Management Accounting Principles and Applications

VerifiedAdded on 2020/02/03

|24

|4708

|434

Report

AI Summary

This assignment delves into the core principles of management accounting by examining practical case studies. It covers a range of topics including budgeting techniques (like Sales Volume Variance), break-even analysis (BEP), ratio analysis, cash flow analysis, and capital budgeting. Students are expected to demonstrate their understanding of these concepts by applying them to real-world scenarios presented in the illustrations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explain management accounting and give essential requirements of different types of

management accounting system in the given case scenario...................................................1

P2 Explain different methods used for management accounting reporting...........................8

Task 2.............................................................................................................................................15

P3 calculate cost using different techniques by preparing income statement under marginal

and absorption costing..........................................................................................................15

TASK 3..........................................................................................................................................16

P4 Explain advantages and disadvantages of different types of planning tools for budgetary

control...................................................................................................................................16

P5 Compare how an entity adopt management accounting systems in order to deal with the

financial problems................................................................................................................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explain management accounting and give essential requirements of different types of

management accounting system in the given case scenario...................................................1

P2 Explain different methods used for management accounting reporting...........................8

Task 2.............................................................................................................................................15

P3 calculate cost using different techniques by preparing income statement under marginal

and absorption costing..........................................................................................................15

TASK 3..........................................................................................................................................16

P4 Explain advantages and disadvantages of different types of planning tools for budgetary

control...................................................................................................................................16

P5 Compare how an entity adopt management accounting systems in order to deal with the

financial problems................................................................................................................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

Illustration Index

Illustration 1: Retail performance....................................................................................................2

Illustration 2: BEP............................................................................................................................2

Illustration 3: Budget.......................................................................................................................4

Illustration 4: Ratio analysis............................................................................................................8

Illustration 5: Cash flow analysis...................................................................................................10

Illustration 6: Capital budgeting....................................................................................................13

Illustration 1: Retail performance....................................................................................................2

Illustration 2: BEP............................................................................................................................2

Illustration 3: Budget.......................................................................................................................4

Illustration 4: Ratio analysis............................................................................................................8

Illustration 5: Cash flow analysis...................................................................................................10

Illustration 6: Capital budgeting....................................................................................................13

INTRODUCTION

Role of management has increases with the introduction of higher amount of

complexities in the external business environment. Nisa Retail store has been selected for this

project report which is growing gradually in boosting the overall economy of the UK. This report

focuses on management accounting systems and management accounting reporting techniques in

complying all kinds of systems fruitful for the business enterprise. Marginal and absorption

costing has been chosen by an entity in improving the business fall under retail sector in the UK.

TASK 1

P1 Explain management accounting and give essential requirements of different types of

management accounting system in the given case scenario

Background

The current sector is regarded as most important sector in the United Kingdom which

generates higher amount of sales and the revenue every year. The economy is boosted by getting

higher revenue from this particular sector which increases the overall scope of all the businesses

fall under this category (Farías, Torres and Mora Cortez, 2017). There are different kinds of

businesses involves in this sector such as furniture, food and grocery, clothing and accessories

and electronics.

Nisa retail store has been selected in the present report which is small scale entity located

in the United Kingdom. It deals in providing grocery market products or services in order to

facilitate the needs and expectations of all the consumers. Management accountant of Nisa retail

store will take important decisions for the betterment of the current business as their desired

market aim is to achieve all the aims and the objectives within a given span of time. Analytical

ability of a manager gets increases by taking important decisions in their business.

Financial perspective

1

Role of management has increases with the introduction of higher amount of

complexities in the external business environment. Nisa Retail store has been selected for this

project report which is growing gradually in boosting the overall economy of the UK. This report

focuses on management accounting systems and management accounting reporting techniques in

complying all kinds of systems fruitful for the business enterprise. Marginal and absorption

costing has been chosen by an entity in improving the business fall under retail sector in the UK.

TASK 1

P1 Explain management accounting and give essential requirements of different types of

management accounting system in the given case scenario

Background

The current sector is regarded as most important sector in the United Kingdom which

generates higher amount of sales and the revenue every year. The economy is boosted by getting

higher revenue from this particular sector which increases the overall scope of all the businesses

fall under this category (Farías, Torres and Mora Cortez, 2017). There are different kinds of

businesses involves in this sector such as furniture, food and grocery, clothing and accessories

and electronics.

Nisa retail store has been selected in the present report which is small scale entity located

in the United Kingdom. It deals in providing grocery market products or services in order to

facilitate the needs and expectations of all the consumers. Management accountant of Nisa retail

store will take important decisions for the betterment of the current business as their desired

market aim is to achieve all the aims and the objectives within a given span of time. Analytical

ability of a manager gets increases by taking important decisions in their business.

Financial perspective

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

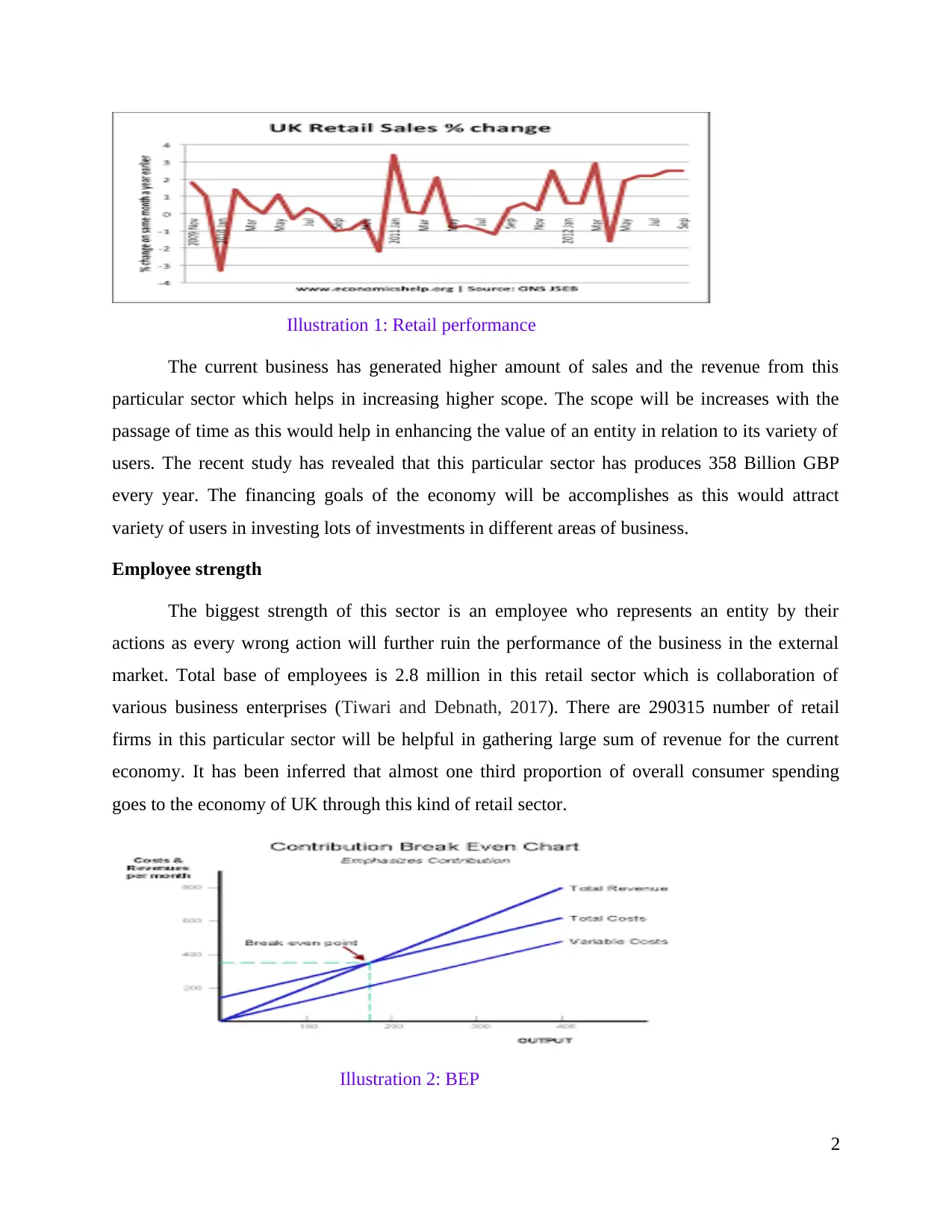

Illustration 1: Retail performance

The current business has generated higher amount of sales and the revenue from this

particular sector which helps in increasing higher scope. The scope will be increases with the

passage of time as this would help in enhancing the value of an entity in relation to its variety of

users. The recent study has revealed that this particular sector has produces 358 Billion GBP

every year. The financing goals of the economy will be accomplishes as this would attract

variety of users in investing lots of investments in different areas of business.

Employee strength

The biggest strength of this sector is an employee who represents an entity by their

actions as every wrong action will further ruin the performance of the business in the external

market. Total base of employees is 2.8 million in this retail sector which is collaboration of

various business enterprises (Tiwari and Debnath, 2017). There are 290315 number of retail

firms in this particular sector will be helpful in gathering large sum of revenue for the current

economy. It has been inferred that almost one third proportion of overall consumer spending

goes to the economy of UK through this kind of retail sector.

Illustration 2: BEP

2

The current business has generated higher amount of sales and the revenue from this

particular sector which helps in increasing higher scope. The scope will be increases with the

passage of time as this would help in enhancing the value of an entity in relation to its variety of

users. The recent study has revealed that this particular sector has produces 358 Billion GBP

every year. The financing goals of the economy will be accomplishes as this would attract

variety of users in investing lots of investments in different areas of business.

Employee strength

The biggest strength of this sector is an employee who represents an entity by their

actions as every wrong action will further ruin the performance of the business in the external

market. Total base of employees is 2.8 million in this retail sector which is collaboration of

various business enterprises (Tiwari and Debnath, 2017). There are 290315 number of retail

firms in this particular sector will be helpful in gathering large sum of revenue for the current

economy. It has been inferred that almost one third proportion of overall consumer spending

goes to the economy of UK through this kind of retail sector.

Illustration 2: BEP

2

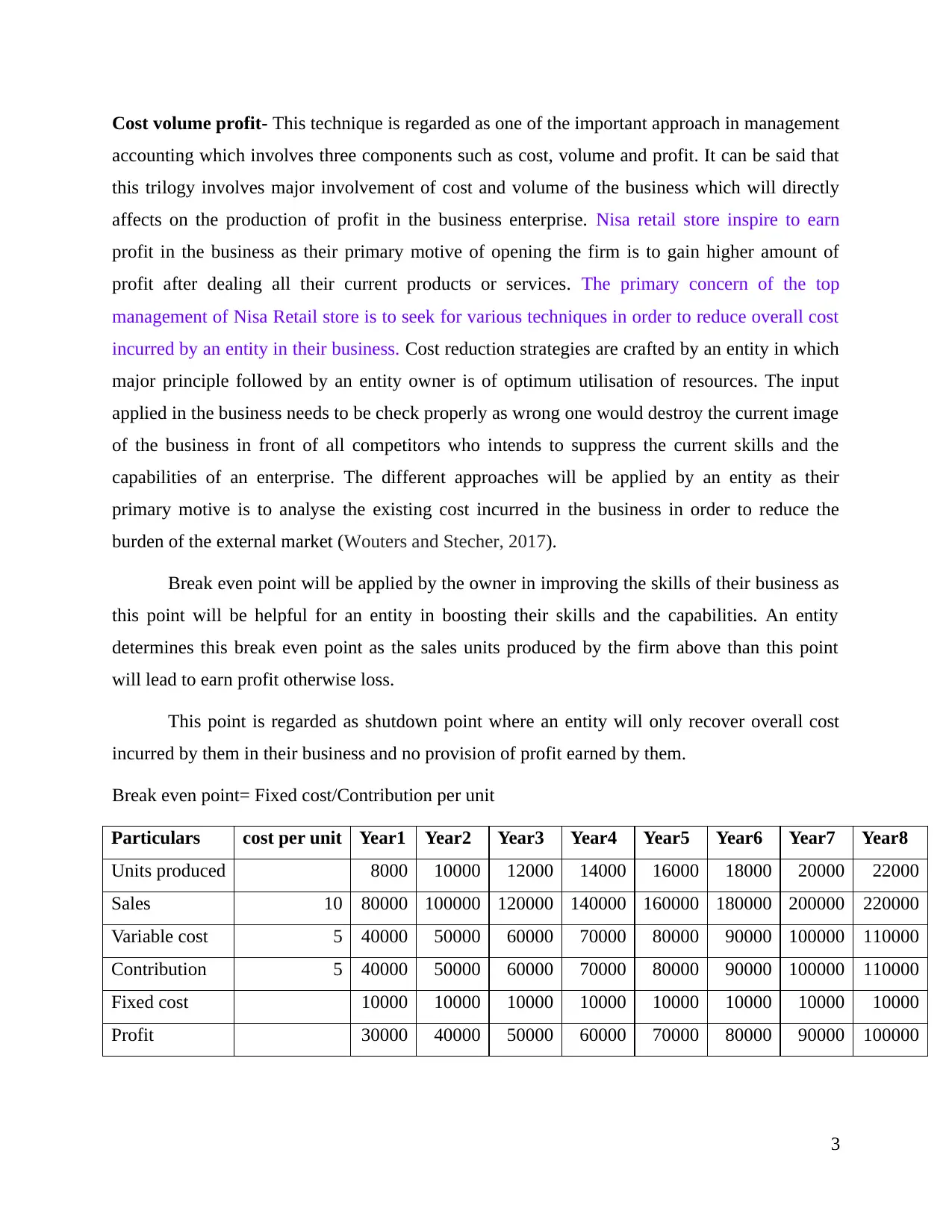

Cost volume profit- This technique is regarded as one of the important approach in management

