Management Accounting: Systems, Reporting, and Cost Analysis

VerifiedAdded on 2023/01/18

|13

|3994

|42

AI Summary

This document provides a comprehensive guide to management accounting, covering topics such as systems, reporting, cost analysis, budgets, and pricing strategies. It explores the benefits of different systems and reports, and their relevance to KEF Ltd. It also discusses various cost analysis techniques and the role of costing in setting prices. Additionally, it provides insights into different types of budgets and alternative budgeting methods. Finally, it offers an overview of different pricing strategies.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

Management accounting is termed as an activity of framing an efficient plans and policies

on the basis of final accounts of an organisation which are produced annually. These includes

cash flow statement, balance sheet, P&L a/c etc. It makes easy for manager to collect and

analyse valuable data both monetary and non-monetary to parties interested to the operations of

an organisation (Bekkers, Dijkstra and Fenger, 2016). KEF Ltd., a UK-based company dealing in

manufacturing sector is taken for the purpose of preparing the present report. The report

discusses the concept of managerial accounting along with its systems with benefits to an

organisation. The report also discusses about reporting systems, costing methods, planning

techniques to monitor and control budget and role of MA systems in tackling fund related issues.

TASK 1

P1

Management accounting: It is an activity of analysing financial stability of company by

examining the figures recorded under financial records. It is the part of decision making process

to take further action to strong financial performance of an organisation (Danoshana and

Ravivathani, 2019).

Origin and evolution of management accounting: Managerial accounting was introduced

at the period of industrial revolution. It came into existence after financial accounting with an

objective of providing valuable financial information to the shareholders of an organisation.

Management accounting systems: It includes various types which every organisation

adopts according to their nature and mission such as price optimisation system, cost accounting

system etc. In the context of KEF Ltd., the managers need to analyse the systems properly and

implement accordingly so as to gain profitable outcome in future.

Difference between management and financial accounting:

Managerial accounting Financial accounting

It facilitates both internal as well as

external parties by providing useful

financial stability of an organisation

It facilitates only external parties by

providing actual financial status of

company.

Conduction of management accounting

is based on the requirements of an

organisation as there is no specific

standards and principles.

Final account are prepared on annual

basis as per the accounting standards

and principles.

Management accounting is termed as an activity of framing an efficient plans and policies

on the basis of final accounts of an organisation which are produced annually. These includes

cash flow statement, balance sheet, P&L a/c etc. It makes easy for manager to collect and

analyse valuable data both monetary and non-monetary to parties interested to the operations of

an organisation (Bekkers, Dijkstra and Fenger, 2016). KEF Ltd., a UK-based company dealing in

manufacturing sector is taken for the purpose of preparing the present report. The report

discusses the concept of managerial accounting along with its systems with benefits to an

organisation. The report also discusses about reporting systems, costing methods, planning

techniques to monitor and control budget and role of MA systems in tackling fund related issues.

TASK 1

P1

Management accounting: It is an activity of analysing financial stability of company by

examining the figures recorded under financial records. It is the part of decision making process

to take further action to strong financial performance of an organisation (Danoshana and

Ravivathani, 2019).

Origin and evolution of management accounting: Managerial accounting was introduced

at the period of industrial revolution. It came into existence after financial accounting with an

objective of providing valuable financial information to the shareholders of an organisation.

Management accounting systems: It includes various types which every organisation

adopts according to their nature and mission such as price optimisation system, cost accounting

system etc. In the context of KEF Ltd., the managers need to analyse the systems properly and

implement accordingly so as to gain profitable outcome in future.

Difference between management and financial accounting:

Managerial accounting Financial accounting

It facilitates both internal as well as

external parties by providing useful

financial stability of an organisation

It facilitates only external parties by

providing actual financial status of

company.

Conduction of management accounting

is based on the requirements of an

organisation as there is no specific

standards and principles.

Final account are prepared on annual

basis as per the accounting standards

and principles.

Description of management accounting systems with relevance to KEF Ltd.

Price optimisation system; It is a system facilitates an organisation by providing

information related with actual perception of targeted customers towards their existing pricing

policy. Thus, it becomes more beneficial for KEP Ltd. to adopt this system to acknowledge the

needs and requirements of customers in respect of their pricing policy and update them

accordingly in order to maintain a good customer strength.

Cost accounting system: It is a system providing information related with the amount

invested in different business activities which makes easy for manager to make an effect budget.

Using of this system by KEF Ltd. help in analysing cost by making comparison of actual

incurred cost with standard. This will save business cost and increase profitability of an

organisation (Kustiyo and et. al., 2015).

Inventory management system: It is a system facilitates company to keep stock in

warehouses in such amount that can make easy for them to meet customers’ requirements.

