Management Accounting Report for Tech (UK) Limited

VerifiedAdded on 2024/05/21

|28

|4253

|242

AI Summary

This report delves into the intricacies of management accounting, focusing on its application within Tech (UK) Limited. It explores the distinction between management and financial accounting, highlighting the essential requirements of a robust management accounting system. The report further examines various costing techniques, including marginal and absorption costing, and their role in preparing income statements. It also analyzes different types of budgets, their advantages and disadvantages, and their importance in planning and control. The report concludes by examining the balance scorecard approach and its application in managing financial problems to achieve sustainable success.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting report for Tech (UK) Limited

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Introduction:....................................................................................................................................4

Task 1...............................................................................................................................................5

a) Explanation of management accounting and the essential requirements of management

accounting system........................................................................................................................5

b) Presenting financial information.............................................................................................9

M1 Evaluate the benefits of management accounting systems and their application within an

organizational context................................................................................................................10

D1 critically evaluates how management accounting systems and management accounting

reporting is integrated within organizational processes.............................................................11

Task 2.............................................................................................................................................12

a) Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs..........................................................................................12

M2 accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents:..................................................................................................14

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities:....................................................................................................................................15

Task 3.............................................................................................................................................16

a) Different kinds of budgets and their advantages and disadvantages.....................................16

b) The budget preparation process including determination of pricing and different costing

systems that can be used............................................................................................................19

c) The importance of budget as a tool for planning and control purposes.................................20

Introduction:....................................................................................................................................4

Task 1...............................................................................................................................................5

a) Explanation of management accounting and the essential requirements of management

accounting system........................................................................................................................5

b) Presenting financial information.............................................................................................9

M1 Evaluate the benefits of management accounting systems and their application within an

organizational context................................................................................................................10

D1 critically evaluates how management accounting systems and management accounting

reporting is integrated within organizational processes.............................................................11

Task 2.............................................................................................................................................12

a) Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs..........................................................................................12

M2 accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents:..................................................................................................14

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities:....................................................................................................................................15

Task 3.............................................................................................................................................16

a) Different kinds of budgets and their advantages and disadvantages.....................................16

b) The budget preparation process including determination of pricing and different costing

systems that can be used............................................................................................................19

c) The importance of budget as a tool for planning and control purposes.................................20

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets....................................................................................................................21

D3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organizations to sustainable success..............................................................22

Task 4.............................................................................................................................................23

a) Balance scorecard approach..................................................................................................23

M4 Analyse how, in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................24

Conclusion:....................................................................................................................................26

References......................................................................................................................................27

forecasting budgets....................................................................................................................21

D3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organizations to sustainable success..............................................................22

Task 4.............................................................................................................................................23

a) Balance scorecard approach..................................................................................................23

M4 Analyse how, in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................24

Conclusion:....................................................................................................................................26

References......................................................................................................................................27

Introduction:

Management accounting is the subject of managing all managerial things sophisticatedly in order

to achieve some goals and make arrangements for further targets. This report study will revolve

around management studies and their evaluation related to Tech UK Ltd. to analyse each and

every phase of management accounting and their significance in the decision-making process.

This report will include a brief description of costing techniques in order to understand each

situation and management & financial changes within the management. It will reveal about cost

analysis process budgetary control process via analysing various planking tools as budget. This

report will include an explanation of marginal and absorption costing to monitor business

activities and managerial tasks within the organisation.

Management accounting is the subject of managing all managerial things sophisticatedly in order

to achieve some goals and make arrangements for further targets. This report study will revolve

around management studies and their evaluation related to Tech UK Ltd. to analyse each and

every phase of management accounting and their significance in the decision-making process.

This report will include a brief description of costing techniques in order to understand each

situation and management & financial changes within the management. It will reveal about cost

analysis process budgetary control process via analysing various planking tools as budget. This

report will include an explanation of marginal and absorption costing to monitor business

activities and managerial tasks within the organisation.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Task 1

a) Explanation of management accounting and the essential requirements of management

accounting system.

I). Difference between management accounting and financial accounting:

Management accounting: it is a study of analysing, observing, evaluating and interpreting data

and facts related to business activities in order to achieve long-term profit. It can be taken as

long-term decision-making process in which management needs to focus on cost, production and

sales activities to maximise more profit. This management accounting tool is based on principle

and analogy and causality to provide effective and relevant information as per managerial

requirements and connectivity.

basis Financial Accounting Management accounting

1. Nature Financial accounting is

basically used in observing

and analysing financial terms

of the business. It provides

transparent and relevant

information to the

management to observe

financial problems.

These are flexible in nature.

This managerial accounting is

used as a profession to making

the decision process easier.

2. objective Its’ major objective is to Through this company

Financial accounting

Management accounting

a) Explanation of management accounting and the essential requirements of management

accounting system.

I). Difference between management accounting and financial accounting:

Management accounting: it is a study of analysing, observing, evaluating and interpreting data

and facts related to business activities in order to achieve long-term profit. It can be taken as

long-term decision-making process in which management needs to focus on cost, production and

sales activities to maximise more profit. This management accounting tool is based on principle

and analogy and causality to provide effective and relevant information as per managerial

requirements and connectivity.

basis Financial Accounting Management accounting

1. Nature Financial accounting is

basically used in observing

and analysing financial terms

of the business. It provides

transparent and relevant

information to the

management to observe

financial problems.

These are flexible in nature.

This managerial accounting is

used as a profession to making

the decision process easier.

