Management Accounting and Techniques for Financial Reporting

VerifiedAdded on 2023/01/17

|18

|4778

|37

AI Summary

This document provides an overview of management accounting and its essential requirements. It discusses the different methods used for management accounting report, including cost accounting techniques to prepare an income statement. It also explores the use of management accounting techniques for financial reporting. The document is relevant for students studying management accounting or anyone interested in understanding the role of management accounting in financial reporting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1 Management accounting and its essential requirements...................................................................3

P2 Methods used for management accounting report............................................................................5

TASK 2..........................................................................................................................................................6

P3: Cost accounting techniques to prepare an income statement..........................................................6

Management accounting techniques and financial reporting documents............................................10

Financial report and its interpretation for business activities...............................................................11

TASK 3........................................................................................................................................................11

P4 Budgetary control and its types along with advantages and disadvantages.....................................11

Utilisation of different planning tools for forecasting budgets..............................................................13

TASK 4........................................................................................................................................................14

P5: Evaluate how organisations are adapting management accounting systems to respond to financial

problems...............................................................................................................................................14

Analysis of how in responding to financial problems management accounting can lead organisations

to sustainable success...........................................................................................................................15

Various planning tools to resolve financial problems............................................................................16

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1 Management accounting and its essential requirements...................................................................3

P2 Methods used for management accounting report............................................................................5

TASK 2..........................................................................................................................................................6

P3: Cost accounting techniques to prepare an income statement..........................................................6

Management accounting techniques and financial reporting documents............................................10

Financial report and its interpretation for business activities...............................................................11

TASK 3........................................................................................................................................................11

P4 Budgetary control and its types along with advantages and disadvantages.....................................11

Utilisation of different planning tools for forecasting budgets..............................................................13

TASK 4........................................................................................................................................................14

P5: Evaluate how organisations are adapting management accounting systems to respond to financial

problems...............................................................................................................................................14

Analysis of how in responding to financial problems management accounting can lead organisations

to sustainable success...........................................................................................................................15

Various planning tools to resolve financial problems............................................................................16

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION

Management accounting is defined as a managerial action or plan to bring an organisation

ahead than their rivals in competitive market by analysing financial statements prepared on

annual basis as per accounting standards (Bartlett and et.al, 2016). It facilitates internal parties to

make relevant decisions for the betterment of an organisation in the future. Management

accounting is not mandatory for an organisation as it only requires as per their requirements.

KEF Ltd. which is a medium sized organisation engaging in manufacturing sector is undertaken

for this assignment report. The report is prepared to promote the understanding between different

departments in the organisation due to which their senior management accountant is held

responsible to explain the importance of management accounting concept and its different

systems with various related concepts such as reporting systems, costing techniques, planning

tools to control budget, use of managerial accounting in resolving financial issues etc.

TASK 1

P1 Management accounting and its essential requirements

Management accounting- This is defined as the process and procedure that is used to

analysis and communicating all the essential information related with financial aspects of

organisation. So with the financial aspects it is easy for organisation to develop and make

effective strategies that increases performance of KEF limited in effective period.

Origin and evolution of management accounting- Management accounting emerges in

organisation to develop as significant activity in industrial revolution. This was originated in the

financial accounting that is used to trace the origin and its role for making different ventures

(Bromwich and Scapens, 2016).

Management accounting system- It refers to a system that is used by managers of KEF

ltd. to keep the record of different function and operational departments of organisation. There

are various types of management are also used by management to KEF ltd. to find actual status

of organisation.

Difference between financial accounting and management accounting

Financial accounting Management accounting

Management accounting is defined as a managerial action or plan to bring an organisation

ahead than their rivals in competitive market by analysing financial statements prepared on

annual basis as per accounting standards (Bartlett and et.al, 2016). It facilitates internal parties to

make relevant decisions for the betterment of an organisation in the future. Management

accounting is not mandatory for an organisation as it only requires as per their requirements.

KEF Ltd. which is a medium sized organisation engaging in manufacturing sector is undertaken

for this assignment report. The report is prepared to promote the understanding between different

departments in the organisation due to which their senior management accountant is held

responsible to explain the importance of management accounting concept and its different

systems with various related concepts such as reporting systems, costing techniques, planning

tools to control budget, use of managerial accounting in resolving financial issues etc.

TASK 1

P1 Management accounting and its essential requirements

Management accounting- This is defined as the process and procedure that is used to

analysis and communicating all the essential information related with financial aspects of

organisation. So with the financial aspects it is easy for organisation to develop and make

effective strategies that increases performance of KEF limited in effective period.

Origin and evolution of management accounting- Management accounting emerges in

organisation to develop as significant activity in industrial revolution. This was originated in the

financial accounting that is used to trace the origin and its role for making different ventures

(Bromwich and Scapens, 2016).

Management accounting system- It refers to a system that is used by managers of KEF

ltd. to keep the record of different function and operational departments of organisation. There

are various types of management are also used by management to KEF ltd. to find actual status

of organisation.

Difference between financial accounting and management accounting

Financial accounting Management accounting

This provides information in the terms of

financial aspects to the external stakeholders

of organisation.

In these types of accounting information

relates with internal stakeholders. This is used

to make effective strategies for organisation.

In order to conduct financial accounting this

is used by management to conduct results as

per accounting standard and rules.

There are less specific standards and principle

that are used to manage management

accounting in effective manner.

Types of management accounting system:

Cost accounting system- With the help of this it is easy for manager to analyse all

different cost such as variable and fixed organisation. In the context of KEF Ltd., it is used by

organisation to deal with detailed information in order to make better construction and services

related with management. Further, direct and indirect cost is also included in organisation to

track all expenses in accurate manner (Chenhall and Moers, 2015).

In context of KEF ltd. this is used to track all cost that is included to complete all

operations in effective manner and their costs.

Inventory management system- This is used by organisation such as KEF limited to

manage and order all inventory that is required for proper tools and management. The main

motive to implement inventory management system is to record and track all items to prepare

accurate finished goods. Further, LIFO and FIFO are used by organisation to make goods as per

cost basis.

With proper inventory management system KEF ltd. leads organisation to minimize

the cost of their finished goods.

Price optimisation system- This system is used by organisation to find out the optimum

prices of all products and its manufacturing system. So the cost of products which are produced

or manufactured by KEF ltd. are sold by organisation at right price. On the other side, this tool is

also used to add value for analysing the right prices and to increase the value of organisation

(Englund and Gerdin, 2014).

financial aspects to the external stakeholders

of organisation.

In these types of accounting information

relates with internal stakeholders. This is used

to make effective strategies for organisation.

In order to conduct financial accounting this

is used by management to conduct results as

per accounting standard and rules.

There are less specific standards and principle

that are used to manage management

accounting in effective manner.

Types of management accounting system:

Cost accounting system- With the help of this it is easy for manager to analyse all

different cost such as variable and fixed organisation. In the context of KEF Ltd., it is used by

organisation to deal with detailed information in order to make better construction and services

related with management. Further, direct and indirect cost is also included in organisation to

track all expenses in accurate manner (Chenhall and Moers, 2015).

In context of KEF ltd. this is used to track all cost that is included to complete all

operations in effective manner and their costs.

Inventory management system- This is used by organisation such as KEF limited to

manage and order all inventory that is required for proper tools and management. The main

motive to implement inventory management system is to record and track all items to prepare

accurate finished goods. Further, LIFO and FIFO are used by organisation to make goods as per

cost basis.

With proper inventory management system KEF ltd. leads organisation to minimize

the cost of their finished goods.

Price optimisation system- This system is used by organisation to find out the optimum

prices of all products and its manufacturing system. So the cost of products which are produced

or manufactured by KEF ltd. are sold by organisation at right price. On the other side, this tool is

also used to add value for analysing the right prices and to increase the value of organisation

(Englund and Gerdin, 2014).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

KEF ltd. utilise this system to select right price for products that leads management

to earn profits and to satisfy the customers expectation.

Job costing system- This system is also used by management to accumulate right cost of

all units which is related with organisation and its performance. In the context of KEF limited

there are various projects are performed by management to complete their work and analyse the

overall cost for organisation. Moreover, with the help of job costing system it leads organisation

to determine cost of all units on individual basis.

With the system of job costing management of KEF ltd. analyse the cost of all units

as per the specification of all units.

P2 Methods used for management accounting report

Management accounting report works as a process that is used to generate better reports on

the basis of information regarding organisational performance. In the context of KEF ltd.

different types of management accounting reports are mention as follow:

Performance report- This report is used to generate to keep and track all the performance

of all operations as well as of their employees who are engaged in organisational operations and

functions. From the perspective of KEF ltd. all the performance related with organisation that is

used to record all the information and business activities. This results the goals and objective are

achieved in shorter period with more efficiency and effectiveness (Fullerton, Kennedy and

Widener, 2014).

