Management Accounting Report: Systems, Tools, Techniques, and Analysis

VerifiedAdded on 2023/01/16

|15

|4196

|27

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and practices, focusing on their application within Excite Entertainment Ltd, a UK-based leisure and entertainment company. The report begins by defining management accounting and differentiating it from financial accounting. It then delves into various management accounting systems, including cost accounting, inventory management, and job costing, detailing their benefits and specific applications within the company. The report further examines different types of managerial accounting reports, such as performance reports, accounts receivable reports, and budget reports, emphasizing the importance of accurate, relevant, and up-to-date information. The integration of these reports and systems for organizational processing is also discussed. A critical evaluation of marginal and absorption costing methods follows, highlighting their advantages and disadvantages. The report then compares and contrasts three planning tools, providing insights into their effectiveness. Finally, the report addresses strategies for preventing financial problems, offering practical recommendations for Excite Entertainment Ltd. The analysis covers the company's operations in promoting festivals and concerts across the UK, providing a practical context for the discussed concepts.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Section A......................................................................................................................................3

(a) Management Accounting Systems:........................................................................................3

(b) Cost accounting system: ........................................................................................................4

(c) Inventory management systems:............................................................................................5

(d) Job Costing Systems:.............................................................................................................6

(e) Benefits of above mentioned accounting systems: ................................................................6

Section B......................................................................................................................................7

(a) Various kinds of managerial accounting report.....................................................................7

(b) Why should information should be accurate, relevant and up to date...................................7

(c) Integration between accounting reports and system for organisational processing...............7

TASK 2............................................................................................................................................8

Critically evaluation of marginal and absorption costing method...............................................8

TASK 3..........................................................................................................................................10

Compare and Contrast three planning tool................................................................................10

TASK 4..........................................................................................................................................11

Preventing from financial problem............................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Section A......................................................................................................................................3

(a) Management Accounting Systems:........................................................................................3

(b) Cost accounting system: ........................................................................................................4

(c) Inventory management systems:............................................................................................5

(d) Job Costing Systems:.............................................................................................................6

(e) Benefits of above mentioned accounting systems: ................................................................6

Section B......................................................................................................................................7

(a) Various kinds of managerial accounting report.....................................................................7

(b) Why should information should be accurate, relevant and up to date...................................7

(c) Integration between accounting reports and system for organisational processing...............7

TASK 2............................................................................................................................................8

Critically evaluation of marginal and absorption costing method...............................................8

TASK 3..........................................................................................................................................10

Compare and Contrast three planning tool................................................................................10

TASK 4..........................................................................................................................................11

Preventing from financial problem............................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Managerial accounting is the contemporary area of accounting that is oriented on the

mechanism of recognizing, assessing, analysing, interpreting, projecting and transmitting the

information to support decision-making procedure with aim to achieve organisational objectives.

This is wider field which deals with all the major aspects of management and accounting.

Managing and accounting officials are main players in management accounting structure as they

handle all the key operations related to management accounting. Management accounting in

organisation required for effective budgeting, planning and assessment of real-time performance

of company (Amahalu, Nweze and Chinyere, 2017) .

This study covers all the major aspects and areas of management accounting like systems,

reports and other concerned tools and techniques in context of Excite Entertainment Ltd. Study

consist of differences among management and financial accounting. Selected corporation Excite

Entertainment Ltd is related to UK's leisures and entertainment sector. Company is engaged in

operations of promoting festivals and concerts at different locations across the UK. Study also

contains comprehensive discussion on planning tools as well as at what extent these help in

effective responding to company's financial issues.

TASK 1

Section A

(a) Management Accounting Systems:

Management Accounting implies to organisational mechanism which collects all the raw

details, facts and information within organisation and transform it in meaningful and relevant

information, primarily for the purpose of decision-making. This is the technique commonly used

by large number of business organisation in order to identify their status. Once it has been

analysed, managers will be able to plan strategies and policies in order to accomplish their goals

and objectives in an effective manner. Management accounting is some times linked to financial

management but these both are two different aspects (Busco and Quattrone, 2018). Here

following is discussion on crucial differences among financial and managerial/management

accounting, as follows:

Managerial accounting is the contemporary area of accounting that is oriented on the

mechanism of recognizing, assessing, analysing, interpreting, projecting and transmitting the

information to support decision-making procedure with aim to achieve organisational objectives.

This is wider field which deals with all the major aspects of management and accounting.

Managing and accounting officials are main players in management accounting structure as they

handle all the key operations related to management accounting. Management accounting in

organisation required for effective budgeting, planning and assessment of real-time performance

of company (Amahalu, Nweze and Chinyere, 2017) .

This study covers all the major aspects and areas of management accounting like systems,

reports and other concerned tools and techniques in context of Excite Entertainment Ltd. Study

consist of differences among management and financial accounting. Selected corporation Excite

Entertainment Ltd is related to UK's leisures and entertainment sector. Company is engaged in

operations of promoting festivals and concerts at different locations across the UK. Study also

contains comprehensive discussion on planning tools as well as at what extent these help in

effective responding to company's financial issues.

