Management Accounting: Planning Tools for Budgetary Control

VerifiedAdded on 2023/01/05

|14

|4017

|70

AI Summary

This report explores the concept of management accounting and its role in decision-making. It focuses on the case of Crest Dairy and discusses different types of management accounting systems, cost calculations, income statements, and planning tools for budgetary control. The advantages and disadvantages of these tools are also analyzed. The report aims to provide a greater understanding of management accounting principles.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

INTRODUCTION

Management Accounting is the practise of planning business operations documents that

allow managers to make short-term as well as long-term decisions. It allows a company to

achieve its objectives by defining, evaluating, assessing, interpreting and transmitting guidance

to stakeholders (Armitage, Webb and Glynn, 2016). Management accounting reflects from all

accounting policies targeted at reminding management of operating business outcomes. It utilizes

data concerning to the cost of goods or services obtained by company. Budgets are also used to

measure decisions taken in the form of organisational planning. Management Accountants use

the performance reviews to observe variances between real outcomes from

budgets. .Management accounting allows managers to make choices within an organisation. The

information recorded covers all areas of reporting that notify the business activities in relation to

price of goods or services purchased by organisation. Management accountants are using budgets

to calculate the marketing strategy of activities.

This report based on Crest Dairy where prime responsibility of management accountant of

the company is to analyse the data provided by managerial accounting to support managers in

making effective actions to meet results. Elizabeth has newly joined the Department as a trainee

junior management accountant, and management accountants must prepare a report that offers

greater understatement of management accounting principles. This report covers several topics

such as different types of management accounting systems, report and methods to calculate cost

of product and overall profit. In addition, it includes the different planning tools which are

required for budgetary control. Along with it, organization needs to identify the ways which

helps in resolving financial problems.

MAIN BODY

TASK 1

Covered in PPT

TASK 2

P3. Cost calculations and preparation of income statement

Cost per unit by using marginal or absorption method:

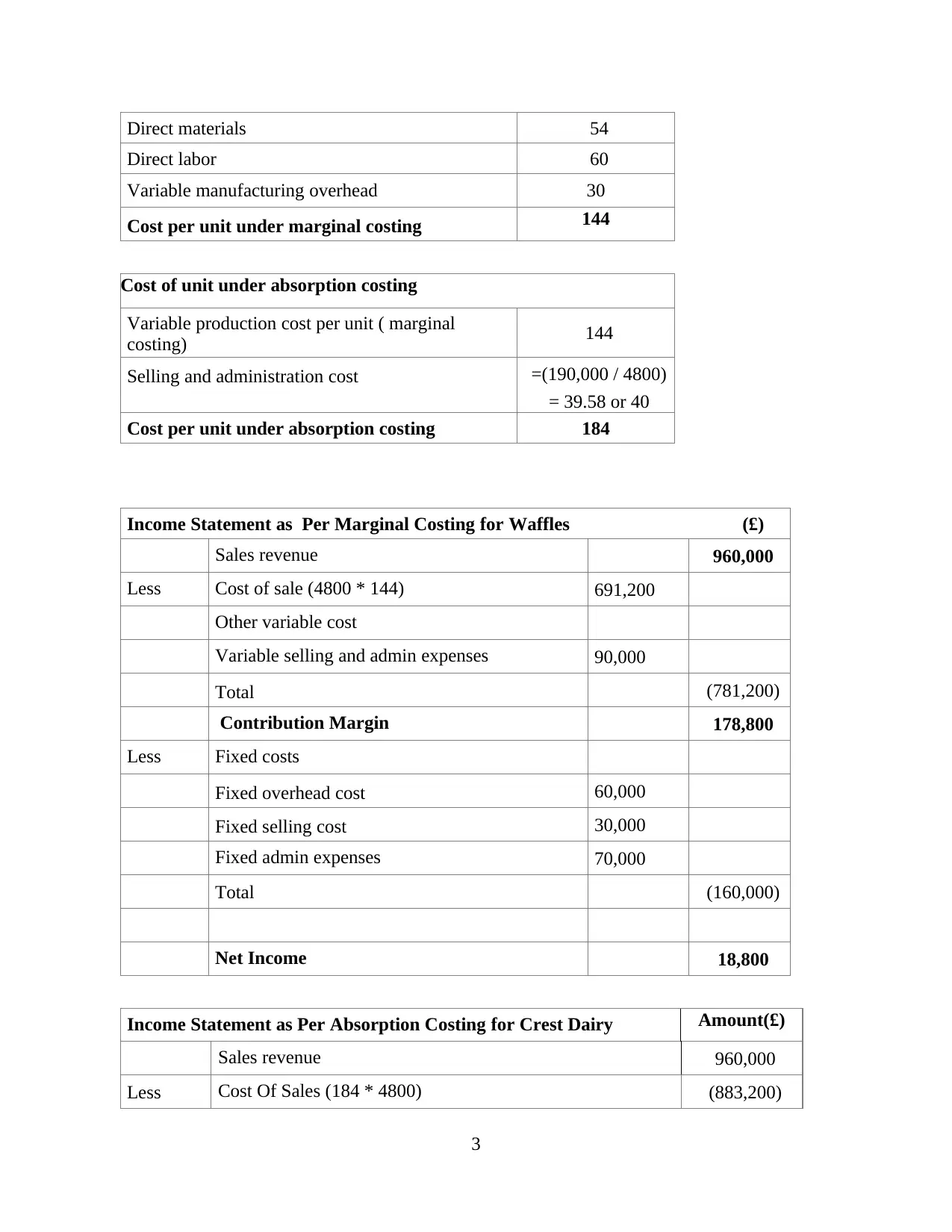

Cost of unit under marginal costing

2

Management Accounting is the practise of planning business operations documents that