Budget report- This reports works as an internal part of the organisation through which

management is able to decide and assign the prices for all its functions. Further, in the context of

KEF Limited budget reports are developed by organisation to complete their work according to

the estimated prices of organisation. So the actual and estimated prices are managed by

organisation to complete their project as per needs of management. This results the profits of

KEF limited increases in better manner (Shipman, Swanquist and Whited, 2016T).

Account receivable report- An account receivable report is defined as a method that is used

to record the list of unpaid invoices. This refers it is to beneficial to collect evidence and to

summarise all credit transactions. KEF Ltd. Utilise account receivable report as a primary tool to

analyse those invoices that are overdue for payment. Further, it also helps the organisation to

to earn profits and to satisfy the customers expectation.

Job costing system- This system is also used by management to accumulate right cost of

all units which is related with organisation and its performance. In the context of KEF limited

there are various projects are performed by management to complete their work and analyse the

overall cost for organisation. Moreover, with the help of job costing system it leads organisation

to determine cost of all units on individual basis.

With the system of job costing management of KEF ltd. analyse the cost of all units

as per the specification of all units.

P2 Methods used for management accounting report

Management accounting report works as a process that is used to generate better reports on

the basis of information regarding organisational performance. In the context of KEF ltd.

different types of management accounting reports are mention as follow:

Performance report- This report is used to generate to keep and track all the performance

of all operations as well as of their employees who are engaged in organisational operations and

functions. From the perspective of KEF ltd. all the performance related with organisation that is

used to record all the information and business activities. This results the goals and objective are

achieved in shorter period with more efficiency and effectiveness (Fullerton, Kennedy and

Widener, 2014).

Budget report- This reports works as an internal part of the organisation through which

management is able to decide and assign the prices for all its functions. Further, in the context of

KEF Limited budget reports are developed by organisation to complete their work according to

the estimated prices of organisation. So the actual and estimated prices are managed by

organisation to complete their project as per needs of management. This results the profits of

KEF limited increases in better manner (Shipman, Swanquist and Whited, 2016T).

Account receivable report- An account receivable report is defined as a method that is used

to record the list of unpaid invoices. This refers it is to beneficial to collect evidence and to

summarise all credit transactions. KEF Ltd. Utilise account receivable report as a primary tool to

analyse those invoices that are overdue for payment. Further, it also helps the organisation to

utilise account report as the contract evidence between organisation and customers. It also ehlps

the organisation to record credit transactions for longer period.

It leads organisation to consider and seprate the actual amounts which are sold by KEF

with the cash and credit basis.

Job costing report- Job costing reports works as an effective tool which leads organisation to

monitor and analyse the overall profits and loss of the organisation. KEF limited implement job

costing report in order to identify the cost of all their projects and services which are offered by

organisation to the customers. With the proper record of job costing it is easy for management to

calculate the actual cost of their operations. Profits of the organisation are efficiently calculated

by organisation through job costing method (Tucker and Lowe, 2014).

With this system management analysis the cost and try those methods that reduces the

overall cost of organisation.

Inter-relation between management accounting and management reporting

All the actions and activities that are undertaken while the process of management

accounting and reporting are inter-related with each other. This governs both of this financial

system leads the management of KEF Ltd to achieve similar goals and objectives. Like job

costing system helps organisation to analyse the actual cost and profits. On the other side, with

the apply of account receivable report it is also easy for management to recover their debts that

are due from longer period.

TASK 2

P3: Cost accounting techniques to prepare an income statement

Cost- Cost is defined as the net amount which is allocated for different business operations

with the expectations of getting maximum return in future. It consists of direct and indirect cost.

Direct cost involves amount which is directly engaged in the process of manufacturing activity of

KEF Ltd. that includes direct labour and direct material. On the other hand, indirect cost includes

the amount which is involved in manufacturing activity indirectly that includes electricity

payments, rent and expenses etc. There are two kinds of costing techniques which are stated as

under:

the organisation to record credit transactions for longer period.

It leads organisation to consider and seprate the actual amounts which are sold by KEF

with the cash and credit basis.

Job costing report- Job costing reports works as an effective tool which leads organisation to

monitor and analyse the overall profits and loss of the organisation. KEF limited implement job

costing report in order to identify the cost of all their projects and services which are offered by

organisation to the customers. With the proper record of job costing it is easy for management to

calculate the actual cost of their operations. Profits of the organisation are efficiently calculated

by organisation through job costing method (Tucker and Lowe, 2014).

With this system management analysis the cost and try those methods that reduces the

overall cost of organisation.

Inter-relation between management accounting and management reporting

All the actions and activities that are undertaken while the process of management

accounting and reporting are inter-related with each other. This governs both of this financial

system leads the management of KEF Ltd to achieve similar goals and objectives. Like job

costing system helps organisation to analyse the actual cost and profits. On the other side, with

the apply of account receivable report it is also easy for management to recover their debts that

are due from longer period.

TASK 2

P3: Cost accounting techniques to prepare an income statement

Cost- Cost is defined as the net amount which is allocated for different business operations

with the expectations of getting maximum return in future. It consists of direct and indirect cost.

Direct cost involves amount which is directly engaged in the process of manufacturing activity of

KEF Ltd. that includes direct labour and direct material. On the other hand, indirect cost includes

the amount which is involved in manufacturing activity indirectly that includes electricity

payments, rent and expenses etc. There are two kinds of costing techniques which are stated as

under:

Marginal costing- This is a technique which is mostly adopted by small and medium sized

organisation such as KEF Ltd. due to providing them an opportunity to show high figures in net

profit than actual under financial statements which can make easy for their management to raise

finance from various investors. It is also known as variable costing method due to including only

variable cost and ignoring fixed cost (Honggowati and et.al., 2017).

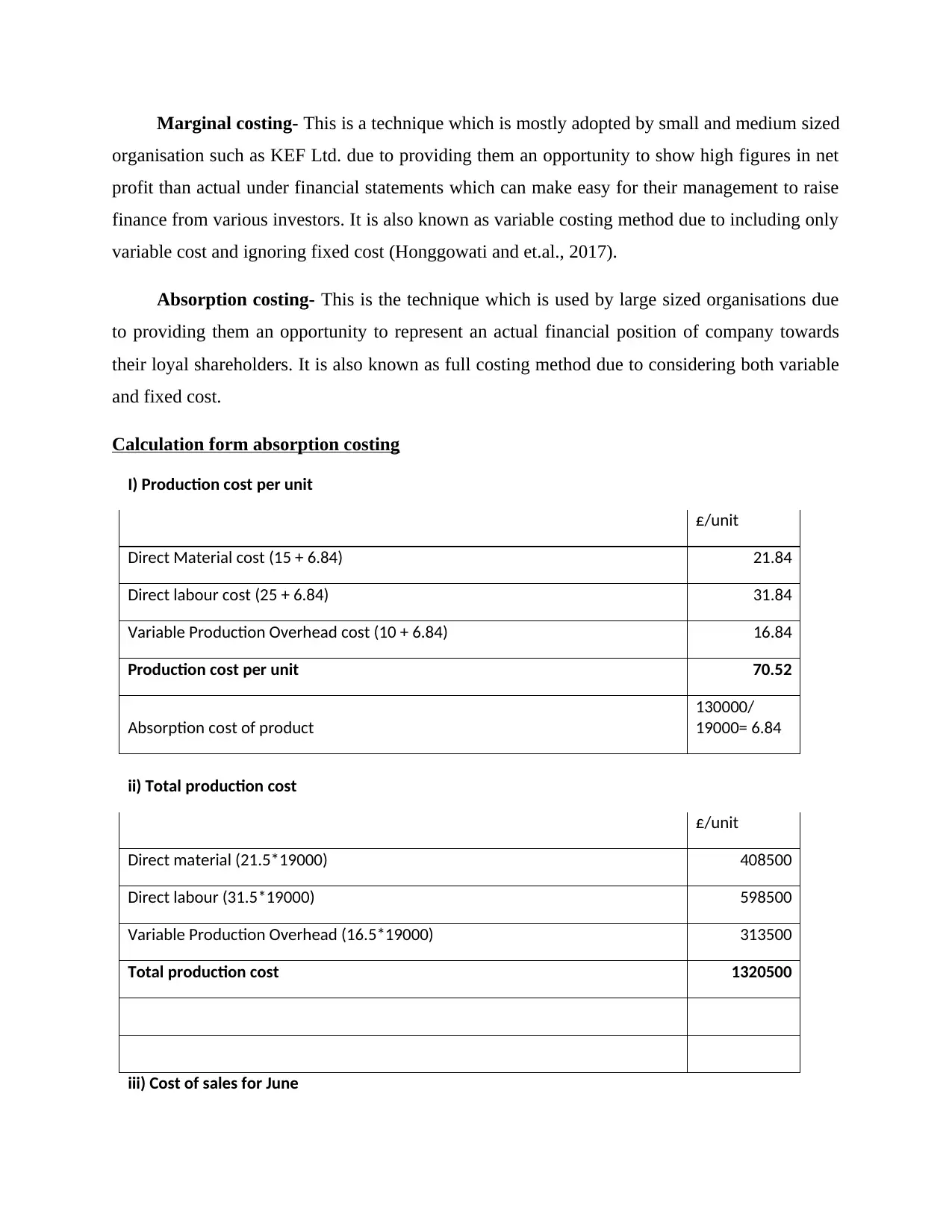

Absorption costing- This is the technique which is used by large sized organisations due

to providing them an opportunity to represent an actual financial position of company towards

their loyal shareholders. It is also known as full costing method due to considering both variable

and fixed cost.