TASK 1

Section A

(a) Management Accounting Systems:

Management Accounting implies to organisational mechanism which collects all the raw

details, facts and information within organisation and transform it in meaningful and relevant

information, primarily for the purpose of decision-making. This is the technique commonly used

by large number of business organisation in order to identify their status. Once it has been

analysed, managers will be able to plan strategies and policies in order to accomplish their goals

and objectives in an effective manner. Management accounting is some times linked to financial

management but these both are two different aspects (Busco and Quattrone, 2018). Here

following is discussion on crucial differences among financial and managerial/management

accounting, as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

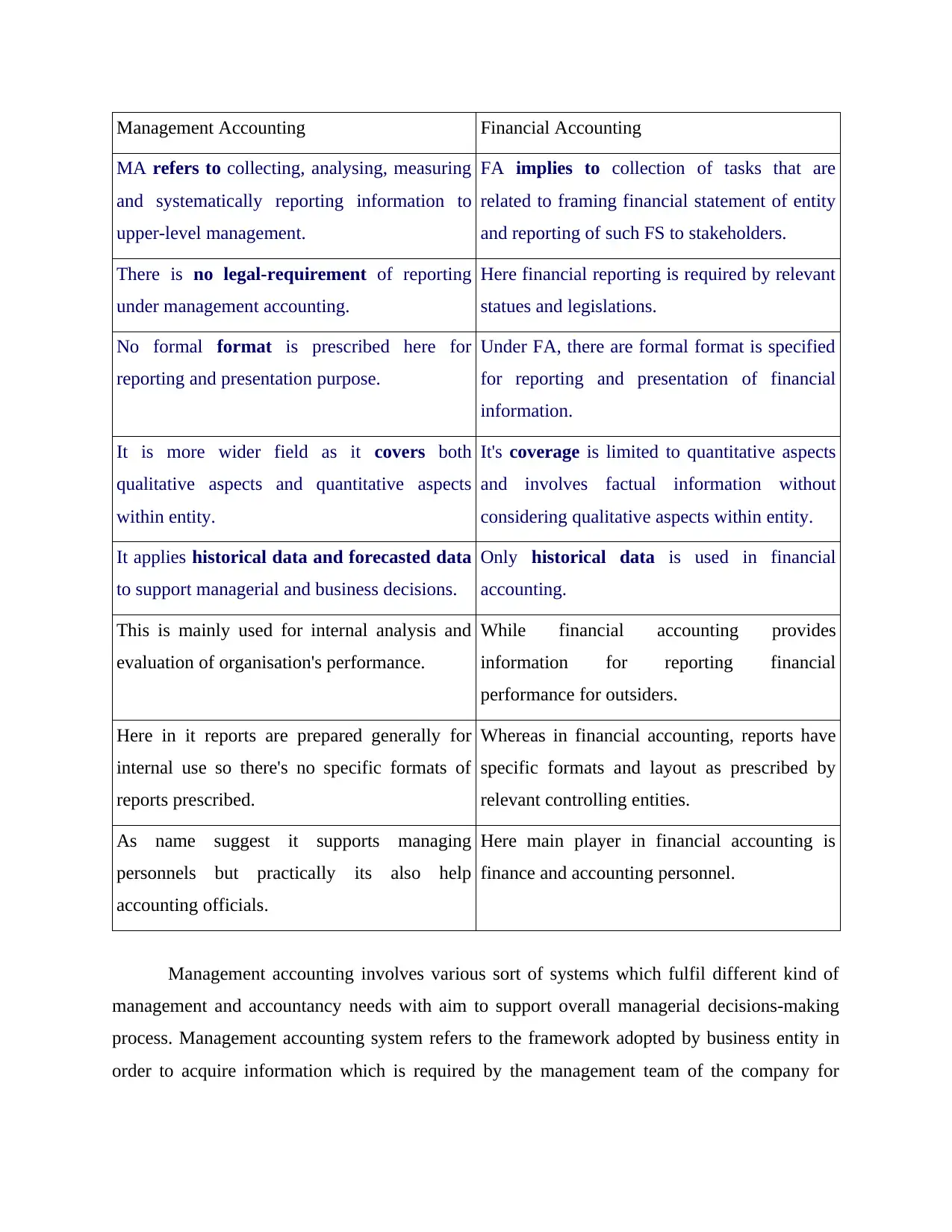

Management Accounting Financial Accounting

MA refers to collecting, analysing, measuring

and systematically reporting information to

upper-level management.

FA implies to collection of tasks that are

related to framing financial statement of entity

and reporting of such FS to stakeholders.

There is no legal-requirement of reporting

under management accounting.

Here financial reporting is required by relevant

statues and legislations.

No formal format is prescribed here for

reporting and presentation purpose.

Under FA, there are formal format is specified

for reporting and presentation of financial

information.

It is more wider field as it covers both

qualitative aspects and quantitative aspects

within entity.

It's coverage is limited to quantitative aspects

and involves factual information without

considering qualitative aspects within entity.

It applies historical data and forecasted data

to support managerial and business decisions.

Only historical data is used in financial

accounting.

This is mainly used for internal analysis and

evaluation of organisation's performance.

While financial accounting provides

information for reporting financial

performance for outsiders.

Here in it reports are prepared generally for

internal use so there's no specific formats of

reports prescribed.

Whereas in financial accounting, reports have

specific formats and layout as prescribed by

relevant controlling entities.

As name suggest it supports managing

personnels but practically its also help

accounting officials.

Here main player in financial accounting is

finance and accounting personnel.

Management accounting involves various sort of systems which fulfil different kind of

management and accountancy needs with aim to support overall managerial decisions-making

process. Management accounting system refers to the framework adopted by business entity in

order to acquire information which is required by the management team of the company for

MA refers to collecting, analysing, measuring

and systematically reporting information to

upper-level management.

FA implies to collection of tasks that are

related to framing financial statement of entity

and reporting of such FS to stakeholders.

There is no legal-requirement of reporting

under management accounting.

Here financial reporting is required by relevant

statues and legislations.

No formal format is prescribed here for

reporting and presentation purpose.

Under FA, there are formal format is specified

for reporting and presentation of financial

information.