2. objective Its’ major objective is to Through this company

Financial accounting

Management accounting

maintain records,

documentation and financial

information to produce

financial statements.

becomes capable to observe

and changeable situation and

make accurate decisions to

meet long-term requirements.

3. relevancy Financial accounting is used in

the company based on past

and previous movements and

action of business.

It provides relevant results

based on historical plus

futuristic environment.

mandatory It is mandatory for all business

operations

But it is not compulsory for all

apply it in the business.

ii) Use of management accounting as decision-making tools:

1. Inventory management decisions: using management accounting as decision-making tools

helps in the business to measure inventory level and storage process as per requirement in the

business. It allows the manager to observe and avoid stock risks to reduce situation of under and

overvaluation in an inventory while making production decisions. It helps to reduce inventory

shortage problem and to allow manger to make a quick assessment of inventory process.

2. Forecasting decisions: management accounting is the tool which helps the management of an

organisation to make profitable decisions as sales forecasting, demand forecasting and gives

inventory decisions

forecasting decisions

pricing decisions

Investment decisions

documentation and financial

information to produce

financial statements.

becomes capable to observe

and changeable situation and

make accurate decisions to

meet long-term requirements.

3. relevancy Financial accounting is used in

the company based on past

and previous movements and

action of business.

It provides relevant results

based on historical plus

futuristic environment.

mandatory It is mandatory for all business

operations

But it is not compulsory for all

apply it in the business.

ii) Use of management accounting as decision-making tools:

1. Inventory management decisions: using management accounting as decision-making tools

helps in the business to measure inventory level and storage process as per requirement in the

business. It allows the manager to observe and avoid stock risks to reduce situation of under and

overvaluation in an inventory while making production decisions. It helps to reduce inventory

shortage problem and to allow manger to make a quick assessment of inventory process.

2. Forecasting decisions: management accounting is the tool which helps the management of an

organisation to make profitable decisions as sales forecasting, demand forecasting and gives

inventory decisions

forecasting decisions

pricing decisions

Investment decisions

accurate information about changes in balance sheets, changes in equity and managerial

profitability.

3. Investment decisions: investment decisions are depended on reliability and accuracy of the

financial projections in which company is going to invest. Management accounting helps the

company to make effective investment policies based accounting norms and principles. It creates

a solution by which and where the company could invest to get maximum returns and higher

ROE%.

4. Pricing decisions: management accounting uses various kinds of tools such as cost analysis,

pricing determination activities to help the management to make an effective decision regarding

prices for their products. It helps sales and production department to make an effective analysis

of the market and set the price of their product to make a higher profit.

Types of management accounting systems:

1. Inventory management systems: Inventory management systems are those systems that are

utilised in the management of control inventory storage procedure to understand the production

an inventory level of the company. The company manages their profit as per requirements and

Inventory managment system

Job cost system

Cost managment system

profitability.

3. Investment decisions: investment decisions are depended on reliability and accuracy of the

financial projections in which company is going to invest. Management accounting helps the

company to make effective investment policies based accounting norms and principles. It creates

a solution by which and where the company could invest to get maximum returns and higher

ROE%.

4. Pricing decisions: management accounting uses various kinds of tools such as cost analysis,

pricing determination activities to help the management to make an effective decision regarding

prices for their products. It helps sales and production department to make an effective analysis

of the market and set the price of their product to make a higher profit.

Types of management accounting systems:

1. Inventory management systems: Inventory management systems are those systems that are

utilised in the management of control inventory storage procedure to understand the production

an inventory level of the company. The company manages their profit as per requirements and

Inventory managment system

Job cost system

Cost managment system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

production level to analyse the effectiveness of inventory to increase the productivity level and

accuracy to avoid stock risk. This system is utilised to manage and take quick decisions

regarding management in case of under and overvaluation of inventory.

2. Job cost systems: Job cost systems are those systems which are applied in the management in

order possess and regulate each and every cost of job orders by tracing those projects. The

company are allowed to keep tracing their works and jobs in order to maintain the level of cost-

effectiveness and efficiency as per requirements and demand for all projects (Strelnik, et. al.,

2015).

3. Cost management systems: cost management systems are also known as product assessing

systems. These systems provide a platform for the company to regulate and control over their

cost by making effective assessment procedure of each project and product. This system is used

or adopted by the management to measure the cost-effectiveness of each cost such as

administrative, production and selling cost to operate the business properly by managing such

effectively. It is a medium of observing and evaluating sales and revenue related to maximising

profitability.

accuracy to avoid stock risk. This system is utilised to manage and take quick decisions

regarding management in case of under and overvaluation of inventory.

2. Job cost systems: Job cost systems are those systems which are applied in the management in

order possess and regulate each and every cost of job orders by tracing those projects. The

company are allowed to keep tracing their works and jobs in order to maintain the level of cost-

effectiveness and efficiency as per requirements and demand for all projects (Strelnik, et. al.,

2015).

3. Cost management systems: cost management systems are also known as product assessing

systems. These systems provide a platform for the company to regulate and control over their

cost by making effective assessment procedure of each project and product. This system is used

or adopted by the management to measure the cost-effectiveness of each cost such as

administrative, production and selling cost to operate the business properly by managing such

effectively. It is a medium of observing and evaluating sales and revenue related to maximising

profitability.

b) Presenting financial information.

Tech UK uses to prepare various kinds of a report for measuring business performance.

These reports are:

1. Budgets: Budgets are prepared in the company as a major financial report to produce financial

plans, implement them for making improvement in financial performance of the company. It is

basically utilised to enhance the financial performance of the company by measuring expenses,

budgeted cost etc. it provides effective results by making a comparison between estimated and

planned behaviour.

