Management Accounting Report: Prime Furniture and TESCO Analysis

VerifiedAdded on 2023/01/12

|10

|2473

|53

Report

AI Summary

This report delves into the core concepts of management accounting, examining the calculation of income statements using both marginal and absorption costing methods. It provides a comparative analysis of these costing techniques, highlighting their impact on profit calculation and the valuation of closing stock, using Prime Furniture Ltd as a case study. The report further investigates the advantages and disadvantages of various planning tools employed for budgetary control, with a specific focus on the context of TESCO plc ltd. It explores the merits and demerits of budgetary control, including its role in cost reduction, performance measurement, and employee motivation, while also addressing potential drawbacks such as time consumption and the potential for inter-departmental conflicts. Finally, the report compares how different organizations utilize management accounting techniques to address diverse financial challenges. This includes examining cost accounting, inventory management, and the application of tools like the Balanced Scorecard and Key Performance Indicators, providing insights into how businesses adapt management accounting to improve their financial performance. The report concludes by summarizing the key findings and emphasizing the relevance of management accounting in addressing financial issues across different organizational contexts.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 2............................................................................................................................................3

P3 Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs of Prime Furniture Ltd......................................3

TASK 3............................................................................................................................................5

P4 Explanation of advantages and disadvantages of various planning tools used for budgetary

control..........................................................................................................................................5

TASK 4............................................................................................................................................7

P5 Comparison of how different organisations are using management accounting techniques to

respond to different financial problems.......................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

2

INTRODUCTION...........................................................................................................................3

TASK 2............................................................................................................................................3

P3 Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs of Prime Furniture Ltd......................................3

TASK 3............................................................................................................................................5

P4 Explanation of advantages and disadvantages of various planning tools used for budgetary

control..........................................................................................................................................5

TASK 4............................................................................................................................................7

P5 Comparison of how different organisations are using management accounting techniques to

respond to different financial problems.......................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