Adoption of this system by KEF Ltd. help in reducing business cost in terms of minimising

storage cost of inventory by facilitating management to order stock whenever required.

Benefits of management accounting systems:

Management accounting system Benefits

Cost accounting system It helps KEF Ltd. to maintain record of cost

invested in different business activities which

minimises the chances of errors in final

accounts.

Price optimisation system It helps KEF Ltd. to make relevant changes in

their existing pricing strategy after examining

the actual thinking of customers towards their

policy. This will increase retention of their

loyal clients.

Inventory management system This will reduce storage cost of KEF Ltd. by

directing managers to order stock whenever

required. This will impact positively on their

net profitability.

P2

Management accounting reporting: It is a documentation process which is necessary to

be done by an organisation to maintain important information and data that are useful for

managers to formulate a suitable plans and strategies for the development of an organisation.

Price optimisation system; It is a system facilitates an organisation by providing

information related with actual perception of targeted customers towards their existing pricing

policy. Thus, it becomes more beneficial for KEP Ltd. to adopt this system to acknowledge the

needs and requirements of customers in respect of their pricing policy and update them

accordingly in order to maintain a good customer strength.

Cost accounting system: It is a system providing information related with the amount

invested in different business activities which makes easy for manager to make an effect budget.

Using of this system by KEF Ltd. help in analysing cost by making comparison of actual

incurred cost with standard. This will save business cost and increase profitability of an

organisation (Kustiyo and et. al., 2015).

Inventory management system: It is a system facilitates company to keep stock in

warehouses in such amount that can make easy for them to meet customers’ requirements.

Adoption of this system by KEF Ltd. help in reducing business cost in terms of minimising

storage cost of inventory by facilitating management to order stock whenever required.

Benefits of management accounting systems:

Management accounting system Benefits

Cost accounting system It helps KEF Ltd. to maintain record of cost

invested in different business activities which

minimises the chances of errors in final

accounts.

Price optimisation system It helps KEF Ltd. to make relevant changes in

their existing pricing strategy after examining

the actual thinking of customers towards their

policy. This will increase retention of their

loyal clients.

Inventory management system This will reduce storage cost of KEF Ltd. by

directing managers to order stock whenever

required. This will impact positively on their

net profitability.

P2

Management accounting reporting: It is a documentation process which is necessary to

be done by an organisation to maintain important information and data that are useful for

managers to formulate a suitable plans and strategies for the development of an organisation.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Characteristics of good information system: High reliability and accuracy of information

maximises the effectiveness of decision made by the management in the context of financial

growth of an organisation (Lunkes and et. al., 2019).

Types of management accounting reporting:

Cost accounting report: It is a report which indicates the differences in results between

actual cost incurred in business functions and expected cost of management. It makes easy for

management of KEF Ltd. to prepare budget after analysing the cost invested in previous year for

same project which impacts positively on net profitability of business.

Inventory management report: It is a report providing inventory related information that

an organisation currently have in warehouses. This will motivate managers of KEF td. To take

future orders from their clients due to having confidence of keeping sufficient level of inventory.

This will reduces storage cost of stock as this report allows managers to order further inventory

only when client orders their products and services (Ng and Li, 2016)).

Account receivable report: This is a report which provides information connected with

the list of debtors whose payments are still due to company. This may affect adversely to the

financial position which emerges the importance of prepare such kind of report. Preparation of

this report by KEF Ltd. help manger in upgrading their current credit policy with more strict

regulations and actions which minimises the chances of receiving delay payments by their

default clients.

Integration of management accounting systems and report in organisational process:

Management accounting and reporting system are much interrelated with each other for the

betterment of an organisation. For an instance, inventory management system can provide

valuable information to the management of KEF Ltd. only when reliable and accurate

information are recorded under inventory management report.

TASK 2

P3

Cost: It is simply explained as the total sum which is needed to be paid by consumer to the

one who sells the product and services. Attracting customers towards the company, KEF Ltd. has

set the range of price which can be easily paid by the users. Several types of costs are available

and they have been explained below:

maximises the effectiveness of decision made by the management in the context of financial

growth of an organisation (Lunkes and et. al., 2019).

Types of management accounting reporting:

Cost accounting report: It is a report which indicates the differences in results between

actual cost incurred in business functions and expected cost of management. It makes easy for

management of KEF Ltd. to prepare budget after analysing the cost invested in previous year for

same project which impacts positively on net profitability of business.

Inventory management report: It is a report providing inventory related information that

an organisation currently have in warehouses. This will motivate managers of KEF td. To take

future orders from their clients due to having confidence of keeping sufficient level of inventory.

This will reduces storage cost of stock as this report allows managers to order further inventory

only when client orders their products and services (Ng and Li, 2016)).

