Comparative Issues in Government Accounting

VerifiedAdded on 2020/10/23

|14

|4034

|309

AI Summary

The assignment provides a detailed analysis of comparative issues in local government accounting. It discusses the importance of strategic management accounting techniques in enhancing business communication processes and determining progress. The document also explores the role of enterprise risk management in addressing challenges faced by local governments. Additionally, it examines the significance of sustainability accounting and accountability in local government settings. The assignment is based on a review of relevant literature from various books and journals, including 'Comparative Issues in Local Government Accounting' and 'Strategic Management'. It provides a comprehensive overview of key concepts and techniques related to management accounting and performance measurement.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

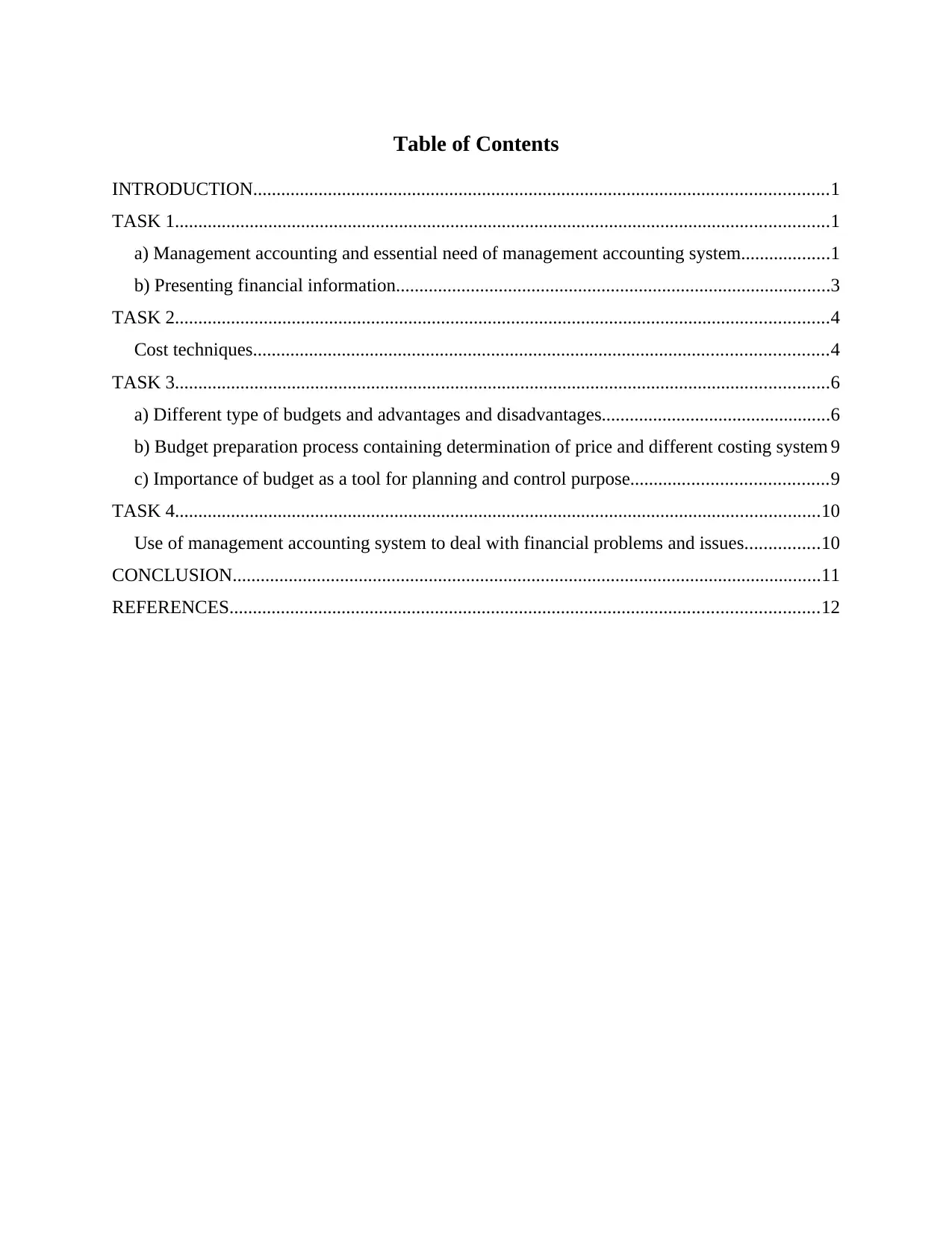

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Management accounting and essential need of management accounting system...................1

b) Presenting financial information.............................................................................................3

TASK 2............................................................................................................................................4

Cost techniques...........................................................................................................................4

TASK 3............................................................................................................................................6

a) Different type of budgets and advantages and disadvantages.................................................6

b) Budget preparation process containing determination of price and different costing system 9

c) Importance of budget as a tool for planning and control purpose..........................................9

TASK 4..........................................................................................................................................10

Use of management accounting system to deal with financial problems and issues................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Management accounting and essential need of management accounting system...................1

b) Presenting financial information.............................................................................................3

TASK 2............................................................................................................................................4

Cost techniques...........................................................................................................................4

TASK 3............................................................................................................................................6

a) Different type of budgets and advantages and disadvantages.................................................6

b) Budget preparation process containing determination of price and different costing system 9

c) Importance of budget as a tool for planning and control purpose..........................................9

TASK 4..........................................................................................................................................10

Use of management accounting system to deal with financial problems and issues................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is a concept which is considered important in organisational

concept subject to ordinate and manage the departments and operations of organisation. It is

utilized by supervisors for taking direction from the arrangements of data to get bolster while

taking choices for an association. By and large, it is a calling that includes association in

administration's division arranging, execution administration and basic leadership frameworks. It

likewise gives skill in the money related answering to help administration in usage of

authoritative techniques.

In this report, wage of Tech (UK) constrained which produces exceptional charger will be

distinguished on peripheral and retention costing techniques. There are four assignments

examined in this report out of which in Errand 1, a report is composed to Executive of Fund to

clarify the elements of Administration Bookkeeping Frameworks. There are 3 comprises of

count of minimal and ingestion costing to discover salary of an organization. Last errand

comprises of adjusted score card of organization. The fundamental goal of this report is to clarify

learning results of Administration Bookkeeping Reports and Planning Frameworks (Anandarajan

and Srinivasan, 2012).

TASK 1

a) Management accounting and essential need of management accounting system

1. Distinguish management accounting from financial accounting

Basis Financial Accounting Management Accounting

External

Review

Evaluators and Controllers survey this

report every year to check its precision.

