Management Accounting Report: Absorption and Marginal Costing Methods

VerifiedAdded on 2020/01/28

|10

|2370

|49

Report

AI Summary

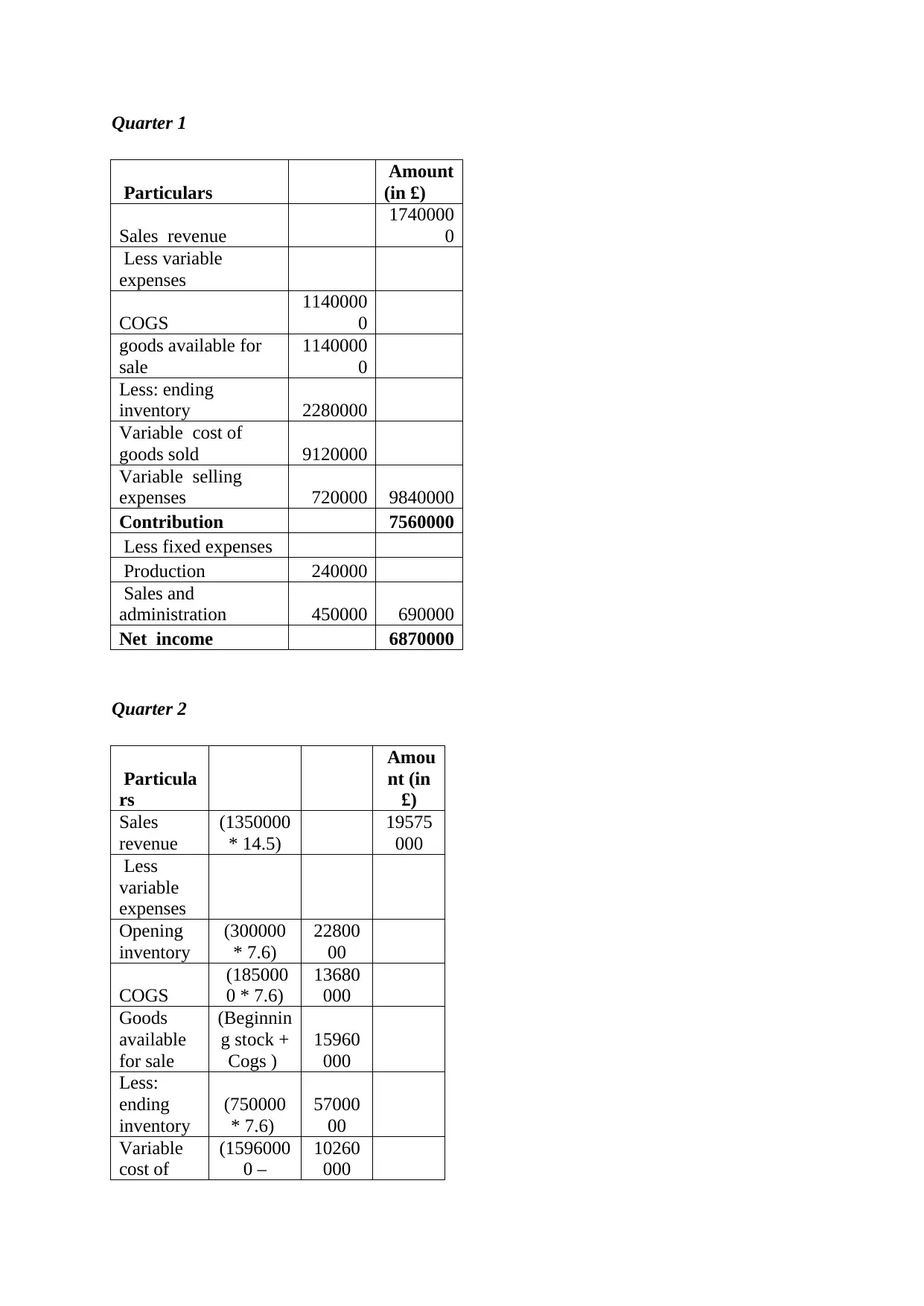

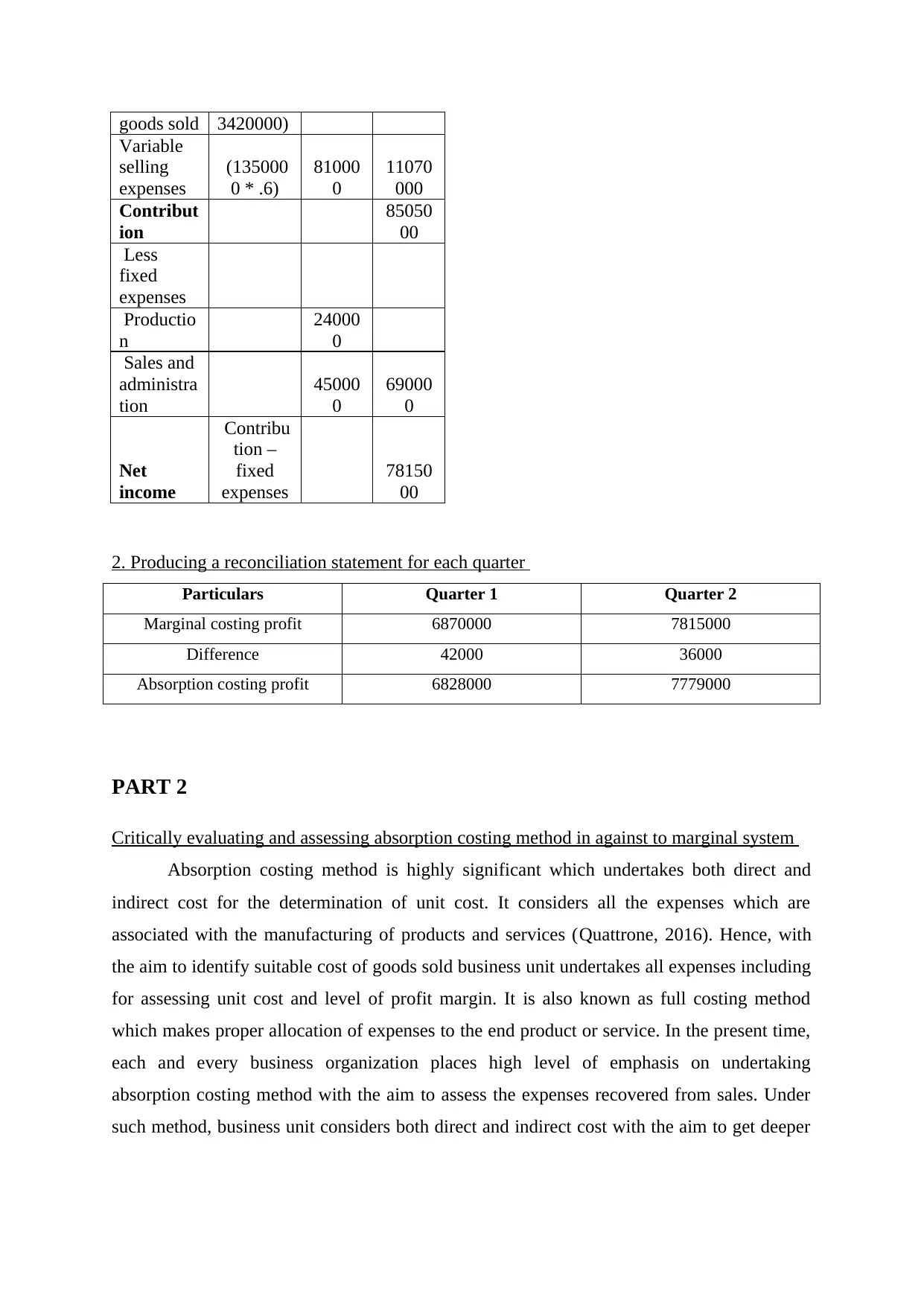

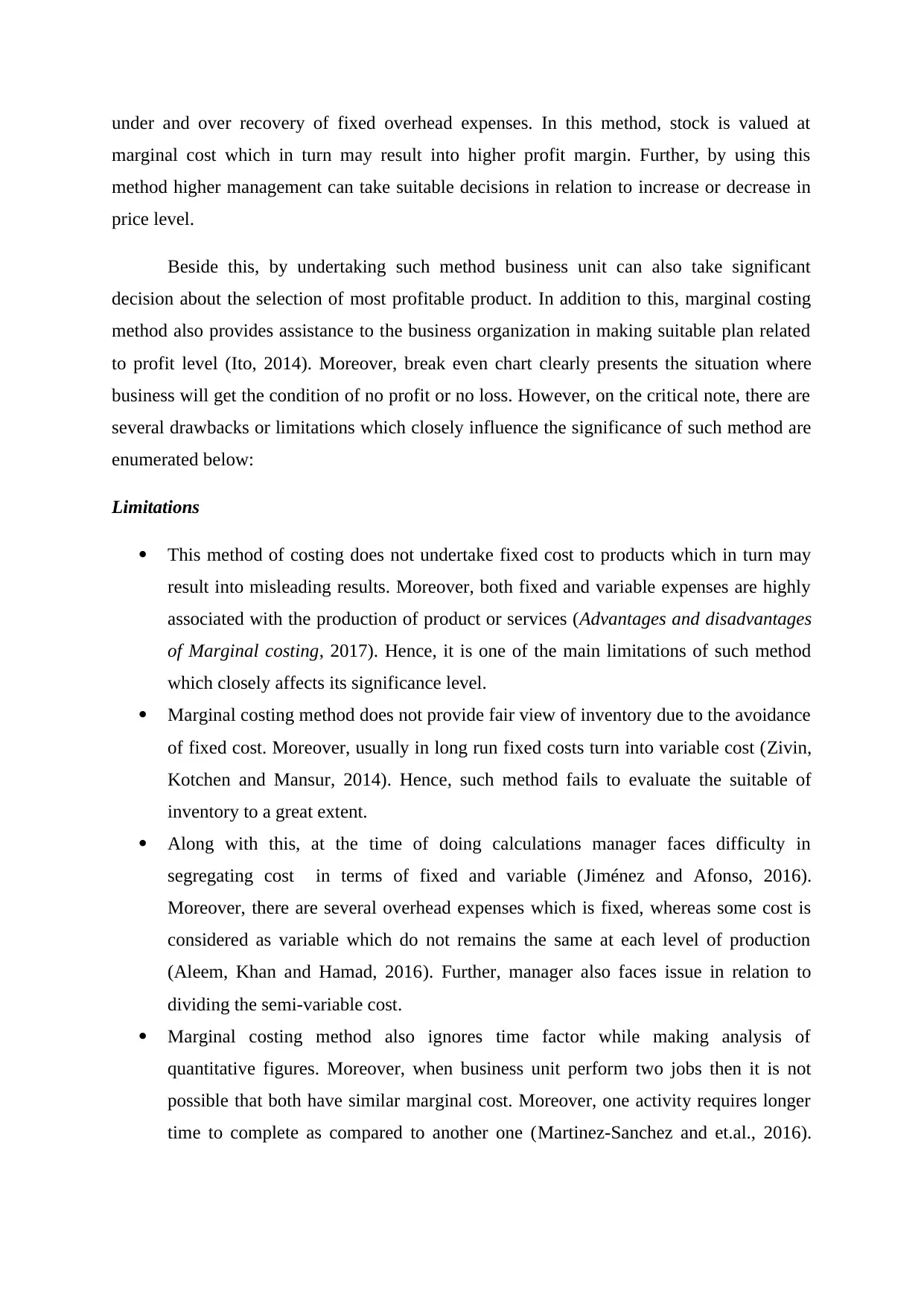

This report delves into the core concepts of management accounting, focusing on the application and comparison of absorption and marginal costing methods. It begins by preparing profit and loss statements using both costing methods for two quarters, followed by the creation of a reconciliation statement for each quarter. The report then critically evaluates and assesses the absorption costing method against the marginal costing system, highlighting their respective advantages and limitations. Absorption costing, which considers both direct and indirect costs, is presented as a method that provides a comprehensive view of profitability and inventory valuation. The report emphasizes its benefits, such as considering fixed costs and providing a fair view of profit margins. Conversely, the report acknowledges the marginal costing system, focusing on variable costs, and discusses its drawbacks, including the potential for misleading results due to the exclusion of fixed costs. The report concludes by summarizing the key differences between the two methods and asserting the superiority of absorption costing for providing reliable information to management and stakeholders, thereby facilitating sound decision-making. The report is supported by a comprehensive list of references to academic journals and online resources.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.