accounting which involves three components such as cost, volume and profit. It can be said that

this trilogy involves major involvement of cost and volume of the business which will directly

affects on the production of profit in the business enterprise. Nisa retail store inspire to earn

profit in the business as their primary motive of opening the firm is to gain higher amount of

profit after dealing all their current products or services. The primary concern of the top

management of Nisa Retail store is to seek for various techniques in order to reduce overall cost

incurred by an entity in their business. Cost reduction strategies are crafted by an entity in which

major principle followed by an entity owner is of optimum utilisation of resources. The input

applied in the business needs to be check properly as wrong one would destroy the current image

of the business in front of all competitors who intends to suppress the current skills and the

capabilities of an enterprise. The different approaches will be applied by an entity as their

primary motive is to analyse the existing cost incurred in the business in order to reduce the

burden of the external market (Wouters and Stecher, 2017).

Break even point will be applied by the owner in improving the skills of their business as

this point will be helpful for an entity in boosting their skills and the capabilities. An entity

determines this break even point as the sales units produced by the firm above than this point

will lead to earn profit otherwise loss.

This point is regarded as shutdown point where an entity will only recover overall cost

incurred by them in their business and no provision of profit earned by them.

Break even point= Fixed cost/Contribution per unit

Particulars cost per unit Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8

Units produced 8000 10000 12000 14000 16000 18000 20000 22000

Sales 10 80000 100000 120000 140000 160000 180000 200000 220000

Variable cost 5 40000 50000 60000 70000 80000 90000 100000 110000

Contribution 5 40000 50000 60000 70000 80000 90000 100000 110000

Fixed cost 10000 10000 10000 10000 10000 10000 10000 10000

Profit 30000 40000 50000 60000 70000 80000 90000 100000

3

accounting which involves three components such as cost, volume and profit. It can be said that

this trilogy involves major involvement of cost and volume of the business which will directly

affects on the production of profit in the business enterprise. Nisa retail store inspire to earn

profit in the business as their primary motive of opening the firm is to gain higher amount of

profit after dealing all their current products or services. The primary concern of the top

management of Nisa Retail store is to seek for various techniques in order to reduce overall cost

incurred by an entity in their business. Cost reduction strategies are crafted by an entity in which

major principle followed by an entity owner is of optimum utilisation of resources. The input

applied in the business needs to be check properly as wrong one would destroy the current image

of the business in front of all competitors who intends to suppress the current skills and the

capabilities of an enterprise. The different approaches will be applied by an entity as their

primary motive is to analyse the existing cost incurred in the business in order to reduce the

burden of the external market (Wouters and Stecher, 2017).

Break even point will be applied by the owner in improving the skills of their business as

this point will be helpful for an entity in boosting their skills and the capabilities. An entity

determines this break even point as the sales units produced by the firm above than this point

will lead to earn profit otherwise loss.

This point is regarded as shutdown point where an entity will only recover overall cost

incurred by them in their business and no provision of profit earned by them.

Break even point= Fixed cost/Contribution per unit

Particulars cost per unit Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8

Units produced 8000 10000 12000 14000 16000 18000 20000 22000

Sales 10 80000 100000 120000 140000 160000 180000 200000 220000

Variable cost 5 40000 50000 60000 70000 80000 90000 100000 110000

Contribution 5 40000 50000 60000 70000 80000 90000 100000 110000

Fixed cost 10000 10000 10000 10000 10000 10000 10000 10000

Profit 30000 40000 50000 60000 70000 80000 90000 100000

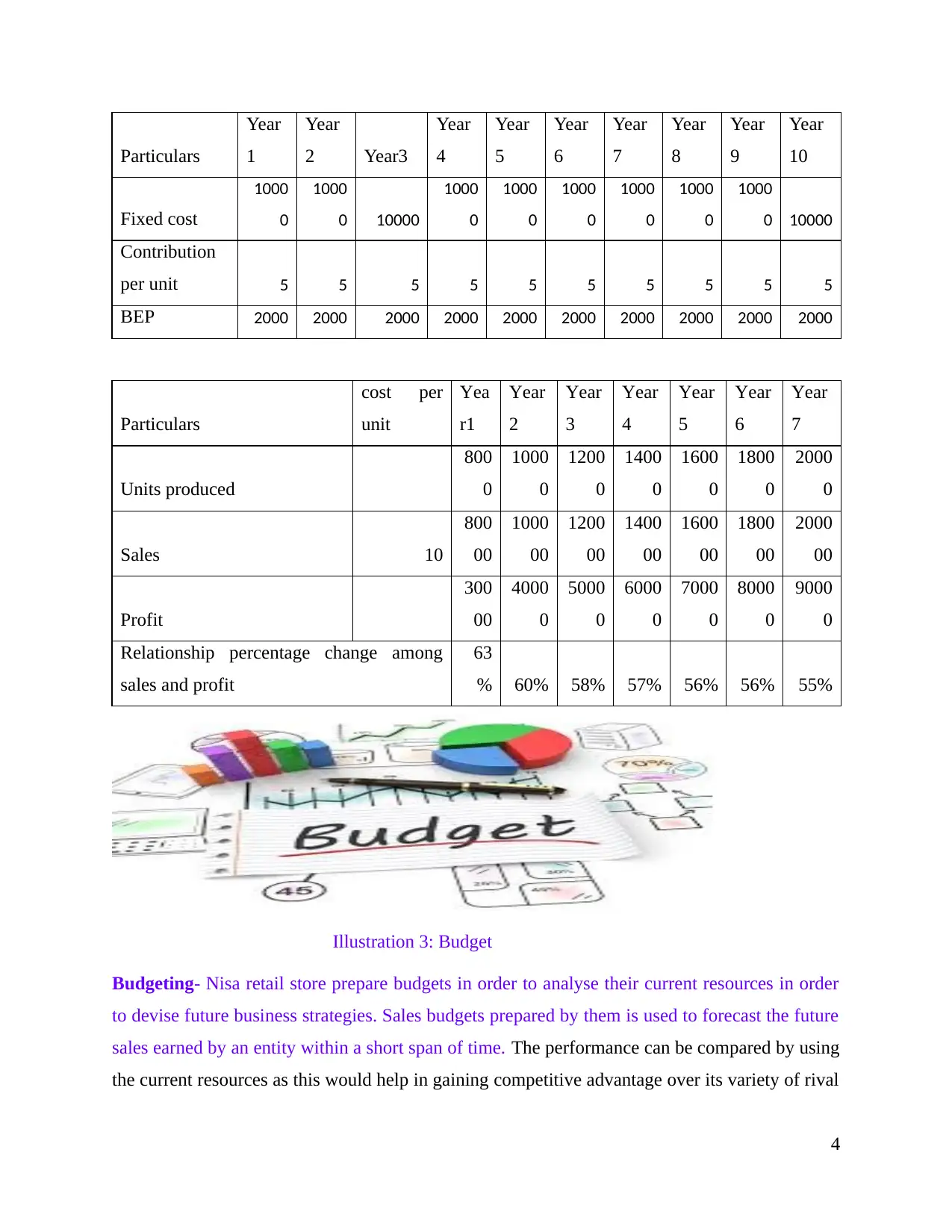

3

Particulars

Year

1

Year

2 Year3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Fixed cost

1000

0

1000

0 10000

1000

0

1000

0

1000

0

1000

0

1000

0

1000

0 10000

Contribution

per unit 5 5 5 5 5 5 5 5 5 5

BEP 2000 2000 2000 2000 2000 2000 2000 2000 2000 2000

Particulars

cost per

unit

Yea

r1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Units produced

800

0

1000

0

1200

0

1400

0

1600

0

1800

0

2000

0

Sales 10

800

00

1000

00

1200

00

1400

00

1600

00

1800

00

2000

00

Profit

300

00

4000

0

5000

0

6000

0

7000

0

8000

0

9000

0

Relationship percentage change among

sales and profit

63

% 60% 58% 57% 56% 56% 55%

Illustration 3: Budget

Budgeting- Nisa retail store prepare budgets in order to analyse their current resources in order

to devise future business strategies. Sales budgets prepared by them is used to forecast the future

sales earned by an entity within a short span of time. The performance can be compared by using

the current resources as this would help in gaining competitive advantage over its variety of rival

4

Year

1

Year

2 Year3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Fixed cost

1000

0

1000

0 10000

1000

0

1000

0

1000

0

1000

0

1000

0

1000

0 10000

Contribution

per unit 5 5 5 5 5 5 5 5 5 5

BEP 2000 2000 2000 2000 2000 2000 2000 2000 2000 2000

Particulars

cost per

unit

Yea

r1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Units produced

800

0

1000

0

1200

0

1400

0

1600

0

1800

0

2000

0

Sales 10

800

00

1000

00

1200

00

1400

00

1600

00

1800

00

2000

00

Profit

300

00

4000

0

5000

0

6000

0

7000

0

8000

0

9000

0

Relationship percentage change among

sales and profit

63

% 60% 58% 57% 56% 56% 55%

Illustration 3: Budget

Budgeting- Nisa retail store prepare budgets in order to analyse their current resources in order

to devise future business strategies. Sales budgets prepared by them is used to forecast the future

sales earned by an entity within a short span of time. The performance can be compared by using

the current resources as this would help in gaining competitive advantage over its variety of rival

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

members in the external market. It is regarded as corporate strategy which gives ultimate

direction to different strategic business units just like budgets prepared for different business

departments of an organisation. It can be said an entity will be able to maintain perfect balance

among income and expenditure incurred by them in a particular year. The budget plan prepared

by an entity in regulating all the expenditures incurred by them in accomplishing their goals and

the objectives as their primary motive is to gain higher image in entire external market (Hiebl,

Gärtner and Duller, 2017).

