Management Accounting: Investment Appraisal at KingtonTech Ltd

VerifiedAdded on 2023/04/23

|14

|2866

|216

Report

AI Summary

This report presents a comprehensive analysis of investment appraisal techniques, using KingtonTech Ltd. as a case study. It begins with an introduction to management accounting and investment appraisal, followed by the calculation of Net Present Value (NPV) and Internal Rate of Return (IRR), with detailed calculations provided in the appendix. The report explores the limitations of these techniques and compares two approaches to capital budgeting decisions using discounted cash flow methods. Additional methods of investment appraisal, such as the payback period and accounting rate of return, are also discussed. The report further examines the significance of non-monetary aspects in investment decisions and outlines four key investment appraisal methods: NPV, IRR, payback period, and average rate of return. Finally, the report covers various pricing approaches, including competitor-based, cost-plus, and economist approaches, before concluding with recommendations for KingtonTech Ltd.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

A) Calculation of Net present value.......................................................................................1

B) Calculation of IRR.............................................................................................................1

C) Limitation of various techniques of proposed investments...............................................1

D) Comparison of two approaches to making capital budgeting decisions by means of

discounted cash flow..............................................................................................................2

E) Another two methods of investment appraisals.................................................................2

F) Can non-monetary aspects are useful to make various decisions related to the investment

projects...................................................................................................................................3

G) Four methods used in investment appraisals are...............................................................3

H) Various approaches to pricing...........................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

APPENDIX......................................................................................................................................7

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

A) Calculation of Net present value.......................................................................................1

B) Calculation of IRR.............................................................................................................1

C) Limitation of various techniques of proposed investments...............................................1

D) Comparison of two approaches to making capital budgeting decisions by means of

discounted cash flow..............................................................................................................2

E) Another two methods of investment appraisals.................................................................2

F) Can non-monetary aspects are useful to make various decisions related to the investment

projects...................................................................................................................................3

G) Four methods used in investment appraisals are...............................................................3

H) Various approaches to pricing...........................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

APPENDIX......................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the process of preparing various financial accounts and

reports in order to analyze the accurate and timely based financial and statistics data which are

required by managers to make day-to-day decisions in order to achieve the short term and long

term objectives of the company. Investment appraisal is a collection of various techniques that

are used to identify the attractiveness of investment. In this report, case study of KingtonTech

Ltd. has being used in order to calculate the NPV and IRR. In this report, two approaches are

compared to make various capital budgeting decisions. In this, methods of investment appraisals

are also discussed.

MAIN BODY

A) Calculation of Net present value

[Enclosed in appendix]

B) Calculation of IRR

[Enclosed in appendix]

C) Limitation of various techniques of proposed investments

The acceptability of proposed investment is that NPV is positive, thus it can be suggested

as a proposed investment in financial terms. In the above calculation, IRR is 16% and discounted

rate of return is only 12% which indicate that IRR is more as compared to discounted rate that is

used. Thus, proposed investment can be financially accepted (Carmichael, 2011). It can be said

that cash flow of the proposed investment in terms of Alpha is inevitable as there is only one

IRR. Therefore, limitation of investment in Alpha is that evaluation of IRR and NPV is highly

reliant on the production and sales volume. Thus, Kingston Tech Ltd. should analyze and

investigate the assumption that is underlying the production and sales volume. Thus one of the

main limitations of NPV is that it requires an estimated cost of capital in order to calculate Net

present Value and at the same time, cash flows should be in terms of dollars not in the term of

percentage. Likewise, the method of IRR cannot be used in a situation in which sign of the cash

flows of a project changes continuously.

1

Management accounting is the process of preparing various financial accounts and

reports in order to analyze the accurate and timely based financial and statistics data which are

required by managers to make day-to-day decisions in order to achieve the short term and long

term objectives of the company. Investment appraisal is a collection of various techniques that

are used to identify the attractiveness of investment. In this report, case study of KingtonTech

Ltd. has being used in order to calculate the NPV and IRR. In this report, two approaches are

compared to make various capital budgeting decisions. In this, methods of investment appraisals

are also discussed.