Account receivable report: This is a report which provides information connected with

the list of debtors whose payments are still due to company. This may affect adversely to the

financial position which emerges the importance of prepare such kind of report. Preparation of

this report by KEF Ltd. help manger in upgrading their current credit policy with more strict

regulations and actions which minimises the chances of receiving delay payments by their

default clients.

Integration of management accounting systems and report in organisational process:

Management accounting and reporting system are much interrelated with each other for the

betterment of an organisation. For an instance, inventory management system can provide

valuable information to the management of KEF Ltd. only when reliable and accurate

information are recorded under inventory management report.

TASK 2

P3

Cost: It is simply explained as the total sum which is needed to be paid by consumer to the

one who sells the product and services. Attracting customers towards the company, KEF Ltd. has

set the range of price which can be easily paid by the users. Several types of costs are available

and they have been explained below:

Direct cost: It can be understood as the cost which are directly incurred at the time of

construction or manufacturing. Some of the example of direct cost are insurance charges,

salaries to the employees etc.

Indirect cost: Those expenses which are not included directly at the time of

manufacturing or construction phase is known as Indirect cost. It adds on rent,

miscellaneous expenses etc.

Cost analysis: It is explained as the procedure which are used by the business organisation

for the purpose of finding that what can be the profit volume which company can earn. In context

of KEF Ltd., they also use cost analysis process in order to determine the decision which are

taken by them are correct or not (Nwonyuku, 2015).

Cost volume profit: It is one of the accounting procedure which is needed to be used by

the management of KEF Ltd. in order to find the fluctuations in cost and volume on business

organisation.

Flexible budgeting: This is one of the type of budget which can be used by business

organisation like KEF Ltd. because they will get the option to alter their business decision as per

the situation which has raised in front of them.

Cost variance: It is the accounting tool which can be used by the business organisation

in order to check the actual and budget cost. In context of KEF Ltd., they also uses cost analysis

for the purpose of forming the plans.

Marginal costing: This is the type of accounting concept where cost per unit never

changes and it is further bifurcated into fixed and variable cost. This types of concepts are

mainly used by the organisation which performs the business at smaller ground.

Absorption costing: It is one of the accounting concept which is used by business

organisation to find out the exact net profit and gross profit. In addition, it is beneficial at the

time of distributing the fixed overhead to any of the department within the business organisation.

Fixed cost: This are the cost who do not changes at the entire time period. Some of the

example of fixed cost are taxation, interest rate and many more (Ruiz and Sirvent, 2016).

Variable cost: Those cost which changes as per the change in unit is knowns ass variable

cost. Some of the example for KEF Ltd. are wages, labour etc.

Cost allocation: It is the process which is used by ABCC Ltd in order to distribute the

necessary amount of fund to different department.

construction or manufacturing. Some of the example of direct cost are insurance charges,

salaries to the employees etc.

Indirect cost: Those expenses which are not included directly at the time of

manufacturing or construction phase is known as Indirect cost. It adds on rent,

miscellaneous expenses etc.

Cost analysis: It is explained as the procedure which are used by the business organisation

for the purpose of finding that what can be the profit volume which company can earn. In context

of KEF Ltd., they also use cost analysis process in order to determine the decision which are

taken by them are correct or not (Nwonyuku, 2015).

Cost volume profit: It is one of the accounting procedure which is needed to be used by

the management of KEF Ltd. in order to find the fluctuations in cost and volume on business

organisation.

Flexible budgeting: This is one of the type of budget which can be used by business

organisation like KEF Ltd. because they will get the option to alter their business decision as per

the situation which has raised in front of them.

Cost variance: It is the accounting tool which can be used by the business organisation

in order to check the actual and budget cost. In context of KEF Ltd., they also uses cost analysis

for the purpose of forming the plans.

Marginal costing: This is the type of accounting concept where cost per unit never

changes and it is further bifurcated into fixed and variable cost. This types of concepts are

mainly used by the organisation which performs the business at smaller ground.

Absorption costing: It is one of the accounting concept which is used by business

organisation to find out the exact net profit and gross profit. In addition, it is beneficial at the

time of distributing the fixed overhead to any of the department within the business organisation.

Fixed cost: This are the cost who do not changes at the entire time period. Some of the

example of fixed cost are taxation, interest rate and many more (Ruiz and Sirvent, 2016).

Variable cost: Those cost which changes as per the change in unit is knowns ass variable

cost. Some of the example for KEF Ltd. are wages, labour etc.

Cost allocation: It is the process which is used by ABCC Ltd in order to distribute the

necessary amount of fund to different department.

Standard costing: It is a technique of costing used by those business organisation which

performs business activity at a greater platform to find the variance between actual and standard

cost.

Activity based costing: It is the type of costing which is used by the business

organisation like KEF Ltd. in order to distribute the cost as per the expenses occurred while

performing any of the task.

