Development of Accounting Conceptual Framework and Changes Issued by AASB

VerifiedAdded on 2022/12/15

|7

|1778

|482

AI Summary

This report explores the development of the Accounting Conceptual Framework, including its history and specific changes issued by AASB. It also discusses the future directions and insights in the development of the Conceptual Framework.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................2

MAIN BODY..................................................................................................................................3

1. Development of the Accounting Conceptual Framework.......................................................3

2. Specific changes and development between Conceptual framework issued by AASB..........3

3. Future directions and insights in development of Conceptual Framework.............................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

In his report a brief description of the history of the development of the Accounting

Conceptual Framework is provided. Also, specific changes and development of the conceptual

INTRODUCTION...........................................................................................................................2

MAIN BODY..................................................................................................................................3

1. Development of the Accounting Conceptual Framework.......................................................3

2. Specific changes and development between Conceptual framework issued by AASB..........3

3. Future directions and insights in development of Conceptual Framework.............................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

In his report a brief description of the history of the development of the Accounting

Conceptual Framework is provided. Also, specific changes and development of the conceptual

framework issued by the AASB is discussed. Further insights about the future direction and

development of conceptual framework is presented in this report.

MAIN BODY

1. Development of the Accounting Conceptual Framework

The Accounting framework is set by the Financial Accounting Standard Board (FASB).

The conceptual framework was presented in a sequence of 7 statements that consists of concepts

related to financial accounting in the late 1978. Later in 1989, the International Accounting

Standard Committee (IASC) developed a framework of the financial statements. The framework

provided by both the FASB and IASC were proved to be inconsistent and unclear (Huber, 2017).

In 2002, under the Norwalk agreement both the authorities jointly develops the accounting

standards and conceptual framework that was said to be more clear and consistent. This joint

project was then inserted in the both FASB and IASB agendas in 2004. It had been observed that

a general conceptual framework is needed as to tackle the accounting issues and would likely to

be help in development of standards which are based on accounting principles. Later in 2010, a

combined chapters were presented that deals with the financial reporting and to maintain quality

of the financial information. To provide integrity the fundamental characteristics to maintain

quality information is re-instated. However the ‘reliability’ is changed with ‘faithfulness’ and

‘relevance’ was unchanged. In the end of year 2010 the joint collaboration of FASB and IASB

got suspended. In 2012 IASB and in 2014, FASB restarted the accounting conceptual framework

project (Handley and et.al, 2020). The Board put focus on the presentation of the financial

reporting which would help the investors and stakeholders to determine the financial

performance. For this purpose the FASB presented a draft of the financial reporting framework

which was issued in 2016. Then in 2018 the IASB, with the revise International Financial

Reporting Standards (IRFS) issued Conceptual framework for accounting. The revise framework

consists of the objectives used for financial reporting, definition of asset, liability, income,

expenses and equity, concepts related to disclosure and maintenance of the capital. For the

companies that are uses conceptual framework for the purpose to create financial policies the

revised conceptual framework by IASB got effected on 2020.

development of conceptual framework is presented in this report.

MAIN BODY

1. Development of the Accounting Conceptual Framework

The Accounting framework is set by the Financial Accounting Standard Board (FASB).

The conceptual framework was presented in a sequence of 7 statements that consists of concepts

related to financial accounting in the late 1978. Later in 1989, the International Accounting

Standard Committee (IASC) developed a framework of the financial statements. The framework

provided by both the FASB and IASC were proved to be inconsistent and unclear (Huber, 2017).

In 2002, under the Norwalk agreement both the authorities jointly develops the accounting

standards and conceptual framework that was said to be more clear and consistent. This joint

project was then inserted in the both FASB and IASB agendas in 2004. It had been observed that

a general conceptual framework is needed as to tackle the accounting issues and would likely to

be help in development of standards which are based on accounting principles. Later in 2010, a

combined chapters were presented that deals with the financial reporting and to maintain quality

of the financial information. To provide integrity the fundamental characteristics to maintain

quality information is re-instated. However the ‘reliability’ is changed with ‘faithfulness’ and

‘relevance’ was unchanged. In the end of year 2010 the joint collaboration of FASB and IASB

got suspended. In 2012 IASB and in 2014, FASB restarted the accounting conceptual framework

project (Handley and et.al, 2020). The Board put focus on the presentation of the financial

reporting which would help the investors and stakeholders to determine the financial

performance. For this purpose the FASB presented a draft of the financial reporting framework

which was issued in 2016. Then in 2018 the IASB, with the revise International Financial

Reporting Standards (IRFS) issued Conceptual framework for accounting. The revise framework

consists of the objectives used for financial reporting, definition of asset, liability, income,

expenses and equity, concepts related to disclosure and maintenance of the capital. For the

companies that are uses conceptual framework for the purpose to create financial policies the

revised conceptual framework by IASB got effected on 2020.