2. Sales report: Sales reports are produced by the company as per sales requirements and market

demands. Tech UK uses to make sales report to analyse sales volume of the company by

measuring the relationship between sales and revenue. Sales report allows the company to

understand changes and increase their sales and productivity by making changes in sales plans

and strategies (Strelnik, et. al., 2015).

3. Performance report: Performance report is produced to measure performance criteria for the

management. These performance records are based on sales, production and other activities and

utilities. This report defines company’s accuracy and liquidity level that how much it is capable

to meet its requirements and obligations.

Tech UK uses to prepare various kinds of a report for measuring business performance.

These reports are:

1. Budgets: Budgets are prepared in the company as a major financial report to produce financial

plans, implement them for making improvement in financial performance of the company. It is

basically utilised to enhance the financial performance of the company by measuring expenses,

budgeted cost etc. it provides effective results by making a comparison between estimated and

planned behaviour.

2. Sales report: Sales reports are produced by the company as per sales requirements and market

demands. Tech UK uses to make sales report to analyse sales volume of the company by

measuring the relationship between sales and revenue. Sales report allows the company to

understand changes and increase their sales and productivity by making changes in sales plans

and strategies (Strelnik, et. al., 2015).

3. Performance report: Performance report is produced to measure performance criteria for the

management. These performance records are based on sales, production and other activities and

utilities. This report defines company’s accuracy and liquidity level that how much it is capable

to meet its requirements and obligations.

M1 Evaluate the benefits of management accounting systems and their application within

an organizational context.

Management accounting is taken as a study of management activities based on business

management and operation criteria. It is used as a decision-making tool to analyse needs of

accurate information, data to provide it to the company at the time of making decisions such as

cost analysis, forecasting decision etc. UK Tech company can be utilised make cost-effective and

productive decision by using management accounting systems and prepare accounting report for

managing flexibility. Application of such systems in the Tech UK Ltd will provide accurate and

flexible information and allow the company to deal with future changes and obstacles.

an organizational context.

Management accounting is taken as a study of management activities based on business

management and operation criteria. It is used as a decision-making tool to analyse needs of

accurate information, data to provide it to the company at the time of making decisions such as

cost analysis, forecasting decision etc. UK Tech company can be utilised make cost-effective and

productive decision by using management accounting systems and prepare accounting report for

managing flexibility. Application of such systems in the Tech UK Ltd will provide accurate and

flexible information and allow the company to deal with future changes and obstacles.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

D1 critically evaluates how management accounting systems and management accounting

reporting is integrated within organizational processes.

Management accounting systems and preparation of management reports are interrelated to

management work and organisational process in order to manage whole work and make proper

management strategies to get relevant results. Management accounting systems are effectively

used and adopted by the company to convert managerial plans into reality. It allows the

management to measure and track organisational tasks and works by analysing cost, maintain

budget and accounts to reduce disorders and run business in a stable manner with competitive

strategies. Management reports help to trace and keeping records of all activities in an efficient

manner to make productive results and decisions by observing the financial health of the

company (Lavia López and Hiebl, 2014).

reporting is integrated within organizational processes.

Management accounting systems and preparation of management reports are interrelated to

management work and organisational process in order to manage whole work and make proper

management strategies to get relevant results. Management accounting systems are effectively

used and adopted by the company to convert managerial plans into reality. It allows the

management to measure and track organisational tasks and works by analysing cost, maintain

budget and accounts to reduce disorders and run business in a stable manner with competitive

strategies. Management reports help to trace and keeping records of all activities in an efficient

manner to make productive results and decisions by observing the financial health of the

company (Lavia López and Hiebl, 2014).

Task 2

a) Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Costing behaviour and analysis can be measured and monitored with the help of various

costing techniques. Marginal and absorption techniques are utilised in the management to

observe cost effectiveness and accuracy to know funds requirements and reduce uncertainty

while making income statements through management accounting systems. Costing techniques

are one of them which are adopted by the organisation to understand the value of fixed and

variable cost within while managing any projects (Otley, 2016).