2

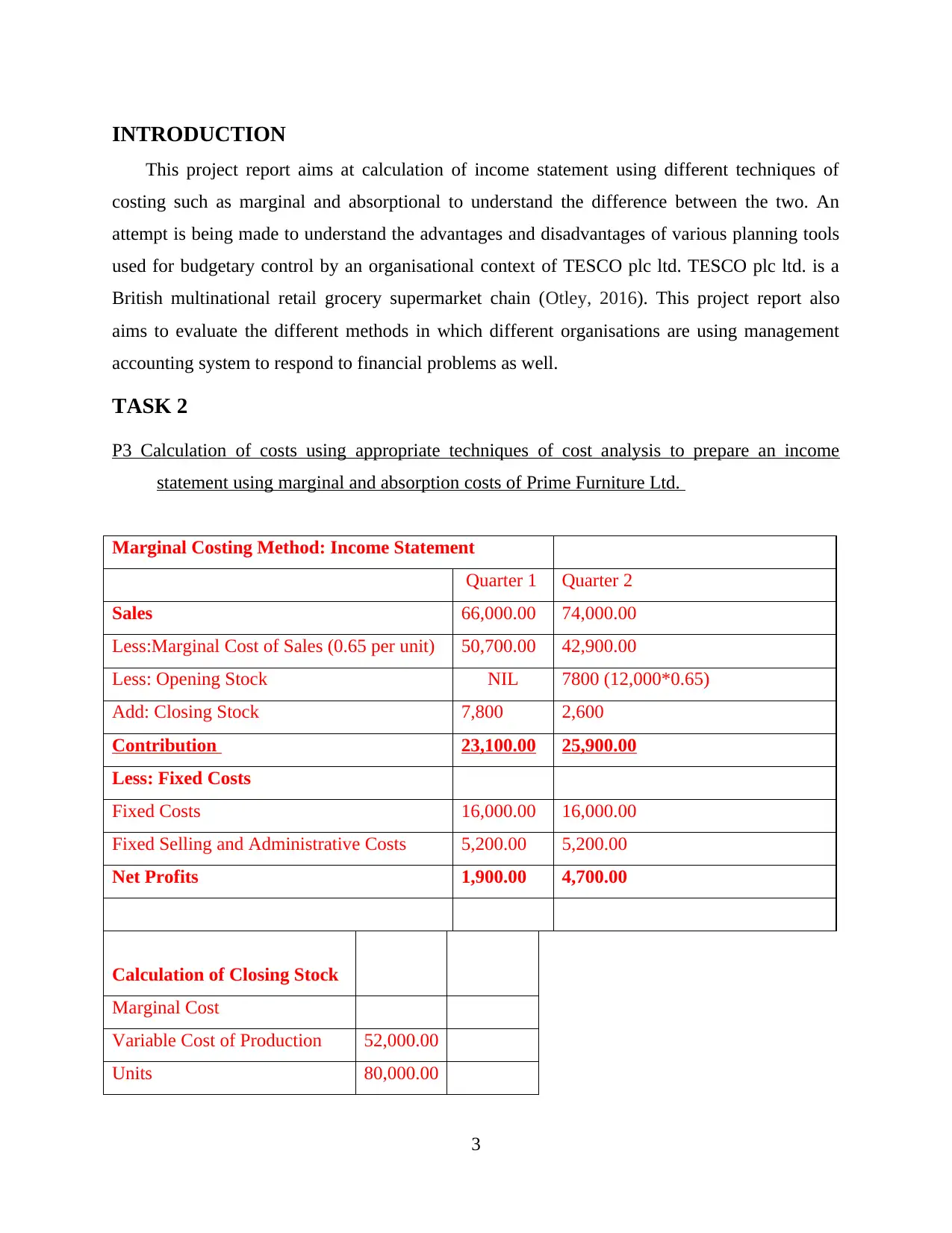

INTRODUCTION

This project report aims at calculation of income statement using different techniques of

costing such as marginal and absorptional to understand the difference between the two. An

attempt is being made to understand the advantages and disadvantages of various planning tools

used for budgetary control by an organisational context of TESCO plc ltd. TESCO plc ltd. is a

British multinational retail grocery supermarket chain (Otley, 2016). This project report also

aims to evaluate the different methods in which different organisations are using management

accounting system to respond to financial problems as well.

TASK 2

P3 Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs of Prime Furniture Ltd.

Marginal Costing Method: Income Statement

Quarter 1 Quarter 2

Sales 66,000.00 74,000.00

Less:Marginal Cost of Sales (0.65 per unit) 50,700.00 42,900.00

Less: Opening Stock NIL 7800 (12,000*0.65)

Add: Closing Stock 7,800 2,600

Contribution 23,100.00 25,900.00

Less: Fixed Costs

Fixed Costs 16,000.00 16,000.00

Fixed Selling and Administrative Costs 5,200.00 5,200.00

Net Profits 1,900.00 4,700.00

Calculation of Closing Stock

Marginal Cost

Variable Cost of Production 52,000.00

Units 80,000.00

3

This project report aims at calculation of income statement using different techniques of

costing such as marginal and absorptional to understand the difference between the two. An

attempt is being made to understand the advantages and disadvantages of various planning tools

used for budgetary control by an organisational context of TESCO plc ltd. TESCO plc ltd. is a

British multinational retail grocery supermarket chain (Otley, 2016). This project report also

aims to evaluate the different methods in which different organisations are using management

accounting system to respond to financial problems as well.

TASK 2

P3 Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs of Prime Furniture Ltd.

Marginal Costing Method: Income Statement

Quarter 1 Quarter 2

Sales 66,000.00 74,000.00

Less:Marginal Cost of Sales (0.65 per unit) 50,700.00 42,900.00

Less: Opening Stock NIL 7800 (12,000*0.65)

Add: Closing Stock 7,800 2,600

Contribution 23,100.00 25,900.00

Less: Fixed Costs

Fixed Costs 16,000.00 16,000.00

Fixed Selling and Administrative Costs 5,200.00 5,200.00

Net Profits 1,900.00 4,700.00

Calculation of Closing Stock

Marginal Cost

Variable Cost of Production 52,000.00

Units 80,000.00

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost per unit 0.65 0.65

Closing Stock units 12,000 4,000

Value of Closing Stock 7,800 2,600

Absorption Costing Method: Income Statement

Quarter 1 Quarter 2

Sales 66,000.00 74,000.00

Less: Cost of Sales

Marginal cost of sales (0.65 p/u) 50,700.00 42,900.00

Fixed cost of production 16,000.00 16,000.00

Less: Opening Stock NIL 10,200 (12,000*0.85)