allow managers to make short-term as well as long-term decisions. It allows a company to

achieve its objectives by defining, evaluating, assessing, interpreting and transmitting guidance

to stakeholders (Armitage, Webb and Glynn, 2016). Management accounting reflects from all

accounting policies targeted at reminding management of operating business outcomes. It utilizes

data concerning to the cost of goods or services obtained by company. Budgets are also used to

measure decisions taken in the form of organisational planning. Management Accountants use

the performance reviews to observe variances between real outcomes from

budgets. .Management accounting allows managers to make choices within an organisation. The

information recorded covers all areas of reporting that notify the business activities in relation to

price of goods or services purchased by organisation. Management accountants are using budgets

to calculate the marketing strategy of activities.

This report based on Crest Dairy where prime responsibility of management accountant of

the company is to analyse the data provided by managerial accounting to support managers in

making effective actions to meet results. Elizabeth has newly joined the Department as a trainee

junior management accountant, and management accountants must prepare a report that offers

greater understatement of management accounting principles. This report covers several topics

such as different types of management accounting systems, report and methods to calculate cost

of product and overall profit. In addition, it includes the different planning tools which are

required for budgetary control. Along with it, organization needs to identify the ways which

helps in resolving financial problems.

MAIN BODY

TASK 1

Covered in PPT

TASK 2

P3. Cost calculations and preparation of income statement

Cost per unit by using marginal or absorption method:

Cost of unit under marginal costing

2

Direct materials 54

Direct labor 60

Variable manufacturing overhead 30

Cost per unit under marginal costing 144

Cost of unit under absorption costing

Variable production cost per unit ( marginal

costing) 144

Selling and administration cost =(190,000 / 4800)

= 39.58 or 40

Cost per unit under absorption costing 184

Income Statement as Per Marginal Costing for Waffles (£)

Sales revenue 960,000

Less Cost of sale (4800 * 144) 691,200

Other variable cost

Variable selling and admin expenses 90,000

Total (781,200)

Contribution Margin 178,800

Less Fixed costs

Fixed overhead cost 60,000

Fixed selling cost 30,000

Fixed admin expenses 70,000

Total (160,000)

Net Income 18,800

Income Statement as Per Absorption Costing for Crest Dairy Amount(£)

Sales revenue 960,000

Less Cost Of Sales (184 * 4800) (883,200)

3

Direct labor 60

Variable manufacturing overhead 30

Cost per unit under marginal costing 144

Cost of unit under absorption costing

Variable production cost per unit ( marginal

costing) 144

Selling and administration cost =(190,000 / 4800)

= 39.58 or 40

Cost per unit under absorption costing 184

Income Statement as Per Marginal Costing for Waffles (£)

Sales revenue 960,000

Less Cost of sale (4800 * 144) 691,200

Other variable cost

Variable selling and admin expenses 90,000

Total (781,200)

Contribution Margin 178,800

Less Fixed costs

Fixed overhead cost 60,000

Fixed selling cost 30,000

Fixed admin expenses 70,000

Total (160,000)

Net Income 18,800

Income Statement as Per Absorption Costing for Crest Dairy Amount(£)

Sales revenue 960,000

Less Cost Of Sales (184 * 4800) (883,200)