Calculation form absorption costing

I) Production cost per unit

£/unit

Direct Material cost (15 + 6.84) 21.84

Direct labour cost (25 + 6.84) 31.84

Variable Production Overhead cost (10 + 6.84) 16.84

Production cost per unit 70.52

Absorption cost of product

130000/

19000= 6.84

ii) Total production cost

£/unit

Direct material (21.5*19000) 408500

Direct labour (31.5*19000) 598500

Variable Production Overhead (16.5*19000) 313500

Total production cost 1320500

iii) Cost of sales for June

organisation such as KEF Ltd. due to providing them an opportunity to show high figures in net

profit than actual under financial statements which can make easy for their management to raise

finance from various investors. It is also known as variable costing method due to including only

variable cost and ignoring fixed cost (Honggowati and et.al., 2017).

Absorption costing- This is the technique which is used by large sized organisations due

to providing them an opportunity to represent an actual financial position of company towards

their loyal shareholders. It is also known as full costing method due to considering both variable

and fixed cost.

Calculation form absorption costing

I) Production cost per unit

£/unit

Direct Material cost (15 + 6.84) 21.84

Direct labour cost (25 + 6.84) 31.84

Variable Production Overhead cost (10 + 6.84) 16.84

Production cost per unit 70.52

Absorption cost of product

130000/

19000= 6.84

ii) Total production cost

£/unit

Direct material (21.5*19000) 408500

Direct labour (31.5*19000) 598500

Variable Production Overhead (16.5*19000) 313500

Total production cost 1320500

iii) Cost of sales for June

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

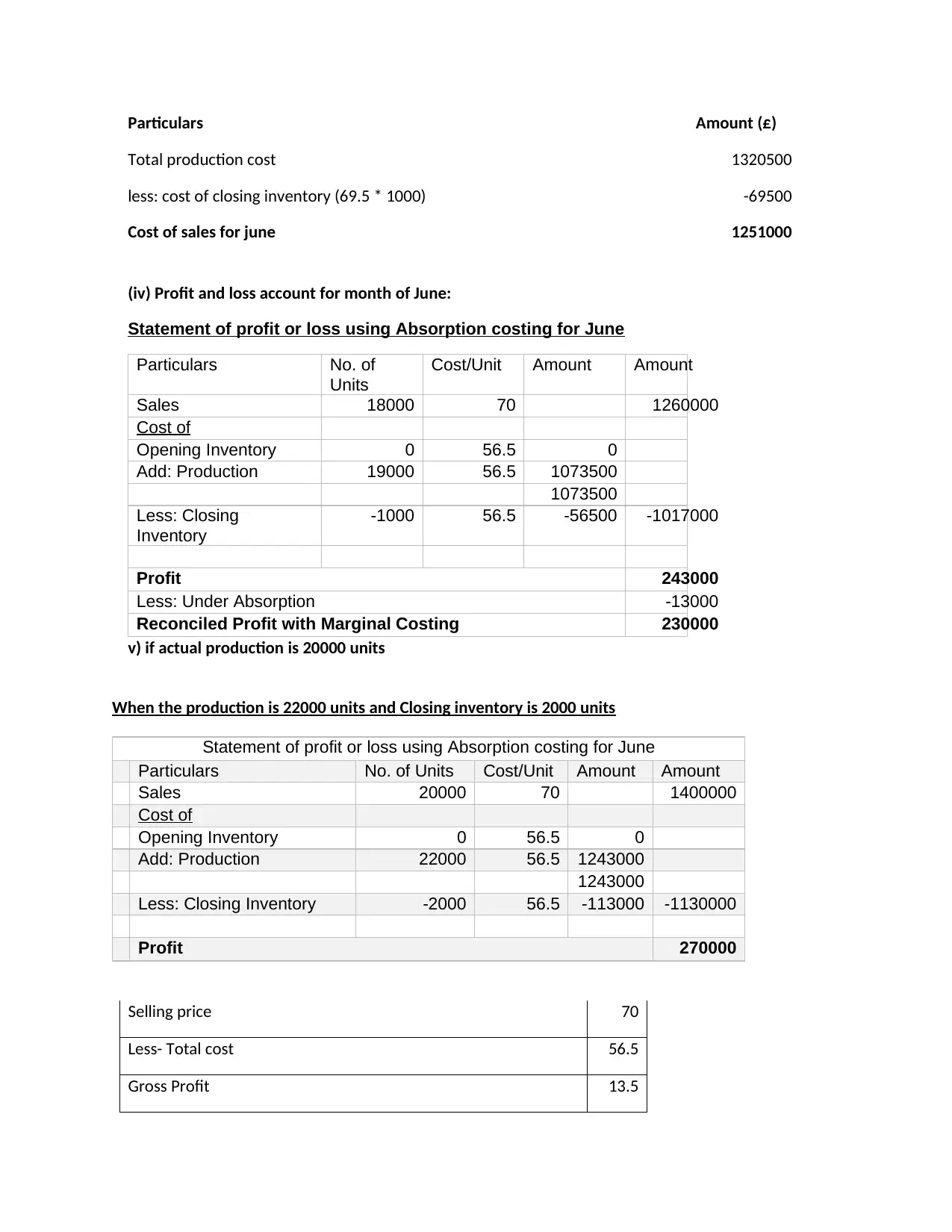

Particulars Amount (£)

Total production cost 1320500

less: cost of closing inventory (69.5 * 1000) -69500

Cost of sales for june 1251000

(iv) Profit and loss account for month of June:

Statement of profit or loss using Absorption costing for June

Particulars No. of

Units

Cost/Unit Amount Amount

Sales 18000 70 1260000

Cost of

Opening Inventory 0 56.5 0

Add: Production 19000 56.5 1073500

1073500

Less: Closing

Inventory

-1000 56.5 -56500 -1017000

Profit 243000

Less: Under Absorption -13000

Reconciled Profit with Marginal Costing 230000

v) if actual production is 20000 units

When the production is 22000 units and Closing inventory is 2000 units

Statement of profit or loss using Absorption costing for June

Particulars No. of Units Cost/Unit Amount Amount

Sales 20000 70 1400000

Cost of

Opening Inventory 0 56.5 0

Add: Production 22000 56.5 1243000

1243000

Less: Closing Inventory -2000 56.5 -113000 -1130000

Profit 270000

Selling price 70

Less- Total cost 56.5

Gross Profit 13.5

Total production cost 1320500

less: cost of closing inventory (69.5 * 1000) -69500

Cost of sales for june 1251000

(iv) Profit and loss account for month of June:

Statement of profit or loss using Absorption costing for June

Particulars No. of

Units

Cost/Unit Amount Amount

Sales 18000 70 1260000

Cost of

Opening Inventory 0 56.5 0

Add: Production 19000 56.5 1073500

1073500

Less: Closing

Inventory

-1000 56.5 -56500 -1017000

Profit 243000

Less: Under Absorption -13000

Reconciled Profit with Marginal Costing 230000

v) if actual production is 20000 units

When the production is 22000 units and Closing inventory is 2000 units

Statement of profit or loss using Absorption costing for June

Particulars No. of Units Cost/Unit Amount Amount

Sales 20000 70 1400000

Cost of

Opening Inventory 0 56.5 0

Add: Production 22000 56.5 1243000

1243000

Less: Closing Inventory -2000 56.5 -113000 -1130000

Profit 270000

Selling price 70

Less- Total cost 56.5

Gross Profit 13.5

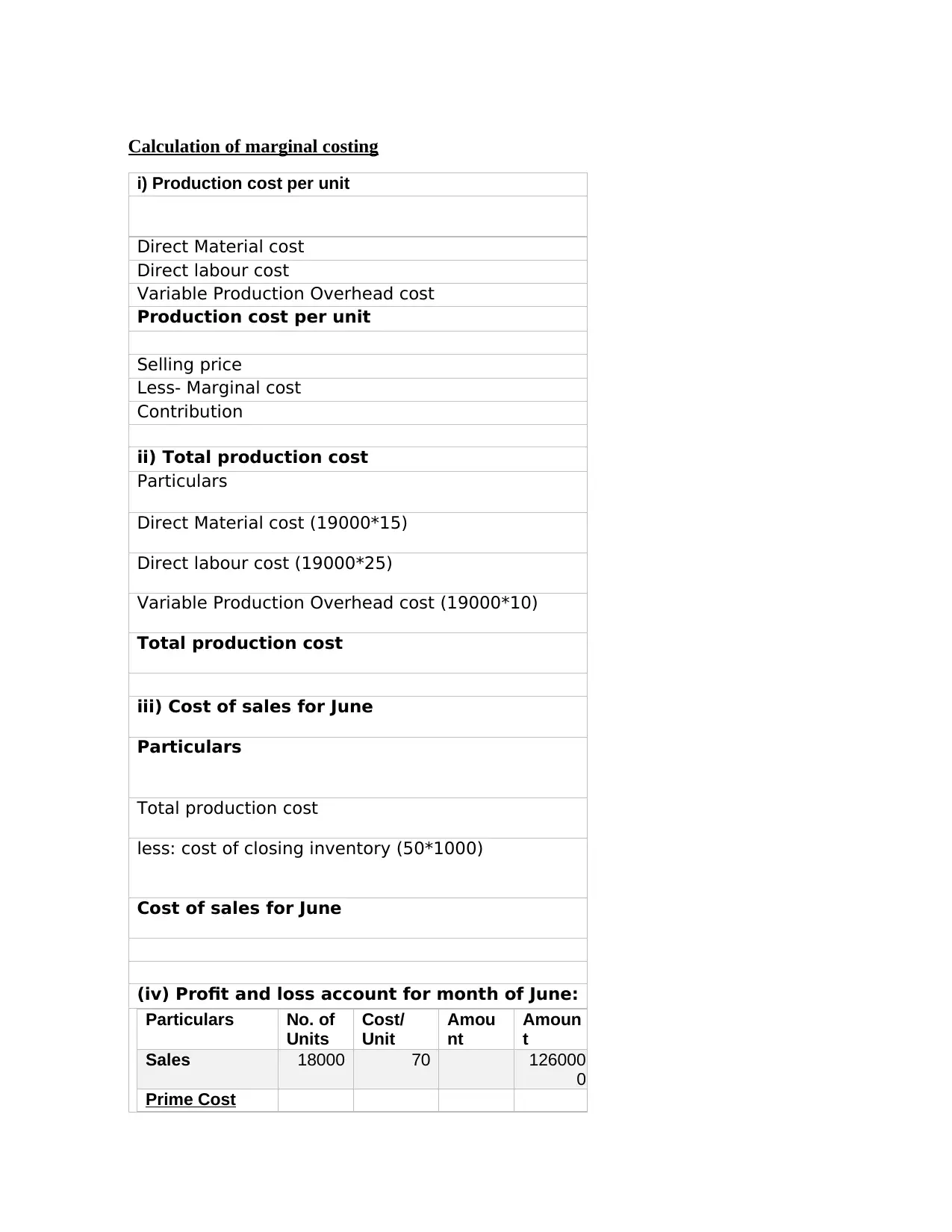

Calculation of marginal costing

i) Production cost per unit

Direct Material cost

Direct labour cost

Variable Production Overhead cost

Production cost per unit

Selling price

Less- Marginal cost

Contribution

ii) Total production cost

Particulars

Direct Material cost (19000*15)

Direct labour cost (19000*25)

Variable Production Overhead cost (19000*10)

Total production cost

iii) Cost of sales for June

Particulars

Total production cost

less: cost of closing inventory (50*1000)

Cost of sales for June

(iv) Profit and loss account for month of June:

Particulars No. of

Units

Cost/

Unit

Amou

nt

Amoun

t

Sales 18000 70 126000

0

Prime Cost

i) Production cost per unit

Direct Material cost

Direct labour cost

Variable Production Overhead cost

Production cost per unit

Selling price

Less- Marginal cost

Contribution

ii) Total production cost

Particulars

Direct Material cost (19000*15)

Direct labour cost (19000*25)

Variable Production Overhead cost (19000*10)

Total production cost

iii) Cost of sales for June

Particulars

Total production cost

less: cost of closing inventory (50*1000)

Cost of sales for June

(iv) Profit and loss account for month of June:

Particulars No. of

Units

Cost/

Unit

Amou

nt

Amoun

t

Sales 18000 70 126000

0

Prime Cost

Opening

Inventory

0 50 0

Add:

Production

19000 50 950000

950000

Less: Closing

Inventory

-1000 50 -50000 -900000

Contribution 360000

Less: Fixed Production Cost -130000

Marginal Profit 230000

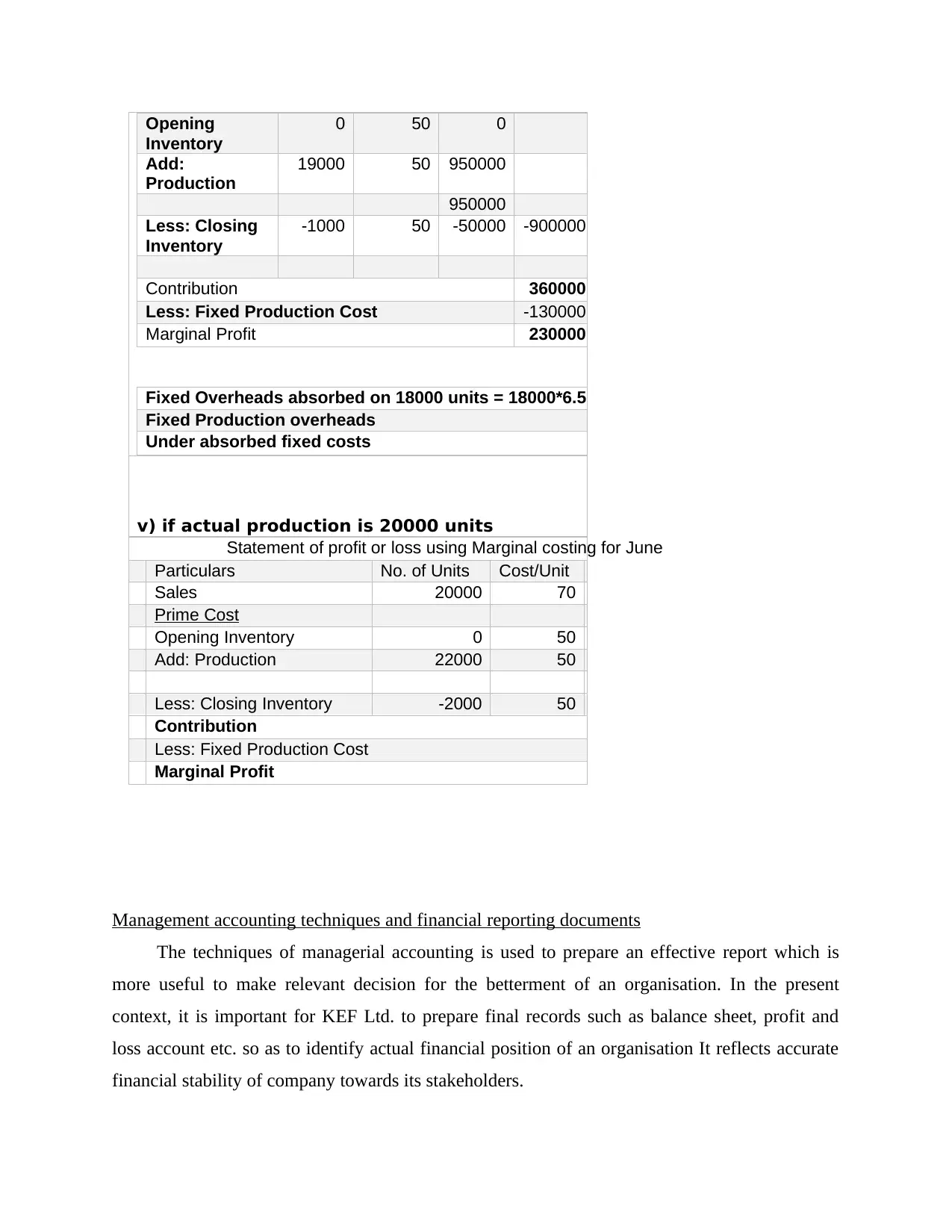

Fixed Overheads absorbed on 18000 units = 18000*6.5

Fixed Production overheads

Under absorbed fixed costs

v) if actual production is 20000 units

Statement of profit or loss using Marginal costing for June

Particulars No. of Units Cost/Unit

Sales 20000 70

Prime Cost

Opening Inventory 0 50

Add: Production 22000 50

Less: Closing Inventory -2000 50

Contribution

Less: Fixed Production Cost

Marginal Profit

Management accounting techniques and financial reporting documents

The techniques of managerial accounting is used to prepare an effective report which is

more useful to make relevant decision for the betterment of an organisation. In the present

context, it is important for KEF Ltd. to prepare final records such as balance sheet, profit and

loss account etc. so as to identify actual financial position of an organisation It reflects accurate

financial stability of company towards its stakeholders.

