Management Accounting Report: Analyzing Organizational Performance

VerifiedAdded on 2020/10/23

|8

|1585

|214

Report

AI Summary

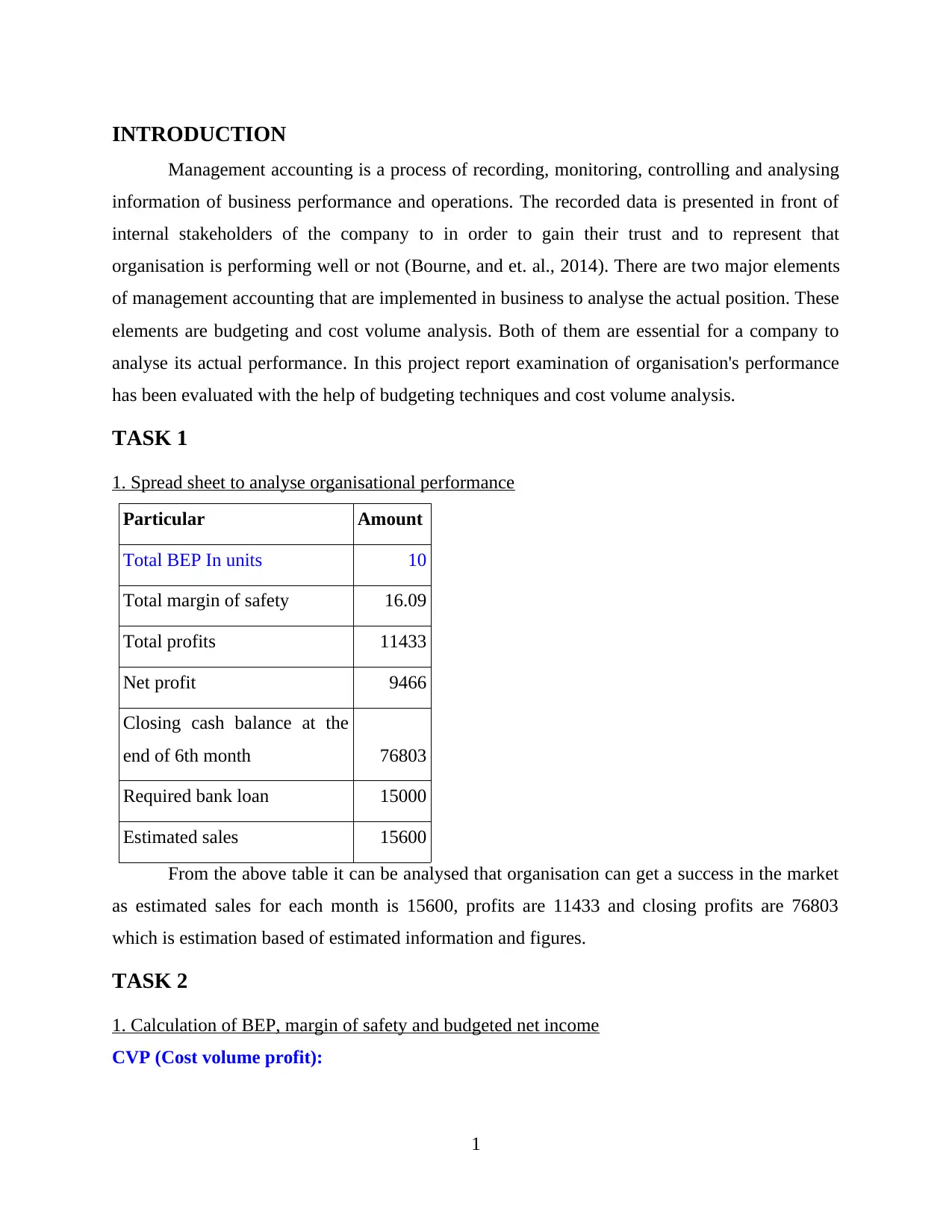

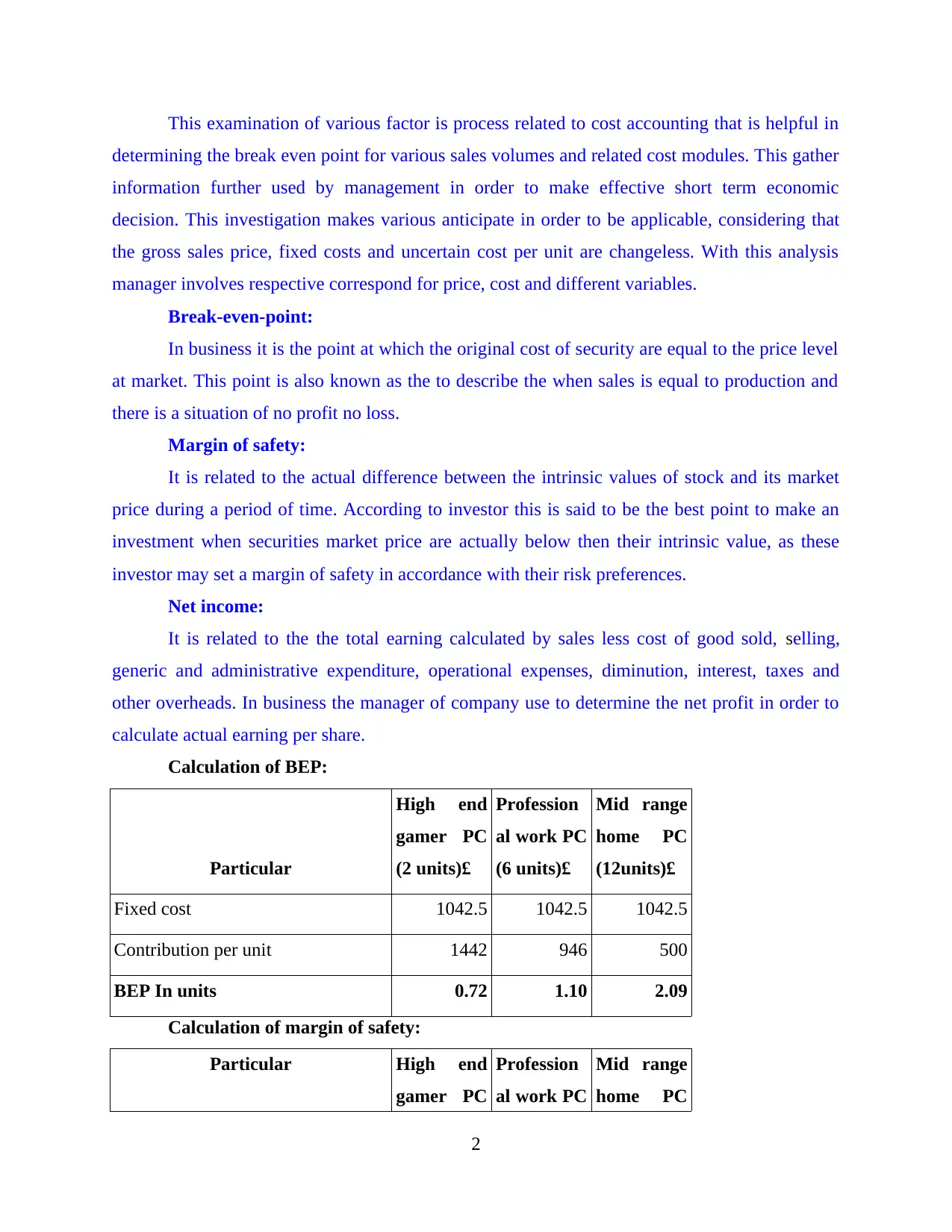

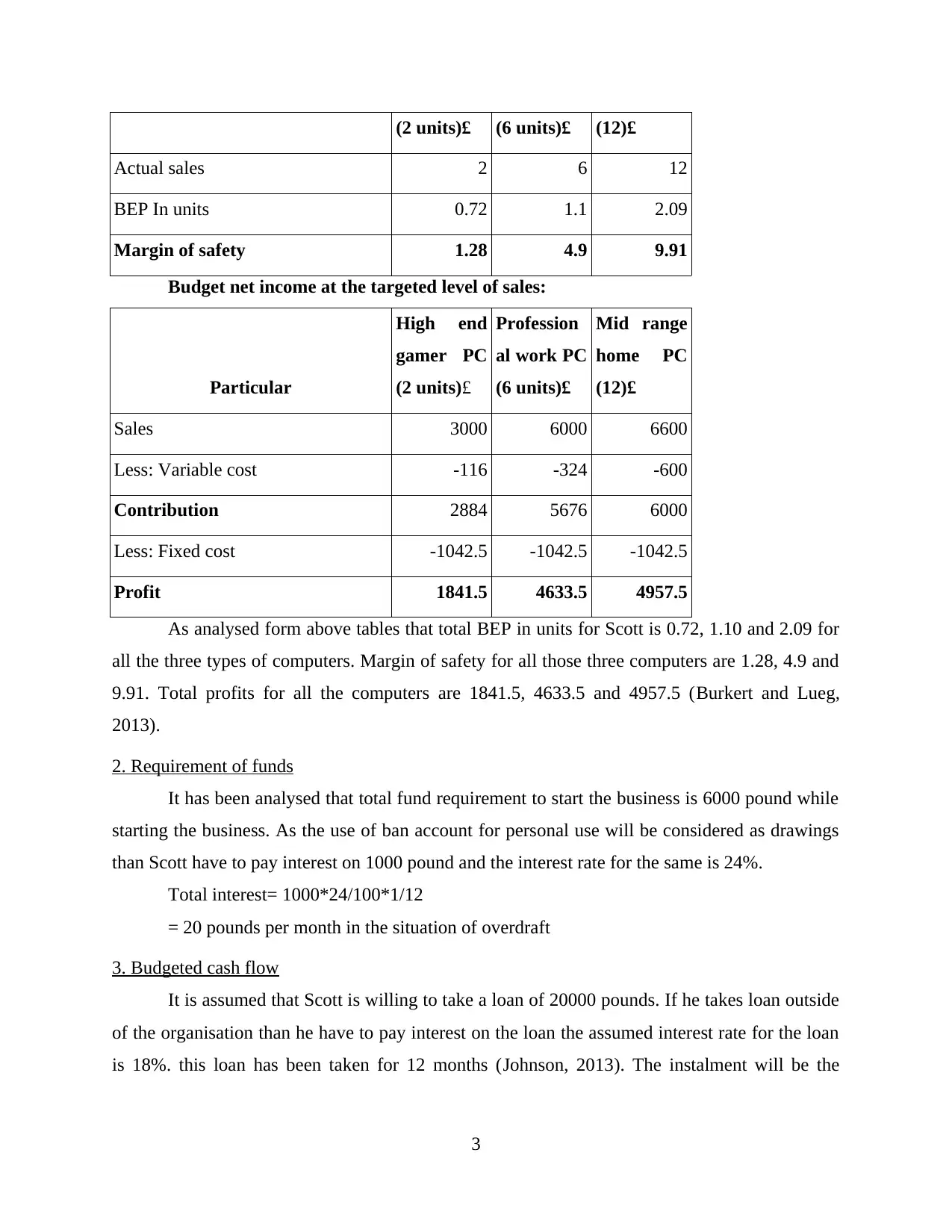