It is more wider field as it covers both

qualitative aspects and quantitative aspects

within entity.

It's coverage is limited to quantitative aspects

and involves factual information without

considering qualitative aspects within entity.

It applies historical data and forecasted data

to support managerial and business decisions.

Only historical data is used in financial

accounting.

This is mainly used for internal analysis and

evaluation of organisation's performance.

While financial accounting provides

information for reporting financial

performance for outsiders.

Here in it reports are prepared generally for

internal use so there's no specific formats of

reports prescribed.

Whereas in financial accounting, reports have

specific formats and layout as prescribed by

relevant controlling entities.

As name suggest it supports managing

personnels but practically its also help

accounting officials.

Here main player in financial accounting is

finance and accounting personnel.

Management accounting involves various sort of systems which fulfil different kind of

management and accountancy needs with aim to support overall managerial decisions-making

process. Management accounting system refers to the framework adopted by business entity in

order to acquire information which is required by the management team of the company for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

developing effective decisions. In this context, Excite Entertainment Ltd is using several key

managerial accounting systems, as discussed below:

(b) Cost accounting system:

It is one of the most essential system which is applied for identifying the costs for

organisational goods and services which help in examining profitability, estimating inventory as

well as controlling the costs. It will aims in order to capture the whole cost of production with

the help of estimating overall input costs in addition to the fixed costs which is included in the

stages of production. For controlling costs incurred in promoting concerts and festivals,

managers in Excite Entertainment Ltd apply this systems by classifying all the costs as direct and

indirect, and applying standard costing. Under standard costing managers set expected costs

against actual costs and any variance is analysed to find out any issue causing excessive costs

(Chiapello, 2017) . Here is explanation of different terms related to this system, as follows:

Direct Costs: There are costs which are directly contributes in corporation's particular

function, project, project and any other cost-object.

Standard Costs: These are costs which are normally linked with corporation's

manufacturing/production costs of direct labour & materials and other manufacturing

expenses. These costs are set as benchmark and compared with actual costs to assess over

and under absorption.

Direct costing: Under this technique direct costs are measured related to any particular

process, function and product. In this method costs are assigned to such cost objects to

evaluate actul cost incurred to each such cost-object.

Standard Costing: In this technique, standard costs are applied to assess the actual

performance level of entity. Variances among standard and actual costs are assessed and

evaluated in this technique.

(c) Inventory management systems:

Here key focus of this systems is on Inventories which denotes goods that are

addressable for sale as well as raw materials are utilised for production of services which are

available to carry out sales. This is main system which deals with managing and handling of all

inventories items. Along with this, it system also prevent firms idling of complete factory in case

if any one of the service or products furnished breaks down and for having a steady stream for

maintaining flow of materials to retailers irrespective of making a identical shipments of services

managerial accounting systems, as discussed below:

(b) Cost accounting system:

It is one of the most essential system which is applied for identifying the costs for

organisational goods and services which help in examining profitability, estimating inventory as

well as controlling the costs. It will aims in order to capture the whole cost of production with

the help of estimating overall input costs in addition to the fixed costs which is included in the

stages of production. For controlling costs incurred in promoting concerts and festivals,

managers in Excite Entertainment Ltd apply this systems by classifying all the costs as direct and

indirect, and applying standard costing. Under standard costing managers set expected costs

against actual costs and any variance is analysed to find out any issue causing excessive costs

(Chiapello, 2017) . Here is explanation of different terms related to this system, as follows:

Direct Costs: There are costs which are directly contributes in corporation's particular

function, project, project and any other cost-object.

Standard Costs: These are costs which are normally linked with corporation's

manufacturing/production costs of direct labour & materials and other manufacturing

expenses. These costs are set as benchmark and compared with actual costs to assess over

and under absorption.

Direct costing: Under this technique direct costs are measured related to any particular

process, function and product. In this method costs are assigned to such cost objects to

evaluate actul cost incurred to each such cost-object.

Standard Costing: In this technique, standard costs are applied to assess the actual

performance level of entity. Variances among standard and actual costs are assessed and

evaluated in this technique.

(c) Inventory management systems:

Here key focus of this systems is on Inventories which denotes goods that are

addressable for sale as well as raw materials are utilised for production of services which are

available to carry out sales. This is main system which deals with managing and handling of all

inventories items. Along with this, it system also prevent firms idling of complete factory in case

if any one of the service or products furnished breaks down and for having a steady stream for

maintaining flow of materials to retailers irrespective of making a identical shipments of services

which are provided by retailers. In this context, Excite Entertainment Ltd is also applying this

system to manage its inventories or items used in promoting concerts.

FIFO: Here assumption that inventories bought first in specific sequence are considered

to sold first, is used to value inventories.

LIFO: Just opposite to FIFO, inventories are valued on assumption that recent/latest

bought inventories are sold first in particular sequence.

Weighted-average cost method: Herein this method, average cost is assessed by assigning

weighted to value inventories.

(d) Job Costing Systems:

This system defined as collection of activities which are related to gathering information

of costs/expenses linked to particular production job. This system concerned with process/tasks

of aggregating data and facts about different costs/expenditures connected to specific job. Then

assign all the costs to each specific job or task. This is crucial systems which contributes in

maintaining accountability in different job within enterprise. As in case of Excite Entertainment

Ltd, managing personnels collects costs details of each job related to promotion of any concert,

event and festival. After recognizing and classification of jobs and relevant costs they allocate all

the costs to each particular job that ultimately assist them to optimise overall promotional costs

((Crutzen Zvezdov and Schaltegger, 2017).

(e) Benefits of above mentioned accounting systems:

Cost accounting system: This system is beneficial because it reveal of all profitable and

unprofitable activities by calculation of cost, selling price and profitability of product.