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

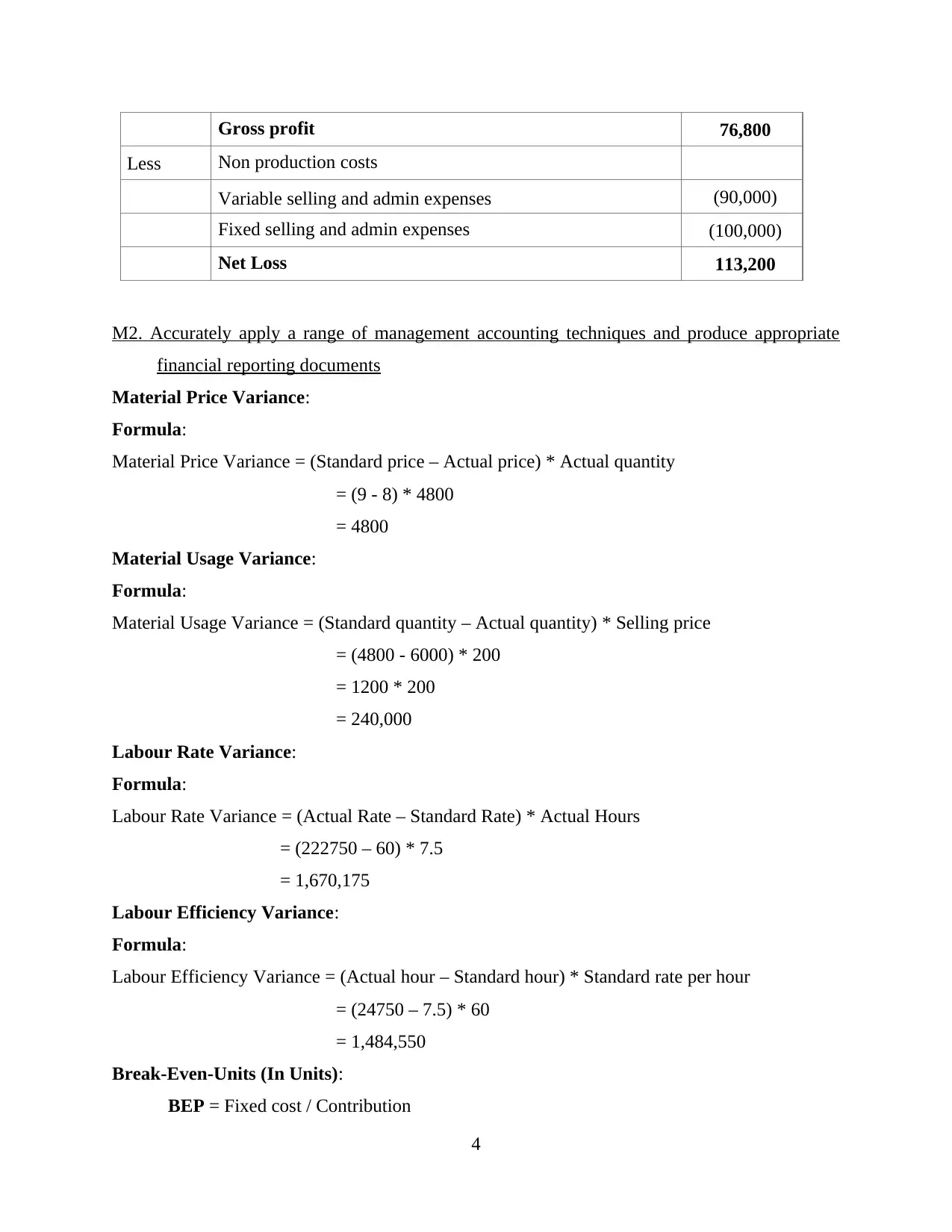

Gross profit 76,800

Less Non production costs

Variable selling and admin expenses (90,000)

Fixed selling and admin expenses (100,000)

Net Loss 113,200

M2. Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents

Material Price Variance:

Formula:

Material Price Variance = (Standard price – Actual price) * Actual quantity

= (9 - 8) * 4800

= 4800

Material Usage Variance:

Formula:

Material Usage Variance = (Standard quantity – Actual quantity) * Selling price

= (4800 - 6000) * 200

= 1200 * 200

= 240,000

Labour Rate Variance:

Formula:

Labour Rate Variance = (Actual Rate – Standard Rate) * Actual Hours

= (222750 – 60) * 7.5

= 1,670,175

Labour Efficiency Variance:

Formula:

Labour Efficiency Variance = (Actual hour – Standard hour) * Standard rate per hour

= (24750 – 7.5) * 60

= 1,484,550

Break-Even-Units (In Units):

BEP = Fixed cost / Contribution

4

Less Non production costs

Variable selling and admin expenses (90,000)

Fixed selling and admin expenses (100,000)

Net Loss 113,200

M2. Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents

Material Price Variance:

Formula:

Material Price Variance = (Standard price – Actual price) * Actual quantity

= (9 - 8) * 4800

= 4800

Material Usage Variance:

Formula:

Material Usage Variance = (Standard quantity – Actual quantity) * Selling price

= (4800 - 6000) * 200

= 1200 * 200

= 240,000

Labour Rate Variance:

Formula:

Labour Rate Variance = (Actual Rate – Standard Rate) * Actual Hours

= (222750 – 60) * 7.5

= 1,670,175

Labour Efficiency Variance:

Formula:

Labour Efficiency Variance = (Actual hour – Standard hour) * Standard rate per hour

= (24750 – 7.5) * 60

= 1,484,550

Break-Even-Units (In Units):

BEP = Fixed cost / Contribution

4

= 160,000 / 4614

= 34.67 units or 35 units

Contribution Units = Sales units – variable units

= 4800 – 184

= 4616

Break-Even-Units (In Value):

BEP = Fixed cost / Contribution to sales ratio

= 160,000 / {(4800 - 184) / 4800}

= 160,000 / 0.96

= 166,666.66

D2. Produce financial report that apply & interpreted within organizational process

While using the marginal or absorption costing approach to measure the price of the product,

it would provide reliable costs that enable the manager build more cost tracking & management

plan for the business production cycle. Such data helps accountants prepare financial reports for

both different stakeholders. All the pertinent information that helps managers in their decision -

making processes is included in the financial statement. The internal operating mechanism can

be changed to further boost performance or performance.

TASK 3

P4. Explanation of the advantages and disadvantages of different types of planning tools used for

budgetary control

Explain the budgetary control:

It is a budgetary terminology for controlling revenue and expenditure. In practice, it

means contrasting the real income or spending on a regular basis with the expected revenue or

expenses to assess whether or not appropriate action is needed (Carlsson-Wall, Kraus and Lind,

2015). It is the method of determining the different real outcomes with the company's actual

spending for future duration and the expectations set, if any, by contrasting the planned results

with the actual output for measuring the variances. The budget is a means, and budgetary control

is the end product. With the help of several type of budget, management accountant of Crest

Dairy prepare operational budget as per requirement and maintain control over it. There are

several types of budgets, but before implementing into their business, it is very essential to

5

= 34.67 units or 35 units

Contribution Units = Sales units – variable units

= 4800 – 184

= 4616

Break-Even-Units (In Value):

BEP = Fixed cost / Contribution to sales ratio

= 160,000 / {(4800 - 184) / 4800}

= 160,000 / 0.96

= 166,666.66

D2. Produce financial report that apply & interpreted within organizational process

While using the marginal or absorption costing approach to measure the price of the product,

it would provide reliable costs that enable the manager build more cost tracking & management

plan for the business production cycle. Such data helps accountants prepare financial reports for

both different stakeholders. All the pertinent information that helps managers in their decision -

making processes is included in the financial statement. The internal operating mechanism can

be changed to further boost performance or performance.