Role of costing in setting price: Costing is one of the important concept which can be

used by the KEF Ltd. in order to find the actual cost which has been incurred at the time of

conducting the business activity. This will allow company to decided that at what price they can

earn the profit (Simmie and Somers, 2015).

Inventory cost: The cost which are incurred for maintaining the stock is known as

inventory cost. Several types of inventory cost are there which is used by KEF Ltd. and they are.

Ordering cost: Those expenses which incurred at the time of giving order to supplier by

KEF Ltd. is called ordering cost.

Carrying cost: Those cost which occurs at the time of maintain the stock within KEF

Ltd. is knowns as carrying cost.

Shortage cost: If in any of the situation company like KEF Ltd. doesn’t have the stock

with them then this types of cost occurs.

Benefits of reducing inventory cost:

Whenever inventory cost is reducing it automatically enhance the revenue of a company

as it saved unnecessary expenses.

It allows to set out the effective price to sell the product due to which company have the

option to compete with rivalries firm.

Valuation methods:

LIFO: Here, those material which are brought recently must be used by KEF Ltd.

FIFO: This is the valuation technique which is used by company where they use those

products in beginning which were brought earlier.

KEF Ltd. uses FIFO method for the purpose of attaining effective results.

Overhead costs: This are those cost which are incurred within the KEF Ltd. at the time

of constructing any of the section and it will be included as a part of overhead cost (Smith and

Driscoll, 2017).

performs business activity at a greater platform to find the variance between actual and standard

cost.

Activity based costing: It is the type of costing which is used by the business

organisation like KEF Ltd. in order to distribute the cost as per the expenses occurred while

performing any of the task.

Role of costing in setting price: Costing is one of the important concept which can be

used by the KEF Ltd. in order to find the actual cost which has been incurred at the time of

conducting the business activity. This will allow company to decided that at what price they can

earn the profit (Simmie and Somers, 2015).

Inventory cost: The cost which are incurred for maintaining the stock is known as

inventory cost. Several types of inventory cost are there which is used by KEF Ltd. and they are.

Ordering cost: Those expenses which incurred at the time of giving order to supplier by

KEF Ltd. is called ordering cost.

Carrying cost: Those cost which occurs at the time of maintain the stock within KEF

Ltd. is knowns as carrying cost.

Shortage cost: If in any of the situation company like KEF Ltd. doesn’t have the stock

with them then this types of cost occurs.

Benefits of reducing inventory cost:

Whenever inventory cost is reducing it automatically enhance the revenue of a company

as it saved unnecessary expenses.

It allows to set out the effective price to sell the product due to which company have the

option to compete with rivalries firm.

Valuation methods:

LIFO: Here, those material which are brought recently must be used by KEF Ltd.

FIFO: This is the valuation technique which is used by company where they use those

products in beginning which were brought earlier.

KEF Ltd. uses FIFO method for the purpose of attaining effective results.

Overhead costs: This are those cost which are incurred within the KEF Ltd. at the time

of constructing any of the section and it will be included as a part of overhead cost (Smith and

Driscoll, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4

Budget: It is one of the accounting tool which is needed to be used by every organisation

in order to estimate the overall cost which can be incurred within the specific time period. This

are mainly used for the specific time period. The main benefit which KEF Ltd. can obtained with

the help of budget is that company can be able to reduce unnecessary expenses for enhancing

profit (Spiering and et. al., 2015).

Preparing a budget: Whenever any of the budget is required to be prepare then it is the

duty of manager to analyse each and every area so that unnecessary problem will not be created.

Now different plans and policies are needed to be formed so that estimated budget can be helpful

for attaining the result.

Different types of budgets:

Capital budget: This are those budget which is prepared by the business organisation to

conduct those activities which are performed at a greater platform. Here, KEF Ltd. prepare the

capital budget whenever they try to take any of the action for the long period of time. Below,

pros and cons are listed.

Advantages Disadvantages

This helps to maintain the records of monetary

resources invested within any of the project

which is performed at a greater platform.

The main problem which can be seen here is

that information about all of the department are

kept at a single place.

Operating budget: It is a budget which is also created to predict all the projected profits

and expenditures that are focused on the organization's expected sales and revenues. This allows

the top level management of the KEF Ltd. to evaluate whether or not the financial assets are

being used correctly by the organization.

Pros and cons are explained below:

Advantages Disadvantages

It helps to determine where resource is being

used as per the requirement or not.

It may overestimate sales and other statistics in

the firm's reports.

P4

Budget: It is one of the accounting tool which is needed to be used by every organisation

in order to estimate the overall cost which can be incurred within the specific time period. This

are mainly used for the specific time period. The main benefit which KEF Ltd. can obtained with

the help of budget is that company can be able to reduce unnecessary expenses for enhancing

profit (Spiering and et. al., 2015).

