Management Accounting Report: Detailed Financial Analysis of KEF Plc

VerifiedAdded on 2021/02/19

|15

|3025

|26

Report

AI Summary

This report provides a comprehensive overview of management accounting practices within KEF Manufacturing Plc, focusing on various accounting systems such as cost accounting, inventory management, price optimization, and job costing. It details different types of accounting reports used, including performance reports, cost accounting reports, inventory reports, and accounts receivable aging reports. The report analyzes the benefits of each management accounting system and discusses the integration of management accounting systems and reports. It also explores marginal and absorption costing methods, presents income statements, and calculates material cost variances. Additionally, the report addresses financial problems faced by KEF Plc and proposes solutions through cost accounting systems and planning tools, aiming to improve financial performance and decision-making within the company. The analysis is conducted from a financial perspective, highlighting the importance of financial planning and control in achieving organizational goals.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The management accounting is a type of accounting system which is related to the

providing financial and non financial information to the managers so that they can take important

decisions regarding to the internal management. This accounting system is different from other

kind of accounting system, this is why because it contains detailed information about monetary

and non monetary transactions. As well as this accounting system is not compulsory to

implement. In this report, different kind of systems and accounting reports are mentioned. Along

with financial statements are prepared with the use of appropriate costing techniques. Apart from

it, benefits and limitations of various planning tools and role of management accounting system

in resolving the financial issues is also described (Songini, Gnan and Malmi, 2013). For details

understanding of this topic, company named Brightstar financial company is chosen which

provide services to the manufacturing company KEF Plc.

LO1

P1.

The management accounting consists different kind of accounting systems that play a

significant role in the context of different kind of organisations. Some accounting systems are

mentioned below which are being used by the KEF manufacturing Plc company:

Cost accounting system- This is a type of accounting system that provides a basis for

computing the cost of various kind of cost of activities. In the absence of this accounting

system it can be difficult for the companies to calculate about how much cost is occurring

in different kind of activities. Eventually, this accounting system is essential for

managing and eliminating the total cost as much as possible. Apart from it, this

accounting system is also beneficial in resolving different kind of financial issues. Such

as in the KEF manufacturing Plc they use this accounting system in the guidance of

Bright- star financial company. Due to this their cost of manufacturing activities get

under control.

Inventory management system- The inventory management system is a kind of

accounting system which is related to the proper management of the stock including raw

material, finished goods etc. As well as in this accounting system companies can take

further decision about purchasing of new material and production of new products. This

The management accounting is a type of accounting system which is related to the

providing financial and non financial information to the managers so that they can take important

decisions regarding to the internal management. This accounting system is different from other

kind of accounting system, this is why because it contains detailed information about monetary

and non monetary transactions. As well as this accounting system is not compulsory to

implement. In this report, different kind of systems and accounting reports are mentioned. Along

with financial statements are prepared with the use of appropriate costing techniques. Apart from

it, benefits and limitations of various planning tools and role of management accounting system

in resolving the financial issues is also described (Songini, Gnan and Malmi, 2013). For details

understanding of this topic, company named Brightstar financial company is chosen which

provide services to the manufacturing company KEF Plc.

LO1

P1.

The management accounting consists different kind of accounting systems that play a

significant role in the context of different kind of organisations. Some accounting systems are

mentioned below which are being used by the KEF manufacturing Plc company:

Cost accounting system- This is a type of accounting system that provides a basis for

computing the cost of various kind of cost of activities. In the absence of this accounting

system it can be difficult for the companies to calculate about how much cost is occurring

in different kind of activities. Eventually, this accounting system is essential for

managing and eliminating the total cost as much as possible. Apart from it, this

accounting system is also beneficial in resolving different kind of financial issues. Such

as in the KEF manufacturing Plc they use this accounting system in the guidance of

Bright- star financial company. Due to this their cost of manufacturing activities get

under control.

Inventory management system- The inventory management system is a kind of

accounting system which is related to the proper management of the stock including raw

material, finished goods etc. As well as in this accounting system companies can take

further decision about purchasing of new material and production of new products. This

is why because on the basis of it, companies can aware about how much stock is

available in the warehouses. Such as in the KEF manufacturing Plc company, they

implement this accounting system to evaluate about the available raw material, finished

goods and make decisions accordingly (Salterio, 2012).

Price optimisation system- The price optimisation system is an accounting system that

determines the price of products and services at an effective level. As well as it is helpful

in analysing customers reaction on different pricing levels. Eventually, in the absence of

this accounting system it can be difficult for the companies to determine the right price of

their products. So this accounting system is essential for right pricing of products and

services. Such as in the KEF manufacturing plc company, they implement this accounting

system for the purpose of allocating right price of different products and services.

Job costing system- The job costing system is a kind of accounting system that

determines the cost of job of different activities separately. Eventually, this is beneficial

in providing detailed information about the cost of jobs and companies can make suitable

decisions about the jobs. So basically, this accounting system is essential for the

controlling the cost of jobs. Herein, the aspect of KEF manufacturing plc, they apply this

accounting system for the purpose of evaluating the cost of job which is assigned in

different kind of activities.

So overall these accounting systems are being used by the KEF manufacturing plc in the

guidance of Bright-star financial consultancy.

P2.

There are various kind of methods preparing the reports, which are being used by the

companies to manage their financial and non financial performance. Such as in the KEF

manufacturing plc, they prepares different kind of accounting reports with the help of accounting

systems. Herein, below some types of accounting reports are mentioned below: Performance report- It is a kind of report that tracks and manage the performance in a

systematic manner. In this report, manager set the financial and non financial goals which

are needed to be achieved after that compare the actual performance with the standards.

So main purpose of the performance report is to control the performance of different

activities as well as of employees. In the KEF manufacturing plc company, they prepare

available in the warehouses. Such as in the KEF manufacturing Plc company, they

implement this accounting system to evaluate about the available raw material, finished

goods and make decisions accordingly (Salterio, 2012).