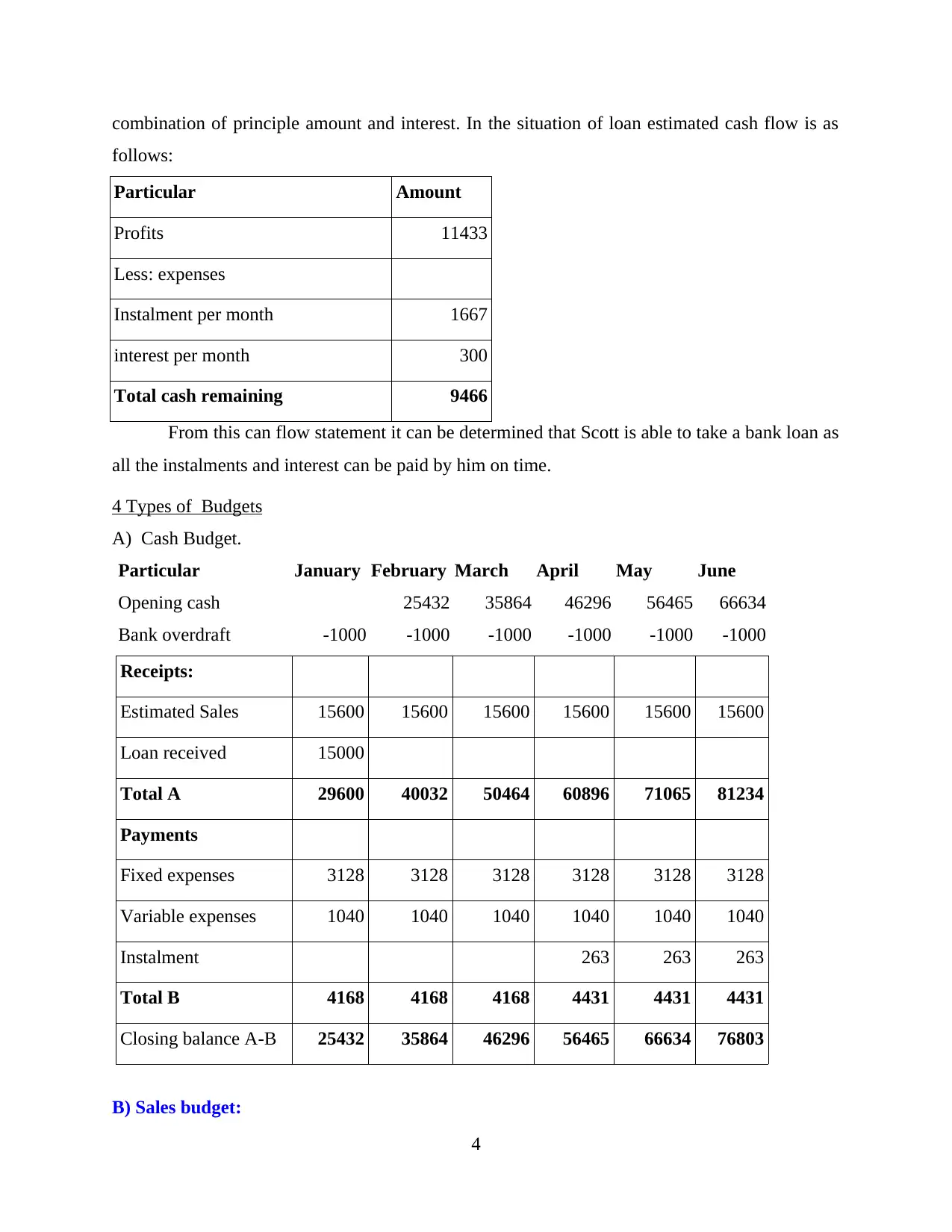

This report delves into management accounting, focusing on analyzing an organization's performance through budgeting and cost-volume-profit (CVP) analysis. The report includes a spreadsheet analysis of key financial metrics such as total break-even point, margin of safety, total profits, and closing cash balance. It further calculates the break-even point, margin of safety, and budgeted net income for different computer types. The report also examines fund requirements, budgeted cash flow, and various types of budgets including cash, sales, inventory, and labor budgets. References to relevant literature are also included, providing a comprehensive overview of management accounting principles and their practical application in business performance evaluation.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.