Such as Excite entertainment Ltd apply this system to collect proper guidance about

future production policies and control unnecessary expenses.

Inventory management system: This system is mainly depended on the utilization of

different stock measurement method in respect to know usage and availability of

resources. In the context of Excite Entertainment use this system to collect detail

information about inventories and store material in warehouse.

Job costing System: It allows a manager to compute the profitability that earned by

individual. It is beneficial system which is supporting them to better determine whether

particular jobs are enviable to pursue in the future. Such as Excite entertainment Ltd

company utilise this system to arrange cost of job effectively.

system to manage its inventories or items used in promoting concerts.

FIFO: Here assumption that inventories bought first in specific sequence are considered

to sold first, is used to value inventories.

LIFO: Just opposite to FIFO, inventories are valued on assumption that recent/latest

bought inventories are sold first in particular sequence.

Weighted-average cost method: Herein this method, average cost is assessed by assigning

weighted to value inventories.

(d) Job Costing Systems:

This system defined as collection of activities which are related to gathering information

of costs/expenses linked to particular production job. This system concerned with process/tasks

of aggregating data and facts about different costs/expenditures connected to specific job. Then

assign all the costs to each specific job or task. This is crucial systems which contributes in

maintaining accountability in different job within enterprise. As in case of Excite Entertainment

Ltd, managing personnels collects costs details of each job related to promotion of any concert,

event and festival. After recognizing and classification of jobs and relevant costs they allocate all

the costs to each particular job that ultimately assist them to optimise overall promotional costs

((Crutzen Zvezdov and Schaltegger, 2017).

(e) Benefits of above mentioned accounting systems:

Cost accounting system: This system is beneficial because it reveal of all profitable and

unprofitable activities by calculation of cost, selling price and profitability of product.

Such as Excite entertainment Ltd apply this system to collect proper guidance about

future production policies and control unnecessary expenses.

Inventory management system: This system is mainly depended on the utilization of

different stock measurement method in respect to know usage and availability of

resources. In the context of Excite Entertainment use this system to collect detail

information about inventories and store material in warehouse.

Job costing System: It allows a manager to compute the profitability that earned by

individual. It is beneficial system which is supporting them to better determine whether

particular jobs are enviable to pursue in the future. Such as Excite entertainment Ltd

company utilise this system to arrange cost of job effectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section B

(a) Various kinds of managerial accounting report

Management accounting reports are preparing by managers to collect all internal

information and present various aspects of an organisation. These reports are helping to take

better decision and collect data from different section of business (Diouf and Boiral, 2017).

Such as, Excite entertainment Ltd prepare these reports such as:

Performance report: This report is produced by an organisation to analysis the

performance of business and staff members at the end of financial year. For this collect

information from various division to prepare report. It is using by management to take

effective decisions for potential tasks that will conduct in future. Such as excite

entertainment Ltd create this report to present capacity of business and individuals and

according to that offer reward for motivation.

Accounts Receivable Report: This report is prepared by the business to record

information about debtors who take goods on credit and pay in certain period of time.

Accounts receivable report prepare by manager to identify defaulters and complete

modification to tighten credit policies to control cash flow in Excite entertain Limited.

Budget Report: A budget report prepare by company to predict future expenditure and

incomes for particular financial year. The estimation based on the previous activities and

add other expenses that add in next year. It is internal part of any organisation that

produce by every type of business to take right decision and prepare strategies. Such as,

excite entertainment use this report to compare actual and budgeted project.

(b) Why should information should be accurate, relevant and up to date

It is required to present financial information in accurate manner that helps to understand

actual situation of business. These information must be related and up to date that supports to

take right decision on time. If information will accurate so an accountant easily produce all

financial statements. Along with, it should be related with all transactions of financial data so

that internal decisions take by the managers. Such as, it is necessary to present financial

information on right time to stakeholders that helps them to analysis position of enterprise.

(a) Various kinds of managerial accounting report

Management accounting reports are preparing by managers to collect all internal

information and present various aspects of an organisation. These reports are helping to take

better decision and collect data from different section of business (Diouf and Boiral, 2017).

Such as, Excite entertainment Ltd prepare these reports such as:

Performance report: This report is produced by an organisation to analysis the

performance of business and staff members at the end of financial year. For this collect

information from various division to prepare report. It is using by management to take

effective decisions for potential tasks that will conduct in future. Such as excite

entertainment Ltd create this report to present capacity of business and individuals and

according to that offer reward for motivation.

Accounts Receivable Report: This report is prepared by the business to record

information about debtors who take goods on credit and pay in certain period of time.

Accounts receivable report prepare by manager to identify defaulters and complete

modification to tighten credit policies to control cash flow in Excite entertain Limited.

Budget Report: A budget report prepare by company to predict future expenditure and

incomes for particular financial year. The estimation based on the previous activities and

add other expenses that add in next year. It is internal part of any organisation that

produce by every type of business to take right decision and prepare strategies. Such as,

excite entertainment use this report to compare actual and budgeted project.