Price optimisation system- The price optimisation system is an accounting system that

determines the price of products and services at an effective level. As well as it is helpful

in analysing customers reaction on different pricing levels. Eventually, in the absence of

this accounting system it can be difficult for the companies to determine the right price of

their products. So this accounting system is essential for right pricing of products and

services. Such as in the KEF manufacturing plc company, they implement this accounting

system for the purpose of allocating right price of different products and services.

Job costing system- The job costing system is a kind of accounting system that

determines the cost of job of different activities separately. Eventually, this is beneficial

in providing detailed information about the cost of jobs and companies can make suitable

decisions about the jobs. So basically, this accounting system is essential for the

controlling the cost of jobs. Herein, the aspect of KEF manufacturing plc, they apply this

accounting system for the purpose of evaluating the cost of job which is assigned in

different kind of activities.

So overall these accounting systems are being used by the KEF manufacturing plc in the

guidance of Bright-star financial consultancy.

P2.

There are various kind of methods preparing the reports, which are being used by the

companies to manage their financial and non financial performance. Such as in the KEF

manufacturing plc, they prepares different kind of accounting reports with the help of accounting

systems. Herein, below some types of accounting reports are mentioned below: Performance report- It is a kind of report that tracks and manage the performance in a

systematic manner. In this report, manager set the financial and non financial goals which

are needed to be achieved after that compare the actual performance with the standards.

So main purpose of the performance report is to control the performance of different

activities as well as of employees. In the KEF manufacturing plc company, they prepare

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

these reports so that they can evaluate the efficiency of their activities and can take

further decisions accordingly. Cost accounting reports- The cost accounting reports are prepared with the help of cost

accounting systems. In this report companies get the detailed information about cost of

different activities and accordingly can evaluate which activities are high cost consuming.

As well as on the basis of these reports, organisations can take better decisions about

minimising the cost. Basically, these reports are suitable for the manufacturing entities

because they are required to have detailed knowledge about cost of activities. Same as in

the KEF manufacturing company, they prepare this report to get information regarding to

the cost of their different kind of activities (Novas, Alves and Sousa, 2017). Inventory reports- The inventory reports are kind of reports which are related to

providing information about quantity of raw material and finished goods available in the

warehouses. Due to this companies can aware about how much stock is available so that

they can purchase new material. Apart from it, this report is also useful in getting

information about various kind of overhead in the process storing the stock. Same as in

the KEF manufacturing plc, they make these reports for the purpose of managing their

raw material and prepared products. This is why because on the basis of it, they can

decide whether they should purchase new material or not.

Account receivable ageing report- This is a kind of report which is associated with the

providing detailed information to the companies about the total payables in the market as

well as about how many debtors are overdue. Apart from it, in this report companies can

get information about dates on which payment is due. So overall main objective of this

report is to help the companies in collection of amount from the debtors. In the above

respected company, they prepare this report for the purpose of getting information about

the total amount due in the market from different debtors.

So these are the reports of accounting which are being used by the KEF manufacturing plc for

getting important information about financial and non financial activities (Rossing, 2013).

M1.

The management accounting system consists various kind of accounting systems which

are mentioned above. Each of these accounting system has some importance which is mentioned

below:

further decisions accordingly. Cost accounting reports- The cost accounting reports are prepared with the help of cost

accounting systems. In this report companies get the detailed information about cost of

different activities and accordingly can evaluate which activities are high cost consuming.

As well as on the basis of these reports, organisations can take better decisions about

minimising the cost. Basically, these reports are suitable for the manufacturing entities

because they are required to have detailed knowledge about cost of activities. Same as in

the KEF manufacturing company, they prepare this report to get information regarding to

the cost of their different kind of activities (Novas, Alves and Sousa, 2017). Inventory reports- The inventory reports are kind of reports which are related to

providing information about quantity of raw material and finished goods available in the

warehouses. Due to this companies can aware about how much stock is available so that

they can purchase new material. Apart from it, this report is also useful in getting

information about various kind of overhead in the process storing the stock. Same as in

the KEF manufacturing plc, they make these reports for the purpose of managing their

raw material and prepared products. This is why because on the basis of it, they can

decide whether they should purchase new material or not.

Account receivable ageing report- This is a kind of report which is associated with the

providing detailed information to the companies about the total payables in the market as

well as about how many debtors are overdue. Apart from it, in this report companies can

get information about dates on which payment is due. So overall main objective of this

report is to help the companies in collection of amount from the debtors. In the above

respected company, they prepare this report for the purpose of getting information about

the total amount due in the market from different debtors.

So these are the reports of accounting which are being used by the KEF manufacturing plc for

getting important information about financial and non financial activities (Rossing, 2013).

M1.

The management accounting system consists various kind of accounting systems which

are mentioned above. Each of these accounting system has some importance which is mentioned