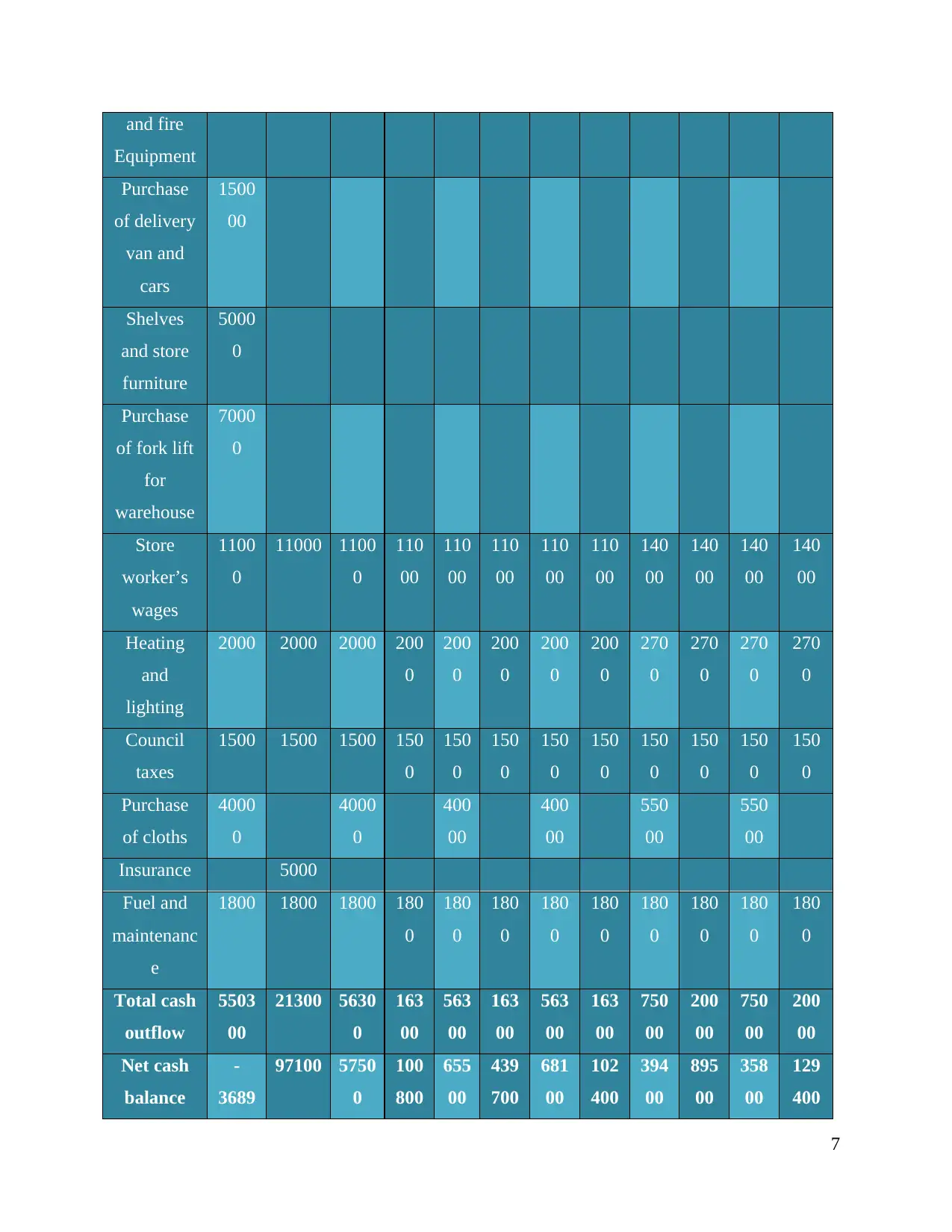

Cash budget is another important statement of cash flow prepared by Nisa retail store in

order to ensure its current earnings in relation to all the expenditures incurred by them in a

particular financial year. Cash flow of future of Nisa retail store are forecasted as being a

supermarket owner they are required to analyse all the resources or inventory currently utilised in

their business in relation to the future targets of their business. Budgets prepared by an entity

will act as forecasting tool which emphasises on predicting the higher performance of the

business in relation to its external market as their primary motive is to gain the trusts of all the

employees working for the sake of an enterprise. Finance imposed by an entity in meeting their

business requirements can be tracked by preparing the budgets. These budgets can be act as

tracking system which helps an entity in order to make important decisions as delayed actions

can be rectified by preparing budgets.

Particular

s

Jan Feb Mar

ch

Apr

il

Ma

y

Jun

e

Jul

y

Au

g

Sep

t

Oct Nov Dec

Initial cash 5000

0

Bank loan 5500

0

Income

from

online

sales

3200

0

40000 3500

0

380

00

410

00

420

00

360

00

280

00

270

00

275

00

280

00

330

00

Income 2240 56400 5680 571 588 620 664 687 654 600 608 644

5

direction to different strategic business units just like budgets prepared for different business

departments of an organisation. It can be said an entity will be able to maintain perfect balance

among income and expenditure incurred by them in a particular year. The budget plan prepared

by an entity in regulating all the expenditures incurred by them in accomplishing their goals and

the objectives as their primary motive is to gain higher image in entire external market (Hiebl,

Gärtner and Duller, 2017).

Cash budget is another important statement of cash flow prepared by Nisa retail store in

order to ensure its current earnings in relation to all the expenditures incurred by them in a

particular financial year. Cash flow of future of Nisa retail store are forecasted as being a

supermarket owner they are required to analyse all the resources or inventory currently utilised in

their business in relation to the future targets of their business. Budgets prepared by an entity

will act as forecasting tool which emphasises on predicting the higher performance of the

business in relation to its external market as their primary motive is to gain the trusts of all the

employees working for the sake of an enterprise. Finance imposed by an entity in meeting their

business requirements can be tracked by preparing the budgets. These budgets can be act as

tracking system which helps an entity in order to make important decisions as delayed actions

can be rectified by preparing budgets.

