Report: Management Accounting Systems and Reporting at Unicorn Limited

VerifiedAdded on 2020/02/03

|21

|5267

|41

Report

AI Summary

This report analyzes management accounting systems and their practical applications within Unicorn Limited, a retail company. It explores various management accounting systems, including traditional cost accounting, lean accounting, throughput accounting, transfer pricing, and price optimization. The report details different reporting methods such as financial planning, financial statement analysis, cost accounting, job cost reports, inventory management reports, debtors reports, and performance reports. The report also discusses the benefits of these systems, such as improved cost allocation, streamlined processes, and better decision-making. It highlights how management accounting helps in managing financial decisions, enhancing business growth, and improving internal reporting to achieve desired outcomes. The report also mentions the importance of internal reports, trend analysis, and cost-effective methods in achieving business success.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT

From: Management accounting

To: General Manager

Unicorn Limited company

Date: 28th April 2017

Subject: Management accounting, its various systems as well as reporting ways which are

applied in the business of Unicorn Limited

INTRODUCTION

In the current business environment, organization focuses upon tracking performance

which can be done in effective manner with the help of management and financial accounting

system. MA is considered as the provision of managing financial data and thus advice that firm

is using the resources for developing the business (Banerjee and Das, 2017). Thus, it is a

profession that involves partnering in order to involve in decision making process and improving

the performance management system. Management accountants plays a crucial role in carrying

out expertise in financial reporting and thus controlling the business process in terms of

improving business performance. Accountants basically prepares a report format in which all the

decisions regarding business has been mentioned and thus it possesses effective responsibility of

managing all the resources and providing suitable and timely information to customers.

Manager of firm undertakes crucial decisions of day to day transactions and thus results

in performing desired activities. Management accounting carries out the responsibility of

following different rules and regulations regarding collecting data and thus linked with

managerial aspects. Apart from this, it focuses on wide range of systems and approaches

involved in MA and supports for making effectual internal business decisions. In the current

study, it undertakes an SME which operates in either manufacturing, retail, hospitality and

construction sector. Unicorn Limited which operates in retail sector carries out its operations

using different tools and thus helps in making effective management accounting decisions.

Report also discusses benefits and limitations of different types of planning techniques and thus

could be utilized for controlling budgeted information.

1

From: Management accounting

To: General Manager

Unicorn Limited company

Date: 28th April 2017

Subject: Management accounting, its various systems as well as reporting ways which are

applied in the business of Unicorn Limited

INTRODUCTION

In the current business environment, organization focuses upon tracking performance

which can be done in effective manner with the help of management and financial accounting

system. MA is considered as the provision of managing financial data and thus advice that firm

is using the resources for developing the business (Banerjee and Das, 2017). Thus, it is a

profession that involves partnering in order to involve in decision making process and improving

the performance management system. Management accountants plays a crucial role in carrying

out expertise in financial reporting and thus controlling the business process in terms of

improving business performance. Accountants basically prepares a report format in which all the

decisions regarding business has been mentioned and thus it possesses effective responsibility of

managing all the resources and providing suitable and timely information to customers.

Manager of firm undertakes crucial decisions of day to day transactions and thus results

in performing desired activities. Management accounting carries out the responsibility of

following different rules and regulations regarding collecting data and thus linked with

managerial aspects. Apart from this, it focuses on wide range of systems and approaches

involved in MA and supports for making effectual internal business decisions. In the current

study, it undertakes an SME which operates in either manufacturing, retail, hospitality and

construction sector. Unicorn Limited which operates in retail sector carries out its operations

using different tools and thus helps in making effective management accounting decisions.

Report also discusses benefits and limitations of different types of planning techniques and thus

could be utilized for controlling budgeted information.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 1

P1

MA is the concept that helps in preparing accounting reports and thus provide accurate

and reliable information in order to make crucial decision making. Management accountants are

required to identify the financial position of firm and thus make effective short term financial

decision in relation to carry out day to day transactions. In regard to this, financial accounting

predicts that producing annual reports is considered as useful for external stakeholders and thus

obtain information from such accounts helps in influencing them to invest within firm (Bhimani

and et.al., 2013). There are different department who carries out financial management activities

and thus generate monthly or weekly reports in relation to identifying the financial performance

of Unicorn Limited. Through preparing reports it helps in reflecting the amount available in cash

in hand, accounts payable, outstanding debts, inventory etc. Thus, all such expenses need to be

recorded so that it comprises of preparing cost-value analysis, variance and other relevant

statistical information. Further, obtaining financial accounting and cost accounting information is

regarded as the main basis of carrying out management accounting. Unicorn Limited carries out

effective operations and thus carries out proper management accounting system so that it results

in carrying out effective information so that suitable outcomes could be generated. Various MA's

systems are explained below:

Traditional cost accounting- It is one of the effective cost accounting system which

results in carrying out traditional cost approach and thus obtain by various

organizations. Here, Unicorn Limited uses such cost accounting system and thus

calculate different cost i.e. direct or material, labour and overhead expenses. While,

carrying out such method it involves cost driver and thus it helps in identifying different

cost involved while carrying out traditional cost accounting method such as direct

material hours, labour and machine hours (Chenhall and Moers, 2015).

Lean accounting system- Further, such method is considered as the new concept that

results in executing management accounting and thus helps in identifying the alterations

that need to be made while carrying out management accounting process. It involves

accounting, controlling and monitoring the process so that Unicorn could improve its

performance (Christ and et.al., 2017). Accountants uses such information in relation to

2

P1

MA is the concept that helps in preparing accounting reports and thus provide accurate

and reliable information in order to make crucial decision making. Management accountants are

required to identify the financial position of firm and thus make effective short term financial

decision in relation to carry out day to day transactions. In regard to this, financial accounting

predicts that producing annual reports is considered as useful for external stakeholders and thus

obtain information from such accounts helps in influencing them to invest within firm (Bhimani

and et.al., 2013). There are different department who carries out financial management activities

and thus generate monthly or weekly reports in relation to identifying the financial performance

of Unicorn Limited. Through preparing reports it helps in reflecting the amount available in cash

in hand, accounts payable, outstanding debts, inventory etc. Thus, all such expenses need to be

recorded so that it comprises of preparing cost-value analysis, variance and other relevant

statistical information. Further, obtaining financial accounting and cost accounting information is

regarded as the main basis of carrying out management accounting. Unicorn Limited carries out

effective operations and thus carries out proper management accounting system so that it results

in carrying out effective information so that suitable outcomes could be generated. Various MA's

systems are explained below:

Traditional cost accounting- It is one of the effective cost accounting system which

results in carrying out traditional cost approach and thus obtain by various

organizations. Here, Unicorn Limited uses such cost accounting system and thus

calculate different cost i.e. direct or material, labour and overhead expenses. While,

carrying out such method it involves cost driver and thus it helps in identifying different

cost involved while carrying out traditional cost accounting method such as direct

material hours, labour and machine hours (Chenhall and Moers, 2015).

Lean accounting system- Further, such method is considered as the new concept that

results in executing management accounting and thus helps in identifying the alterations

that need to be made while carrying out management accounting process. It involves

accounting, controlling and monitoring the process so that Unicorn could improve its

performance (Christ and et.al., 2017). Accountants uses such information in relation to

2

focus upon lean manufacturing and obtain lean thinking which results in achieving

successful business.

Throughput accounting- Such accounting system consists of different elements and

thus obtain constraints in the accounting system and thus produces desired results. Also,

it is based upon the principle of carrying ot simple management technique. In such

system it results in carrying out the principle and approach which is related to simplified

management. In regard to this raising the performance in profitability, cited venture is

supported in terms of making effective decisions (Deegan, 2013).

Transfer pricing- However, such system is considered as effective approach which

results in involving the price in which movement of products and services is being done

and thus calculating the cost of expenses incurred in transfer of products or services.

Cost accounting system- Through using such system it helps in carrying out effective

framework so that it helps in estimating product cost for the profitability analysis and

valuation of inventory. Unicorn helps in providing assistance in regard to minimize their

product cost and helps in making sure that business could attain profitability (Bhimani

and et.al., 2013).

Price optimisation system: This is another system through which firm makes decisions

for charging specific amount of the retail items from customers. Key need of this system

for Unicorn Limited is for making profitable kind of the pricing decisions in the

workplace.

Job costing system: A firm when produces or sales different range of the products then

required to compute cost of each batch or job products. Further, Unicorn Limited

considers this system for assessing total cost associated with each job in the workplace.