TASK 3

P4. Explanation of the advantages and disadvantages of different types of planning tools used for

budgetary control

Explain the budgetary control:

It is a budgetary terminology for controlling revenue and expenditure. In practice, it

means contrasting the real income or spending on a regular basis with the expected revenue or

expenses to assess whether or not appropriate action is needed (Carlsson-Wall, Kraus and Lind,

2015). It is the method of determining the different real outcomes with the company's actual

spending for future duration and the expectations set, if any, by contrasting the planned results

with the actual output for measuring the variances. The budget is a means, and budgetary control

is the end product. With the help of several type of budget, management accountant of Crest

Dairy prepare operational budget as per requirement and maintain control over it. There are

several types of budgets, but before implementing into their business, it is very essential to

5

identify its advantages or disadvantages which help in better decision to adopt. These are

discussed below:

Budget: It refers to the design, execution and annual budgets process. Budgeting as a

management mechanism sets out a plan to ensure that perhaps the real operations of the company

are less deviated from scheduled activities. The budgets can be used to provide a summary of the

company and its activities. The budget encourages the effective distribution of finite resources

though that the budget controls amount of goods and services to be generated. The budget is also

used to manage cost of production generated. Budgets may be called on others to play a number

of roles. Three are key roles, such as planning, encouragement and assessment, and the other two

are minor ones, such as teamwork and education. Budget allows manager to identify decisions

about how to generate, where and how to produce, the amount or quantities of the goods to be

manufactured each day, week, month or annually. The Crest Dairy can also use budgets

as budgetary control tool to measure and benchmark the effectiveness of business division in a

major business or the entire performance of a small business. They may also use budgets to

assess different projects. It has some advantages or disadvantages which are as follow:

Advantages: Planning orientation is the process of making a budget that removes

administration in its short-term, day-to-day operations and encourages it to consider long

term (Gunarathne and Lee, 2015). This really is the key objective of budget, even if

planning is not effective in achieving its targets as described throughout the budget-at

least thought about strategic and financial situation of the firm and how to strengthen it.

Profitability examination is the simple way to lose focus of where an organisation is

producing almost all of its money throughout the day-to-day market. A well organised

budget shows the areas of business generate money but which aspects use it, which

allows the company to decide whether certain aspects of company can be sacrificed or

expanded to others. It requires management to understand why organisation is in

operation, and its main assumptions about its business climate. Periodic reassessment of

such issues may lead to a shift in assumptions that may, in turn, change the way

management chooses to work.

Disadvantages: Basically budget is associated with a set of assumptions which are

usually not that far from operational conditions by which it was developed. If the market

environment dramatically changes, the sales or cost structure of an organization will shift

6

discussed below:

Budget: It refers to the design, execution and annual budgets process. Budgeting as a

management mechanism sets out a plan to ensure that perhaps the real operations of the company

are less deviated from scheduled activities. The budgets can be used to provide a summary of the

company and its activities. The budget encourages the effective distribution of finite resources

though that the budget controls amount of goods and services to be generated. The budget is also

used to manage cost of production generated. Budgets may be called on others to play a number

of roles. Three are key roles, such as planning, encouragement and assessment, and the other two

are minor ones, such as teamwork and education. Budget allows manager to identify decisions

about how to generate, where and how to produce, the amount or quantities of the goods to be

manufactured each day, week, month or annually. The Crest Dairy can also use budgets

as budgetary control tool to measure and benchmark the effectiveness of business division in a

major business or the entire performance of a small business. They may also use budgets to

assess different projects. It has some advantages or disadvantages which are as follow:

Advantages: Planning orientation is the process of making a budget that removes

administration in its short-term, day-to-day operations and encourages it to consider long

term (Gunarathne and Lee, 2015). This really is the key objective of budget, even if

planning is not effective in achieving its targets as described throughout the budget-at

least thought about strategic and financial situation of the firm and how to strengthen it.

Profitability examination is the simple way to lose focus of where an organisation is

producing almost all of its money throughout the day-to-day market. A well organised

budget shows the areas of business generate money but which aspects use it, which

allows the company to decide whether certain aspects of company can be sacrificed or

expanded to others. It requires management to understand why organisation is in

operation, and its main assumptions about its business climate. Periodic reassessment of

such issues may lead to a shift in assumptions that may, in turn, change the way

management chooses to work.

Disadvantages: Basically budget is associated with a set of assumptions which are

usually not that far from operational conditions by which it was developed. If the market

environment dramatically changes, the sales or cost structure of an organization will shift

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

so drastically that actual outcomes may quickly deviate from targets set out in budget.