Add: Closing Stock 10,200.00 3,560.00

Gross profit: 9,500.00 8,460.00

Less: Selling & Administration cost

Fixed Selling and Administrative Costs 5,200.00 5,200.00

Net Profits 4,300.00 3,260.00

Calculation of Closing Stock

Absorption Cost Q1 Q2

Variable Cost of Production 50,700 42,900

Fixed Cost of Production 16,000 16,000

66,700 58,900

Units 78,000.00 66,000.00

Cost per unit 0.85 0.89

Closing Stock units 12,000 4,000

Value of Closing Stock 10,200 3560

Reconcilation of Profits:

Quarter 1:

4

Closing Stock units 12,000 4,000

Value of Closing Stock 7,800 2,600

Absorption Costing Method: Income Statement

Quarter 1 Quarter 2

Sales 66,000.00 74,000.00

Less: Cost of Sales

Marginal cost of sales (0.65 p/u) 50,700.00 42,900.00

Fixed cost of production 16,000.00 16,000.00

Less: Opening Stock NIL 10,200 (12,000*0.85)

Add: Closing Stock 10,200.00 3,560.00

Gross profit: 9,500.00 8,460.00

Less: Selling & Administration cost

Fixed Selling and Administrative Costs 5,200.00 5,200.00

Net Profits 4,300.00 3,260.00

Calculation of Closing Stock

Absorption Cost Q1 Q2

Variable Cost of Production 50,700 42,900

Fixed Cost of Production 16,000 16,000

66,700 58,900

Units 78,000.00 66,000.00

Cost per unit 0.85 0.89

Closing Stock units 12,000 4,000

Value of Closing Stock 10,200 3560

Reconcilation of Profits:

Quarter 1:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Difference in profit: 4,300 – 1,900 = 2400

Overabsorption of fixed costs in valuation of closing stock in absorptional costing = 10,200-

7,800 = 2,400.

Therefore, difference in profits = overabsorption of fixed costs in valuation of fixed costs.

Quarter 2:

Difference in profit: 3,260 – 4,700 = 1,440

Overabsorption of fixed costs in valuation of closing stock in absorptional costing =

(10,200-7,800) – (3,560-2600) = 2,400 - 960 = 1,440

Therefore, difference in profits = overabsorption of fixed costs in valuation of fixed costs.

The difference in amount of profit of Prime Furniture calculated under both the methods of

absorptional and marginal costing is due to the difference in amount of closing stock. Closing

stock is valued at only variable cost of production under marginal costing method which leads to

an increase in the amount of profit whereas under absorptional costing, closing stock is valued at

total cost of production which included both variable and fixed manufacturing costs which leads

to a decrease in the amount of profit (Malmi, 2016). Absorptional costing is considered as the

more appropriate method out of the two since it values the closing stock at the total cost of

production and not only variable cost which is arguably the right approach.

TASK 3

P4 Explanation of advantages and disadvantages of various planning tools used for budgetary

control.

Budgetary control is one of the most important tool of management accounting which

helps the managers to effectively manage and control the operations of the organisation

(Management accounting- meaning, advantages and functions, 2019). Some of the main budgets

prepared by the management of the TESCO plc ltd include:

Capital budget: Capital budget is prepared to evaluate the various alternative of capital

expenditure than the TESCO has and then taking a decision based on the evaluation as to invest

in which of the project according to profitability and maturity period.

Cash budget: This budget is prepared to determine the cash requirements of the company

and ascertaining sources of liquidity and cash inflows within a specific time period.

5

Overabsorption of fixed costs in valuation of closing stock in absorptional costing = 10,200-

7,800 = 2,400.

Therefore, difference in profits = overabsorption of fixed costs in valuation of fixed costs.