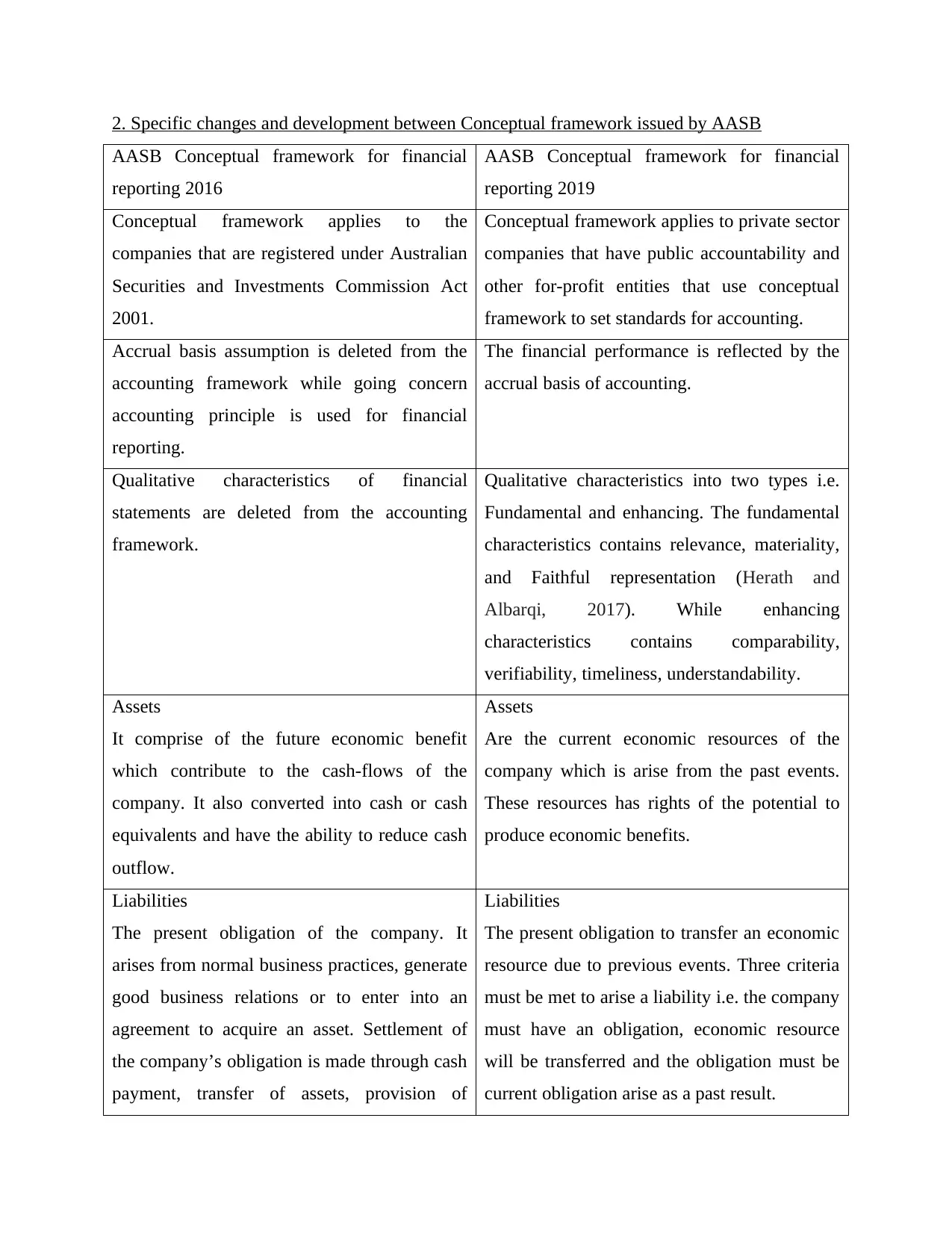

2. Specific changes and development between Conceptual framework issued by AASB

AASB Conceptual framework for financial

reporting 2016

AASB Conceptual framework for financial

reporting 2019

Conceptual framework applies to the

companies that are registered under Australian

Securities and Investments Commission Act

2001.

