Detailed Analysis of XLG Company: Management Accounting Report

VerifiedAdded on 2023/01/09

|12

|3134

|71

Report

AI Summary

This report provides a detailed analysis of XLG Company's financial performance using management accounting principles. The report begins with an introduction to management accounting and its significance in business decision-making. Part A focuses on variance analysis, including sales price variance, sales volume contribution variance, material price planning variance, and material price operational variance, providing calculations and interpretations based on the case study. A critical analysis of the merits and demerits of using variances in assessing managerial performance is also included. Part B examines the competitive advantage of Fama Q for XLG, the impact of increased demand for chemicals X and Y, and the implications of production costs and delivery times. The report concludes by summarizing the key findings and offering recommendations for XLG Company. References are provided to support the analysis.

MANAGEMENT ACCOUNTING - REPORT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Sales price variance and sales volume contribution variance..................................................1

2. Material price planning variance and material price operational variance..............................2

3. Critically analysing key merits and demerits in relation to use of variances in assessing

manager’s performance:..............................................................................................................4

PART B...........................................................................................................................................7

1. FamaQ gives XLG competitive advantage..............................................................................7

2. Demand for chemical X and Y has increased by 45% which is likely to continue according

to market research........................................................................................................................7

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days................................................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

PART A...........................................................................................................................................1

1. Sales price variance and sales volume contribution variance..................................................1

2. Material price planning variance and material price operational variance..............................2

3. Critically analysing key merits and demerits in relation to use of variances in assessing

manager’s performance:..............................................................................................................4

PART B...........................................................................................................................................7

1. FamaQ gives XLG competitive advantage..............................................................................7

2. Demand for chemical X and Y has increased by 45% which is likely to continue according

to market research........................................................................................................................7

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days................................................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

In continuous changing business settings every corporation is facing issue related to making

decisions and manage business in effective manner. Management Accounting is first choice of

managing personnel to deal with such issue as this is wider aspect which offers multiple

techniques and tools to support managerial decision-making framework. The study covers the

major aspects of managerial accounting that necessary to evaluate for business's sustainable

success (Otley, 2016). The entire study consists of 2 parts: A and B. The first part covers

practical sum related to computation of multiple variances based on the case study of XLG

Company. It also covers detailed evaluation about merits and limitations of applying variances in

the assessing managing personnel performance. While the another part covers risk may arise by

making import Farma Q as well as how this may impact XLG Company during lock-down based

on the provided case study.

PART A

1. Sales price variance and sales volume contribution variance

Given Information:

Total units sold: 1600

Material price variance: £ 27000 F

Sales and Contribution:

Chemical X Chemical Y

budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

Standard margin £ 25 £ 20

1

In continuous changing business settings every corporation is facing issue related to making

decisions and manage business in effective manner. Management Accounting is first choice of

managing personnel to deal with such issue as this is wider aspect which offers multiple

techniques and tools to support managerial decision-making framework. The study covers the

major aspects of managerial accounting that necessary to evaluate for business's sustainable

success (Otley, 2016). The entire study consists of 2 parts: A and B. The first part covers

practical sum related to computation of multiple variances based on the case study of XLG

Company. It also covers detailed evaluation about merits and limitations of applying variances in

the assessing managing personnel performance. While the another part covers risk may arise by

making import Farma Q as well as how this may impact XLG Company during lock-down based

on the provided case study.

PART A

1. Sales price variance and sales volume contribution variance

Given Information:

Total units sold: 1600

Material price variance: £ 27000 F

Sales and Contribution:

Chemical X Chemical Y

budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

Standard margin £ 25 £ 20

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

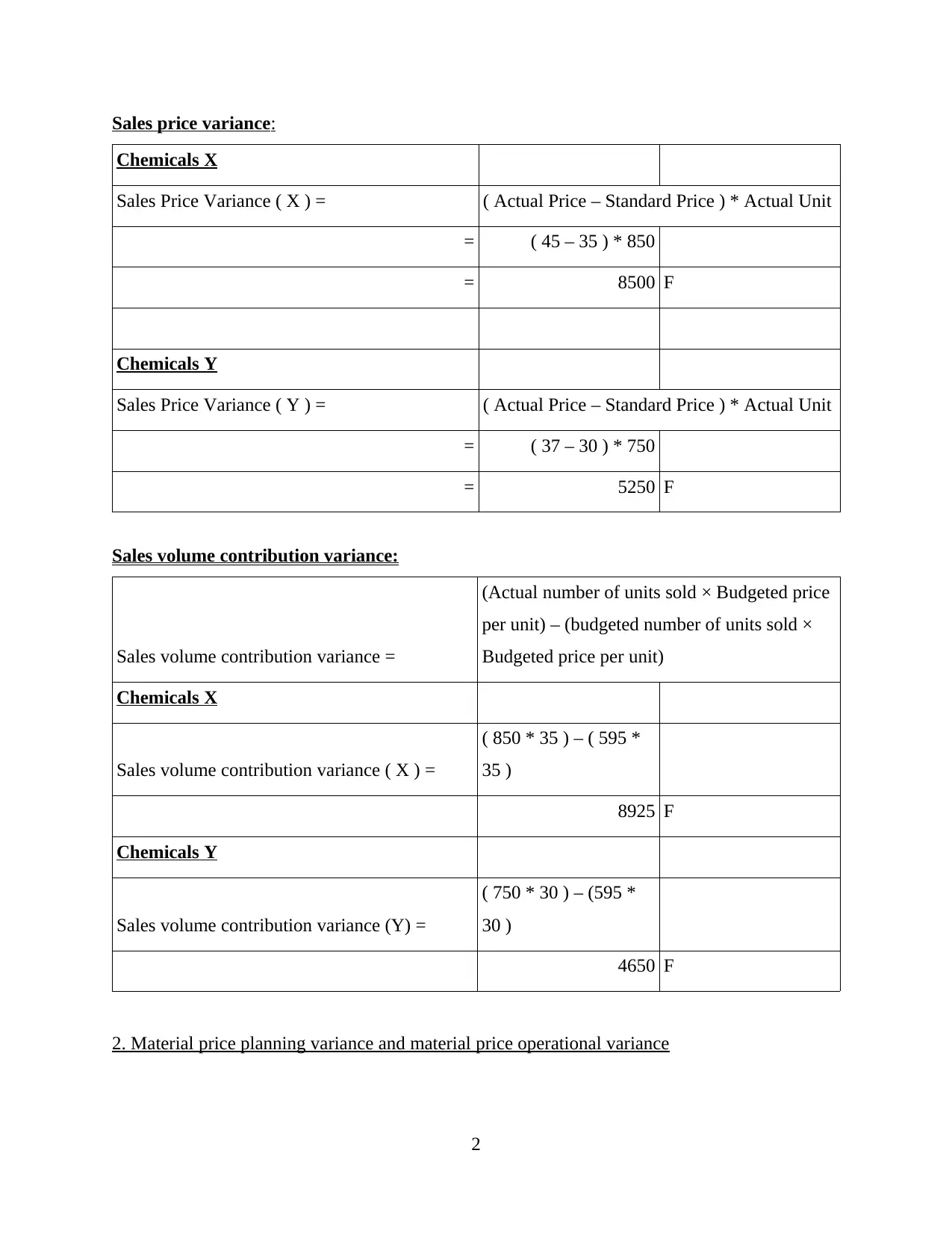

Sales price variance:

Chemicals X

Sales Price Variance ( X ) = ( Actual Price – Standard Price ) * Actual Unit

= ( 45 – 35 ) * 850

= 8500 F

Chemicals Y

Sales Price Variance ( Y ) = ( Actual Price – Standard Price ) * Actual Unit

= ( 37 – 30 ) * 750

= 5250 F

Sales volume contribution variance:

Sales volume contribution variance =

(Actual number of units sold × Budgeted price

per unit) – (budgeted number of units sold ×

Budgeted price per unit)

Chemicals X

Sales volume contribution variance ( X ) =

( 850 * 35 ) – ( 595 *

35 )

8925 F

Chemicals Y

Sales volume contribution variance (Y) =

( 750 * 30 ) – (595 *

30 )

4650 F

2. Material price planning variance and material price operational variance

2

Chemicals X

Sales Price Variance ( X ) = ( Actual Price – Standard Price ) * Actual Unit

= ( 45 – 35 ) * 850

= 8500 F

Chemicals Y

Sales Price Variance ( Y ) = ( Actual Price – Standard Price ) * Actual Unit

= ( 37 – 30 ) * 750

= 5250 F

Sales volume contribution variance:

Sales volume contribution variance =

(Actual number of units sold × Budgeted price

per unit) – (budgeted number of units sold ×

Budgeted price per unit)

Chemicals X

Sales volume contribution variance ( X ) =

( 850 * 35 ) – ( 595 *

35 )

8925 F

Chemicals Y

Sales volume contribution variance (Y) =

( 750 * 30 ) – (595 *

30 )

