Variance Analysis in Management Accounting

VerifiedAdded on 2023/01/09

|10

|3238

|89

AI Summary

This report provides an insight into variance analysis in management accounting, specifically focusing on sales price variance, sales volume contribution variance, material price planning variance, and material price operational variance. It discusses the benefits and limitations of using variances in analyzing manager performance. The report also includes computations and explanations for each variance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING - REPORT

ACCOUNTING - REPORT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

1. Computation of sales price variance and sales volume contribution variance...................3

2. The material price planning variance and material price operational variance..................5

3. Critically evaluating benefits and limitation of using the variances in analysing the

performance of managers.......................................................................................................7

PART B............................................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

1. Computation of sales price variance and sales volume contribution variance...................3

2. The material price planning variance and material price operational variance..................5

3. Critically evaluating benefits and limitation of using the variances in analysing the

performance of managers.......................................................................................................7

PART B............................................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

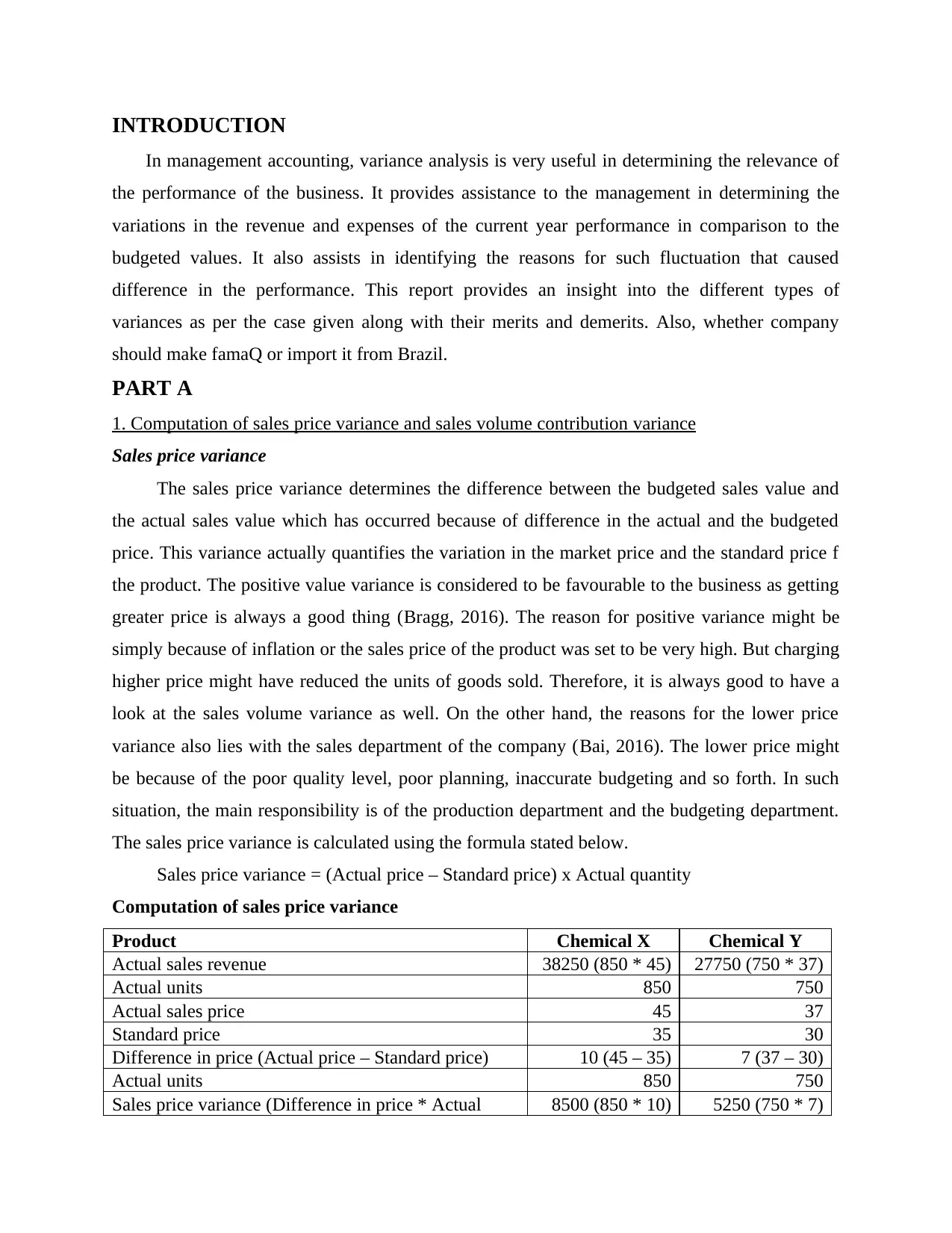

INTRODUCTION

In management accounting, variance analysis is very useful in determining the relevance of

the performance of the business. It provides assistance to the management in determining the

variations in the revenue and expenses of the current year performance in comparison to the

budgeted values. It also assists in identifying the reasons for such fluctuation that caused

difference in the performance. This report provides an insight into the different types of

variances as per the case given along with their merits and demerits. Also, whether company

should make famaQ or import it from Brazil.