Conceptual framework applies to private sector

companies that have public accountability and

other for-profit entities that use conceptual

framework to set standards for accounting.

Accrual basis assumption is deleted from the

accounting framework while going concern

accounting principle is used for financial

reporting.

The financial performance is reflected by the

accrual basis of accounting.

Qualitative characteristics of financial

statements are deleted from the accounting

framework.

Qualitative characteristics into two types i.e.

Fundamental and enhancing. The fundamental

characteristics contains relevance, materiality,

and Faithful representation (Herath and

Albarqi, 2017). While enhancing

characteristics contains comparability,

verifiability, timeliness, understandability.

Assets

It comprise of the future economic benefit

which contribute to the cash-flows of the

company. It also converted into cash or cash

equivalents and have the ability to reduce cash

outflow.

Assets

Are the current economic resources of the

company which is arise from the past events.

These resources has rights of the potential to

produce economic benefits.

Liabilities

The present obligation of the company. It

arises from normal business practices, generate

good business relations or to enter into an

agreement to acquire an asset. Settlement of

the company’s obligation is made through cash

payment, transfer of assets, provision of

Liabilities

The present obligation to transfer an economic

resource due to previous events. Three criteria

must be met to arise a liability i.e. the company

must have an obligation, economic resource

will be transferred and the obligation must be

current obligation arise as a past result.

AASB Conceptual framework for financial

reporting 2016

AASB Conceptual framework for financial

reporting 2019

Conceptual framework applies to the

companies that are registered under Australian

Securities and Investments Commission Act

2001.

Conceptual framework applies to private sector

companies that have public accountability and

other for-profit entities that use conceptual

framework to set standards for accounting.

Accrual basis assumption is deleted from the

accounting framework while going concern

accounting principle is used for financial

reporting.

The financial performance is reflected by the

accrual basis of accounting.

Qualitative characteristics of financial

statements are deleted from the accounting

framework.

Qualitative characteristics into two types i.e.

Fundamental and enhancing. The fundamental

characteristics contains relevance, materiality,

and Faithful representation (Herath and

Albarqi, 2017). While enhancing

characteristics contains comparability,

verifiability, timeliness, understandability.

Assets

It comprise of the future economic benefit

which contribute to the cash-flows of the

company. It also converted into cash or cash

equivalents and have the ability to reduce cash

outflow.

Assets

Are the current economic resources of the

company which is arise from the past events.

These resources has rights of the potential to

produce economic benefits.

Liabilities

The present obligation of the company. It

arises from normal business practices, generate

good business relations or to enter into an

agreement to acquire an asset. Settlement of

the company’s obligation is made through cash

payment, transfer of assets, provision of

Liabilities

The present obligation to transfer an economic

resource due to previous events. Three criteria

must be met to arise a liability i.e. the company

must have an obligation, economic resource

will be transferred and the obligation must be

current obligation arise as a past result.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

