Management Accounting Report: Financial Planning and Analysis Module

VerifiedAdded on 2020/10/22

|17

|5808

|165

Report

AI Summary

This report delves into the realm of management accounting, focusing on its crucial role in organizations like Unicorn Grocery. It explores various accounting systems, including cost accounting, inventory management, and price optimization, highlighting their significance in financial planning, decision-making, and budgetary control. The report analyzes different types of accounting reporting systems, such as performance reports, cost management reports, and inventory management reports, emphasizing their importance for stakeholders. Furthermore, it examines marginal and absorption costing methods, along with the advantages and disadvantages of planning tools for budgetary control. The report also includes an evaluation of the benefits of these systems, critical analyses of management accounting techniques, and a comparison with other companies in responding to financial issues. The report concludes with an assessment of the planning tools used to resolve financial issues.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: About management accounting and their essential requirement......................................1

P2: Different types of accounting reporting system...............................................................3

M1. Evaluating benefits of accounting system.......................................................................5

D1. Critical evaluation of management accounting systems and reporting...........................5

TASK 2............................................................................................................................................6

P3: Explain Marginal and Absorption costing methods.........................................................6

M2: Analysis of various accounting techniques.....................................................................8

D2: Interpretation..................................................................................................................8

TASK 3............................................................................................................................................8

P4: Advantage and disadvantage of using types of planning tools for budgetary control.....8

M3: Application of the planning tools for preparing, forecasting and analysing budgets...11

TASK 4..........................................................................................................................................12

P5: Comparison with other companies regarding respond to financial issues.....................12

M4: Analysis of management accounting techniques..........................................................13

D3: Evaluation to deal with planning tools used to resolve financial issues........................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: About management accounting and their essential requirement......................................1

P2: Different types of accounting reporting system...............................................................3

M1. Evaluating benefits of accounting system.......................................................................5

D1. Critical evaluation of management accounting systems and reporting...........................5

TASK 2............................................................................................................................................6

P3: Explain Marginal and Absorption costing methods.........................................................6

M2: Analysis of various accounting techniques.....................................................................8

D2: Interpretation..................................................................................................................8

TASK 3............................................................................................................................................8

P4: Advantage and disadvantage of using types of planning tools for budgetary control.....8

M3: Application of the planning tools for preparing, forecasting and analysing budgets...11

TASK 4..........................................................................................................................................12

P5: Comparison with other companies regarding respond to financial issues.....................12

M4: Analysis of management accounting techniques..........................................................13

D3: Evaluation to deal with planning tools used to resolve financial issues........................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION

Management includes interlocking operation of creating corporate policy and overall

planning, organising and directing an organisation resources in respect to attain its aims and

objectives in more quick time. While accounting is systematic process of summarising, recording

financial transaction that are done by the company within an organisation. Overall recording and

formulation of policies and plans are implemented in respect to get more benefits in coming

period of time. The role of manager in “Unicorn Grocery Ltd” is to organise all essential

requirements those are needed to increase growth and stability of the company.

This project module aims to focus on effective utilisation of various types of accounting

systems and reporting. Apart from this, different types of costing those are reliable fore

calculation net profit and loss of the company. Likewise, some planning tools for budgetary

control are discussed under this report (Tappura and et. al., 2015). At the end of this report,

comparison with other companies those are adopting management accounting systems to respond

to financial issues are mentioned properly.

TASK 1

P1: About management accounting and their essential requirement

In current era, it has been seen that managers are playing vital role in formulating various

systems those are helpful in recording various financial and non-financial transaction those are

done within an accounting period of time. This will assist manager of Unicorn Grocery to make

effective decision those are crucial for future planning and sustainability of the company. In

present business environment, business wants to overall all performance data that goes beyond as

per the basis of cost based information. Better management accounting consists of vital role and

responsibility to managers at a wide scale to get more reliable and effective outcomes in coming

period of time (Groot and Selto, 2013). A good accounting consists to a responsibility to manage

a large range of critical management data and their techniques such as cost volume analysis,

budgetary control and cash budgets etc. It is a provision that influence effective decision making

and provide expertise in areas of financial reporting during formulation and development of

organisational strategies. Mainly, it seems to be the effective activity of preparing and

implementing financial data regarding all that information those are collected with the help of

financial accounting.

1

Management includes interlocking operation of creating corporate policy and overall

planning, organising and directing an organisation resources in respect to attain its aims and

objectives in more quick time. While accounting is systematic process of summarising, recording

financial transaction that are done by the company within an organisation. Overall recording and

formulation of policies and plans are implemented in respect to get more benefits in coming

period of time. The role of manager in “Unicorn Grocery Ltd” is to organise all essential

requirements those are needed to increase growth and stability of the company.