Quarter 2:

Difference in profit: 3,260 – 4,700 = 1,440

Overabsorption of fixed costs in valuation of closing stock in absorptional costing =

(10,200-7,800) – (3,560-2600) = 2,400 - 960 = 1,440

Therefore, difference in profits = overabsorption of fixed costs in valuation of fixed costs.

The difference in amount of profit of Prime Furniture calculated under both the methods of

absorptional and marginal costing is due to the difference in amount of closing stock. Closing

stock is valued at only variable cost of production under marginal costing method which leads to

an increase in the amount of profit whereas under absorptional costing, closing stock is valued at

total cost of production which included both variable and fixed manufacturing costs which leads

to a decrease in the amount of profit (Malmi, 2016). Absorptional costing is considered as the

more appropriate method out of the two since it values the closing stock at the total cost of

production and not only variable cost which is arguably the right approach.

TASK 3

P4 Explanation of advantages and disadvantages of various planning tools used for budgetary

control.

Budgetary control is one of the most important tool of management accounting which

helps the managers to effectively manage and control the operations of the organisation

(Management accounting- meaning, advantages and functions, 2019). Some of the main budgets

prepared by the management of the TESCO plc ltd include:

Capital budget: Capital budget is prepared to evaluate the various alternative of capital

expenditure than the TESCO has and then taking a decision based on the evaluation as to invest

in which of the project according to profitability and maturity period.

Cash budget: This budget is prepared to determine the cash requirements of the company

and ascertaining sources of liquidity and cash inflows within a specific time period.

5

Operational budget: This budget is prepared to determine performance standards and

targets for operational department such as production department, sales department etcetera.

Budgetary control has both advantages and disadvantages in an organisation context.

Some of the merits and demerits of budgetary control are as follows:

Advantages of Budgetary control:

Reduction in costs: Budgetary control helps the management of TESCO plc ltd to reduce

the cost of production and various costs which are involved in the operations of the organisations

(Advantages of budgetary control, 2017). It aims at optimum utilisation of resources and ensures

that no wastage of resource is being done in the production and manufacturing process of the

organisation because preparation of budget doesn’t include a provision of wastage and these

wastage and increase in costs can be easily identified upon comparison between actual

performance and standard performance.

Tools for measurement of performance: Budgetary control act as important tool which

helps the management to measure the performance of its employees and teams against a standard

which helps in achieving organisational objectives and targets.

Specific aims: Budget preparation helps in determination of standard of performance for

each and every employee of the organisation which makes the employees aware of the efficiency

expected out of them and helps in fixing specific aims.

Improving employee motivation: Budgetary control is an important management tool

used by TESCO plc ltd for monitoring and controlling and employees know that their

performance is being evaluated at every point in time which increases their motivation to

perform to their best potential and efficiency in desire of achieving rewards linked to

performance targets.

Disadvantages of Budgetary control:

Timely and costly: Preparation of budget and budgetary control is a very timely process

and requires a lot of human efforts and costs (Evans and Mason, 2018). The management of

TESCO plc ltd makes sure that the cost involved in preparation of budget is not more than the

benefits derived out of its implementation.

Uncertainty: Budgetary control is based on budgets which are prepared with the help of

forecasts made by the management for future business conditions and environments which is

6

targets for operational department such as production department, sales department etcetera.

Budgetary control has both advantages and disadvantages in an organisation context.

Some of the merits and demerits of budgetary control are as follows:

Advantages of Budgetary control:

Reduction in costs: Budgetary control helps the management of TESCO plc ltd to reduce

the cost of production and various costs which are involved in the operations of the organisations

(Advantages of budgetary control, 2017). It aims at optimum utilisation of resources and ensures

that no wastage of resource is being done in the production and manufacturing process of the

organisation because preparation of budget doesn’t include a provision of wastage and these

wastage and increase in costs can be easily identified upon comparison between actual

performance and standard performance.

Tools for measurement of performance: Budgetary control act as important tool which

helps the management to measure the performance of its employees and teams against a standard

which helps in achieving organisational objectives and targets.