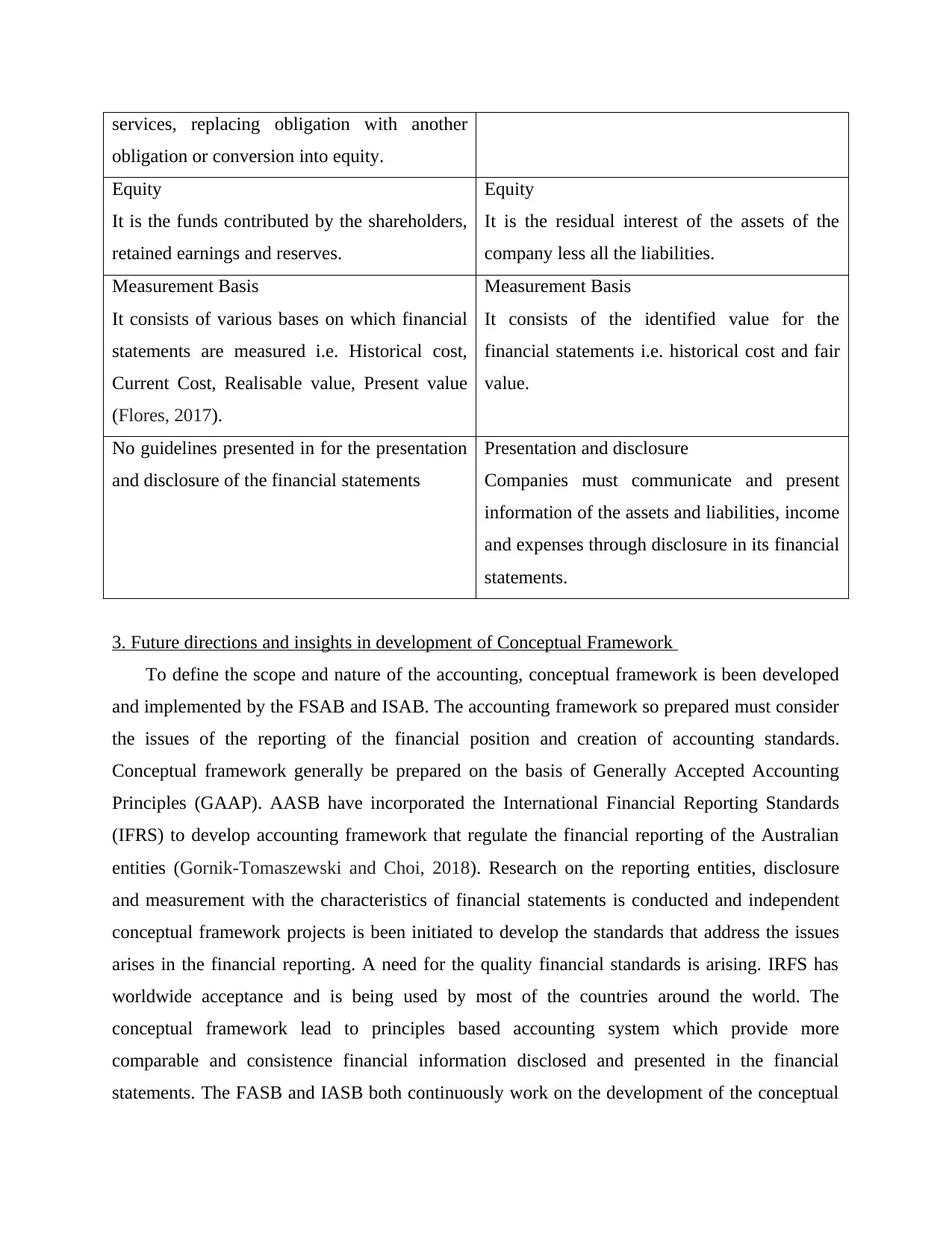

services, replacing obligation with another

obligation or conversion into equity.

Equity

It is the funds contributed by the shareholders,

retained earnings and reserves.

Equity

It is the residual interest of the assets of the

company less all the liabilities.

Measurement Basis

It consists of various bases on which financial

statements are measured i.e. Historical cost,

Current Cost, Realisable value, Present value

(Flores, 2017).

Measurement Basis

It consists of the identified value for the

financial statements i.e. historical cost and fair

value.

No guidelines presented in for the presentation

and disclosure of the financial statements

Presentation and disclosure

Companies must communicate and present

information of the assets and liabilities, income

and expenses through disclosure in its financial

statements.

3. Future directions and insights in development of Conceptual Framework

To define the scope and nature of the accounting, conceptual framework is been developed

and implemented by the FSAB and ISAB. The accounting framework so prepared must consider

the issues of the reporting of the financial position and creation of accounting standards.