This project module aims to focus on effective utilisation of various types of accounting

systems and reporting. Apart from this, different types of costing those are reliable fore

calculation net profit and loss of the company. Likewise, some planning tools for budgetary

control are discussed under this report (Tappura and et. al., 2015). At the end of this report,

comparison with other companies those are adopting management accounting systems to respond

to financial issues are mentioned properly.

TASK 1

P1: About management accounting and their essential requirement

In current era, it has been seen that managers are playing vital role in formulating various

systems those are helpful in recording various financial and non-financial transaction those are

done within an accounting period of time. This will assist manager of Unicorn Grocery to make

effective decision those are crucial for future planning and sustainability of the company. In

present business environment, business wants to overall all performance data that goes beyond as

per the basis of cost based information. Better management accounting consists of vital role and

responsibility to managers at a wide scale to get more reliable and effective outcomes in coming

period of time (Groot and Selto, 2013). A good accounting consists to a responsibility to manage

a large range of critical management data and their techniques such as cost volume analysis,

budgetary control and cash budgets etc. It is a provision that influence effective decision making

and provide expertise in areas of financial reporting during formulation and development of

organisational strategies. Mainly, it seems to be the effective activity of preparing and

implementing financial data regarding all that information those are collected with the help of

financial accounting.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Definition: Management accounting is the process of formulating management reports

and account that used to provide reliable and timely financial and numerical data by the

managers to make every day and short-term decisions. It used to generate monthly or weekly

reports for an organisations internal people such as department managers and other higher

authorities.

According to J. Batty: Management accounting is known as vital term which used to

describe the accounting techniques with special knowledge and ability in their task of increasing

profit or loss period.

Types of Management accounting system

Cost accounting system: It is a vital system for an organisation which is being used for

the determining the forecasted cost for their product, profitability evaluation, stock

valuation and to control overall additional cost. In order to get profitable operation in

near future, they need to make proper estimation of cost that are used during production

of product and services. There are various types of cost systems which are taken into

account while analysing cost for a product. Such as standard costing, normal and actual

costing (Schäffer, 2013).

Inventory management system: It is said to be valuable quantity of product owned and

kept by an organisation that is intended either for resale or as new material and elements

that is being used to producing product for the company. There is an effective system

which is being used in stock management is Just-in-time (JIT). It is the strategy of

companies that employ to enhance overall efficiency and reduce waste through receiving

products only as they are required in manufacturing process. This seems to be helpful for

producers to estimate demand in reliable manner.

Price optimisation system: It seems to be utmost important strategies which a company,

after collecting information from various customer regarding the products they make

certain decision. It is uses as numerical analysis in respect to analyse how clients will

react to other prices for their products and services. It is used to estimate the prices that a

company used to examine would be best suitable for their objectives such as increasing

operational gains during the time. This seems to be formal methods to invent pricing

structure that optimise goal such as earning or customer procurement.

2

and account that used to provide reliable and timely financial and numerical data by the

managers to make every day and short-term decisions. It used to generate monthly or weekly

reports for an organisations internal people such as department managers and other higher

authorities.

According to J. Batty: Management accounting is known as vital term which used to

describe the accounting techniques with special knowledge and ability in their task of increasing

profit or loss period.

Types of Management accounting system

Cost accounting system: It is a vital system for an organisation which is being used for

the determining the forecasted cost for their product, profitability evaluation, stock

valuation and to control overall additional cost. In order to get profitable operation in

near future, they need to make proper estimation of cost that are used during production

of product and services. There are various types of cost systems which are taken into

account while analysing cost for a product. Such as standard costing, normal and actual

costing (Schäffer, 2013).

Inventory management system: It is said to be valuable quantity of product owned and

kept by an organisation that is intended either for resale or as new material and elements

that is being used to producing product for the company. There is an effective system

which is being used in stock management is Just-in-time (JIT). It is the strategy of

companies that employ to enhance overall efficiency and reduce waste through receiving

products only as they are required in manufacturing process. This seems to be helpful for

producers to estimate demand in reliable manner.

Price optimisation system: It seems to be utmost important strategies which a company,

after collecting information from various customer regarding the products they make

certain decision. It is uses as numerical analysis in respect to analyse how clients will

react to other prices for their products and services. It is used to estimate the prices that a

company used to examine would be best suitable for their objectives such as increasing

operational gains during the time. This seems to be formal methods to invent pricing

structure that optimise goal such as earning or customer procurement.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system: It used to track the cost for labour that is being used within a job. In

case job is associated with service, direct labour and can be nearly every of the cost job.

It is used for assigning production costs to a separate products or batches of goods. It will

record the direct material and labour that is actually utilise plus the production overhead

to individual job. The Unicorn grocery used to make proper utilisation of all those

products that are produce within an accounting period of time.