Nobody survey these administration

bookkeeping reports.

Focus It is for the most part reliant and

concentrated on the past exchanges.

Its fundamental spotlight is on data

to get bolster in basic leadership.

Frequency It is required Quarterly, Month to

month and Yearly.

It is set aside a few minutes of its

prerequisite by Supervisors and

leaders.

Primary

Audience

All the outside partners like banks,

investors, budgetary foundations and

Its fundamental group of onlookers is

just inward workers like best

1

Management accounting is a concept which is considered important in organisational

concept subject to ordinate and manage the departments and operations of organisation. It is

utilized by supervisors for taking direction from the arrangements of data to get bolster while

taking choices for an association. By and large, it is a calling that includes association in

administration's division arranging, execution administration and basic leadership frameworks. It

likewise gives skill in the money related answering to help administration in usage of

authoritative techniques.

In this report, wage of Tech (UK) constrained which produces exceptional charger will be

distinguished on peripheral and retention costing techniques. There are four assignments

examined in this report out of which in Errand 1, a report is composed to Executive of Fund to

clarify the elements of Administration Bookkeeping Frameworks. There are 3 comprises of

count of minimal and ingestion costing to discover salary of an organization. Last errand

comprises of adjusted score card of organization. The fundamental goal of this report is to clarify

learning results of Administration Bookkeeping Reports and Planning Frameworks (Anandarajan

and Srinivasan, 2012).

TASK 1

a) Management accounting and essential need of management accounting system

1. Distinguish management accounting from financial accounting

Basis Financial Accounting Management Accounting

External

Review

Evaluators and Controllers survey this

report every year to check its precision.

Nobody survey these administration

bookkeeping reports.

Focus It is for the most part reliant and

concentrated on the past exchanges.

Its fundamental spotlight is on data

to get bolster in basic leadership.

Frequency It is required Quarterly, Month to

month and Yearly.

It is set aside a few minutes of its

prerequisite by Supervisors and

leaders.

Primary

Audience

All the outside partners like banks,

investors, budgetary foundations and

Its fundamental group of onlookers is

just inward workers like best

1

financial specialists are its essential

group of onlookers.

administration, line directors and

bookkeeping divisions.

Purpose Its primary intention is to educate

business concerning finance related

position of the organization.

Its fundamental target is to offer help

to top administration of an

organization in basic leadership

process.

Regulations IFRS, GAAP and IAS It doesn't take after any directions

Scope Its extension is wide as it is helpful for

different organizations in that specific

industry.

Its degree is restricted as its

utilization is constrained to item

portion as it were.

Uses It is required for each organization's

which are associated with finance

sector.

It is discretionary as it is just required

or utilized at the season of

composing an answer to the

administration.

2. Management accounting information as a decision making tool

Utilizing the Data: A portion of the cases of these apparatuses are planning, monetary

explanation projections and adjusted scorecards. This device enables administration on settling

on choices on the most proficient method to develop their electric business.

Relevant Cost Analysis: These instruments likewise help administration in choosing

whether to include product offerings or stop activities. Administrative Bookkeeping Data is used

by administration of an organisation to settle on choices on what ought to be sold and how to

offer it.

Make or Buy Analysis: It examinations different expenses of making and purchasing an

item and picks that choice which comprises of less expenses (Bebbington, Unerman and

O'Dwyer, 2014). This instrument helps organization in deciding if to purchase or make an item

or not.

Activity-based Costing Techniques: This apparatus additionally underpins organization

in choosing the exercises required to deliver a specific product offering. This instrument of

Administration Bookkeeping Data enables chiefs in settling on choices to distinguish to whom to

organization should offer the items.

2

group of onlookers.

administration, line directors and

bookkeeping divisions.

Purpose Its primary intention is to educate

business concerning finance related

position of the organization.

Its fundamental target is to offer help

to top administration of an

organization in basic leadership

process.

Regulations IFRS, GAAP and IAS It doesn't take after any directions

Scope Its extension is wide as it is helpful for

different organizations in that specific

industry.

Its degree is restricted as its

utilization is constrained to item

portion as it were.

Uses It is required for each organization's

which are associated with finance

sector.

It is discretionary as it is just required

or utilized at the season of

composing an answer to the

administration.

2. Management accounting information as a decision making tool

Utilizing the Data: A portion of the cases of these apparatuses are planning, monetary

explanation projections and adjusted scorecards. This device enables administration on settling

on choices on the most proficient method to develop their electric business.

Relevant Cost Analysis: These instruments likewise help administration in choosing

whether to include product offerings or stop activities. Administrative Bookkeeping Data is used

by administration of an organisation to settle on choices on what ought to be sold and how to

offer it.

Make or Buy Analysis: It examinations different expenses of making and purchasing an

item and picks that choice which comprises of less expenses (Bebbington, Unerman and

O'Dwyer, 2014). This instrument helps organization in deciding if to purchase or make an item

or not.

Activity-based Costing Techniques: This apparatus additionally underpins organization

in choosing the exercises required to deliver a specific product offering. This instrument of

Administration Bookkeeping Data enables chiefs in settling on choices to distinguish to whom to

organization should offer the items.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

3. Cost accounting system

Actual: It designates these expenses by utilizing real amount of distribution base. This

costing framework is the account of item costs which depends on real expenses of work,

materials, overhead and plant.

Normal: It generally recognizes foreordained assembling overhead rate in light of

evaluated costs. This costing is utilized for the valuation of made items like material, coordinate

work and assembling overhead expenses.

Standard costing: It is essentially used to esteem the cost of products sold and

inventories. This cost bookkeeping framework write works like typical cost bookkeeping yet the

fundamental contrast is that it predetermines material, coordinate work and assembling overhead

costs in view of the past data.

4. Inventory management system: this is one of the important accounting system which

helps to manage the inventory levels and flow of stock with in organisational context. A

stock administration framework includes the utilization of work area programming,

standardized tag scanners, scanner tag printers and cell phones keeping in mind the end

goal to oversee stock administration like stock, merchandise, consumables, supplies, and

so forth. There are type of inventory methods are used to manage and control the

minimum level of stock, raw material requirement and units to be produced for required

output.

5. Job costing: This costing framework is utilized as a part of request to indicate the

assembling costs for bunches of individual items or items, for the most part the cost

arrangement of the activity arrange is utilized just when the fabricated items are very not

the same as each other.

b) Presenting financial information

1. Type of management accounting reports

There are different administrative bookkeeping reports which are talked about as follows:

Records Receivable Maturing Report: It is utilized as a measure to decide money

related state of the clients of an organization. Capable maturing is an intermittent report that gets

an organization's record every once in a while which is a receipt extraordinary.