below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

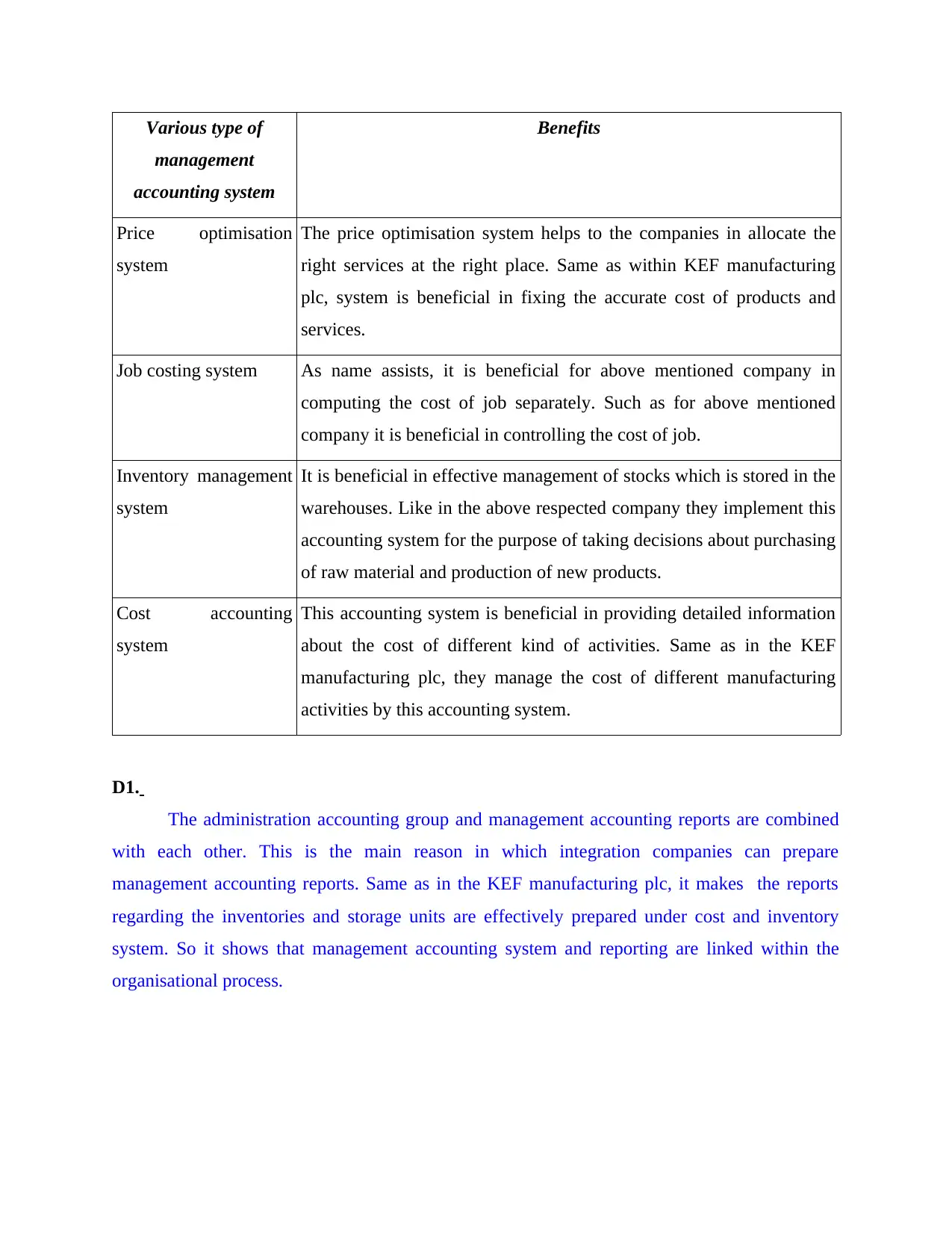

Various type of

management

accounting system

Benefits

Price optimisation

system

The price optimisation system helps to the companies in allocate the

right services at the right place. Same as within KEF manufacturing

plc, system is beneficial in fixing the accurate cost of products and

services.

Job costing system As name assists, it is beneficial for above mentioned company in

computing the cost of job separately. Such as for above mentioned

company it is beneficial in controlling the cost of job.

Inventory management

system

It is beneficial in effective management of stocks which is stored in the

warehouses. Like in the above respected company they implement this

accounting system for the purpose of taking decisions about purchasing

of raw material and production of new products.

Cost accounting

system

This accounting system is beneficial in providing detailed information

about the cost of different kind of activities. Same as in the KEF

manufacturing plc, they manage the cost of different manufacturing

activities by this accounting system.

D1.

The administration accounting group and management accounting reports are combined

with each other. This is the main reason in which integration companies can prepare

management accounting reports. Same as in the KEF manufacturing plc, it makes the reports

regarding the inventories and storage units are effectively prepared under cost and inventory

system. So it shows that management accounting system and reporting are linked within the

organisational process.

management

accounting system

Benefits

Price optimisation

system

The price optimisation system helps to the companies in allocate the

right services at the right place. Same as within KEF manufacturing

plc, system is beneficial in fixing the accurate cost of products and

services.

Job costing system As name assists, it is beneficial for above mentioned company in

computing the cost of job separately. Such as for above mentioned

company it is beneficial in controlling the cost of job.

Inventory management

system

It is beneficial in effective management of stocks which is stored in the

warehouses. Like in the above respected company they implement this

accounting system for the purpose of taking decisions about purchasing

of raw material and production of new products.

Cost accounting

system

This accounting system is beneficial in providing detailed information

about the cost of different kind of activities. Same as in the KEF

manufacturing plc, they manage the cost of different manufacturing

activities by this accounting system.

D1.

The administration accounting group and management accounting reports are combined

with each other. This is the main reason in which integration companies can prepare

management accounting reports. Same as in the KEF manufacturing plc, it makes the reports

regarding the inventories and storage units are effectively prepared under cost and inventory

system. So it shows that management accounting system and reporting are linked within the

organisational process.