Particular

s

Jan Feb Mar

ch

Apr

il

Ma

y

Jun

e

Jul

y

Au

g

Sep

t

Oct Nov Dec

Initial cash 5000

0

Bank loan 5500

0

Income

from

online

sales

3200

0

40000 3500

0

380

00

410

00

420

00

360

00

280

00

270

00

275

00

280

00

330

00

Income 2240 56400 5680 571 588 620 664 687 654 600 608 644

5

from in-

store sales

0 0 00 00 00 00 00 00 00 00 00

Sales

income

from

fashion

clothing

1000

0

10000 1000

0

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

Sales

income

from hair

and beauty

products

1200

0

12000 1200

0

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

Receipts

from

disposal of

old store

building

300

000

Total

interest

receivables

300

00

300

00

Total cash

income

1814

00

11840

0

1138

00

117

100

121

800

456

000

124

400

118

700

114

400

109

500

110

800

149

400

Cash

disburseme

nt

Store and

warehouse

building

lease rental

1440

00

Purchase

of office

8000

0

6

store sales

0 0 00 00 00 00 00 00 00 00 00

Sales

income

from

fashion

clothing

1000

0

10000 1000

0

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

Sales

income

from hair

and beauty

products

1200

0

12000 1200

0

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

Receipts

from

disposal of

old store

building

300

000

Total

interest

receivables

300

00

300

00

Total cash

income

1814

00

11840

0

1138

00

117

100

121

800

456

000

124

400

118

700

114

400

109

500

110

800

149

400

Cash

disburseme

nt

Store and

warehouse

building

lease rental

1440

00

Purchase

of office

8000

0

6

and fire

Equipment

Purchase

of delivery

van and

cars

1500

00

Shelves

and store

furniture

5000

0

Purchase

of fork lift

for

warehouse

7000

0

Store

worker’s

wages

1100

0

11000 1100

0

110

00

110

00

110

00

110

00

110

00

140

00

140

00

140

00

140

00

Heating

and

lighting

2000 2000 2000 200

0

200

0

200

0

200

0

200

0

270

0

270

0

270

0

270

0

Council

taxes

1500 1500 1500 150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

Purchase

of cloths

4000

0

4000

0

400

00

400

00

550

00

550

00

Insurance 5000

Fuel and

maintenanc

e

1800 1800 1800 180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

Total cash

outflow

5503

00

21300 5630

0

163

00

563

00

163

00

563

00

163

00

750

00

200

00

750

00

200

00

Net cash

balance

-

3689

97100 5750

0

100

800

655

00

439

700

681

00

102

400

394

00

895

00

358

00

129

400

7

Equipment

Purchase

of delivery

van and

cars

1500

00

Shelves

and store

furniture

5000

0

Purchase

of fork lift

for

warehouse

7000

0

Store

worker’s

wages

1100

0

11000 1100

0

110

00

110

00

110

00

110

00

110

00

140

00

140

00

140

00

140

00

Heating

and

lighting

2000 2000 2000 200

0

200

0

200

0

200

0

200

0

270

0

270

0

270

0

270

0

Council

taxes

1500 1500 1500 150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

Purchase

of cloths

4000

0

4000

0

400

00

400

00

550

00

550

00

Insurance 5000

Fuel and

maintenanc

e

1800 1800 1800 180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

Total cash

outflow

5503

00

21300 5630

0

163

00

563

00

163

00

563

00

163

00

750

00

200

00

750

00

200

00

Net cash

balance

-

3689

97100 5750

0

100

800

655

00

439

700

681

00

102

400

394

00

895

00

358

00

129

400

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

00

Opening

cash

balance

0 -

36890

0

-

2718

00

-

214

300

-

113

500

-

480

00

391

700

459

800

562

200

601

600

691

100

726

900

Closing

cash

balance

-

3689

00

-

27180

0

-

2143

00

-

113

500

-

480

00

391

700

459

800

562

200

601

600

691

100

726

900

856

300

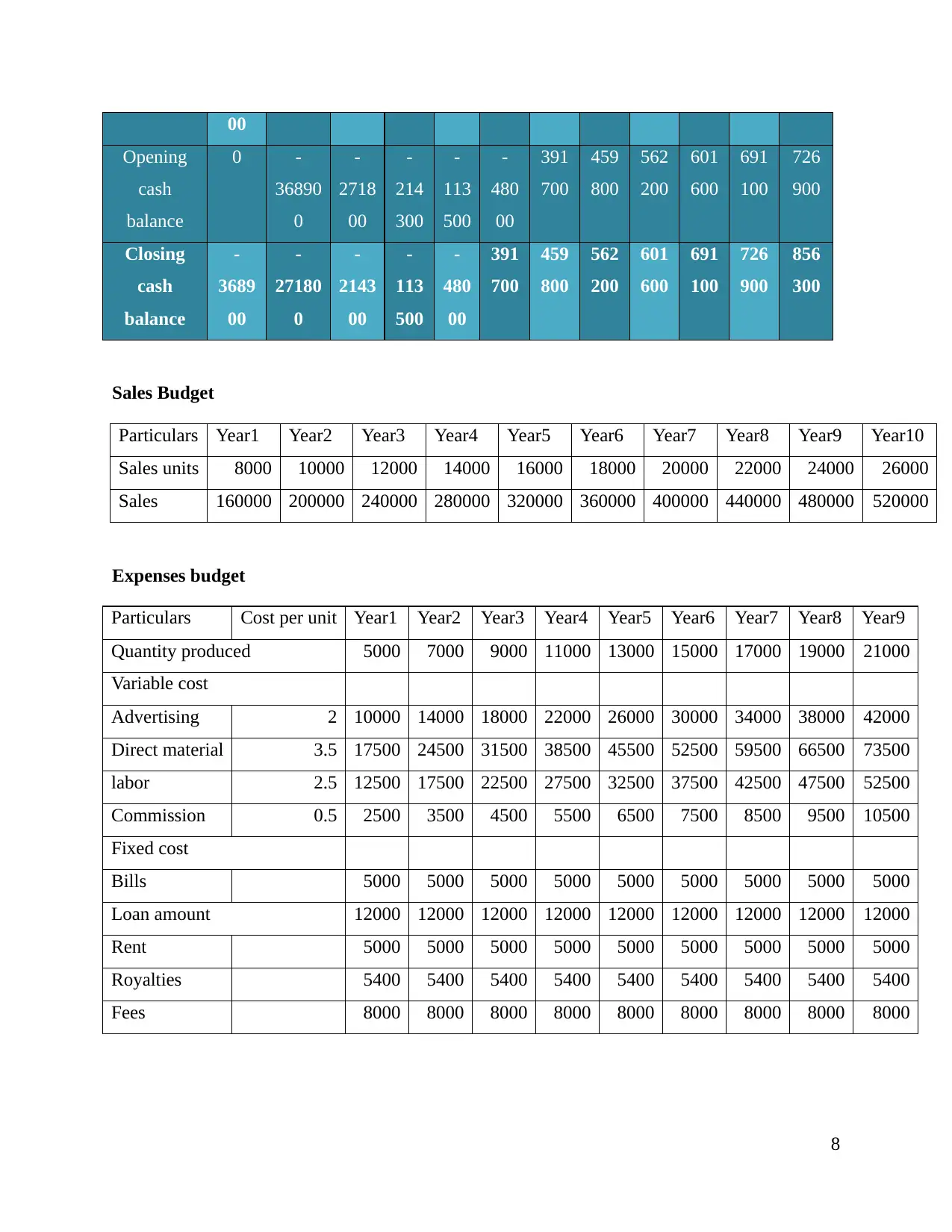

Sales Budget

Particulars Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9 Year10

Sales units 8000 10000 12000 14000 16000 18000 20000 22000 24000 26000

Sales 160000 200000 240000 280000 320000 360000 400000 440000 480000 520000

Expenses budget

Particulars Cost per unit Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9

Quantity produced 5000 7000 9000 11000 13000 15000 17000 19000 21000

Variable cost

Advertising 2 10000 14000 18000 22000 26000 30000 34000 38000 42000

Direct material 3.5 17500 24500 31500 38500 45500 52500 59500 66500 73500

labor 2.5 12500 17500 22500 27500 32500 37500 42500 47500 52500

Commission 0.5 2500 3500 4500 5500 6500 7500 8500 9500 10500

Fixed cost

Bills 5000 5000 5000 5000 5000 5000 5000 5000 5000

Loan amount 12000 12000 12000 12000 12000 12000 12000 12000 12000

Rent 5000 5000 5000 5000 5000 5000 5000 5000 5000

Royalties 5400 5400 5400 5400 5400 5400 5400 5400 5400

Fees 8000 8000 8000 8000 8000 8000 8000 8000 8000

8

Opening

cash

balance

0 -

36890

0

-

2718

00

-

214

300

-

113

500

-

480

00

391

700

459

800

562

200

601

600

691

100

726

900

Closing

cash

balance

-

3689

00

-

27180

0

-

2143

00

-

113

500

-

480

00

391

700

459

800

562

200

601

600

691

100

726

900

856

300

Sales Budget

Particulars Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9 Year10

Sales units 8000 10000 12000 14000 16000 18000 20000 22000 24000 26000

Sales 160000 200000 240000 280000 320000 360000 400000 440000 480000 520000

Expenses budget

Particulars Cost per unit Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9

Quantity produced 5000 7000 9000 11000 13000 15000 17000 19000 21000

Variable cost

Advertising 2 10000 14000 18000 22000 26000 30000 34000 38000 42000

Direct material 3.5 17500 24500 31500 38500 45500 52500 59500 66500 73500

labor 2.5 12500 17500 22500 27500 32500 37500 42500 47500 52500

Commission 0.5 2500 3500 4500 5500 6500 7500 8500 9500 10500

Fixed cost

Bills 5000 5000 5000 5000 5000 5000 5000 5000 5000

Loan amount 12000 12000 12000 12000 12000 12000 12000 12000 12000

Rent 5000 5000 5000 5000 5000 5000 5000 5000 5000

Royalties 5400 5400 5400 5400 5400 5400 5400 5400 5400

Fees 8000 8000 8000 8000 8000 8000 8000 8000 8000

8

P2 Explain different methods used for management accounting reporting

Financial accounting method

Illustration 4: Ratio analysis

Ratio analysis- Comparative performance measurement tool that analysed the current

performance of an enterprise in accordance with its previous year performance in uplifting their

current conditions of the business. The ratio analysis is widely used technique of assessing the

current financial statements. Different forms of financial statement of several stores of Nisa retail

store are compared in relation to the headquarter of its supermarket to determine their current

performance. Income statement of all the stores contain sales and the revenue which are

compared in relation to the common goals framed by the main branch of the supermarket store in

order to ascertain the financial performance in order to gain higher competitive advantage.

Different variety of the ratio analysis states that it ascertains the performance of the business in

relation to various parameters such as profitability and liquidity (Müller-Stewens and Möller,

2017). The favourable or adverse results of all these ratios to the notice of the management as the

adverse results can be rectified by the management by making important decisions in order to

regulate their performance. The performance of an entity can be managed or regulated by

removing the causes of incurring adverse ratios. The deficiency from the management can be

rectified by focusing on capabilities of the business as an enterprise owner focuses on reducing

their weaknesses. Cost of sales and taxation are those deficiencies that reduce the capability of an

entity which will be regulated. On the other hand, liquidity is essential for the management as

expenses incurred in the business can be managed

Profitability ratios

Particulars Formula 2015 2016

9

Financial accounting method

Illustration 4: Ratio analysis

Ratio analysis- Comparative performance measurement tool that analysed the current

performance of an enterprise in accordance with its previous year performance in uplifting their

current conditions of the business. The ratio analysis is widely used technique of assessing the

current financial statements. Different forms of financial statement of several stores of Nisa retail

store are compared in relation to the headquarter of its supermarket to determine their current

performance. Income statement of all the stores contain sales and the revenue which are

compared in relation to the common goals framed by the main branch of the supermarket store in

order to ascertain the financial performance in order to gain higher competitive advantage.

Different variety of the ratio analysis states that it ascertains the performance of the business in

relation to various parameters such as profitability and liquidity (Müller-Stewens and Möller,

2017). The favourable or adverse results of all these ratios to the notice of the management as the

adverse results can be rectified by the management by making important decisions in order to

regulate their performance. The performance of an entity can be managed or regulated by

removing the causes of incurring adverse ratios. The deficiency from the management can be

rectified by focusing on capabilities of the business as an enterprise owner focuses on reducing

their weaknesses. Cost of sales and taxation are those deficiencies that reduce the capability of an

entity which will be regulated. On the other hand, liquidity is essential for the management as

expenses incurred in the business can be managed

Profitability ratios

Particulars Formula 2015 2016

9

Revenue 1220 1255

GP 175 178

Net Profit 23 33

Gross profit Ratio GP/Net sales*100 14.34426 14.18327

Net profit Net profit/Net sales*100 1.885246 2.629482

Liquidity ratio 2015 2016

Current assets 746 785

Current liabilities 309 317

Current ratio Current asset/Current liabilities 2.414239 2.476341

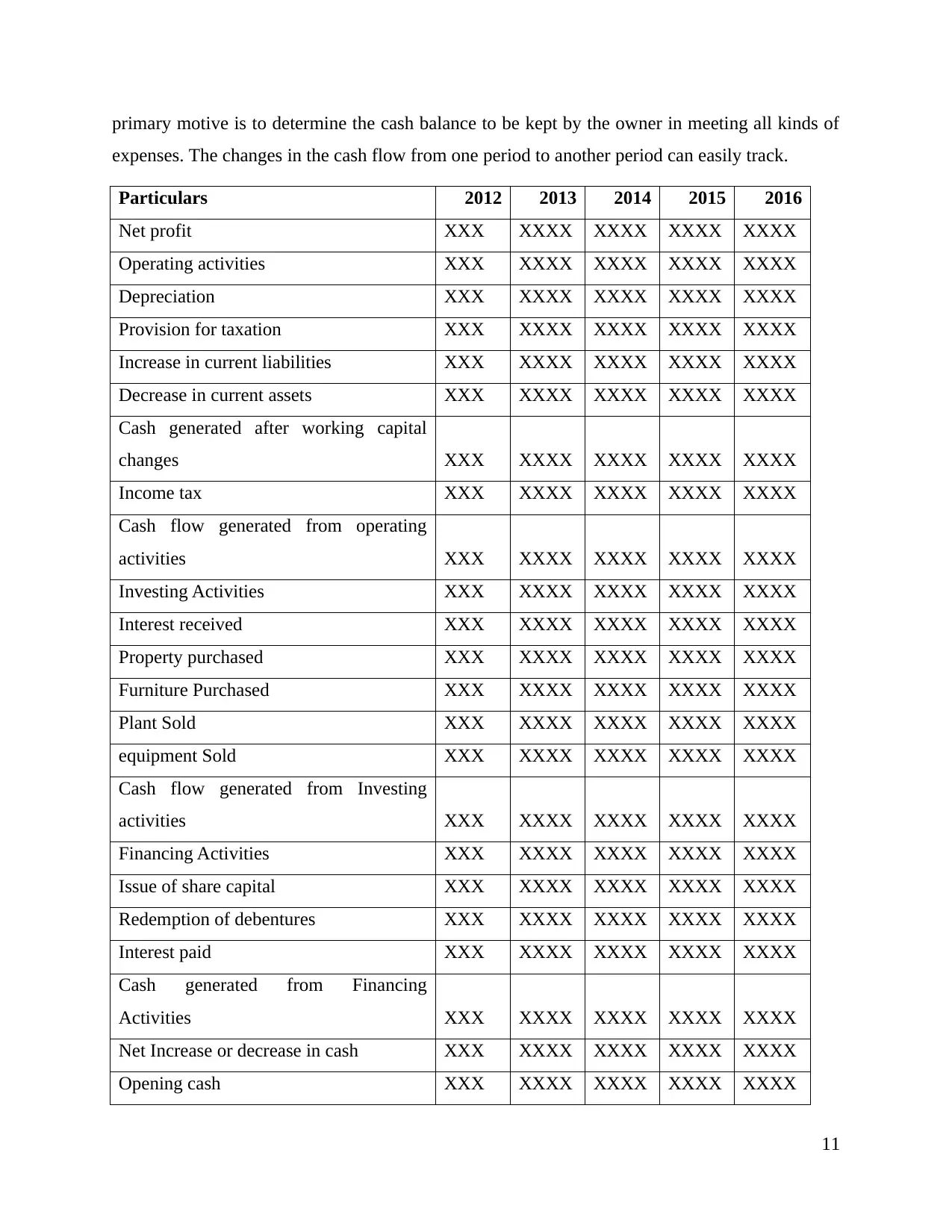

Cash flow analysis

Illustration 5: Cash flow analysis

Cash flow statements prepared in the firm in order to assess the overall movement of cash

in the business enterprise. The movement of cash inflow or outflow can be ascertained by an

enterprise owner as cash is regarded as important component for the business. The current

statement will only consider all this transaction which are only in cash as credit transactions are

not included in this particular statement. This can be prepared by categorizing into three

activities operating, financing and investing activities which will involve all business

transactions. Nisa retail store is small based entity are not under any kind of obligation while

preparing its financial statements such as cash flow statement. IAS 7 is related to the accounting

treatment of cash transactions in an entity on an international level. The slightly changes are

done while preparation of these statements under indirect or direct method of preparation whose

10

GP 175 178

Net Profit 23 33

Gross profit Ratio GP/Net sales*100 14.34426 14.18327

Net profit Net profit/Net sales*100 1.885246 2.629482

Liquidity ratio 2015 2016

Current assets 746 785

Current liabilities 309 317

Current ratio Current asset/Current liabilities 2.414239 2.476341

Cash flow analysis

Illustration 5: Cash flow analysis

Cash flow statements prepared in the firm in order to assess the overall movement of cash

in the business enterprise. The movement of cash inflow or outflow can be ascertained by an

enterprise owner as cash is regarded as important component for the business. The current

statement will only consider all this transaction which are only in cash as credit transactions are

not included in this particular statement. This can be prepared by categorizing into three

activities operating, financing and investing activities which will involve all business

transactions. Nisa retail store is small based entity are not under any kind of obligation while

preparing its financial statements such as cash flow statement. IAS 7 is related to the accounting

treatment of cash transactions in an entity on an international level. The slightly changes are

done while preparation of these statements under indirect or direct method of preparation whose

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

primary motive is to determine the cash balance to be kept by the owner in meeting all kinds of

expenses. The changes in the cash flow from one period to another period can easily track.