Job Costs Reports: They have been colonized by sellers to help the cost of an

occupation for bookkeeping framework. It is not quite the same as the quantity of employments

3

Actual: It designates these expenses by utilizing real amount of distribution base. This

costing framework is the account of item costs which depends on real expenses of work,

materials, overhead and plant.

Normal: It generally recognizes foreordained assembling overhead rate in light of

evaluated costs. This costing is utilized for the valuation of made items like material, coordinate

work and assembling overhead expenses.

Standard costing: It is essentially used to esteem the cost of products sold and

inventories. This cost bookkeeping framework write works like typical cost bookkeeping yet the

fundamental contrast is that it predetermines material, coordinate work and assembling overhead

costs in view of the past data.

4. Inventory management system: this is one of the important accounting system which

helps to manage the inventory levels and flow of stock with in organisational context. A

stock administration framework includes the utilization of work area programming,

standardized tag scanners, scanner tag printers and cell phones keeping in mind the end

goal to oversee stock administration like stock, merchandise, consumables, supplies, and

so forth. There are type of inventory methods are used to manage and control the

minimum level of stock, raw material requirement and units to be produced for required

output.

5. Job costing: This costing framework is utilized as a part of request to indicate the

assembling costs for bunches of individual items or items, for the most part the cost

arrangement of the activity arrange is utilized just when the fabricated items are very not

the same as each other.

b) Presenting financial information

1. Type of management accounting reports

There are different administrative bookkeeping reports which are talked about as follows:

Records Receivable Maturing Report: It is utilized as a measure to decide money

related state of the clients of an organization. Capable maturing is an intermittent report that gets

an organization's record every once in a while which is a receipt extraordinary.

Job Costs Reports: They have been colonized by sellers to help the cost of an

occupation for bookkeeping framework. It is not quite the same as the quantity of employments

3

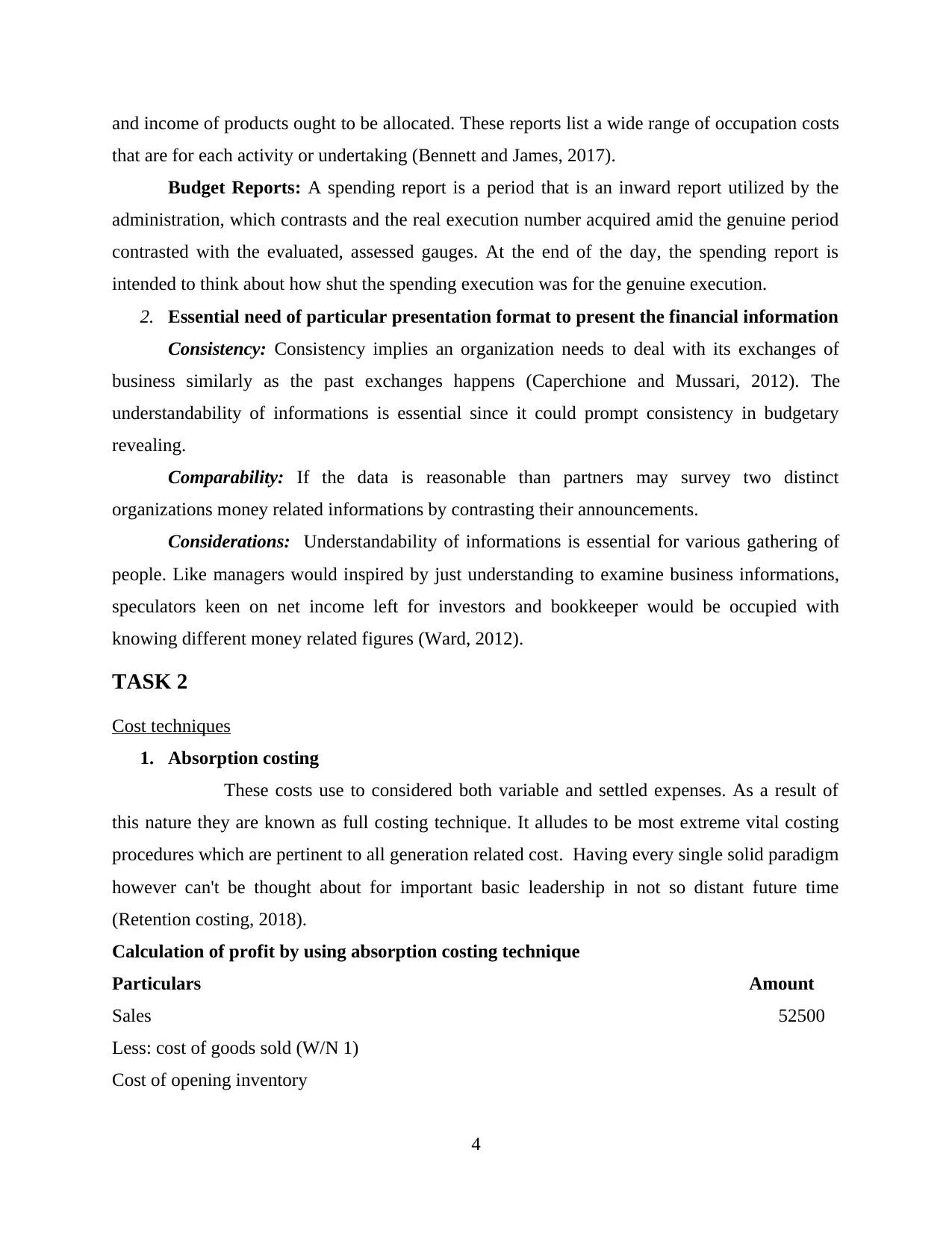

and income of products ought to be allocated. These reports list a wide range of occupation costs

that are for each activity or undertaking (Bennett and James, 2017).

Budget Reports: A spending report is a period that is an inward report utilized by the

administration, which contrasts and the real execution number acquired amid the genuine period

contrasted with the evaluated, assessed gauges. At the end of the day, the spending report is

intended to think about how shut the spending execution was for the genuine execution.

2. Essential need of particular presentation format to present the financial information

Consistency: Consistency implies an organization needs to deal with its exchanges of

business similarly as the past exchanges happens (Caperchione and Mussari, 2012). The

understandability of informations is essential since it could prompt consistency in budgetary

revealing.

Comparability: If the data is reasonable than partners may survey two distinct

organizations money related informations by contrasting their announcements.