Inventory

0 50 0

Add:

Production

19000 50 950000

950000

Less: Closing

Inventory

-1000 50 -50000 -900000

Contribution 360000

Less: Fixed Production Cost -130000

Marginal Profit 230000

Fixed Overheads absorbed on 18000 units = 18000*6.5

Fixed Production overheads

Under absorbed fixed costs

v) if actual production is 20000 units

Statement of profit or loss using Marginal costing for June

Particulars No. of Units Cost/Unit

Sales 20000 70

Prime Cost

Opening Inventory 0 50

Add: Production 22000 50

Less: Closing Inventory -2000 50

Contribution

Less: Fixed Production Cost

Marginal Profit

Management accounting techniques and financial reporting documents

The techniques of managerial accounting is used to prepare an effective report which is

more useful to make relevant decision for the betterment of an organisation. In the present

context, it is important for KEF Ltd. to prepare final records such as balance sheet, profit and

loss account etc. so as to identify actual financial position of an organisation It reflects accurate

financial stability of company towards its stakeholders.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Financial report and its interpretation for business activities

Financial statement represents financial stability of an organisation which can make good

image in the stakeholders’ mind. Thus, preparing financial records is must on annual basis as per

accounting standards otherwise an organisation must be penalised. The differences in profit

between marginal and absorption costing method is due to inclusion of fixed cost.

TASK 3

P4 Budgetary control and its types along with advantages and disadvantages

Budget is defined as an amount which is invested in the execution of project activities by

allocation of cost to different project activities with a hope of getting maximum profitable

outcomes (Budget, 2019).

Types of Budget

The budget is a forecast of an organization's sources and requirements of funds for the

next financial period (month, quarter, year). It can be of various types based on different

classifications. Most common of the different types of budget are :

Cash Budget: A cash budget estimates the projected sources and applications of cash

and cash equivalents for the next periods. It ascertains whether operations and other activities of

KEF Ltd. will generate enough cash to meet budgeted requirements. If not, management has to

find additional sources for funding (Lindholm, Laine and Suomala, 2017).

Static Budget: A static budget uses anticipated values of inputs and outputs conceived.

The static budget remains unchanged even after experiencing high differences with actual figures

Planning Tools to Control Budget

A successful budget is the result of good coordination of financial and non-financial

planning aimed at achieving organizational goals. Following points should be kept in mind by

the management of KEF Ltd. while preparing the budget for the organization.

Support of Top Management: It is the duty of directors, chairpersons and chief

executives of KEF Ltd. to clearly specify the long term goals of the company for which the

budget is to be prepared. It is also the role of top management to convey these goals to the

middle management.

Financial statement represents financial stability of an organisation which can make good

image in the stakeholders’ mind. Thus, preparing financial records is must on annual basis as per

accounting standards otherwise an organisation must be penalised. The differences in profit

between marginal and absorption costing method is due to inclusion of fixed cost.

TASK 3

P4 Budgetary control and its types along with advantages and disadvantages

Budget is defined as an amount which is invested in the execution of project activities by

allocation of cost to different project activities with a hope of getting maximum profitable

outcomes (Budget, 2019).

Types of Budget

The budget is a forecast of an organization's sources and requirements of funds for the

next financial period (month, quarter, year). It can be of various types based on different

classifications. Most common of the different types of budget are :

Cash Budget: A cash budget estimates the projected sources and applications of cash

and cash equivalents for the next periods. It ascertains whether operations and other activities of

KEF Ltd. will generate enough cash to meet budgeted requirements. If not, management has to

find additional sources for funding (Lindholm, Laine and Suomala, 2017).

Static Budget: A static budget uses anticipated values of inputs and outputs conceived.

The static budget remains unchanged even after experiencing high differences with actual figures

Planning Tools to Control Budget

A successful budget is the result of good coordination of financial and non-financial

planning aimed at achieving organizational goals. Following points should be kept in mind by

the management of KEF Ltd. while preparing the budget for the organization.

Support of Top Management: It is the duty of directors, chairpersons and chief

executives of KEF Ltd. to clearly specify the long term goals of the company for which the

budget is to be prepared. It is also the role of top management to convey these goals to the

middle management.

Participation in Goal Setting: Budgets are plans on how to acquire and use

organizational resources to achieve long term goals. The success of the planned budget is

directly related to employees' inputs to the budgetary plan (Lindholm, Laine and Suomala,

2017).

Flexibility: Businesses are dynamic, and thus require flexibility in its plans to survive in

the market. The important variables must always be kept an eye on and adjusted from time to

time as the need be.

Follow-up: The actual revenues and expenditures must be compared with budgeted

figures and the deviations so arising, must be adjusted for in the subsequent budgets.

Master Budget

Master budget is the integration of operating and financial budgets. Operating budget

includes the budgeted income statement elements such as revenue and expenses whereas

financial budget forecasts the balance sheet elements such as expected value of assets, liabilities,

and owner's funds. It consists of absolute forecasted figures and is rigid in nature. Its advantages

and disadvantages for KEF Ltd. are as follows:

S. No Advantages Disadvantages

1 It provides all required functional budgets in

single format.

It limits the scope of innovation and change

in the organization.

2 It provides complete idea of the forecasted

performance of the organization in terms of

expected profits

It is often very time consuming and costly to

the KEF Ltd. as it involves rigorous planning.

Flexible Budget

The flexible budget is calculated on the actual output units. Budgeted amounts (i.e.,

selling prices or costs) are multiplied by actual units to determine what particular number will be

given to a level of output or sales (McVay, Kennedy and Fullerton, 2016). The calculation yields

the total variable costs involved in production of KEF Ltd. The second component of the flexible

organizational resources to achieve long term goals. The success of the planned budget is

directly related to employees' inputs to the budgetary plan (Lindholm, Laine and Suomala,

2017).

Flexibility: Businesses are dynamic, and thus require flexibility in its plans to survive in

the market. The important variables must always be kept an eye on and adjusted from time to

time as the need be.

Follow-up: The actual revenues and expenditures must be compared with budgeted

figures and the deviations so arising, must be adjusted for in the subsequent budgets.

Master Budget

Master budget is the integration of operating and financial budgets. Operating budget

includes the budgeted income statement elements such as revenue and expenses whereas

financial budget forecasts the balance sheet elements such as expected value of assets, liabilities,

and owner's funds. It consists of absolute forecasted figures and is rigid in nature. Its advantages

and disadvantages for KEF Ltd. are as follows:

S. No Advantages Disadvantages

1 It provides all required functional budgets in

single format.

It limits the scope of innovation and change

in the organization.

2 It provides complete idea of the forecasted

performance of the organization in terms of

expected profits

It is often very time consuming and costly to

the KEF Ltd. as it involves rigorous planning.