4650 F

2. Material price planning variance and material price operational variance

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

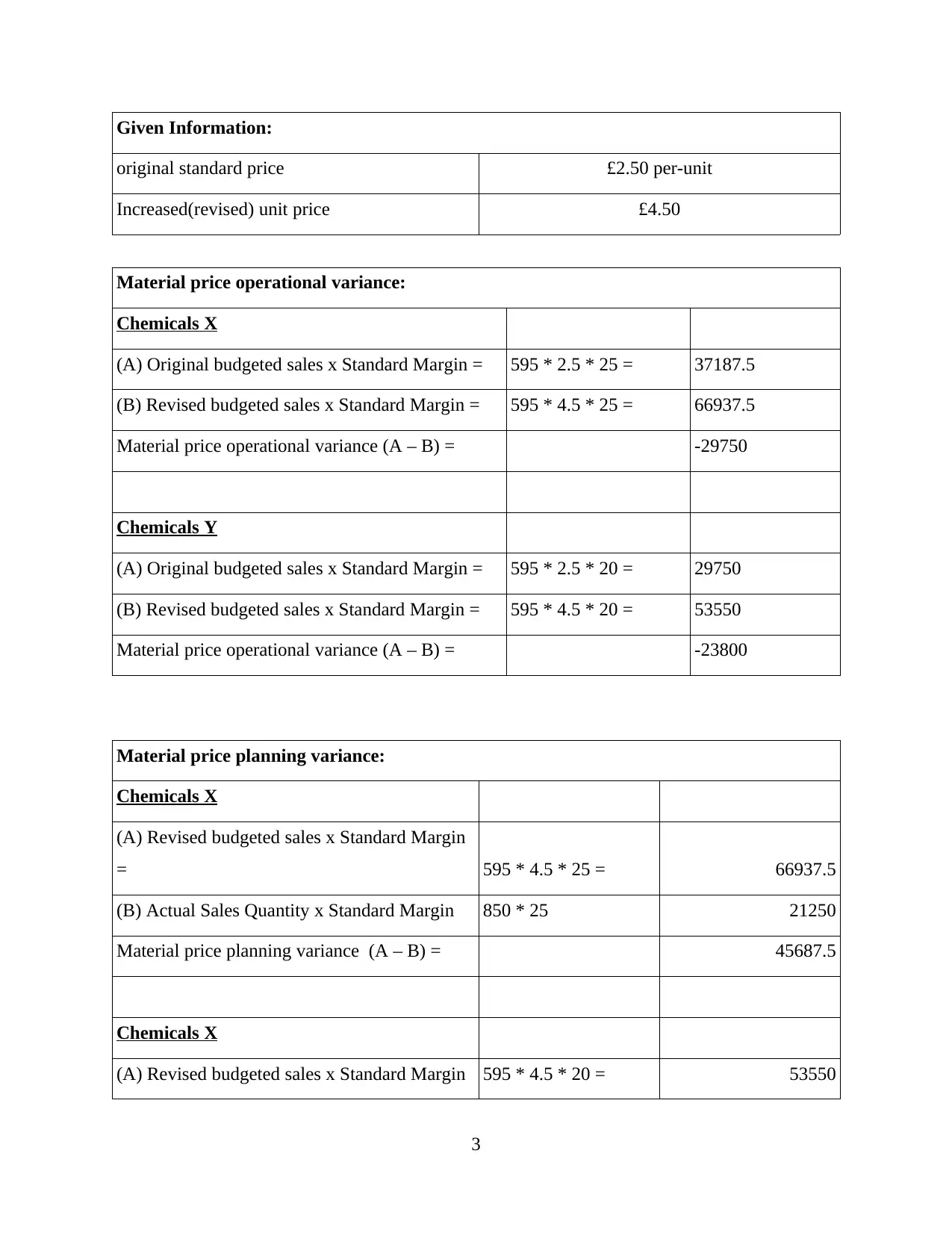

Given Information:

original standard price £2.50 per-unit

Increased(revised) unit price £4.50

Material price operational variance:

Chemicals X

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 25 = 37187.5

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 25 = 66937.5

Material price operational variance (A – B) = -29750

Chemicals Y

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 20 = 29750

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 20 = 53550

Material price operational variance (A – B) = -23800

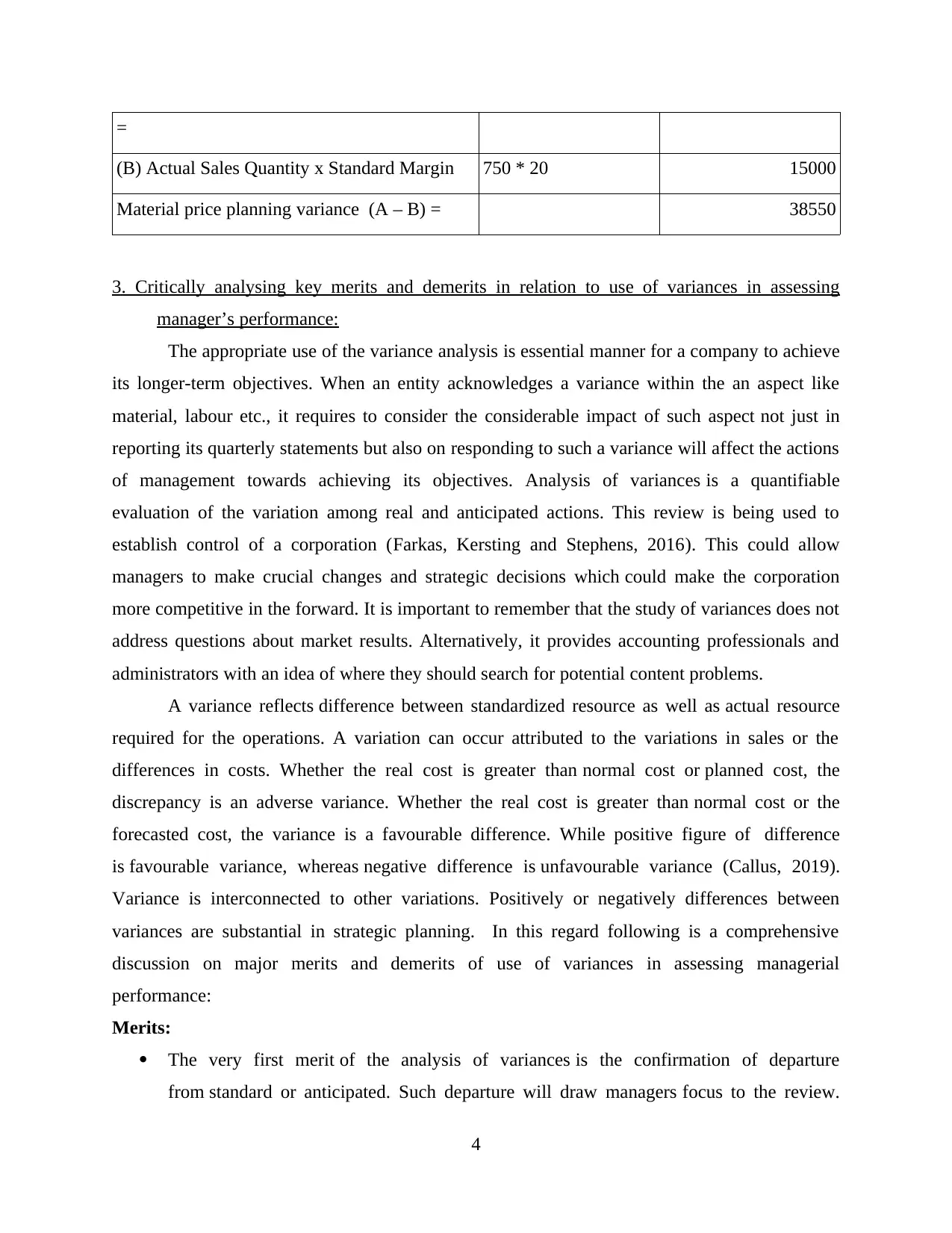

Material price planning variance:

Chemicals X

(A) Revised budgeted sales x Standard Margin

= 595 * 4.5 * 25 = 66937.5

(B) Actual Sales Quantity x Standard Margin 850 * 25 21250

Material price planning variance (A – B) = 45687.5

Chemicals X

(A) Revised budgeted sales x Standard Margin 595 * 4.5 * 20 = 53550

3

original standard price £2.50 per-unit

Increased(revised) unit price £4.50

Material price operational variance:

Chemicals X

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 25 = 37187.5

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 25 = 66937.5

Material price operational variance (A – B) = -29750

Chemicals Y

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 20 = 29750

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 20 = 53550

Material price operational variance (A – B) = -23800

Material price planning variance:

Chemicals X

(A) Revised budgeted sales x Standard Margin

= 595 * 4.5 * 25 = 66937.5

(B) Actual Sales Quantity x Standard Margin 850 * 25 21250

Material price planning variance (A – B) = 45687.5

Chemicals X

(A) Revised budgeted sales x Standard Margin 595 * 4.5 * 20 = 53550

3

=

(B) Actual Sales Quantity x Standard Margin 750 * 20 15000

Material price planning variance (A – B) = 38550

3. Critically analysing key merits and demerits in relation to use of variances in assessing

manager’s performance:

The appropriate use of the variance analysis is essential manner for a company to achieve

its longer-term objectives. When an entity acknowledges a variance within the an aspect like

material, labour etc., it requires to consider the considerable impact of such aspect not just in

reporting its quarterly statements but also on responding to such a variance will affect the actions

of management towards achieving its objectives. Analysis of variances is a quantifiable

evaluation of the variation among real and anticipated actions. This review is being used to

establish control of a corporation (Farkas, Kersting and Stephens, 2016). This could allow

managers to make crucial changes and strategic decisions which could make the corporation

more competitive in the forward. It is important to remember that the study of variances does not

address questions about market results. Alternatively, it provides accounting professionals and

administrators with an idea of where they should search for potential content problems.