MAIN BODY

A) Calculation of Net present value

[Enclosed in appendix]

B) Calculation of IRR

[Enclosed in appendix]

C) Limitation of various techniques of proposed investments

The acceptability of proposed investment is that NPV is positive, thus it can be suggested

as a proposed investment in financial terms. In the above calculation, IRR is 16% and discounted

rate of return is only 12% which indicate that IRR is more as compared to discounted rate that is

used. Thus, proposed investment can be financially accepted (Carmichael, 2011). It can be said

that cash flow of the proposed investment in terms of Alpha is inevitable as there is only one

IRR. Therefore, limitation of investment in Alpha is that evaluation of IRR and NPV is highly

reliant on the production and sales volume. Thus, Kingston Tech Ltd. should analyze and

investigate the assumption that is underlying the production and sales volume. Thus one of the

main limitations of NPV is that it requires an estimated cost of capital in order to calculate Net

present Value and at the same time, cash flows should be in terms of dollars not in the term of

percentage. Likewise, the method of IRR cannot be used in a situation in which sign of the cash

flows of a project changes continuously.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D) Comparison of two approaches to making capital budgeting decisions by means of discounted

cash flow

The two approaches to make capital budgeting decisions by the means of discounted cash

flow are NPV and IRR. Company should make an efforts to select/accept the investment

proposal that gives positive NPV as it can increase the market value of company to the great

extent as per the increment in NPV. In order to increase the wealth of shareholders, companies

should always make effects to investment in the proposal which gives the positive NPV

(Garleanu and Pedersen, 2011). At the same time, in order to increase the wealth of shareholders,

Kingston Tech Ltd. can also accept the projects that have profitability IRR. The condition of

profitability IRR arises when IRR is higher than the uniform discounted rate. Technique of IRR

is used for making various necessary decisions for the management.

NPV at 20% -£92,387

NPV at 12% £91,154

IRR 15.97 16%

By taking into consideration, it could be concluded that Kingston Tech Ltd. should move

on with the NPV at 12% because it is given positive cash flow which in turn will aid company to

increase the shareholder’s wealth. At the same time, IRR at 16% should be selected in order to

achieve the profitability IRR.

E) Another two methods of investment appraisals

Another two methods of investment appraisals which management accountant can use are

payback period method and Accounting rate of return.

Pay Back Period Method is the method of analyzing the time period after that investment

made will be recovered back (Irani, 2010). This method will provide the manager of Kingston

Tech Ltd. an indication that how many year will take place in order to recover the original

investment cost. This method makes an allowance for the risk by focusing attention on the near

future term. The advantage of this method is that it helps to identify the project which is having

fastest return on investment made. This method is especially beneficial for the newly opened

firm in order to know the actual time frame for recovering the amount invested. However,

drawback of this method is that it does not consider the time value of money which in turn could

lead to wrong decision making. Furthermore, it ignores cash flows that occur after the payback

2

cash flow

The two approaches to make capital budgeting decisions by the means of discounted cash

flow are NPV and IRR. Company should make an efforts to select/accept the investment

proposal that gives positive NPV as it can increase the market value of company to the great

extent as per the increment in NPV. In order to increase the wealth of shareholders, companies

should always make effects to investment in the proposal which gives the positive NPV

(Garleanu and Pedersen, 2011). At the same time, in order to increase the wealth of shareholders,

Kingston Tech Ltd. can also accept the projects that have profitability IRR. The condition of

profitability IRR arises when IRR is higher than the uniform discounted rate. Technique of IRR

is used for making various necessary decisions for the management.

NPV at 20% -£92,387

NPV at 12% £91,154

IRR 15.97 16%

By taking into consideration, it could be concluded that Kingston Tech Ltd. should move

on with the NPV at 12% because it is given positive cash flow which in turn will aid company to

increase the shareholder’s wealth. At the same time, IRR at 16% should be selected in order to

achieve the profitability IRR.

E) Another two methods of investment appraisals

Another two methods of investment appraisals which management accountant can use are

payback period method and Accounting rate of return.

Pay Back Period Method is the method of analyzing the time period after that investment

made will be recovered back (Irani, 2010). This method will provide the manager of Kingston

Tech Ltd. an indication that how many year will take place in order to recover the original

investment cost. This method makes an allowance for the risk by focusing attention on the near

future term. The advantage of this method is that it helps to identify the project which is having

fastest return on investment made. This method is especially beneficial for the newly opened

firm in order to know the actual time frame for recovering the amount invested. However,

drawback of this method is that it does not consider the time value of money which in turn could

lead to wrong decision making. Furthermore, it ignores cash flows that occur after the payback

2

period which indicates that there is the possibility of ignoring the complete return which a

project can generate.

Likewise, on the other hand Average Rate of Return is the percentage of average

accounting profit that is earned over the average accounting value of investment earned (Kaplan

and Atkinson, 2015). This method normally focuses on the accounting profit generated than that

of cash flows. The approach of this method is to estimate revenues that will be generated by a

proposed investment and then, deducting all the projected operating expenses that are associated

with the project. Advantage of this method is that it uses the entire streams of net operating

income which in turn assists investors and creditors to evaluate the performance of business.