PART A

1. Computation of sales price variance and sales volume contribution variance

Sales price variance

The sales price variance determines the difference between the budgeted sales value and

the actual sales value which has occurred because of difference in the actual and the budgeted

price. This variance actually quantifies the variation in the market price and the standard price f

the product. The positive value variance is considered to be favourable to the business as getting

greater price is always a good thing (Bragg, 2016). The reason for positive variance might be

simply because of inflation or the sales price of the product was set to be very high. But charging

higher price might have reduced the units of goods sold. Therefore, it is always good to have a

look at the sales volume variance as well. On the other hand, the reasons for the lower price

variance also lies with the sales department of the company (Bai, 2016). The lower price might

be because of the poor quality level, poor planning, inaccurate budgeting and so forth. In such

situation, the main responsibility is of the production department and the budgeting department.

The sales price variance is calculated using the formula stated below.

Sales price variance = (Actual price – Standard price) x Actual quantity

Computation of sales price variance

Product Chemical X Chemical Y

Actual sales revenue 38250 (850 * 45) 27750 (750 * 37)

Actual units 850 750

Actual sales price 45 37

Standard price 35 30

Difference in price (Actual price – Standard price) 10 (45 – 35) 7 (37 – 30)

Actual units 850 750

Sales price variance (Difference in price * Actual 8500 (850 * 10) 5250 (750 * 7)

In management accounting, variance analysis is very useful in determining the relevance of

the performance of the business. It provides assistance to the management in determining the

variations in the revenue and expenses of the current year performance in comparison to the

budgeted values. It also assists in identifying the reasons for such fluctuation that caused

difference in the performance. This report provides an insight into the different types of

variances as per the case given along with their merits and demerits. Also, whether company

should make famaQ or import it from Brazil.

PART A

1. Computation of sales price variance and sales volume contribution variance

Sales price variance

The sales price variance determines the difference between the budgeted sales value and

the actual sales value which has occurred because of difference in the actual and the budgeted

price. This variance actually quantifies the variation in the market price and the standard price f

the product. The positive value variance is considered to be favourable to the business as getting

greater price is always a good thing (Bragg, 2016). The reason for positive variance might be

simply because of inflation or the sales price of the product was set to be very high. But charging

higher price might have reduced the units of goods sold. Therefore, it is always good to have a

look at the sales volume variance as well. On the other hand, the reasons for the lower price

variance also lies with the sales department of the company (Bai, 2016). The lower price might

be because of the poor quality level, poor planning, inaccurate budgeting and so forth. In such

situation, the main responsibility is of the production department and the budgeting department.

The sales price variance is calculated using the formula stated below.

Sales price variance = (Actual price – Standard price) x Actual quantity

Computation of sales price variance

Product Chemical X Chemical Y

Actual sales revenue 38250 (850 * 45) 27750 (750 * 37)

Actual units 850 750

Actual sales price 45 37

Standard price 35 30

Difference in price (Actual price – Standard price) 10 (45 – 35) 7 (37 – 30)

Actual units 850 750

Sales price variance (Difference in price * Actual 8500 (850 * 10) 5250 (750 * 7)