Particulars 2012 2013 2014 2015 2016

Net profit XXX XXXX XXXX XXXX XXXX

Operating activities XXX XXXX XXXX XXXX XXXX

Depreciation XXX XXXX XXXX XXXX XXXX

Provision for taxation XXX XXXX XXXX XXXX XXXX

Increase in current liabilities XXX XXXX XXXX XXXX XXXX

Decrease in current assets XXX XXXX XXXX XXXX XXXX

Cash generated after working capital

changes XXX XXXX XXXX XXXX XXXX

Income tax XXX XXXX XXXX XXXX XXXX

Cash flow generated from operating

activities XXX XXXX XXXX XXXX XXXX

Investing Activities XXX XXXX XXXX XXXX XXXX

Interest received XXX XXXX XXXX XXXX XXXX

Property purchased XXX XXXX XXXX XXXX XXXX

Furniture Purchased XXX XXXX XXXX XXXX XXXX

Plant Sold XXX XXXX XXXX XXXX XXXX

equipment Sold XXX XXXX XXXX XXXX XXXX

Cash flow generated from Investing

activities XXX XXXX XXXX XXXX XXXX

Financing Activities XXX XXXX XXXX XXXX XXXX

Issue of share capital XXX XXXX XXXX XXXX XXXX

Redemption of debentures XXX XXXX XXXX XXXX XXXX

Interest paid XXX XXXX XXXX XXXX XXXX

Cash generated from Financing

Activities XXX XXXX XXXX XXXX XXXX

Net Increase or decrease in cash XXX XXXX XXXX XXXX XXXX

Opening cash XXX XXXX XXXX XXXX XXXX

11

expenses. The changes in the cash flow from one period to another period can easily track.

Particulars 2012 2013 2014 2015 2016

Net profit XXX XXXX XXXX XXXX XXXX

Operating activities XXX XXXX XXXX XXXX XXXX

Depreciation XXX XXXX XXXX XXXX XXXX

Provision for taxation XXX XXXX XXXX XXXX XXXX

Increase in current liabilities XXX XXXX XXXX XXXX XXXX

Decrease in current assets XXX XXXX XXXX XXXX XXXX

Cash generated after working capital

changes XXX XXXX XXXX XXXX XXXX

Income tax XXX XXXX XXXX XXXX XXXX

Cash flow generated from operating

activities XXX XXXX XXXX XXXX XXXX

Investing Activities XXX XXXX XXXX XXXX XXXX

Interest received XXX XXXX XXXX XXXX XXXX

Property purchased XXX XXXX XXXX XXXX XXXX

Furniture Purchased XXX XXXX XXXX XXXX XXXX

Plant Sold XXX XXXX XXXX XXXX XXXX

equipment Sold XXX XXXX XXXX XXXX XXXX

Cash flow generated from Investing

activities XXX XXXX XXXX XXXX XXXX

Financing Activities XXX XXXX XXXX XXXX XXXX

Issue of share capital XXX XXXX XXXX XXXX XXXX

Redemption of debentures XXX XXXX XXXX XXXX XXXX

Interest paid XXX XXXX XXXX XXXX XXXX

Cash generated from Financing

Activities XXX XXXX XXXX XXXX XXXX

Net Increase or decrease in cash XXX XXXX XXXX XXXX XXXX

Opening cash XXX XXXX XXXX XXXX XXXX

11

Closing cash XXX XXXX XXXX XXXX XXXX

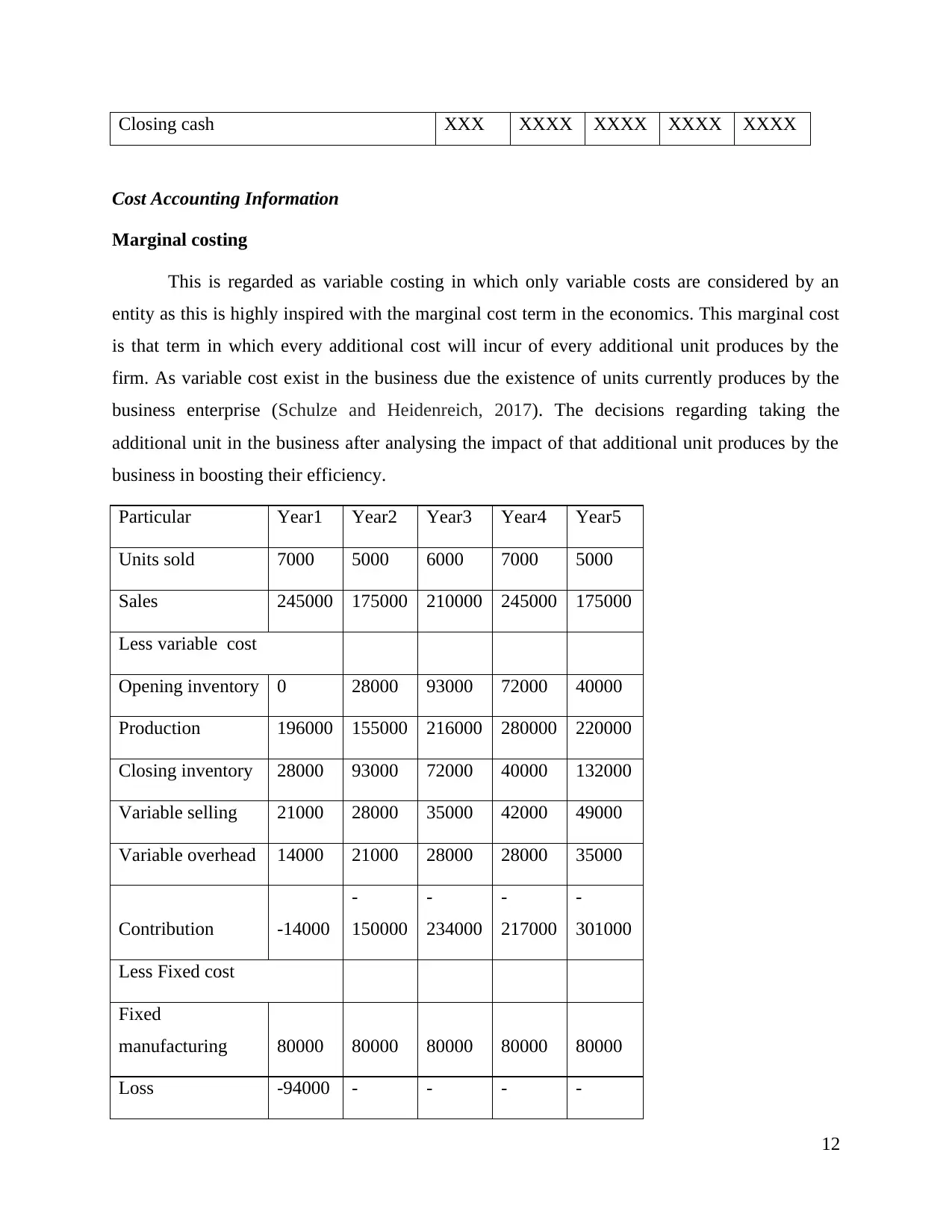

Cost Accounting Information

Marginal costing

This is regarded as variable costing in which only variable costs are considered by an

entity as this is highly inspired with the marginal cost term in the economics. This marginal cost

is that term in which every additional cost will incur of every additional unit produces by the

firm. As variable cost exist in the business due the existence of units currently produces by the

business enterprise (Schulze and Heidenreich, 2017). The decisions regarding taking the

additional unit in the business after analysing the impact of that additional unit produces by the

business in boosting their efficiency.

Particular Year1 Year2 Year3 Year4 Year5

Units sold 7000 5000 6000 7000 5000

Sales 245000 175000 210000 245000 175000

Less variable cost

Opening inventory 0 28000 93000 72000 40000

Production 196000 155000 216000 280000 220000

Closing inventory 28000 93000 72000 40000 132000

Variable selling 21000 28000 35000 42000 49000

Variable overhead 14000 21000 28000 28000 35000

Contribution -14000

-

150000

-

234000

-

217000

-

301000

Less Fixed cost

Fixed

manufacturing 80000 80000 80000 80000 80000

Loss -94000 - - - -

12

Cost Accounting Information

Marginal costing

This is regarded as variable costing in which only variable costs are considered by an

entity as this is highly inspired with the marginal cost term in the economics. This marginal cost

is that term in which every additional cost will incur of every additional unit produces by the

firm. As variable cost exist in the business due the existence of units currently produces by the

business enterprise (Schulze and Heidenreich, 2017). The decisions regarding taking the

additional unit in the business after analysing the impact of that additional unit produces by the

business in boosting their efficiency.