(b) Why should information should be accurate, relevant and up to date

It is required to present financial information in accurate manner that helps to understand

actual situation of business. These information must be related and up to date that supports to

take right decision on time. If information will accurate so an accountant easily produce all

financial statements. Along with, it should be related with all transactions of financial data so

that internal decisions take by the managers. Such as, it is necessary to present financial

information on right time to stakeholders that helps them to analysis position of enterprise.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

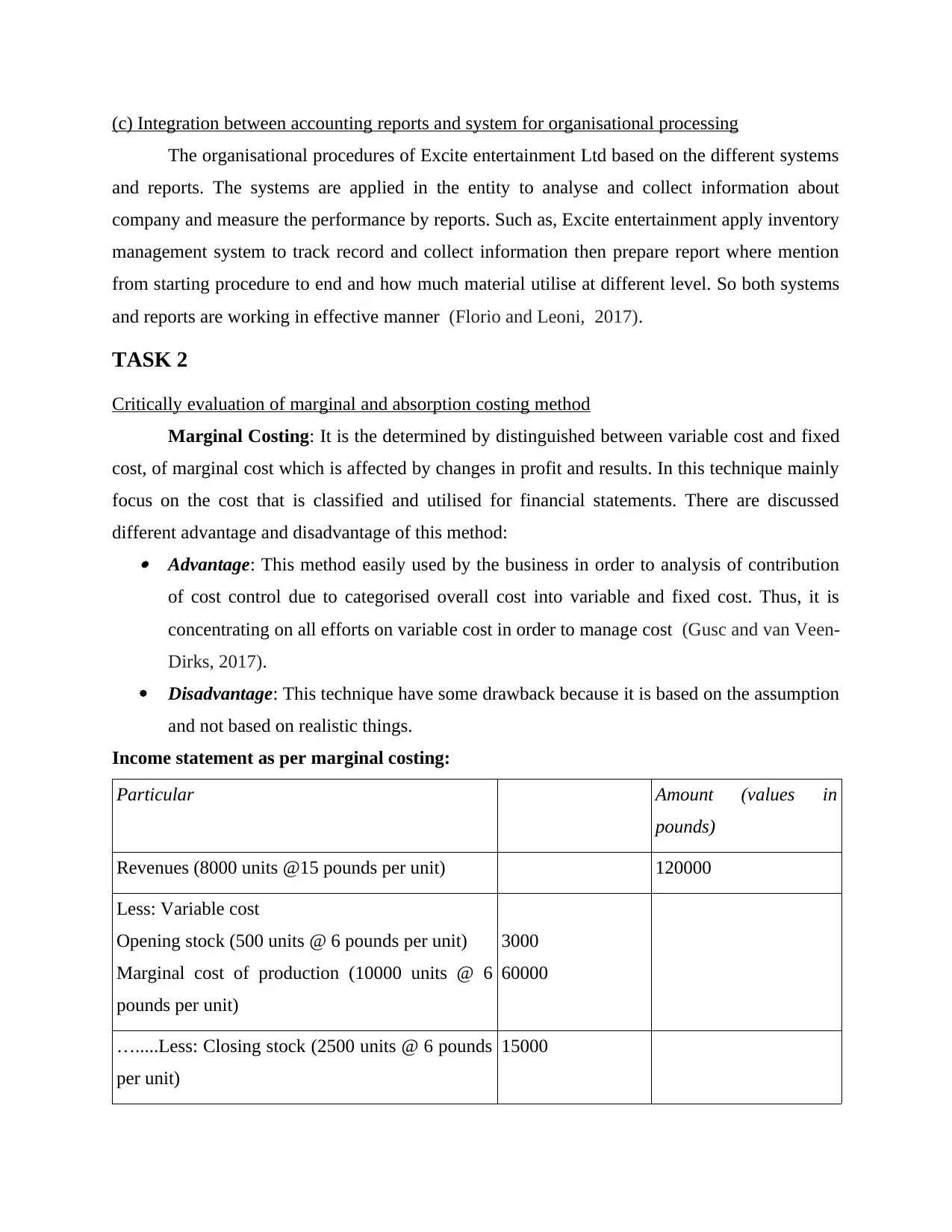

(c) Integration between accounting reports and system for organisational processing

The organisational procedures of Excite entertainment Ltd based on the different systems

and reports. The systems are applied in the entity to analyse and collect information about

company and measure the performance by reports. Such as, Excite entertainment apply inventory

management system to track record and collect information then prepare report where mention

from starting procedure to end and how much material utilise at different level. So both systems

and reports are working in effective manner (Florio and Leoni, 2017).

TASK 2

Critically evaluation of marginal and absorption costing method

Marginal Costing: It is the determined by distinguished between variable cost and fixed

cost, of marginal cost which is affected by changes in profit and results. In this technique mainly

focus on the cost that is classified and utilised for financial statements. There are discussed

different advantage and disadvantage of this method: Advantage: This method easily used by the business in order to analysis of contribution

of cost control due to categorised overall cost into variable and fixed cost. Thus, it is

concentrating on all efforts on variable cost in order to manage cost (Gusc and van Veen-

Dirks, 2017).

Disadvantage: This technique have some drawback because it is based on the assumption

and not based on realistic things.

Income statement as per marginal costing:

Particular Amount (values in

pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less: Variable cost

Opening stock (500 units @ 6 pounds per unit)

Marginal cost of production (10000 units @ 6

pounds per unit)

3000

60000

….....Less: Closing stock (2500 units @ 6 pounds

per unit)

15000

The organisational procedures of Excite entertainment Ltd based on the different systems

and reports. The systems are applied in the entity to analyse and collect information about

company and measure the performance by reports. Such as, Excite entertainment apply inventory

management system to track record and collect information then prepare report where mention

from starting procedure to end and how much material utilise at different level. So both systems

and reports are working in effective manner (Florio and Leoni, 2017).

TASK 2

Critically evaluation of marginal and absorption costing method

Marginal Costing: It is the determined by distinguished between variable cost and fixed

cost, of marginal cost which is affected by changes in profit and results. In this technique mainly

focus on the cost that is classified and utilised for financial statements. There are discussed

different advantage and disadvantage of this method: Advantage: This method easily used by the business in order to analysis of contribution

of cost control due to categorised overall cost into variable and fixed cost. Thus, it is

concentrating on all efforts on variable cost in order to manage cost (Gusc and van Veen-

Dirks, 2017).