Inventory management system: By using this method, stock level is managed and

reduced in the firm which is sign of enhancing inventory turnover ratio. Further, methods

involved in this are LIFO, weighted average and FIFO.

P2

It involves several methods which are being used in terms of management accounting

reporting and record daily transactions so that decision making could be done in an effective

way-

3

successful business.

Throughput accounting- Such accounting system consists of different elements and

thus obtain constraints in the accounting system and thus produces desired results. Also,

it is based upon the principle of carrying ot simple management technique. In such

system it results in carrying out the principle and approach which is related to simplified

management. In regard to this raising the performance in profitability, cited venture is

supported in terms of making effective decisions (Deegan, 2013).

Transfer pricing- However, such system is considered as effective approach which

results in involving the price in which movement of products and services is being done

and thus calculating the cost of expenses incurred in transfer of products or services.

Cost accounting system- Through using such system it helps in carrying out effective

framework so that it helps in estimating product cost for the profitability analysis and

valuation of inventory. Unicorn helps in providing assistance in regard to minimize their

product cost and helps in making sure that business could attain profitability (Bhimani

and et.al., 2013).

Price optimisation system: This is another system through which firm makes decisions

for charging specific amount of the retail items from customers. Key need of this system

for Unicorn Limited is for making profitable kind of the pricing decisions in the

workplace.

Job costing system: A firm when produces or sales different range of the products then

required to compute cost of each batch or job products. Further, Unicorn Limited

considers this system for assessing total cost associated with each job in the workplace.

Inventory management system: By using this method, stock level is managed and

reduced in the firm which is sign of enhancing inventory turnover ratio. Further, methods

involved in this are LIFO, weighted average and FIFO.

P2

It involves several methods which are being used in terms of management accounting

reporting and record daily transactions so that decision making could be done in an effective

way-

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial planning- It is considered as one of the best method through which financial

planning helps in offering effective decision making in regard to carry out business

activities. Through developing sound decision making power it helps in achieving

profitability within firm (Quattrone, 2016).

Analysing financial statement- Through carrying out comparative financial statement

analysis it results in identifying the profit and loss statement and balance sheet in regard

to gain insight to obtain financial statement of firm. Through analysing the financial

statement it helps business to evaluate the outcomes on yearly basis and identify the

profit or loss obtained by firm in an accounting period (Saladrigues and Tena, 2017).

Cost accounting- Such method is being used by management accountant in relation in

order to report or determine the cost related information. It helps in revealing the data that

is related to cost of product, department fees, process charges etc. Thus, it results in

identifying the actual cost obtained by organization and compare it with the budgeted

one. It helps in identifying the deviation in regard to improve the performance of firm in

market (Zimmerman and Yahya-Zadeh, 2011).

Job Cost Reports: A method of reporting in which costs or expenses related to each job

are recorded is known as job cost reports. Further, sum of this expenditure is transacted in

the books of profit and loss.

Inventory Management Reports: Under this, level of stock is recorded in two ways

which are such as units and amounts. Moreover, inventory of Unicorn Limited at the end

of year and beginning of the financial year are recorded in proper direction.

Debtors / Accounts Receivable Ageing reports: As per this reporting method, amount

of credit sales is recorded properly. Through this, payment which will be received from

credit customers are mentioned. Total of this report is part of balance sheet where in

terms of debtors transacted.

Performance Reports: At the last, this specific report is prepared in order to analyse and

discuss performance of the Unicorn Limited at the end of financial period. For this,

basically variance analysis tool is undertaken by the management.

M1

Through using different management accounting system it helps in providing benefits

which are as follows-

4

planning helps in offering effective decision making in regard to carry out business

activities. Through developing sound decision making power it helps in achieving

profitability within firm (Quattrone, 2016).

Analysing financial statement- Through carrying out comparative financial statement

analysis it results in identifying the profit and loss statement and balance sheet in regard

to gain insight to obtain financial statement of firm. Through analysing the financial

statement it helps business to evaluate the outcomes on yearly basis and identify the

profit or loss obtained by firm in an accounting period (Saladrigues and Tena, 2017).

Cost accounting- Such method is being used by management accountant in relation in

order to report or determine the cost related information. It helps in revealing the data that

is related to cost of product, department fees, process charges etc. Thus, it results in

identifying the actual cost obtained by organization and compare it with the budgeted

one. It helps in identifying the deviation in regard to improve the performance of firm in

market (Zimmerman and Yahya-Zadeh, 2011).