LO2

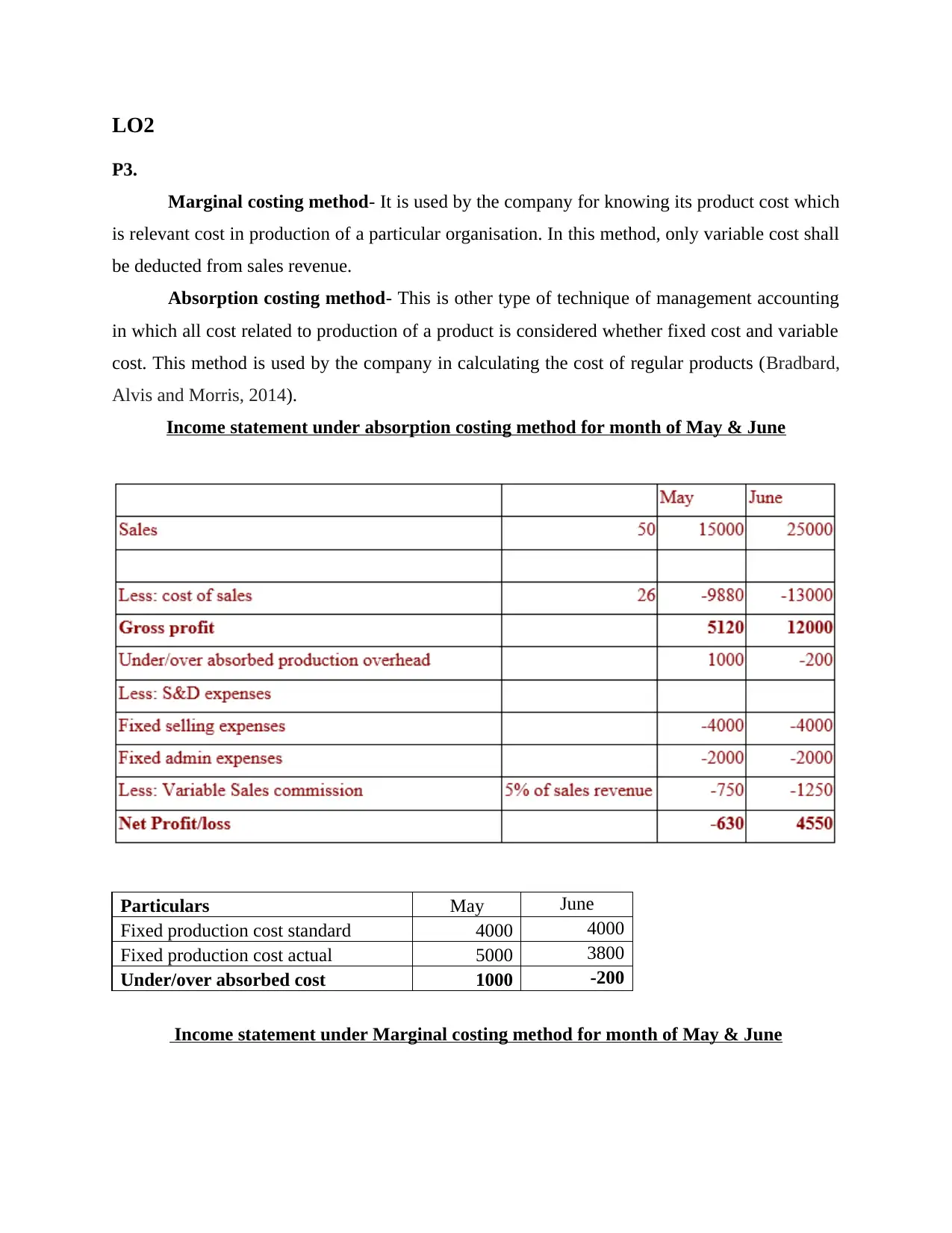

P3.

Marginal costing method- It is used by the company for knowing its product cost which

is relevant cost in production of a particular organisation. In this method, only variable cost shall

be deducted from sales revenue.

Absorption costing method- This is other type of technique of management accounting

in which all cost related to production of a product is considered whether fixed cost and variable

cost. This method is used by the company in calculating the cost of regular products (Bradbard,

Alvis and Morris, 2014).

Income statement under absorption costing method for month of May & June

Particulars May June

Fixed production cost standard 4000 4000

Fixed production cost actual 5000 3800

Under/over absorbed cost 1000 -200

Income statement under Marginal costing method for month of May & June

P3.

Marginal costing method- It is used by the company for knowing its product cost which

is relevant cost in production of a particular organisation. In this method, only variable cost shall

be deducted from sales revenue.

Absorption costing method- This is other type of technique of management accounting

in which all cost related to production of a product is considered whether fixed cost and variable

cost. This method is used by the company in calculating the cost of regular products (Bradbard,

Alvis and Morris, 2014).

