Financial Performance: A Management Accounting Report on DIHL Ltd

VerifiedAdded on 2023/06/05

|7

|962

|156

Report

AI Summary

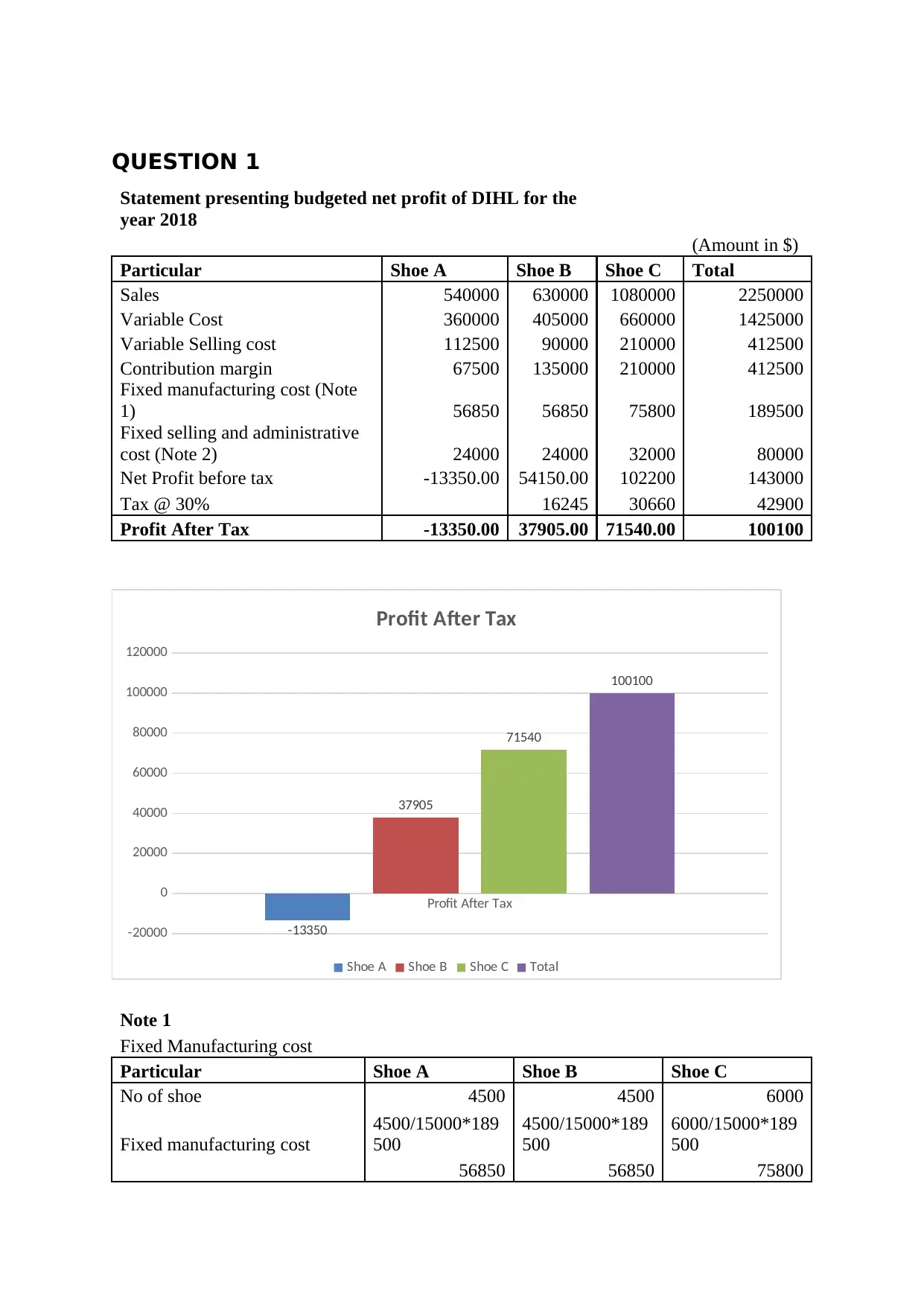

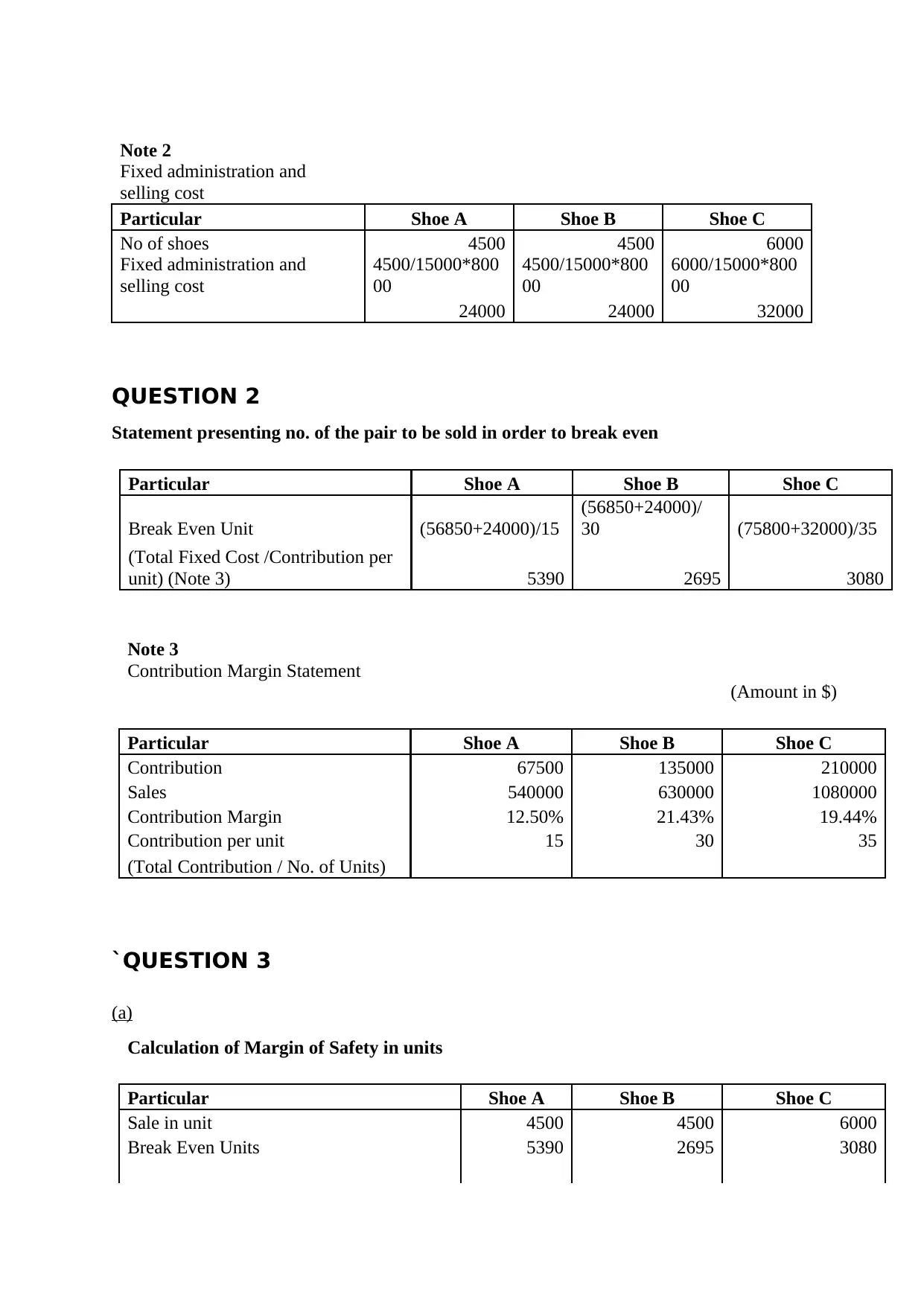

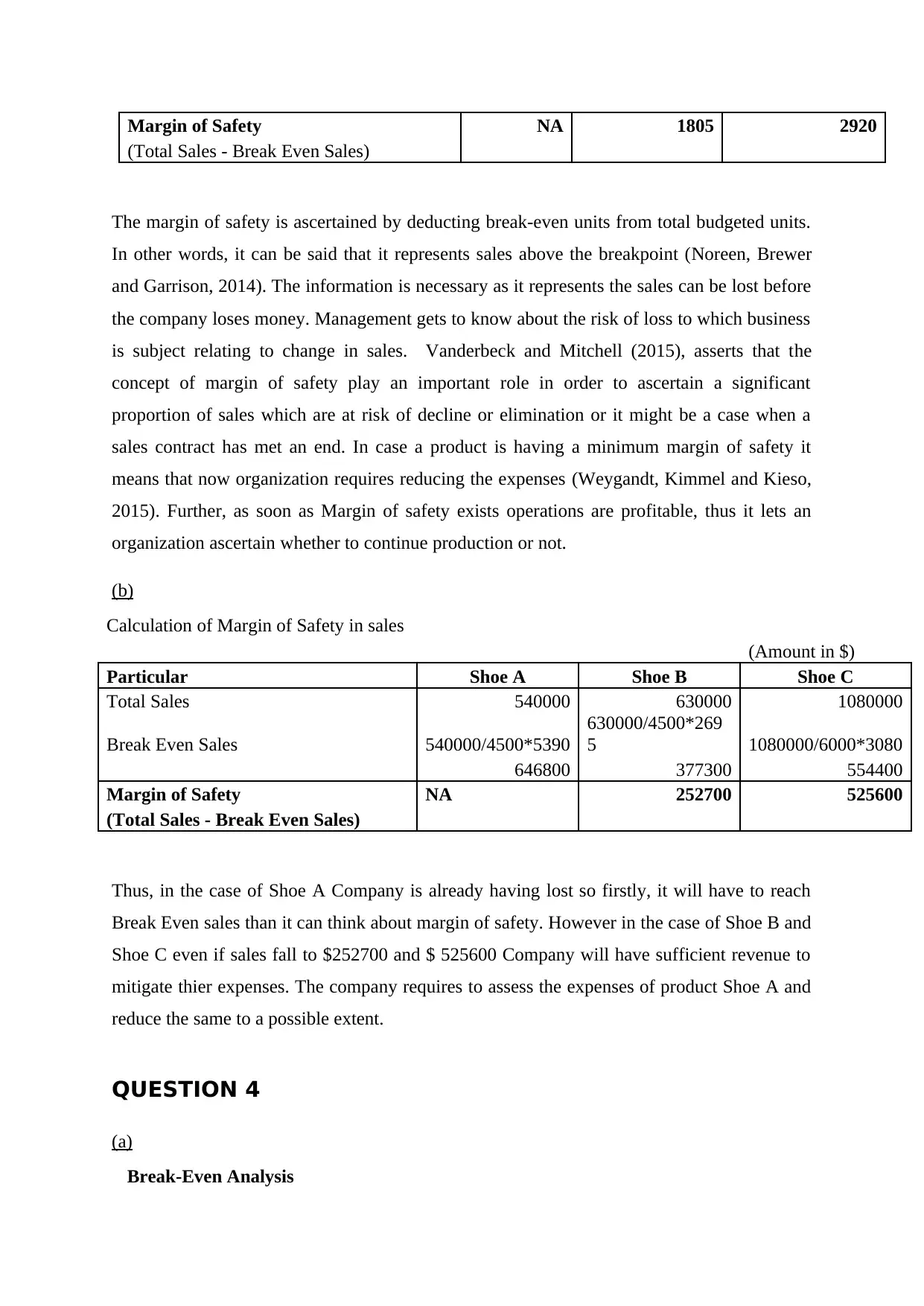

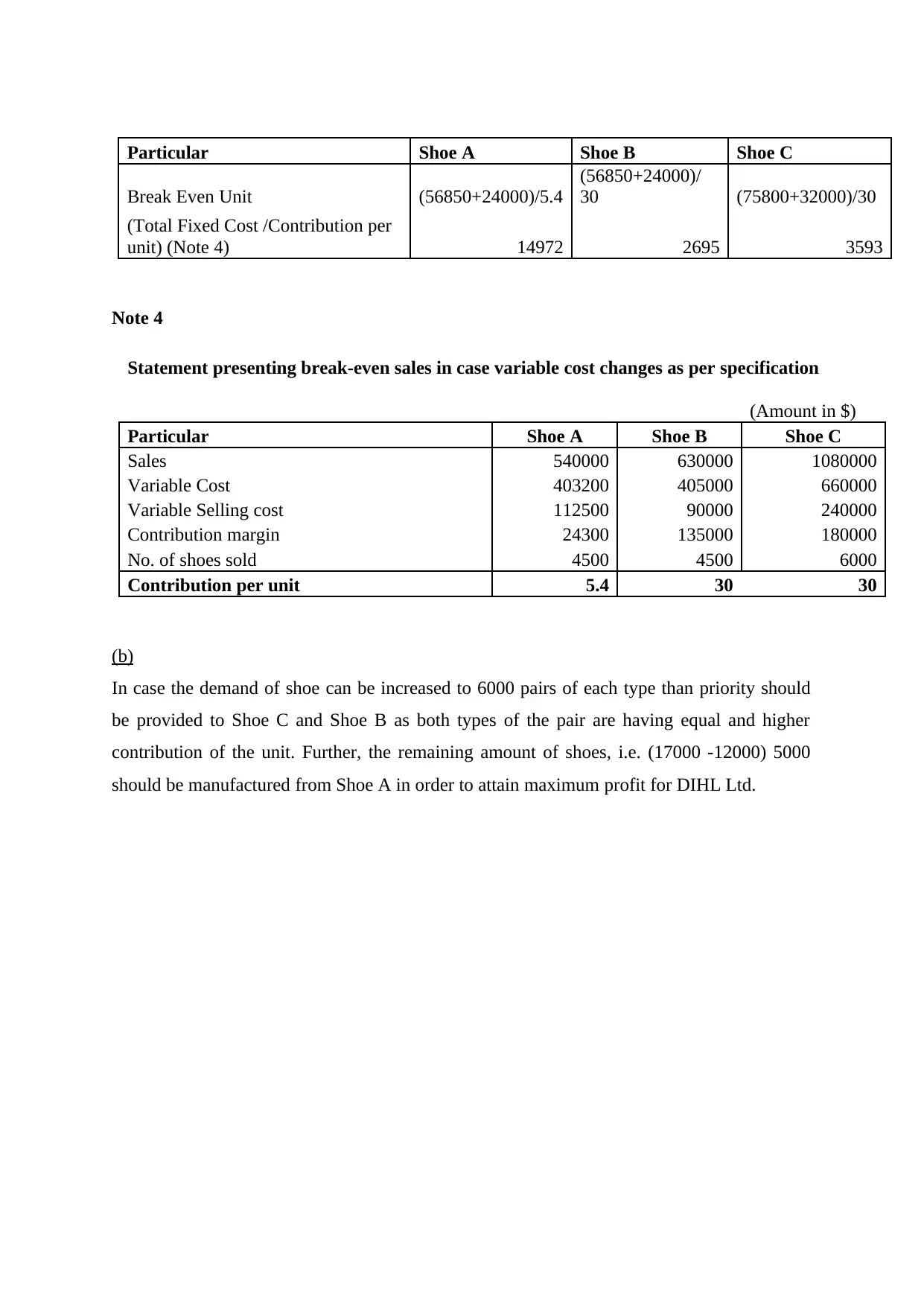

This management accounting report presents a detailed financial analysis of DIHL Ltd for the year 2018. It includes a budgeted net profit statement, break-even analysis, and margin of safety calculations for three shoe types (A, B, and C). The report assesses the impact of variable cost changes on break-even points and recommends production priorities based on contribution margins. The analysis indicates that Shoe A faces challenges in achieving profitability, while Shoe B and Shoe C demonstrate stronger financial performance. The report uses relevant accounting principles and references to support its findings and recommendations, providing insights into DIHL Ltd's financial strategies and operational decisions. Desklib offers a platform for students to access similar solved assignments and past papers for academic support.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.