Job Cost Reports: A method of reporting in which costs or expenses related to each job

are recorded is known as job cost reports. Further, sum of this expenditure is transacted in

the books of profit and loss.

Inventory Management Reports: Under this, level of stock is recorded in two ways

which are such as units and amounts. Moreover, inventory of Unicorn Limited at the end

of year and beginning of the financial year are recorded in proper direction.

Debtors / Accounts Receivable Ageing reports: As per this reporting method, amount

of credit sales is recorded properly. Through this, payment which will be received from

credit customers are mentioned. Total of this report is part of balance sheet where in

terms of debtors transacted.

Performance Reports: At the last, this specific report is prepared in order to analyse and

discuss performance of the Unicorn Limited at the end of financial period. For this,

basically variance analysis tool is undertaken by the management.

M1

Through using different management accounting system it helps in providing benefits

which are as follows-

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Traditional cost accounting- Main benefit of using traditional cost accounting system

helps in easily implementing the particular system so that it aids in directly determining

the cost of goods sold by Unicorn Limited. Thus, it helps in benefiting an effective

allocation of cost and thus linked with material, labour and overheads. Such system helps

in obtaining crucial information in regard to identify the final price of Unicorn products

that will be sold to consumers (Marginal and absorption costing. 2016).

Lean accounting- Further, benefit of using lean accounting which results in assessing

that it is less complex and obtains crucial information in relation to compare the same

with traditional accounting. Also, carrying out such application results in obtaining

required information within Unicorn and thus improve the performance of firm in market.

Throughput accounting- Moreover, such system of accounting provides benefit in

relation to control the actions which takes place in regard to carry out production within

Unicorn Limited. It involves inadequate level of material, labour or product capacity so

that helps in facilitating business. Further, it also helps in minimizing the cost and

improves the profitability of firm in market (Romano, 2015).

Transfer pricing- With the help of such type of management system it helps in

benefiting business in terms of determining the cost that is related to movement of

products. However, such system helps in identifying the total cost of product

manufactured by Unicorn which involves all the expenses related to producing the

product.

Systems or methods of MA like cost accounting is highly beneficial for calculating total

cost of production and operation incurred in the workplace. Using inventory system, Unicorn

Limited able to analyse stock and make strategies for utilising it in optimum direction. When

looking at the price optimisation then it helps to the retail organisation in order to make decisions

for charging price of the products. From job costing, it is supportive for computing total

expenses included in each job.

D1

Through carrying out management accounting system it is beneficial for Unicorn to

integrate and carry out effective results so that financial activities within firm is being managed.

However, it helps in managing business decision and thus enhance growth and success in market.

Unicorn management uses effective management accounting system which results in managing

5

helps in easily implementing the particular system so that it aids in directly determining

the cost of goods sold by Unicorn Limited. Thus, it helps in benefiting an effective

allocation of cost and thus linked with material, labour and overheads. Such system helps

in obtaining crucial information in regard to identify the final price of Unicorn products

that will be sold to consumers (Marginal and absorption costing. 2016).

Lean accounting- Further, benefit of using lean accounting which results in assessing

that it is less complex and obtains crucial information in relation to compare the same

with traditional accounting. Also, carrying out such application results in obtaining

required information within Unicorn and thus improve the performance of firm in market.

Throughput accounting- Moreover, such system of accounting provides benefit in

relation to control the actions which takes place in regard to carry out production within

Unicorn Limited. It involves inadequate level of material, labour or product capacity so

that helps in facilitating business. Further, it also helps in minimizing the cost and

improves the profitability of firm in market (Romano, 2015).

Transfer pricing- With the help of such type of management system it helps in

benefiting business in terms of determining the cost that is related to movement of

products. However, such system helps in identifying the total cost of product

manufactured by Unicorn which involves all the expenses related to producing the

product.

Systems or methods of MA like cost accounting is highly beneficial for calculating total

cost of production and operation incurred in the workplace. Using inventory system, Unicorn

Limited able to analyse stock and make strategies for utilising it in optimum direction. When

looking at the price optimisation then it helps to the retail organisation in order to make decisions

for charging price of the products. From job costing, it is supportive for computing total

expenses included in each job.