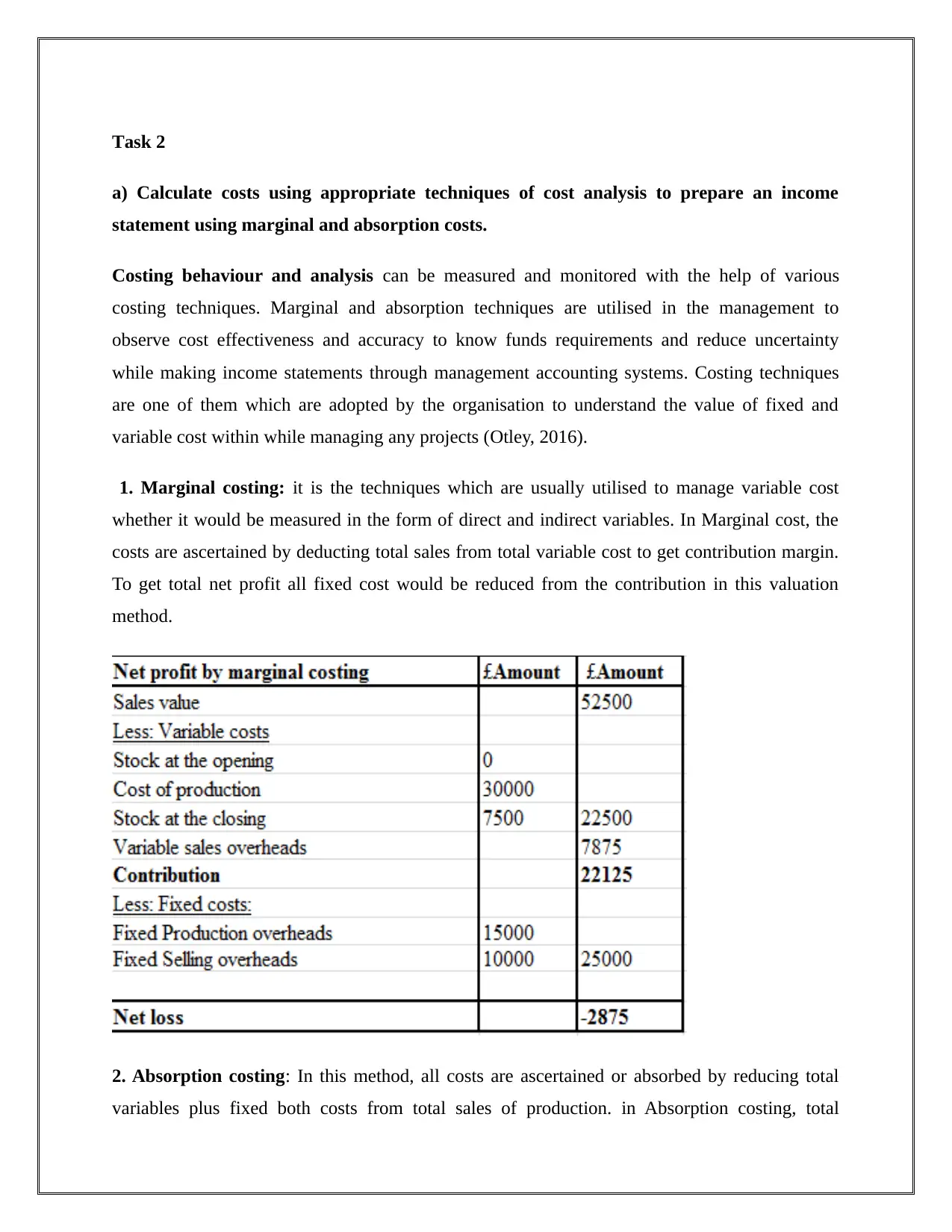

1. Marginal costing: it is the techniques which are usually utilised to manage variable cost

whether it would be measured in the form of direct and indirect variables. In Marginal cost, the

costs are ascertained by deducting total sales from total variable cost to get contribution margin.

To get total net profit all fixed cost would be reduced from the contribution in this valuation

method.