Disadvantage: This technique have some drawback because it is based on the assumption

and not based on realistic things.

Income statement as per marginal costing:

Particular Amount (values in

pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less: Variable cost

Opening stock (500 units @ 6 pounds per unit)

Marginal cost of production (10000 units @ 6

pounds per unit)

3000

60000

….....Less: Closing stock (2500 units @ 6 pounds

per unit)

15000

Marginal cost of sale 48000

Contribution (15-6)= 9 x 8000 72000

Fixed cost 40000

Net Profit 32000

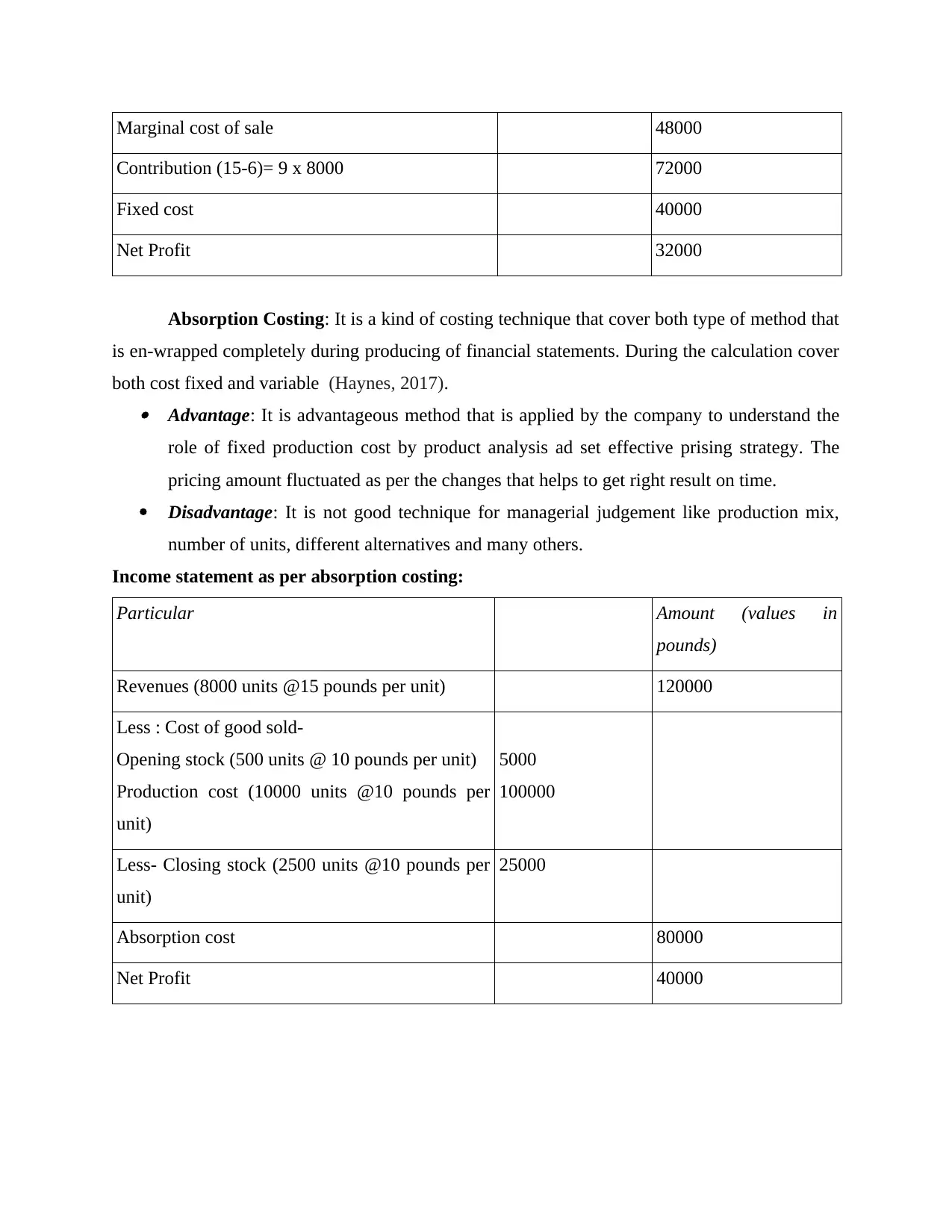

Absorption Costing: It is a kind of costing technique that cover both type of method that

is en-wrapped completely during producing of financial statements. During the calculation cover

both cost fixed and variable (Haynes, 2017). Advantage: It is advantageous method that is applied by the company to understand the

role of fixed production cost by product analysis ad set effective prising strategy. The

pricing amount fluctuated as per the changes that helps to get right result on time.

Disadvantage: It is not good technique for managerial judgement like production mix,

number of units, different alternatives and many others.

Income statement as per absorption costing:

Particular Amount (values in

pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less : Cost of good sold-

Opening stock (500 units @ 10 pounds per unit)

Production cost (10000 units @10 pounds per

unit)

5000

100000

Less- Closing stock (2500 units @10 pounds per

unit)

25000

Absorption cost 80000

Net Profit 40000

Contribution (15-6)= 9 x 8000 72000

Fixed cost 40000

Net Profit 32000

Absorption Costing: It is a kind of costing technique that cover both type of method that

is en-wrapped completely during producing of financial statements. During the calculation cover

both cost fixed and variable (Haynes, 2017). Advantage: It is advantageous method that is applied by the company to understand the

role of fixed production cost by product analysis ad set effective prising strategy. The

pricing amount fluctuated as per the changes that helps to get right result on time.