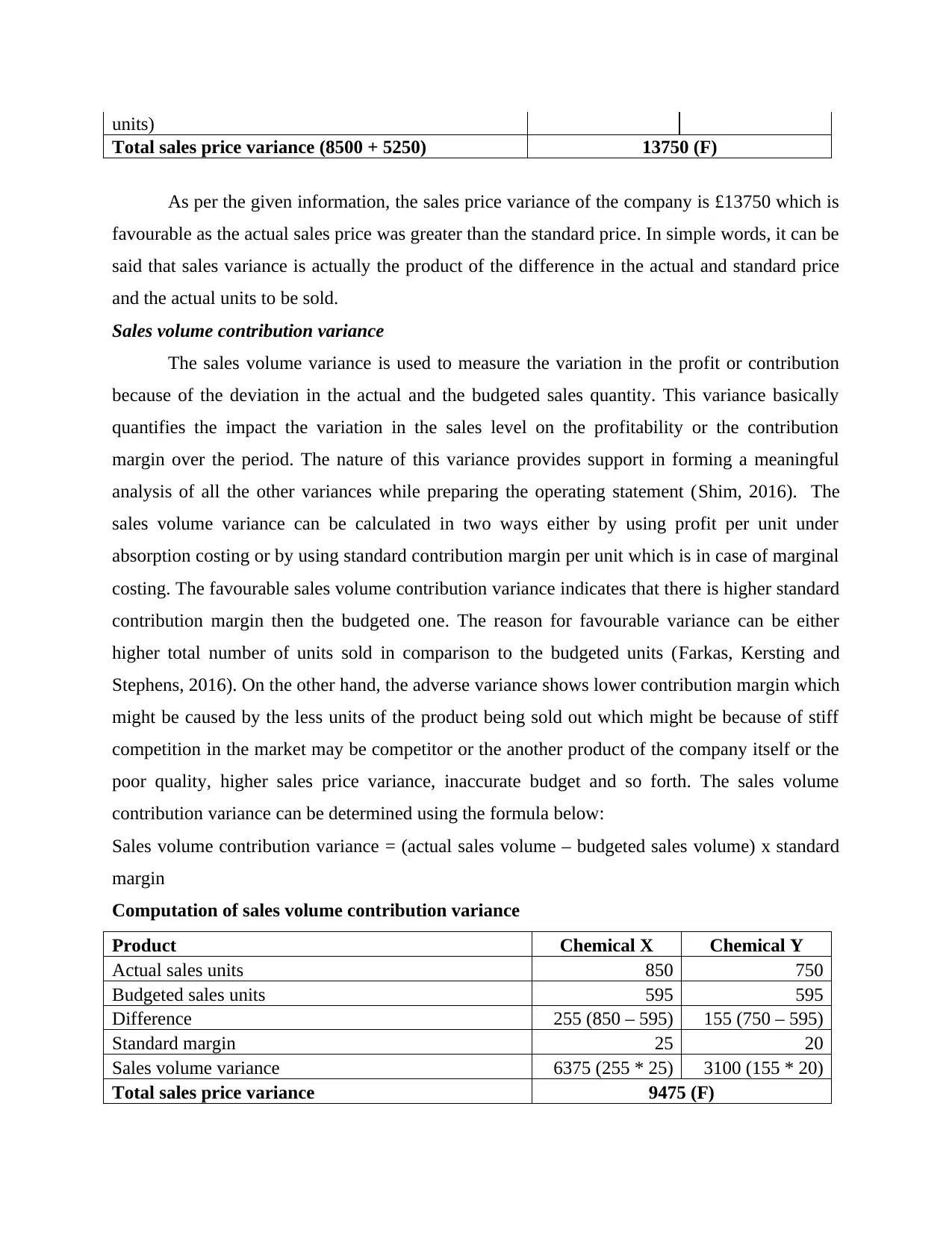

units)

Total sales price variance (8500 + 5250) 13750 (F)

As per the given information, the sales price variance of the company is £13750 which is

favourable as the actual sales price was greater than the standard price. In simple words, it can be

said that sales variance is actually the product of the difference in the actual and standard price

and the actual units to be sold.

Sales volume contribution variance

The sales volume variance is used to measure the variation in the profit or contribution

because of the deviation in the actual and the budgeted sales quantity. This variance basically

quantifies the impact the variation in the sales level on the profitability or the contribution

margin over the period. The nature of this variance provides support in forming a meaningful

analysis of all the other variances while preparing the operating statement (Shim, 2016). The

sales volume variance can be calculated in two ways either by using profit per unit under

absorption costing or by using standard contribution margin per unit which is in case of marginal

costing. The favourable sales volume contribution variance indicates that there is higher standard

contribution margin then the budgeted one. The reason for favourable variance can be either

higher total number of units sold in comparison to the budgeted units (Farkas, Kersting and

Stephens, 2016). On the other hand, the adverse variance shows lower contribution margin which

might be caused by the less units of the product being sold out which might be because of stiff

competition in the market may be competitor or the another product of the company itself or the

poor quality, higher sales price variance, inaccurate budget and so forth. The sales volume

contribution variance can be determined using the formula below:

Sales volume contribution variance = (actual sales volume – budgeted sales volume) x standard

margin

Computation of sales volume contribution variance

Product Chemical X Chemical Y

Actual sales units 850 750

Budgeted sales units 595 595

Difference 255 (850 – 595) 155 (750 – 595)

Standard margin 25 20

Sales volume variance 6375 (255 * 25) 3100 (155 * 20)

Total sales price variance 9475 (F)

Total sales price variance (8500 + 5250) 13750 (F)

As per the given information, the sales price variance of the company is £13750 which is

favourable as the actual sales price was greater than the standard price. In simple words, it can be

said that sales variance is actually the product of the difference in the actual and standard price

and the actual units to be sold.

Sales volume contribution variance

The sales volume variance is used to measure the variation in the profit or contribution

because of the deviation in the actual and the budgeted sales quantity. This variance basically

quantifies the impact the variation in the sales level on the profitability or the contribution

margin over the period. The nature of this variance provides support in forming a meaningful

analysis of all the other variances while preparing the operating statement (Shim, 2016). The

sales volume variance can be calculated in two ways either by using profit per unit under

absorption costing or by using standard contribution margin per unit which is in case of marginal

costing. The favourable sales volume contribution variance indicates that there is higher standard

contribution margin then the budgeted one. The reason for favourable variance can be either

higher total number of units sold in comparison to the budgeted units (Farkas, Kersting and

Stephens, 2016). On the other hand, the adverse variance shows lower contribution margin which

might be caused by the less units of the product being sold out which might be because of stiff

competition in the market may be competitor or the another product of the company itself or the

poor quality, higher sales price variance, inaccurate budget and so forth. The sales volume

contribution variance can be determined using the formula below:

Sales volume contribution variance = (actual sales volume – budgeted sales volume) x standard

margin

Computation of sales volume contribution variance

Product Chemical X Chemical Y

Actual sales units 850 750

Budgeted sales units 595 595

Difference 255 (850 – 595) 155 (750 – 595)

Standard margin 25 20

Sales volume variance 6375 (255 * 25) 3100 (155 * 20)

Total sales price variance 9475 (F)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Based on the information available, the total sales price variance is £9475 which is

favourable. This is because the number of units sold are higher than the units budgeted which

turned out to be favourable for the company.