Moreover, there is also a drawback of this method. This method ignores the time value of money

which is a major decision factor which aids company in taking various financial decisions

F) Can non-monetary aspects are useful to make various decisions related to the investment

projects

It is true that all monetary aspects are important and beneficial in order to find out the

best investment proposal/ project. There is no doubt that these methods aid investors to analyze

the time period after which they are able to recover the particular amount of money invested.

But, all the time, decisions taken on these basis are not correct (Lukka and Modell, 2010).

Meanwhile, it could also be concluded that only by using various monetary aspects for making

investment decision is not a right way. Investment decisions should be made by taking into

consideration both the monetary and non-monetary aspects. Monetary aspects include various

methods of capital budgeting like Payback period, IRR, NPV, ARR and many more. Similarly,

non-monetary aspects includes various internal and external factors that are available in the

environment. These factors could be identified by conducting SWOT or PESTLE analysis or by

using various relevant models. Thus, at last, it suggests that in order to take correct decisions,

Kingston Tech Ltd. should undertake both the monetary and non-monetary aspects. This in turn

will aid company to properly found the time period after which they are able to recover the

invested amount.

G) Four methods used in investment appraisals are

Out of the four investment appraisal methods, company can use more than one method at

a time. These four methods (i.e. NPV, IRR, ARR and Pay Back period) contribute towards the

broader understanding of the investment projects. These methods also assist company to rank

3

project can generate.

Likewise, on the other hand Average Rate of Return is the percentage of average

accounting profit that is earned over the average accounting value of investment earned (Kaplan

and Atkinson, 2015). This method normally focuses on the accounting profit generated than that

of cash flows. The approach of this method is to estimate revenues that will be generated by a

proposed investment and then, deducting all the projected operating expenses that are associated

with the project. Advantage of this method is that it uses the entire streams of net operating

income which in turn assists investors and creditors to evaluate the performance of business.

Moreover, there is also a drawback of this method. This method ignores the time value of money

which is a major decision factor which aids company in taking various financial decisions

F) Can non-monetary aspects are useful to make various decisions related to the investment

projects

It is true that all monetary aspects are important and beneficial in order to find out the

best investment proposal/ project. There is no doubt that these methods aid investors to analyze

the time period after which they are able to recover the particular amount of money invested.

But, all the time, decisions taken on these basis are not correct (Lukka and Modell, 2010).

Meanwhile, it could also be concluded that only by using various monetary aspects for making

investment decision is not a right way. Investment decisions should be made by taking into

consideration both the monetary and non-monetary aspects. Monetary aspects include various

methods of capital budgeting like Payback period, IRR, NPV, ARR and many more. Similarly,

non-monetary aspects includes various internal and external factors that are available in the

environment. These factors could be identified by conducting SWOT or PESTLE analysis or by

using various relevant models. Thus, at last, it suggests that in order to take correct decisions,

Kingston Tech Ltd. should undertake both the monetary and non-monetary aspects. This in turn

will aid company to properly found the time period after which they are able to recover the

invested amount.

G) Four methods used in investment appraisals are

Out of the four investment appraisal methods, company can use more than one method at

a time. These four methods (i.e. NPV, IRR, ARR and Pay Back period) contribute towards the

broader understanding of the investment projects. These methods also assist company to rank

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

various investment that can be made according to their optimality and efficiency of return in

order to select the best investment proposal.

But, at the same time, it cannot be ignored that each of the methods has its own risk

factors and different methods are suitable for the different type of business organization. Features

of different types of methods are as follow:- Net Present Value: - NPV takes into account the size, risk factor and timing of the future

cash flow which in turn aid managers to determine the viability on the cost of capital of

the company based on the selected project (Maharjan, Zhang and Gjessing, 2011). Internal Rate of Return: - IRR takes the cash flows of investment projects into account

along with the time value of money (Otley, 1999). This method will aid manager to

decide and analyze whether the selected investment proposal/ project is profitable from

the company’s point of view or it will increase the cost of company. Moreover, this

method can be considered as one of the best methods for ranking projects. Pay Back period: - This method reduces the cost of company due to its simplicity. At the

same time, this method will aid company to analyze the number of years when it is able

to recover the amount of money investment (Willcocks, 2013).

Average Rate of Return: - ARR does not take into account the concept of time value of

money. This method is used by company in order to calculate the return earned out of the

net income generated from the proposed capital investment (Zimmerman and Yahya-

Zadeh, 2011).

Furthermore, it is analyzed that using more than one method of investment appraisals

reduces the risk involved and at the same time, decreases the chance of discrepancy

between actual and budgeted revenue. Sum of methods also reduces the cost of project.

