Detailed Management Accounting Report for Imda Tech

VerifiedAdded on 2019/12/18

|18

|5800

|232

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application to Imda Tech, a company dealing in mobile chargers and electronic gadgets. It begins by defining management accounting and differentiating it from financial accounting, emphasizing its importance in decision-making and resource allocation. The report delves into various types of management accounting systems, including cost accounting, standard costing, normal costing, actual costing, and inventory management systems, highlighting their significance in cost control, pricing, and inventory optimization. The report also explores marginal costing and absorption costing, showcasing their roles in profit calculation and decision-making. Furthermore, it discusses budgeting processes and pricing strategies. Finally, the report touches upon the balance scorecard approach to performance evaluation and provides a conclusion summarizing the key findings. The report aims to offer insights into Imda Tech's financial strategies and operational efficiency.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION..........................................................................................................................3

TASK1.............................................................................................................................................3

A)............................................................................................................................................3

1. Management accounting and its differences financial accounting:....................................3

2.Importance of management accounting:.............................................................................4

B).Types of management accounting system: .......................................................................5

TASK.2............................................................................................................................................7

Income as per absorption and marginal costing:....................................................................7

TASK 3..........................................................................................................................................11

(a) Different types of budget................................................................................................11

(b) Process of preparing Budget...........................................................................................12

(c) Pricing Strategies............................................................................................................12

TASK 4 .........................................................................................................................................13

Balance score card approach................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION..........................................................................................................................3

TASK1.............................................................................................................................................3

A)............................................................................................................................................3

1. Management accounting and its differences financial accounting:....................................3

2.Importance of management accounting:.............................................................................4

B).Types of management accounting system: .......................................................................5

TASK.2............................................................................................................................................7

Income as per absorption and marginal costing:....................................................................7

TASK 3..........................................................................................................................................11

(a) Different types of budget................................................................................................11

(b) Process of preparing Budget...........................................................................................12

(c) Pricing Strategies............................................................................................................12

TASK 4 .........................................................................................................................................13

Balance score card approach................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is the method which is used by the organisations in dealing with

the different types of the cost that gets incurred in the various activities of the firm. Management

accounting is a very essential element of the firm as because it helps in the making of the

decision and it also helps in identifying the financial resources that are required in the operations

of the organisation. With the help of the management accounting system the management team

of the organisation can be able to make several plans as well as strategies so that the operations

of the firm can be carried out in an effective manner (Angelakis,Theriouand Floropoulos,2010).

The issues that are regarding preparing the budgets can also be well planned with the help of it,

and the organisation's performances can also be enhanced with this. The risk factors that are

involved in the various activities of the firm can be very effectively managed in the firm and the

solutions can also be identified with the help of the management accounting systems.

Imda Tech Limited is dealing in the chargers of the mobiles and also in the different

electronic gadgets. The organisation is having the lack of financial resources to carry out its

operation, due to which the whole operation is getting hampered. Therefore the study will help in

understanding the various methods through which the firm can resolve the issues.

TASK1

A).

1. Management accounting and its differences between FA and MA:

Definition of MA:

Management accounting is the process of making reports and accounts which render adequate

and timely financial and statistical information needed by the managers to frame routine and

short term decisions. With the help of management accounting, Imda tech needs to operates their

operations in a better manner so the the objectives of the company can attained. Managerial

accounting is also known as the cost accounting. The main difference between managerial and

financial accounting is managerial accounting information is focused at assisting managers under

the cited firm to frame decisions, while on the other hands, financial accounting is entirely

focused at rendering information to the parties outside the firm.

Definition of FA:

Management accounting is the method which is used by the organisations in dealing with

the different types of the cost that gets incurred in the various activities of the firm. Management

accounting is a very essential element of the firm as because it helps in the making of the

decision and it also helps in identifying the financial resources that are required in the operations

of the organisation. With the help of the management accounting system the management team

of the organisation can be able to make several plans as well as strategies so that the operations

of the firm can be carried out in an effective manner (Angelakis,Theriouand Floropoulos,2010).

The issues that are regarding preparing the budgets can also be well planned with the help of it,

and the organisation's performances can also be enhanced with this. The risk factors that are

involved in the various activities of the firm can be very effectively managed in the firm and the

solutions can also be identified with the help of the management accounting systems.

Imda Tech Limited is dealing in the chargers of the mobiles and also in the different

electronic gadgets. The organisation is having the lack of financial resources to carry out its

operation, due to which the whole operation is getting hampered. Therefore the study will help in

understanding the various methods through which the firm can resolve the issues.

TASK1

A).