Income statement under absorption costing method for month of May & June

Particulars May June

Fixed production cost standard 4000 4000

Fixed production cost actual 5000 3800

Under/over absorbed cost 1000 -200

Income statement under Marginal costing method for month of May & June

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

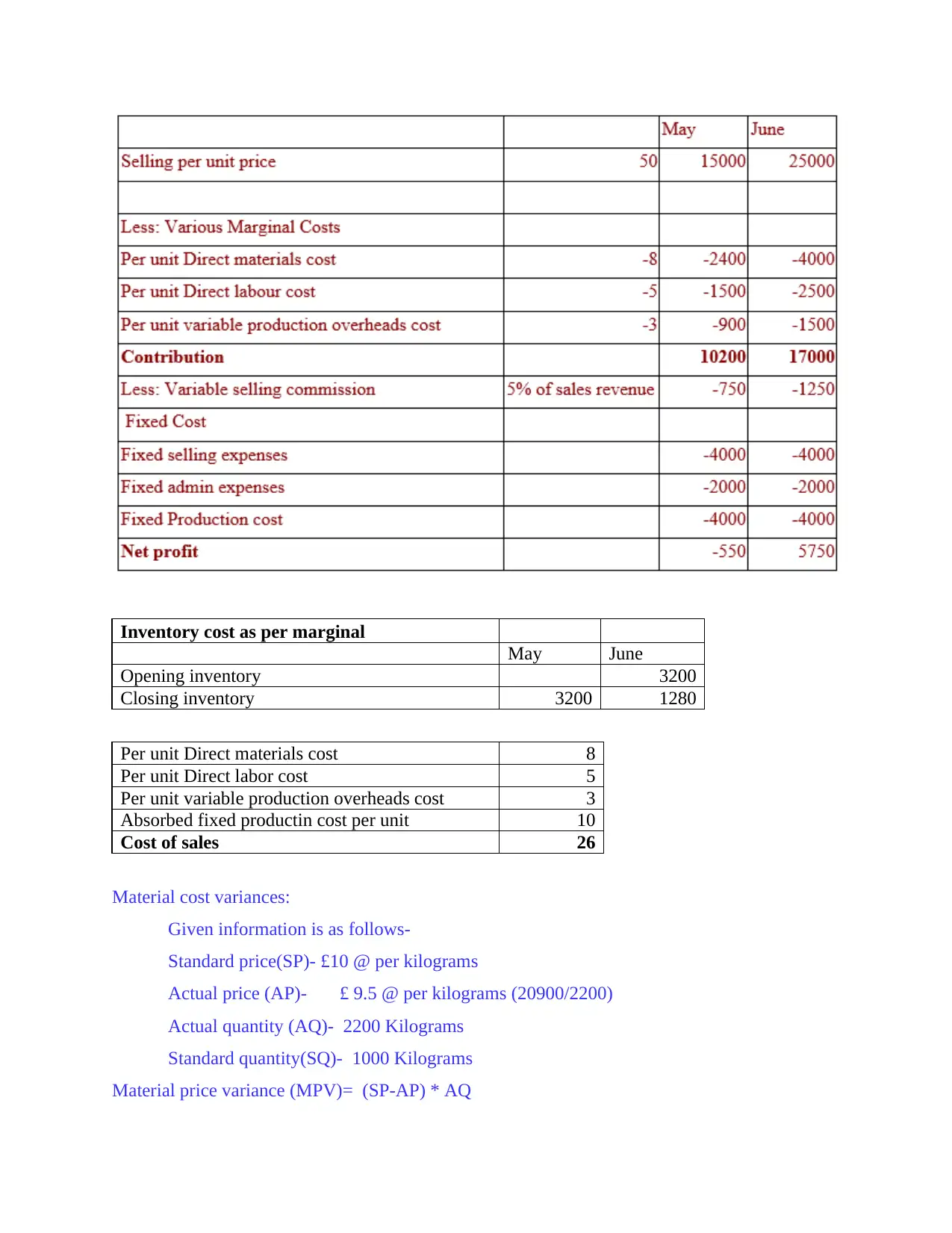

Inventory cost as per marginal

May June

Opening inventory 3200

Closing inventory 3200 1280

Per unit Direct materials cost 8

Per unit Direct labor cost 5

Per unit variable production overheads cost 3

Absorbed fixed productin cost per unit 10

Cost of sales 26

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

May June

Opening inventory 3200

Closing inventory 3200 1280

Per unit Direct materials cost 8

Per unit Direct labor cost 5

Per unit variable production overheads cost 3

Absorbed fixed productin cost per unit 10

Cost of sales 26

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

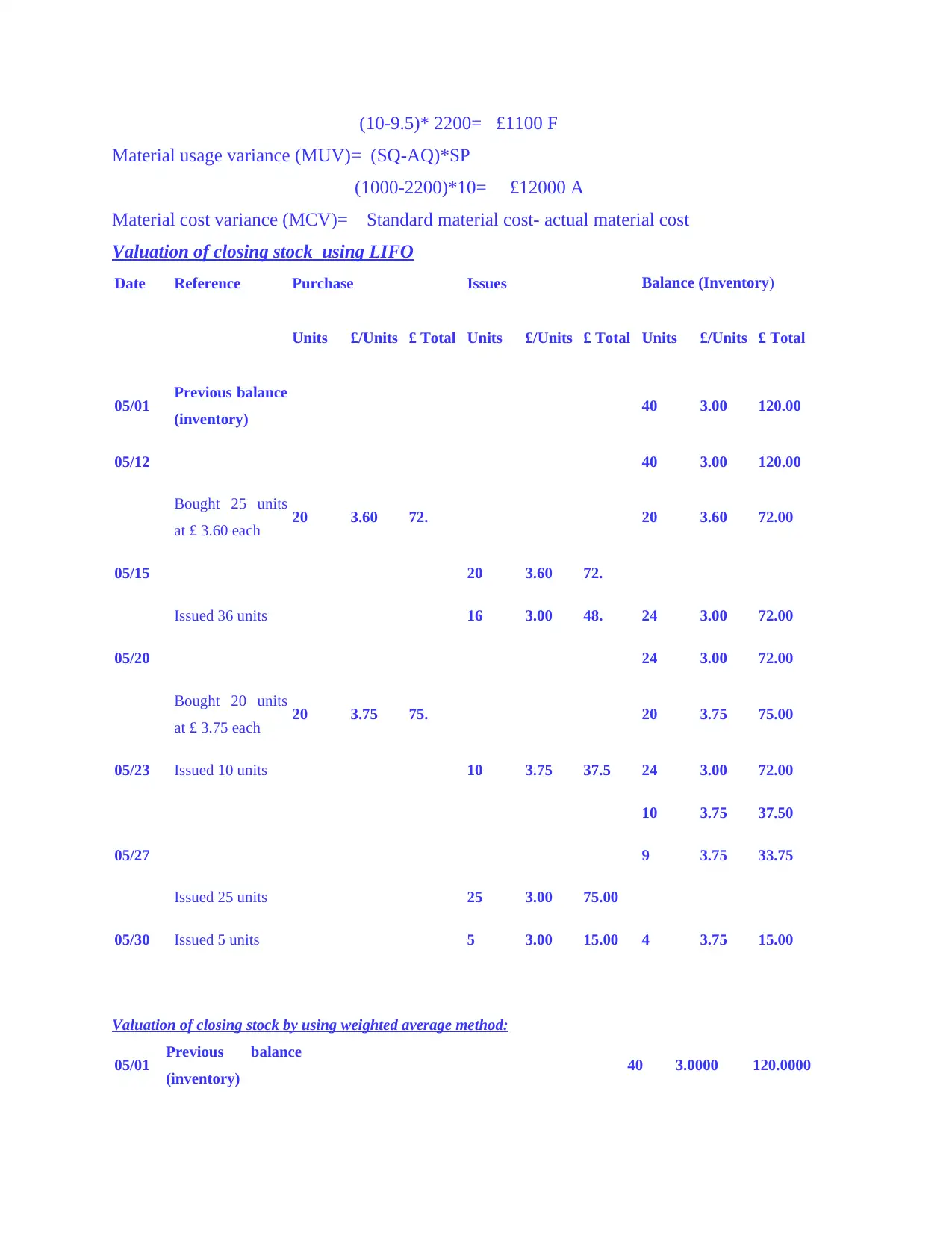

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Units £/Units £ Total Units £/Units £ Total Units £/Units £ Total

