be 3.8. The variance that is actual minus standard

is – 0.6 per unit, favourable for the company as actual expenditure per unit is lower than

the standard expense per unit.

Recommendations to Amana’s CEO On Areas of Improvement

PA T AR ICUL RS A AV RI NCES F/U

Material o t arianceC s V -80000 n a ora le(u f v b )

Material Price arianceV -1 n a ora le(u f v b )

a or o t arianceL b C s V -120000 n a ora le(u f v b )

a or ate arianceL b R V -1.5 n a ora le(u f v b )

aria le er ead arianceV b Ov h V 0 -

aria le er ead ate arianceV b Ov h R V 0 -

i ed er ead arianceF x Ov h V 45000 a ora le(f v b )

The above table summarises the variances computed for the Amana Ltd. The favourable

variance means that the performance of the company is better than the expected performance,

incurred cost are lower that expectations, revenues are higher than expected revenues. On the

other hand, the negative or unfavourable balances means that the results are worst then the

expected results, cost are higher and revenue are less than the expectations. On the basis of these

results recommendations to the CEO of the company are:

Preparation of Budget – It is recommended to Amana Ltd. that it must ensure that the

management prepares a budget that is realistic and also it should be feasible for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

enterprise to achieve it during the time for which it has been prepared. Having a realistic

budget facilitates the management to accomplish the goals.

Figure Projection – Another recommendation for Amana Ltd is that it should reconsider

the standard amount that are set for materials, labour and variable overheads to ensure

that these are updated (Assrfa and et.al., 2020).

Assessing the Processes – Further it must be ensured that all the processes that are carried

by the company are such that it omits every kind to activities that leads to wastage of

materials.

Preparation of variance analysis report – It is recommended for the Amana Ltd. to

prepare a variance analysis report. Such a report will help the company to outline all the

reasons behind the unfavourable balances so that the company can reconsider it and take

the essential measures for its resolving (Erokhin and et.al., 2019). For instance, the report

may bring into light that the current supplier is selling low quality material at the price of

standard material and because of the company’s is spending more on wastage production.