Activity based accounting: It is an accounting method that identifies and expenses or

costs incurred to overhead activities and then assign those costs to products. It is also

known as Activity based costing (ABC). It is the system recognizes the relationship

between costs, overhead activities and costs of products. ABC technique is mostly used

in manufacturing industries and ensures reliability of cost data. Quantifying true costs

and classifying the costs.

P2: Different types of accounting reporting system

Business enterprises is working in respect to increase overall profitability and growth for the

company. it is known as public reporting of operating and financial information through a

business enterprise. These reports are majorly useful for the better decision making on the basis

of evaluating financial position of the company. A reporting entity is considering as firm,

industry and companies that used to prepare financial reports (Fourie and et. al., 2011).

Accounting report are said to be compilation of financial data that are associated from the

accounting statement of the company. The role of manager is to collect all essential data about

current position of Unicorn grocery about their overall sales done within an accounting period of

time. These reports are submitted to the various investors or outside stakeholders. On the basis of

financial stability of the company they used to make their valuable decision regarding capital

investments.

The overall strength of an organisation can also be decided by analysing their position.

These are said to be custom made reports make with the intention for particular objectives, like

detailed evaluation of sales through region or capability of a specific goods line. There are

various types of accounting reports which are needed to be followed by the manager to reach a

certain level in coming future time. The main motive of the company is to control their addition

cost that are making maximum effective on the reputation. There are various sources from which

data can be collected in respect to prepare report of the company. all the reports are equally

3

case job is associated with service, direct labour and can be nearly every of the cost job.

It is used for assigning production costs to a separate products or batches of goods. It will

record the direct material and labour that is actually utilise plus the production overhead

to individual job. The Unicorn grocery used to make proper utilisation of all those

products that are produce within an accounting period of time.

Activity based accounting: It is an accounting method that identifies and expenses or

costs incurred to overhead activities and then assign those costs to products. It is also

known as Activity based costing (ABC). It is the system recognizes the relationship

between costs, overhead activities and costs of products. ABC technique is mostly used

in manufacturing industries and ensures reliability of cost data. Quantifying true costs

and classifying the costs.

P2: Different types of accounting reporting system

Business enterprises is working in respect to increase overall profitability and growth for the

company. it is known as public reporting of operating and financial information through a

business enterprise. These reports are majorly useful for the better decision making on the basis

of evaluating financial position of the company. A reporting entity is considering as firm,

industry and companies that used to prepare financial reports (Fourie and et. al., 2011).

Accounting report are said to be compilation of financial data that are associated from the

accounting statement of the company. The role of manager is to collect all essential data about

current position of Unicorn grocery about their overall sales done within an accounting period of

time. These reports are submitted to the various investors or outside stakeholders. On the basis of

financial stability of the company they used to make their valuable decision regarding capital

investments.

The overall strength of an organisation can also be decided by analysing their position.

These are said to be custom made reports make with the intention for particular objectives, like

detailed evaluation of sales through region or capability of a specific goods line. There are

various types of accounting reports which are needed to be followed by the manager to reach a

certain level in coming future time. The main motive of the company is to control their addition

cost that are making maximum effective on the reputation. There are various sources from which

data can be collected in respect to prepare report of the company. all the reports are equally

3

summarising and given imported while making any kind of decision in coming period of time.

Some of the vital reporting systems that are taken into consideration re discussed underneath:

Performance report: It is known as utmost important activity in project evaluation

management. It consists of various activity such as collecting and dispersion of project

information, progress of project and proper utilisation of resources and overall status of

the stakeholders. It is a detailed information that is used to measure the outcomes of some

vital activity in relation for their success over a particular time period. These are regularly

prepared by higher authorities and government bodies which is being financed by public

money those are required to show the money incurred effectively during the time.

Account receivable report: This seems to be an effective report which is being prepared

in order to analyse total list of unpaid customer’s invoices and unutilised credit amount

memos. It is considering as primary tools that is being used by the collection of personnel

to estimate which invoice are overdue for payment. In some cases, it is known as

reconciliation statements that uses to divide amount owned by all clients as per the

duration of time they are outstanding and unpaid (Bovens, Goodin and Schillemans,

2014).

Cost management accounting report: Cost management accounting also known as

management accounting or cost managerial accounting. It is the process of identifying,

measuring, analysing, interpreting and communicating information to managers for the

achieving organisation's desired goals. Overall, it is a process for quantifying and

minimising the costs and pertain sets of techniques to assist the management in

developing several budgets, standards and ascertain the cost of production of any product

or services in business.