Henceforth, after analyzing all the four methods of investment appraisals, it could be

concluded that NPV is one of the suitable methods for the long term investment. Thus, on the

other hand, it could be concluded that Pay Back period is suitable for analyzing the short term

investment.

H) Various approaches to pricing

There are three main approaches which Kingston Tech Ltd. can consider (i.e. competitor

based approach, economist approach and cost plus pricing approach).

4

order to select the best investment proposal.

But, at the same time, it cannot be ignored that each of the methods has its own risk

factors and different methods are suitable for the different type of business organization. Features

of different types of methods are as follow:- Net Present Value: - NPV takes into account the size, risk factor and timing of the future

cash flow which in turn aid managers to determine the viability on the cost of capital of

the company based on the selected project (Maharjan, Zhang and Gjessing, 2011). Internal Rate of Return: - IRR takes the cash flows of investment projects into account

along with the time value of money (Otley, 1999). This method will aid manager to

decide and analyze whether the selected investment proposal/ project is profitable from

the company’s point of view or it will increase the cost of company. Moreover, this

method can be considered as one of the best methods for ranking projects. Pay Back period: - This method reduces the cost of company due to its simplicity. At the

same time, this method will aid company to analyze the number of years when it is able

to recover the amount of money investment (Willcocks, 2013).

Average Rate of Return: - ARR does not take into account the concept of time value of

money. This method is used by company in order to calculate the return earned out of the

net income generated from the proposed capital investment (Zimmerman and Yahya-

Zadeh, 2011).

Furthermore, it is analyzed that using more than one method of investment appraisals

reduces the risk involved and at the same time, decreases the chance of discrepancy

between actual and budgeted revenue. Sum of methods also reduces the cost of project.

Henceforth, after analyzing all the four methods of investment appraisals, it could be

concluded that NPV is one of the suitable methods for the long term investment. Thus, on the

other hand, it could be concluded that Pay Back period is suitable for analyzing the short term

investment.

H) Various approaches to pricing

There are three main approaches which Kingston Tech Ltd. can consider (i.e. competitor

based approach, economist approach and cost plus pricing approach).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Competitor based pricing approach: - It is one of the effective pricing methods in which

seller considers the price of competitors as a benchmark for setting its own prices. Main

advantage of this method is that it helps company to set their prices in a competitive

manner (Andor, Mohanty and Toth, 2011). But, on the other hand, drawbacks of the

approach cannot be ignored, this is a very time consuming approach and competitors are

also able to change its price easily.

Cost plus pricing approach: - In this method, markup is applied to the base cost in order

to determine the targeted selling price. This method will assist Kingston Tech Ltd. to

easily identify the amount of expenditure that is incurred by the company at the time of

manufacturing goods.

According to me, most suitable pricing method for Kingston Tech Ltd. is the cost plus

pricing approach because this method will reduce the risk as well as uncertainty and at the same

time, it assures company to make profit since its cost are reimbursed so it will initially make

profit and there is no risk of losses.

CONCLUSION

From the following report, it could be concluded that Net Present value is one of the best

methods for analyzing the long term investment and payback period method will be beneficial

for meeting the short term investments. At last, it can also be said that out of the three selected

approaches, Cost plus approach is one of the best approaches for the Kingston Tech Ltd.

5

seller considers the price of competitors as a benchmark for setting its own prices. Main

advantage of this method is that it helps company to set their prices in a competitive

manner (Andor, Mohanty and Toth, 2011). But, on the other hand, drawbacks of the

approach cannot be ignored, this is a very time consuming approach and competitors are

also able to change its price easily.

Cost plus pricing approach: - In this method, markup is applied to the base cost in order

to determine the targeted selling price. This method will assist Kingston Tech Ltd. to

easily identify the amount of expenditure that is incurred by the company at the time of

manufacturing goods.

According to me, most suitable pricing method for Kingston Tech Ltd. is the cost plus

pricing approach because this method will reduce the risk as well as uncertainty and at the same

time, it assures company to make profit since its cost are reimbursed so it will initially make

profit and there is no risk of losses.

CONCLUSION

From the following report, it could be concluded that Net Present value is one of the best

methods for analyzing the long term investment and payback period method will be beneficial

for meeting the short term investments. At last, it can also be said that out of the three selected

approaches, Cost plus approach is one of the best approaches for the Kingston Tech Ltd.

5

REFERENCES

Books and Journals

Carmichael, D. G., 2011. An alternative approach to capital investment appraisal. The

Engineering Economist. 56(2). pp.123-139.

Garleanu, N. and Pedersen, L. H., 2011. Margin-based asset pricing and deviations from the law

of one price. Review of Financial Studies, p.hhr027.