2. The material price planning variance and material price operational variance

The material price variance is very useful for the companies a sit help in providing

feedback in respect to how the skilled managers of the organization are estimating the future

prices of the product. The planning variance compares the original budget and the revised

budget. The material price operational variance is considered to be more meaningful as it helps

in measuring the efficiency of the purchasing department with respect to the prevailing market

conditions at that point of time (Messer, 2016). It does not take into consideration the factors that

cannot be controlled by the purchasing department. The planning and operational variance makes

the standard costing more holistic and meaningful. The operating variance provides the company

with an up to date information about its operating efficiency. The material price planning and

operational variance helps in analysing those variances which are either controllable or

uncontrollable by the organization (Zarzycka and et.al, 2017). This helps the managers in

identifying the areas were actual does not match the budgeted which resulted into unfavourable

results such as faulty standard setting, poor planning and so forth. It will highlight how the

planning and standard setting can be further improved and enhanced in order to be more

accurate, relevant and appropriate.

The planning variance allows the managers to determine how effectively the

organizations planning process is. It helps in identifying the point where the revision in the

budget is required with respect to the changes in the business environment which are

unforeseeable when the budget was created (Zhang, 2017). However, in situations where the

standards fail to anticipate the market trends then it reflects the fault in the standard setting

system of the organization and also there are certain planning variances caused because of poor

standard setting can in fact over them actions can be taken as it is controllable in nature at the

planning stage. The use planning and operational variance provides assistance to the

management in drawing distinction between the variances which has been caused because of the

extraneous factors of the organization and the planning variances or the errors and the other

variances which are caused because of the factors which are in the control of the management.

favourable. This is because the number of units sold are higher than the units budgeted which

turned out to be favourable for the company.

2. The material price planning variance and material price operational variance

The material price variance is very useful for the companies a sit help in providing

feedback in respect to how the skilled managers of the organization are estimating the future

prices of the product. The planning variance compares the original budget and the revised

budget. The material price operational variance is considered to be more meaningful as it helps

in measuring the efficiency of the purchasing department with respect to the prevailing market

conditions at that point of time (Messer, 2016). It does not take into consideration the factors that

cannot be controlled by the purchasing department. The planning and operational variance makes

the standard costing more holistic and meaningful. The operating variance provides the company

with an up to date information about its operating efficiency. The material price planning and

operational variance helps in analysing those variances which are either controllable or

uncontrollable by the organization (Zarzycka and et.al, 2017). This helps the managers in

identifying the areas were actual does not match the budgeted which resulted into unfavourable

results such as faulty standard setting, poor planning and so forth. It will highlight how the

planning and standard setting can be further improved and enhanced in order to be more

accurate, relevant and appropriate.

The planning variance allows the managers to determine how effectively the

organizations planning process is. It helps in identifying the point where the revision in the

budget is required with respect to the changes in the business environment which are

unforeseeable when the budget was created (Zhang, 2017). However, in situations where the

standards fail to anticipate the market trends then it reflects the fault in the standard setting

system of the organization and also there are certain planning variances caused because of poor

standard setting can in fact over them actions can be taken as it is controllable in nature at the

planning stage. The use planning and operational variance provides assistance to the

management in drawing distinction between the variances which has been caused because of the

extraneous factors of the organization and the planning variances or the errors and the other

variances which are caused because of the factors which are in the control of the management.

Based on this, the less time is actually spent on investigating the variances which are not in

control of the management which reduces the chances of getting the staff being held responsible

for the variances which has been caused by the factors which are uncontrollable.

The operational managers performance is then compared to the adjusted standards which

indicates the conditions in which the manager usually work under the given reporting period

(Datar and Rajan, 2018). In case, the planning and operational variances of the organization are

not distinguished in that situation there is a potential for a dysfunctional behaviour in the

circumstances where the manager has been operating properly and appropriately and is also

being judged by the factors over which there is no control.