This situation is a great concern whenever there is a significant economic downturn, as

the budget provides for a certain amount of expenditure which is no longer eligible

underneath a suddenly reduced amount of profitability. Unless management needs

quickly to circumvent the budget, administrators will keep spending on the basis of their

original budgetary authorisations, breaking down any chance of making a profit. The

budgetary control only focused the team's attention mostly on plan during the budget

planning stage at end of year. There is also no formal obligation to revise the plan for the

remainder of the year.

Variance analysis: It is a variation in actual activity from forecast or anticipated activity in

budget or management accounting. That's also mainly worried with how the disparity between

real and expected behaviours shows how market output is affected. Measuring and analysing

variances will help track costs and control costs and increase operating performance. It's being

used to evaluate the explanations for the financial results variations from the expectations set by

company in its budget (Klychova, Faskhutdinova and Sadrieva, 2014). It allows the management

to retain control over its operational efficiency. This planning tool can be used by the Crest Dairy

as a budgetary control tool, so before adopting this tool management should analyse its

advantages and disadvantages which are as follow:

Advantages: The first advantage of variance is indication of deviation from norm or

predicted. This dismissal would give management focus to the investigation.

Management shall obtain relevant facts for this departure, in particular for adverse

departures or variances where costs are more than anticipated. A further benefit of

variance has been its role in managing expenditure. Management shall take reasonable

control measures in the event of adverse variance. During the first place, the cause of

unfavourable variance shall be investigated, where adequate explanations are not given,

and appropriate measures shall be taken. Future modification of budget projections where

there is no reasonable explanation for deviation other than an inaccurate budget estimate,

the budgeted estimate for the future shall be adjusted or updated.

Disadvantages: Variance analysis is focused on financial statements, which are

published far later since quarter closure; there could be a time delay that may have an

effect on the corrective action taken to that degree (Melnyk and et.al., 2014). Not all

7

This situation is a great concern whenever there is a significant economic downturn, as

the budget provides for a certain amount of expenditure which is no longer eligible

underneath a suddenly reduced amount of profitability. Unless management needs

quickly to circumvent the budget, administrators will keep spending on the basis of their

original budgetary authorisations, breaking down any chance of making a profit. The

budgetary control only focused the team's attention mostly on plan during the budget

planning stage at end of year. There is also no formal obligation to revise the plan for the

remainder of the year.

Variance analysis: It is a variation in actual activity from forecast or anticipated activity in

budget or management accounting. That's also mainly worried with how the disparity between

real and expected behaviours shows how market output is affected. Measuring and analysing

variances will help track costs and control costs and increase operating performance. It's being

used to evaluate the explanations for the financial results variations from the expectations set by

company in its budget (Klychova, Faskhutdinova and Sadrieva, 2014). It allows the management

to retain control over its operational efficiency. This planning tool can be used by the Crest Dairy

as a budgetary control tool, so before adopting this tool management should analyse its

advantages and disadvantages which are as follow:

Advantages: The first advantage of variance is indication of deviation from norm or

predicted. This dismissal would give management focus to the investigation.

Management shall obtain relevant facts for this departure, in particular for adverse

departures or variances where costs are more than anticipated. A further benefit of

variance has been its role in managing expenditure. Management shall take reasonable

control measures in the event of adverse variance. During the first place, the cause of

unfavourable variance shall be investigated, where adequate explanations are not given,

and appropriate measures shall be taken. Future modification of budget projections where

there is no reasonable explanation for deviation other than an inaccurate budget estimate,

the budgeted estimate for the future shall be adjusted or updated.

Disadvantages: Variance analysis is focused on financial statements, which are

published far later since quarter closure; there could be a time delay that may have an

effect on the corrective action taken to that degree (Melnyk and et.al., 2014). Not all

7

causes of variation can also be included in financial data that makes it difficult to act on

variances. If the budgetary control is not carried out, taking into account the thorough

examination of each aspect, budgetary exercise may well be carried out loosely, which is

required to differ from actual figures. After this examination of variances, that might not

be a useful practise. The downside of variation is it is not easy to understand. Users of

variance also use it specifically to consider the square root of the value, which means the

standard deviation of data collection.

Responsibility Center: It is an administrative unit or agency inside an organisation that is

responsible for operations and tasks organised for that particular unit. These centres have their

very own goals, personnel, goals, practices and processes and financial reports. They are being

used to balance the obligations relating to the expenditures incurred, the profits generated and

money spent to the individual. In a large or multinational company, such as Crest Dairy, the

activities of the organisation are divided into sub-tasks but each task is also allocated to a number

of small divisions or classes. In this sense, all groups within the organisation are

responsible centers. This budgetary tool can be used by the Crest Dairy for the budget control in

their business operations. But, before that manager has to evaluate its advantages or

disadvantages those are discussed below:

Advantages: Responsibility assigned to each part, each and every person is associated

and guided towards a target of responsibility which is compatible with the roles. The

person or agency will be monitored, and no one can transfer the blame to someone else,

assuming that something goes wrong (Mistry, Sharma and Low, 2014). The concept of

having to delegate tasks and duties to a single individual will have to serve as a

motivating force. Realizing that the success will be monitored and submitted to the upper

executives, the divisions and stakeholders will do their best to make it happen on their

greatest result. Responsibility centres support decision-making management, as the

knowledge distributed and gathered from multiple centres allows them to prepare all of

their potential actions. It lets them recognize the segment-wise breakdown of sales,

expenses, problems, future action plans, etc.