Preparing a budget: Whenever any of the budget is required to be prepare then it is the

duty of manager to analyse each and every area so that unnecessary problem will not be created.

Now different plans and policies are needed to be formed so that estimated budget can be helpful

for attaining the result.

Different types of budgets:

Capital budget: This are those budget which is prepared by the business organisation to

conduct those activities which are performed at a greater platform. Here, KEF Ltd. prepare the

capital budget whenever they try to take any of the action for the long period of time. Below,

pros and cons are listed.

Advantages Disadvantages

This helps to maintain the records of monetary

resources invested within any of the project

which is performed at a greater platform.

The main problem which can be seen here is

that information about all of the department are

kept at a single place.

Operating budget: It is a budget which is also created to predict all the projected profits

and expenditures that are focused on the organization's expected sales and revenues. This allows

the top level management of the KEF Ltd. to evaluate whether or not the financial assets are

being used correctly by the organization.

Pros and cons are explained below:

Advantages Disadvantages

It helps to determine where resource is being

used as per the requirement or not.

It may overestimate sales and other statistics in

the firm's reports.

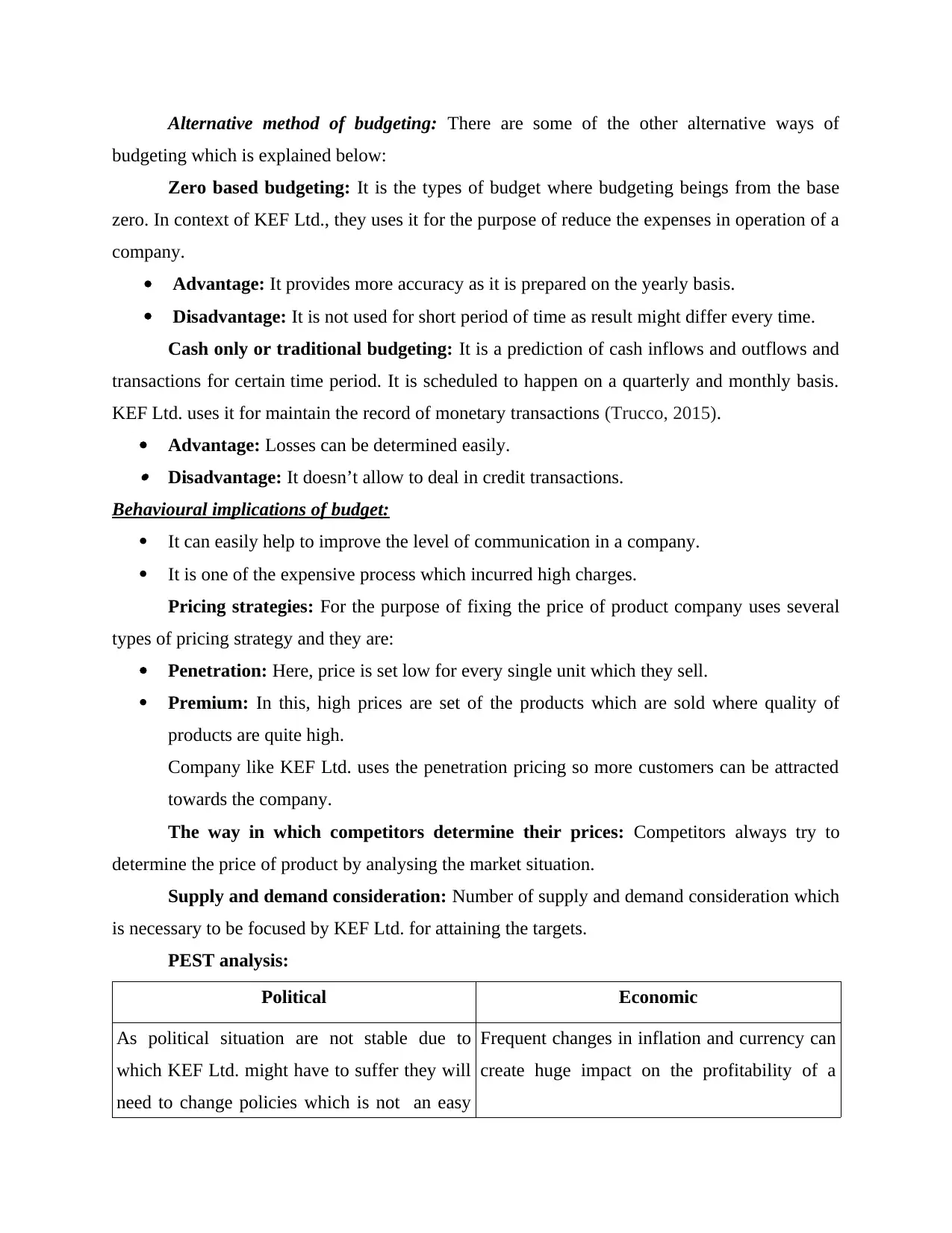

Alternative method of budgeting: There are some of the other alternative ways of

budgeting which is explained below:

Zero based budgeting: It is the types of budget where budgeting beings from the base

zero. In context of KEF Ltd., they uses it for the purpose of reduce the expenses in operation of a

company.