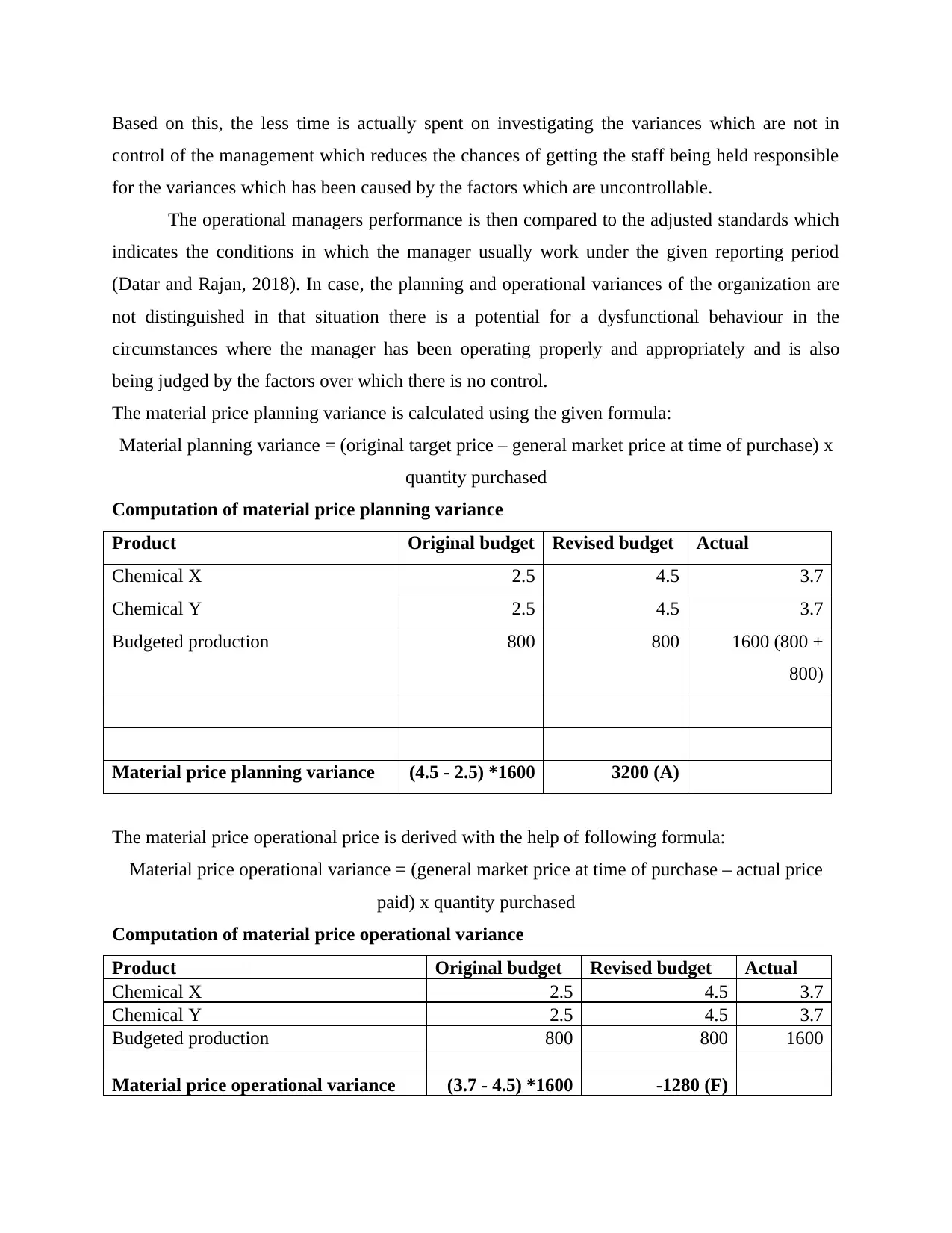

The material price planning variance is calculated using the given formula:

Material planning variance = (original target price – general market price at time of purchase) x

quantity purchased

Computation of material price planning variance

Product Original budget Revised budget Actual

Chemical X 2.5 4.5 3.7

Chemical Y 2.5 4.5 3.7

Budgeted production 800 800 1600 (800 +

800)

Material price planning variance (4.5 - 2.5) *1600 3200 (A)

The material price operational price is derived with the help of following formula:

Material price operational variance = (general market price at time of purchase – actual price

paid) x quantity purchased

Computation of material price operational variance

Product Original budget Revised budget Actual

Chemical X 2.5 4.5 3.7

Chemical Y 2.5 4.5 3.7

Budgeted production 800 800 1600

Material price operational variance (3.7 - 4.5) *1600 -1280 (F)

control of the management which reduces the chances of getting the staff being held responsible

for the variances which has been caused by the factors which are uncontrollable.

The operational managers performance is then compared to the adjusted standards which

indicates the conditions in which the manager usually work under the given reporting period

(Datar and Rajan, 2018). In case, the planning and operational variances of the organization are

not distinguished in that situation there is a potential for a dysfunctional behaviour in the

circumstances where the manager has been operating properly and appropriately and is also

being judged by the factors over which there is no control.

The material price planning variance is calculated using the given formula:

Material planning variance = (original target price – general market price at time of purchase) x

quantity purchased

Computation of material price planning variance

Product Original budget Revised budget Actual

Chemical X 2.5 4.5 3.7

Chemical Y 2.5 4.5 3.7

Budgeted production 800 800 1600 (800 +

800)

Material price planning variance (4.5 - 2.5) *1600 3200 (A)

The material price operational price is derived with the help of following formula:

Material price operational variance = (general market price at time of purchase – actual price

paid) x quantity purchased

Computation of material price operational variance

Product Original budget Revised budget Actual

Chemical X 2.5 4.5 3.7

Chemical Y 2.5 4.5 3.7

Budgeted production 800 800 1600

Material price operational variance (3.7 - 4.5) *1600 -1280 (F)

3. Critically evaluating benefits and limitation of using the variances in analysing the

performance of managers

Vera and et.al. (2016) reviewed that variance analysis referred as the comparison of the

pre-determined information and historic cost related data for ascertaining an adherence to the

plans. Variance analysis is counted as the most useful tool for the managers to assess

performance & in reducing risk of the company. It provides valuable information which helps

the managers in assessing future risk whereas other enables in improving the previous

performance of an entity. This tool looks at performance of the proposal, department, company

and division with that of standard performance so that gap between the budgeted and actual

performance can be measured in effective manner. Management of the company establishes

standards against which the performance would be measured. It is the process of determining the

cause of the variation in expenses & income of current year from that of budgeted values. It aids

in efficient budgeting action as the firm's management wishes for having lower amount of

deviations from that of planned budget. This helps the managers in making forward-looking &

detailed budgetary decisions. It acts as the control mechanism where analysis of the significant

difference on important items helps an enterprise in knowing causes and assist management in

looking towards possible ways of finding out deviations and ensuring effective controlling.

However, this tool is an activity which is mainly based on the financial results that are revealed

after a quarter. This time gap might affect the remedial actions in taking an ability up-to certain

extent. In case the budgeting or analysis is not been made in consideration with detailed

assessment of every factor, exercise of budgeting might lose, that is bound to deviate from actual

numbers.