Inventory management report: As per this report, the manager need to make backup

plan for their stocks those are kept by the company. The major aim of management is to

control their inventories those are coming and going from the business within an

accounting period of time. It seems to be essential element of supply chain management

that used to control flow of product from manufacturers to warehouses. It need to follow

certain documents such as Just in time, ABC analysis, First in first out (FIFO) and Last in

first out (LIFO).

4

Some of the vital reporting systems that are taken into consideration re discussed underneath:

Performance report: It is known as utmost important activity in project evaluation

management. It consists of various activity such as collecting and dispersion of project

information, progress of project and proper utilisation of resources and overall status of

the stakeholders. It is a detailed information that is used to measure the outcomes of some

vital activity in relation for their success over a particular time period. These are regularly

prepared by higher authorities and government bodies which is being financed by public

money those are required to show the money incurred effectively during the time.

Account receivable report: This seems to be an effective report which is being prepared

in order to analyse total list of unpaid customer’s invoices and unutilised credit amount

memos. It is considering as primary tools that is being used by the collection of personnel

to estimate which invoice are overdue for payment. In some cases, it is known as

reconciliation statements that uses to divide amount owned by all clients as per the

duration of time they are outstanding and unpaid (Bovens, Goodin and Schillemans,

2014).

Cost management accounting report: Cost management accounting also known as

management accounting or cost managerial accounting. It is the process of identifying,

measuring, analysing, interpreting and communicating information to managers for the

achieving organisation's desired goals. Overall, it is a process for quantifying and

minimising the costs and pertain sets of techniques to assist the management in

developing several budgets, standards and ascertain the cost of production of any product

or services in business.

Inventory management report: As per this report, the manager need to make backup

plan for their stocks those are kept by the company. The major aim of management is to

control their inventories those are coming and going from the business within an

accounting period of time. It seems to be essential element of supply chain management

that used to control flow of product from manufacturers to warehouses. It need to follow

certain documents such as Just in time, ABC analysis, First in first out (FIFO) and Last in

first out (LIFO).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job cost report: It is known as one of the vital method which is being used to record the

costs of producing job in steed of a processing them. By the help of this, a project

controllers and accountant can easily be able to control and track of each job, regulating

data which is being often more related with the operations of a businesses. There are

various types of costing techniques which are taken into consideration such as batch,

process and standard costing.

M1. Evaluating benefits of accounting system

One of the crucial point to the taken into account that every management accounting

systems is equally important for “Unicorn grocery”. This will assist them to plan their future

budgets and production related activities in effective manner (Harris and Durden, 2012). In the

present scenario, most of the managers are searching or investing in attaining best system for an

organisation that will useful in recording all necessary transactions those are done within the

department. Some of them are:

Cost accounting system: By the help of this, manager can have used to analyse cost

related to the revenue and expenses that can be clustered through cost objects, product

line and distribution channel.

Inventory management system: Increase information transparency within an

organisation in case company used to order more or in case of over and under-stocked.

Price optimisation system: It is essential in a company that want to connect to their

business capacity with profit and more significantly. It is considering as utmost important

part of price management system.

Job costing system: Accessibility is the primary benefit to the management in case they

are using this system. Total expenses that are incurred in them can be determine under

this system.

D1. Critical evaluation of management accounting systems and reporting

In order to get more benefit in near future time organisation need to make plan effectively

for control their expenses and cost so that maximum gain can be incurred. This seems to be vital

aspects for Unicorn grocery to make use of all those systems and reporting that are responsible

enough to provide maximum benefit to increase reputation in front of other. According to the

Melnyk and et. al., (2014) both management accounting system and reporting are directly related

with one another. All the information collected from the department are analyse by using

5

costs of producing job in steed of a processing them. By the help of this, a project

controllers and accountant can easily be able to control and track of each job, regulating

data which is being often more related with the operations of a businesses. There are

various types of costing techniques which are taken into consideration such as batch,

process and standard costing.

M1. Evaluating benefits of accounting system

One of the crucial point to the taken into account that every management accounting

systems is equally important for “Unicorn grocery”. This will assist them to plan their future

budgets and production related activities in effective manner (Harris and Durden, 2012). In the

present scenario, most of the managers are searching or investing in attaining best system for an

organisation that will useful in recording all necessary transactions those are done within the

department. Some of them are:

Cost accounting system: By the help of this, manager can have used to analyse cost

related to the revenue and expenses that can be clustered through cost objects, product

line and distribution channel.

Inventory management system: Increase information transparency within an

organisation in case company used to order more or in case of over and under-stocked.

Price optimisation system: It is essential in a company that want to connect to their

business capacity with profit and more significantly. It is considering as utmost important

part of price management system.

Job costing system: Accessibility is the primary benefit to the management in case they

are using this system. Total expenses that are incurred in them can be determine under

this system.