1. Management accounting and its differences between FA and MA:

Definition of MA:

Management accounting is the process of making reports and accounts which render adequate

and timely financial and statistical information needed by the managers to frame routine and

short term decisions. With the help of management accounting, Imda tech needs to operates their

operations in a better manner so the the objectives of the company can attained. Managerial

accounting is also known as the cost accounting. The main difference between managerial and

financial accounting is managerial accounting information is focused at assisting managers under

the cited firm to frame decisions, while on the other hands, financial accounting is entirely

focused at rendering information to the parties outside the firm.

Definition of FA:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial accounting is a particular branch of accounting which keeps track of firm's financial

transactions. With the help of standardized guidelines, the finance related translations are

recorded, summarized, and presented in a financial statement.

Difference between MA and FA:

There are basically few differences between management accounting and financial

accounting:

Basis of difference Management Accounting Financial Accounting

Aggregation MA reports at more defined

level.

FA reports on the outcome of

the whole business.

Efficiency It reports on more particularly

on what are the causing issues

and how to fix them.

FA reports on profitability of a

firm.

Proven information It frequently deals with the

forecasting instead of proven

and verifiable facts.

It needs that records to be held

in considerable precision, that

are required to be assured that

the financial statements are

correct.

Standards It does not need to comply any

of the standards while

reporting.

It needs to comply with so

many accounting standards in

order to make the business

sustainable.

2.Importance of management accounting:

Management accounting reports renders data driven inputs to these decisions, that could

enhance decision making. Managers could leverage this strong method to assist in making

business more successful and effective.

Relevant cost Analysis: Management accounting reports aids to the administration of the firm to

identify what are need to sold and how to sell it. For instance, a small entrepreneurs might be not

transactions. With the help of standardized guidelines, the finance related translations are

recorded, summarized, and presented in a financial statement.

Difference between MA and FA:

There are basically few differences between management accounting and financial

accounting:

Basis of difference Management Accounting Financial Accounting

Aggregation MA reports at more defined

level.

FA reports on the outcome of

the whole business.

Efficiency It reports on more particularly

on what are the causing issues

and how to fix them.

FA reports on profitability of a

firm.

Proven information It frequently deals with the

forecasting instead of proven

and verifiable facts.

It needs that records to be held

in considerable precision, that

are required to be assured that

the financial statements are

correct.

Standards It does not need to comply any

of the standards while

reporting.

It needs to comply with so

many accounting standards in

order to make the business

sustainable.

2.Importance of management accounting:

Management accounting reports renders data driven inputs to these decisions, that could

enhance decision making. Managers could leverage this strong method to assist in making

business more successful and effective.

Relevant cost Analysis: Management accounting reports aids to the administration of the firm to

identify what are need to sold and how to sell it. For instance, a small entrepreneurs might be not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sure where they should concentrate his marketing efforts. For assessing this decisions, a manager

from accounts departments, could assess the costs which differ between advertising options for

each product, avoiding common cost. This procedure is called as the relevant cost analysis.

Make or Buy Analysis: The management information aids in making the manufacturing process

effective. For instance, an entrepreneur need to know about whether he needs to produce the item

or purchase from the supplier. The managers of the company needs to asssess the cost for

producing the cost so that they would know about whether there is a need to manufacture or need

to purchase.

B).Types of management accounting system:

Cost accounting systems: A cost accounting is said to be that framework used by the

company in order to determine cost of there product for evaluation of profitability, inventory

analysis and to control the extra cost those are incurred on the expenses.

Standard costing: It is one of the traditional cost accounting system under this cost of the

product is decided on the basis of historical costs (Baldvinsdottir, Mitchell and Nørreklit, 2010).

Normal costing: Under this costing actual prices are used in direct lobar and direct materials,

and only overhead cost are determine. In additional it also shows the various kinds of budgets for

better understanding about capital used by the organization to establish their business for smooth

running. In other words budgets are used for overall description of the amount is going to

invested in the company to acquire more and more profit with the help of appropriate balance

sheet which shows all the expenses incurred by the enterprise. Basically it also includes the

balance score card which is also consider as useful method or technique of management

accounting and job costing method by analysing the particular job of the employees. Under this

actual labour and costs are compared with the standard cost.

Actual costing: It is a method of setting the price of the product on the actual labour and cost

arises for making the product. Cost accounting: This bookkeeping framework is worried with the distinctive cost of the

items. With the assistance of this framework supervisors take different choices in regards

to the fund distribution. Subsequent to dissecting the diverse alternatives accessible with

the chiefs they pick the best reasonable one by contrasting it and the previous year

reports(Zimmerman and Yahya-Zadeh, 2011). Taken a toll bookkeeping likewise help in

keeping control over the distinctive cost of creation by keeping appropriate mind the

from accounts departments, could assess the costs which differ between advertising options for

each product, avoiding common cost. This procedure is called as the relevant cost analysis.

Make or Buy Analysis: The management information aids in making the manufacturing process

effective. For instance, an entrepreneur need to know about whether he needs to produce the item

or purchase from the supplier. The managers of the company needs to asssess the cost for

producing the cost so that they would know about whether there is a need to manufacture or need

to purchase.

