MAA262 Management Accounting Assignment: Individual Assessment

VerifiedAdded on 2022/10/15

|9

|1397

|26

Homework Assignment

AI Summary

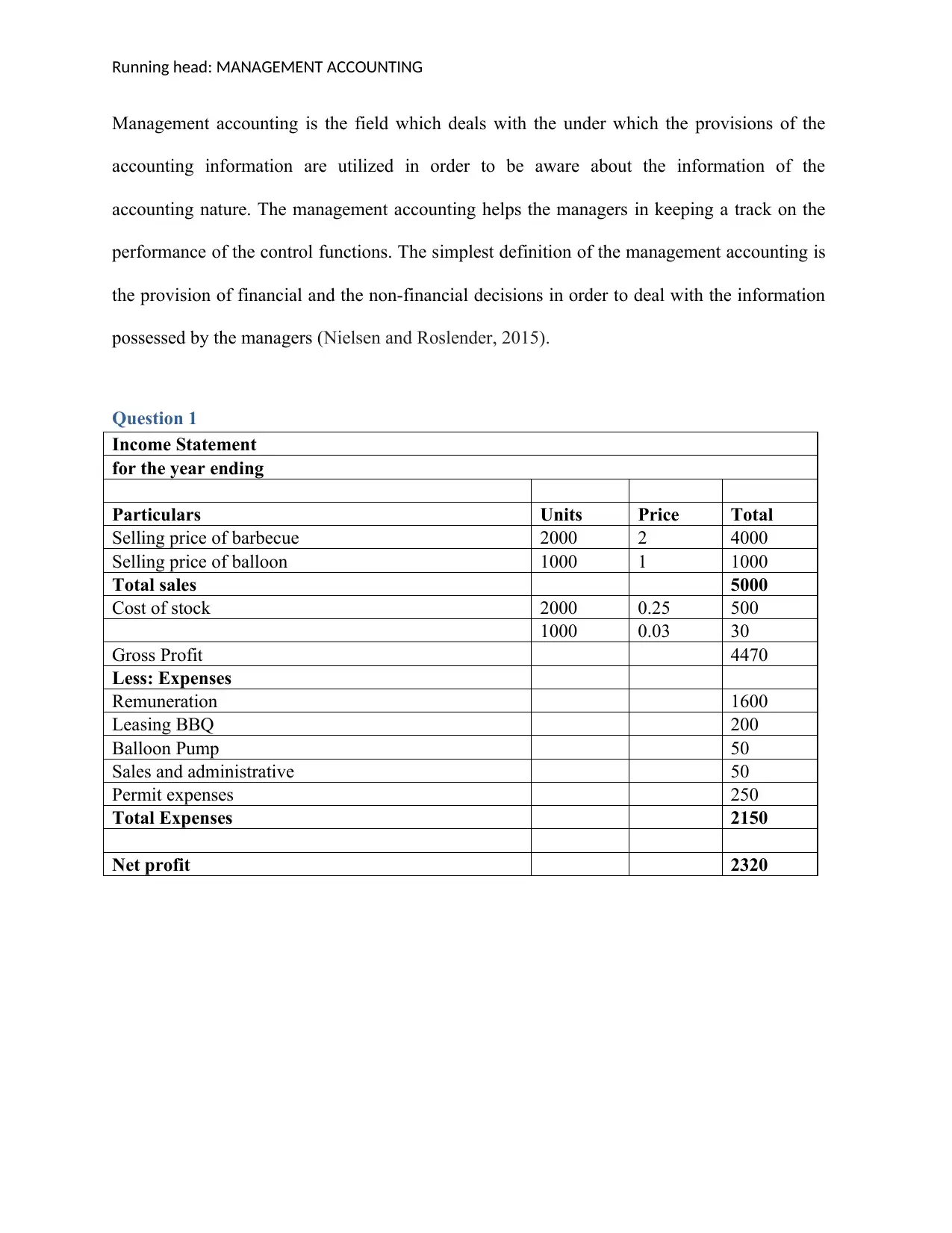

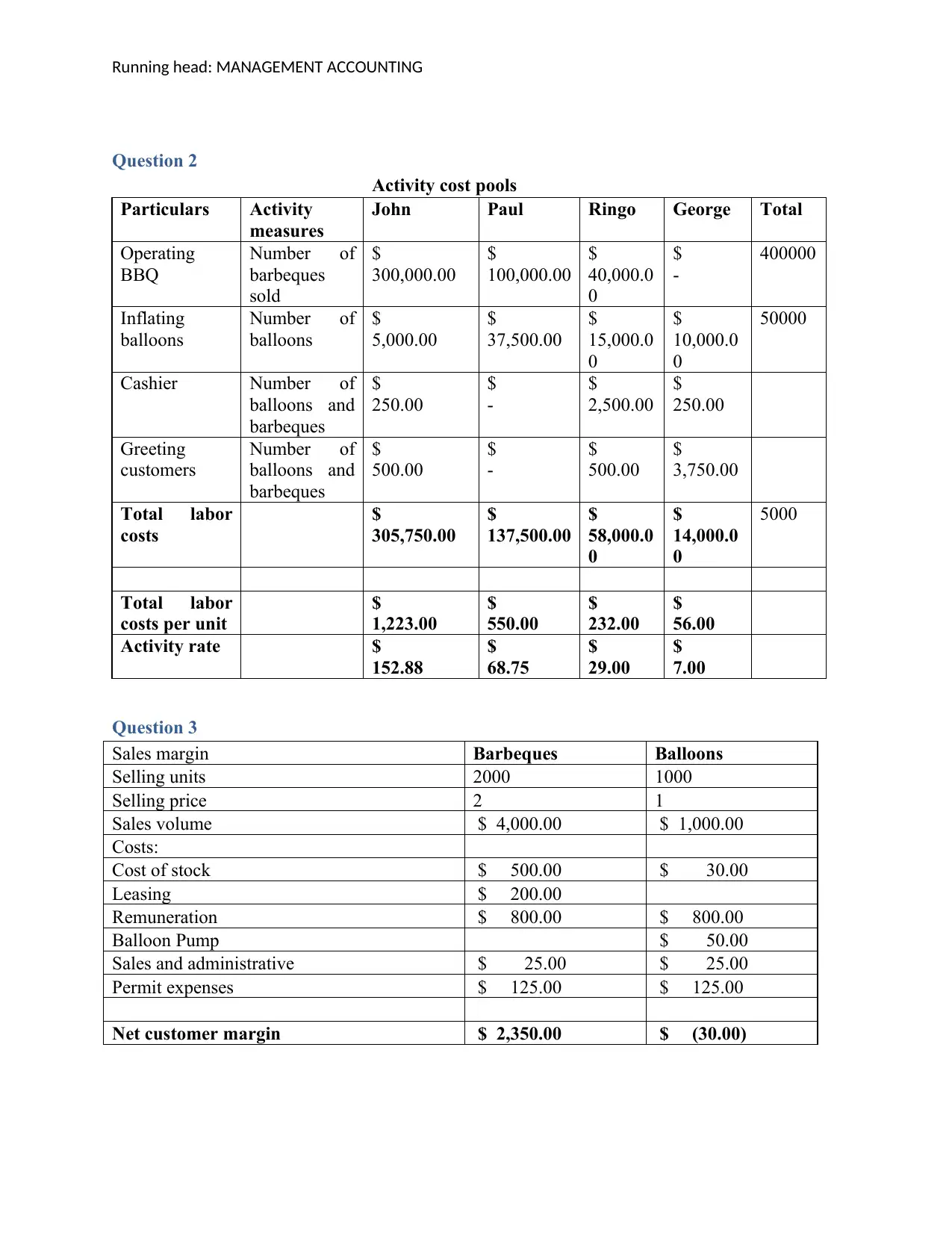

This document presents a comprehensive solution to a management accounting assignment, likely for the MAA262 course at Deakin University. The solution includes an income statement, activity-based costing analysis, and sales margin calculations. It also addresses questions on the justifiability of decisions and performance evaluations, incorporating variance analysis to compare planned and actual budgets. The assignment delves into material and quantity variances for both BBQ and balloon sales, providing a detailed breakdown of cost and revenue calculations. The solution provides a complete analysis of the business's financial performance and offers insights into management decision-making.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.