D1

Through carrying out management accounting system it is beneficial for Unicorn to

integrate and carry out effective results so that financial activities within firm is being managed.

However, it helps in managing business decision and thus enhance growth and success in market.

Unicorn management uses effective management accounting system which results in managing

5

financial decision so that appropriate decision could be taken in relation attain desired outcomes.

Managers of Unicorn need not to focus upon bringing improvement within the operational areas

and thsu results in minimizing the cost involves in operating the business so that high return

could be obtained (Banerjee and Das, 2017). However, using effective management accounting

system results in reporting within firm and thus improving the performance of firm in relation to

prepare appropriate budget and thus evaluate the outcomes that results in improving success.

Furthermore, management accounting reporting results in preparing job report, cost

report and budgeting etc. which helps in evaluating the business performance in regard to create

appropriate planning so that desired results could be attained. Thus, it is the best way which

helps in evaluating the perceptions of business and thus creates appropriate planning in order to

report the transactions and create crucial decision to manage the business operations (Bhimani

and et.al., 2013).

Through carrying out internal business reports within Unicorn Limited it helps in

identifying the business functions and accomplish the same within specified time duration.

Management accounting consists of different reports that presents specific information about

Unicorn daily transactions so that preparing trend analysis results in forecasting the same

information that is going to be occur in future (Chenhall and Moers, 2015). It also results in

obtaining useful information and thus carry out trend analysis so that it results in reducing the

wastage of resources and thus obtain cost effective method so that business success could be

achieved.

TASK 2

P3

Through determining cost it helps business to improve the managerial decision and thus

results in carrying out the business functions which results in identifying the cost involves in

business operations. Also, identifying inaccurate costs results in adversely affecting Unicorn's

pricing decision (Deegan, 2013). It involves distinctive techniques which are being used by firm

in relation to determine the cost and identify marginal costing, absorption costing and other

methods in relation to calculate the costs which are discussed underneath-

Marginal costing- A technique which comprises with only those costs which are in

nature of the variable and change in accordance to the production level. Further, level of

6

Managers of Unicorn need not to focus upon bringing improvement within the operational areas

and thsu results in minimizing the cost involves in operating the business so that high return

could be obtained (Banerjee and Das, 2017). However, using effective management accounting

system results in reporting within firm and thus improving the performance of firm in relation to

prepare appropriate budget and thus evaluate the outcomes that results in improving success.

Furthermore, management accounting reporting results in preparing job report, cost

report and budgeting etc. which helps in evaluating the business performance in regard to create

appropriate planning so that desired results could be attained. Thus, it is the best way which

helps in evaluating the perceptions of business and thus creates appropriate planning in order to

report the transactions and create crucial decision to manage the business operations (Bhimani

and et.al., 2013).

Through carrying out internal business reports within Unicorn Limited it helps in

identifying the business functions and accomplish the same within specified time duration.

Management accounting consists of different reports that presents specific information about

Unicorn daily transactions so that preparing trend analysis results in forecasting the same

information that is going to be occur in future (Chenhall and Moers, 2015). It also results in

obtaining useful information and thus carry out trend analysis so that it results in reducing the

wastage of resources and thus obtain cost effective method so that business success could be

achieved.

TASK 2

P3

Through determining cost it helps business to improve the managerial decision and thus

results in carrying out the business functions which results in identifying the cost involves in

business operations. Also, identifying inaccurate costs results in adversely affecting Unicorn's

pricing decision (Deegan, 2013). It involves distinctive techniques which are being used by firm

in relation to determine the cost and identify marginal costing, absorption costing and other

methods in relation to calculate the costs which are discussed underneath-

Marginal costing- A technique which comprises with only those costs which are in

nature of the variable and change in accordance to the production level. Further, level of