B).Types of management accounting system:

Cost accounting systems: A cost accounting is said to be that framework used by the

company in order to determine cost of there product for evaluation of profitability, inventory

analysis and to control the extra cost those are incurred on the expenses.

Standard costing: It is one of the traditional cost accounting system under this cost of the

product is decided on the basis of historical costs (Baldvinsdottir, Mitchell and Nørreklit, 2010).

Normal costing: Under this costing actual prices are used in direct lobar and direct materials,

and only overhead cost are determine. In additional it also shows the various kinds of budgets for

better understanding about capital used by the organization to establish their business for smooth

running. In other words budgets are used for overall description of the amount is going to

invested in the company to acquire more and more profit with the help of appropriate balance

sheet which shows all the expenses incurred by the enterprise. Basically it also includes the

balance score card which is also consider as useful method or technique of management

accounting and job costing method by analysing the particular job of the employees. Under this

actual labour and costs are compared with the standard cost.

Actual costing: It is a method of setting the price of the product on the actual labour and cost

arises for making the product. Cost accounting: This bookkeeping framework is worried with the distinctive cost of the

items. With the assistance of this framework supervisors take different choices in regards

to the fund distribution. Subsequent to dissecting the diverse alternatives accessible with

the chiefs they pick the best reasonable one by contrasting it and the previous year

reports(Zimmerman and Yahya-Zadeh, 2011). Taken a toll bookkeeping likewise help in

keeping control over the distinctive cost of creation by keeping appropriate mind the

diverse components of the generation procedure. With the assistance of this framework

organization can take the choice of future extension too. All these are the useful

techniques used by the enterprises to set the price of the product. Managers of the Imda

tech can use these techniques in order to set the prices for their products and can create

proper revenue for them.

Inventory management systems: Inventory management system is an tool of

management accounting system. Under this enterprises try to manage an optimum level

of inventory in order to minimising the cost or at the same time meeting all the demands

of the customers. stock alludes to the raw material kept in the business which will be

changed over into final products by processed them. It is critical to have great stock

administration framework so that circumstance of non accessibility of crude material can

be maintained a strategic distance from as this will prompt wastage of time and

furthermore loss of potential customers(Lukka and Modell, 2010). It is additionally

critical to stay away from the circumstance of abundance in the association so as to

maintain a strategic distance from the cost of capacity and upkeep which further is added

to the aggregate cost of the item. If an enterprises has its stock in a bulk that it will give

rise to the storage cost which indirectly increases the overall cost of the product. On the

other hand it the enterprise store small number of stock that that enterprise will fail to

meet the demands of the customers and this will hamper the goodwill or image of the

company. Some of the techniques are: EOQ: It is said to be that method used by the

company to keep the record of there stocks. The ideal order quantity of a company that

should related with cost of production and demand rate. LIFO: Under this method of

inventory system which is used by the company in order to make count of that stocks

which are last in and first out.

Job costing systems: it is the another tool of management accounting. Under this

manager of the enterprises study the cost or benefit relate with the each job and managers

of the enterprises give much focuses on the job which are more beneficial for the

enterprise and delete the jobs who are not producing enough revenues for the enterprises

(Bodie, 2013). It is one of the effective tool and this helps in increasing the profit or

organization can take the choice of future extension too. All these are the useful

techniques used by the enterprises to set the price of the product. Managers of the Imda

tech can use these techniques in order to set the prices for their products and can create

proper revenue for them.

Inventory management systems: Inventory management system is an tool of

management accounting system. Under this enterprises try to manage an optimum level

of inventory in order to minimising the cost or at the same time meeting all the demands

of the customers. stock alludes to the raw material kept in the business which will be

changed over into final products by processed them. It is critical to have great stock

administration framework so that circumstance of non accessibility of crude material can

be maintained a strategic distance from as this will prompt wastage of time and

furthermore loss of potential customers(Lukka and Modell, 2010). It is additionally

critical to stay away from the circumstance of abundance in the association so as to

maintain a strategic distance from the cost of capacity and upkeep which further is added

to the aggregate cost of the item. If an enterprises has its stock in a bulk that it will give

rise to the storage cost which indirectly increases the overall cost of the product. On the

other hand it the enterprise store small number of stock that that enterprise will fail to

meet the demands of the customers and this will hamper the goodwill or image of the

company. Some of the techniques are: EOQ: It is said to be that method used by the

company to keep the record of there stocks. The ideal order quantity of a company that

should related with cost of production and demand rate. LIFO: Under this method of

inventory system which is used by the company in order to make count of that stocks

which are last in and first out.