Flexible Budget

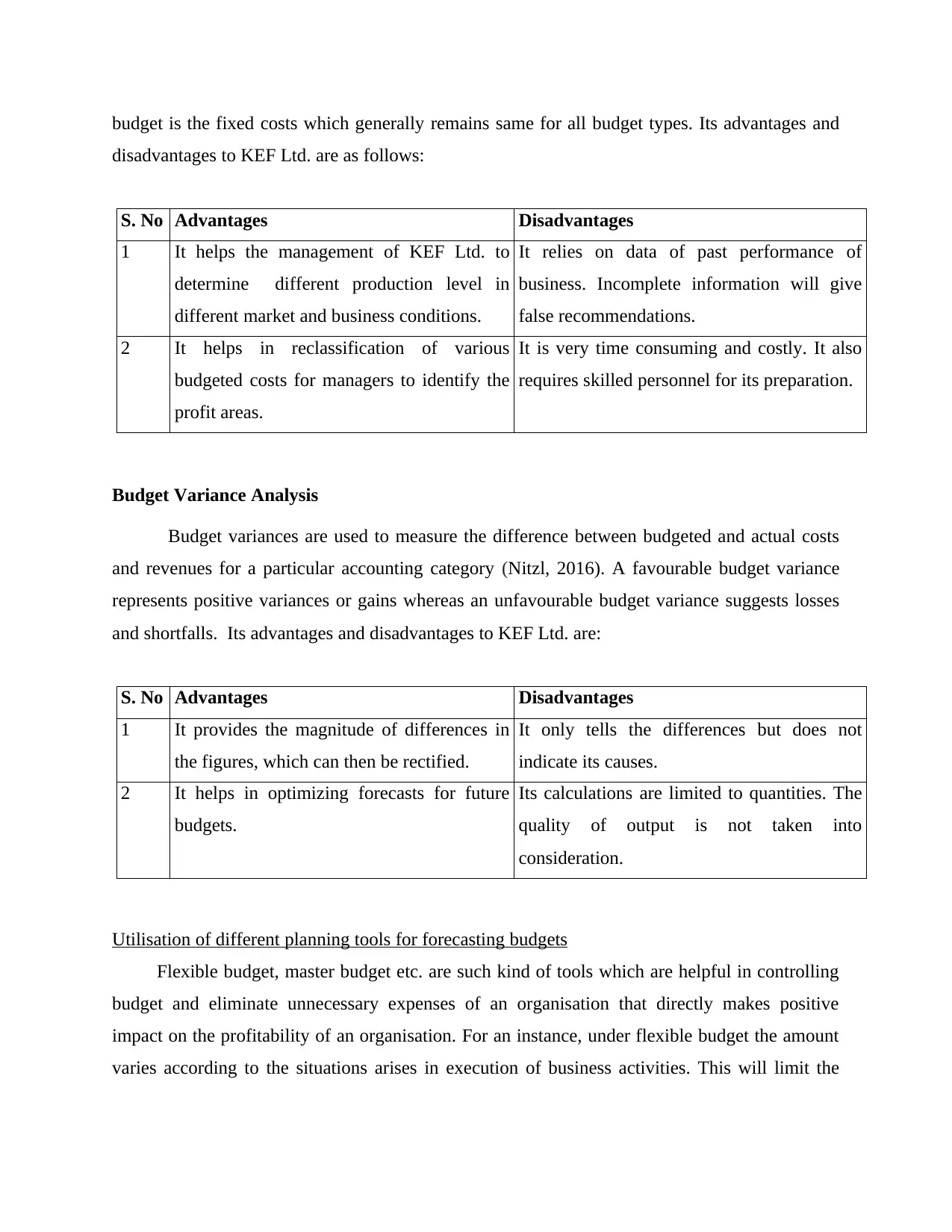

The flexible budget is calculated on the actual output units. Budgeted amounts (i.e.,

selling prices or costs) are multiplied by actual units to determine what particular number will be

given to a level of output or sales (McVay, Kennedy and Fullerton, 2016). The calculation yields

the total variable costs involved in production of KEF Ltd. The second component of the flexible

budget is the fixed costs which generally remains same for all budget types. Its advantages and

disadvantages to KEF Ltd. are as follows:

S. No Advantages Disadvantages

1 It helps the management of KEF Ltd. to

determine different production level in

different market and business conditions.

It relies on data of past performance of

business. Incomplete information will give

false recommendations.

2 It helps in reclassification of various

budgeted costs for managers to identify the

profit areas.

It is very time consuming and costly. It also

requires skilled personnel for its preparation.

Budget Variance Analysis

Budget variances are used to measure the difference between budgeted and actual costs

and revenues for a particular accounting category (Nitzl, 2016). A favourable budget variance

represents positive variances or gains whereas an unfavourable budget variance suggests losses

and shortfalls. Its advantages and disadvantages to KEF Ltd. are:

S. No Advantages Disadvantages

1 It provides the magnitude of differences in

the figures, which can then be rectified.

It only tells the differences but does not

indicate its causes.

2 It helps in optimizing forecasts for future

budgets.

Its calculations are limited to quantities. The

quality of output is not taken into

consideration.

Utilisation of different planning tools for forecasting budgets

Flexible budget, master budget etc. are such kind of tools which are helpful in controlling

budget and eliminate unnecessary expenses of an organisation that directly makes positive

impact on the profitability of an organisation. For an instance, under flexible budget the amount

varies according to the situations arises in execution of business activities. This will limit the

disadvantages to KEF Ltd. are as follows:

S. No Advantages Disadvantages

1 It helps the management of KEF Ltd. to

determine different production level in

different market and business conditions.

It relies on data of past performance of

business. Incomplete information will give

false recommendations.

2 It helps in reclassification of various

budgeted costs for managers to identify the

profit areas.

It is very time consuming and costly. It also

requires skilled personnel for its preparation.

Budget Variance Analysis

Budget variances are used to measure the difference between budgeted and actual costs

and revenues for a particular accounting category (Nitzl, 2016). A favourable budget variance

represents positive variances or gains whereas an unfavourable budget variance suggests losses

and shortfalls. Its advantages and disadvantages to KEF Ltd. are:

S. No Advantages Disadvantages

1 It provides the magnitude of differences in

the figures, which can then be rectified.

It only tells the differences but does not

indicate its causes.

2 It helps in optimizing forecasts for future

budgets.

Its calculations are limited to quantities. The

quality of output is not taken into

consideration.

Utilisation of different planning tools for forecasting budgets

Flexible budget, master budget etc. are such kind of tools which are helpful in controlling

budget and eliminate unnecessary expenses of an organisation that directly makes positive

impact on the profitability of an organisation. For an instance, under flexible budget the amount

varies according to the situations arises in execution of business activities. This will limit the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

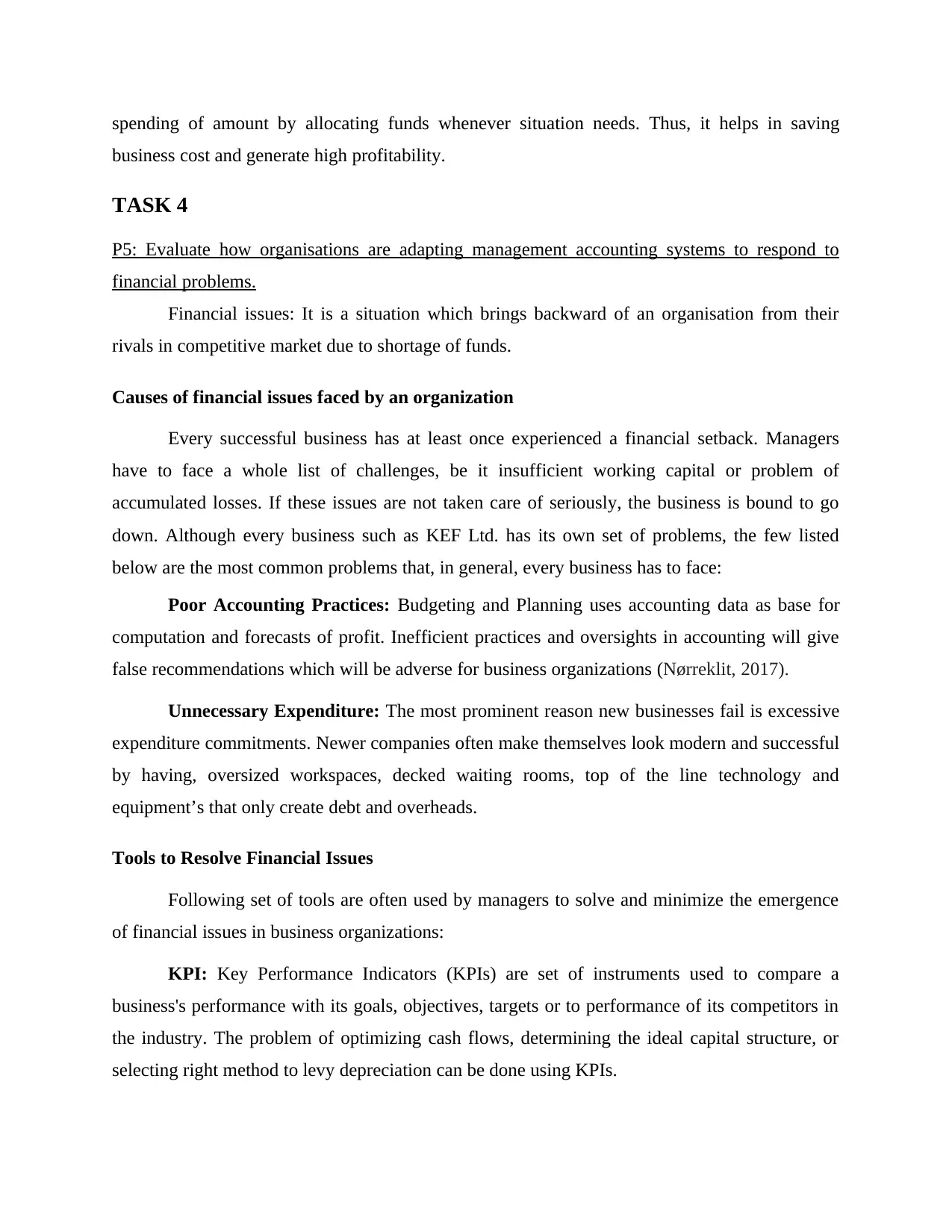

spending of amount by allocating funds whenever situation needs. Thus, it helps in saving

business cost and generate high profitability.