A variance reflects difference between standardized resource as well as actual resource

required for the operations. A variation can occur attributed to the variations in sales or the

differences in costs. Whether the real cost is greater than normal cost or planned cost, the

discrepancy is an adverse variance. Whether the real cost is greater than normal cost or the

forecasted cost, the variance is a favourable difference. While positive figure of difference

is favourable variance, whereas negative difference is unfavourable variance (Callus, 2019).

Variance is interconnected to other variations. Positively or negatively differences between

variances are substantial in strategic planning. In this regard following is a comprehensive

discussion on major merits and demerits of use of variances in assessing managerial

performance:

Merits:

The very first merit of the analysis of variances is the confirmation of departure

from standard or anticipated. Such departure will draw managers focus to the review.

4

(B) Actual Sales Quantity x Standard Margin 750 * 20 15000

Material price planning variance (A – B) = 38550

3. Critically analysing key merits and demerits in relation to use of variances in assessing

manager’s performance:

The appropriate use of the variance analysis is essential manner for a company to achieve

its longer-term objectives. When an entity acknowledges a variance within the an aspect like

material, labour etc., it requires to consider the considerable impact of such aspect not just in

reporting its quarterly statements but also on responding to such a variance will affect the actions

of management towards achieving its objectives. Analysis of variances is a quantifiable

evaluation of the variation among real and anticipated actions. This review is being used to

establish control of a corporation (Farkas, Kersting and Stephens, 2016). This could allow

managers to make crucial changes and strategic decisions which could make the corporation

more competitive in the forward. It is important to remember that the study of variances does not

address questions about market results. Alternatively, it provides accounting professionals and

administrators with an idea of where they should search for potential content problems.

A variance reflects difference between standardized resource as well as actual resource

required for the operations. A variation can occur attributed to the variations in sales or the

differences in costs. Whether the real cost is greater than normal cost or planned cost, the

discrepancy is an adverse variance. Whether the real cost is greater than normal cost or the

forecasted cost, the variance is a favourable difference. While positive figure of difference

is favourable variance, whereas negative difference is unfavourable variance (Callus, 2019).

Variance is interconnected to other variations. Positively or negatively differences between

variances are substantial in strategic planning. In this regard following is a comprehensive

discussion on major merits and demerits of use of variances in assessing managerial

performance:

Merits:

The very first merit of the analysis of variances is the confirmation of departure

from standard or anticipated. Such departure will draw managers focus to the review.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management shall be provided with the pertinent facts for such a departure, in particular

for unfavourable variance (cost is above expected).

The second merit of variance will be its importance in the controlling of expenditures.

Managers take reasonable control measures in the event of unfavourable variation. In first

position, justification of an adverse variance is evaluated, where appropriate explanations

are not provided, and adequate control measures are taken.

The third merit in variance or variance analyses is the potential modification in budget

forecasts. if there's no reasonable explanation for variability besides an inaccurate budget

forecast, the budgeted prediction for the potential will be modified or revised.

Fourth merit of variance is to ascertain the efficiency of the managers and, in

particular, controlling manager. positive variance exhibit better performance status of

the manger, while unfavourable variance implies weak performance.

Fifth merit of analysis of variances is the establishment of a framework of duties and

responsibilities within the organisation. The definition of duties and responsibilities

enhances productivity and control mechanisms within the entity (Kumar, 2019).

Computation of variances or review of variances shall create a framework of

transparency within the company. Everybody is answerable for the outcomes of

unfavourable variances (material or labour costs are above expected).

In certain situations, budget vs. real variances can suggest need to reassess the

corporation 's product range or targeted consumer base. There is a lot of conjecture about

readying a budget. When those expectations lead budget to blow-up, that may be

since the underlying estimates are completely incorrect for a number of factors. This may

be as easy as a shift in economy or as complex as problems in bringing goods out to

consumers. The required improvements within the company could be demonstrated

at end of each day (Style, 2020).

It assists the business to achieve its strategic goals and ensure efficacious use

of corporation’s resources. It also aims to build values for its stakeholders.

When variance analysis provides a series of findings that generate broad variances

in report, it may suggest that there have been major problems in way the budgets

are being planned. Issues may contribute to use of incorrect data or information, or there

may be calculation errors in spreadsheet that used plan either a budget or a actual

5

for unfavourable variance (cost is above expected).

The second merit of variance will be its importance in the controlling of expenditures.

Managers take reasonable control measures in the event of unfavourable variation. In first

position, justification of an adverse variance is evaluated, where appropriate explanations

are not provided, and adequate control measures are taken.

The third merit in variance or variance analyses is the potential modification in budget

forecasts. if there's no reasonable explanation for variability besides an inaccurate budget

forecast, the budgeted prediction for the potential will be modified or revised.