Job costing systems: it is the another tool of management accounting. Under this

manager of the enterprises study the cost or benefit relate with the each job and managers

of the enterprises give much focuses on the job which are more beneficial for the

enterprise and delete the jobs who are not producing enough revenues for the enterprises

(Bodie, 2013). It is one of the effective tool and this helps in increasing the profit or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

generate more revenues for the enterprise. Managers of the Imda tech can use this tool in

order to increase the overall effectiveness of their business operations.

Price optimising systems: This method is used by the enterprises in order to set the prices

for their products. It is harmful for the enterprise to set a low or high price for the product

because this will not create proper revenues for the enterprise on the other hand high

price will not influence the customers to buy the product. So it is very important to set an

optimum price for the product which will give not only helps the enterprises in generating

proper revenues but also give value for mopey to the customers. Some of the price

optimising techniques are:

Initial price optimising works according to the life cycle of products those are related

with grocery stores and other commodities.

Promotional pricing is use to set temporary prices to spur sales of items with long term

durability of a product.

Markdown pricing: It is use to sell short term product life cycle product those are subject

according to current trends.

TASK.2

Income as per absorption and marginal costing:

In order to calculate the net profit for Imda tech. Various techniques can be used. In order

to get the profit amount the company is calculating the net profit with the help of absorption

costing and marginal costing.

Marginal Costing: Marginal costing is the system in which the variable cost is charged against

the goods in order to write off the fixed cost a particular time period. This costing helps in the

decision making process by the mangers(Garrison and et. al.2010) . It is directly related to the

marginal which is effected by change in the total output (manaBurritt,and et. al., 2011). Marginal

cost is the change in the total cost due to a unit increase in the total output. With the help of

marginal costing the change in the total profit due to change in output is also calculated.

order to increase the overall effectiveness of their business operations.

Price optimising systems: This method is used by the enterprises in order to set the prices

for their products. It is harmful for the enterprise to set a low or high price for the product

because this will not create proper revenues for the enterprise on the other hand high

price will not influence the customers to buy the product. So it is very important to set an

optimum price for the product which will give not only helps the enterprises in generating

proper revenues but also give value for mopey to the customers. Some of the price

optimising techniques are:

Initial price optimising works according to the life cycle of products those are related

with grocery stores and other commodities.

Promotional pricing is use to set temporary prices to spur sales of items with long term

durability of a product.

Markdown pricing: It is use to sell short term product life cycle product those are subject

according to current trends.

TASK.2

Income as per absorption and marginal costing:

In order to calculate the net profit for Imda tech. Various techniques can be used. In order

to get the profit amount the company is calculating the net profit with the help of absorption

costing and marginal costing.

Marginal Costing: Marginal costing is the system in which the variable cost is charged against

the goods in order to write off the fixed cost a particular time period. This costing helps in the

decision making process by the mangers(Garrison and et. al.2010) . It is directly related to the

marginal which is effected by change in the total output (manaBurritt,and et. al., 2011). Marginal

cost is the change in the total cost due to a unit increase in the total output. With the help of

marginal costing the change in the total profit due to change in output is also calculated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal costing is a opportunity cost which arise the cost in the other product. it is a

additional cost at a each level that can be evaluated by the next product as well as unit. Basically

it is a variable cost which is charge according to the foxed cost and it is a alternative cost which

can be define the aggregate contribution in the company (Lukka,and Modell,2010). It is a

decision making process which is evaluated by the other cost of the product. It is a total cost of

the all fixed cost which can be arise when production level of the product are increase and it can

be include the additional cost which can help to evaluate the break even analysis. The margin

costing include the different elements that can be define the contribution in the company profit.

Marginal costing is all about emergence of opportunity cost due to the increases in a unit of

production which helps in understanding the accounting systems.

Apart from this marginal costing is the difference in between opportunity or chances

which may arises when there is a change in the quantity of the production due to change in all

the existing factors of the organization. In other words marginal costing is a reformation in total

cost due to the increase or decrease in one unit of output of the production process (Li,and et. al.,

2012) . Management accounting is the term which shows the overall description of numerical

terms with the help various appropriate methods and techniques to get accurate results. In fact

management of a accounting systems really need a specialised and skilled persons to organize

and control overall accounting systems of the organization. Imda tech is a one of the famous

multinational organization whose main motive is to manufacture a charger of mobile phones by

satisfying their domestic as well as foreign clients. Apart from this, this report also covers the

usage of absorption costing by explaining the role of marginal costing in the organization by

describing it in a efficient manner (Macintoshand Quattrone,2010). All the existing

environmental factors are very much influence the marginal costing because of their role in the

business and due to which a cited enterprise run their business effectively and efficiently.

Last but not the least marginal costing also plays a very eminent role in the management

accounting system because of their specific role in the production process. In fact it get affected

due to change in a unit of production.