Particular Year1 Year2 Year3 Year4 Year5

Units sold 7000 5000 6000 7000 5000

Sales 245000 175000 210000 245000 175000

Less variable cost

Opening inventory 0 28000 93000 72000 40000

Production 196000 155000 216000 280000 220000

Closing inventory 28000 93000 72000 40000 132000

Variable selling 21000 28000 35000 42000 49000

Variable overhead 14000 21000 28000 28000 35000

Contribution -14000

-

150000

-

234000

-

217000

-

301000

Less Fixed cost

Fixed

manufacturing 80000 80000 80000 80000 80000

Loss -94000 - - - -

12

230000 314000 297000 381000

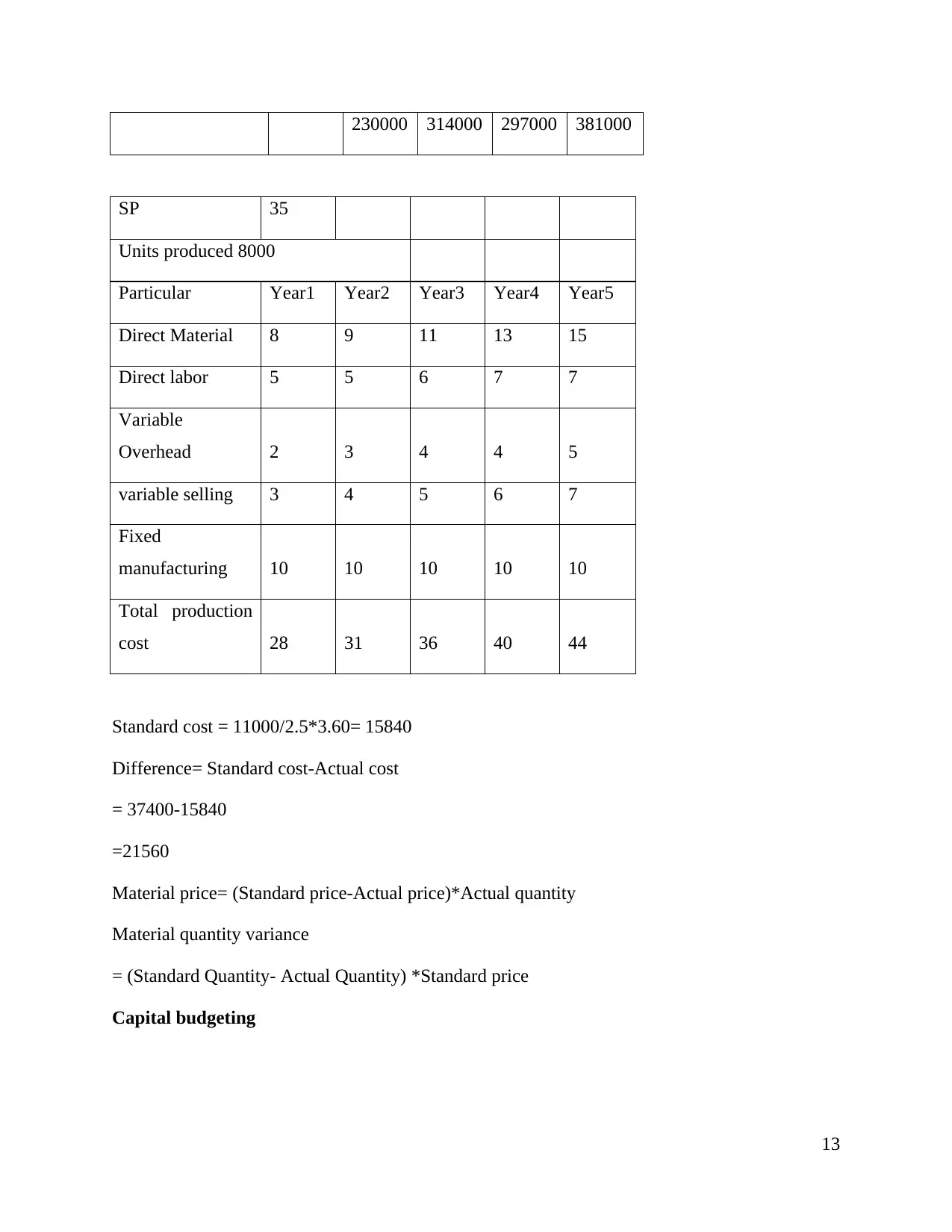

SP 35

Units produced 8000

Particular Year1 Year2 Year3 Year4 Year5

Direct Material 8 9 11 13 15

Direct labor 5 5 6 7 7

Variable

Overhead 2 3 4 4 5

variable selling 3 4 5 6 7

Fixed

manufacturing 10 10 10 10 10

Total production

cost 28 31 36 40 44

Standard cost = 11000/2.5*3.60= 15840

Difference= Standard cost-Actual cost

= 37400-15840

=21560

Material price= (Standard price-Actual price)*Actual quantity

Material quantity variance

= (Standard Quantity- Actual Quantity) *Standard price

Capital budgeting

13

SP 35

Units produced 8000

Particular Year1 Year2 Year3 Year4 Year5

Direct Material 8 9 11 13 15

Direct labor 5 5 6 7 7

Variable

Overhead 2 3 4 4 5

variable selling 3 4 5 6 7

Fixed

manufacturing 10 10 10 10 10

Total production

cost 28 31 36 40 44

Standard cost = 11000/2.5*3.60= 15840

Difference= Standard cost-Actual cost

= 37400-15840

=21560

Material price= (Standard price-Actual price)*Actual quantity

Material quantity variance

= (Standard Quantity- Actual Quantity) *Standard price

Capital budgeting

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

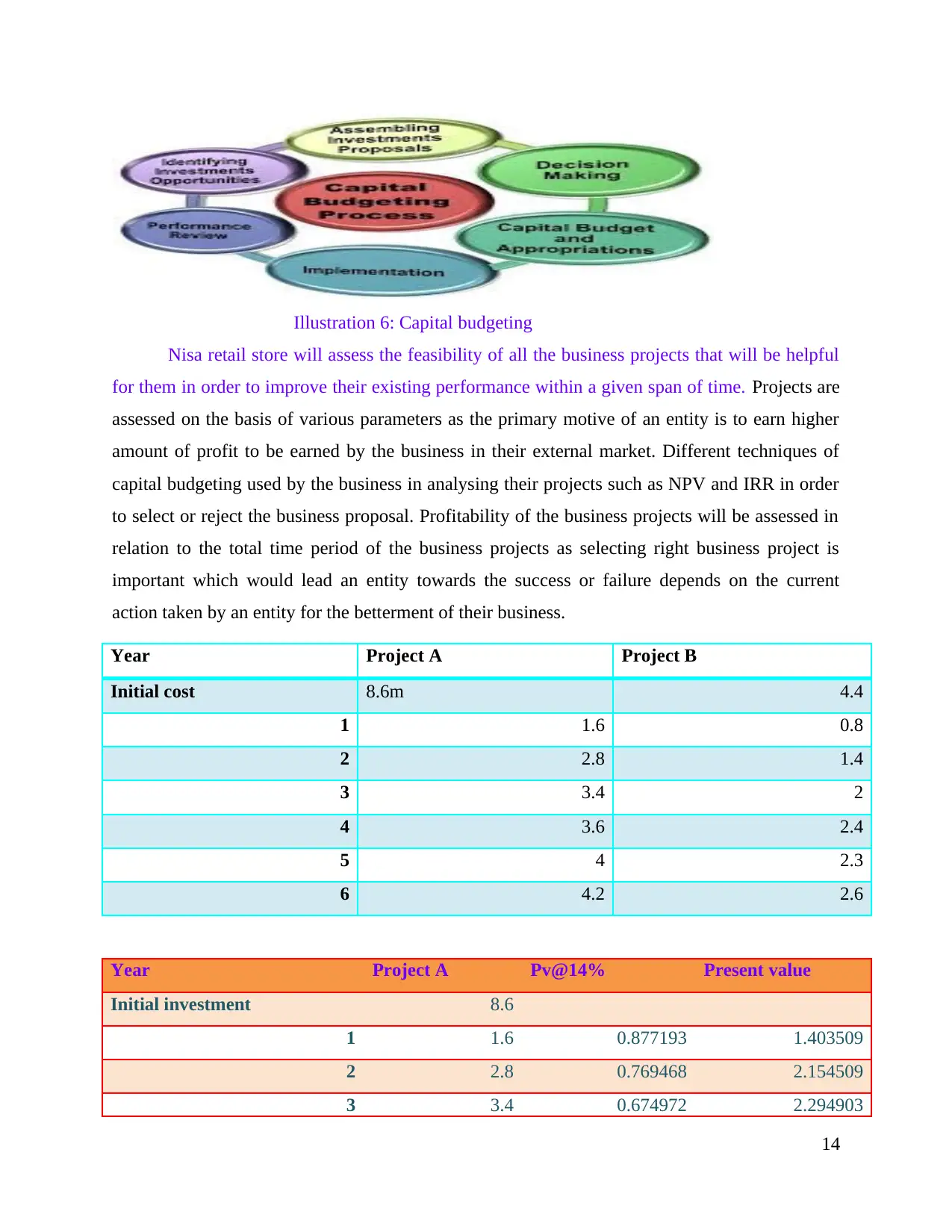

Illustration 6: Capital budgeting

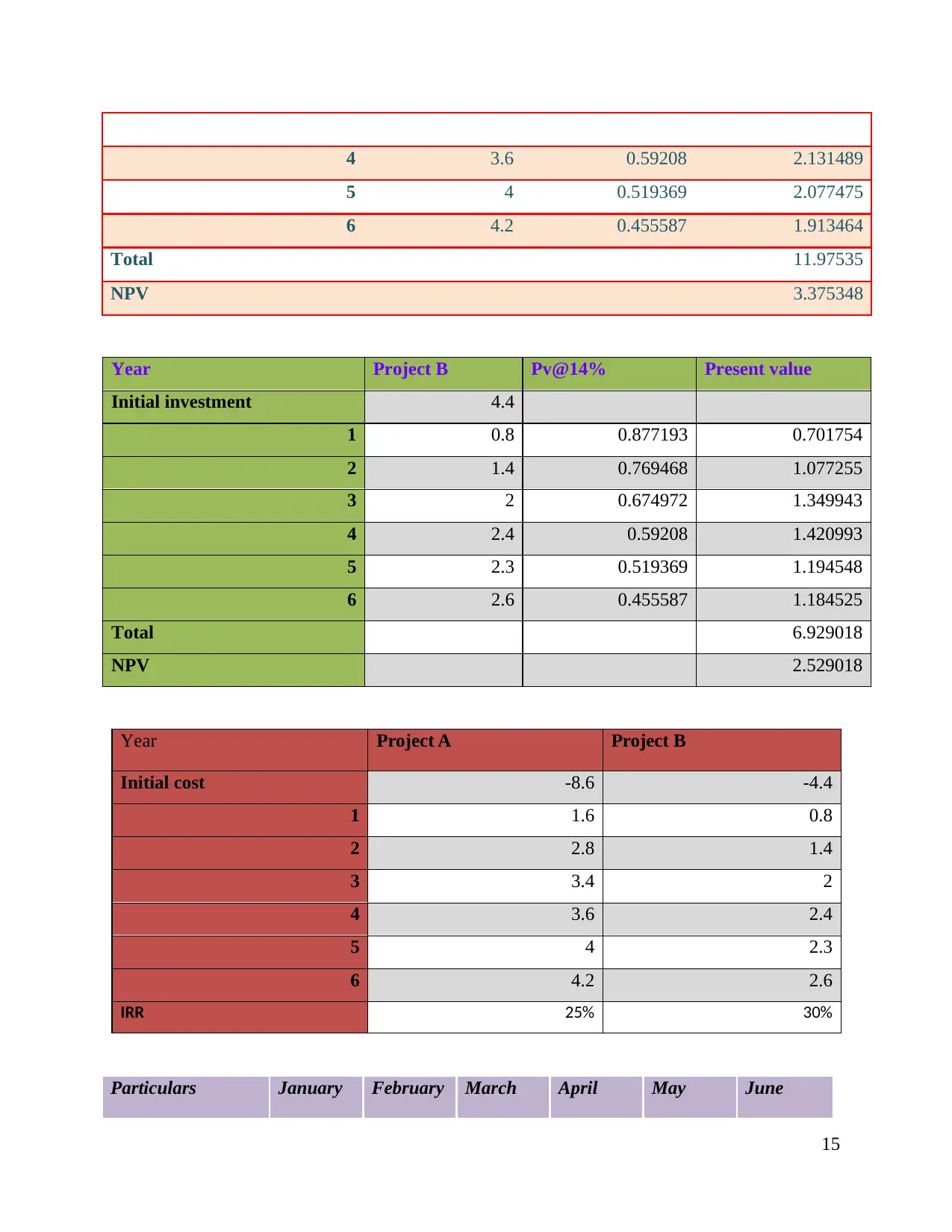

Nisa retail store will assess the feasibility of all the business projects that will be helpful

for them in order to improve their existing performance within a given span of time. Projects are

assessed on the basis of various parameters as the primary motive of an entity is to earn higher

amount of profit to be earned by the business in their external market. Different techniques of

capital budgeting used by the business in analysing their projects such as NPV and IRR in order

to select or reject the business proposal. Profitability of the business projects will be assessed in

relation to the total time period of the business projects as selecting right business project is

important which would lead an entity towards the success or failure depends on the current

action taken by an entity for the betterment of their business.

Year Project A Project B

Initial cost 8.6m 4.4

1 1.6 0.8

2 2.8 1.4

3 3.4 2

4 3.6 2.4

5 4 2.3

6 4.2 2.6

Year Project A Pv@14% Present value

Initial investment 8.6

1 1.6 0.877193 1.403509

2 2.8 0.769468 2.154509

3 3.4 0.674972 2.294903

14

Nisa retail store will assess the feasibility of all the business projects that will be helpful

for them in order to improve their existing performance within a given span of time. Projects are

assessed on the basis of various parameters as the primary motive of an entity is to earn higher

amount of profit to be earned by the business in their external market. Different techniques of

capital budgeting used by the business in analysing their projects such as NPV and IRR in order

to select or reject the business proposal. Profitability of the business projects will be assessed in

relation to the total time period of the business projects as selecting right business project is

important which would lead an entity towards the success or failure depends on the current

action taken by an entity for the betterment of their business.