Considerations: Understandability of informations is essential for various gathering of

people. Like managers would inspired by just understanding to examine business informations,

speculators keen on net income left for investors and bookkeeper would be occupied with

knowing different money related figures (Ward, 2012).

TASK 2

Cost techniques

1. Absorption costing

These costs use to considered both variable and settled expenses. As a result of

this nature they are known as full costing technique. It alludes to be most extreme vital costing

procedures which are pertinent to all generation related cost. Having every single solid paradigm

however can't be thought about for important basic leadership in not so distant future time

(Retention costing, 2018).

Calculation of profit by using absorption costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

4

that are for each activity or undertaking (Bennett and James, 2017).

Budget Reports: A spending report is a period that is an inward report utilized by the

administration, which contrasts and the real execution number acquired amid the genuine period

contrasted with the evaluated, assessed gauges. At the end of the day, the spending report is

intended to think about how shut the spending execution was for the genuine execution.

2. Essential need of particular presentation format to present the financial information

Consistency: Consistency implies an organization needs to deal with its exchanges of

business similarly as the past exchanges happens (Caperchione and Mussari, 2012). The

understandability of informations is essential since it could prompt consistency in budgetary

revealing.

Comparability: If the data is reasonable than partners may survey two distinct

organizations money related informations by contrasting their announcements.

Considerations: Understandability of informations is essential for various gathering of

people. Like managers would inspired by just understanding to examine business informations,

speculators keen on net income left for investors and bookkeeper would be occupied with

knowing different money related figures (Ward, 2012).

TASK 2

Cost techniques

1. Absorption costing

These costs use to considered both variable and settled expenses. As a result of

this nature they are known as full costing technique. It alludes to be most extreme vital costing

procedures which are pertinent to all generation related cost. Having every single solid paradigm

however can't be thought about for important basic leadership in not so distant future time

(Retention costing, 2018).

Calculation of profit by using absorption costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

4

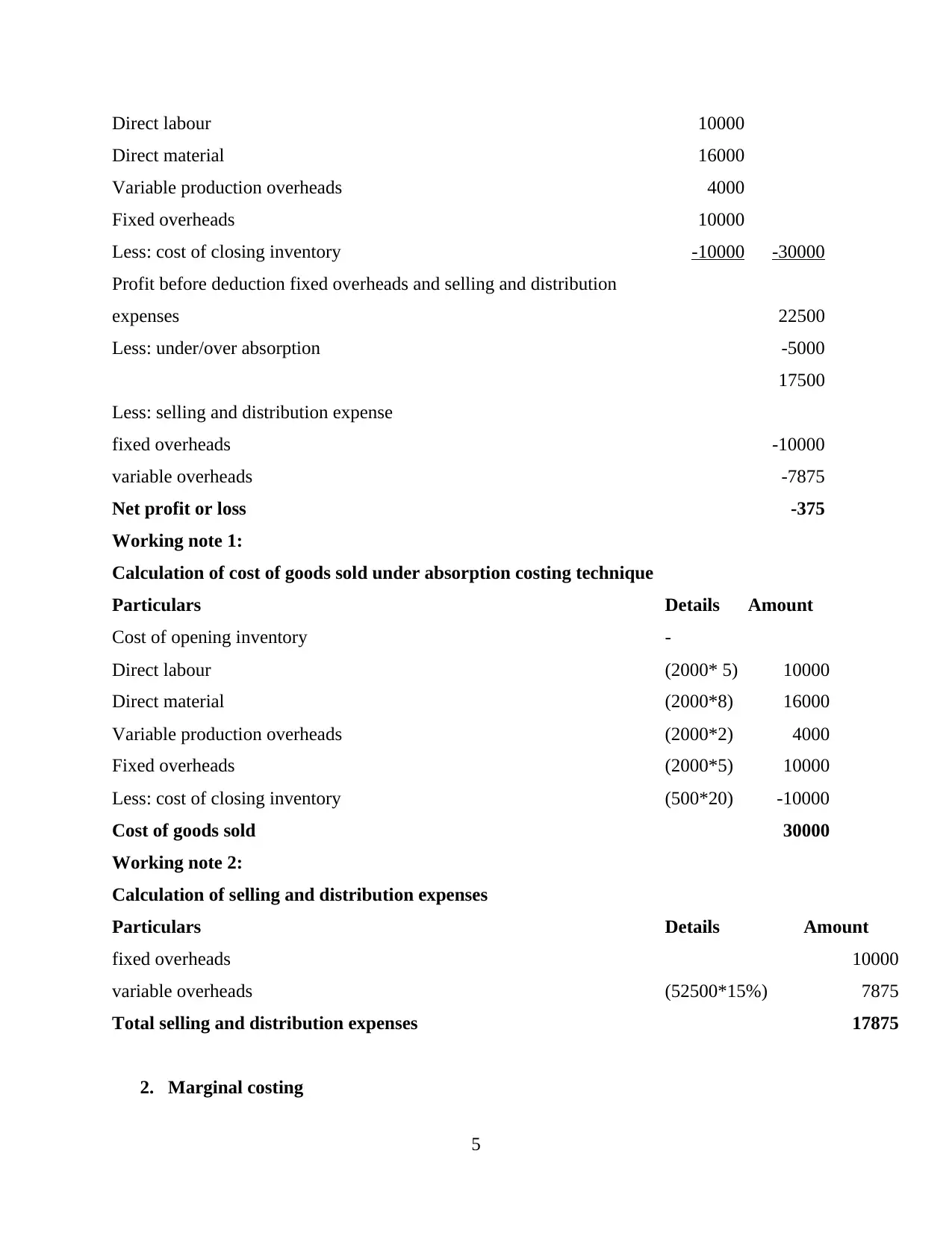

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling and distribution

expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

Working note 1:

Calculation of cost of goods sold under absorption costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Fixed overheads (2000*5) 10000

Less: cost of closing inventory (500*20) -10000

Cost of goods sold 30000

Working note 2:

Calculation of selling and distribution expenses

Particulars Details Amount

fixed overheads 10000

variable overheads (52500*15%) 7875

Total selling and distribution expenses 17875

2. Marginal costing

5

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling and distribution

expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

Working note 1:

Calculation of cost of goods sold under absorption costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Fixed overheads (2000*5) 10000

Less: cost of closing inventory (500*20) -10000

Cost of goods sold 30000

Working note 2:

Calculation of selling and distribution expenses

Particulars Details Amount

fixed overheads 10000

variable overheads (52500*15%) 7875

Total selling and distribution expenses 17875

2. Marginal costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

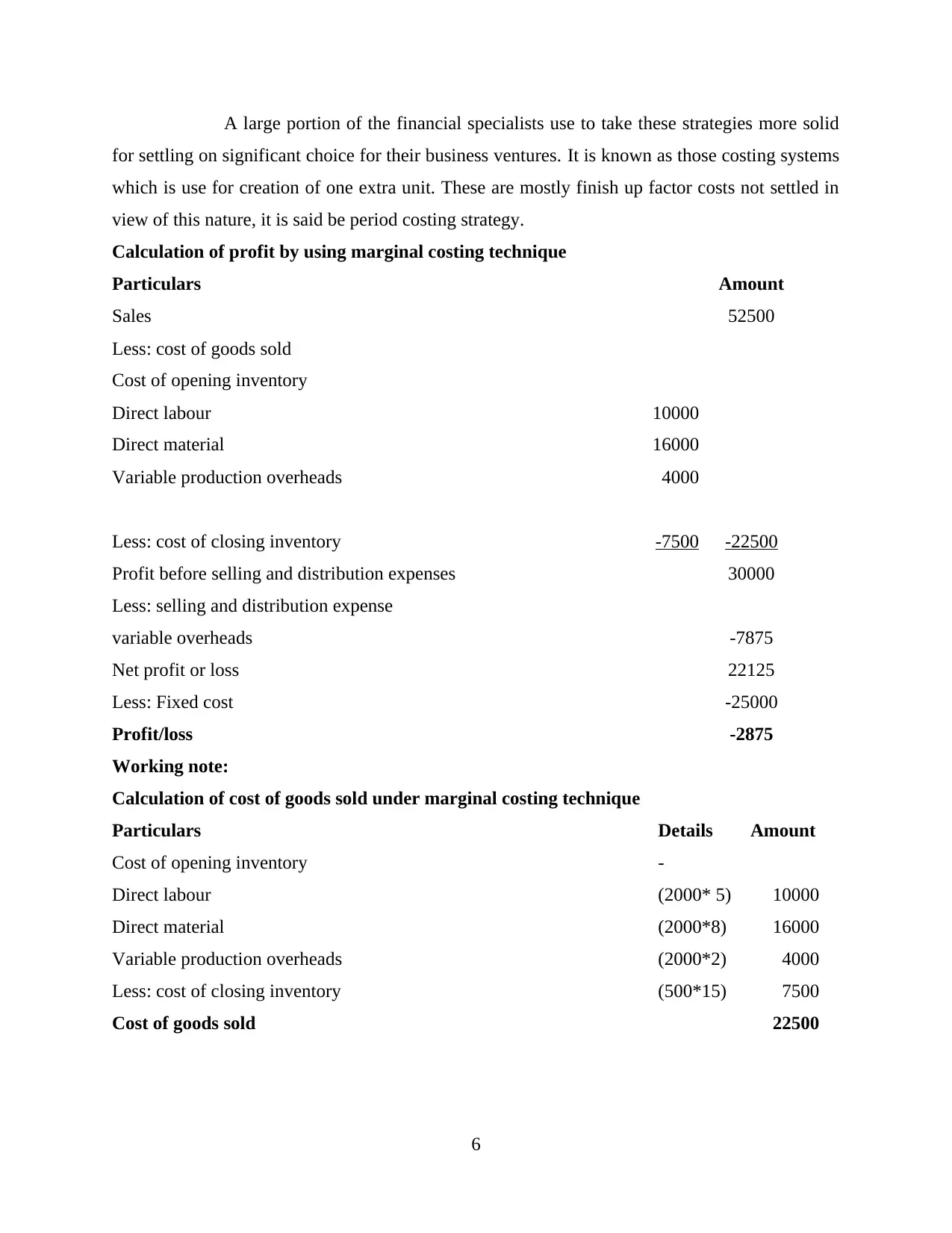

A large portion of the financial specialists use to take these strategies more solid

for settling on significant choice for their business ventures. It is known as those costing systems

which is use for creation of one extra unit. These are mostly finish up factor costs not settled in

view of this nature, it is said be period costing strategy.

Calculation of profit by using marginal costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Less: cost of closing inventory -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

Working note:

Calculation of cost of goods sold under marginal costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 22500

6

for settling on significant choice for their business ventures. It is known as those costing systems

which is use for creation of one extra unit. These are mostly finish up factor costs not settled in

view of this nature, it is said be period costing strategy.

Calculation of profit by using marginal costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Less: cost of closing inventory -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

Working note:

Calculation of cost of goods sold under marginal costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 22500