D1. Critical evaluation of management accounting systems and reporting

In order to get more benefit in near future time organisation need to make plan effectively

for control their expenses and cost so that maximum gain can be incurred. This seems to be vital

aspects for Unicorn grocery to make use of all those systems and reporting that are responsible

enough to provide maximum benefit to increase reputation in front of other. According to the

Melnyk and et. al., (2014) both management accounting system and reporting are directly related

with one another. All the information collected from the department are analyse by using

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

effective system and formulate report on the basis. These are compilations of financial data that

are derived from accounting statements of Unicorn grocery financial reports.

TASK 2

P3: Explain Marginal and Absorption costing methods

Cost is said to be value which is been paid by the company in order to earn something.

There are various types of cost those are essential for to be taken into account. This will be more

vital to determine correct cost for the production process. Some of them are discussed

underneath;

Fixed expenses: It refers to those expenses which remains constant every month during a

specified period of time. These expenses cannot be changed easily and normally paid on regular

basis may be monthly, weekly quarterly or yearly. These are not the variable expenses.

Variable cost: It refers to those expenses which includes daily basic expenses to operate

the business, these expenses are considered as discretionary. Variable expenses are those which

changes according to the requirement they are not the fixed expenses. Variable costs changes

according to change in the units of production, contribution is the core concept of marginal

costing which is calculated by determining the difference between all variable costs and sales

price. Marginal costing is a decision making technique which is used to make effective decision

about various expenditures incurred by the company.

Marginal costing method – Marginal costing method is a technique of profit

ascertainment by charging all marginal or variable cost against unit costs of produced goods and

writing off all fixed overheads whether selling or production expenses against contribution.

Marginal costing involves calculation of marginal cost which is a sum of all direct costs such as

direct material cost, direct labour costs, variable production and selling expenses, any changes in

variable costs or units directly effects the income or profit of the company (Marginal Costing.

2018).

Absorption costing method – Absorption costing is also known as full costing as it

involves all manufacturing expenses either variable or fixed, absorption costing is an accounting

technique in which all costs of goods sold are charged against selling price of sold goods to

determine gross profit (Callahan, Stetz and Brooks, 2011).

Prepare an Income statement using Marginal and Absorption costing method

6

are derived from accounting statements of Unicorn grocery financial reports.

TASK 2

P3: Explain Marginal and Absorption costing methods

Cost is said to be value which is been paid by the company in order to earn something.

There are various types of cost those are essential for to be taken into account. This will be more

vital to determine correct cost for the production process. Some of them are discussed

underneath;

Fixed expenses: It refers to those expenses which remains constant every month during a

specified period of time. These expenses cannot be changed easily and normally paid on regular

basis may be monthly, weekly quarterly or yearly. These are not the variable expenses.

Variable cost: It refers to those expenses which includes daily basic expenses to operate

the business, these expenses are considered as discretionary. Variable expenses are those which

changes according to the requirement they are not the fixed expenses. Variable costs changes

according to change in the units of production, contribution is the core concept of marginal

costing which is calculated by determining the difference between all variable costs and sales

price. Marginal costing is a decision making technique which is used to make effective decision

about various expenditures incurred by the company.

Marginal costing method – Marginal costing method is a technique of profit

ascertainment by charging all marginal or variable cost against unit costs of produced goods and

writing off all fixed overheads whether selling or production expenses against contribution.

Marginal costing involves calculation of marginal cost which is a sum of all direct costs such as

direct material cost, direct labour costs, variable production and selling expenses, any changes in

variable costs or units directly effects the income or profit of the company (Marginal Costing.

2018).

Absorption costing method – Absorption costing is also known as full costing as it

involves all manufacturing expenses either variable or fixed, absorption costing is an accounting

technique in which all costs of goods sold are charged against selling price of sold goods to

determine gross profit (Callahan, Stetz and Brooks, 2011).