Year Project A Project B

Initial cost 8.6m 4.4

1 1.6 0.8

2 2.8 1.4

3 3.4 2

4 3.6 2.4

5 4 2.3

6 4.2 2.6

Year Project A Pv@14% Present value

Initial investment 8.6

1 1.6 0.877193 1.403509

2 2.8 0.769468 2.154509

3 3.4 0.674972 2.294903

14

4 3.6 0.59208 2.131489

5 4 0.519369 2.077475

6 4.2 0.455587 1.913464

Total 11.97535

NPV 3.375348

Year Project B Pv@14% Present value

Initial investment 4.4

1 0.8 0.877193 0.701754

2 1.4 0.769468 1.077255

3 2 0.674972 1.349943

4 2.4 0.59208 1.420993

5 2.3 0.519369 1.194548

6 2.6 0.455587 1.184525

Total 6.929018

NPV 2.529018

Year Project A Project B

Initial cost -8.6 -4.4

1 1.6 0.8

2 2.8 1.4

3 3.4 2

4 3.6 2.4

5 4 2.3

6 4.2 2.6

IRR 25% 30%

Particulars January February March April May June

15

5 4 0.519369 2.077475

6 4.2 0.455587 1.913464

Total 11.97535

NPV 3.375348

Year Project B Pv@14% Present value

Initial investment 4.4

1 0.8 0.877193 0.701754

2 1.4 0.769468 1.077255

3 2 0.674972 1.349943

4 2.4 0.59208 1.420993

5 2.3 0.519369 1.194548

6 2.6 0.455587 1.184525

Total 6.929018

NPV 2.529018

Year Project A Project B

Initial cost -8.6 -4.4

1 1.6 0.8

2 2.8 1.4

3 3.4 2

4 3.6 2.4

5 4 2.3

6 4.2 2.6

IRR 25% 30%

Particulars January February March April May June

15

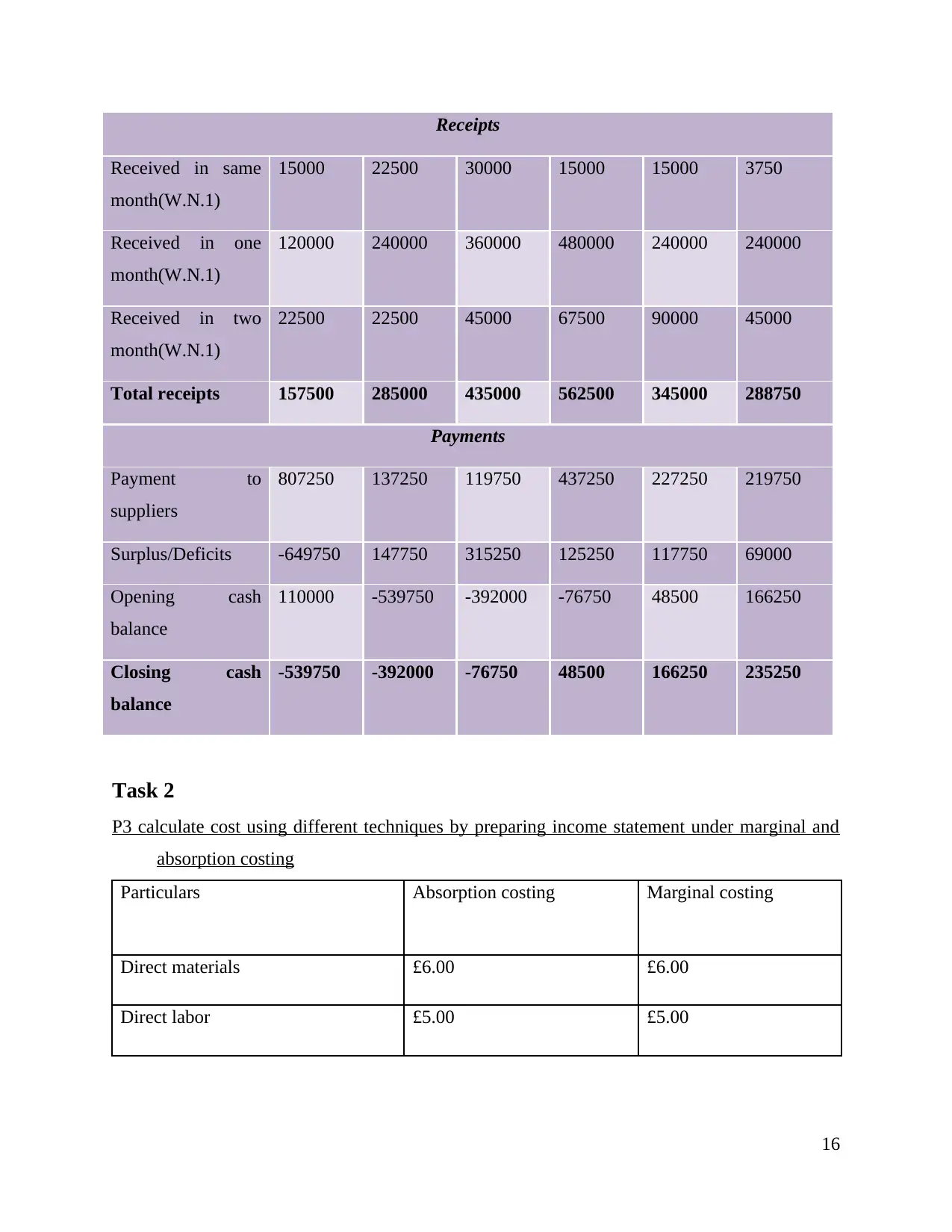

Receipts

Received in same

month(W.N.1)

15000 22500 30000 15000 15000 3750

Received in one

month(W.N.1)

120000 240000 360000 480000 240000 240000

Received in two

month(W.N.1)

22500 22500 45000 67500 90000 45000

Total receipts 157500 285000 435000 562500 345000 288750

Payments

Payment to

suppliers

807250 137250 119750 437250 227250 219750

Surplus/Deficits -649750 147750 315250 125250 117750 69000

Opening cash

balance

110000 -539750 -392000 -76750 48500 166250

Closing cash

balance

-539750 -392000 -76750 48500 166250 235250

Task 2

P3 calculate cost using different techniques by preparing income statement under marginal and

absorption costing

Particulars Absorption costing Marginal costing

Direct materials £6.00 £6.00

Direct labor £5.00 £5.00

16

Received in same

month(W.N.1)

15000 22500 30000 15000 15000 3750

Received in one

month(W.N.1)

120000 240000 360000 480000 240000 240000

Received in two

month(W.N.1)

22500 22500 45000 67500 90000 45000

Total receipts 157500 285000 435000 562500 345000 288750

Payments

Payment to

suppliers

807250 137250 119750 437250 227250 219750

Surplus/Deficits -649750 147750 315250 125250 117750 69000

Opening cash

balance

110000 -539750 -392000 -76750 48500 166250

Closing cash

balance

-539750 -392000 -76750 48500 166250 235250

Task 2

P3 calculate cost using different techniques by preparing income statement under marginal and

absorption costing

Particulars Absorption costing Marginal costing

Direct materials £6.00 £6.00

Direct labor £5.00 £5.00

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

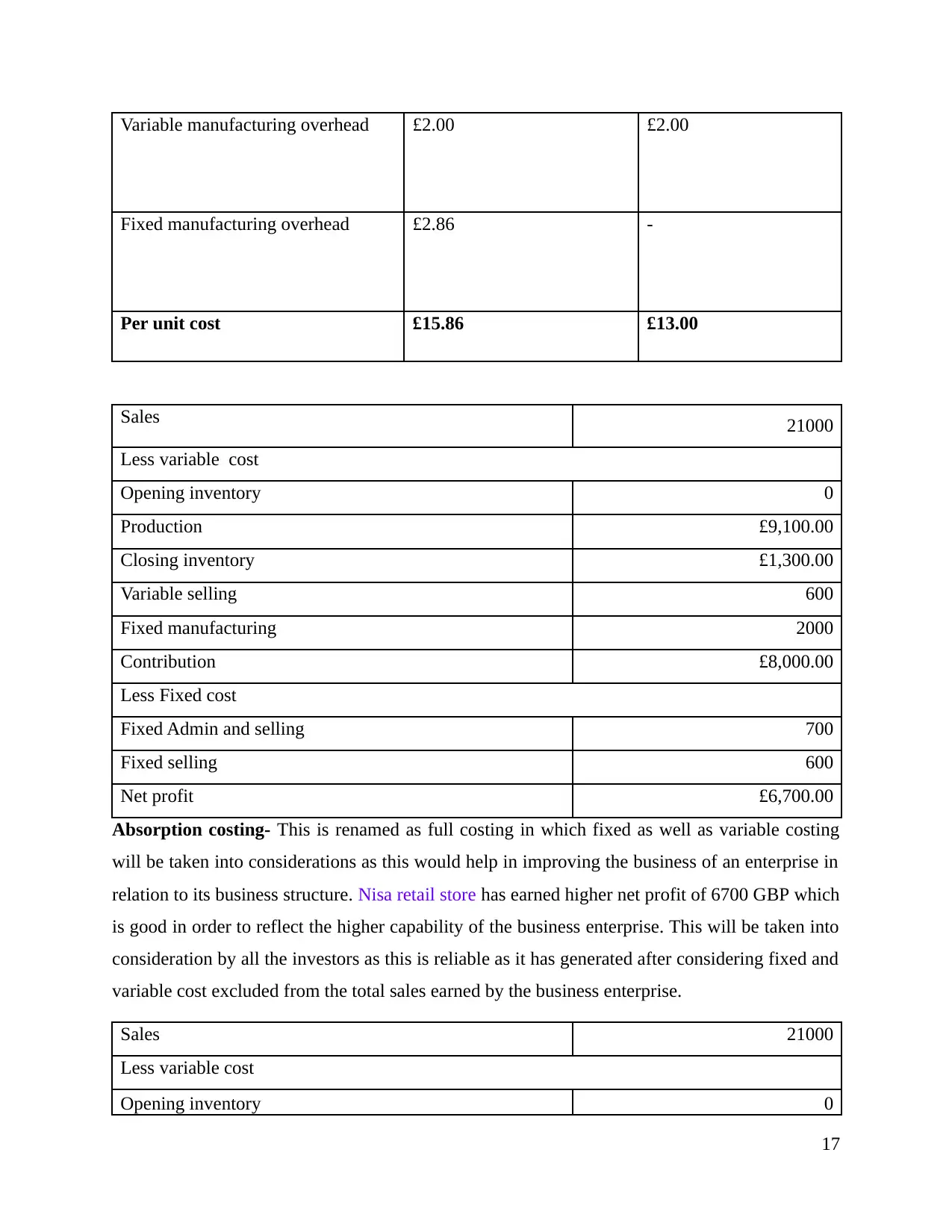

Variable manufacturing overhead £2.00 £2.00

Fixed manufacturing overhead £2.86 -

Per unit cost £15.86 £13.00

Sales 21000

Less variable cost

Opening inventory 0

Production £9,100.00

Closing inventory £1,300.00

Variable selling 600

Fixed manufacturing 2000

Contribution £8,000.00

Less Fixed cost

Fixed Admin and selling 700

Fixed selling 600

Net profit £6,700.00

Absorption costing- This is renamed as full costing in which fixed as well as variable costing

will be taken into considerations as this would help in improving the business of an enterprise in

relation to its business structure. Nisa retail store has earned higher net profit of 6700 GBP which

is good in order to reflect the higher capability of the business enterprise. This will be taken into

consideration by all the investors as this is reliable as it has generated after considering fixed and

variable cost excluded from the total sales earned by the business enterprise.

Sales 21000

Less variable cost

Opening inventory 0

17

Fixed manufacturing overhead £2.86 -

Per unit cost £15.86 £13.00

Sales 21000

Less variable cost

Opening inventory 0

Production £9,100.00

Closing inventory £1,300.00

Variable selling 600

Fixed manufacturing 2000

Contribution £8,000.00

Less Fixed cost

Fixed Admin and selling 700

Fixed selling 600

Net profit £6,700.00

Absorption costing- This is renamed as full costing in which fixed as well as variable costing

will be taken into considerations as this would help in improving the business of an enterprise in

relation to its business structure. Nisa retail store has earned higher net profit of 6700 GBP which

is good in order to reflect the higher capability of the business enterprise. This will be taken into

consideration by all the investors as this is reliable as it has generated after considering fixed and

variable cost excluded from the total sales earned by the business enterprise.

