Case Study: Budgeting Process Improvement at Exhibition Furniture

VerifiedAdded on 2023/06/15

|12

|777

|422

Case Study

AI Summary

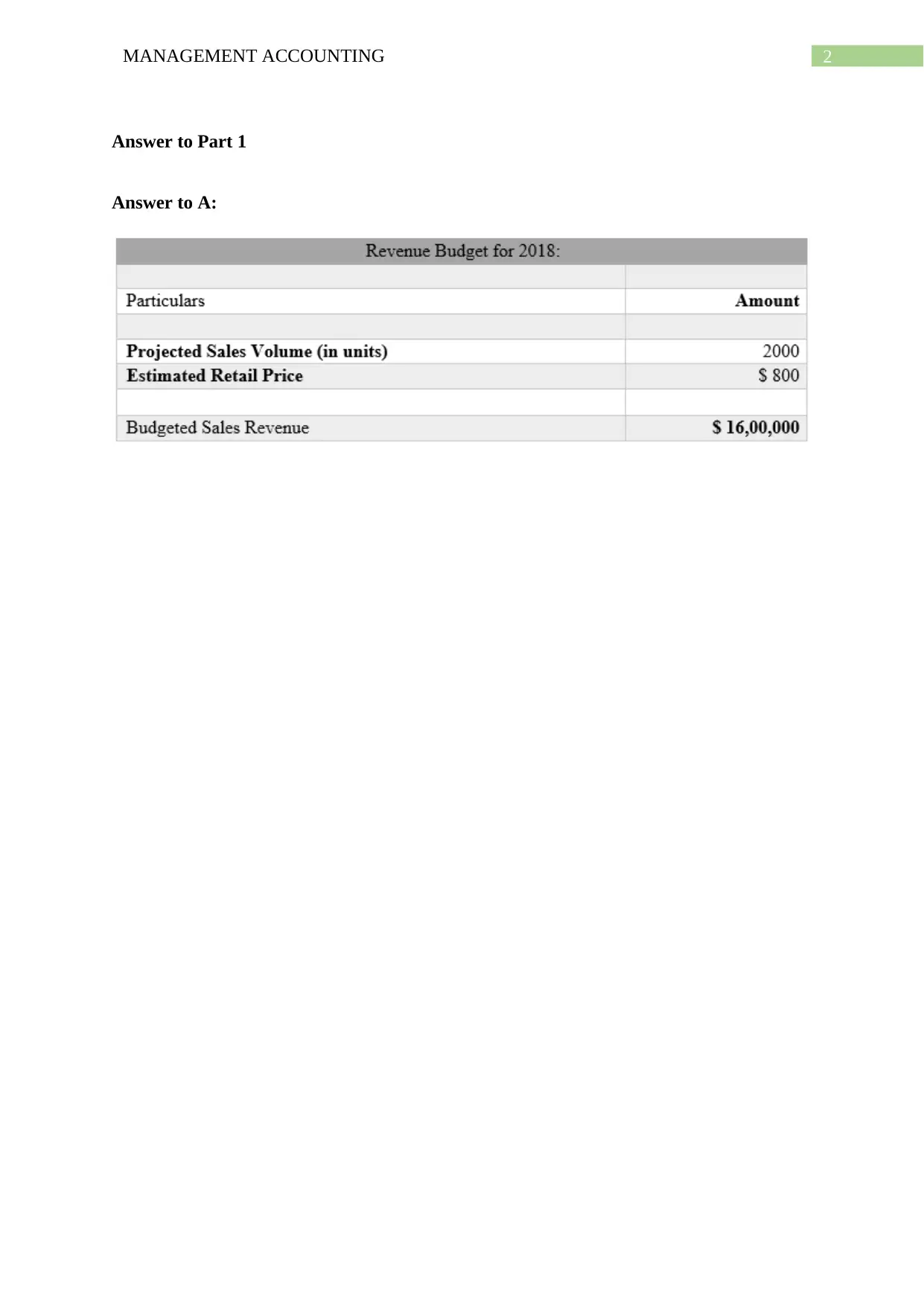

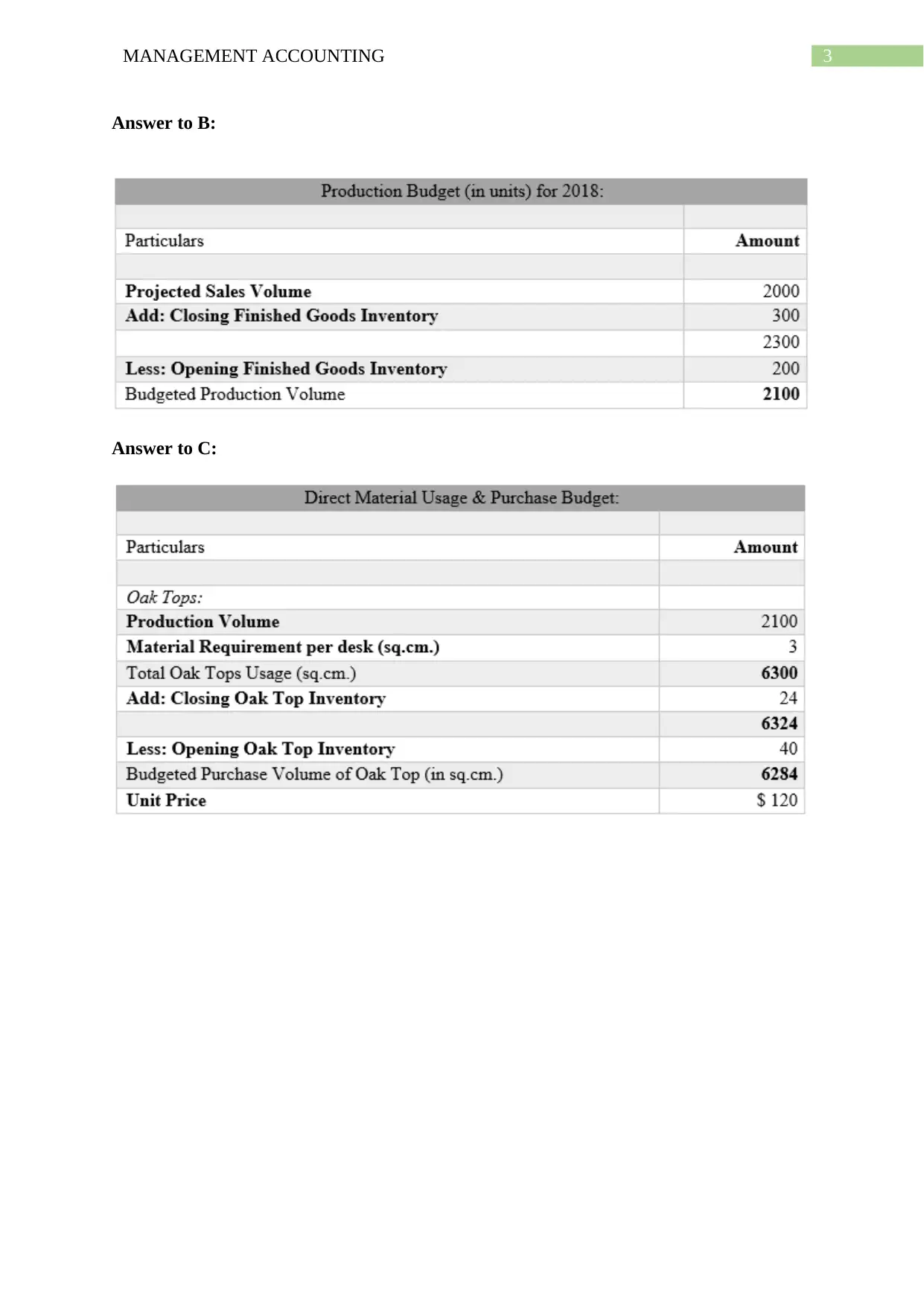