Prepare an Income statement using Marginal and Absorption costing method

6

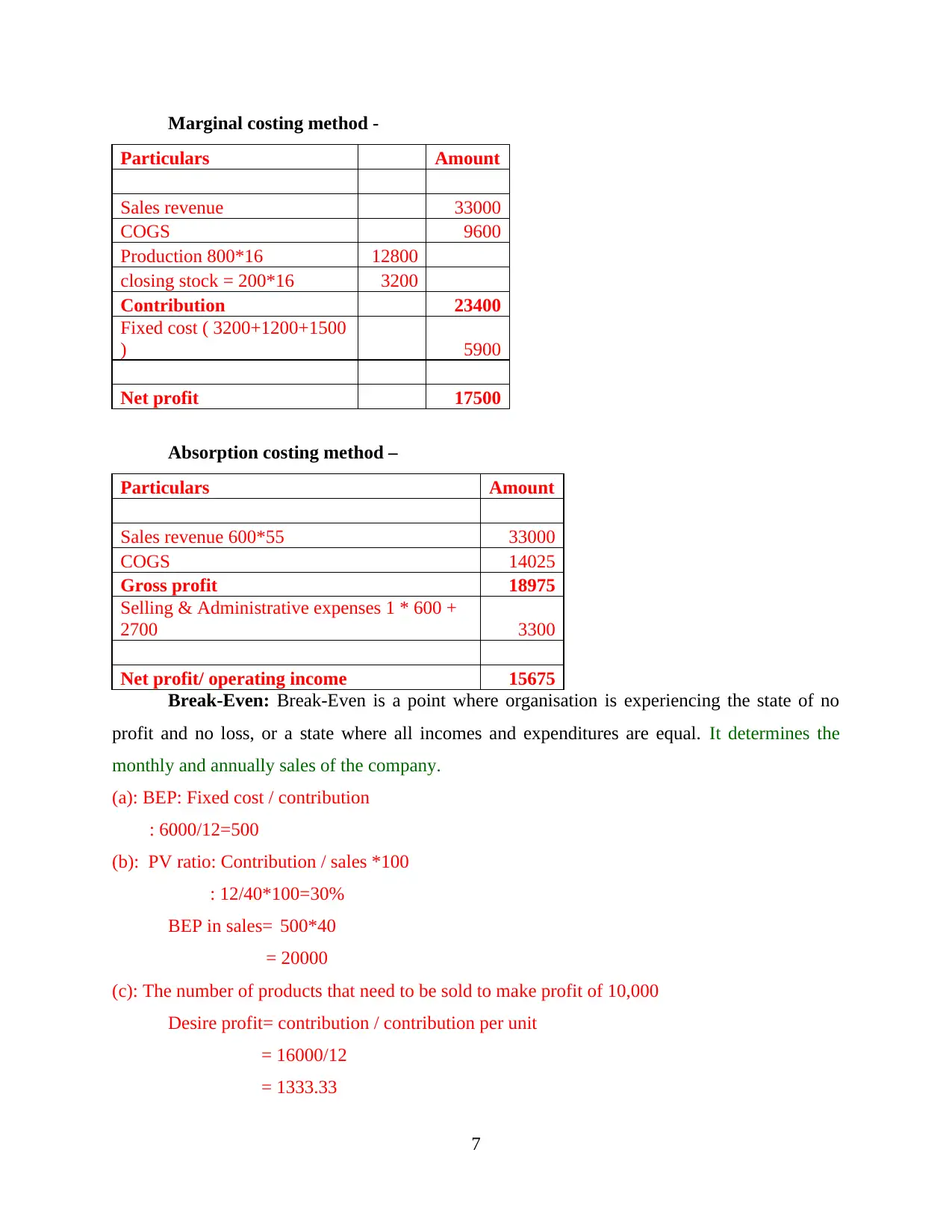

Marginal costing method -

Particulars Amount

Sales revenue 33000

COGS 9600

Production 800*16 12800

closing stock = 200*16 3200

Contribution 23400

Fixed cost ( 3200+1200+1500

) 5900

Net profit 17500

Absorption costing method –

Particulars Amount

Sales revenue 600*55 33000

COGS 14025

Gross profit 18975

Selling & Administrative expenses 1 * 600 +

2700 3300

Net profit/ operating income 15675

Break-Even: Break-Even is a point where organisation is experiencing the state of no

profit and no loss, or a state where all incomes and expenditures are equal. It determines the

monthly and annually sales of the company.

(a): BEP: Fixed cost / contribution

: 6000/12=500

(b): PV ratio: Contribution / sales *100

: 12/40*100=30%

BEP in sales= 500*40

= 20000

(c): The number of products that need to be sold to make profit of 10,000

Desire profit= contribution / contribution per unit

= 16000/12

= 1333.33

7

Particulars Amount

Sales revenue 33000

COGS 9600

Production 800*16 12800

closing stock = 200*16 3200

Contribution 23400

Fixed cost ( 3200+1200+1500

) 5900

Net profit 17500

Absorption costing method –

Particulars Amount

Sales revenue 600*55 33000

COGS 14025

Gross profit 18975

Selling & Administrative expenses 1 * 600 +

2700 3300

Net profit/ operating income 15675

Break-Even: Break-Even is a point where organisation is experiencing the state of no

profit and no loss, or a state where all incomes and expenditures are equal. It determines the

monthly and annually sales of the company.