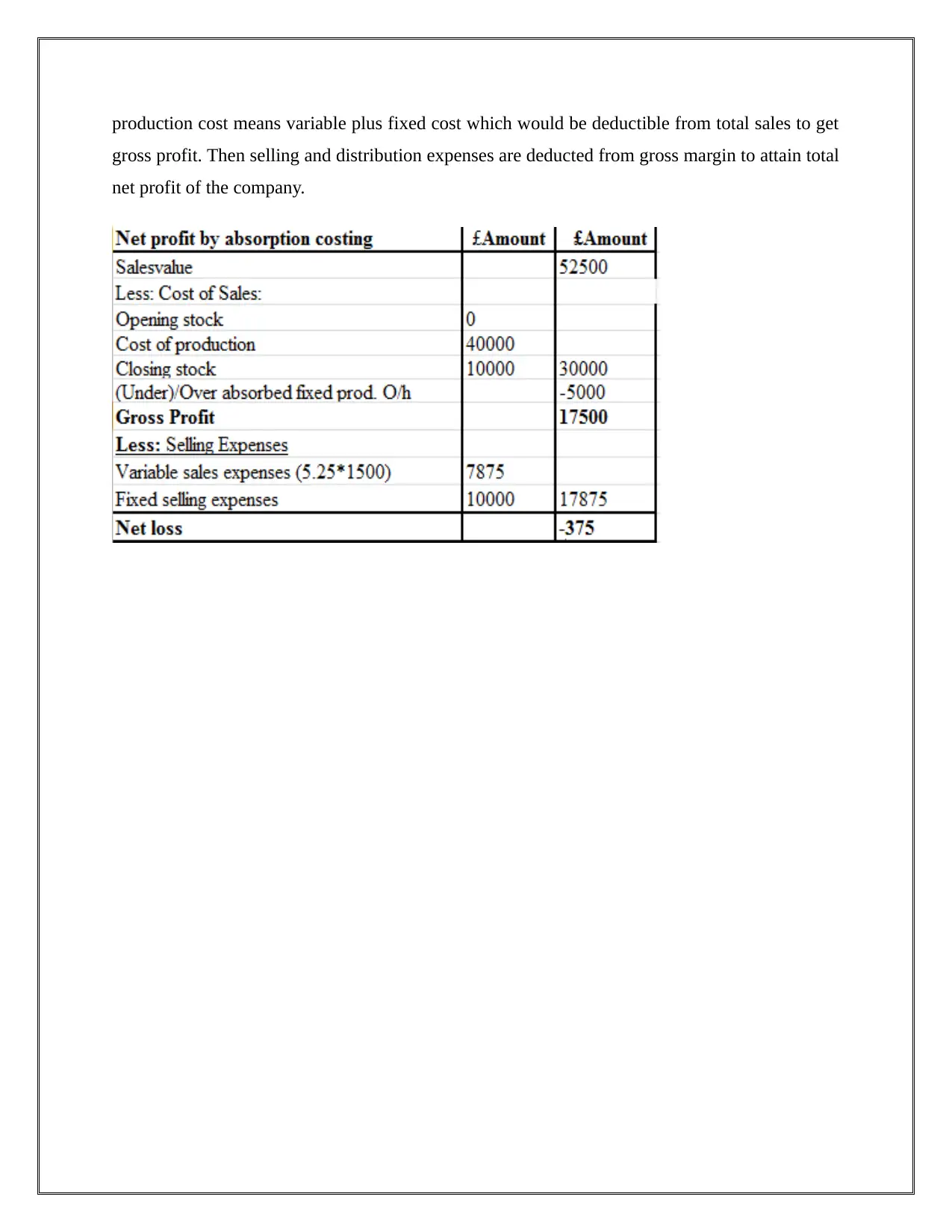

2. Absorption costing: In this method, all costs are ascertained or absorbed by reducing total

variables plus fixed both costs from total sales of production. in Absorption costing, total

a) Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Costing behaviour and analysis can be measured and monitored with the help of various

costing techniques. Marginal and absorption techniques are utilised in the management to

observe cost effectiveness and accuracy to know funds requirements and reduce uncertainty

while making income statements through management accounting systems. Costing techniques

are one of them which are adopted by the organisation to understand the value of fixed and

variable cost within while managing any projects (Otley, 2016).

1. Marginal costing: it is the techniques which are usually utilised to manage variable cost

whether it would be measured in the form of direct and indirect variables. In Marginal cost, the

costs are ascertained by deducting total sales from total variable cost to get contribution margin.

To get total net profit all fixed cost would be reduced from the contribution in this valuation

method.

2. Absorption costing: In this method, all costs are ascertained or absorbed by reducing total

variables plus fixed both costs from total sales of production. in Absorption costing, total

production cost means variable plus fixed cost which would be deductible from total sales to get

gross profit. Then selling and distribution expenses are deducted from gross margin to attain total

net profit of the company.

gross profit. Then selling and distribution expenses are deducted from gross margin to attain total

net profit of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2 accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents:

Costing analysis such as marginal and absorption costing techniques are produced in the

management to get long-term results by getting cost analysis, measuring cost-effectiveness to get

long-term results in order to make profitable decisions in the organisation. Marginal costing and

absorption method, both are different in utilising and monitoring business activities. While

getting cost ascertainment procedure in the business, it helps to measure accuracy and funds

requirements while making financial statements. In these methods, valuation of closing stock

through marginal is lesser than the valuation of closing inventory through absorption costing

(Aruomoaghe & Agbo, 2013).

appropriate financial reporting documents:

Costing analysis such as marginal and absorption costing techniques are produced in the

management to get long-term results by getting cost analysis, measuring cost-effectiveness to get

long-term results in order to make profitable decisions in the organisation. Marginal costing and

absorption method, both are different in utilising and monitoring business activities. While

getting cost ascertainment procedure in the business, it helps to measure accuracy and funds

requirements while making financial statements. In these methods, valuation of closing stock

through marginal is lesser than the valuation of closing inventory through absorption costing

(Aruomoaghe & Agbo, 2013).

D2 Produce financial reports that accurately apply and interpret data for a range of

business activities:

Cost analysis can be done through management cost techniques in order to manage cost

effectiveness and make a proper valuation of stock to get effective results while making

inventory and production decisions. Making of financial reports through costing techniques

creates different values due to different methods and utility process. It creates less valuation of

closing stock while using marginal costing in the comparison of absorption costing techniques

(Aruomoaghe & Agbo, 2013).

business activities:

Cost analysis can be done through management cost techniques in order to manage cost

effectiveness and make a proper valuation of stock to get effective results while making

inventory and production decisions. Making of financial reports through costing techniques

creates different values due to different methods and utility process. It creates less valuation of

closing stock while using marginal costing in the comparison of absorption costing techniques

(Aruomoaghe & Agbo, 2013).

Task 3

a) Different kinds of budgets and their advantages and disadvantages.

1. Master budget:

Master budgets are the combination of business projects and activities which includes sales,

production, operation and other kinds of business activities. Master budgets allow the company

to formulate a business decision based on all kinds of business activities’ decisions (Benli &

Celayir, 2014). Master budgets are utilised by the company to allocate all kinds of resources at

one time and trace all kinds of activities together.

Advantages:

Master budgets are used to measure all financial records in an easy and effective manner.

Managers are trace and measure different kinds of records and transactions process from

different locations.

Types of budgets

operation

budget

master

budget

sales

budget

a) Different kinds of budgets and their advantages and disadvantages.

1. Master budget:

Master budgets are the combination of business projects and activities which includes sales,

production, operation and other kinds of business activities. Master budgets allow the company

to formulate a business decision based on all kinds of business activities’ decisions (Benli &

Celayir, 2014). Master budgets are utilised by the company to allocate all kinds of resources at

one time and trace all kinds of activities together.

Advantages:

Master budgets are used to measure all financial records in an easy and effective manner.

Managers are trace and measure different kinds of records and transactions process from

different locations.

Types of budgets

operation

budget

master

budget

sales

budget

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

It creates a great combination of financial information and business cost-effectively

through allocating cost resources in a reliable manner of Tech UK.

Disadvantages:

Sometimes it creates difficulties to recognise and coordinate with budgets.

The company sometimes cannot identify and assess the effectiveness of all financial

transactions due to lack of financial variables and non-financial terms.