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

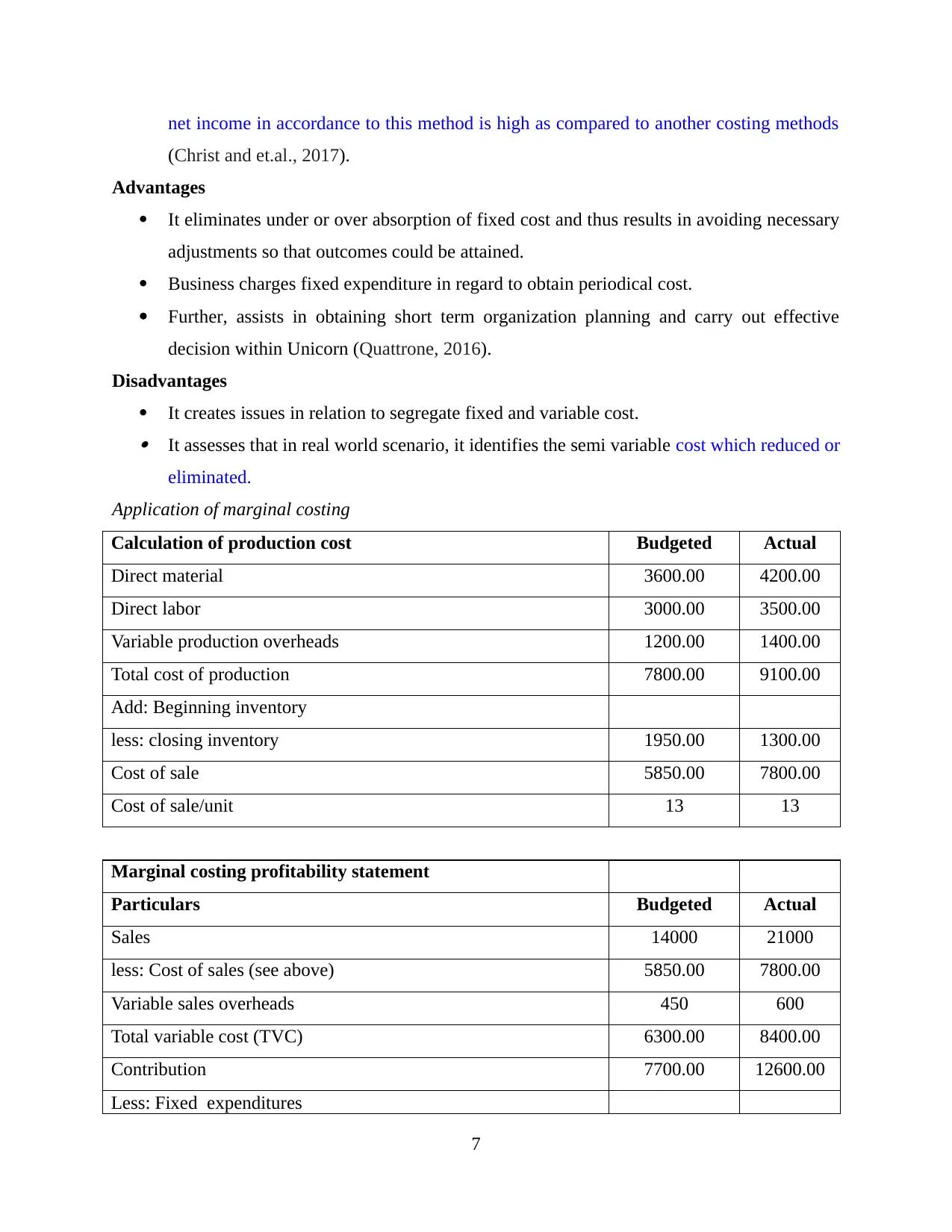

net income in accordance to this method is high as compared to another costing methods

(Christ and et.al., 2017).

Advantages

It eliminates under or over absorption of fixed cost and thus results in avoiding necessary

adjustments so that outcomes could be attained.

Business charges fixed expenditure in regard to obtain periodical cost.

Further, assists in obtaining short term organization planning and carry out effective

decision within Unicorn (Quattrone, 2016).

Disadvantages

It creates issues in relation to segregate fixed and variable cost. It assesses that in real world scenario, it identifies the semi variable cost which reduced or

eliminated.

Application of marginal costing

Calculation of production cost Budgeted Actual

Direct material 3600.00 4200.00

Direct labor 3000.00 3500.00

Variable production overheads 1200.00 1400.00

Total cost of production 7800.00 9100.00

Add: Beginning inventory

less: closing inventory 1950.00 1300.00

Cost of sale 5850.00 7800.00

Cost of sale/unit 13 13

Marginal costing profitability statement

Particulars Budgeted Actual

Sales 14000 21000

less: Cost of sales (see above) 5850.00 7800.00

Variable sales overheads 450 600

Total variable cost (TVC) 6300.00 8400.00

Contribution 7700.00 12600.00

Less: Fixed expenditures

7

(Christ and et.al., 2017).