It has been analysed by Hoch and et.al. (2018) that variance analysis allows controlling

of cost and evaluation of performance through comparing the actual and standard figures. The

main objective of controlling cost is producing item at low cost in accordance to the pre-

determined standards of quality. It motivates workers for accomplishing goals and pinpointing

responsibility for the undesirable performance in order to take corrective action. On other side, it

encourages insensitivity on managers part as they neglect the other important tools which might

benefit to companies. It facilitates connection within firm like top management & supervisors

which encourages staff in performing optimally. However, in this there might be tendency to

focus on meeting standards to an exclusion of other crucial objective like improving &

performance of managers

Vera and et.al. (2016) reviewed that variance analysis referred as the comparison of the

pre-determined information and historic cost related data for ascertaining an adherence to the

plans. Variance analysis is counted as the most useful tool for the managers to assess

performance & in reducing risk of the company. It provides valuable information which helps

the managers in assessing future risk whereas other enables in improving the previous

performance of an entity. This tool looks at performance of the proposal, department, company

and division with that of standard performance so that gap between the budgeted and actual

performance can be measured in effective manner. Management of the company establishes

standards against which the performance would be measured. It is the process of determining the

cause of the variation in expenses & income of current year from that of budgeted values. It aids

in efficient budgeting action as the firm's management wishes for having lower amount of

deviations from that of planned budget. This helps the managers in making forward-looking &

detailed budgetary decisions. It acts as the control mechanism where analysis of the significant

difference on important items helps an enterprise in knowing causes and assist management in

looking towards possible ways of finding out deviations and ensuring effective controlling.

However, this tool is an activity which is mainly based on the financial results that are revealed

after a quarter. This time gap might affect the remedial actions in taking an ability up-to certain

extent. In case the budgeting or analysis is not been made in consideration with detailed

assessment of every factor, exercise of budgeting might lose, that is bound to deviate from actual

numbers.

It has been analysed by Hoch and et.al. (2018) that variance analysis allows controlling

of cost and evaluation of performance through comparing the actual and standard figures. The

main objective of controlling cost is producing item at low cost in accordance to the pre-

determined standards of quality. It motivates workers for accomplishing goals and pinpointing

responsibility for the undesirable performance in order to take corrective action. On other side, it

encourages insensitivity on managers part as they neglect the other important tools which might

benefit to companies. It facilitates connection within firm like top management & supervisors

which encourages staff in performing optimally. However, in this there might be tendency to

focus on meeting standards to an exclusion of other crucial objective like improving &

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maintaining quality, satisfaction of customers and timely delivery. Moreover, it ensures that an

entity is in good financial state and also ensures that the supervisors or managers emphasize and

encourage orientation of results. On other side, it discourages initiation as the workers might not

need for bringing innovation particularly if such type of new idea might result to negative or

adverse variance in starting. It might also lead to an inaccurate decision that might result in

falling of company since data that is used in calculating variances might be counted as defective.

With respect to the given case, before calculating the material price planning and the

operational variances, the only information which was made available in regard to purchasing

was that the material price variance of £27000 which was favourable. As defined by Hout

(2017), the purchasing department of the company will be further assessed on account of this

variance since it cannot be considered as a reliable indicator of the efficiency of the purchasing

department of the organization. The main cause is not that it is not reliable but because of the

changing market conditions which consequently leading to the rise in the prices and this change

is actually not in the control of the purchasing department. Also, by further analysing the

material price variance and breaking it into two parts which are planning and operational

variances which is mainly considered as the most useful tool in assessing the performance. As

stated by Marzlin Marzuki and Ismail, (2019), the planning variance mainly states about the

uncontrollable element whereas the operational variance states about the controllable factors.

Both the variances can be easily calculated but for some businesses it is very easy but in some

case it turns out to be very difficult. The operational variance is also very meaningful as it is

utilized in determining the efficiency level of the purchasing department of the organization

under the set market conditions. It provides assistance in improving the morale and motivational

level of the staff of the organization.

But there are certain things which are required to be stated clearly like these variances are

also affected by the certain limitations which the organization must work on in order to

overcome it in case they are actually implemented in the practice. Based on Nishimura (2019),

things like standards set should be attainable and achievable and should not be vague. There can

be times when all the variances can be easily justified as because of the wrong and poor planning

which will result into no operational variances being highlighted. Also, in order to avoid any

type of error or mistakes, revising and analysing the variances will be very costly and time

consuming process. This may affect the budget of the company as well. Therefore, it can be sad

entity is in good financial state and also ensures that the supervisors or managers emphasize and

encourage orientation of results. On other side, it discourages initiation as the workers might not

need for bringing innovation particularly if such type of new idea might result to negative or

adverse variance in starting. It might also lead to an inaccurate decision that might result in

falling of company since data that is used in calculating variances might be counted as defective.

With respect to the given case, before calculating the material price planning and the

operational variances, the only information which was made available in regard to purchasing

was that the material price variance of £27000 which was favourable. As defined by Hout

(2017), the purchasing department of the company will be further assessed on account of this

variance since it cannot be considered as a reliable indicator of the efficiency of the purchasing

department of the organization. The main cause is not that it is not reliable but because of the

changing market conditions which consequently leading to the rise in the prices and this change

is actually not in the control of the purchasing department. Also, by further analysing the

material price variance and breaking it into two parts which are planning and operational

variances which is mainly considered as the most useful tool in assessing the performance. As

stated by Marzlin Marzuki and Ismail, (2019), the planning variance mainly states about the

uncontrollable element whereas the operational variance states about the controllable factors.