2. Operation budget:

Operational budgets are prepared by the tech UK Ltd in order to measure all expenses and cost

related to business activities. All activities which are related to operating expenses and cost are

covered by operational budget (Benli & Celayir, 2014).

Advantages:

Operation Budget is utilised in the business to operate all kinds of expenses and cost in

the business.

It is beneficial to operate and measure all kinds of cost within the organisation while

measuring and making decisions on operational projects.

Disadvantages:

Manager feels difficulties sometimes to measure accuracy and flexibility because these

budgets are prepared on assumptions and previous activities.

All expenses would be focused and considered as well proper allocation is not possible

for each project

3. Sales budgets:

Sales budgets are produced as basic and major primary component of the master budget. Sales

budgets include various information related to production and promotion activities to regulate

through allocating cost resources in a reliable manner of Tech UK.

Disadvantages:

Sometimes it creates difficulties to recognise and coordinate with budgets.

The company sometimes cannot identify and assess the effectiveness of all financial

transactions due to lack of financial variables and non-financial terms.

2. Operation budget:

Operational budgets are prepared by the tech UK Ltd in order to measure all expenses and cost

related to business activities. All activities which are related to operating expenses and cost are

covered by operational budget (Benli & Celayir, 2014).

Advantages:

Operation Budget is utilised in the business to operate all kinds of expenses and cost in

the business.

It is beneficial to operate and measure all kinds of cost within the organisation while

measuring and making decisions on operational projects.

Disadvantages:

Manager feels difficulties sometimes to measure accuracy and flexibility because these

budgets are prepared on assumptions and previous activities.

All expenses would be focused and considered as well proper allocation is not possible

for each project

3. Sales budgets:

Sales budgets are produced as basic and major primary component of the master budget. Sales

budgets include various information related to production and promotion activities to regulate

sales and revenue relation while making sales forecasting, it helps within the organisation to

make the effective analysis as per company’s requirements.

Advantages:

Sales volumes and effectiveness cannot be measured and monitored without producing

sales budget.

It allows the company to measure and increase production level by analysing sales

requirements and market demands through this budget (Fullerton, et. al., 2014).

Disadvantages:

It is not able to handle qualitative factors based on sales report and management.

Sometimes it becomes difficult for the sales department to handle and measure sales

activities through sales budget.

make the effective analysis as per company’s requirements.

Advantages:

Sales volumes and effectiveness cannot be measured and monitored without producing

sales budget.

It allows the company to measure and increase production level by analysing sales

requirements and market demands through this budget (Fullerton, et. al., 2014).

Disadvantages:

It is not able to handle qualitative factors based on sales report and management.

Sometimes it becomes difficult for the sales department to handle and measure sales

activities through sales budget.

b) The budget preparation process including determination of pricing and different

costing systems that can be used.

Budgets are prepared by the financial department by assessing management and financial

activities recorded in financial reports and statements. Techs UK Company needs to measure

financial performance and it's liquidity position to get organisational objectives by recognising

financial threats and obstacles. After identifying all hurdles and problems budgets are produced

in order to make a comparison between planned behaviour and actual attributes to attain desired

goals. The company needs to prepare various kinds of budgets and reports based on past and

previous records so that past mistakes could not be repeated while making research model and

company could take forecasting decision based on budget effectiveness and accuracy (Egbide

and Agbude, 2014)

costing systems that can be used.

Budgets are prepared by the financial department by assessing management and financial

activities recorded in financial reports and statements. Techs UK Company needs to measure

financial performance and it's liquidity position to get organisational objectives by recognising

financial threats and obstacles. After identifying all hurdles and problems budgets are produced

in order to make a comparison between planned behaviour and actual attributes to attain desired

goals. The company needs to prepare various kinds of budgets and reports based on past and

previous records so that past mistakes could not be repeated while making research model and

company could take forecasting decision based on budget effectiveness and accuracy (Egbide

and Agbude, 2014)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c) The importance of budget as a tool for planning and control purposes.

The importance of budgets as planning tools:

Budgets are the blueprints of financial strategies made by an organisation to get long-term

objectives. Budgets are produced quarterly, annually, monthly as per company’s requirements. It

provides a platform for the managers to observe and monitor business financial activities by

allocating resources effectively. Managers can take effective steps by evaluating financial

changes occurred in the external environment by reading and analysing facts, data and measuring

financial requirements and needs of the company to make decisions (Aurora, 2013).

It compares between estimated plans and actual budgetary outcomes to make productive

decisions.

It gives an effective and reliable result that allows the managers to measure data accuracy

and store them safely.

It gives opportunities to the management to assess projects and trace business activities to

make sales records and increase productivity level of the company (Baldauf, et. al.,

2015).

The importance of budgets as planning tools:

Budgets are the blueprints of financial strategies made by an organisation to get long-term

objectives. Budgets are produced quarterly, annually, monthly as per company’s requirements. It

provides a platform for the managers to observe and monitor business financial activities by

allocating resources effectively. Managers can take effective steps by evaluating financial

changes occurred in the external environment by reading and analysing facts, data and measuring

financial requirements and needs of the company to make decisions (Aurora, 2013).

It compares between estimated plans and actual budgetary outcomes to make productive

decisions.

It gives an effective and reliable result that allows the managers to measure data accuracy

and store them safely.

It gives opportunities to the management to assess projects and trace business activities to

make sales records and increase productivity level of the company (Baldauf, et. al.,

2015).

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets.