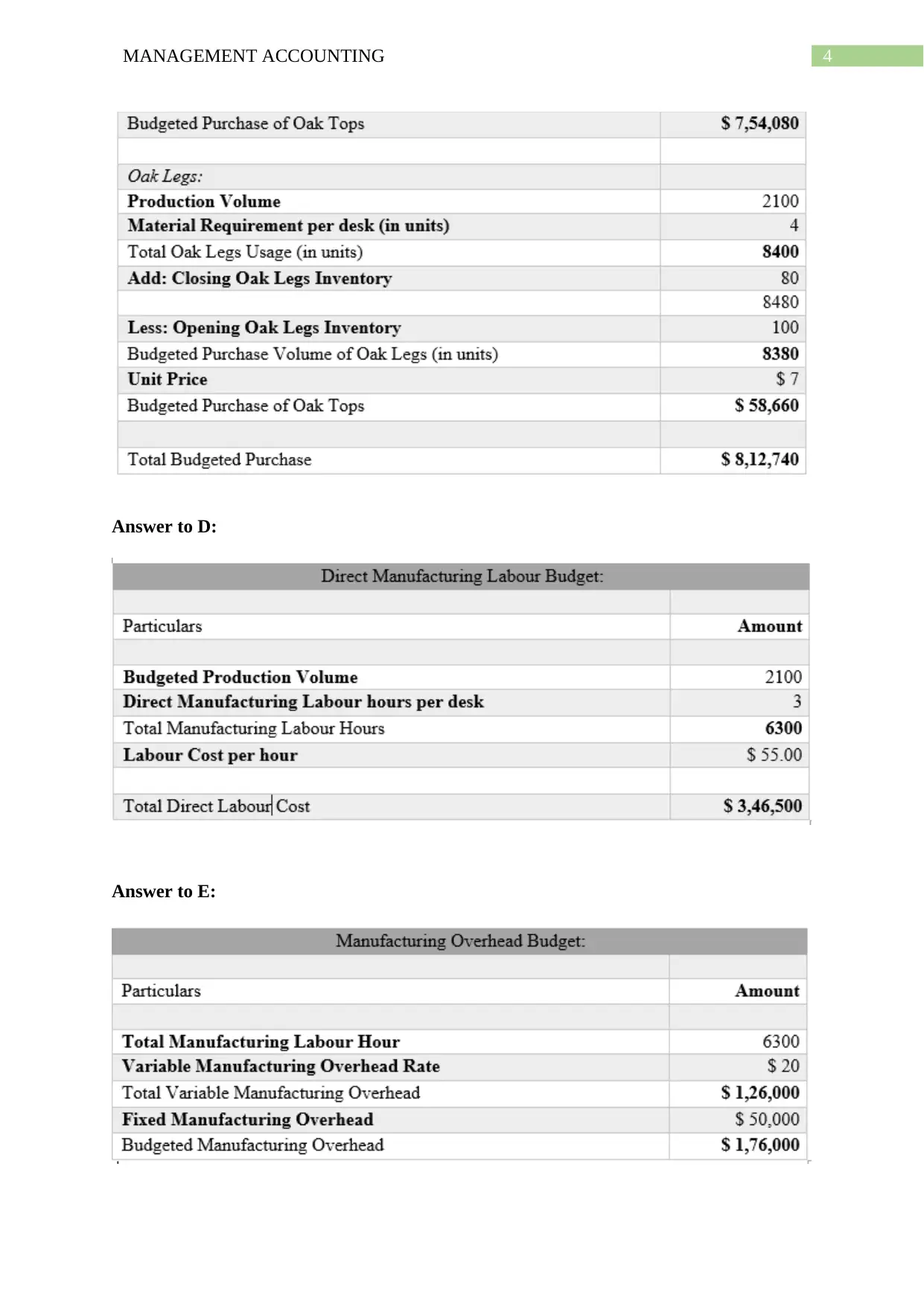

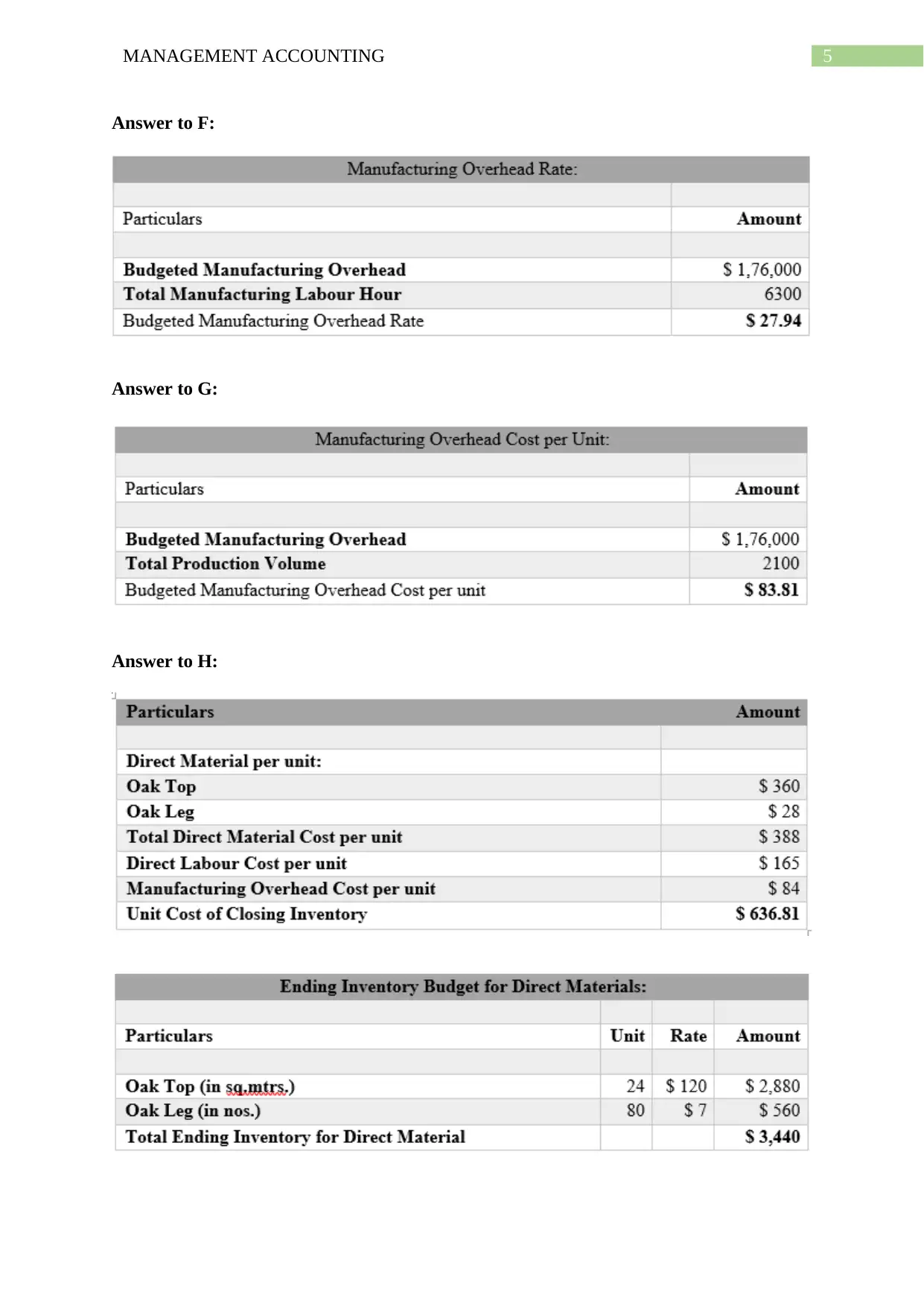

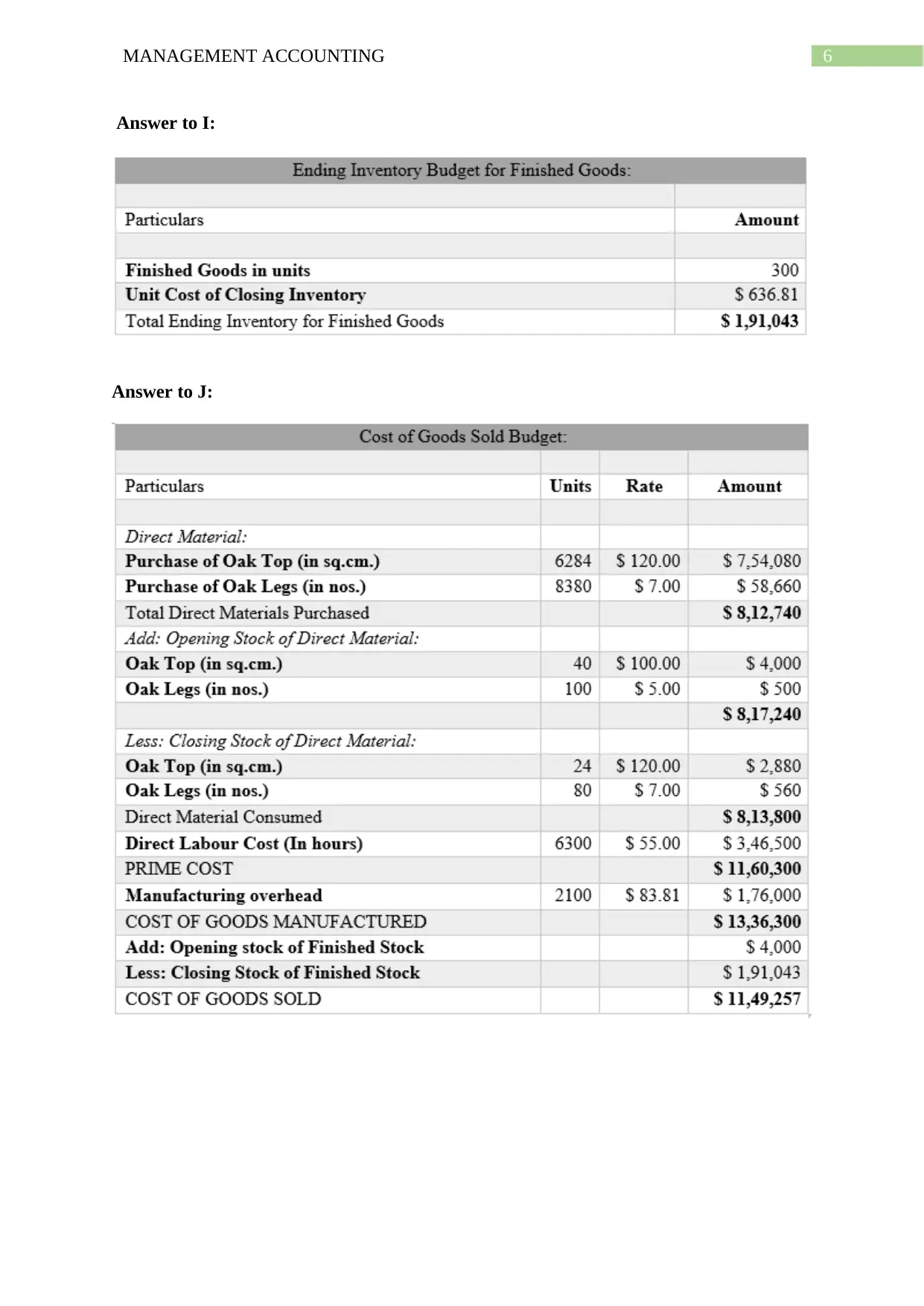

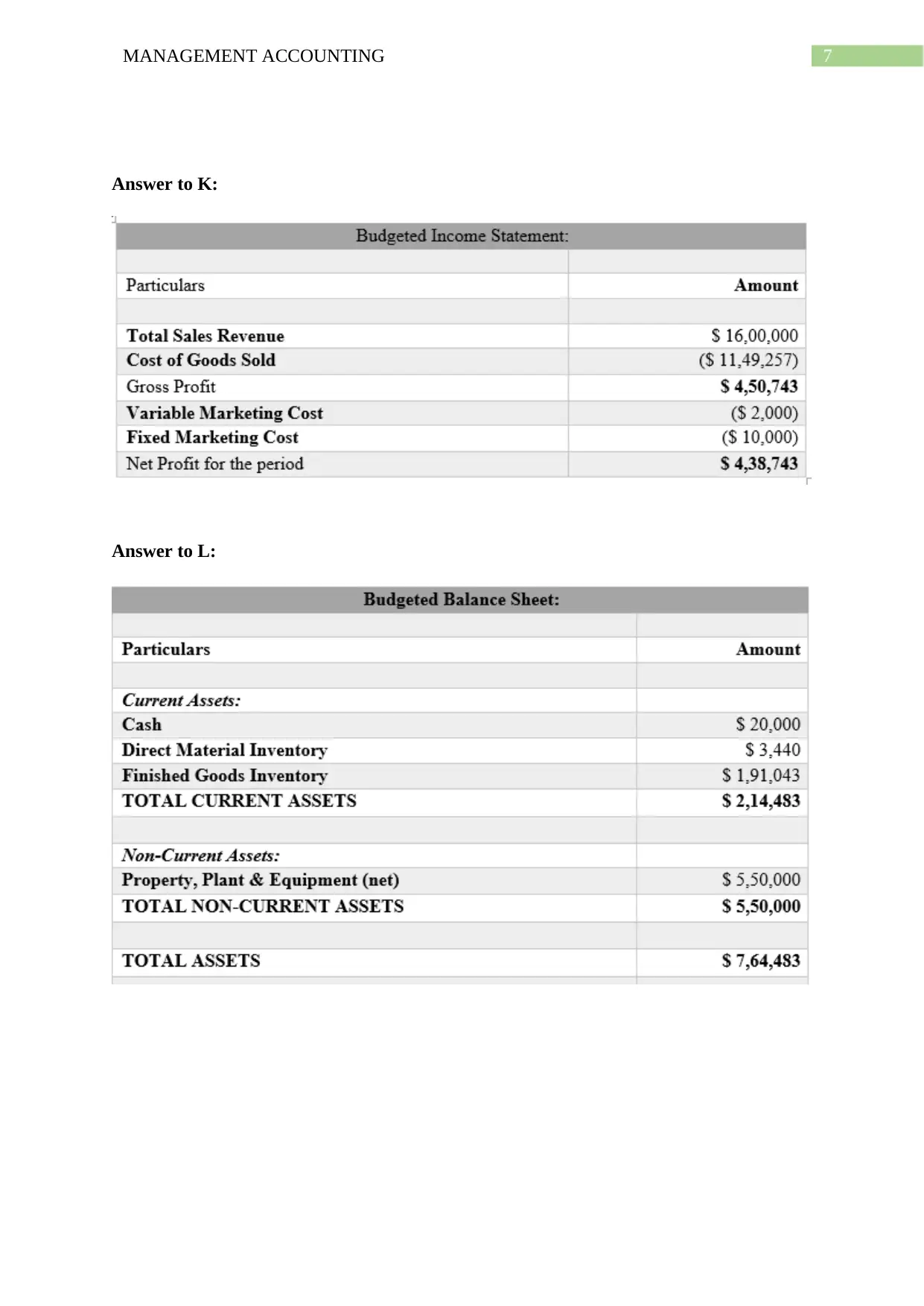

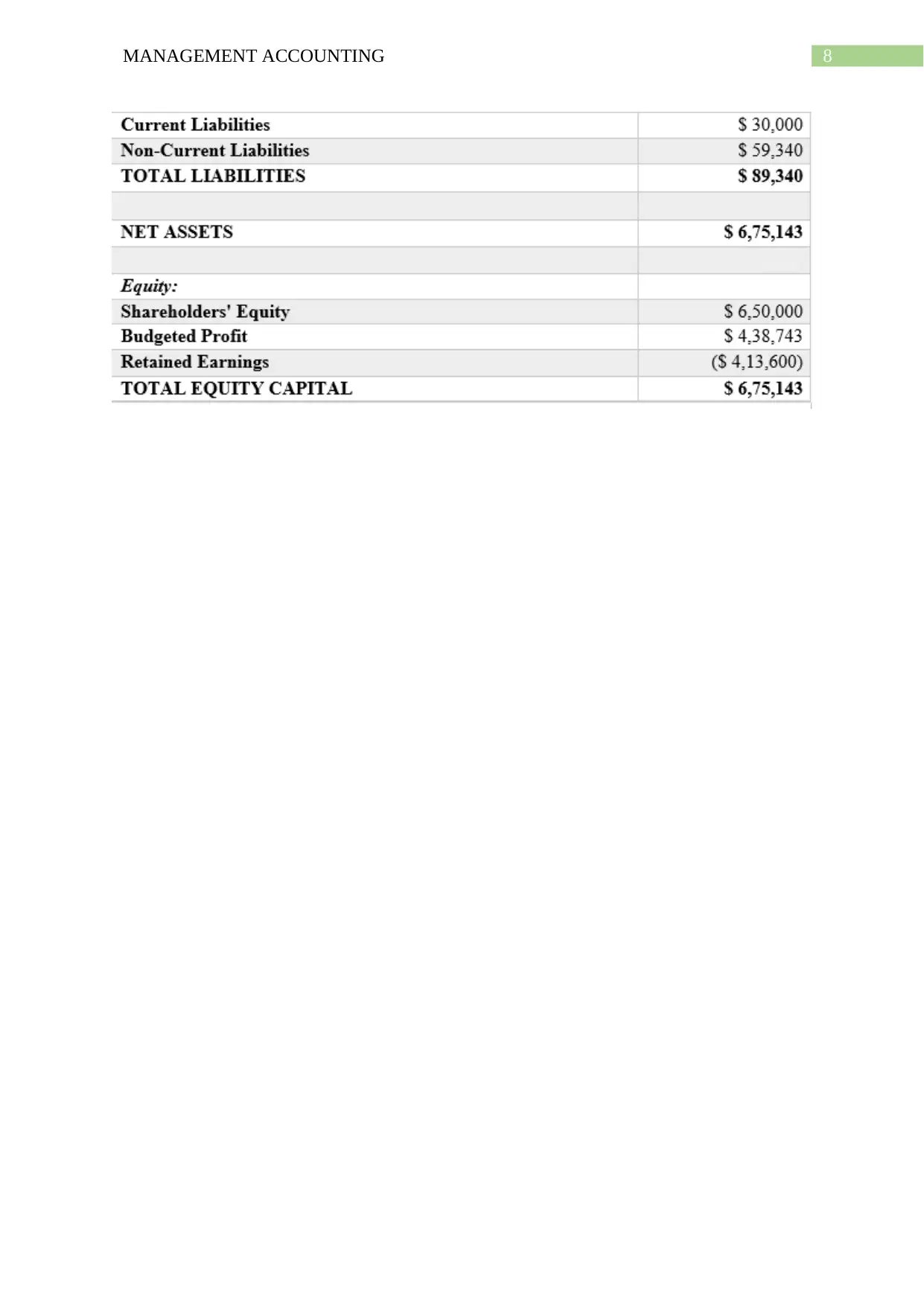

This assignment presents a comprehensive solution to a management accounting case study focused on Exhibition Furniture, a desk manufacturer. The solution addresses various aspects of budgeting, including direct material consumption, flexible budgeting implementation, overhead cost segregation, and variance analysis. It includes a memorandum to the CEO of Exhibition Furniture, providing recommendations for improving the budgetary process through constant improvement, flexible budgeting, and variance analysis. The memorandum suggests focusing on direct material usage, setting up quarterly budgets for better financial projection, and controlling overhead costs to enhance profitability. The analysis covers both oak tops and oak legs, emphasizing the importance of aligning costs with revenue generation and applying budget variance regulations to manage expenses effectively. This document, contributed to Desklib, provides valuable insights for students studying management accounting and seeking practical applications of budgeting principles.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.