Advantages

It eliminates under or over absorption of fixed cost and thus results in avoiding necessary

adjustments so that outcomes could be attained.

Business charges fixed expenditure in regard to obtain periodical cost.

Further, assists in obtaining short term organization planning and carry out effective

decision within Unicorn (Quattrone, 2016).

Disadvantages

It creates issues in relation to segregate fixed and variable cost. It assesses that in real world scenario, it identifies the semi variable cost which reduced or

eliminated.

Application of marginal costing

Calculation of production cost Budgeted Actual

Direct material 3600.00 4200.00

Direct labor 3000.00 3500.00

Variable production overheads 1200.00 1400.00

Total cost of production 7800.00 9100.00

Add: Beginning inventory

less: closing inventory 1950.00 1300.00

Cost of sale 5850.00 7800.00

Cost of sale/unit 13 13

Marginal costing profitability statement

Particulars Budgeted Actual

Sales 14000 21000

less: Cost of sales (see above) 5850.00 7800.00

Variable sales overheads 450 600

Total variable cost (TVC) 6300.00 8400.00

Contribution 7700.00 12600.00

Less: Fixed expenditures

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

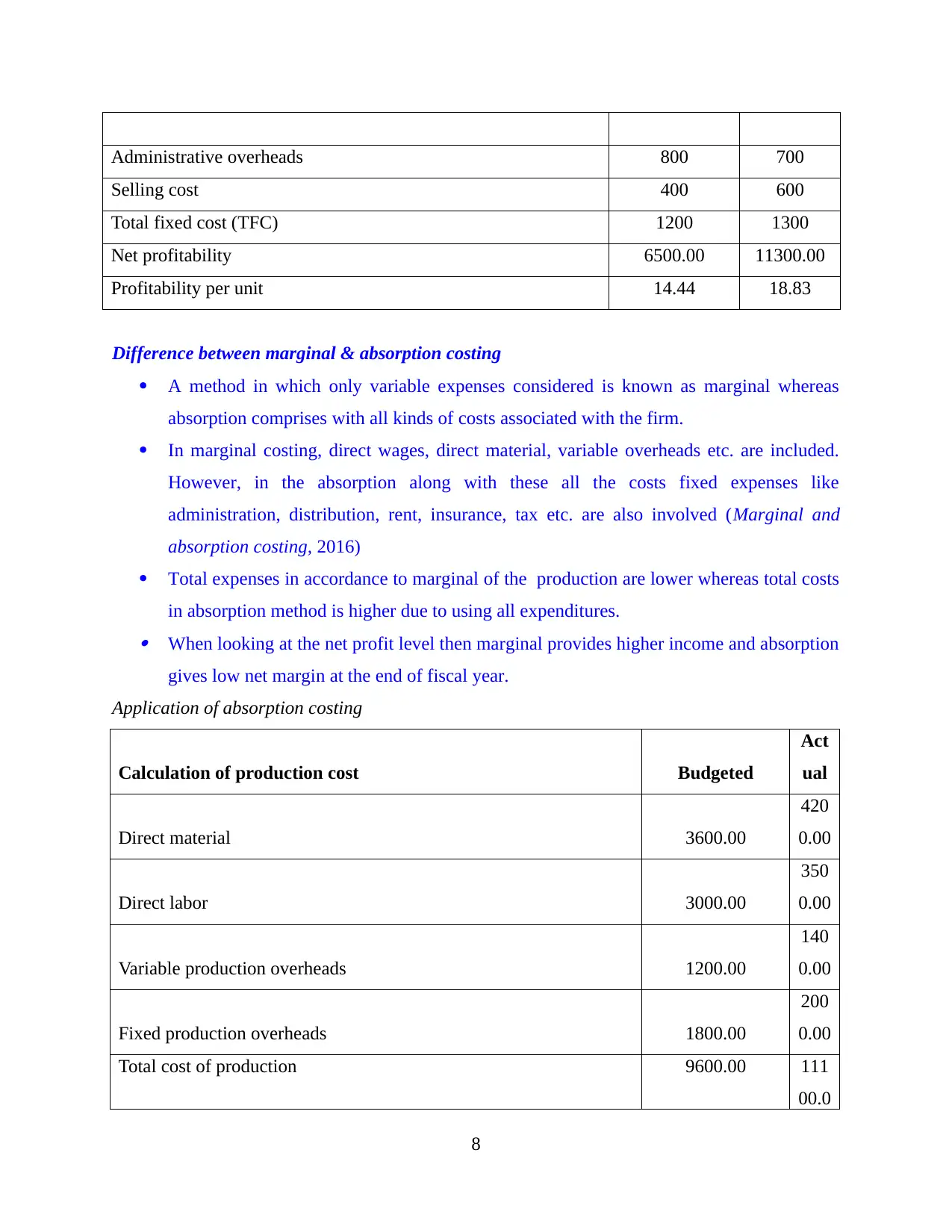

Administrative overheads 800 700

Selling cost 400 600

Total fixed cost (TFC) 1200 1300

Net profitability 6500.00 11300.00

Profitability per unit 14.44 18.83

Difference between marginal & absorption costing

A method in which only variable expenses considered is known as marginal whereas

absorption comprises with all kinds of costs associated with the firm.

In marginal costing, direct wages, direct material, variable overheads etc. are included.

However, in the absorption along with these all the costs fixed expenses like

administration, distribution, rent, insurance, tax etc. are also involved (Marginal and

absorption costing, 2016)

Total expenses in accordance to marginal of the production are lower whereas total costs

in absorption method is higher due to using all expenditures. When looking at the net profit level then marginal provides higher income and absorption

gives low net margin at the end of fiscal year.

Application of absorption costing

Calculation of production cost Budgeted

Act

ual

Direct material 3600.00

420

0.00

Direct labor 3000.00

350

0.00

Variable production overheads 1200.00

140

0.00

Fixed production overheads 1800.00

200

0.00