6

TASK 3

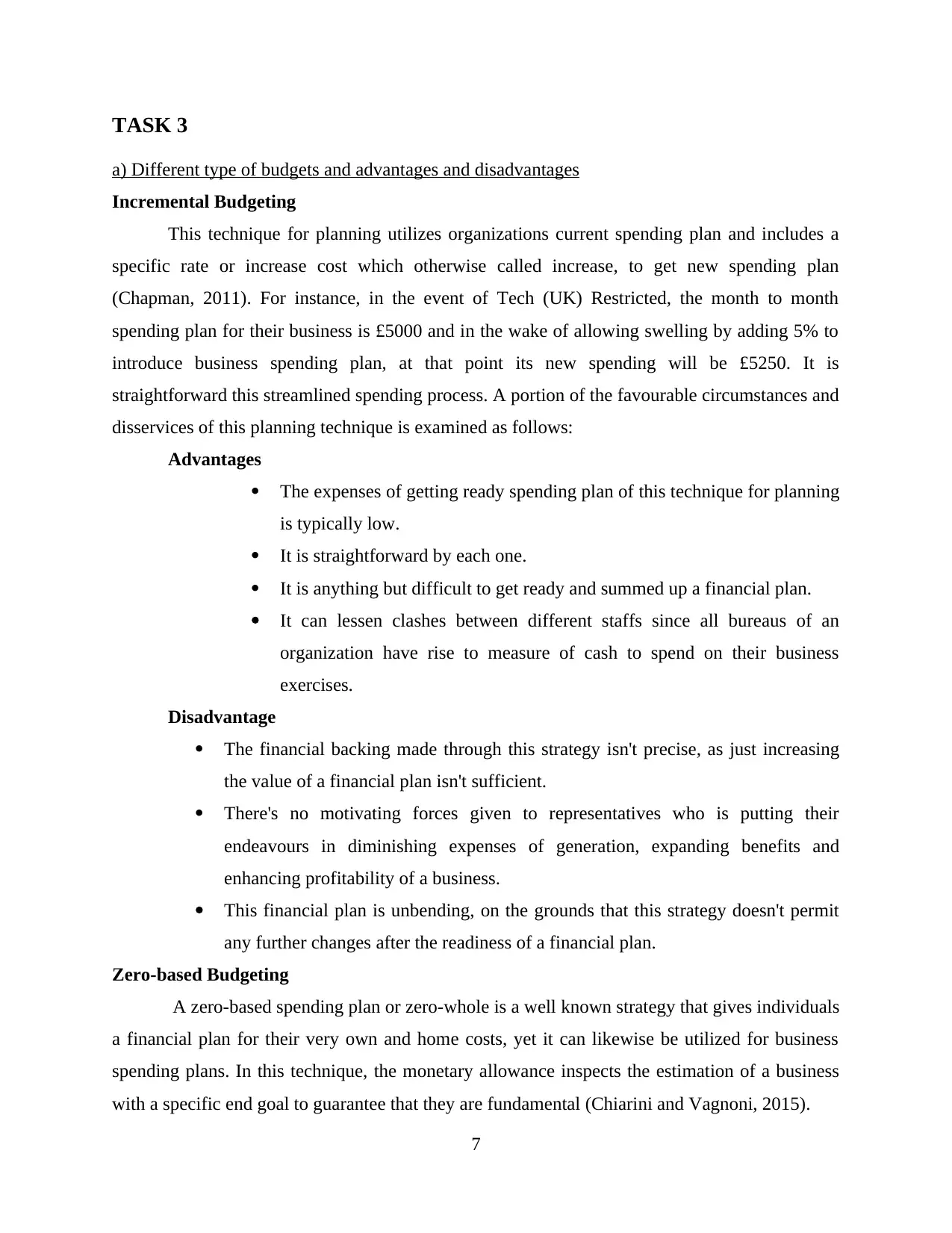

a) Different type of budgets and advantages and disadvantages

Incremental Budgeting

This technique for planning utilizes organizations current spending plan and includes a

specific rate or increase cost which otherwise called increase, to get new spending plan

(Chapman, 2011). For instance, in the event of Tech (UK) Restricted, the month to month

spending plan for their business is £5000 and in the wake of allowing swelling by adding 5% to

introduce business spending plan, at that point its new spending will be £5250. It is

straightforward this streamlined spending process. A portion of the favourable circumstances and

disservices of this planning technique is examined as follows:

Advantages

The expenses of getting ready spending plan of this technique for planning

is typically low.

It is straightforward by each one.

It is anything but difficult to get ready and summed up a financial plan.

It can lessen clashes between different staffs since all bureaus of an

organization have rise to measure of cash to spend on their business

exercises.

Disadvantage

The financial backing made through this strategy isn't precise, as just increasing

the value of a financial plan isn't sufficient.

There's no motivating forces given to representatives who is putting their

endeavours in diminishing expenses of generation, expanding benefits and

enhancing profitability of a business.

This financial plan is unbending, on the grounds that this strategy doesn't permit

any further changes after the readiness of a financial plan.

Zero-based Budgeting

A zero-based spending plan or zero-whole is a well known strategy that gives individuals

a financial plan for their very own and home costs, yet it can likewise be utilized for business

spending plans. In this technique, the monetary allowance inspects the estimation of a business

with a specific end goal to guarantee that they are fundamental (Chiarini and Vagnoni, 2015).

7

a) Different type of budgets and advantages and disadvantages

Incremental Budgeting

This technique for planning utilizes organizations current spending plan and includes a

specific rate or increase cost which otherwise called increase, to get new spending plan

(Chapman, 2011). For instance, in the event of Tech (UK) Restricted, the month to month

spending plan for their business is £5000 and in the wake of allowing swelling by adding 5% to

introduce business spending plan, at that point its new spending will be £5250. It is

straightforward this streamlined spending process. A portion of the favourable circumstances and

disservices of this planning technique is examined as follows:

Advantages

The expenses of getting ready spending plan of this technique for planning

is typically low.

It is straightforward by each one.

It is anything but difficult to get ready and summed up a financial plan.

It can lessen clashes between different staffs since all bureaus of an

organization have rise to measure of cash to spend on their business

exercises.

Disadvantage

The financial backing made through this strategy isn't precise, as just increasing

the value of a financial plan isn't sufficient.

There's no motivating forces given to representatives who is putting their

endeavours in diminishing expenses of generation, expanding benefits and

enhancing profitability of a business.

This financial plan is unbending, on the grounds that this strategy doesn't permit

any further changes after the readiness of a financial plan.

Zero-based Budgeting

A zero-based spending plan or zero-whole is a well known strategy that gives individuals

a financial plan for their very own and home costs, yet it can likewise be utilized for business

spending plans. In this technique, the monetary allowance inspects the estimation of a business

with a specific end goal to guarantee that they are fundamental (Chiarini and Vagnoni, 2015).

7

Zero-based spending plan is made in following three stages given as follows:

Stage 1: Exercises are controlled by supervisors. There exercises are later uses in basic

leadership process.

Stage 2: In this progression administration offers positions to every procedure all

together, this request later sort in sliding configurations of advantages.

Stage 3: Here in this last stage, reserves are allotted to various spending

recommendations in view of their needs.

Advantages

Asset and assets are productively dispensed.

It perceives inefficient exercises and later wipes out such exercises.

It helps supervisors in driving cost decrease techniques.

Disadvantage

It's anything but a simple technique, it contains complex advances and

expends heaps of labour and time (Chiarini, 2012).

It isn't reasonable for huge associations, as huge measure of informations

are there. Utilizing these informations may requires basic points of interest

of it.

Because of the circumstance of over spending plan, inside clashes between

various representatives may rises.

Workers and administrators requires fundamental preparing to actualize

such a financial plan.

Top Down Budgeting:

The fundamental favourable position of this technique is that, an administrator does not

have to believe others to give spending data and it can spare time. In any case, if administrators

are not all around engaged with the everyday organization's business, at that point they won't not

have all the data expected to utilize this spending strategy (Damodaran, 2012). This may bring

about the distribution of assets in a few regions and the assignment of assets in others.

Under this planning technique, the most abnormal amount of business is done inside the

business, individual can work with any overhead administration, spend gauges and the assessed

benefit of your business and make a financial plan in like manner.

Advantages

8

Stage 1: Exercises are controlled by supervisors. There exercises are later uses in basic

leadership process.

Stage 2: In this progression administration offers positions to every procedure all

together, this request later sort in sliding configurations of advantages.