Budgets are produced in the organisation by the finance department. These are blueprints of

financial plans which would be implemented in the business to regulate expenses and cost

optimised in non-value projects. The budgetary process includes preparation of plans, organising

and implementing plan successfully to make various kinds of decision such as cost, finance,

production and decisions related to investment. Through budgets, the company becomes able to

operate business activities effectively by comparing actual and estimated variables based on

financial planning. It is produced in the business to analyse cost-effectiveness, financial

resources utility after allocating them as per company’s requirements. Financial budgets are

produced to allow the manager to determine prices, profit for future goals and achievements.

forecasting budgets.

Budgets are produced in the organisation by the finance department. These are blueprints of

financial plans which would be implemented in the business to regulate expenses and cost

optimised in non-value projects. The budgetary process includes preparation of plans, organising

and implementing plan successfully to make various kinds of decision such as cost, finance,

production and decisions related to investment. Through budgets, the company becomes able to

operate business activities effectively by comparing actual and estimated variables based on

financial planning. It is produced in the business to analyse cost-effectiveness, financial

resources utility after allocating them as per company’s requirements. Financial budgets are

produced to allow the manager to determine prices, profit for future goals and achievements.

D3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organizations to sustainable success.

Tech UK Ltd. is the multinational company which needs to use and manage their records with

the help of budget and financial report. Budgets are helpful in managing, observing and

analysing whole financial process and activities which allows the company to get beneficial

results through budgetary control and auditory process. The company can make financial plans

and implement them to measure their business accuracy and financial performance. It is based on

previous data which can be utilised to implement them and make logical decisions to control the

adverse situation and financial obstacles to make decisions more effective (De et. al., 2012).

problems to lead organizations to sustainable success.

Tech UK Ltd. is the multinational company which needs to use and manage their records with

the help of budget and financial report. Budgets are helpful in managing, observing and

analysing whole financial process and activities which allows the company to get beneficial

results through budgetary control and auditory process. The company can make financial plans

and implement them to measure their business accuracy and financial performance. It is based on

previous data which can be utilised to implement them and make logical decisions to control the

adverse situation and financial obstacles to make decisions more effective (De et. al., 2012).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Task 4

a) Balance scorecard approach

Balance scorecard is the tools form which company gets along term benefits such as allocation of

cost and financial resources, measuring cost-effectiveness, promoting business activities and

decision-making process to get long-term achievements (Zizlavsky, 2014). This tool is worked

on four major components at learning level, competitive level, employees’ interest and

customers’ satisfaction. Tech UK Ltd can use this tool as decision-making process to enhance

business projects and regain learning outcomes; it allows the company to focus on customers’

choices and make an effective calculation how to increase the efficiency of the business to

determine goals and attain long-term benefits. It considers on the conceptual process from which

employees can give their 100% efforts to convert estimated and planned behaviour into the

reality of success (Anna, 2015).

Importance of balance scorecard:

1. Balance scorecard is highly effective and reliable tool from which Tech UK can get a long-

term benefit.

2. It allows the management to assign and regulate their work and establish employee’s interest

to convert individual goal into general goals.

Application of balance scorecard in managing company and responding financial

problems:

Balance scorecard is the conceptual management tool. It is utilised in the management to get

effective results based on learning outcomes, competitive outcomes and financial outcomes.

Balance scorecard is utilised by the company to make effective strategies within their

organisation to make effective decisions related to sales and production activities. Balance

scorecard is taken as tools for decision-making process which allows the company to get to know

the financial results and changes in the performance. It allows the company to analyse the

effectiveness and analyse the cost to make an effective and reliable decision and get long-term

achievements (Zizlavsky, 2014).

a) Balance scorecard approach

Balance scorecard is the tools form which company gets along term benefits such as allocation of

cost and financial resources, measuring cost-effectiveness, promoting business activities and

decision-making process to get long-term achievements (Zizlavsky, 2014). This tool is worked

on four major components at learning level, competitive level, employees’ interest and

customers’ satisfaction. Tech UK Ltd can use this tool as decision-making process to enhance

business projects and regain learning outcomes; it allows the company to focus on customers’

choices and make an effective calculation how to increase the efficiency of the business to

determine goals and attain long-term benefits. It considers on the conceptual process from which

employees can give their 100% efforts to convert estimated and planned behaviour into the

reality of success (Anna, 2015).

Importance of balance scorecard:

1. Balance scorecard is highly effective and reliable tool from which Tech UK can get a long-

term benefit.

2. It allows the management to assign and regulate their work and establish employee’s interest

to convert individual goal into general goals.

Application of balance scorecard in managing company and responding financial

problems:

Balance scorecard is the conceptual management tool. It is utilised in the management to get

effective results based on learning outcomes, competitive outcomes and financial outcomes.

Balance scorecard is utilised by the company to make effective strategies within their

organisation to make effective decisions related to sales and production activities. Balance

scorecard is taken as tools for decision-making process which allows the company to get to know

the financial results and changes in the performance. It allows the company to analyse the

effectiveness and analyse the cost to make an effective and reliable decision and get long-term

achievements (Zizlavsky, 2014).

M4 Analyse how, in responding to financial problems, management accounting can lead

organizations to sustainable success.

Management accounting tools are utilised in the management to analyse the effectiveness of

business activities, making business planning and implementing them for successful and long-

term financial and operational achievements. These systems such as variance analysis, cost

analysis, budgets and so on are helpful in the management for making business decision

accurately. These systems give priority to the accounting principles and concept to reach the

effective conclusion (Amirya, et. al., 2014).

organizations to sustainable success.