Total cost of production 9600.00 111

00.0

8

Selling cost 400 600

Total fixed cost (TFC) 1200 1300

Net profitability 6500.00 11300.00

Profitability per unit 14.44 18.83

Difference between marginal & absorption costing

A method in which only variable expenses considered is known as marginal whereas

absorption comprises with all kinds of costs associated with the firm.

In marginal costing, direct wages, direct material, variable overheads etc. are included.

However, in the absorption along with these all the costs fixed expenses like

administration, distribution, rent, insurance, tax etc. are also involved (Marginal and

absorption costing, 2016)

Total expenses in accordance to marginal of the production are lower whereas total costs

in absorption method is higher due to using all expenditures. When looking at the net profit level then marginal provides higher income and absorption

gives low net margin at the end of fiscal year.

Application of absorption costing

Calculation of production cost Budgeted

Act

ual

Direct material 3600.00

420

0.00

Direct labor 3000.00

350

0.00

Variable production overheads 1200.00

140

0.00

Fixed production overheads 1800.00

200

0.00

Total cost of production 9600.00 111

00.0

8

0

Add: Beginning inventory

less: closing inventory 2400.00

158

5.71

Cost of sale 7200.00

951

4.29

Cost of sale/unit 16

15.8

6

Absorption costing profitability statement

Particulars Budgeted

Act

ual

Sales 14000

210

00

less: Cost of sales 7200.00

951

4.29

Gross profit 6800.00

114

85.7

1

Less: indirect expenditures

Variable sales overheads 450 600

Administrative overheads 800 700

Selling cost 400 600

Total indirect expenditures 1650

190

0

Net profitability 5150.00

958

5.71

Profitability per unit 11.44

15.9

8

Income statement using marginal costing

9

Add: Beginning inventory

less: closing inventory 2400.00

158

5.71

Cost of sale 7200.00

951

4.29

Cost of sale/unit 16

15.8

6

Absorption costing profitability statement

Particulars Budgeted

Act

ual

Sales 14000

210

00

less: Cost of sales 7200.00

951

4.29

Gross profit 6800.00

114

85.7

1

Less: indirect expenditures

Variable sales overheads 450 600

Administrative overheads 800 700

Selling cost 400 600

Total indirect expenditures 1650

190

0

Net profitability 5150.00

958

5.71

Profitability per unit 11.44

15.9

8

Income statement using marginal costing

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.