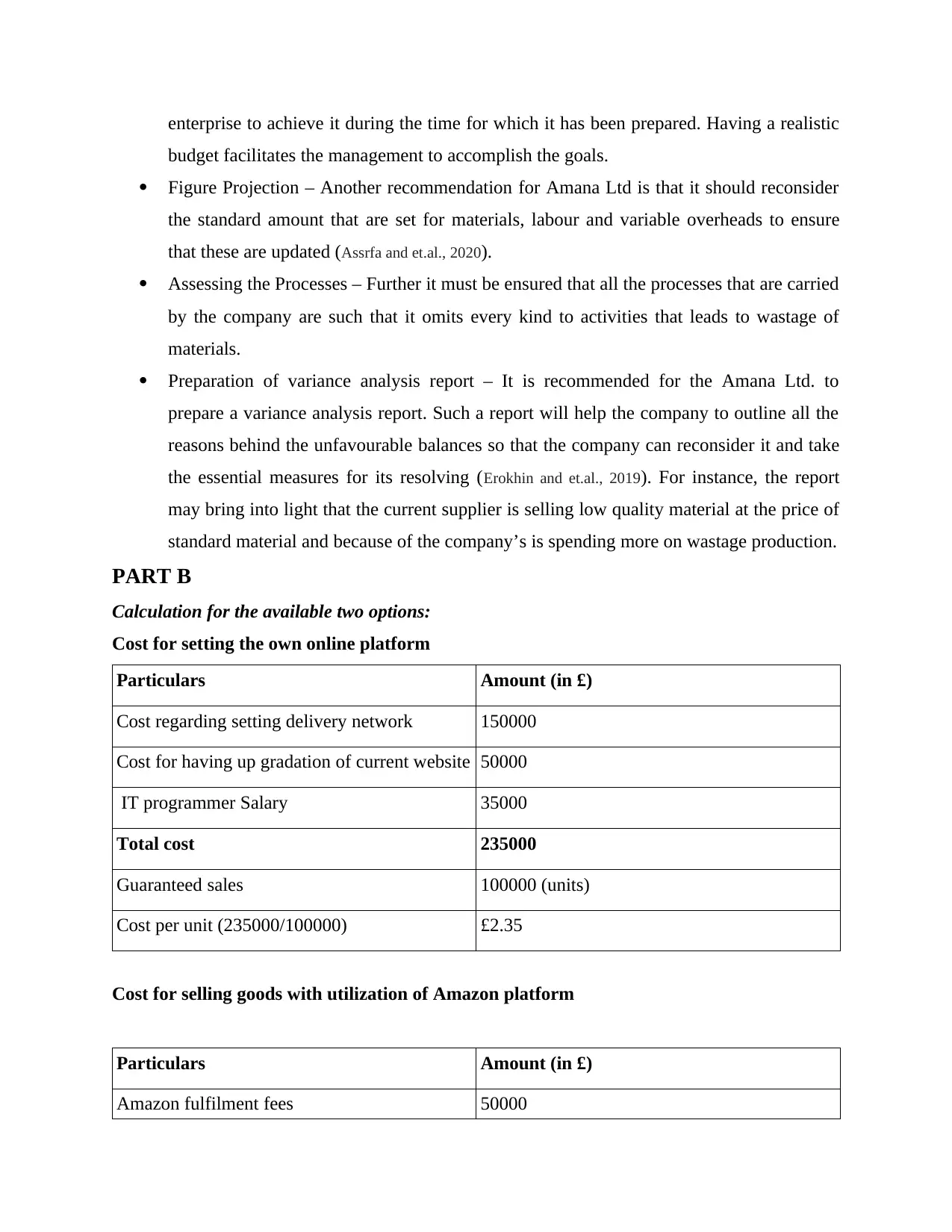

PART B

Calculation for the available two options:

Cost for setting the own online platform

Particulars Amount (in £)

Cost regarding setting delivery network 150000

Cost for having up gradation of current website 50000

IT programmer Salary 35000

Total cost 235000

Guaranteed sales 100000 (units)