Disadvantages: There may have been a risk related to conflict of interest among the

individual and organisation. A salesperson may attempt to force selling in such restricted

areas to raise the profits listed under their obligation centre, while the management does

8

variances. If the budgetary control is not carried out, taking into account the thorough

examination of each aspect, budgetary exercise may well be carried out loosely, which is

required to differ from actual figures. After this examination of variances, that might not

be a useful practise. The downside of variation is it is not easy to understand. Users of

variance also use it specifically to consider the square root of the value, which means the

standard deviation of data collection.

Responsibility Center: It is an administrative unit or agency inside an organisation that is

responsible for operations and tasks organised for that particular unit. These centres have their

very own goals, personnel, goals, practices and processes and financial reports. They are being

used to balance the obligations relating to the expenditures incurred, the profits generated and

money spent to the individual. In a large or multinational company, such as Crest Dairy, the

activities of the organisation are divided into sub-tasks but each task is also allocated to a number

of small divisions or classes. In this sense, all groups within the organisation are

responsible centers. This budgetary tool can be used by the Crest Dairy for the budget control in

their business operations. But, before that manager has to evaluate its advantages or

disadvantages those are discussed below:

Advantages: Responsibility assigned to each part, each and every person is associated

and guided towards a target of responsibility which is compatible with the roles. The

person or agency will be monitored, and no one can transfer the blame to someone else,

assuming that something goes wrong (Mistry, Sharma and Low, 2014). The concept of

having to delegate tasks and duties to a single individual will have to serve as a

motivating force. Realizing that the success will be monitored and submitted to the upper

executives, the divisions and stakeholders will do their best to make it happen on their

greatest result. Responsibility centres support decision-making management, as the

knowledge distributed and gathered from multiple centres allows them to prepare all of

their potential actions. It lets them recognize the segment-wise breakdown of sales,

expenses, problems, future action plans, etc.

Disadvantages: There may have been a risk related to conflict of interest among the

individual and organisation. A salesperson may attempt to force selling in such restricted

areas to raise the profits listed under their obligation centre, while the management does

8

have its rule prohibited the same. This method needs a significant time and resources

on part of the administration to thoroughly prepare and follow the necessary plan of

action. If something goes wrong throughout the planning process, the whole process is

destined for failure and will be nothing but a disaster waiting to happen. The delay in

such a system is that it might be too process-oriented to concentrate on division and

assignment of duty to different segments. There is also so much time, attention and

emphasis on such acts.

Above discussed planning tool which can be used by the Crest Dairy for budgetary control

and it helps the managers to estimate overall income and expenses on the basis of specific tool. It

also helps in making operational or strategic decisions which further helps in improving

productivity as well as profitability.

M3. Analyse the use of different planning tools and their application for preparing and

forecasting budgets

Above discussed planning tools are used for budgetary control which helps the

management of Crest Dairy for forecasting their budget and ensure that estimation should be

accurate which provide better results (Nielsen, Mitchell and Nørreklit, 2015). By using variance

analysis, managers are able to revaluate the difference and also evaluate that how it affect the

business operations and financial performance. On the other side, budget is useful for planning,

prediction and it is easy to understand and further managers used in decision making process.

TASK 4

P5. Evaluate that how organisations are adapting management accounting systems to respond to

financial problems

Financial issues: It is the financial burden that causes a situation where organisation and

owners are depressed and faced with hard times due to a lack of capital. In relation to the

business and objectives of market, they must carry out an analysis of the business in order to

determine the financial issues that impact productivity as well as profitability. Some of Crest

Dairy's financial problems have been listed below:

Unforeseen Expenditures: There are many costs in company that unexpectedly emerge

and there are general financial difficulties. So the company's administrators have to control their

financial resources to try to reduce them.

9

on part of the administration to thoroughly prepare and follow the necessary plan of

action. If something goes wrong throughout the planning process, the whole process is

destined for failure and will be nothing but a disaster waiting to happen. The delay in

such a system is that it might be too process-oriented to concentrate on division and

assignment of duty to different segments. There is also so much time, attention and

emphasis on such acts.

Above discussed planning tool which can be used by the Crest Dairy for budgetary control

and it helps the managers to estimate overall income and expenses on the basis of specific tool. It

also helps in making operational or strategic decisions which further helps in improving

productivity as well as profitability.

M3. Analyse the use of different planning tools and their application for preparing and

forecasting budgets

Above discussed planning tools are used for budgetary control which helps the

management of Crest Dairy for forecasting their budget and ensure that estimation should be

accurate which provide better results (Nielsen, Mitchell and Nørreklit, 2015). By using variance

analysis, managers are able to revaluate the difference and also evaluate that how it affect the

business operations and financial performance. On the other side, budget is useful for planning,

prediction and it is easy to understand and further managers used in decision making process.

TASK 4

P5. Evaluate that how organisations are adapting management accounting systems to respond to

financial problems

Financial issues: It is the financial burden that causes a situation where organisation and

owners are depressed and faced with hard times due to a lack of capital. In relation to the

business and objectives of market, they must carry out an analysis of the business in order to

determine the financial issues that impact productivity as well as profitability. Some of Crest

Dairy's financial problems have been listed below:

Unforeseen Expenditures: There are many costs in company that unexpectedly emerge

and there are general financial difficulties. So the company's administrators have to control their

financial resources to try to reduce them.