Absorption Costing:- In the method of absorption costing all the different cost are absorbed in

the cost of the unit produced. Different costs can be direct or indirect(Davies and Crawford,

additional cost at a each level that can be evaluated by the next product as well as unit. Basically

it is a variable cost which is charge according to the foxed cost and it is a alternative cost which

can be define the aggregate contribution in the company (Lukka,and Modell,2010). It is a

decision making process which is evaluated by the other cost of the product. It is a total cost of

the all fixed cost which can be arise when production level of the product are increase and it can

be include the additional cost which can help to evaluate the break even analysis. The margin

costing include the different elements that can be define the contribution in the company profit.

Marginal costing is all about emergence of opportunity cost due to the increases in a unit of

production which helps in understanding the accounting systems.

Apart from this marginal costing is the difference in between opportunity or chances

which may arises when there is a change in the quantity of the production due to change in all

the existing factors of the organization. In other words marginal costing is a reformation in total

cost due to the increase or decrease in one unit of output of the production process (Li,and et. al.,

2012) . Management accounting is the term which shows the overall description of numerical

terms with the help various appropriate methods and techniques to get accurate results. In fact

management of a accounting systems really need a specialised and skilled persons to organize

and control overall accounting systems of the organization. Imda tech is a one of the famous

multinational organization whose main motive is to manufacture a charger of mobile phones by

satisfying their domestic as well as foreign clients. Apart from this, this report also covers the

usage of absorption costing by explaining the role of marginal costing in the organization by

describing it in a efficient manner (Macintoshand Quattrone,2010). All the existing

environmental factors are very much influence the marginal costing because of their role in the

business and due to which a cited enterprise run their business effectively and efficiently.

Last but not the least marginal costing also plays a very eminent role in the management

accounting system because of their specific role in the production process. In fact it get affected

due to change in a unit of production.