Cost per unit (235000/100000) £2.35

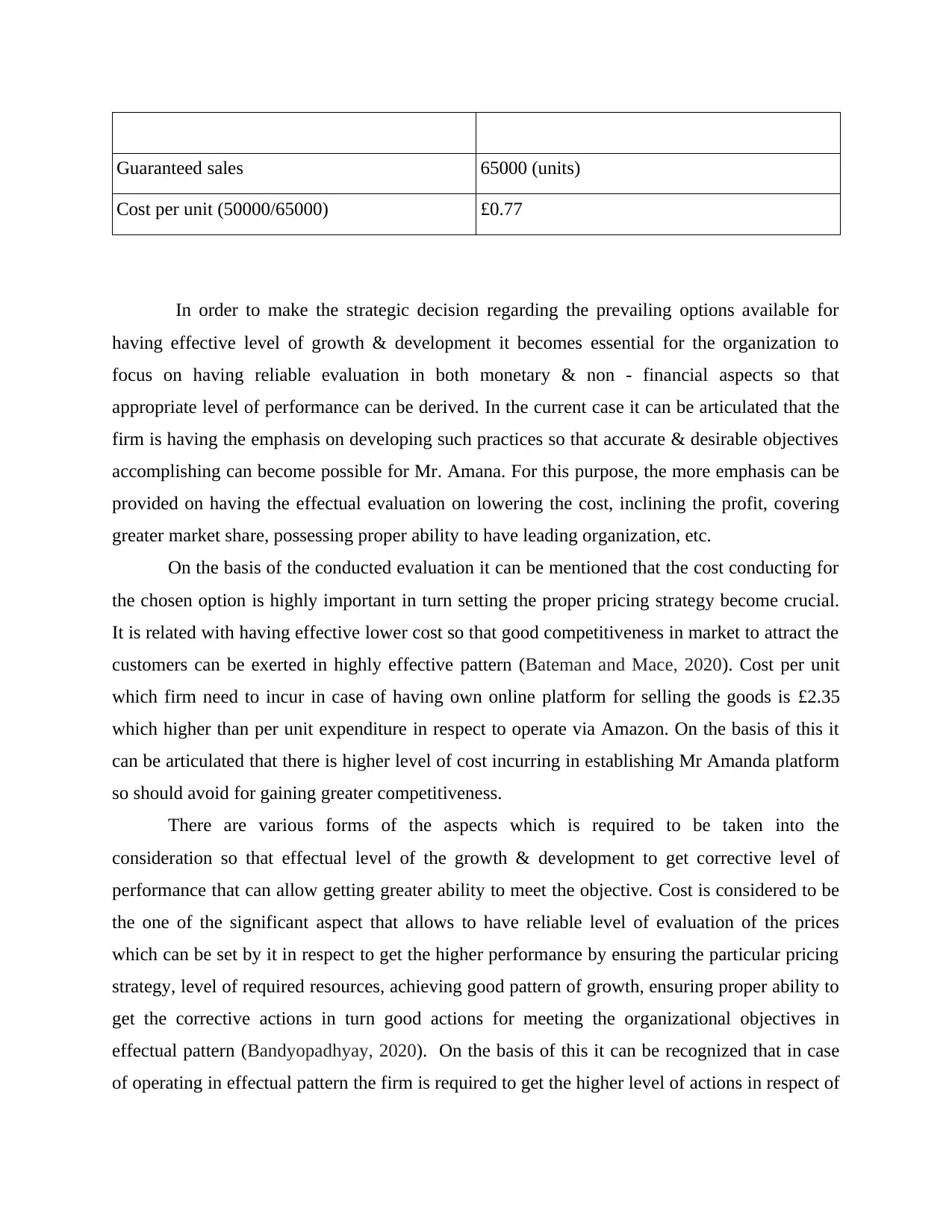

Cost for selling goods with utilization of Amazon platform

Particulars Amount (in £)

Amazon fulfilment fees 50000

budget facilitates the management to accomplish the goals.

Figure Projection – Another recommendation for Amana Ltd is that it should reconsider

the standard amount that are set for materials, labour and variable overheads to ensure

that these are updated (Assrfa and et.al., 2020).

Assessing the Processes – Further it must be ensured that all the processes that are carried

by the company are such that it omits every kind to activities that leads to wastage of

materials.

Preparation of variance analysis report – It is recommended for the Amana Ltd. to

prepare a variance analysis report. Such a report will help the company to outline all the

reasons behind the unfavourable balances so that the company can reconsider it and take

the essential measures for its resolving (Erokhin and et.al., 2019). For instance, the report

may bring into light that the current supplier is selling low quality material at the price of

standard material and because of the company’s is spending more on wastage production.

PART B

Calculation for the available two options:

Cost for setting the own online platform

Particulars Amount (in £)

Cost regarding setting delivery network 150000

Cost for having up gradation of current website 50000

IT programmer Salary 35000

Total cost 235000

Guaranteed sales 100000 (units)

Cost per unit (235000/100000) £2.35

Cost for selling goods with utilization of Amazon platform

Particulars Amount (in £)

Amazon fulfilment fees 50000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Guaranteed sales 65000 (units)

Cost per unit (50000/65000) £0.77

In order to make the strategic decision regarding the prevailing options available for

having effective level of growth & development it becomes essential for the organization to

focus on having reliable evaluation in both monetary & non - financial aspects so that

appropriate level of performance can be derived. In the current case it can be articulated that the

firm is having the emphasis on developing such practices so that accurate & desirable objectives

accomplishing can become possible for Mr. Amana. For this purpose, the more emphasis can be

provided on having the effectual evaluation on lowering the cost, inclining the profit, covering

greater market share, possessing proper ability to have leading organization, etc.

On the basis of the conducted evaluation it can be mentioned that the cost conducting for

the chosen option is highly important in turn setting the proper pricing strategy become crucial.

It is related with having effective lower cost so that good competitiveness in market to attract the

customers can be exerted in highly effective pattern (Bateman and Mace, 2020). Cost per unit

which firm need to incur in case of having own online platform for selling the goods is £2.35

which higher than per unit expenditure in respect to operate via Amazon. On the basis of this it

can be articulated that there is higher level of cost incurring in establishing Mr Amanda platform

so should avoid for gaining greater competitiveness.

There are various forms of the aspects which is required to be taken into the

consideration so that effectual level of the growth & development to get corrective level of

performance that can allow getting greater ability to meet the objective. Cost is considered to be

the one of the significant aspect that allows to have reliable level of evaluation of the prices

which can be set by it in respect to get the higher performance by ensuring the particular pricing

strategy, level of required resources, achieving good pattern of growth, ensuring proper ability to

get the corrective actions in turn good actions for meeting the organizational objectives in

effectual pattern (Bandyopadhyay, 2020). On the basis of this it can be recognized that in case

of operating in effectual pattern the firm is required to get the higher level of actions in respect of

Cost per unit (50000/65000) £0.77

In order to make the strategic decision regarding the prevailing options available for

having effective level of growth & development it becomes essential for the organization to

focus on having reliable evaluation in both monetary & non - financial aspects so that

appropriate level of performance can be derived. In the current case it can be articulated that the

firm is having the emphasis on developing such practices so that accurate & desirable objectives

accomplishing can become possible for Mr. Amana. For this purpose, the more emphasis can be

provided on having the effectual evaluation on lowering the cost, inclining the profit, covering

greater market share, possessing proper ability to have leading organization, etc.