Stage 3: Here in this last stage, reserves are allotted to various spending

recommendations in view of their needs.

Advantages

Asset and assets are productively dispensed.

It perceives inefficient exercises and later wipes out such exercises.

It helps supervisors in driving cost decrease techniques.

Disadvantage

It's anything but a simple technique, it contains complex advances and

expends heaps of labour and time (Chiarini, 2012).

It isn't reasonable for huge associations, as huge measure of informations

are there. Utilizing these informations may requires basic points of interest

of it.

Because of the circumstance of over spending plan, inside clashes between

various representatives may rises.

Workers and administrators requires fundamental preparing to actualize

such a financial plan.

Top Down Budgeting:

The fundamental favourable position of this technique is that, an administrator does not

have to believe others to give spending data and it can spare time. In any case, if administrators

are not all around engaged with the everyday organization's business, at that point they won't not

have all the data expected to utilize this spending strategy (Damodaran, 2012). This may bring

about the distribution of assets in a few regions and the assignment of assets in others.

Under this planning technique, the most abnormal amount of business is done inside the

business, individual can work with any overhead administration, spend gauges and the assessed

benefit of your business and make a financial plan in like manner.

Advantages

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

This technique advances upper-level designation of experts.

It requires less investment to make a financial plan.

It helps administration in tending to hierarchical targets.

Disadvantage

Because of disposing of contribution of subordinates, it can bring down

their spirits.

The real impediment of this strategy may be ascends because of wrong

choices of upper administrators in view of inadequate information. This

could bring about inadequate assignment of planned assets among

different divisions and their execution may likewise diminish (Shields,

2015).

Bottom up planning: It raises the odds of working out of assets and prerequisites of store. This

technique begins with assurance of all the accessible dangers that are included and affecting

amid usage of a task.

Advantages

All representatives are included which builds their spirit and inspiration

level.

It gives clear and point by point informations to top administration.

Disadvantage

Lower level administrators may not fit to cover every basic territory.

Top administration has a less control over entire planning procedure of

this strategy.

This strategy could overstated a few sections of spending plan.

It is tedious and expensive technique.

b) Budget preparation process containing determination of price and different costing system

This is the process which remain associated with proper alignment and implementation of

strategies and plans

Step 1: this is the step in which basic framework is prepared by collecting information

Step 2: in this step the information and data are aligned in specified format

9

It requires less investment to make a financial plan.

It helps administration in tending to hierarchical targets.

Disadvantage

Because of disposing of contribution of subordinates, it can bring down

their spirits.

The real impediment of this strategy may be ascends because of wrong

choices of upper administrators in view of inadequate information. This

could bring about inadequate assignment of planned assets among

different divisions and their execution may likewise diminish (Shields,

2015).

Bottom up planning: It raises the odds of working out of assets and prerequisites of store. This

technique begins with assurance of all the accessible dangers that are included and affecting

amid usage of a task.

Advantages

All representatives are included which builds their spirit and inspiration

level.

It gives clear and point by point informations to top administration.

Disadvantage

Lower level administrators may not fit to cover every basic territory.

Top administration has a less control over entire planning procedure of

this strategy.

This strategy could overstated a few sections of spending plan.

It is tedious and expensive technique.

b) Budget preparation process containing determination of price and different costing system

This is the process which remain associated with proper alignment and implementation of

strategies and plans

Step 1: this is the step in which basic framework is prepared by collecting information

Step 2: in this step the information and data are aligned in specified format

9

Step 3: there is a particular order is setted and prepared in specific format so that effective

management and operation be done in effective manner.

Step 4: In this step the important aspects are rectified before implementation.

Step 5: this is the stage in which reviews and checks are validate and constructed in

predetermined format.

c) Importance of budget as a tool for planning and control purpose

Arranging is a fundamental procedure by which an association can accomplish their

targets by legitimate using assets of the organization. To determine them as quickly as time

permits is essential focus of the organization. For this reason, they are utilizing key execution

markers and money related administration to manage those issues. Equalization scorecards is a

fundamental arranging devices which are considered in charge of control all monetary related

issues those are having tremendous effects on the general execution of an organisation. In each

business there are sure kinds of business issues that are emerge without giving earlier signs.

There are different devices, for example, determining which use by administrators to assess up

and coming estimation of their expenses. Though situation and possibility instruments are

another significant devices that are useful for TECH Ltd.

TASK 4

Use of management accounting system to deal with financial problems and issues

It has been seen that "TECH Ltd" is connected with the generation of versatile charges

and other electronic contraptions. They are additionally connected with create unique sort of

charges to the clients. The administration of association has chosen to embrace adjust scorecard

technique to diminish their present misfortunes. As per back record, it has been watched that the

refered to organization has recorded a net loss of £ 1.5 million amid the year. Along these lines,

wide number of budgetary issues is emerging in association office in agreement to reserves. In

this stage, administration bookkeeping assumes a famous part to determine those issues and

make legitimate getting ready for boosting by the utilization of different strategies. This happens

to be a most extreme critical procedure which is useful in confronting all sort of money related

and non-monetary issues (Leitner, 2013).

Balance scorecard technique:

10

management and operation be done in effective manner.

Step 4: In this step the important aspects are rectified before implementation.

Step 5: this is the stage in which reviews and checks are validate and constructed in

predetermined format.

c) Importance of budget as a tool for planning and control purpose

Arranging is a fundamental procedure by which an association can accomplish their

targets by legitimate using assets of the organization. To determine them as quickly as time

permits is essential focus of the organization. For this reason, they are utilizing key execution

markers and money related administration to manage those issues. Equalization scorecards is a

fundamental arranging devices which are considered in charge of control all monetary related

issues those are having tremendous effects on the general execution of an organisation. In each

business there are sure kinds of business issues that are emerge without giving earlier signs.

There are different devices, for example, determining which use by administrators to assess up

and coming estimation of their expenses. Though situation and possibility instruments are

another significant devices that are useful for TECH Ltd.

TASK 4

Use of management accounting system to deal with financial problems and issues

It has been seen that "TECH Ltd" is connected with the generation of versatile charges

and other electronic contraptions. They are additionally connected with create unique sort of

charges to the clients. The administration of association has chosen to embrace adjust scorecard

technique to diminish their present misfortunes. As per back record, it has been watched that the

refered to organization has recorded a net loss of £ 1.5 million amid the year. Along these lines,

wide number of budgetary issues is emerging in association office in agreement to reserves. In

this stage, administration bookkeeping assumes a famous part to determine those issues and

make legitimate getting ready for boosting by the utilization of different strategies. This happens

to be a most extreme critical procedure which is useful in confronting all sort of money related

and non-monetary issues (Leitner, 2013).