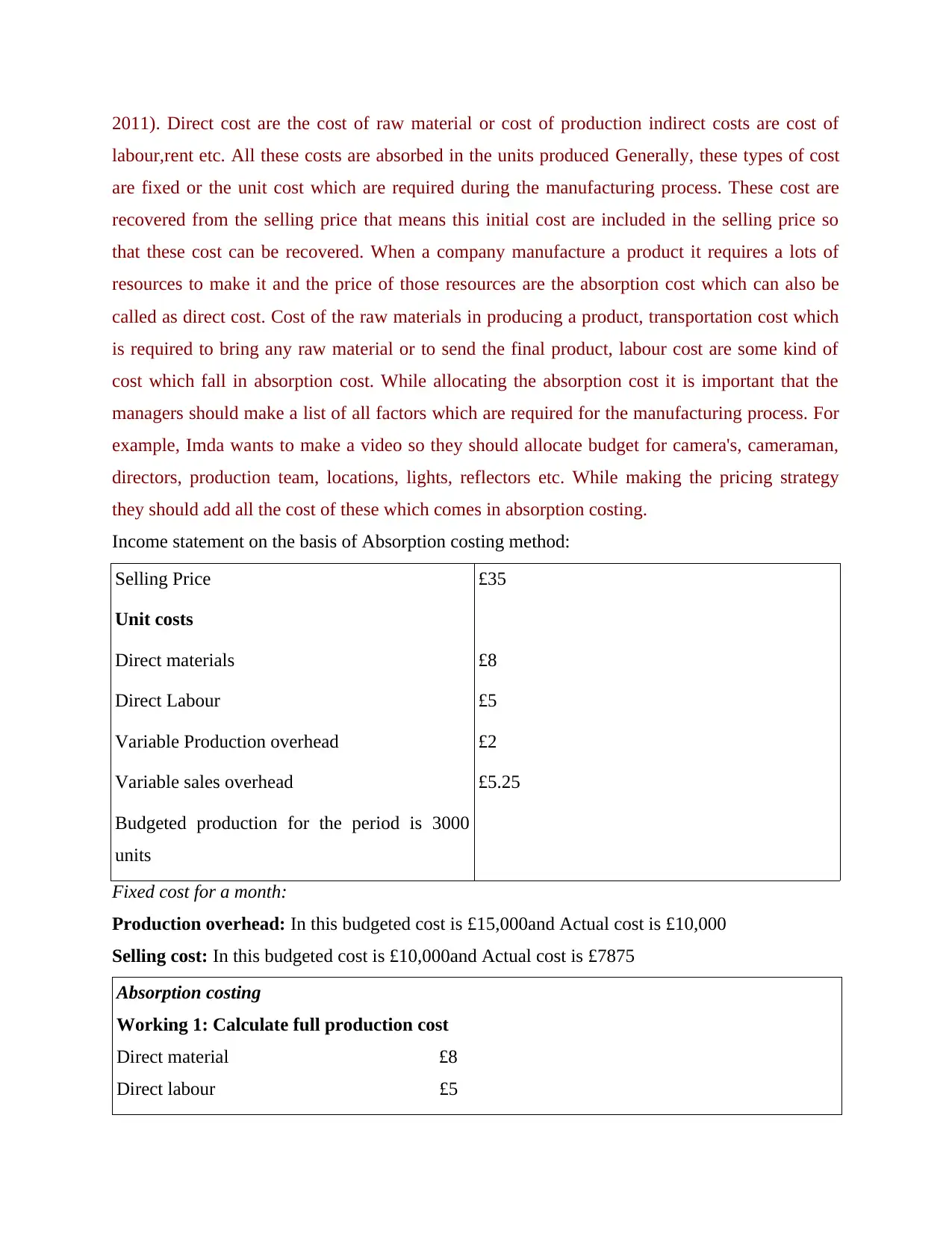

Absorption Costing:- In the method of absorption costing all the different cost are absorbed in

the cost of the unit produced. Different costs can be direct or indirect(Davies and Crawford,

2011). Direct cost are the cost of raw material or cost of production indirect costs are cost of

labour,rent etc. All these costs are absorbed in the units produced Generally, these types of cost

are fixed or the unit cost which are required during the manufacturing process. These cost are

recovered from the selling price that means this initial cost are included in the selling price so

that these cost can be recovered. When a company manufacture a product it requires a lots of

resources to make it and the price of those resources are the absorption cost which can also be

called as direct cost. Cost of the raw materials in producing a product, transportation cost which

is required to bring any raw material or to send the final product, labour cost are some kind of

cost which fall in absorption cost. While allocating the absorption cost it is important that the

managers should make a list of all factors which are required for the manufacturing process. For

example, Imda wants to make a video so they should allocate budget for camera's, cameraman,

directors, production team, locations, lights, reflectors etc. While making the pricing strategy

they should add all the cost of these which comes in absorption costing.

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £8

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing

Working 1: Calculate full production cost

Direct material £8

Direct labour £5

labour,rent etc. All these costs are absorbed in the units produced Generally, these types of cost

are fixed or the unit cost which are required during the manufacturing process. These cost are

recovered from the selling price that means this initial cost are included in the selling price so

that these cost can be recovered. When a company manufacture a product it requires a lots of

resources to make it and the price of those resources are the absorption cost which can also be

called as direct cost. Cost of the raw materials in producing a product, transportation cost which

is required to bring any raw material or to send the final product, labour cost are some kind of

cost which fall in absorption cost. While allocating the absorption cost it is important that the

managers should make a list of all factors which are required for the manufacturing process. For

example, Imda wants to make a video so they should allocate budget for camera's, cameraman,

directors, production team, locations, lights, reflectors etc. While making the pricing strategy

they should add all the cost of these which comes in absorption costing.