Fourth merit of variance is to ascertain the efficiency of the managers and, in

particular, controlling manager. positive variance exhibit better performance status of

the manger, while unfavourable variance implies weak performance.

Fifth merit of analysis of variances is the establishment of a framework of duties and

responsibilities within the organisation. The definition of duties and responsibilities

enhances productivity and control mechanisms within the entity (Kumar, 2019).

Computation of variances or review of variances shall create a framework of

transparency within the company. Everybody is answerable for the outcomes of

unfavourable variances (material or labour costs are above expected).

In certain situations, budget vs. real variances can suggest need to reassess the

corporation 's product range or targeted consumer base. There is a lot of conjecture about

readying a budget. When those expectations lead budget to blow-up, that may be

since the underlying estimates are completely incorrect for a number of factors. This may

be as easy as a shift in economy or as complex as problems in bringing goods out to

consumers. The required improvements within the company could be demonstrated

at end of each day (Style, 2020).

It assists the business to achieve its strategic goals and ensure efficacious use

of corporation’s resources. It also aims to build values for its stakeholders.

When variance analysis provides a series of findings that generate broad variances

in report, it may suggest that there have been major problems in way the budgets

are being planned. Issues may contribute to use of incorrect data or information, or there

may be calculation errors in spreadsheet that used plan either a budget or a actual

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

variance review. In fact, variance assessment is a helpful way to test the corporation's

budgeting system. Through taking effort to enhance the budgeting system, the entity

wants to become much more effective.

Variance analysis is vital monitoring method as it brings emphasis to aspects where real

activity varies from expected operations. Another benefit is that can be beneficial in

finding aspects where resources are not being used effectively and aspects where changes

are needed. Therefore, the study of variance encourages flexibility in management.

Variance analysis may also be utilized to find places where costs overruns and to assess if

the defined standardized cost is appropriate.

Demerits:

Accounting personnel collects variances at ending of each month prior presenting the

outcomes to managers. For most situations, management needs input much quicker, so it

prefers to focus on alarm signs or on-site measures.

Plenty of the factors for variances/variations are not present in accounting reports, so

accounts department have to review and analyse details like labours routing, materials

expenses, and payroll reports to determine the causes for these variances. This add-on

operation is cost-effective unless the managers has been able to successfully address the

issues on the basis of information received.

When budgeting is not carried out on the basis of a thorough review of each variable, the

budgeting procedure may be handled loosely, which would differ from actual figures. In

such case, the analysis of variances may not make any sense (Marzlin Marzuki and

Ismail, 2019).

A variance-analysis has a significant downside in that this takes a longer time to analyse

the impact of the variation and thus the remedial actions may be delayed. The tracking

mechanism leads in a substantial delay in time-frame and thus the introduction of

prevention strategies would be drastically delayed.

6

budgeting system. Through taking effort to enhance the budgeting system, the entity

wants to become much more effective.

Variance analysis is vital monitoring method as it brings emphasis to aspects where real

activity varies from expected operations. Another benefit is that can be beneficial in

finding aspects where resources are not being used effectively and aspects where changes

are needed. Therefore, the study of variance encourages flexibility in management.

Variance analysis may also be utilized to find places where costs overruns and to assess if

the defined standardized cost is appropriate.

Demerits:

Accounting personnel collects variances at ending of each month prior presenting the

outcomes to managers. For most situations, management needs input much quicker, so it

prefers to focus on alarm signs or on-site measures.

Plenty of the factors for variances/variations are not present in accounting reports, so

accounts department have to review and analyse details like labours routing, materials

expenses, and payroll reports to determine the causes for these variances. This add-on

operation is cost-effective unless the managers has been able to successfully address the

issues on the basis of information received.

When budgeting is not carried out on the basis of a thorough review of each variable, the

budgeting procedure may be handled loosely, which would differ from actual figures. In

such case, the analysis of variances may not make any sense (Marzlin Marzuki and

Ismail, 2019).

A variance-analysis has a significant downside in that this takes a longer time to analyse

the impact of the variation and thus the remedial actions may be delayed. The tracking

mechanism leads in a substantial delay in time-frame and thus the introduction of

prevention strategies would be drastically delayed.

6

PART B

1. FamaQ gives XLG competitive advantage

It is true that Fama Q provide comparative advantage to the XLG Company because it is

superior cleaning agent of the business and XLG take patent in order to safe their market leading

position in the UK from its competitors (Azudin and Mansor, 2018). Sales price variance for the

Chemical X is £ 8500 which is in favourable position and for Chemical Y it is £ 5250 which is

also in favour. Sales volume contribution variance of Chemical X and Y is £ 8925 and £ 4650

respectively and both are in favourable condition for the XLG Company. On the other side,

material price operational variance for the Chemical X is adverse that is -£ 29750 and for

Chemical Y is -£ 23800 that is also adverse which means it is not beneficial as well as profitable

for the organizations. In addition, material price planning variance is for Chemical X and Y is £

45687.5 and £ 38550 respectively (Carini, Giacomini and Teodori, 2019). XLG Company should

stop importing from Brazil and also focus on in house production to save their transportation

cost. XLG Company should focus on online sales due to corona virus spread all over the world.