Both the variances can be easily calculated but for some businesses it is very easy but in some

case it turns out to be very difficult. The operational variance is also very meaningful as it is

utilized in determining the efficiency level of the purchasing department of the organization

under the set market conditions. It provides assistance in improving the morale and motivational

level of the staff of the organization.

But there are certain things which are required to be stated clearly like these variances are

also affected by the certain limitations which the organization must work on in order to

overcome it in case they are actually implemented in the practice. Based on Nishimura (2019),

things like standards set should be attainable and achievable and should not be vague. There can

be times when all the variances can be easily justified as because of the wrong and poor planning

which will result into no operational variances being highlighted. Also, in order to avoid any

type of error or mistakes, revising and analysing the variances will be very costly and time

consuming process. This may affect the budget of the company as well. Therefore, it can be sad

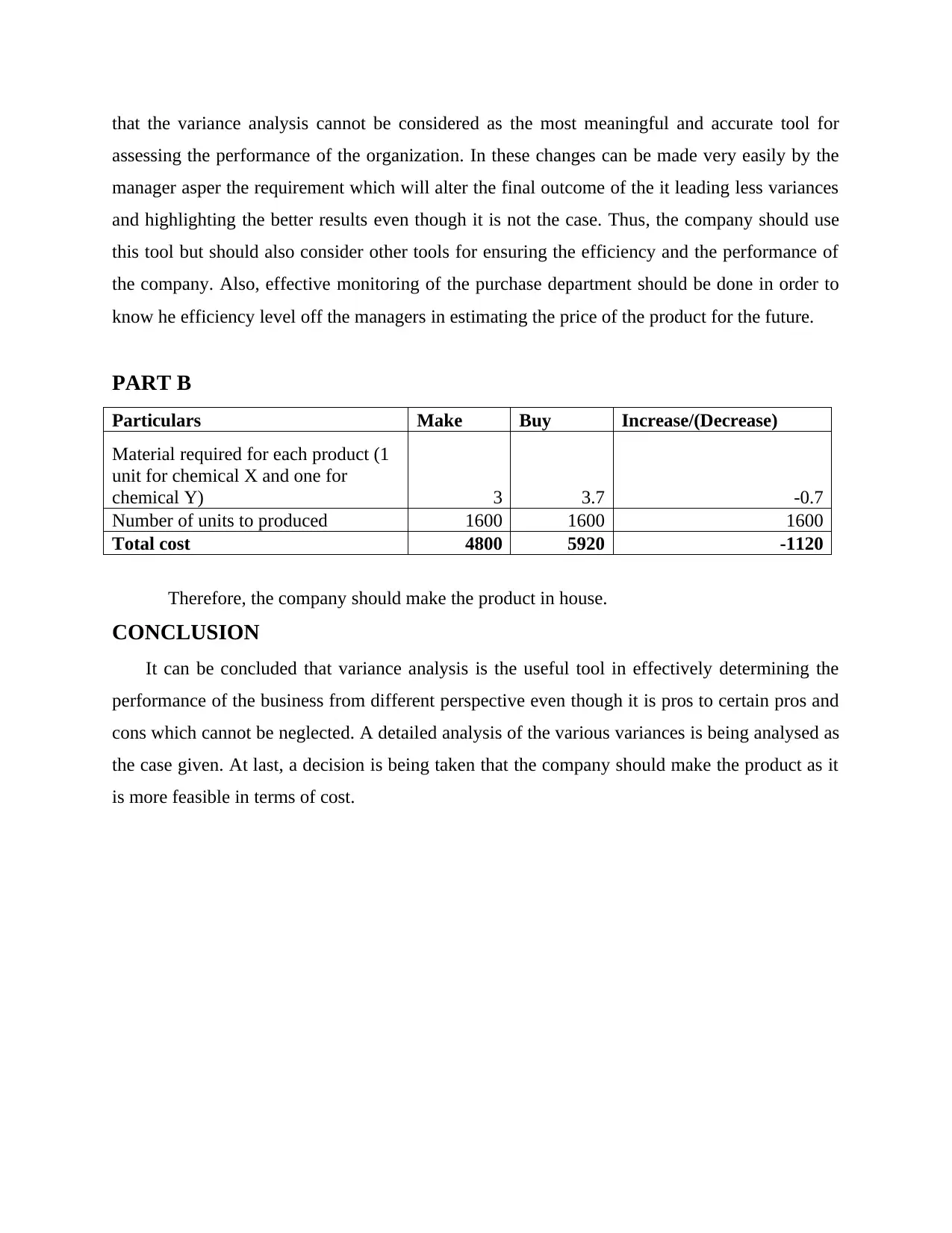

that the variance analysis cannot be considered as the most meaningful and accurate tool for

assessing the performance of the organization. In these changes can be made very easily by the

manager asper the requirement which will alter the final outcome of the it leading less variances

and highlighting the better results even though it is not the case. Thus, the company should use

this tool but should also consider other tools for ensuring the efficiency and the performance of

the company. Also, effective monitoring of the purchase department should be done in order to

know he efficiency level off the managers in estimating the price of the product for the future.

PART B

Particulars Make Buy Increase/(Decrease)

Material required for each product (1

unit for chemical X and one for

chemical Y) 3 3.7 -0.7

Number of units to produced 1600 1600 1600

Total cost 4800 5920 -1120

Therefore, the company should make the product in house.