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Late Payment by Suppliers: All companies must negotiate with or sustain a long-term

partnership with Suppliers (Quinn and Jackson, 2014). They therefore have to negotiate with

vendors on a credit basis to increase profits. Almost all of the time, it has occurred that creditors

are unable to pay the sum on time and also that the company is faced with a shortage of

monetary capital.

Management accounting techniques:

Key Performance Indicator (KPI): It is a measuring instrument that helps the company

assesses its progress on the basis of a variety of metrics. There are generally two types of key

metrics, such as monetary or non - monetary. With the aid of financial KPI, Crest Dairy

managers establish unpredictable and non-financial costs used to recognize flaws in business

processes. Using this strategy, the managers of AstraZeneca Plc address the financial dilemma of

unexpected expenditures.

Benchmarking: This is the competitive methods that company has used to equate its

results to the leaders in the market (Strauss, Kristandl and Quinn, 2015). With the aid of this

strategy, managers are able to recognise areas for change. In Crest Dairy, managers define the

issue of late payment of suppliers by contrasting it with their credit policy. It allows managers to

create an effective plan to solve these problems.

Financial governance: It refers to the different laws and regulations to be enforced by the

company. This includes how companies can monitor their financial status, the productivity of

management, control data, compliance, etc. Throughout the Crest Dairy, the corporation faces

financial challenges in order to guarantee that the enterprise meets fundamental principles or not.

At the time of documenting financial reports, different principles or criteria must be followed.

Comparison of two organizations:

Basis Crest Dairy Creams Ltd

Management

accounting system

In order to overcome unforeseen

costs, Crest Dairy’s manager

implemented the cost

management system (Van der

Stede, 2015). They can define the

cost per unit with the help of it.

Business shall track operating

The business used the price

optimization system to define

customer behaviour in relation to

cost of the commodity. With the aid

of this, managers can overcome the

problem of late payments from

distributors. But they've decided to

10

partnership with Suppliers (Quinn and Jackson, 2014). They therefore have to negotiate with

vendors on a credit basis to increase profits. Almost all of the time, it has occurred that creditors

are unable to pay the sum on time and also that the company is faced with a shortage of

monetary capital.

Management accounting techniques:

Key Performance Indicator (KPI): It is a measuring instrument that helps the company

assesses its progress on the basis of a variety of metrics. There are generally two types of key

metrics, such as monetary or non - monetary. With the aid of financial KPI, Crest Dairy

managers establish unpredictable and non-financial costs used to recognize flaws in business

processes. Using this strategy, the managers of AstraZeneca Plc address the financial dilemma of

unexpected expenditures.

Benchmarking: This is the competitive methods that company has used to equate its

results to the leaders in the market (Strauss, Kristandl and Quinn, 2015). With the aid of this

strategy, managers are able to recognise areas for change. In Crest Dairy, managers define the

issue of late payment of suppliers by contrasting it with their credit policy. It allows managers to

create an effective plan to solve these problems.

Financial governance: It refers to the different laws and regulations to be enforced by the

company. This includes how companies can monitor their financial status, the productivity of

management, control data, compliance, etc. Throughout the Crest Dairy, the corporation faces

financial challenges in order to guarantee that the enterprise meets fundamental principles or not.

At the time of documenting financial reports, different principles or criteria must be followed.

Comparison of two organizations:

Basis Crest Dairy Creams Ltd

Management

accounting system

In order to overcome unforeseen

costs, Crest Dairy’s manager

implemented the cost

management system (Van der

Stede, 2015). They can define the

cost per unit with the help of it.

Business shall track operating

The business used the price

optimization system to define

customer behaviour in relation to

cost of the commodity. With the aid

of this, managers can overcome the

problem of late payments from

distributors. But they've decided to

10

activities on a daily basis to detect

additional issues.

make their pricing structure more

competitive so they don't ask for

credit.

Management

accounting

technique

In order to resolve above financial

issues, Crest Dairy adopts KPI

technique which helps the

managers to evaluate valuable or

non-valuable activities and try to

eliminate non-profitable activities

to minimise cost or maximise profit

margin.

In the Creams Ltd, manager

implement benchmarking technique

to compare their current

performance with previous one and

identify the reason and make sure

that overall performance should be

increases.

M4. Analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success

There are different forms of financial problems facing Crest Dairy organisations, such as

delayed in payment from suppliers and unexpected expenditures. By using different methods,

such as the Key Performance Indicator (KPI) and benchmarking, the organisation is helping to

address its financial issues. In addition, administrators often ensure that businesses obey risk

management or not because they'll have to report their details to stakeholders. They will ensure

that certain accounting concepts are practised or not.

D3. Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success

It is analysed critically that various forms of budget support managers to address their

financial issues (Wagenhofer, 2016). With the aid of the budget, managers are able to determine

each product that solves the unexpected cost issue or late payment from suppliers. By evaluating

each product cost, manager of the organisation able to determine which behaviour is essential to

the operations. These preparation tools help Crest Dairy address its financial challenges that

ensure sustainable progress in the company.

11

additional issues.

make their pricing structure more

competitive so they don't ask for

credit.

Management

accounting

technique

In order to resolve above financial

issues, Crest Dairy adopts KPI

technique which helps the

managers to evaluate valuable or

non-valuable activities and try to

eliminate non-profitable activities

to minimise cost or maximise profit

margin.