Fama Q provide competitive advantage to the XLG Company but in the lockdown period

price of per unit increases to £ 4.50 and further XLG has to pay £ 3.70 to Fama Q which become

costly for them. Company need to stop importing from Brazil due to high air transport charges

which further increase the selling price of cleaning products. From the values of sales and

material variances, it has been observed that importing material from Brazil by air transform

increase the overall price of each unit.

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to

market research

Demand for Chemical X and Y increases by 45% then company should continue its

production as per the market research where they need to stop importing products from Brazil.

Due to lockdown process in the country and all over the world affect the organization as well as

every member of the country which has to suffer (Qian, Hörisch and Schaltegger, 2018).

Original standards price of ingredient is £ 2.50 per unit but due to this pandemic situation it will

increases unit price £ 4.50 per unit and in result XLG Company has to pay £ 3.70 rate for per unit

to Fama Q. It will minimise the profit margin of the company which is not beneficial because of

air transport of material which generate high cost.

7

1. FamaQ gives XLG competitive advantage

It is true that Fama Q provide comparative advantage to the XLG Company because it is

superior cleaning agent of the business and XLG take patent in order to safe their market leading

position in the UK from its competitors (Azudin and Mansor, 2018). Sales price variance for the

Chemical X is £ 8500 which is in favourable position and for Chemical Y it is £ 5250 which is

also in favour. Sales volume contribution variance of Chemical X and Y is £ 8925 and £ 4650

respectively and both are in favourable condition for the XLG Company. On the other side,

material price operational variance for the Chemical X is adverse that is -£ 29750 and for

Chemical Y is -£ 23800 that is also adverse which means it is not beneficial as well as profitable

for the organizations. In addition, material price planning variance is for Chemical X and Y is £

45687.5 and £ 38550 respectively (Carini, Giacomini and Teodori, 2019). XLG Company should

stop importing from Brazil and also focus on in house production to save their transportation

cost. XLG Company should focus on online sales due to corona virus spread all over the world.

Fama Q provide competitive advantage to the XLG Company but in the lockdown period

price of per unit increases to £ 4.50 and further XLG has to pay £ 3.70 to Fama Q which become

costly for them. Company need to stop importing from Brazil due to high air transport charges

which further increase the selling price of cleaning products. From the values of sales and

material variances, it has been observed that importing material from Brazil by air transform

increase the overall price of each unit.

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to

market research

Demand for Chemical X and Y increases by 45% then company should continue its

production as per the market research where they need to stop importing products from Brazil.

Due to lockdown process in the country and all over the world affect the organization as well as

every member of the country which has to suffer (Qian, Hörisch and Schaltegger, 2018).

Original standards price of ingredient is £ 2.50 per unit but due to this pandemic situation it will

increases unit price £ 4.50 per unit and in result XLG Company has to pay £ 3.70 rate for per unit

to Fama Q. It will minimise the profit margin of the company which is not beneficial because of

air transport of material which generate high cost.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In order to increase their profit margin in this situation, they need to stop importing goods

from Brazil and find its replace or produce itself in the UK to control their cost. Because due to

high transport cost, original produce price increases this can minimise the demand or also

minimise the profit margin for XLG Company.

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days

Making products in the UK minimise the overall cost as well as also reduces the delivery

time which is quite effective and helps in targeting more people. Because people prefer those

brand or company which deliver goods & services at minimum prices. If company get lower cost

through making units of Fama Q in the UK, then they have to continue this process and stop

importing from Brazil until the situation become normal.

Currently XLG Company paid £ 3.70 to Fama Q and if they start making in UK then they

having £ 3 cost per unit which take 15 days less time to deliver products. Fastest delivery option

is comes under the customer satisfaction and their buying experience which improves the brand

image or helps in maximising their demand in the market (Rikhardsson and Yigitbasioglu, 2018).

XLG Company has to shift their focus and start making products in the UK because it minimise

the cost through reducing transport charges and taxes. Importing products from outside UK also

take many working days which can cause to cancel the order from customer’s sides.

After analysing all the aspects and factors which leads to generate more cost and

automatically increase the selling price, managers will identify and make strategic decisions

which they has to follow in respect of company to maintain its profitability as well as demand of

products & services in the market in this pandemic situation.

Lookdown satiations generate huge crises for the world where surviving of the organizations

are quite difficult, people struggle for keeping their job safe and entities for generating revenues.