TASK 4

P5: Evaluate how organisations are adapting management accounting systems to respond to

financial problems.

Financial issues: It is a situation which brings backward of an organisation from their

rivals in competitive market due to shortage of funds.

Causes of financial issues faced by an organization

Every successful business has at least once experienced a financial setback. Managers

have to face a whole list of challenges, be it insufficient working capital or problem of

accumulated losses. If these issues are not taken care of seriously, the business is bound to go

down. Although every business such as KEF Ltd. has its own set of problems, the few listed

below are the most common problems that, in general, every business has to face:

Poor Accounting Practices: Budgeting and Planning uses accounting data as base for

computation and forecasts of profit. Inefficient practices and oversights in accounting will give

false recommendations which will be adverse for business organizations (Nørreklit, 2017).

Unnecessary Expenditure: The most prominent reason new businesses fail is excessive

expenditure commitments. Newer companies often make themselves look modern and successful

by having, oversized workspaces, decked waiting rooms, top of the line technology and

equipment’s that only create debt and overheads.

Tools to Resolve Financial Issues

Following set of tools are often used by managers to solve and minimize the emergence

of financial issues in business organizations:

KPI: Key Performance Indicators (KPIs) are set of instruments used to compare a

business's performance with its goals, objectives, targets or to performance of its competitors in

the industry. The problem of optimizing cash flows, determining the ideal capital structure, or

selecting right method to levy depreciation can be done using KPIs.

business cost and generate high profitability.

TASK 4

P5: Evaluate how organisations are adapting management accounting systems to respond to

financial problems.

Financial issues: It is a situation which brings backward of an organisation from their

rivals in competitive market due to shortage of funds.

Causes of financial issues faced by an organization

Every successful business has at least once experienced a financial setback. Managers

have to face a whole list of challenges, be it insufficient working capital or problem of

accumulated losses. If these issues are not taken care of seriously, the business is bound to go

down. Although every business such as KEF Ltd. has its own set of problems, the few listed

below are the most common problems that, in general, every business has to face:

Poor Accounting Practices: Budgeting and Planning uses accounting data as base for

computation and forecasts of profit. Inefficient practices and oversights in accounting will give

false recommendations which will be adverse for business organizations (Nørreklit, 2017).

Unnecessary Expenditure: The most prominent reason new businesses fail is excessive

expenditure commitments. Newer companies often make themselves look modern and successful

by having, oversized workspaces, decked waiting rooms, top of the line technology and

equipment’s that only create debt and overheads.

Tools to Resolve Financial Issues

Following set of tools are often used by managers to solve and minimize the emergence

of financial issues in business organizations:

KPI: Key Performance Indicators (KPIs) are set of instruments used to compare a

business's performance with its goals, objectives, targets or to performance of its competitors in

the industry. The problem of optimizing cash flows, determining the ideal capital structure, or

selecting right method to levy depreciation can be done using KPIs.

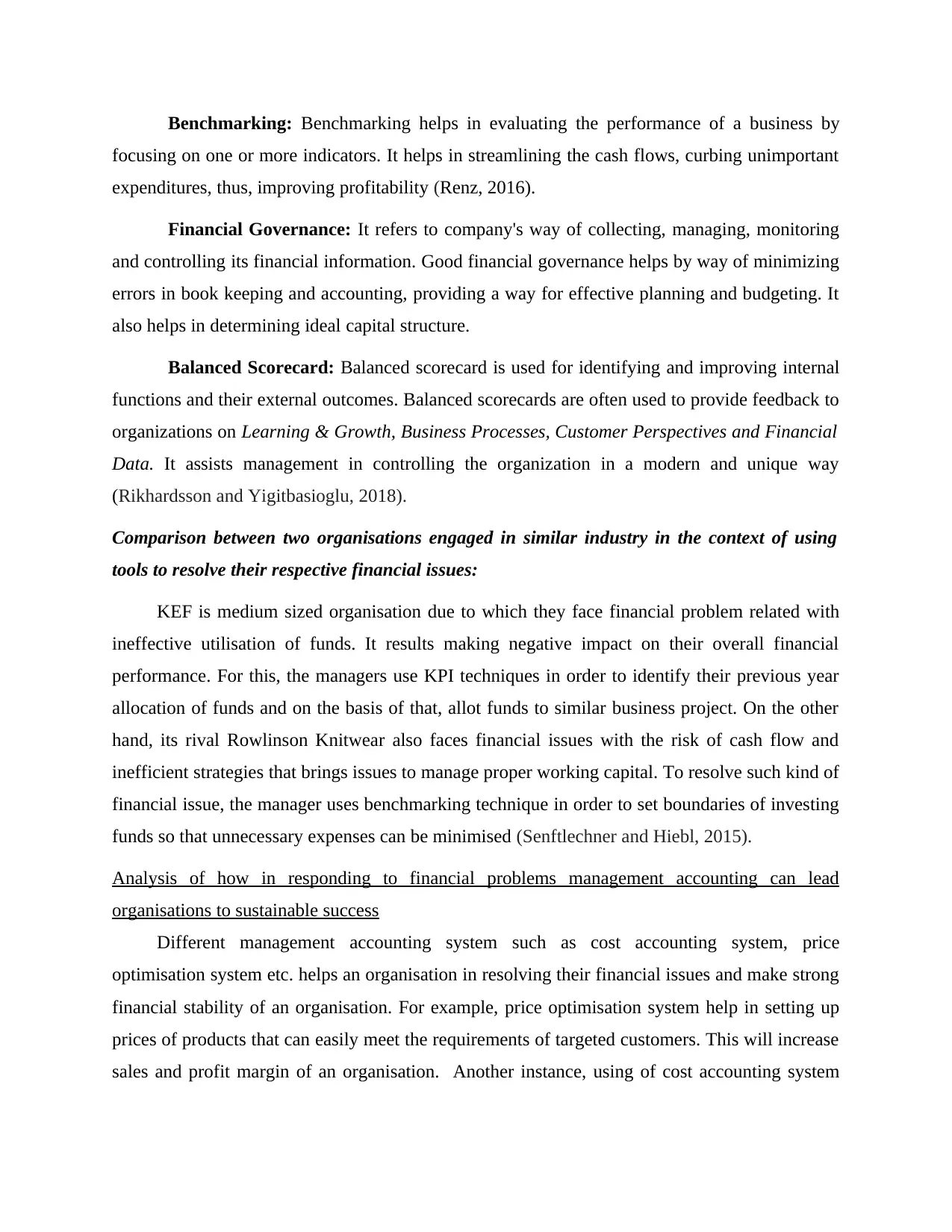

Benchmarking: Benchmarking helps in evaluating the performance of a business by

focusing on one or more indicators. It helps in streamlining the cash flows, curbing unimportant

expenditures, thus, improving profitability (Renz, 2016).

Financial Governance: It refers to company's way of collecting, managing, monitoring

and controlling its financial information. Good financial governance helps by way of minimizing

errors in book keeping and accounting, providing a way for effective planning and budgeting. It

also helps in determining ideal capital structure.

Balanced Scorecard: Balanced scorecard is used for identifying and improving internal

functions and their external outcomes. Balanced scorecards are often used to provide feedback to

organizations on Learning & Growth, Business Processes, Customer Perspectives and Financial

Data. It assists management in controlling the organization in a modern and unique way

(Rikhardsson and Yigitbasioglu, 2018).