Specific aims: Budget preparation helps in determination of standard of performance for

each and every employee of the organisation which makes the employees aware of the efficiency

expected out of them and helps in fixing specific aims.

Improving employee motivation: Budgetary control is an important management tool

used by TESCO plc ltd for monitoring and controlling and employees know that their

performance is being evaluated at every point in time which increases their motivation to

perform to their best potential and efficiency in desire of achieving rewards linked to

performance targets.

Disadvantages of Budgetary control:

Timely and costly: Preparation of budget and budgetary control is a very timely process

and requires a lot of human efforts and costs (Evans and Mason, 2018). The management of

TESCO plc ltd makes sure that the cost involved in preparation of budget is not more than the

benefits derived out of its implementation.

Uncertainty: Budgetary control is based on budgets which are prepared with the help of

forecasts made by the management for future business conditions and environments which is

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

highly dynamic and uncertain. So the budgetary control has a feature of uncertainty and can’t be

held true in every business condition.

Inter-departmental disputes: Budgetary control paves way for inter-departmental

conflicts and disputes in every organisation to some extent or other due to a difference in

personal interest and the desire for every department to come out as the best performer.

Tool of restriction: Budgets are often perceived as tools of restriction used by the

management to set a limit on expenditure and activities within the organisation for the

employees. This leads to demotivation of members and hinders the application of creative skills

and talents by the employees which might help the organisation to get a competitive edge in the

industry. It hinders the process of creativity.

TASK 4

P5 Comparison of how different organisations are using management accounting techniques to

respond to different financial problems.

Management accounting systems are very helpful for any organisation to respond and

solve financial problems as well (What is managerial accounting, 2020). Here is an example of

how different management accounting systems are being used by different organisation to solve

different problems related to the financial performance of the company:

Cost accounting:

The management of Prime Furnitures Ltd. recently encountered a problem of a sudden

increase in costs of production which badly affected the profitability of the company. The

managers analysed the periodic cost sheet prepared by the management accountants of the

company and identified that the rise in cost of production was due to a lot of wastage being done

in the production process due to outdates machinery and thus the management was able to solve

this problem by replacing the machinery (Drury, 2013). The same management accounting

concept was used by the managers of TESCO plc ltd in a very different way to calculate the

profit margin and offer additional discount on its products to attract a larger customer base and

increase the sales of the company to achieve organisational goals and targets.

Inventory management:

Inventory management concepts are being used the Prime Furniture to decrease the

storage costs related to the inventory and stock to increase operational efficiency and financial

7

held true in every business condition.

Inter-departmental disputes: Budgetary control paves way for inter-departmental

conflicts and disputes in every organisation to some extent or other due to a difference in

personal interest and the desire for every department to come out as the best performer.

Tool of restriction: Budgets are often perceived as tools of restriction used by the

management to set a limit on expenditure and activities within the organisation for the

employees. This leads to demotivation of members and hinders the application of creative skills

and talents by the employees which might help the organisation to get a competitive edge in the

industry. It hinders the process of creativity.

TASK 4

P5 Comparison of how different organisations are using management accounting techniques to

respond to different financial problems.

Management accounting systems are very helpful for any organisation to respond and

solve financial problems as well (What is managerial accounting, 2020). Here is an example of

how different management accounting systems are being used by different organisation to solve

different problems related to the financial performance of the company:

Cost accounting:

The management of Prime Furnitures Ltd. recently encountered a problem of a sudden

increase in costs of production which badly affected the profitability of the company. The

managers analysed the periodic cost sheet prepared by the management accountants of the

company and identified that the rise in cost of production was due to a lot of wastage being done

in the production process due to outdates machinery and thus the management was able to solve

this problem by replacing the machinery (Drury, 2013). The same management accounting

concept was used by the managers of TESCO plc ltd in a very different way to calculate the

profit margin and offer additional discount on its products to attract a larger customer base and

increase the sales of the company to achieve organisational goals and targets.