Conceptual framework generally be prepared on the basis of Generally Accepted Accounting

Principles (GAAP). AASB have incorporated the International Financial Reporting Standards

(IFRS) to develop accounting framework that regulate the financial reporting of the Australian

entities (Gornik-Tomaszewski and Choi, 2018). Research on the reporting entities, disclosure

and measurement with the characteristics of financial statements is conducted and independent

conceptual framework projects is been initiated to develop the standards that address the issues

arises in the financial reporting. A need for the quality financial standards is arising. IRFS has

worldwide acceptance and is being used by most of the countries around the world. The

conceptual framework lead to principles based accounting system which provide more

comparable and consistence financial information disclosed and presented in the financial

statements. The FASB and IASB both continuously work on the development of the conceptual

obligation or conversion into equity.

Equity

It is the funds contributed by the shareholders,

retained earnings and reserves.

Equity

It is the residual interest of the assets of the

company less all the liabilities.

Measurement Basis

It consists of various bases on which financial

statements are measured i.e. Historical cost,

Current Cost, Realisable value, Present value

(Flores, 2017).

Measurement Basis

It consists of the identified value for the

financial statements i.e. historical cost and fair

value.

No guidelines presented in for the presentation

and disclosure of the financial statements

Presentation and disclosure

Companies must communicate and present

information of the assets and liabilities, income

and expenses through disclosure in its financial

statements.

3. Future directions and insights in development of Conceptual Framework

To define the scope and nature of the accounting, conceptual framework is been developed

and implemented by the FSAB and ISAB. The accounting framework so prepared must consider

the issues of the reporting of the financial position and creation of accounting standards.

Conceptual framework generally be prepared on the basis of Generally Accepted Accounting

Principles (GAAP). AASB have incorporated the International Financial Reporting Standards

(IFRS) to develop accounting framework that regulate the financial reporting of the Australian

entities (Gornik-Tomaszewski and Choi, 2018). Research on the reporting entities, disclosure

and measurement with the characteristics of financial statements is conducted and independent

conceptual framework projects is been initiated to develop the standards that address the issues

arises in the financial reporting. A need for the quality financial standards is arising. IRFS has

worldwide acceptance and is being used by most of the countries around the world. The

conceptual framework lead to principles based accounting system which provide more

comparable and consistence financial information disclosed and presented in the financial

statements. The FASB and IASB both continuously work on the development of the conceptual

framework of accounting. The AASB uses conceptual framework for financial reporting that is

consists of IFRS content (Walton, 2018). This conceptual framework provide assistance to the

AASB to prepare Australian Accounting Standards and policies. Conceptual framework are not

standards and are revised from time to time. It provide the basis for preparation of the standards.

Due to globalisation and expansion of the entities worldwide the business operations of the

entities are growing rapidly. The financial transactions are made rapidly and with the emergence

of the new technologies collection and recording of the financial information becomes easy

(Tudor, 2019). But the preparation and disclosure of the financial statements are mandatory

requirement that the companies have to fulfil. For to ensure quality in the reporting of the

financial information, companies follow accounting standards provided by the legal authorities.

These accounting standards are prepared on the basis of the conceptual framework that helps in

providing transparency and enable stakeholders of the company to take financial decisions. Also

help in regulators to analysis of the financial information and to take corrective actions. With the

increase in the awareness the importance of the financial reporting is also growing. Conceptual

framework provide a base on which relevant and quality standards are prepared which provide

clarity and consistency in the presentation of the financial information of the companies.

CONCLUSION

From the above study it has been concluded that in order to create conceptual framework for

accounting FASB and IASB played an important role. On the basis of which the AASB prepares

its conceptual framework (Kieso and et.al, 2020). It help in the development of the standards that

will provide guidance for reporting of the financial information and measurement, presentation

and disclosure of financial statements.

consists of IFRS content (Walton, 2018). This conceptual framework provide assistance to the

AASB to prepare Australian Accounting Standards and policies. Conceptual framework are not

standards and are revised from time to time. It provide the basis for preparation of the standards.

Due to globalisation and expansion of the entities worldwide the business operations of the

entities are growing rapidly. The financial transactions are made rapidly and with the emergence

of the new technologies collection and recording of the financial information becomes easy

(Tudor, 2019). But the preparation and disclosure of the financial statements are mandatory

requirement that the companies have to fulfil. For to ensure quality in the reporting of the

financial information, companies follow accounting standards provided by the legal authorities.