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £8

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing

Working 1: Calculate full production cost

Direct material £8

Direct labour £5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

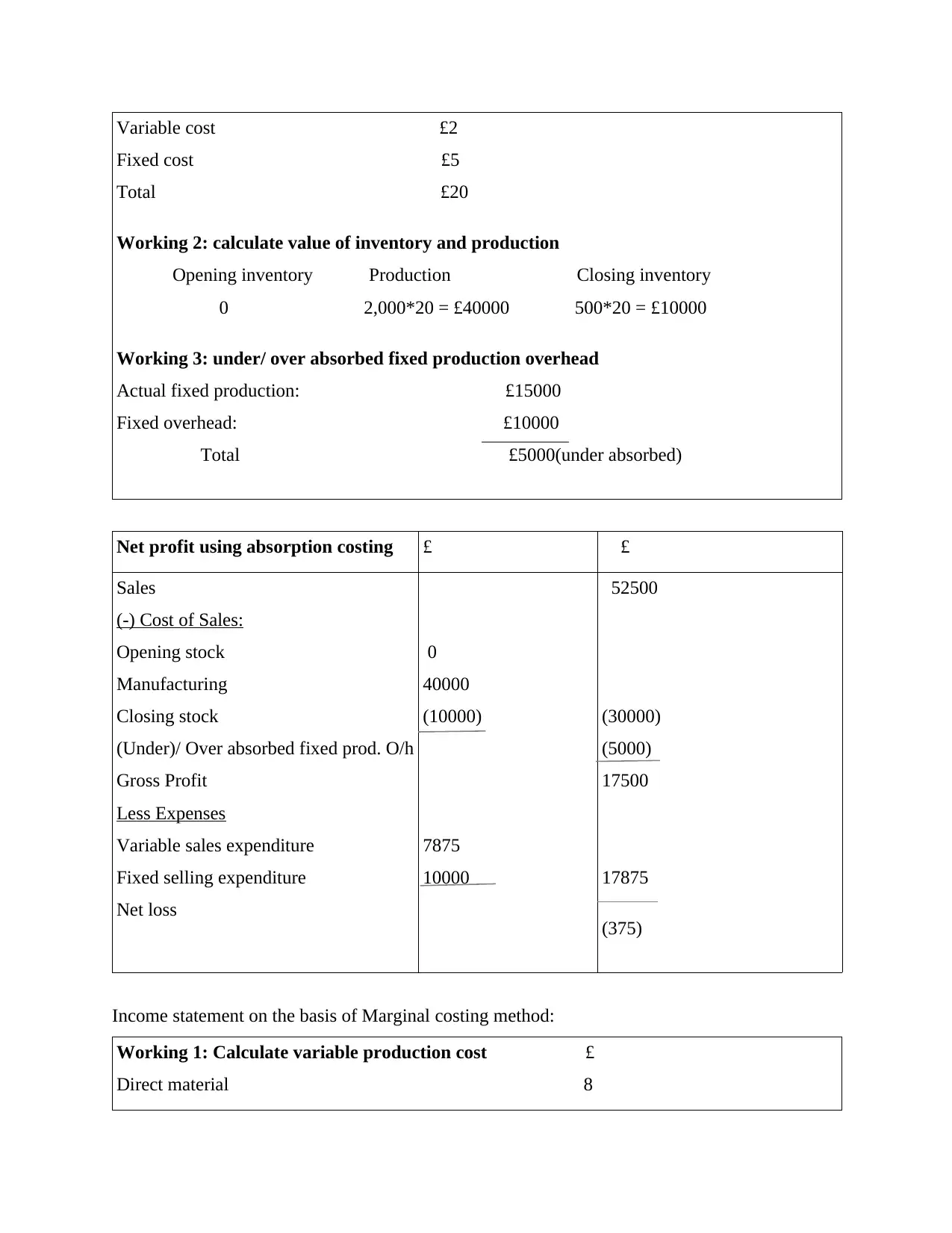

Variable cost £2

Fixed cost £5

Total £20

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375)

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 8

Fixed cost £5

Total £20

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375)