05/01 Previous balance

(inventory) 40 3.00 120.00

05/12 40 3.00 120.00

Bought 25 units

at £ 3.60 each 20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units

at £ 3.75 each 20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

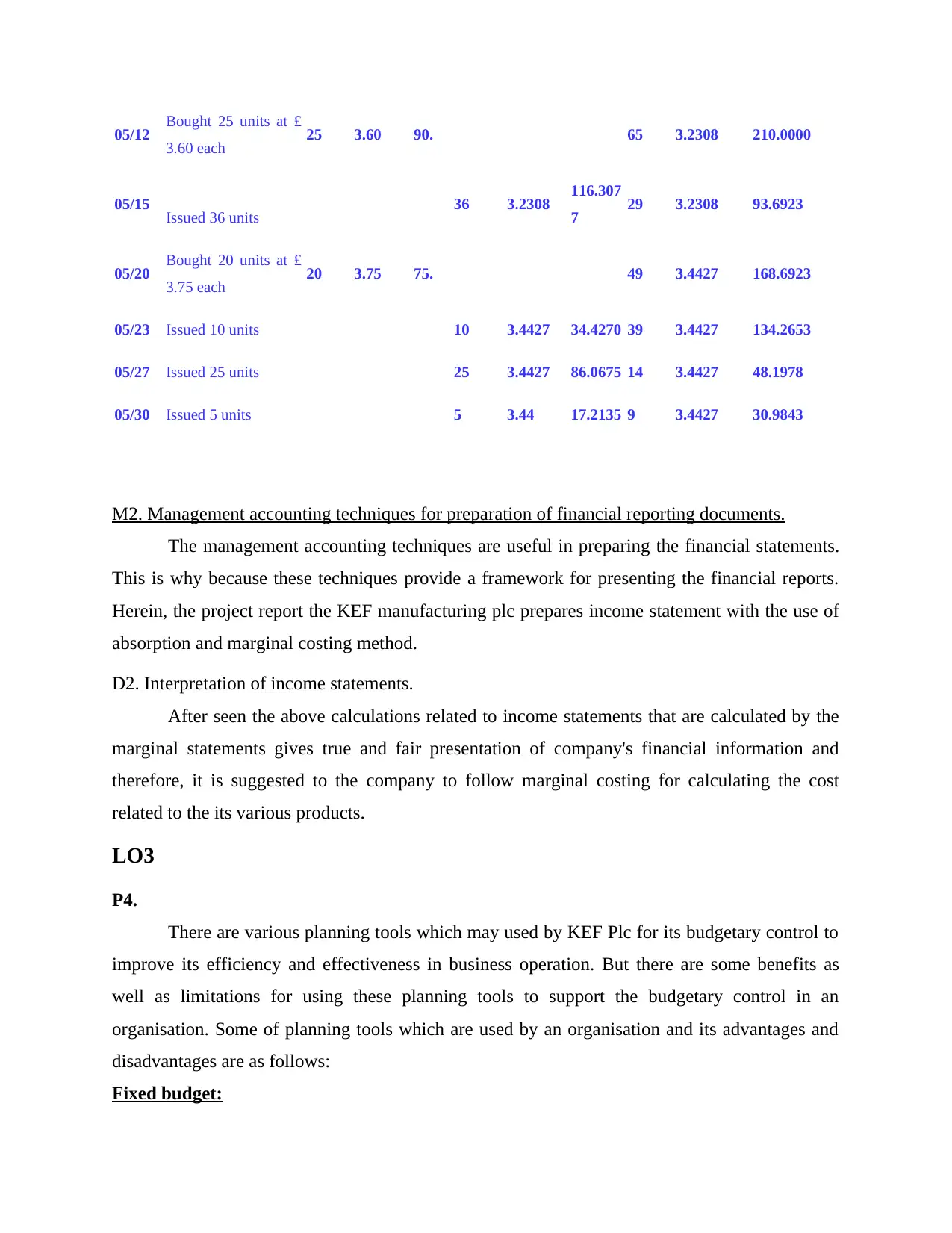

Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.0000

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Units £/Units £ Total Units £/Units £ Total Units £/Units £ Total

05/01 Previous balance

(inventory) 40 3.00 120.00

05/12 40 3.00 120.00

Bought 25 units

at £ 3.60 each 20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units

at £ 3.75 each 20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.0000

05/12 Bought 25 units at £

3.60 each 25 3.60 90. 65 3.2308 210.0000

05/15 Issued 36 units 36 3.2308 116.307

7 29 3.2308 93.6923

05/20 Bought 20 units at £

3.75 each 20 3.75 75. 49 3.4427 168.6923

05/23 Issued 10 units 10 3.4427 34.4270 39 3.4427 134.2653

05/27 Issued 25 units 25 3.4427 86.0675 14 3.4427 48.1978

05/30 Issued 5 units 5 3.44 17.2135 9 3.4427 30.9843

M2. Management accounting techniques for preparation of financial reporting documents.