(a): BEP: Fixed cost / contribution

: 6000/12=500

(b): PV ratio: Contribution / sales *100

: 12/40*100=30%

BEP in sales= 500*40

= 20000

(c): The number of products that need to be sold to make profit of 10,000

Desire profit= contribution / contribution per unit

= 16000/12

= 1333.33

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(d): The margin of safety if 800 products are sold

Actual sales: 800

BEP sales: 500

MOS: 800-500 /800 * 100: 37.5%

The margin of safety is considered as the financial ratios which measures the sales

amount that exceed the break-even point.

M2: Analysis of various accounting techniques

Management accounting techniques like marginal costing and absorption costing are used

to determine net income or profitability of this organisation here net income determined using

marginal costing method is higher than the net income calculated using absorption costing, as

absorption costing takes all costs into account either fixed or variable. Management accounting

techniques like standard costing and historical cost accounting are not used by this organisation

as they seemed to earn more effective financial statements by using marginal and absorption

costing.

Using marginal costing, an organisation can determine contribution, whereas using

absorption costing an organisation can determine gross profit on which fixed costs and selling-

distribution costs are charged respectively to ascertain net incomes.

D2: Interpretation

In the above scenario, organisation can earn profit if they produce goods more than 500

units as the breakeven point is 500. It is the state where organisation is no profit and no loss. The

above organisation is needed to produce at least 1334 units to earn a profit of 10,000, using these

techniques an organisation can determine the profit making ability.

Margin of safety shows safety level of an organisation or it can be said that MOS shows

how much sales can fall before a company can reach breakeven point.

TASK 3

P4: Advantage and disadvantage of using types of planning tools for budgetary control

Planning is said to be an effective process of thinking regarding the activities needed to attain

a desired aims and objective of an organisation. It consists of innovation, creation and overall

maintenance of a plan. It is said that management starts with planning and plan begins with the

formulation of aims of the company. It is more crucial with the formulation of strategies in

8

Actual sales: 800

BEP sales: 500

MOS: 800-500 /800 * 100: 37.5%

The margin of safety is considered as the financial ratios which measures the sales

amount that exceed the break-even point.

M2: Analysis of various accounting techniques

Management accounting techniques like marginal costing and absorption costing are used

to determine net income or profitability of this organisation here net income determined using

marginal costing method is higher than the net income calculated using absorption costing, as

absorption costing takes all costs into account either fixed or variable. Management accounting

techniques like standard costing and historical cost accounting are not used by this organisation

as they seemed to earn more effective financial statements by using marginal and absorption

costing.

Using marginal costing, an organisation can determine contribution, whereas using

absorption costing an organisation can determine gross profit on which fixed costs and selling-

distribution costs are charged respectively to ascertain net incomes.

D2: Interpretation

In the above scenario, organisation can earn profit if they produce goods more than 500

units as the breakeven point is 500. It is the state where organisation is no profit and no loss. The

above organisation is needed to produce at least 1334 units to earn a profit of 10,000, using these

techniques an organisation can determine the profit making ability.

Margin of safety shows safety level of an organisation or it can be said that MOS shows

how much sales can fall before a company can reach breakeven point.

TASK 3

P4: Advantage and disadvantage of using types of planning tools for budgetary control

Planning is said to be an effective process of thinking regarding the activities needed to attain

a desired aims and objective of an organisation. It consists of innovation, creation and overall

maintenance of a plan. It is said that management starts with planning and plan begins with the

formulation of aims of the company. It is more crucial with the formulation of strategies in

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budgets. Because budgets are more reliable and vital aspects for every business organisation

those are responsible for deriving overall strength and position of the company at the same

period of time. It is considering as financial plan for set duration of time, usually for a year. It

can also include sales volume and revenues, cost and expenditure and other cash flows

information about the company (Abrahamsson, Englund and Gerdin, 2011).

Zero based budget: It refers to those budgets which are usually prepared without using any

year priority budget, as these type of budgets are prepared under the process of zero based

budgeting(ZBB), without using previous year's budget or spending numbers. Overall, ZBB is the

technique of preparing the budgets which are based on 'zero base' by evaluating every cost and

every expenses.

Budgetary control is said to be effective process through which budget are prepared for the

future period and are compared with the actual performance for finding out variances. If any.

Objective of budgetary control:

Defining the objective of the enterprise.

Provide plan for attaining objective that are so defined.

Coordinating the activities of various departments.

Advantage of budgetary control

Define the aims, plan and policies

Fixed target

Help the management in case of any contingency.

Reduce cost of production

Disadvantage:

Budgets are prepared for the future period which is always uncertain.

It is considering as only management tool.

It is used for the purpose of planning and performance evaluation which can consist of

spending for fixed assets and rolling out initial products and further training activities. In order to

control additional cost for the company they need to make use of various budgets such as

operating, cash and master budgets. These types of budgets are reliable enough in providing

necessary information for the company in future. In case any problem found in budget they need

to use of planning tools. Such as:

9

those are responsible for deriving overall strength and position of the company at the same

period of time. It is considering as financial plan for set duration of time, usually for a year. It

can also include sales volume and revenues, cost and expenditure and other cash flows

information about the company (Abrahamsson, Englund and Gerdin, 2011).