These accounting standards are prepared on the basis of the conceptual framework that helps in

providing transparency and enable stakeholders of the company to take financial decisions. Also

help in regulators to analysis of the financial information and to take corrective actions. With the

increase in the awareness the importance of the financial reporting is also growing. Conceptual

framework provide a base on which relevant and quality standards are prepared which provide

clarity and consistency in the presentation of the financial information of the companies.

CONCLUSION

From the above study it has been concluded that in order to create conceptual framework for

accounting FASB and IASB played an important role. On the basis of which the AASB prepares

its conceptual framework (Kieso and et.al, 2020). It help in the development of the standards that

will provide guidance for reporting of the financial information and measurement, presentation

and disclosure of financial statements.

REFERENCES

Books and Journals

Flores, N.E., 2017. Conceptual framework for nonmarket valuation. In A primer on nonmarket

valuation (pp. 27-54). Springer, Dordrecht.

Gornik-Tomaszewski, S. and Choi, Y.C., 2018. The conceptual framework: past, present, and

future. Review of Business, 38(1), pp.47-58.

Handley and et.al, 2020. Understanding participation in accounting standard‐setting: the case of

AASB ED 192 Revised Differential Reporting Framework. Accounting & Finance, 60(4),

pp.3621-3645.

Herath, S.K. and Albarqi, N., 2017. Financial reporting quality: A literature review. International

Journal of Business Management and Commerce, 2(2), pp.1-14.

Huber, W.D., 2017. Irreconcilable differences? The FASB's conceptual framework and the

public interest. International Journal of Critical Accounting, 9(5-6), pp.514-523.

Kieso and et.al, 2020. Intermediate accounting IFRS. John Wiley & Sons.

Tudor, L.A., 2019, September. The Effects of Globalization on Financial Reporting. In 12th

Annual Conference of the EuroMed Academy of Business.

Walton, P., 2018. Discussion of barker and Teixeira ([2018]. Gaps in the IFRS conceptual

framework. Accounting in Europe, 15) and Van Mourik and Katsuo ([2018]. Profit or loss in the

IASB conceptual framework. Accounting in Europe, 15). Accounting in Europe, 15(2), pp.193-

199.

Online

Conceptual Framework for Financial Reporting, 2021. [Online]. Available through <

https://www.ifrs.org/issued-standards/list-of-standards/conceptual-framework/ >

MANAGEMENT ACCOUNTING, 2021. [Online]. Available through <

https://www.cpaaustralia.com.au/cpa-program/foundation-exams/structure/management-

accounting>

Books and Journals

Flores, N.E., 2017. Conceptual framework for nonmarket valuation. In A primer on nonmarket

valuation (pp. 27-54). Springer, Dordrecht.

Gornik-Tomaszewski, S. and Choi, Y.C., 2018. The conceptual framework: past, present, and

future. Review of Business, 38(1), pp.47-58.

Handley and et.al, 2020. Understanding participation in accounting standard‐setting: the case of

AASB ED 192 Revised Differential Reporting Framework. Accounting & Finance, 60(4),

pp.3621-3645.

Herath, S.K. and Albarqi, N., 2017. Financial reporting quality: A literature review. International

Journal of Business Management and Commerce, 2(2), pp.1-14.

Huber, W.D., 2017. Irreconcilable differences? The FASB's conceptual framework and the

public interest. International Journal of Critical Accounting, 9(5-6), pp.514-523.

Kieso and et.al, 2020. Intermediate accounting IFRS. John Wiley & Sons.

Tudor, L.A., 2019, September. The Effects of Globalization on Financial Reporting. In 12th

Annual Conference of the EuroMed Academy of Business.

Walton, P., 2018. Discussion of barker and Teixeira ([2018]. Gaps in the IFRS conceptual

framework. Accounting in Europe, 15) and Van Mourik and Katsuo ([2018]. Profit or loss in the

IASB conceptual framework. Accounting in Europe, 15). Accounting in Europe, 15(2), pp.193-

199.

Online

Conceptual Framework for Financial Reporting, 2021. [Online]. Available through <

https://www.ifrs.org/issued-standards/list-of-standards/conceptual-framework/ >

MANAGEMENT ACCOUNTING, 2021. [Online]. Available through <

https://www.cpaaustralia.com.au/cpa-program/foundation-exams/structure/management-

accounting>

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.