CONCLUSION

It can be concluded that variance analysis is the useful tool in effectively determining the

performance of the business from different perspective even though it is pros to certain pros and

cons which cannot be neglected. A detailed analysis of the various variances is being analysed as

the case given. At last, a decision is being taken that the company should make the product as it

is more feasible in terms of cost.

assessing the performance of the organization. In these changes can be made very easily by the

manager asper the requirement which will alter the final outcome of the it leading less variances

and highlighting the better results even though it is not the case. Thus, the company should use

this tool but should also consider other tools for ensuring the efficiency and the performance of

the company. Also, effective monitoring of the purchase department should be done in order to

know he efficiency level off the managers in estimating the price of the product for the future.

PART B

Particulars Make Buy Increase/(Decrease)

Material required for each product (1

unit for chemical X and one for

chemical Y) 3 3.7 -0.7

Number of units to produced 1600 1600 1600

Total cost 4800 5920 -1120

Therefore, the company should make the product in house.

CONCLUSION

It can be concluded that variance analysis is the useful tool in effectively determining the

performance of the business from different perspective even though it is pros to certain pros and

cons which cannot be neglected. A detailed analysis of the various variances is being analysed as

the case given. At last, a decision is being taken that the company should make the product as it

is more feasible in terms of cost.

REFERENCES

Books and journal

Bai, G., 2016. Applying variance analysis to understand California hospitals' expense recovery

status by patient groups. Accounting Horizons. 30(2). pp.211-223.

Bragg, S. M., 2016. Cost accounting fundamentals. Colorado, CO: Accounting Tools.

Datar, S. M. and Rajan, M., 2018. Horngren's cost accounting: A managerial emphasis.

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education. 35. pp.56-

68.

Hoch, J. E. and et.al., 2018. Do ethical, authentic, and servant leadership explain variance

above and beyond transformational leadership? A meta-analysis. Journal of

Management. 44(2). pp.501-529.

Hout, B., 2017. Cost accounting approaches: The lean success. SAGE Publications: SAGE

Business Cases Originals.

Marzlin Marzuki, N.A.R. and Ismail, J., 2019. Benefits and limitations of variance analysis in

management accounting. ACCOUNTING BULLETIN. p.15.

Messer, R., 2016. Teaching Variance Analysis for Cost Accounting: How to Achieve above Par

Performance. In Advances in Accounting Education: Teaching and Curriculum

Innovations. Emerald Group Publishing Limited.

Nishimura, A., 2019. Profit opportunity, strategic innovation, and management accounting.

In Management, uncertainty, and accounting (pp. 97-127). Palgrave Macmillan, Singapore.

Shim, J. K., 2016. Accounting and finance for the nonfinancial executive: An Integrated

Resource Management Guide for the 21st Century. CRC Press.

Zarzycka, E. and et.al, 2017. Comparative Studies of the Use of Management Accounting

Information. EMAJ: Emerging Markets Journal. 7(2). pp.1-7.

Zhang, C., 2017. The Application of Variance Analysis in FP&A Organizations: Survey

Evidence and Recommendations for Enhancement. Journal of Accounting and

Finance. 17(8). pp.54-70.

Vera, O. D. and et.al., 2016. Assessing psychology students’ difficulties in elementary variance

analysis. Revista Diálogo Educacional. 16(48). pp.487-511.

Books and journal

Bai, G., 2016. Applying variance analysis to understand California hospitals' expense recovery

status by patient groups. Accounting Horizons. 30(2). pp.211-223.

Bragg, S. M., 2016. Cost accounting fundamentals. Colorado, CO: Accounting Tools.

Datar, S. M. and Rajan, M., 2018. Horngren's cost accounting: A managerial emphasis.

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education. 35. pp.56-

68.

Hoch, J. E. and et.al., 2018. Do ethical, authentic, and servant leadership explain variance

above and beyond transformational leadership? A meta-analysis. Journal of

Management. 44(2). pp.501-529.

Hout, B., 2017. Cost accounting approaches: The lean success. SAGE Publications: SAGE

Business Cases Originals.

Marzlin Marzuki, N.A.R. and Ismail, J., 2019. Benefits and limitations of variance analysis in

management accounting. ACCOUNTING BULLETIN. p.15.

Messer, R., 2016. Teaching Variance Analysis for Cost Accounting: How to Achieve above Par

Performance. In Advances in Accounting Education: Teaching and Curriculum

Innovations. Emerald Group Publishing Limited.

Nishimura, A., 2019. Profit opportunity, strategic innovation, and management accounting.

In Management, uncertainty, and accounting (pp. 97-127). Palgrave Macmillan, Singapore.

Shim, J. K., 2016. Accounting and finance for the nonfinancial executive: An Integrated

Resource Management Guide for the 21st Century. CRC Press.

Zarzycka, E. and et.al, 2017. Comparative Studies of the Use of Management Accounting

Information. EMAJ: Emerging Markets Journal. 7(2). pp.1-7.

Zhang, C., 2017. The Application of Variance Analysis in FP&A Organizations: Survey

Evidence and Recommendations for Enhancement. Journal of Accounting and

Finance. 17(8). pp.54-70.

Vera, O. D. and et.al., 2016. Assessing psychology students’ difficulties in elementary variance

analysis. Revista Diálogo Educacional. 16(48). pp.487-511.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.