Zero based budget: It refers to those budgets which are usually prepared without using any

year priority budget, as these type of budgets are prepared under the process of zero based

budgeting(ZBB), without using previous year's budget or spending numbers. Overall, ZBB is the

technique of preparing the budgets which are based on 'zero base' by evaluating every cost and

every expenses.

Budgetary control is said to be effective process through which budget are prepared for the

future period and are compared with the actual performance for finding out variances. If any.

Objective of budgetary control:

Defining the objective of the enterprise.

Provide plan for attaining objective that are so defined.

Coordinating the activities of various departments.

Advantage of budgetary control

Define the aims, plan and policies

Fixed target

Help the management in case of any contingency.

Reduce cost of production

Disadvantage:

Budgets are prepared for the future period which is always uncertain.

It is considering as only management tool.

It is used for the purpose of planning and performance evaluation which can consist of

spending for fixed assets and rolling out initial products and further training activities. In order to

control additional cost for the company they need to make use of various budgets such as

operating, cash and master budgets. These types of budgets are reliable enough in providing

necessary information for the company in future. In case any problem found in budget they need

to use of planning tools. Such as:

9

Forecasting tool: It is known as estimation of unknown condition those are arises in the

departments without providing any information. Estimation is more similar, but can be more

common terms and usually refers to estimation of time value of money, cross-sectional and other

factors. It begins with certain assumption those are based on management experiences and

judgment etc.

Advantage: This method can be use by an individual organisation that relies on data

present and sector in which the company operates. It used to provide valuable

information about financial position of the company.

Disadvantage: It is very tough to make accurate prediction about the future events.

Making accurate decision on forecasted can provide reliable outcomes in financial

downfalls (Nielsen, Mitchell and Nørreklit, 2015).

Scenario tool: It is known as thinking about strategic planning techniques that few

organisations can make use of flexible and long term plans those are effective helpful in near

future time. It will be operative in case of critical situation that are arises within an organisation.

They need to develop suitable situation for markets to enable them and control all implications

that are arise in an organisation.

Advantage: It is innovative thinking regarding future possible behavioural directions of a

system. It is vital in wider learning process within the department.

Disadvantage: The growth and dependency would rely on plenty of conditions such as

plausibility and relevance of scenarios, their coherence and other challenging narrative

aspects of a given scenario.

Contingency tools: It is known as effective plan that devised for getting a reliable results

other than their usual planning. It is often asked for risk management during an exceptional risk

that unlikely would have certain to handle for the company can be resolve by using appropriate

accounting tools. The budget which will be made within an accounting time can be control by

using appropriate methods. All those activities those are undertaken to ensure that proper and

follow-up process will be taken into consideration in an organisation.

Advantage: It used to hold steady, even in case of disaster. Business can have used to

maintain the best state of operations that are best possible to handle any kind of crucial

situations those are arises in the department.

10

departments without providing any information. Estimation is more similar, but can be more

common terms and usually refers to estimation of time value of money, cross-sectional and other

factors. It begins with certain assumption those are based on management experiences and

judgment etc.

Advantage: This method can be use by an individual organisation that relies on data

present and sector in which the company operates. It used to provide valuable

information about financial position of the company.

Disadvantage: It is very tough to make accurate prediction about the future events.

Making accurate decision on forecasted can provide reliable outcomes in financial

downfalls (Nielsen, Mitchell and Nørreklit, 2015).

Scenario tool: It is known as thinking about strategic planning techniques that few

organisations can make use of flexible and long term plans those are effective helpful in near

future time. It will be operative in case of critical situation that are arises within an organisation.

They need to develop suitable situation for markets to enable them and control all implications

that are arise in an organisation.

Advantage: It is innovative thinking regarding future possible behavioural directions of a

system. It is vital in wider learning process within the department.

Disadvantage: The growth and dependency would rely on plenty of conditions such as

plausibility and relevance of scenarios, their coherence and other challenging narrative

aspects of a given scenario.

Contingency tools: It is known as effective plan that devised for getting a reliable results

other than their usual planning. It is often asked for risk management during an exceptional risk

that unlikely would have certain to handle for the company can be resolve by using appropriate

accounting tools. The budget which will be made within an accounting time can be control by

using appropriate methods. All those activities those are undertaken to ensure that proper and

follow-up process will be taken into consideration in an organisation.

Advantage: It used to hold steady, even in case of disaster. Business can have used to

maintain the best state of operations that are best possible to handle any kind of crucial

situations those are arises in the department.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.