The management accounting techniques are useful in preparing the financial statements.

This is why because these techniques provide a framework for presenting the financial reports.

Herein, the project report the KEF manufacturing plc prepares income statement with the use of

absorption and marginal costing method.

D2. Interpretation of income statements.

After seen the above calculations related to income statements that are calculated by the

marginal statements gives true and fair presentation of company's financial information and

therefore, it is suggested to the company to follow marginal costing for calculating the cost

related to the its various products.

LO3

P4.

There are various planning tools which may used by KEF Plc for its budgetary control to

improve its efficiency and effectiveness in business operation. But there are some benefits as

well as limitations for using these planning tools to support the budgetary control in an

organisation. Some of planning tools which are used by an organisation and its advantages and

disadvantages are as follows:

Fixed budget:

3.60 each 25 3.60 90. 65 3.2308 210.0000

05/15 Issued 36 units 36 3.2308 116.307

7 29 3.2308 93.6923

05/20 Bought 20 units at £

3.75 each 20 3.75 75. 49 3.4427 168.6923

05/23 Issued 10 units 10 3.4427 34.4270 39 3.4427 134.2653

05/27 Issued 25 units 25 3.4427 86.0675 14 3.4427 48.1978

05/30 Issued 5 units 5 3.44 17.2135 9 3.4427 30.9843

M2. Management accounting techniques for preparation of financial reporting documents.

The management accounting techniques are useful in preparing the financial statements.

This is why because these techniques provide a framework for presenting the financial reports.

Herein, the project report the KEF manufacturing plc prepares income statement with the use of

absorption and marginal costing method.

D2. Interpretation of income statements.

After seen the above calculations related to income statements that are calculated by the

marginal statements gives true and fair presentation of company's financial information and

therefore, it is suggested to the company to follow marginal costing for calculating the cost

related to the its various products.

LO3

P4.

There are various planning tools which may used by KEF Plc for its budgetary control to

improve its efficiency and effectiveness in business operation. But there are some benefits as

well as limitations for using these planning tools to support the budgetary control in an

organisation. Some of planning tools which are used by an organisation and its advantages and

disadvantages are as follows:

Fixed budget:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed budget is prepared by the management accountant for fixed scale of operation and

it can not be change according to the actual scale of operation (i.e. actual production of given

period). In other words, it can not change or flex according to change in volume of production.

Advantages:

It is based on the past (historical) data and current state of the business.

It is easy to prepare and forward looking view for the organisation.

Disadvantages:

Company can not change this budget during that year, even though there is a changes in

the level of business operations.

It requires more time to find out the exact financial resources required and also cost

involved is very high (Chan, Tong and Zhang, 2012).

Flexible Budget:

Flexible budget is a budget that can be change or can adjust according to the time scale of

business operation. This budget is more sophisticated than static (fixed) budget. It is also called a

variable budget because it is a financial plan of estimated revenues and expenses based on the

actual amount of output.

Advantages:

Management accountant is free to establish budget for any level of activity within

relevant range even after the relevant period over.

Flexible budget helps the company in assessing the performance of the various

department heads (Wagner, 2015).

Disadvantages:

In this budget, there is linearity of cost and also there is no specific record in an

organisation.

It is based on the assumption of continuity, due to this, it does not consider the going

concern (i.e. in case of any issue in continuity of activity, it may be stopped).

Zero based budget:

This budget starts from zero base function in which every function within the

organisation like KEF Plc is analysed and evaluated according to the needs and costs and

thereafter, zero based budget is prepared around the what is needed for upcoming period.

Advantages:

it can not be change according to the actual scale of operation (i.e. actual production of given

period). In other words, it can not change or flex according to change in volume of production.

Advantages:

It is based on the past (historical) data and current state of the business.

It is easy to prepare and forward looking view for the organisation.

Disadvantages:

Company can not change this budget during that year, even though there is a changes in

the level of business operations.

It requires more time to find out the exact financial resources required and also cost

involved is very high (Chan, Tong and Zhang, 2012).

Flexible Budget:

Flexible budget is a budget that can be change or can adjust according to the time scale of

business operation. This budget is more sophisticated than static (fixed) budget. It is also called a

variable budget because it is a financial plan of estimated revenues and expenses based on the

actual amount of output.

Advantages:

Management accountant is free to establish budget for any level of activity within

relevant range even after the relevant period over.

Flexible budget helps the company in assessing the performance of the various

department heads (Wagner, 2015).

Disadvantages:

In this budget, there is linearity of cost and also there is no specific record in an

organisation.

It is based on the assumption of continuity, due to this, it does not consider the going

concern (i.e. in case of any issue in continuity of activity, it may be stopped).

Zero based budget:

This budget starts from zero base function in which every function within the

organisation like KEF Plc is analysed and evaluated according to the needs and costs and

thereafter, zero based budget is prepared around the what is needed for upcoming period.

Advantages:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In preparing this budget, there is no requirement of much spending, it may prepared with

justified spending (Clinton and White, 2012).

It helps in finding out the redundancies in the business operations and it also helps in

elimination of waste, focuses use of resources.

Disadvantages:

Although, there is many benefits in preparing such budget but it is very costly and

complex to prepare.

A company prepared this budget may suffers loss of long term planning and this budget

is not useful in manufacturing sector.

Incremental budget:

This is a budget prepared by using a previous period's budget and in other words, it is

prepared for using actual performance as a basis with incremental amount added in previous year

budget. In this budget, while preparing this, resources are allocated on the basis of previous

period.

Advantages:

There is inefficient or obsolete operations may be find out and consequently, it

may be eliminated (Nilsson and Stockenstrand, 2015).