Inventory management:

Inventory management concepts are being used the Prime Furniture to decrease the

storage costs related to the inventory and stock to increase operational efficiency and financial

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance of the company, the company was facing a problem of increase storage cost of the

inventory and hence an optimum level of stock helped the company to overcome that problem

with inventory management. TESCO plc ltd. has a number of suppliers from distant areas which

results in a high ordering and carrying costs. The management of the company used the tools of

inventory management to determine an economical order quantity based on its inventory

requirements throughout a certain period which resulted in decreased costs and better operational

profit for the company.

Use of Balanced Score Card by TESCO Ltd:

Balanced Score Card can be defined as a framework which is being used by business

managers as a tool of management accounting to translate the goals and objectives of the

organisation into different set of standards used for measurement of performance and

effectiveness. Four different perspectives can be used by the management of any organisation

under this approach to evaluate the operations of the company which are financial perspective,

customer service perspective, business internal perspective and innovation perspective

(Nørreklit, Kure and Trenca, 2018). The management of TESCO Ltd. uses this approach to

evaluate the performance of the company beyond the traditional notion of economic benefits and

profits. Customer service along with innovation and learning perspective is the primary objective

of management of TESCO Ltd. which is being used for measurement of the company’s

performance. A high score on both these areas determines the effectiveness of the company in

meeting the objectives and vision of the organisation.

Use of Key Performance Indicators by Prime Furnitures Ltd:

Key Performance Indicators refers to a measurable value which is used to demonstrate

the effectiveness of a business organisation in achieving the objectives and goals of the

company. It is one of the most important tool of management accounting used to determine

business success (Parmenter, 2015). For example, the management of Prime Furnitures

determines the Key Performance Indicators for the organisation on the basis of business strategy

and objectives. Further, by evaluation of those KPIs, the management of the company is able to

picture the effectiveness of the company in meeting and accomplishing business objectives and

goals. Customer retention rate is one of the key performance indicator for the management of

Prime Furnitures Ltd. and by assessment of the increase or decrease in the customer retention

8

inventory and hence an optimum level of stock helped the company to overcome that problem

with inventory management. TESCO plc ltd. has a number of suppliers from distant areas which

results in a high ordering and carrying costs. The management of the company used the tools of

inventory management to determine an economical order quantity based on its inventory

requirements throughout a certain period which resulted in decreased costs and better operational

profit for the company.

Use of Balanced Score Card by TESCO Ltd:

Balanced Score Card can be defined as a framework which is being used by business

managers as a tool of management accounting to translate the goals and objectives of the

organisation into different set of standards used for measurement of performance and

effectiveness. Four different perspectives can be used by the management of any organisation

under this approach to evaluate the operations of the company which are financial perspective,

customer service perspective, business internal perspective and innovation perspective

(Nørreklit, Kure and Trenca, 2018). The management of TESCO Ltd. uses this approach to

evaluate the performance of the company beyond the traditional notion of economic benefits and

profits. Customer service along with innovation and learning perspective is the primary objective

of management of TESCO Ltd. which is being used for measurement of the company’s

performance. A high score on both these areas determines the effectiveness of the company in

meeting the objectives and vision of the organisation.

Use of Key Performance Indicators by Prime Furnitures Ltd:

Key Performance Indicators refers to a measurable value which is used to demonstrate

the effectiveness of a business organisation in achieving the objectives and goals of the

company. It is one of the most important tool of management accounting used to determine

business success (Parmenter, 2015). For example, the management of Prime Furnitures

determines the Key Performance Indicators for the organisation on the basis of business strategy

and objectives. Further, by evaluation of those KPIs, the management of the company is able to

picture the effectiveness of the company in meeting and accomplishing business objectives and

goals. Customer retention rate is one of the key performance indicator for the management of

Prime Furnitures Ltd. and by assessment of the increase or decrease in the customer retention

8

rate over a period of time, management of the company is able to determine whether

organisational goals and objectives are being achieved or not.

Thus, it can be said that management accounting concepts are contrast being used by

different organisation to respond to the financial problems of the organisation as well (Ward,

2012). This adds to the importance and popularity of management accounting as an

unconventional concept of business organisations.