On the basis of the conducted evaluation it can be mentioned that the cost conducting for

the chosen option is highly important in turn setting the proper pricing strategy become crucial.

It is related with having effective lower cost so that good competitiveness in market to attract the

customers can be exerted in highly effective pattern (Bateman and Mace, 2020). Cost per unit

which firm need to incur in case of having own online platform for selling the goods is £2.35

which higher than per unit expenditure in respect to operate via Amazon. On the basis of this it

can be articulated that there is higher level of cost incurring in establishing Mr Amanda platform

so should avoid for gaining greater competitiveness.

There are various forms of the aspects which is required to be taken into the

consideration so that effectual level of the growth & development to get corrective level of

performance that can allow getting greater ability to meet the objective. Cost is considered to be

the one of the significant aspect that allows to have reliable level of evaluation of the prices

which can be set by it in respect to get the higher performance by ensuring the particular pricing

strategy, level of required resources, achieving good pattern of growth, ensuring proper ability to

get the corrective actions in turn good actions for meeting the organizational objectives in

effectual pattern (Bandyopadhyay, 2020). On the basis of this it can be recognized that in case

of operating in effectual pattern the firm is required to get the higher level of actions in respect of

cost incurring. The cost utilization while operating via formulating own platform is greater that

can increase its complications in order to earn the profitability. The main objective of the earning

the profitability by declining cost which can be only become possible by focusing on having the

appropriate level of growth & development through meeting the objective of having proper

functioning. The higher cost in case of operating by formulating own platform can lead to offer

the varied level of challenges that can give more complexity which hampers the performance of

the organization.

It provides the assistance in taking such form of the corrective level of organizational

decision which can lead firm towards performance that can allow to meet the objectives of

having particular extent of guarantee sales which can permit to increase its competitiveness. This

offers the wide range of ability to competitive with similar organization operating in market. It

can promote corrective patter of strategies that can provide the assistance in attaining the

organizational objectives which can lead towards success (Florio, Morretta and Willak, 2018).

On the basis of this it can be mentioned that how specific firm is meeting the objective by

declining cost related with setting delivery network, up gradation of current website, offering

salary, etc. with help of the conducted evaluation it can be articulated that there is requirement of

having higher profitability in turn attaining the goal of possessing competitiveness.

From the analysis it can be articulated that the relevant cost for both the mentioned two

options is setting delivery network, up gradation of website, IT programmer salary, etc. are

offering the total cost such as 235000 which is higher than the expenses required to be incurred

for fulfillment fees which is 50000. This aids in identifying that there firm to adopt the selling

through Amazon which permits to have greater objective of having higher profitability &

stability. On the basis of this it can be mentioned that there are distinct types of the aspects which

provides the assistance in deriving the reliable organizational performance according to the

distinct types of objectives such as good ability to cover market share with less competition can

become possible when the organization is involving into the market. This become possible due

to the lower price offering as attracting the customers in effectual pattern become possible. With

referring the both the calculation and provided analysis it can be mentioned that the organization

can good pattern of growth & development when it focuses on sselling by establishing on

Amazon platform.

can increase its complications in order to earn the profitability. The main objective of the earning

the profitability by declining cost which can be only become possible by focusing on having the

appropriate level of growth & development through meeting the objective of having proper

functioning. The higher cost in case of operating by formulating own platform can lead to offer

the varied level of challenges that can give more complexity which hampers the performance of

the organization.

It provides the assistance in taking such form of the corrective level of organizational

decision which can lead firm towards performance that can allow to meet the objectives of

having particular extent of guarantee sales which can permit to increase its competitiveness. This

offers the wide range of ability to competitive with similar organization operating in market. It

can promote corrective patter of strategies that can provide the assistance in attaining the

organizational objectives which can lead towards success (Florio, Morretta and Willak, 2018).

On the basis of this it can be mentioned that how specific firm is meeting the objective by

declining cost related with setting delivery network, up gradation of current website, offering

salary, etc. with help of the conducted evaluation it can be articulated that there is requirement of

having higher profitability in turn attaining the goal of possessing competitiveness.