Advantage: It provides more accuracy as it is prepared on the yearly basis.

Disadvantage: It is not used for short period of time as result might differ every time.

Cash only or traditional budgeting: It is a prediction of cash inflows and outflows and

transactions for certain time period. It is scheduled to happen on a quarterly and monthly basis.

KEF Ltd. uses it for maintain the record of monetary transactions (Trucco, 2015).

Advantage: Losses can be determined easily. Disadvantage: It doesn’t allow to deal in credit transactions.

Behavioural implications of budget:

It can easily help to improve the level of communication in a company.

It is one of the expensive process which incurred high charges.

Pricing strategies: For the purpose of fixing the price of product company uses several

types of pricing strategy and they are:

Penetration: Here, price is set low for every single unit which they sell.

Premium: In this, high prices are set of the products which are sold where quality of

products are quite high.

Company like KEF Ltd. uses the penetration pricing so more customers can be attracted

towards the company.

The way in which competitors determine their prices: Competitors always try to

determine the price of product by analysing the market situation.

Supply and demand consideration: Number of supply and demand consideration which

is necessary to be focused by KEF Ltd. for attaining the targets.

PEST analysis:

Political Economic

As political situation are not stable due to

which KEF Ltd. might have to suffer they will

need to change policies which is not an easy

Frequent changes in inflation and currency can

create huge impact on the profitability of a

budgeting which is explained below:

Zero based budgeting: It is the types of budget where budgeting beings from the base

zero. In context of KEF Ltd., they uses it for the purpose of reduce the expenses in operation of a

company.

Advantage: It provides more accuracy as it is prepared on the yearly basis.

Disadvantage: It is not used for short period of time as result might differ every time.

Cash only or traditional budgeting: It is a prediction of cash inflows and outflows and

transactions for certain time period. It is scheduled to happen on a quarterly and monthly basis.

KEF Ltd. uses it for maintain the record of monetary transactions (Trucco, 2015).

Advantage: Losses can be determined easily. Disadvantage: It doesn’t allow to deal in credit transactions.

Behavioural implications of budget:

It can easily help to improve the level of communication in a company.

It is one of the expensive process which incurred high charges.

Pricing strategies: For the purpose of fixing the price of product company uses several

types of pricing strategy and they are:

Penetration: Here, price is set low for every single unit which they sell.

Premium: In this, high prices are set of the products which are sold where quality of

products are quite high.

Company like KEF Ltd. uses the penetration pricing so more customers can be attracted

towards the company.

The way in which competitors determine their prices: Competitors always try to

determine the price of product by analysing the market situation.

Supply and demand consideration: Number of supply and demand consideration which

is necessary to be focused by KEF Ltd. for attaining the targets.

PEST analysis:

Political Economic

As political situation are not stable due to

which KEF Ltd. might have to suffer they will

need to change policies which is not an easy

Frequent changes in inflation and currency can

create huge impact on the profitability of a

task. company.