In the Creams Ltd, manager

implement benchmarking technique

to compare their current

performance with previous one and

identify the reason and make sure

that overall performance should be

increases.

M4. Analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success

There are different forms of financial problems facing Crest Dairy organisations, such as

delayed in payment from suppliers and unexpected expenditures. By using different methods,

such as the Key Performance Indicator (KPI) and benchmarking, the organisation is helping to

address its financial issues. In addition, administrators often ensure that businesses obey risk

management or not because they'll have to report their details to stakeholders. They will ensure

that certain accounting concepts are practised or not.

D3. Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success

It is analysed critically that various forms of budget support managers to address their

financial issues (Wagenhofer, 2016). With the aid of the budget, managers are able to determine

each product that solves the unexpected cost issue or late payment from suppliers. By evaluating

each product cost, manager of the organisation able to determine which behaviour is essential to

the operations. These preparation tools help Crest Dairy address its financial challenges that

ensure sustainable progress in the company.

11

CONCLUSION

It has been inferred from the above analysis that management accounting is the method that

any corporation has to know in order to coordinate their business processes and other internal

stakeholders. In order to optimize organizational performance and also productivity, there are

different accounting systems and reports used by the company's managers. It also helps

executives to make strategic decisions to meet corporate priorities and goals. It supports and

works appropriately with both the help of preparation instruments including the budget and

variance analysis. Companies have to face several financial challenges and strive to reduce them

through using different strategies, such as KPI, benchmarking and financial governance.

12

It has been inferred from the above analysis that management accounting is the method that

any corporation has to know in order to coordinate their business processes and other internal

stakeholders. In order to optimize organizational performance and also productivity, there are

different accounting systems and reports used by the company's managers. It also helps

executives to make strategic decisions to meet corporate priorities and goals. It supports and

works appropriately with both the help of preparation instruments including the budget and

variance analysis. Companies have to face several financial challenges and strive to reduce them

through using different strategies, such as KPI, benchmarking and financial governance.

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books & Journals

Armitage, H. M., Webb, A. and Glynn, J., 2016. The use of management accounting techniques

by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives. 15(1). pp.31-69.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Gunarathne, N. and Lee, K. H., 2015. Environmental Management Accounting (EMA) for

environmental management and organizational change: An eco-control

approach. Journal of Accounting & Organizational Change. 11(3). pp.362-383.

Klychova, G. S., Faskhutdinova, М. S. and Sadrieva, E. R., 2014. Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences. 5(24). p.79.

Melnyk, S. A. and et.al., 2014. Is performance measurement and management fit for the

future?. Management Accounting Research. 25(2). pp.173-186.

Mistry, V., Sharma, U. and Low, M., 2014. Management accountants' perception of their role in

accounting for sustainable development: An exploratory study. Pacific Accounting

Review. 26(1/2). pp.112-133.

Nielsen, L. B., Mitchell, F. and Nørreklit, H., 2015. March. Management accounting and

decision making: Two case studies of outsourcing. In Accounting Forum (Vol. 39, No.

1, pp. 66-82). Taylor & Francis.

Quinn, M. and Jackson, W. J., 2014. Accounting for war risk costs: Management accounting

change at Guinness during the First World War. Accounting History Review. 24(2-3).

pp.191-209.

Strauss, E., Kristandl, G. and Quinn, M., 2015. The effects of cloud technology on management

accounting and decision-making. Management and Financial Accounting Report. 10(6).

Van der Stede, W.A., 2015. Management accounting: Where from, where now, where

to?. Journal of Management Accounting Research. 27(1). pp.171-176.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in management

accounting. Management Accounting Research. 31. pp.112-117.

13

Books & Journals

Armitage, H. M., Webb, A. and Glynn, J., 2016. The use of management accounting techniques

by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives. 15(1). pp.31-69.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Gunarathne, N. and Lee, K. H., 2015. Environmental Management Accounting (EMA) for

environmental management and organizational change: An eco-control

approach. Journal of Accounting & Organizational Change. 11(3). pp.362-383.

Klychova, G. S., Faskhutdinova, М. S. and Sadrieva, E. R., 2014. Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences. 5(24). p.79.

Melnyk, S. A. and et.al., 2014. Is performance measurement and management fit for the

future?. Management Accounting Research. 25(2). pp.173-186.

Mistry, V., Sharma, U. and Low, M., 2014. Management accountants' perception of their role in

accounting for sustainable development: An exploratory study. Pacific Accounting

Review. 26(1/2). pp.112-133.

Nielsen, L. B., Mitchell, F. and Nørreklit, H., 2015. March. Management accounting and

decision making: Two case studies of outsourcing. In Accounting Forum (Vol. 39, No.

1, pp. 66-82). Taylor & Francis.

Quinn, M. and Jackson, W. J., 2014. Accounting for war risk costs: Management accounting

change at Guinness during the First World War. Accounting History Review. 24(2-3).

pp.191-209.

Strauss, E., Kristandl, G. and Quinn, M., 2015. The effects of cloud technology on management

accounting and decision-making. Management and Financial Accounting Report. 10(6).

Van der Stede, W.A., 2015. Management accounting: Where from, where now, where

to?. Journal of Management Accounting Research. 27(1). pp.171-176.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in management

accounting. Management Accounting Research. 31. pp.112-117.

13

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.