Management accounting tools are utilised in the management to analyse the effectiveness of

business activities, making business planning and implementing them for successful and long-

term financial and operational achievements. These systems such as variance analysis, cost

analysis, budgets and so on are helpful in the management for making business decision

accurately. These systems give priority to the accounting principles and concept to reach the

effective conclusion (Amirya, et. al., 2014).

1. Financial decision:

Management accounting systems and planning tools are adopted in the business to allow the

company to make financial decisions. It provides the an accurate and flexible platform by

observing and analysing such things which are important for the company and how the additional

cost can be reduced to increase financial efficiency. It produces financial statements to help the

company with accurate financial decisions.

2. Enhancing productivity:

These planning tools are also useful in measuring company’s requirements and help them to

enhance their productivity at strategic and operational level. It reduces all non-value cost and

helps them increase productivity level which leads the company towards growth (Amirya, et. al.,

2014).

Management accounting systems and planning tools are adopted in the business to allow the

company to make financial decisions. It provides the an accurate and flexible platform by

observing and analysing such things which are important for the company and how the additional

cost can be reduced to increase financial efficiency. It produces financial statements to help the

company with accurate financial decisions.

2. Enhancing productivity:

These planning tools are also useful in measuring company’s requirements and help them to

enhance their productivity at strategic and operational level. It reduces all non-value cost and

helps them increase productivity level which leads the company towards growth (Amirya, et. al.,

2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion:

This report provides an essential knowledge of management accounting by differentiating

between management accounting and financial accounting. This reading has been provided with

a brief description of management accounting and their significance to get long-term

achievement and objectives. It has been described cost technologies such as marginal and

absorption costing in order to measure accuracy and relevancy to the company. This reading has

been defined by budgets and their types to measure the financial performance of the company

related to Tech UK Ltd. The major aim of preparing this report was to understand reliability and

flexibility of management accounting systems using balance scorecard and their function in order

to get long-term results.

This report provides an essential knowledge of management accounting by differentiating

between management accounting and financial accounting. This reading has been provided with

a brief description of management accounting and their significance to get long-term

achievement and objectives. It has been described cost technologies such as marginal and

absorption costing in order to measure accuracy and relevancy to the company. This reading has

been defined by budgets and their types to measure the financial performance of the company

related to Tech UK Ltd. The major aim of preparing this report was to understand reliability and

flexibility of management accounting systems using balance scorecard and their function in order

to get long-term results.

References

Amirya, M., Djamhuri, A., & Ludigdo, U., 2014. Development of Accounting and

Budget System of General Services Board in Universitas Brawijaya: Study of

Interpretive. International Journal of Humanities and Social Science.

Anna, A., 2015. Strategic Management Tools and Techniques and Organizational

Performance: Findings from the Czech Republic. Journal of Competitiveness.

Aruomoaghe, J., & Agbo, S., 2013. Application of cost Analysis for Performance

Evaluation: A Cost/Benefit Approach. Research Journal of Finance and Accounting.

Baldauf, J., Steckel, R., & Steller, M., 2015. The Influence of Audit Risk and Materiality

Guidelines on Auditor’s Planning Materiality Assessment. Accounting and Finance

Research.

Benli, V. F., & Celayir, D., 2014. Risk-Based Internal Auditing And Risk Assessment

Process. European Journal of Accounting Auditing and Finance Research.

Mahal, I., & Hossain, A.M., 2015. Activity-Based Costing (ABC) – An Effective Tool

for Better Management. vol.6, no.4. Research Journal of Finance and Accounting.

Strelnik, E.U., Usanova, D.S. and Khairullin, I.G., 2015. Key performance indicators in

corporate finance. Asian Social Science, 11(11), p.369.

Zizlavsky, O., 2014. The Balanced Scorecard: Innovative Performance Measurement and

Management Control System. Journal of Technology Management & Innovation.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Amirya, M., Djamhuri, A., & Ludigdo, U., 2014. Development of Accounting and

Budget System of General Services Board in Universitas Brawijaya: Study of

Interpretive. International Journal of Humanities and Social Science.

Anna, A., 2015. Strategic Management Tools and Techniques and Organizational

Performance: Findings from the Czech Republic. Journal of Competitiveness.

Aruomoaghe, J., & Agbo, S., 2013. Application of cost Analysis for Performance

Evaluation: A Cost/Benefit Approach. Research Journal of Finance and Accounting.

Baldauf, J., Steckel, R., & Steller, M., 2015. The Influence of Audit Risk and Materiality

Guidelines on Auditor’s Planning Materiality Assessment. Accounting and Finance

Research.

Benli, V. F., & Celayir, D., 2014. Risk-Based Internal Auditing And Risk Assessment

Process. European Journal of Accounting Auditing and Finance Research.

Mahal, I., & Hossain, A.M., 2015. Activity-Based Costing (ABC) – An Effective Tool

for Better Management. vol.6, no.4. Research Journal of Finance and Accounting.

Strelnik, E.U., Usanova, D.S. and Khairullin, I.G., 2015. Key performance indicators in

corporate finance. Asian Social Science, 11(11), p.369.

Zizlavsky, O., 2014. The Balanced Scorecard: Innovative Performance Measurement and

Management Control System. Journal of Technology Management & Innovation.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-

sized enterprises: current knowledge and avenues for further research. Journal of

Management Accounting Research, 27(1), pp.81-119.

sized enterprises: current knowledge and avenues for further research. Journal of

Management Accounting Research, 27(1), pp.81-119.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.