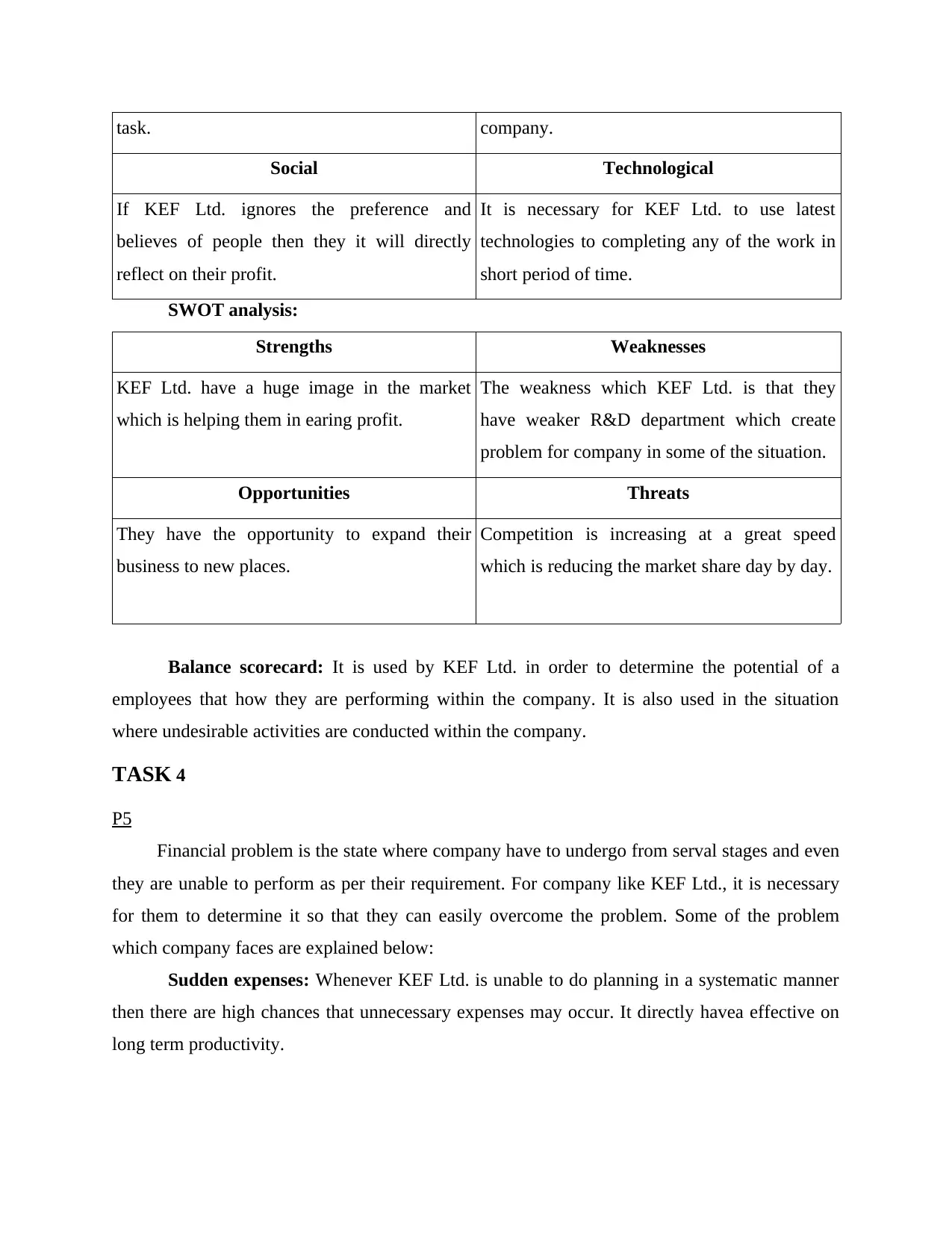

Social Technological

If KEF Ltd. ignores the preference and

believes of people then they it will directly

reflect on their profit.

It is necessary for KEF Ltd. to use latest

technologies to completing any of the work in

short period of time.

SWOT analysis:

Strengths Weaknesses

KEF Ltd. have a huge image in the market

which is helping them in earing profit.

The weakness which KEF Ltd. is that they

have weaker R&D department which create

problem for company in some of the situation.

Opportunities Threats

They have the opportunity to expand their

business to new places.

Competition is increasing at a great speed

which is reducing the market share day by day.

Balance scorecard: It is used by KEF Ltd. in order to determine the potential of a

employees that how they are performing within the company. It is also used in the situation

where undesirable activities are conducted within the company.

TASK 4

P5

Financial problem is the state where company have to undergo from serval stages and even

they are unable to perform as per their requirement. For company like KEF Ltd., it is necessary

for them to determine it so that they can easily overcome the problem. Some of the problem

which company faces are explained below:

Sudden expenses: Whenever KEF Ltd. is unable to do planning in a systematic manner

then there are high chances that unnecessary expenses may occur. It directly havea effective on

long term productivity.

Social Technological

If KEF Ltd. ignores the preference and

believes of people then they it will directly

reflect on their profit.

It is necessary for KEF Ltd. to use latest

technologies to completing any of the work in

short period of time.

SWOT analysis:

Strengths Weaknesses

KEF Ltd. have a huge image in the market

which is helping them in earing profit.

The weakness which KEF Ltd. is that they

have weaker R&D department which create

problem for company in some of the situation.

Opportunities Threats

They have the opportunity to expand their

business to new places.

Competition is increasing at a great speed

which is reducing the market share day by day.

Balance scorecard: It is used by KEF Ltd. in order to determine the potential of a

employees that how they are performing within the company. It is also used in the situation

where undesirable activities are conducted within the company.

TASK 4

P5

Financial problem is the state where company have to undergo from serval stages and even

they are unable to perform as per their requirement. For company like KEF Ltd., it is necessary

for them to determine it so that they can easily overcome the problem. Some of the problem

which company faces are explained below:

Sudden expenses: Whenever KEF Ltd. is unable to do planning in a systematic manner

then there are high chances that unnecessary expenses may occur. It directly havea effective on

long term productivity.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Late payments by customers: As KEF Ltd. provides the credit facilities to their

customer and there are some of the situation where customersdonot give money back on time

which create issues for the company.