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

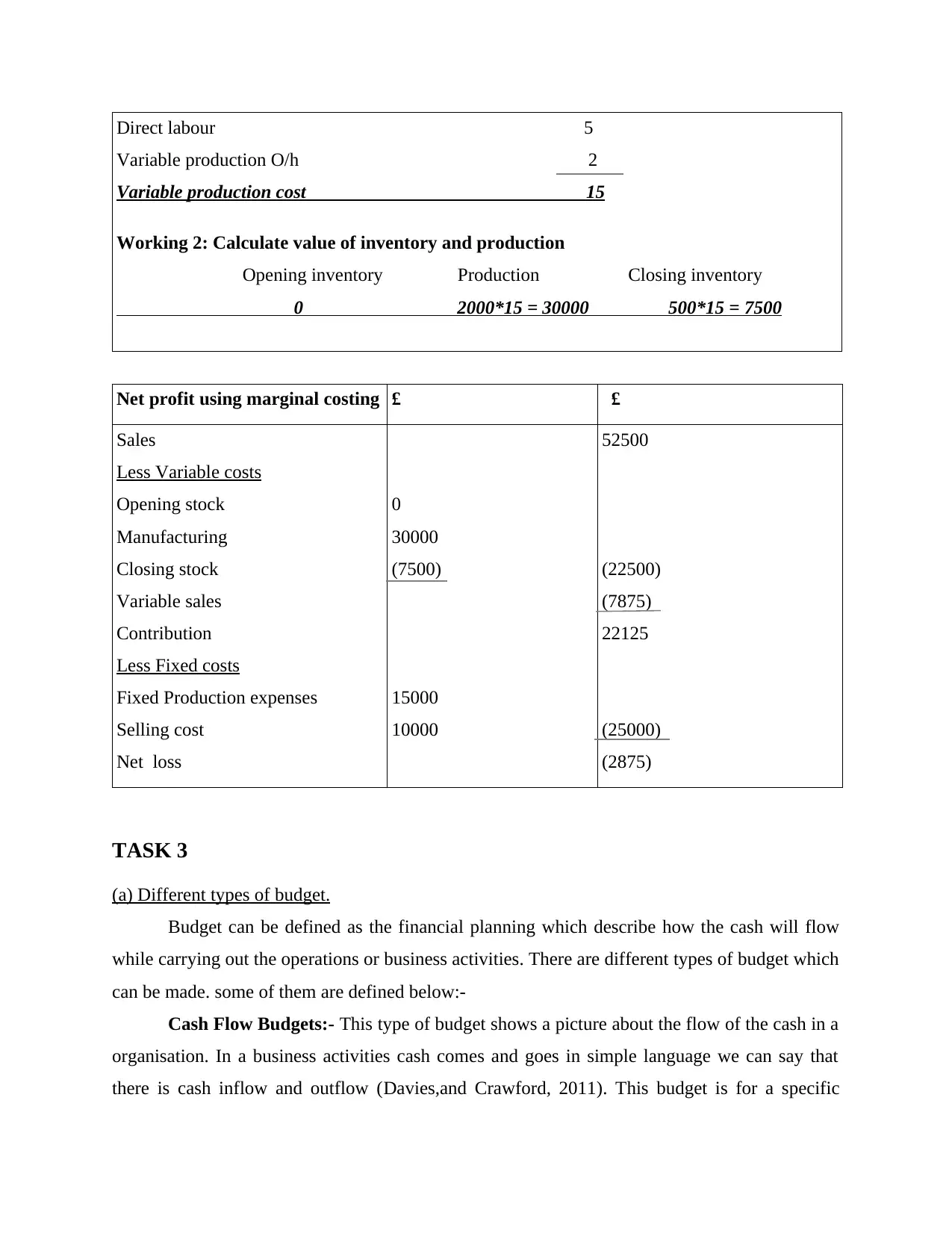

Direct labour 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

TASK 3

(a) Different types of budget.

Budget can be defined as the financial planning which describe how the cash will flow

while carrying out the operations or business activities. There are different types of budget which

can be made. some of them are defined below:-

Cash Flow Budgets:- This type of budget shows a picture about the flow of the cash in a

organisation. In a business activities cash comes and goes in simple language we can say that

there is cash inflow and outflow (Davies,and Crawford, 2011). This budget is for a specific

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

TASK 3

(a) Different types of budget.

Budget can be defined as the financial planning which describe how the cash will flow

while carrying out the operations or business activities. There are different types of budget which

can be made. some of them are defined below:-

Cash Flow Budgets:- This type of budget shows a picture about the flow of the cash in a

organisation. In a business activities cash comes and goes in simple language we can say that

there is cash inflow and outflow (Davies,and Crawford, 2011). This budget is for a specific

period of time and through this a company can get to know its status of the money which are

coming and going in the market which is its advantage. They have the detailed information that

how much money is required for a certain task after projected the resources available to the

company.

Advantages and disadvantages of cash flow budget:

This assist the management to concentrate their focus on an important matters which is

not proceeding as per the plan.

This assists to enhance communication, great understanding and harmonious connection

among the employee. This assist to link the activities of entire department in Imda ltd.

It aids in reducing the cost and profit maximization.

Disadvantages:

It success based on cooperation or operation of staffs.

It's is made on prediction.

It's so much expensive to operate a budget.

It might take higher time to attain.

Financial Budget:- This budget type are responsible for managing the income, expenses

and assets of the company. Allocation of this kind of budget is important because they are cover

almost all the expenditure of the company.

Operating Budget:- This is an assumptions that how much money will be required or

what all expenses will be there for a business task (Garrison,and et. al., 2010). It has various

elements for which budgeting is done that are labour cost, material cost, manufacturing cost and

managing cost. Depending upon the requirement of the company they can be prepared within a

month, week or for a year. They help a company in managing the initial cost or the cost which is

required in manufacturing the product.

Master Budget:- This budget helps a company in analysing the overall performance of

the company because in this all the factors are included which are required in a financial activity.

Factors like sales, operating expenses, assets and income are some which decides the goals and

targets of the company so they should be properly funded.

Static Budget:- Such kind of budget is fixed because these are the factors which is

compulsory for a business activity (DRURY,2013). For example a company is setting up budget

coming and going in the market which is its advantage. They have the detailed information that

how much money is required for a certain task after projected the resources available to the

company.

Advantages and disadvantages of cash flow budget:

This assist the management to concentrate their focus on an important matters which is

not proceeding as per the plan.

This assists to enhance communication, great understanding and harmonious connection

among the employee. This assist to link the activities of entire department in Imda ltd.

It aids in reducing the cost and profit maximization.

Disadvantages:

It success based on cooperation or operation of staffs.

It's is made on prediction.

It's so much expensive to operate a budget.

It might take higher time to attain.

Financial Budget:- This budget type are responsible for managing the income, expenses

and assets of the company. Allocation of this kind of budget is important because they are cover

almost all the expenditure of the company.

Operating Budget:- This is an assumptions that how much money will be required or

what all expenses will be there for a business task (Garrison,and et. al., 2010). It has various

elements for which budgeting is done that are labour cost, material cost, manufacturing cost and

managing cost. Depending upon the requirement of the company they can be prepared within a

month, week or for a year. They help a company in managing the initial cost or the cost which is

required in manufacturing the product.

Master Budget:- This budget helps a company in analysing the overall performance of

the company because in this all the factors are included which are required in a financial activity.

Factors like sales, operating expenses, assets and income are some which decides the goals and

targets of the company so they should be properly funded.

Static Budget:- Such kind of budget is fixed because these are the factors which is

compulsory for a business activity (DRURY,2013). For example a company is setting up budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.