It is the greatest opportunity for the organization to maintain their profitability in this critical

situation.

CONCLUSION

From the overall discussion it has been observed that changing business environment create

several issues as well as challenges which affect the company’s production and profitability.

Using management accounting concepts, managers are able to make effective strategic decisions

8

from Brazil and find its replace or produce itself in the UK to control their cost. Because due to

high transport cost, original produce price increases this can minimise the demand or also

minimise the profit margin for XLG Company.

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days

Making products in the UK minimise the overall cost as well as also reduces the delivery

time which is quite effective and helps in targeting more people. Because people prefer those

brand or company which deliver goods & services at minimum prices. If company get lower cost

through making units of Fama Q in the UK, then they have to continue this process and stop

importing from Brazil until the situation become normal.

Currently XLG Company paid £ 3.70 to Fama Q and if they start making in UK then they

having £ 3 cost per unit which take 15 days less time to deliver products. Fastest delivery option

is comes under the customer satisfaction and their buying experience which improves the brand

image or helps in maximising their demand in the market (Rikhardsson and Yigitbasioglu, 2018).

XLG Company has to shift their focus and start making products in the UK because it minimise

the cost through reducing transport charges and taxes. Importing products from outside UK also

take many working days which can cause to cancel the order from customer’s sides.

After analysing all the aspects and factors which leads to generate more cost and

automatically increase the selling price, managers will identify and make strategic decisions

which they has to follow in respect of company to maintain its profitability as well as demand of

products & services in the market in this pandemic situation.

Lookdown satiations generate huge crises for the world where surviving of the organizations

are quite difficult, people struggle for keeping their job safe and entities for generating revenues.

It is the greatest opportunity for the organization to maintain their profitability in this critical

situation.

CONCLUSION

From the overall discussion it has been observed that changing business environment create

several issues as well as challenges which affect the company’s production and profitability.

Using management accounting concepts, managers are able to make effective strategic decisions

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as per the current circumstances which entity faces. Through identifying sales and material

variances, managers identify the profitability situations of the business operations and also

measure that which action is in favour of production or not. In the lockdown situations, every

organization get affect but it is better to understand the situations and identify the possible

solutions to recover from such difficult time.

9

variances, managers identify the profitability situations of the business operations and also

measure that which action is in favour of production or not. In the lockdown situations, every

organization get affect but it is better to understand the situations and identify the possible

solutions to recover from such difficult time.

9

REFERENCES

Books & Journals

Azudin, A. and Mansor, N., 2018. Management accounting practices of SMEs: The impact of

organizational DNA, business potential and operational technology. Asia Pacific

Management Review. 23(3). pp.222-226.

Callus, K., 2019. The relevance of standard costing and variance analysis in Maltese

bakeries (Master's thesis, University of Malta).

Carini, C., Giacomini, D. and Teodori, C., 2019. Accounting reform in Italy and perceptions on

the local government consolidated report. International Journal of Public

Administration. 42(3). pp.195-204.

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education, 35,

pp.56-68.

Kumar, A., 2019. Standard Costing and Labour Cost Variance. The Management Accountant

Journal, 54(10), pp.65-73.

Marzlin Marzuki, N.A.R. and Ismail, J., 2019. Benefits and limitations of variance analysis in

management accounting. ACCOUNTING BULLETIN, p.15.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Qian, W., Hörisch, J. and Schaltegger, S., 2018. Environmental management accounting and its

effects on carbon management and disclosure quality. Journal of Cleaner

Production. 174. pp.1608-1619.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Style, A.P.A., 2020. Budgeting, Variance Analysis, and Performance Evaluations SLP 4. Order.

10

Books & Journals

Azudin, A. and Mansor, N., 2018. Management accounting practices of SMEs: The impact of

organizational DNA, business potential and operational technology. Asia Pacific

Management Review. 23(3). pp.222-226.

Callus, K., 2019. The relevance of standard costing and variance analysis in Maltese

bakeries (Master's thesis, University of Malta).

Carini, C., Giacomini, D. and Teodori, C., 2019. Accounting reform in Italy and perceptions on

the local government consolidated report. International Journal of Public

Administration. 42(3). pp.195-204.

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education, 35,

pp.56-68.

Kumar, A., 2019. Standard Costing and Labour Cost Variance. The Management Accountant

Journal, 54(10), pp.65-73.

Marzlin Marzuki, N.A.R. and Ismail, J., 2019. Benefits and limitations of variance analysis in

management accounting. ACCOUNTING BULLETIN, p.15.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Qian, W., Hörisch, J. and Schaltegger, S., 2018. Environmental management accounting and its

effects on carbon management and disclosure quality. Journal of Cleaner

Production. 174. pp.1608-1619.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Style, A.P.A., 2020. Budgeting, Variance Analysis, and Performance Evaluations SLP 4. Order.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.