Balance scorecard technique:

10

It would give incredible open door in understanding to making of direct association

among association inner capacities and their points by powerful control and correspondence to

decrease those issues. It is a basic technique which is use by administration for making change in

their inner task and accomplishment of want results. There are different points of view which are

characterized under this:

Financial: This would learn with respect to the association current fund position and

their different clients those using asset of the organization.

Client: It is important to take data with respect to the all partners about execution of an

association (Weygandt, Kimmel and Kieso, 2015).

Inner process: gathering data from inside division on regular routine to look at nature of

their merchandise and ventures.

Authoritative volume: Social affair criticism with respect to hierarchical execution through

capital, framework and different perspectives.

CONCLUSION

The above report is prepared to illustrate management accounting in organisational

context. Dimensions of use of management accounting system subject to decision making

process and analysing the financial stability with in the organisation. Each cost ought to be

legitimized or it ought to be disposed of. The operational approach of adjust scorecard is

basically in light of the smooth task of the exchange association. This can lessen business

consumption in light of the fact that the financial backing has been decreased deeply. At last,

individuals' approach includes sets of objectives that help the business' point of view of business.

This is a vital key arranging and administration apparatus that is to enhance the correspondence

procedures of the capacities utilized by the firm, determine to work, measure advance and

screen.

11

among association inner capacities and their points by powerful control and correspondence to

decrease those issues. It is a basic technique which is use by administration for making change in

their inner task and accomplishment of want results. There are different points of view which are

characterized under this:

Financial: This would learn with respect to the association current fund position and

their different clients those using asset of the organization.

Client: It is important to take data with respect to the all partners about execution of an

association (Weygandt, Kimmel and Kieso, 2015).

Inner process: gathering data from inside division on regular routine to look at nature of

their merchandise and ventures.

Authoritative volume: Social affair criticism with respect to hierarchical execution through

capital, framework and different perspectives.

CONCLUSION

The above report is prepared to illustrate management accounting in organisational

context. Dimensions of use of management accounting system subject to decision making

process and analysing the financial stability with in the organisation. Each cost ought to be

legitimized or it ought to be disposed of. The operational approach of adjust scorecard is

basically in light of the smooth task of the exchange association. This can lessen business

consumption in light of the fact that the financial backing has been decreased deeply. At last,

individuals' approach includes sets of objectives that help the business' point of view of business.

This is a vital key arranging and administration apparatus that is to enhance the correspondence

procedures of the capacities utilized by the firm, determine to work, measure advance and

screen.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Chiarini, A. and Vagnoni, E., 2015. World-class manufacturing by Fiat. Comparison with Toyota

production system from a strategic management, management accounting, operations

management and performance measurement dimension. International Journal of

Production Research. 53(2). pp.590-606.

Chapman, R. J., 2011. Simple tools and techniques for enterprise risk management. John Wiley

& Sons.

Caperchione, E. and Mussari, R. eds., 2012. Comparative issues in local government

accounting. Springer Science & Business Media.

Bennett, M. and James, P. eds., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Bebbington, J., Unerman, J. and O'Dwyer, B. eds., 2014. Sustainability accounting and

accountability. Routledge.

Banerjee, B., 2010. Financial policy and management accounting. PHI Learning Pvt. Ltd..

Bac, A. ed., 2013. International comparative issues in government accounting: The similarities

and differences between central government accounting and local government

accounting within or between countries. Springer Science & Business Media.

Anandarajan, M., Anandarajan, A. and Srinivasan, C.A. eds., 2012. Business intelligence

techniques: a perspective from accounting and finance. Springer Science & Business

Media.

Ward, K., 2012. Strategic management accounting. Routledge.

Shields, M. D., 2015. Established management accounting knowledge. Journal of Management

Accounting Research. 27(1). pp.123-132.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Fowzia, R., 2011. Strategic management accounting techniques: Relationship with business

strategy and strategic effectiveness of manufacturing organizations in

Bangladesh. World Journal of Management. 3(2). pp.54-69.

DRURY, C. M., 2013. Management and cost accounting. Springer.

David, F. R., 2011. Strategic management: Concepts and cases. Peaeson/Prentice Hall.

Damodaran, A., 2012. Investment valuation: Tools and techniques for determining the value of

any asset (Vol. 666). John Wiley & Sons.

Chiarini, A., 2012. Lean production: mistakes and limitations of accounting systems inside the

SME sector. Journal of Manufacturing Technology Management. 23(5). pp.681-700.

12

Books and Journals:

Chiarini, A. and Vagnoni, E., 2015. World-class manufacturing by Fiat. Comparison with Toyota

production system from a strategic management, management accounting, operations

management and performance measurement dimension. International Journal of

Production Research. 53(2). pp.590-606.

Chapman, R. J., 2011. Simple tools and techniques for enterprise risk management. John Wiley

& Sons.

Caperchione, E. and Mussari, R. eds., 2012. Comparative issues in local government

accounting. Springer Science & Business Media.

Bennett, M. and James, P. eds., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Bebbington, J., Unerman, J. and O'Dwyer, B. eds., 2014. Sustainability accounting and

accountability. Routledge.

Banerjee, B., 2010. Financial policy and management accounting. PHI Learning Pvt. Ltd..

Bac, A. ed., 2013. International comparative issues in government accounting: The similarities

and differences between central government accounting and local government

accounting within or between countries. Springer Science & Business Media.

Anandarajan, M., Anandarajan, A. and Srinivasan, C.A. eds., 2012. Business intelligence

techniques: a perspective from accounting and finance. Springer Science & Business

Media.

Ward, K., 2012. Strategic management accounting. Routledge.

Shields, M. D., 2015. Established management accounting knowledge. Journal of Management

Accounting Research. 27(1). pp.123-132.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Fowzia, R., 2011. Strategic management accounting techniques: Relationship with business

strategy and strategic effectiveness of manufacturing organizations in

Bangladesh. World Journal of Management. 3(2). pp.54-69.

DRURY, C. M., 2013. Management and cost accounting. Springer.

David, F. R., 2011. Strategic management: Concepts and cases. Peaeson/Prentice Hall.

Damodaran, A., 2012. Investment valuation: Tools and techniques for determining the value of

any asset (Vol. 666). John Wiley & Sons.

Chiarini, A., 2012. Lean production: mistakes and limitations of accounting systems inside the

SME sector. Journal of Manufacturing Technology Management. 23(5). pp.681-700.

12

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.