Sales 21000

Less variable cost

Opening inventory 0

17

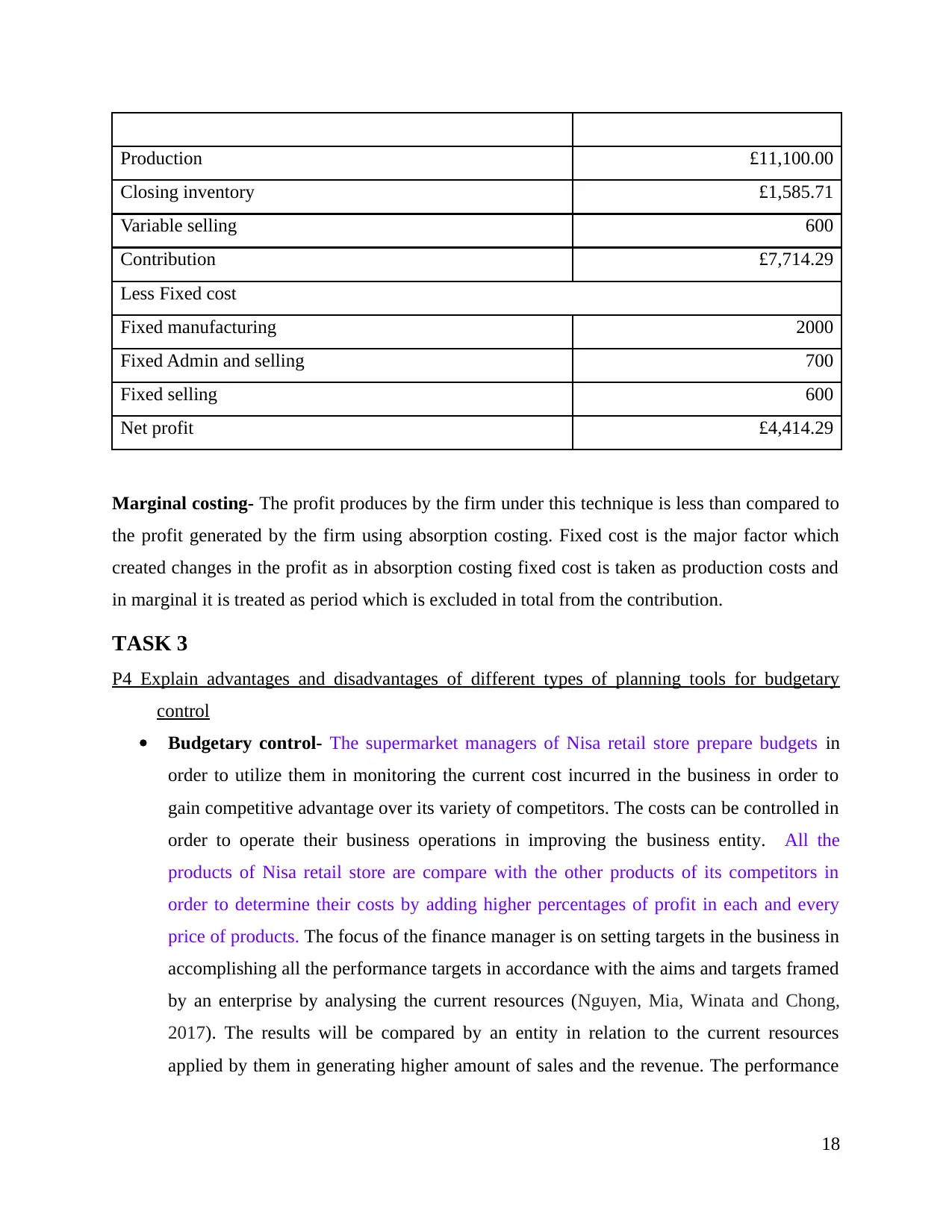

Production £11,100.00

Closing inventory £1,585.71

Variable selling 600

Contribution £7,714.29

Less Fixed cost

Fixed manufacturing 2000

Fixed Admin and selling 700

Fixed selling 600

Net profit £4,414.29

Marginal costing- The profit produces by the firm under this technique is less than compared to

the profit generated by the firm using absorption costing. Fixed cost is the major factor which

created changes in the profit as in absorption costing fixed cost is taken as production costs and

in marginal it is treated as period which is excluded in total from the contribution.

TASK 3

P4 Explain advantages and disadvantages of different types of planning tools for budgetary

control

Budgetary control- The supermarket managers of Nisa retail store prepare budgets in

order to utilize them in monitoring the current cost incurred in the business in order to

gain competitive advantage over its variety of competitors. The costs can be controlled in

order to operate their business operations in improving the business entity. All the

products of Nisa retail store are compare with the other products of its competitors in

order to determine their costs by adding higher percentages of profit in each and every

price of products. The focus of the finance manager is on setting targets in the business in

accomplishing all the performance targets in accordance with the aims and targets framed

by an enterprise by analysing the current resources (Nguyen, Mia, Winata and Chong,

2017). The results will be compared by an entity in relation to the current resources

applied by them in generating higher amount of sales and the revenue. The performance

18

Closing inventory £1,585.71

Variable selling 600

Contribution £7,714.29

Less Fixed cost

Fixed manufacturing 2000

Fixed Admin and selling 700

Fixed selling 600

Net profit £4,414.29

Marginal costing- The profit produces by the firm under this technique is less than compared to

the profit generated by the firm using absorption costing. Fixed cost is the major factor which

created changes in the profit as in absorption costing fixed cost is taken as production costs and

in marginal it is treated as period which is excluded in total from the contribution.

TASK 3

P4 Explain advantages and disadvantages of different types of planning tools for budgetary

control

Budgetary control- The supermarket managers of Nisa retail store prepare budgets in

order to utilize them in monitoring the current cost incurred in the business in order to

gain competitive advantage over its variety of competitors. The costs can be controlled in

order to operate their business operations in improving the business entity. All the

products of Nisa retail store are compare with the other products of its competitors in

order to determine their costs by adding higher percentages of profit in each and every

price of products. The focus of the finance manager is on setting targets in the business in

accomplishing all the performance targets in accordance with the aims and targets framed

by an enterprise by analysing the current resources (Nguyen, Mia, Winata and Chong,

2017). The results will be compared by an entity in relation to the current resources

applied by them in generating higher amount of sales and the revenue. The performance

18

adjustment measures will be taken by an entity in accessing external market opportunities

as this would help in improving their skills and the capabilities.

Coordination- Discipline is essential factor in an organisation as this would help an

entity in order to improve their working conditions. There are different departments in an

entity whose major objective is to gain competitive advantage over its variety of

customers. Budgets are prepared in order to segregate different tasks and duties among

various departments. It is essential for the business in order to use custodian of

responsibilities in which duty of one employee will be checked by other employee in

absence of them. The primary motive of this entity is to improve the efficiency of the

business in relation to its outcome generated by them.

Communication- Budgeting is regarded as one of the important source of

communication as it conveys important financial information from one end too another.

Lower departments generally prepared various budgets like sales, purchases, expenses

and capital budget in order to convey the information to the top management. The

adverse results will be rectified by the top management by making important decisions as

their primary motive is to improve their efficiency in terms of all the deficiencies of an

entity. The external market challenges impose on the firm will be improved with the

passage of time. Email is used as important source of communication among all the

employees in a supermarket of Nisa store related to the daily responsibilities.

Resource allocation- It can be also said that budgets prepared by an enterprise is used as

important method in allocating all the resources in the business. Sales budgets prepared

by an entity in which units produces by the business are recorded in the budgets

(Horngren and et.al., 2015). This sales budget will be helpful for an entity in order to

make important decisions regarding allocating financial or human resources properly

handling the departments of sales in an enterprise. The efficiency of all the departments

will be improved due to proper allocation of resources in order to generate higher amount

of sales and the revenue.

Disadvantages

Lack of participation- in an organisation there are three stages of management such as

top, middle and bottom management level in the business. Budgets prepared by lower

19

as this would help in improving their skills and the capabilities.

Coordination- Discipline is essential factor in an organisation as this would help an

entity in order to improve their working conditions. There are different departments in an

entity whose major objective is to gain competitive advantage over its variety of

customers. Budgets are prepared in order to segregate different tasks and duties among

various departments. It is essential for the business in order to use custodian of

responsibilities in which duty of one employee will be checked by other employee in

absence of them. The primary motive of this entity is to improve the efficiency of the

business in relation to its outcome generated by them.

Communication- Budgeting is regarded as one of the important source of

communication as it conveys important financial information from one end too another.

Lower departments generally prepared various budgets like sales, purchases, expenses

and capital budget in order to convey the information to the top management. The

adverse results will be rectified by the top management by making important decisions as

their primary motive is to improve their efficiency in terms of all the deficiencies of an

entity. The external market challenges impose on the firm will be improved with the

passage of time. Email is used as important source of communication among all the

employees in a supermarket of Nisa store related to the daily responsibilities.

Resource allocation- It can be also said that budgets prepared by an enterprise is used as

important method in allocating all the resources in the business. Sales budgets prepared

by an entity in which units produces by the business are recorded in the budgets

(Horngren and et.al., 2015). This sales budget will be helpful for an entity in order to

make important decisions regarding allocating financial or human resources properly

handling the departments of sales in an enterprise. The efficiency of all the departments

will be improved due to proper allocation of resources in order to generate higher amount

of sales and the revenue.

Disadvantages

Lack of participation- in an organisation there are three stages of management such as

top, middle and bottom management level in the business. Budgets prepared by lower

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

management level will further supply to the top management who will approve it in

order to execute in the business enterprise. While preparing budgets if there is lack of

participation among different departments that restricts the performance of

accomplishing various gaols and the objectives. Objectives are essential in order to

complete within the prescribed time period as it is important in order to make important

decisions in the business.

Creates competition- The rules and regulations prepared by an entity in order to

increase their business efficiency as their primary motive is to comply all the policies.

The legislations and internal code of conduct prepared by an entity owner will in turn

creates lots of competition in the internal environment. Employees working in the

business will try to pull each other working in the same firm in order to remain ahead in

the race of top employees. Employees working in the business needs to improve their

efficiencies as their wrong action will ruin the current performance of an entity.

P5 Compare how an entity adopt management accounting systems in order to deal with the

financial problems

Management accounting is vast topic in which various tools and techniques will be

adopted by an individual in order to improve their business. Several techniques will be adopted

by an entity owner in reducing their weaknesses as their primary motive is to reduce all kinds of

expenses incurred in the business in relation to the income earned by them in a particular year

(Tucker and Parker, 2014). There are various ways which helps in improving the business

performance of an entity is given as follows:

Financial information can be gathered by using ratio analysis that helps in comparing the

performance of an entity of current year with its previous years.

Cost accounting related information can be gather from preparing marginal or absorption

costing systems as their primary motive is to ascertain the cost of a product or service.

CONCLUSION

It can be concluded from thee above assignment that management accounting principles

will be helpful for an enterprise in gaining higher market opportunities in minimising all kinds of

deficiencies currently lies in the external market. The focus of this entity lies on applying

marginal and absorption costing system in improving the business enterprise. The best suitable

20

order to execute in the business enterprise. While preparing budgets if there is lack of

participation among different departments that restricts the performance of

accomplishing various gaols and the objectives. Objectives are essential in order to

complete within the prescribed time period as it is important in order to make important

decisions in the business.

Creates competition- The rules and regulations prepared by an entity in order to

increase their business efficiency as their primary motive is to comply all the policies.

The legislations and internal code of conduct prepared by an entity owner will in turn

creates lots of competition in the internal environment. Employees working in the

business will try to pull each other working in the same firm in order to remain ahead in

the race of top employees. Employees working in the business needs to improve their

efficiencies as their wrong action will ruin the current performance of an entity.

P5 Compare how an entity adopt management accounting systems in order to deal with the

financial problems

Management accounting is vast topic in which various tools and techniques will be

adopted by an individual in order to improve their business. Several techniques will be adopted

by an entity owner in reducing their weaknesses as their primary motive is to reduce all kinds of

expenses incurred in the business in relation to the income earned by them in a particular year

(Tucker and Parker, 2014). There are various ways which helps in improving the business

performance of an entity is given as follows:

Financial information can be gathered by using ratio analysis that helps in comparing the

performance of an entity of current year with its previous years.

Cost accounting related information can be gather from preparing marginal or absorption

costing systems as their primary motive is to ascertain the cost of a product or service.

CONCLUSION

It can be concluded from thee above assignment that management accounting principles

will be helpful for an enterprise in gaining higher market opportunities in minimising all kinds of

deficiencies currently lies in the external market. The focus of this entity lies on applying

marginal and absorption costing system in improving the business enterprise. The best suitable

20

approach out of these two is absorption as this generated higher amount of net profit as compared

to the profit generated by the marginal costing systems.

21

to the profit generated by the marginal costing systems.

21

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.