Irani, Z., 2010. Investment evaluation within project management: an information systems

perspective. Journal of the Operational Research Society. 61(6). pp.917-928.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Lukka, K. and Modell, S., 2010. Validation in interpretive management accounting research.

Accounting, Organizations and Society. 35(4). pp.462-477.

Maharjan, S., Zhang, Y. and Gjessing, S., 2011. Economic approaches for cognitive radio

networks: A survey. Wireless Personal Communications. 57(1). pp.33-51.

Otley, D., 1999. Performance management: a framework for management control systems

research. Management accounting research. 10(4). pp.363-382.

Willcocks, L., 2013. Information management: the evaluation of information systems

investments. Springer.

Zimmerman, J. L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control.

Issues in Accounting Education. 26(1). pp.258-259.

Online

Andor, G., Mohanty, S.K. and Toth, T., 2011. Capital Budgeting Practices: A Survey of Central

and Eastern European Firms. Available

through:<http://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL

%20MEETINGS/2011-Braga/papers/0118.pdf>[Assessed on 30th December, 2015].

6

Books and Journals

Carmichael, D. G., 2011. An alternative approach to capital investment appraisal. The

Engineering Economist. 56(2). pp.123-139.

Garleanu, N. and Pedersen, L. H., 2011. Margin-based asset pricing and deviations from the law

of one price. Review of Financial Studies, p.hhr027.

Irani, Z., 2010. Investment evaluation within project management: an information systems

perspective. Journal of the Operational Research Society. 61(6). pp.917-928.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Lukka, K. and Modell, S., 2010. Validation in interpretive management accounting research.

Accounting, Organizations and Society. 35(4). pp.462-477.

Maharjan, S., Zhang, Y. and Gjessing, S., 2011. Economic approaches for cognitive radio

networks: A survey. Wireless Personal Communications. 57(1). pp.33-51.

Otley, D., 1999. Performance management: a framework for management control systems

research. Management accounting research. 10(4). pp.363-382.

Willcocks, L., 2013. Information management: the evaluation of information systems

investments. Springer.

Zimmerman, J. L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control.

Issues in Accounting Education. 26(1). pp.258-259.

Online

Andor, G., Mohanty, S.K. and Toth, T., 2011. Capital Budgeting Practices: A Survey of Central

and Eastern European Firms. Available

through:<http://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL

%20MEETINGS/2011-Braga/papers/0118.pdf>[Assessed on 30th December, 2015].