Disadvantage: It is not good technique for managerial judgement like production mix,

number of units, different alternatives and many others.

Income statement as per absorption costing:

Particular Amount (values in

pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less : Cost of good sold-

Opening stock (500 units @ 10 pounds per unit)

Production cost (10000 units @10 pounds per

unit)

5000

100000

Less- Closing stock (2500 units @10 pounds per

unit)

25000

Absorption cost 80000

Net Profit 40000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0

5000

10000

15000

20000

25000

30000

35000

40000

45000 40000

32000

Net profit (Absorption costing)

Net profit (Marginal costing)

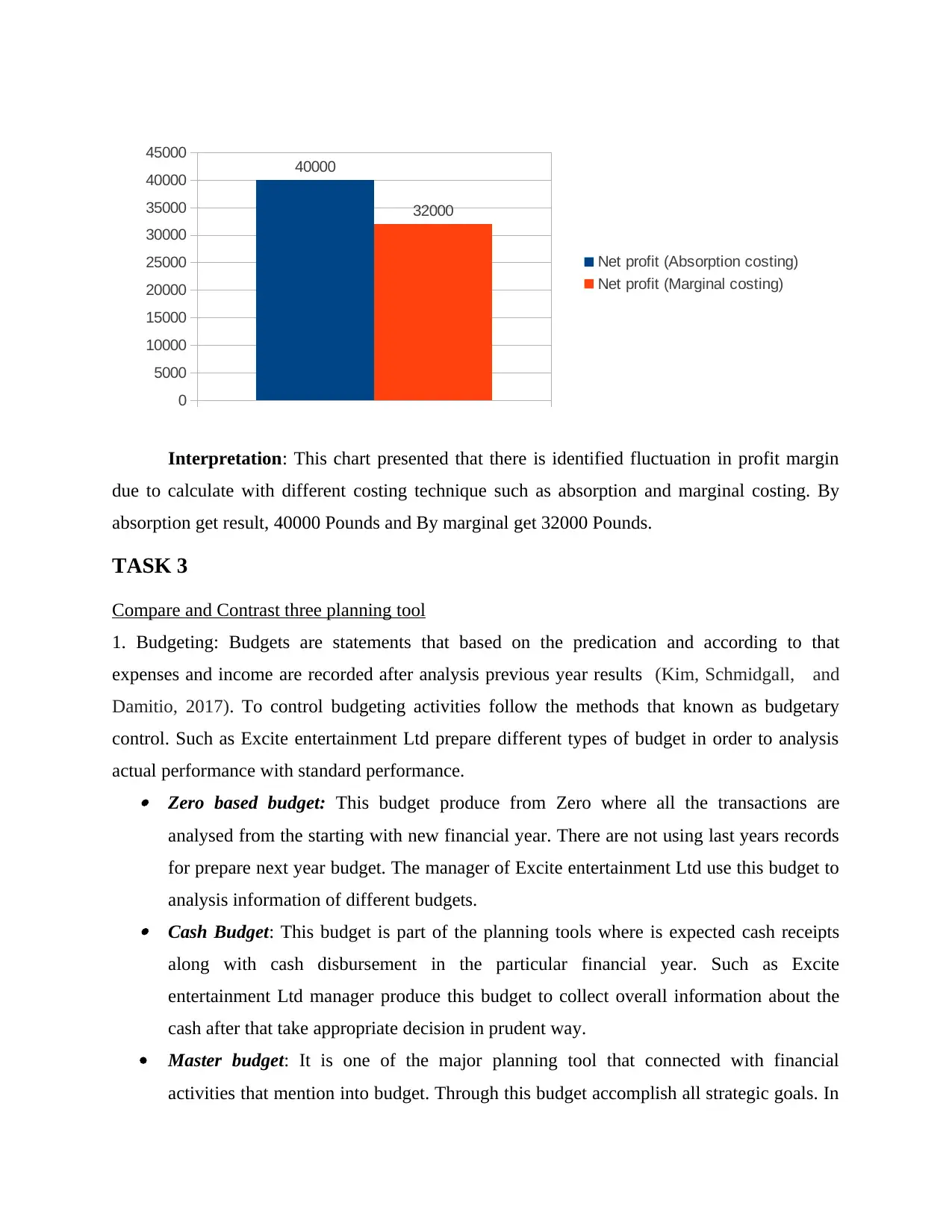

Interpretation: This chart presented that there is identified fluctuation in profit margin

due to calculate with different costing technique such as absorption and marginal costing. By

absorption get result, 40000 Pounds and By marginal get 32000 Pounds.

TASK 3

Compare and Contrast three planning tool

1. Budgeting: Budgets are statements that based on the predication and according to that

expenses and income are recorded after analysis previous year results (Kim, Schmidgall, and

Damitio, 2017). To control budgeting activities follow the methods that known as budgetary

control. Such as Excite entertainment Ltd prepare different types of budget in order to analysis

actual performance with standard performance. Zero based budget: This budget produce from Zero where all the transactions are

analysed from the starting with new financial year. There are not using last years records

for prepare next year budget. The manager of Excite entertainment Ltd use this budget to

analysis information of different budgets. Cash Budget: This budget is part of the planning tools where is expected cash receipts

along with cash disbursement in the particular financial year. Such as Excite

entertainment Ltd manager produce this budget to collect overall information about the

cash after that take appropriate decision in prudent way.