Comparison between two organisations engaged in similar industry in the context of using

tools to resolve their respective financial issues:

KEF is medium sized organisation due to which they face financial problem related with

ineffective utilisation of funds. It results making negative impact on their overall financial

performance. For this, the managers use KPI techniques in order to identify their previous year

allocation of funds and on the basis of that, allot funds to similar business project. On the other

hand, its rival Rowlinson Knitwear also faces financial issues with the risk of cash flow and

inefficient strategies that brings issues to manage proper working capital. To resolve such kind of

financial issue, the manager uses benchmarking technique in order to set boundaries of investing

funds so that unnecessary expenses can be minimised (Senftlechner and Hiebl, 2015).

Analysis of how in responding to financial problems management accounting can lead

organisations to sustainable success

Different management accounting system such as cost accounting system, price

optimisation system etc. helps an organisation in resolving their financial issues and make strong

financial stability of an organisation. For example, price optimisation system help in setting up

prices of products that can easily meet the requirements of targeted customers. This will increase

sales and profit margin of an organisation. Another instance, using of cost accounting system

focusing on one or more indicators. It helps in streamlining the cash flows, curbing unimportant

expenditures, thus, improving profitability (Renz, 2016).

Financial Governance: It refers to company's way of collecting, managing, monitoring

and controlling its financial information. Good financial governance helps by way of minimizing

errors in book keeping and accounting, providing a way for effective planning and budgeting. It

also helps in determining ideal capital structure.

Balanced Scorecard: Balanced scorecard is used for identifying and improving internal

functions and their external outcomes. Balanced scorecards are often used to provide feedback to

organizations on Learning & Growth, Business Processes, Customer Perspectives and Financial

Data. It assists management in controlling the organization in a modern and unique way

(Rikhardsson and Yigitbasioglu, 2018).

Comparison between two organisations engaged in similar industry in the context of using

tools to resolve their respective financial issues:

KEF is medium sized organisation due to which they face financial problem related with

ineffective utilisation of funds. It results making negative impact on their overall financial

performance. For this, the managers use KPI techniques in order to identify their previous year

allocation of funds and on the basis of that, allot funds to similar business project. On the other

hand, its rival Rowlinson Knitwear also faces financial issues with the risk of cash flow and

inefficient strategies that brings issues to manage proper working capital. To resolve such kind of

financial issue, the manager uses benchmarking technique in order to set boundaries of investing

funds so that unnecessary expenses can be minimised (Senftlechner and Hiebl, 2015).

Analysis of how in responding to financial problems management accounting can lead

organisations to sustainable success

Different management accounting system such as cost accounting system, price

optimisation system etc. helps an organisation in resolving their financial issues and make strong

financial stability of an organisation. For example, price optimisation system help in setting up

prices of products that can easily meet the requirements of targeted customers. This will increase

sales and profit margin of an organisation. Another instance, using of cost accounting system

help in analysing the total cost of production which helps manager in minimising the

unnecessary expenses.

Various planning tools to resolve financial problems

KPI and benchmarking are two techniques which improves the performance level of

employees which makes positive impact on the sustainability of an organisation. For example,

KPI analyse the performance level of employees by comparing actual with desired performance.

It makes easy for managers to make further actions for future improvements. On the other hand,

benchmarking is another effective tool which is used to set target regarding investment of funds

and restrict managers to spend economically.

CONCLUSION

It has been concluded from the above discussion that understanding of management

accounting concept is important due to receiving maximum support towards organisational goals

and objectives. The manager is responsible to take decision for the betterment of an organisation

using taking support from various final records such as profit and loss account, balance sheet etc.

Various costing techniques are available to adopt for an organisation among which best method

will be adopt according to their objectives and market position.

unnecessary expenses.

Various planning tools to resolve financial problems

KPI and benchmarking are two techniques which improves the performance level of

employees which makes positive impact on the sustainability of an organisation. For example,

KPI analyse the performance level of employees by comparing actual with desired performance.

It makes easy for managers to make further actions for future improvements. On the other hand,

benchmarking is another effective tool which is used to set target regarding investment of funds

and restrict managers to spend economically.

CONCLUSION

It has been concluded from the above discussion that understanding of management

accounting concept is important due to receiving maximum support towards organisational goals

and objectives. The manager is responsible to take decision for the betterment of an organisation

using taking support from various final records such as profit and loss account, balance sheet etc.

Various costing techniques are available to adopt for an organisation among which best method

will be adopt according to their objectives and market position.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Bartlett, G. D. and et.al, 2016. Factors influencing recruitment of non-accounting business

professionals into internal auditing. Behavioral Research in Accounting. 29(1). pp.119-

130.

Bromwich, M. and Scapens, R. W., 2016. Management accounting research: 25 years on.

Management Accounting Research. 31. pp.1-9.

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Englund, H. and Gerdin, J., 2014. Structuration theory in accounting research: Applications and

applicability. Critical Perspectives on Accounting. 25(2). pp.162-180.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7-8). pp.414-428.

Honggowati, S. and et.al., 2017. Corporate governance and strategic management accounting

disclosure. Indonesian Journal of Sustainability Accounting and Management. 1(1).

pp.23-30.

Lindholm, A., Laine, T. J. and Suomala, P., 2017. The potential of management accounting and

control in global operations: Profitability-driven service business development. Journal

of Service Theory and Practice. 27(2). pp.496-514.

Lindholm, A., Laine, T. J. and Suomala, P., 2017. The potential of management accounting and

control in global operations: Profitability-driven service business development. Journal

of Service Theory and Practice. 27(2). pp.496-514.

McVay, G., Kennedy, F. and Fullerton, R., 2016. Accounting in the lean enterprise: providing

simple, practical, and decision-relevant information. Productivity Press.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature. 37. pp.19-35.

Nørreklit, H. ed., 2017. A philosophy of management accounting: A pragmatic constructivist

approach. Taylor & Francis.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Books and Journals

Bartlett, G. D. and et.al, 2016. Factors influencing recruitment of non-accounting business

professionals into internal auditing. Behavioral Research in Accounting. 29(1). pp.119-

130.

Bromwich, M. and Scapens, R. W., 2016. Management accounting research: 25 years on.

Management Accounting Research. 31. pp.1-9.

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Englund, H. and Gerdin, J., 2014. Structuration theory in accounting research: Applications and

applicability. Critical Perspectives on Accounting. 25(2). pp.162-180.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7-8). pp.414-428.

Honggowati, S. and et.al., 2017. Corporate governance and strategic management accounting

disclosure. Indonesian Journal of Sustainability Accounting and Management. 1(1).

pp.23-30.

Lindholm, A., Laine, T. J. and Suomala, P., 2017. The potential of management accounting and

control in global operations: Profitability-driven service business development. Journal

of Service Theory and Practice. 27(2). pp.496-514.

Lindholm, A., Laine, T. J. and Suomala, P., 2017. The potential of management accounting and

control in global operations: Profitability-driven service business development. Journal

of Service Theory and Practice. 27(2). pp.496-514.

McVay, G., Kennedy, F. and Fullerton, R., 2016. Accounting in the lean enterprise: providing

simple, practical, and decision-relevant information. Productivity Press.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature. 37. pp.19-35.

Nørreklit, H. ed., 2017. A philosophy of management accounting: A pragmatic constructivist

approach. Taylor & Francis.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Senftlechner, D. and Hiebl, M. R., 2015. Management accounting and management control in

family businesses: Past accomplishments and future opportunities. Journal of

Accounting & Organizational Change. 11(4). pp.573-606.

Shipman, J. E., Swanquist, Q. T. and Whited, R. L., 2016. Propensity score matching in

accounting research. The Accounting Review. 92(1). pp.213-244.

Tucker, B. P. and Lowe, A. D., 2014. Practitioners are from Mars; academics are from Venus?

An investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal. 27(3). pp.394-425.

Online

Budget. 2019. [Online]. Available through:

<https://www.mymoneycoach.ca/budgeting/what-is-a-budget-planning-forecasting>

family businesses: Past accomplishments and future opportunities. Journal of

Accounting & Organizational Change. 11(4). pp.573-606.

Shipman, J. E., Swanquist, Q. T. and Whited, R. L., 2016. Propensity score matching in

accounting research. The Accounting Review. 92(1). pp.213-244.

Tucker, B. P. and Lowe, A. D., 2014. Practitioners are from Mars; academics are from Venus?

An investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal. 27(3). pp.394-425.

Online

Budget. 2019. [Online]. Available through:

<https://www.mymoneycoach.ca/budgeting/what-is-a-budget-planning-forecasting>

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.