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPENDIX

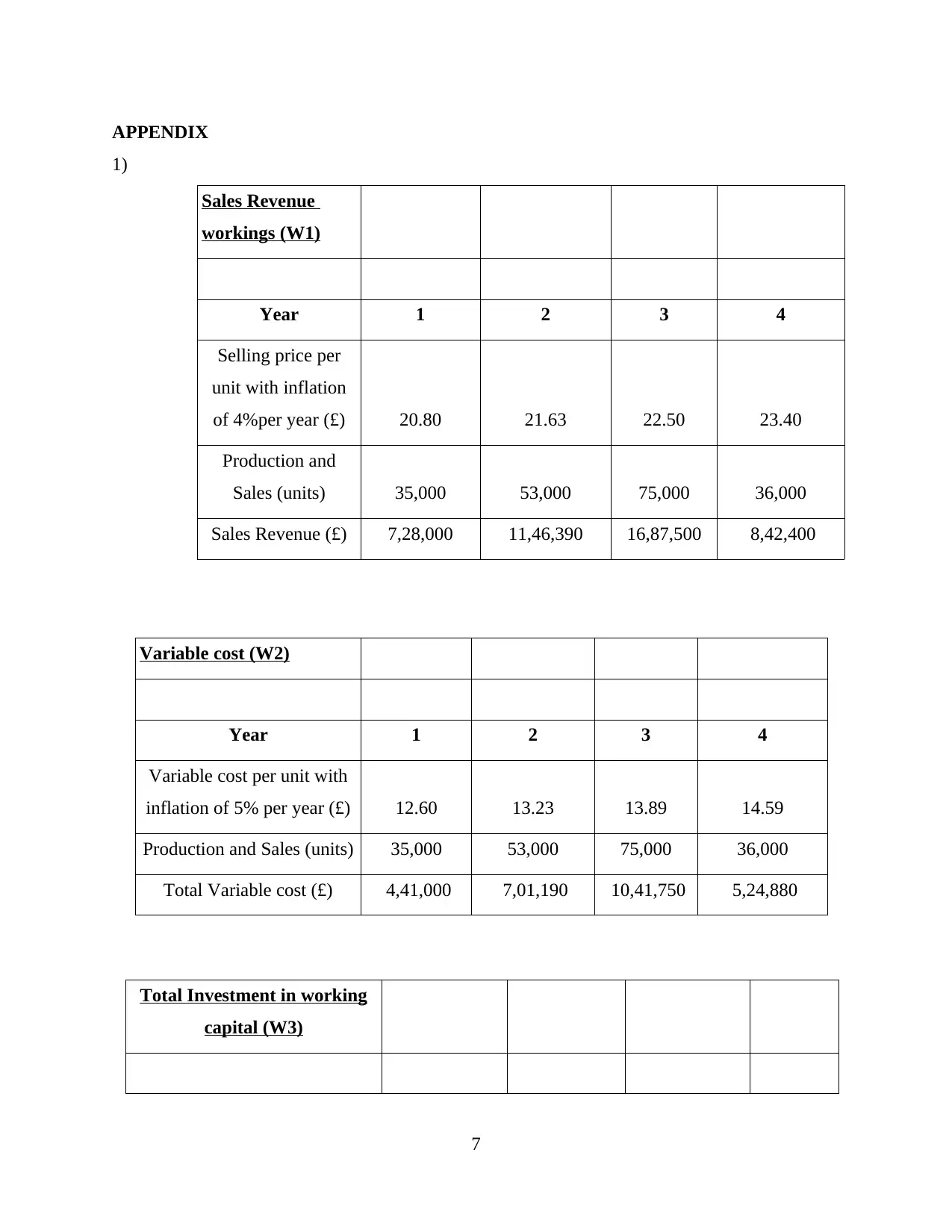

1)

Sales Revenue

workings (W1)

Year 1 2 3 4

Selling price per

unit with inflation

of 4%per year (£) 20.80 21.63 22.50 23.40

Production and

Sales (units) 35,000 53,000 75,000 36,000

Sales Revenue (£) 7,28,000 11,46,390 16,87,500 8,42,400

Variable cost (W2)

Year 1 2 3 4

Variable cost per unit with

inflation of 5% per year (£) 12.60 13.23 13.89 14.59

Production and Sales (units) 35,000 53,000 75,000 36,000

Total Variable cost (£) 4,41,000 7,01,190 10,41,750 5,24,880

Total Investment in working

capital (W3)

7

1)

Sales Revenue

workings (W1)

Year 1 2 3 4

Selling price per

unit with inflation

of 4%per year (£) 20.80 21.63 22.50 23.40

Production and

Sales (units) 35,000 53,000 75,000 36,000

Sales Revenue (£) 7,28,000 11,46,390 16,87,500 8,42,400

Variable cost (W2)

Year 1 2 3 4

Variable cost per unit with

inflation of 5% per year (£) 12.60 13.23 13.89 14.59

Production and Sales (units) 35,000 53,000 75,000 36,000

Total Variable cost (£) 4,41,000 7,01,190 10,41,750 5,24,880

Total Investment in working

capital (W3)