Master budget: It is one of the major planning tool that connected with financial

activities that mention into budget. Through this budget accomplish all strategic goals. In

5000

10000

15000

20000

25000

30000

35000

40000

45000 40000

32000

Net profit (Absorption costing)

Net profit (Marginal costing)

Interpretation: This chart presented that there is identified fluctuation in profit margin

due to calculate with different costing technique such as absorption and marginal costing. By

absorption get result, 40000 Pounds and By marginal get 32000 Pounds.

TASK 3

Compare and Contrast three planning tool

1. Budgeting: Budgets are statements that based on the predication and according to that

expenses and income are recorded after analysis previous year results (Kim, Schmidgall, and

Damitio, 2017). To control budgeting activities follow the methods that known as budgetary

control. Such as Excite entertainment Ltd prepare different types of budget in order to analysis

actual performance with standard performance. Zero based budget: This budget produce from Zero where all the transactions are

analysed from the starting with new financial year. There are not using last years records

for prepare next year budget. The manager of Excite entertainment Ltd use this budget to

analysis information of different budgets. Cash Budget: This budget is part of the planning tools where is expected cash receipts

along with cash disbursement in the particular financial year. Such as Excite

entertainment Ltd manager produce this budget to collect overall information about the

cash after that take appropriate decision in prudent way.

Master budget: It is one of the major planning tool that connected with financial

activities that mention into budget. Through this budget accomplish all strategic goals. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this budget consist of summary of all department budget to analysis actual position of the

company. Such as Excite entertainment use this budget to easily collect information

about all departments after that take effective decision (Kind, Wouter Botzen and Aerts,

2017).

Comparison between master, zero and cash budget

Basis of comparison Cash budget Zero budget Master budget

Meaning This budget is

explained that analysis

the transactions of

cash in the context of

receipts as well as

expenditure.

To produce this budget

require to make a plan

and from beginning

collect all the

information that are

recorded in the budget

as zero base.

Master budget is

mainly based on the

term plan where

involves every division

budget within

company.

Main objective The main reason to

prepare this budget

that Excite

entertainment get

proper information

about the cash

position and in which

items spend money to

control as per the

structure.

It is mainly produced by

the company to collect

information from

starting and deduct

unwanted cost.

The main objective to

prepare of this budget

that set rough

instructions to fulfil

the requirement and set

the objectives for

certain period of time.

TASK 4

Preventing from financial problem

1. Contribution Margin: It is a product's price less all related variables cost resulting in the

increasing profit generated through each unit sold. In general manner, from sales less variable

cost get amount of contribution (Napitupulu, 2018). As per the given data calculate contribution

margin such as:

company. Such as Excite entertainment use this budget to easily collect information

about all departments after that take effective decision (Kind, Wouter Botzen and Aerts,

2017).

Comparison between master, zero and cash budget

Basis of comparison Cash budget Zero budget Master budget

Meaning This budget is

explained that analysis

the transactions of

cash in the context of

receipts as well as

expenditure.

To produce this budget

require to make a plan

and from beginning

collect all the

information that are

recorded in the budget

as zero base.

Master budget is

mainly based on the

term plan where

involves every division

budget within

company.

Main objective The main reason to

prepare this budget

that Excite

entertainment get

proper information

about the cash

position and in which

items spend money to

control as per the

structure.

It is mainly produced by

the company to collect

information from

starting and deduct

unwanted cost.

The main objective to

prepare of this budget

that set rough

instructions to fulfil

the requirement and set

the objectives for

certain period of time.

TASK 4

Preventing from financial problem

1. Contribution Margin: It is a product's price less all related variables cost resulting in the

increasing profit generated through each unit sold. In general manner, from sales less variable

cost get amount of contribution (Napitupulu, 2018). As per the given data calculate contribution

margin such as:

Particulars Amount (Values in

pounds)

Selling price per unit 40

Less- Variable cost per unit 10

Contribution per unit 30

Break even point: That point where company get no profit and no loss after calculation. There

are calculated it as per the given data such as:

Particulars Amount (Values in

pounds)

Fixed cost (A) 120000

Contribution per unit (B) 30

Break even points (A/B) 4000

3. Units to achieve: There are predicted unit that on which level organisation received desired

profit. To calculate profit apply particular formula such as:

Units to attain desired profit: Fix Cost + Desired profit/ Contribution per unit

Particulars Amount (Values in pounds)

Fixed cost 120000

Desired profit 90000

Contribution per unit 30

Units to attain desired profit 7000 units

Sensitivity Analysis: It is a kind of technique that applied by the business to analysis

uncertainty in result of a mathematical model as well as system. This analysis helps in decision

making procedure, employing different assumption that linked with variable. Such as, an

accountant set expected level of revenues that may be accomplished as a result of an investment

in machine through projected level of demand etc.

pounds)

Selling price per unit 40

Less- Variable cost per unit 10

Contribution per unit 30

Break even point: That point where company get no profit and no loss after calculation. There

are calculated it as per the given data such as:

Particulars Amount (Values in

pounds)

Fixed cost (A) 120000

Contribution per unit (B) 30

Break even points (A/B) 4000

3. Units to achieve: There are predicted unit that on which level organisation received desired

profit. To calculate profit apply particular formula such as:

Units to attain desired profit: Fix Cost + Desired profit/ Contribution per unit

Particulars Amount (Values in pounds)

Fixed cost 120000

Desired profit 90000

Contribution per unit 30

Units to attain desired profit 7000 units

Sensitivity Analysis: It is a kind of technique that applied by the business to analysis

uncertainty in result of a mathematical model as well as system. This analysis helps in decision

making procedure, employing different assumption that linked with variable. Such as, an

accountant set expected level of revenues that may be accomplished as a result of an investment

in machine through projected level of demand etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.