From the analysis it can be articulated that the relevant cost for both the mentioned two

options is setting delivery network, up gradation of website, IT programmer salary, etc. are

offering the total cost such as 235000 which is higher than the expenses required to be incurred

for fulfillment fees which is 50000. This aids in identifying that there firm to adopt the selling

through Amazon which permits to have greater objective of having higher profitability &

stability. On the basis of this it can be mentioned that there are distinct types of the aspects which

provides the assistance in deriving the reliable organizational performance according to the

distinct types of objectives such as good ability to cover market share with less competition can

become possible when the organization is involving into the market. This become possible due

to the lower price offering as attracting the customers in effectual pattern become possible. With

referring the both the calculation and provided analysis it can be mentioned that the organization

can good pattern of growth & development when it focuses on sselling by establishing on

Amazon platform.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

Based on the above study it is clear that management accounting is concerned with the

preparation of budgets, that helps the management to formulate effective strategic decisions. The

significance of preparing budgets lies the fact that it helps in analysing the performance of a

business organization. In the current report monthly control report has been prepared for the

Amana Ltd., a company in tourist industry, inclusive of the original and flexed budget and the

actual expenditures the firm incurs. On the basis of such control report a report has been

prepared that includes the performance of the company. Results of the variances calculated

represents the performance of the company on the basis of which recommendations have been

provided. The company’s decision of moving half on its business to online business has been

analysed in this report.

Based on the above study it is clear that management accounting is concerned with the

preparation of budgets, that helps the management to formulate effective strategic decisions. The

significance of preparing budgets lies the fact that it helps in analysing the performance of a

business organization. In the current report monthly control report has been prepared for the

Amana Ltd., a company in tourist industry, inclusive of the original and flexed budget and the

actual expenditures the firm incurs. On the basis of such control report a report has been

prepared that includes the performance of the company. Results of the variances calculated

represents the performance of the company on the basis of which recommendations have been

provided. The company’s decision of moving half on its business to online business has been

analysed in this report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Assrfa, M. and et.al., 2020. Designing of accounting information system for small and medium enterprises:

Application of PLS-SEM. International Journal of Sciences: Basic and Applied Research (IJSBAR)(2020)

Volume. 54. pp.124-139.

Bandyopadhyay, S., 2020. Pinch analysis for economic appraisal of sustainable projects. Process

Integration and Optimization for Sustainability. 4(2). pp.171-182.

Bateman, I.J. and Mace, G.M., 2020. The natural capital framework for sustainably efficient and

equitable decision making. Nature Sustainability. 3(10). pp.776-783.

Eldenburg, L. G. and et.al., 2020. Management accounting. John Wiley & Sons.

Erokhin, V. and et.al., 2019. Management accounting change as a sustainable economic development strategy

during pre-recession and recession periods: evidence from Russia. Sustainability. 11(11). p.3139.

Florio, M., Morretta, V. and Willak, W., 2018. Cost-benefit analysis and European Union

cohesion policy: Economic versus financial returns in investment project

appraisal. Journal of Benefit-Cost Analysis. 9(1). pp.147-180.s

Knardal, P. S. and Bjørnenak, T., 2020. Managerial characteristics and budget use in festival organizations. Journal

of management control. 31(4). pp.379-402.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of Management Accounting.

Sultan Chand & Sons.

1

Books and Journals

Assrfa, M. and et.al., 2020. Designing of accounting information system for small and medium enterprises:

Application of PLS-SEM. International Journal of Sciences: Basic and Applied Research (IJSBAR)(2020)

Volume. 54. pp.124-139.

Bandyopadhyay, S., 2020. Pinch analysis for economic appraisal of sustainable projects. Process

Integration and Optimization for Sustainability. 4(2). pp.171-182.

Bateman, I.J. and Mace, G.M., 2020. The natural capital framework for sustainably efficient and

equitable decision making. Nature Sustainability. 3(10). pp.776-783.

Eldenburg, L. G. and et.al., 2020. Management accounting. John Wiley & Sons.

Erokhin, V. and et.al., 2019. Management accounting change as a sustainable economic development strategy

during pre-recession and recession periods: evidence from Russia. Sustainability. 11(11). p.3139.

Florio, M., Morretta, V. and Willak, W., 2018. Cost-benefit analysis and European Union

cohesion policy: Economic versus financial returns in investment project

appraisal. Journal of Benefit-Cost Analysis. 9(1). pp.147-180.s

Knardal, P. S. and Bjørnenak, T., 2020. Managerial characteristics and budget use in festival organizations. Journal

of management control. 31(4). pp.379-402.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of Management Accounting.

Sultan Chand & Sons.

1

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.