CONCLUSION

It can be concluded from the above report that absorption and marginal costing methods of

preparing income statement value closing stock using different methods which leads to a

difference in the amount of net profits. It can also be concluded that the various planning tools

used for budgetary control have advantages such as tool for measurement but at the same time

they are costly and require a lot of time and efforts (Cadez and Guilding, 2012). At last, it can be

concluded that management accounting system and concept are being used different by

organisations such as TESCO and Prime Furnitures to respond to different financial problems. It

can be inferred that management accounting is no more an optional practice but is crucial for

every business organisation to monitor its operations and exercise effective control.

9

organisational goals and objectives are being achieved or not.

Thus, it can be said that management accounting concepts are contrast being used by

different organisation to respond to the financial problems of the organisation as well (Ward,

2012). This adds to the importance and popularity of management accounting as an

unconventional concept of business organisations.

CONCLUSION

It can be concluded from the above report that absorption and marginal costing methods of

preparing income statement value closing stock using different methods which leads to a

difference in the amount of net profits. It can also be concluded that the various planning tools

used for budgetary control have advantages such as tool for measurement but at the same time

they are costly and require a lot of time and efforts (Cadez and Guilding, 2012). At last, it can be

concluded that management accounting system and concept are being used different by

organisations such as TESCO and Prime Furnitures to respond to different financial problems. It

can be inferred that management accounting is no more an optional practice but is crucial for

every business organisation to monitor its operations and exercise effective control.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Cadez, S. and Guilding, C., 2012. Strategy, strategic management accounting and performance: a

configurational analysis. Industrial Management & Data Systems.

Drury, C.M., 2013. Management and cost accounting. Springer.

Evans, B. and Mason, R., 2018. The lean supply chain: managing the challenge at Tesco. Kogan

Page Publishers.

Hiebl, M.R., 2014. Upper echelons theory in management accounting and control

research. Journal of Management Control. 24(3). pp.223-240.

Malmi, T., 2016. Managerialist studies in management accounting: 1990–2014. Management

Accounting Research. 31. pp.31-44.

Nørreklit, H., Kure, N. and Trenca, M., 2018. Balanced Scorecard. The International

Encyclopedia of Strategic Communication, pp.1-6.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Parmenter, D., 2015. Key performance indicators: developing, implementing, and using winning

KPIs. John Wiley & Sons.

Ward, K., 2012. Strategic management accounting. Routledge.

Online

Advantages of budgetary control. 2017. [Online]. Available through<

https://hmhub.me/budgetary-control-advantages-disadvantages/>.

Management accounting- meaning, advantages and functions. 2019. [Online]. Available

through< https://cleartax.in/s/management-accounting>.

What is managerial accounting. 2020. [Online]. Available through<

https://www.investopedia.com/terms/m/managerialaccounting.asp>.

10

Books and Journals

Cadez, S. and Guilding, C., 2012. Strategy, strategic management accounting and performance: a

configurational analysis. Industrial Management & Data Systems.

Drury, C.M., 2013. Management and cost accounting. Springer.

Evans, B. and Mason, R., 2018. The lean supply chain: managing the challenge at Tesco. Kogan

Page Publishers.

Hiebl, M.R., 2014. Upper echelons theory in management accounting and control

research. Journal of Management Control. 24(3). pp.223-240.

Malmi, T., 2016. Managerialist studies in management accounting: 1990–2014. Management

Accounting Research. 31. pp.31-44.

Nørreklit, H., Kure, N. and Trenca, M., 2018. Balanced Scorecard. The International

Encyclopedia of Strategic Communication, pp.1-6.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Parmenter, D., 2015. Key performance indicators: developing, implementing, and using winning

KPIs. John Wiley & Sons.

Ward, K., 2012. Strategic management accounting. Routledge.

Online

Advantages of budgetary control. 2017. [Online]. Available through<

https://hmhub.me/budgetary-control-advantages-disadvantages/>.

Management accounting- meaning, advantages and functions. 2019. [Online]. Available

through< https://cleartax.in/s/management-accounting>.

What is managerial accounting. 2020. [Online]. Available through<

https://www.investopedia.com/terms/m/managerialaccounting.asp>.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.