It is good to prepare this budget because it responds the changing business

environment and in this, resources may be allocated efficiently and economically.

Disadvantages:

Incremental budget has more emphasis on the short term benefits or goals and

consequently, it detriments (ignores) the long term goals.

The process of preparing the incremental budget may be rigid, due to this, company

like KEF Plc may not be able to response various threats or opportunities in the

external environment.

M3.

Budget preparation requires application of these planing tools as stated above for

increasing the efficiency and effectiveness of business operations by improving the working style

of workers and its employees. For systematic process of any budget, these planning tools play a

critical and important role. These includes cash budget, master budget, flexible budget etc. for

providing a basis for planned figures of probable events. By including planning tools in

justified spending (Clinton and White, 2012).

It helps in finding out the redundancies in the business operations and it also helps in

elimination of waste, focuses use of resources.

Disadvantages:

Although, there is many benefits in preparing such budget but it is very costly and

complex to prepare.

A company prepared this budget may suffers loss of long term planning and this budget

is not useful in manufacturing sector.

Incremental budget:

This is a budget prepared by using a previous period's budget and in other words, it is

prepared for using actual performance as a basis with incremental amount added in previous year

budget. In this budget, while preparing this, resources are allocated on the basis of previous

period.

Advantages:

There is inefficient or obsolete operations may be find out and consequently, it

may be eliminated (Nilsson and Stockenstrand, 2015).

It is good to prepare this budget because it responds the changing business

environment and in this, resources may be allocated efficiently and economically.

Disadvantages:

Incremental budget has more emphasis on the short term benefits or goals and

consequently, it detriments (ignores) the long term goals.

The process of preparing the incremental budget may be rigid, due to this, company

like KEF Plc may not be able to response various threats or opportunities in the

external environment.

M3.

Budget preparation requires application of these planing tools as stated above for

increasing the efficiency and effectiveness of business operations by improving the working style

of workers and its employees. For systematic process of any budget, these planning tools play a

critical and important role. These includes cash budget, master budget, flexible budget etc. for

providing a basis for planned figures of probable events. By including planning tools in

budgetary control, management personnel may make the reliable estimate of probable

performance of organisation and mangers may also use this for reporting purpose. For this, KEF

Plc company also uses different tools and their application such as zero cost budget for some

circumstances, cash budget for some different circumstances and so on. Therefore, it adopts

these as per the need of company (Halbouni and Nour, 2014).

LO4

P5.

In every organisation, whether small, medium or large, at each level of activities and

functions, there are some issue can be raise due to positive business environment. Financial problems

is a situation where money is the sole cause of problems in any business organisation like KEF Plc.

By adopting management accounting system at early stage, a company may resolve its financial

problems which helps the enterprises to achieve consistency in growth and ensure long term survival.

In medium sized entities like KEF Plc less knowledge of financial problem can lead to major

financial issues such insolvency in long run and so on. Some of these problems are as follows:

Lack of liquid funds: This is a major financial problem of KEF Plc, it means that company is

not able to pay its day to day expenses due non availability of liquid assets in short period of

time. It is linked to organisation's working capital directly. As company is manufacturing

entity so company should maintain adequate liquid funds for any sudden expenditure or

contingent manufacturing expense. If there is a non availability of liquid funds frequently, it

may cause the non functioning of business operations which are essential (Boyns, Edwards

and Nikitin, 2013).

Poor cash management: Another problem of an entity like KEF Plc are not proper utilising of

cash funds (i.e. cash management problems). It may be represented by the negative cash

flows from operating activities, loss of cash by theft, cash deficit (i.e. Expenses are more than

cash available). For resolving this problem, there is requirement to manage the cash in best

possible manner by make plans for applications of cash funds. If in any company, there is a

no proper management for cash then it may lead to liquidity problems.

Some of the significant techniques which may be used by managerial personnel to resolve financial

problems in an organisation are as follows:

Benchmarking: It is a process by which certain levels and criteria may be set for doing

works towards achievement of these criteria or assess performance of entity based on such

performance of organisation and mangers may also use this for reporting purpose. For this, KEF

Plc company also uses different tools and their application such as zero cost budget for some

circumstances, cash budget for some different circumstances and so on. Therefore, it adopts

these as per the need of company (Halbouni and Nour, 2014).

LO4

P5.

In every organisation, whether small, medium or large, at each level of activities and

functions, there are some issue can be raise due to positive business environment. Financial problems

is a situation where money is the sole cause of problems in any business organisation like KEF Plc.

By adopting management accounting system at early stage, a company may resolve its financial

problems which helps the enterprises to achieve consistency in growth and ensure long term survival.

In medium sized entities like KEF Plc less knowledge of financial problem can lead to major

financial issues such insolvency in long run and so on. Some of these problems are as follows:

Lack of liquid funds: This is a major financial problem of KEF Plc, it means that company is

not able to pay its day to day expenses due non availability of liquid assets in short period of

time. It is linked to organisation's working capital directly. As company is manufacturing

entity so company should maintain adequate liquid funds for any sudden expenditure or

contingent manufacturing expense. If there is a non availability of liquid funds frequently, it

may cause the non functioning of business operations which are essential (Boyns, Edwards

and Nikitin, 2013).

Poor cash management: Another problem of an entity like KEF Plc are not proper utilising of

cash funds (i.e. cash management problems). It may be represented by the negative cash

flows from operating activities, loss of cash by theft, cash deficit (i.e. Expenses are more than

cash available). For resolving this problem, there is requirement to manage the cash in best

possible manner by make plans for applications of cash funds. If in any company, there is a

no proper management for cash then it may lead to liquidity problems.

Some of the significant techniques which may be used by managerial personnel to resolve financial

problems in an organisation are as follows:

Benchmarking: It is a process by which certain levels and criteria may be set for doing

works towards achievement of these criteria or assess performance of entity based on such

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.