7

Paraphrase This Document

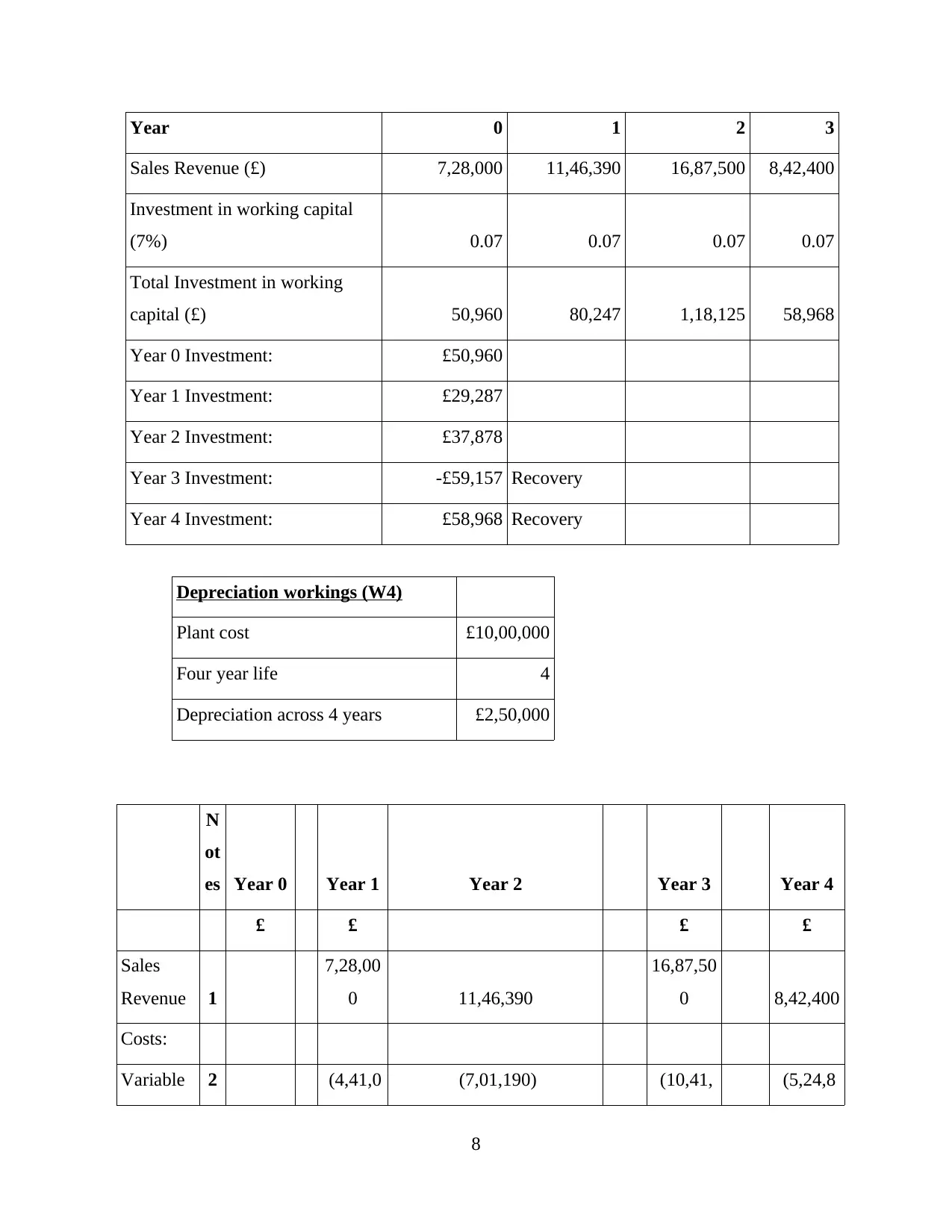

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Year 0 1 2 3

Sales Revenue (£) 7,28,000 11,46,390 16,87,500 8,42,400

Investment in working capital

(7%) 0.07 0.07 0.07 0.07

Total Investment in working

capital (£) 50,960 80,247 1,18,125 58,968

Year 0 Investment: £50,960

Year 1 Investment: £29,287

Year 2 Investment: £37,878

Year 3 Investment: -£59,157 Recovery

Year 4 Investment: £58,968 Recovery

Depreciation workings (W4)

Plant cost £10,00,000

Four year life 4

Depreciation across 4 years £2,50,000

N

ot

es Year 0 Year 1 Year 2 Year 3 Year 4

£ £ £ £

Sales

Revenue 1

7,28,00

0 11,46,390

16,87,50

0 8,42,400

Costs:

Variable 2 (4,41,0 (7,01,190) (10,41, (5,24,8

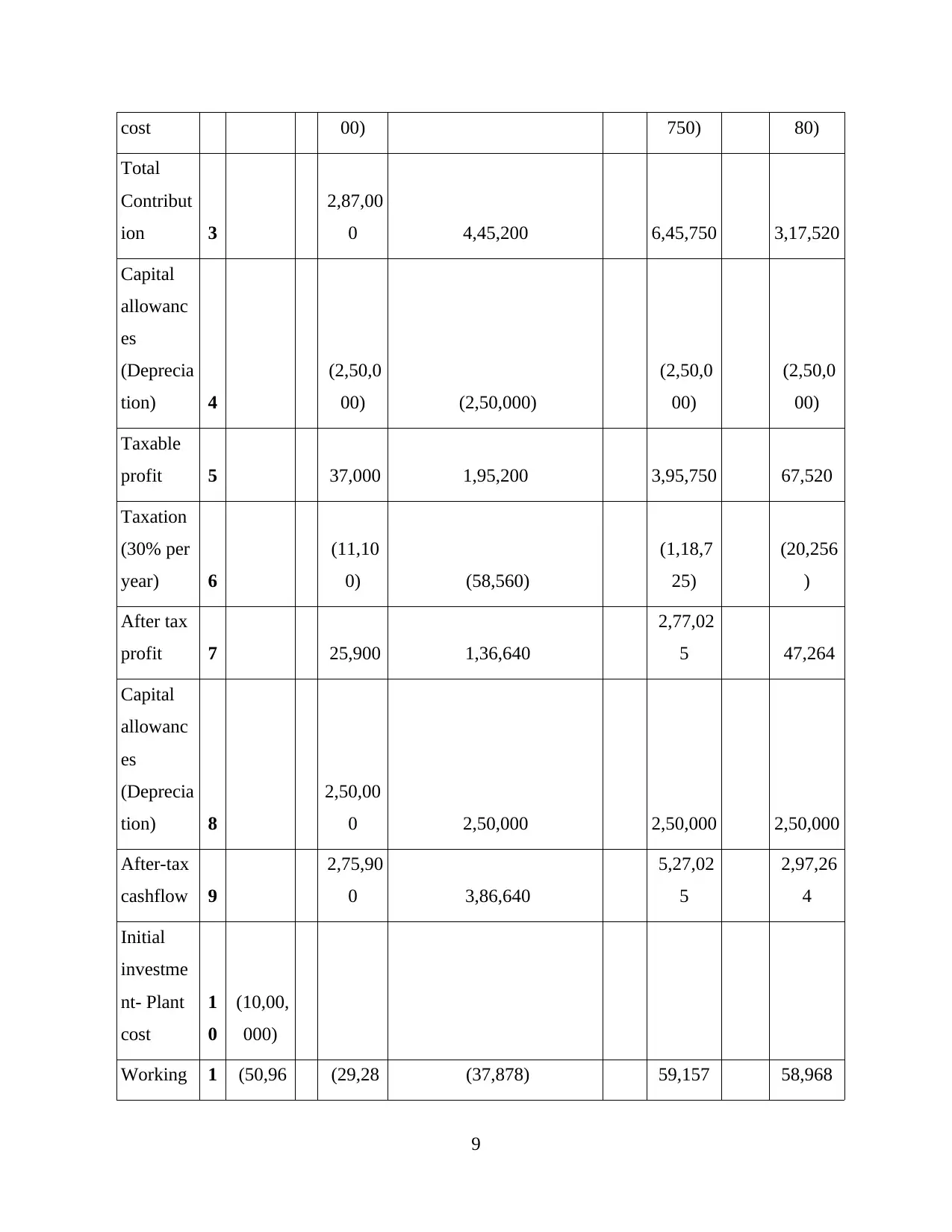

8

Sales Revenue (£) 7,28,000 11,46,390 16,87,500 8,42,400

Investment in working capital

(7%) 0.07 0.07 0.07 0.07

Total Investment in working

capital (£) 50,960 80,247 1,18,125 58,968

Year 0 Investment: £50,960

Year 1 Investment: £29,287

Year 2 Investment: £37,878

Year 3 Investment: -£59,157 Recovery

Year 4 Investment: £58,968 Recovery

Depreciation workings (W4)

Plant cost £10,00,000

Four year life 4

Depreciation across 4 years £2,50,000

N

ot

es Year 0 Year 1 Year 2 Year 3 Year 4

£ £ £ £

Sales

Revenue 1

7,28,00

0 11,46,390

16,87,50

0 8,42,400

Costs:

Variable 2 (4,41,0 (7,01,190) (10,41, (5,24,8

8

cost 00) 750) 80)

Total

Contribut

ion 3

2,87,00

0 4,45,200 6,45,750 3,17,520

Capital

allowanc

es

(Deprecia

tion) 4

(2,50,0

00) (2,50,000)

(2,50,0

00)

(2,50,0

00)

Taxable

profit 5 37,000 1,95,200 3,95,750 67,520

Taxation

(30% per

year) 6

(11,10

0) (58,560)

(1,18,7

25)

(20,256

)

After tax

profit 7 25,900 1,36,640

2,77,02

5 47,264

Capital

allowanc

es

(Deprecia

tion) 8

2,50,00

0 2,50,000 2,50,000 2,50,000

After-tax

cashflow 9

2,75,90

0 3,86,640

5,27,02

5

2,97,26

4

Initial

investme

nt- Plant

cost

1

0

(10,00,

000)

Working 1 (50,96 (29,28 (37,878) 59,157 58,968

9

Total

Contribut

ion 3

2,87,00

0 4,45,200 6,45,750 3,17,520

Capital

allowanc

es

(Deprecia

tion) 4

(2,50,0

00) (2,50,000)

(2,50,0

00)

(2,50,0

00)

Taxable

profit 5 37,000 1,95,200 3,95,750 67,520

Taxation

(30% per

year) 6

(11,10

0) (58,560)

(1,18,7

25)

(20,256

)

After tax

profit 7 25,900 1,36,640

2,77,02

5 47,264

Capital

allowanc

es

(Deprecia

tion) 8

2,50,00

0 2,50,000 2,50,000 2,50,000

After-tax

cashflow 9

2,75,90

0 3,86,640

5,27,02

5

2,97,26

4

Initial

investme

nt- Plant

cost

1

0

(10,00,

000)

Working 1 (50,96 (29,28 (37,878) 59,157 58,968

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.