By looking at the problem some of the appropriate solutions are required in order to

overcomes the problem which company is facing. Below, some of the techniques have been

explained in detail (Wouters and Pelz, 2018).

KPIs (Key Performance Indicators): It is used in the situation where company is

needed to evaluate the performance of a company. Two types of KPIs are there and they are

Financial and non-financial.Financial is used for finding unnecessary expenses in a company

where as non-financial is used of problem being faced by company in operating day to day

activity. KEF Ltd. uses financial KPI for finding the reason for sudden expenses so that result

can be improved.

Benchmarking: Here, company gets the chances to compare themselves with other

company. Here, ABC uses the benchmarking process to identify the main reason behind the

failure in collecting of credit amount.

Budgetary targets: It is an estimation of funds for the specific time period. It is prepared

by the company in order to identify the differentiate between actual and standard figure so that

financial issues can be solved by the company.

Financial governance: It is explained as the process where company is required to

follows a standard financial principle which are required to be followed within the company. It is

used to detect the organization's approach through analysing whether or not suitable financial

principles are preceded.

Effective management accountant along with its characteristics and the way of

resolving financial problems:

An effective management accountant must have different types of skills to deal with

different situation by forming plans so that positive results can be achieved.

Decision making skill is also required by the company in order to solved the problem

which are faced by the company.

Comparison:

KEF Ltd. DEF Ltd.

Company uses cost accounting system for the Inventory Management system is used by the

customer and there are some of the situation where customersdonot give money back on time

which create issues for the company.

By looking at the problem some of the appropriate solutions are required in order to

overcomes the problem which company is facing. Below, some of the techniques have been

explained in detail (Wouters and Pelz, 2018).

KPIs (Key Performance Indicators): It is used in the situation where company is

needed to evaluate the performance of a company. Two types of KPIs are there and they are

Financial and non-financial.Financial is used for finding unnecessary expenses in a company

where as non-financial is used of problem being faced by company in operating day to day

activity. KEF Ltd. uses financial KPI for finding the reason for sudden expenses so that result

can be improved.

Benchmarking: Here, company gets the chances to compare themselves with other

company. Here, ABC uses the benchmarking process to identify the main reason behind the

failure in collecting of credit amount.

Budgetary targets: It is an estimation of funds for the specific time period. It is prepared

by the company in order to identify the differentiate between actual and standard figure so that

financial issues can be solved by the company.

Financial governance: It is explained as the process where company is required to

follows a standard financial principle which are required to be followed within the company. It is

used to detect the organization's approach through analysing whether or not suitable financial

principles are preceded.

Effective management accountant along with its characteristics and the way of

resolving financial problems:

An effective management accountant must have different types of skills to deal with

different situation by forming plans so that positive results can be achieved.

Decision making skill is also required by the company in order to solved the problem

which are faced by the company.

Comparison:

KEF Ltd. DEF Ltd.

Company uses cost accounting system for the Inventory Management system is used by the

purpose of analysing the situation through

which they can deal with sudden and

unplanned expenses.

company to maintain the record of every stock

and even there will be less chances of arising

any of the problem.

For the purpose of setting the suitable prices

company use price optimisation system. This

will allow to resolve the problem of credit and

late payment which is mainly done by the

company.

They uses the cost accounting system for the

purpose of resolving the problem related to

keeping record of every customers.

Financial governance is implied of reporting

on given time period.

Financial Governance strategy is used by the

company to disclose about the accurate

position of company with stakeholders.

CONCLUSION

It can be summarised from the above discussion that managerial accounting is an

important part in their growth and success of enterprises operating in competitive market by

driving them with an effective plans and policies. For this, accounting manager critically

evaluates the different management accounting and reporting systems so that maximum outcome

can be gain by using them. Different tools are also such as zero based, operating budget etc. to

control budget which makes positive impact on overall profitability of an organisation.

which they can deal with sudden and

unplanned expenses.

company to maintain the record of every stock

and even there will be less chances of arising

any of the problem.

For the purpose of setting the suitable prices

company use price optimisation system. This

will allow to resolve the problem of credit and

late payment which is mainly done by the

company.

They uses the cost accounting system for the

purpose of resolving the problem related to

keeping record of every customers.

Financial governance is implied of reporting

on given time period.

Financial Governance strategy is used by the

company to disclose about the accurate

position of company with stakeholders.

CONCLUSION

It can be summarised from the above discussion that managerial accounting is an

important part in their growth and success of enterprises operating in competitive market by

driving them with an effective plans and policies. For this, accounting manager critically

evaluates the different management accounting and reporting systems so that maximum outcome

can be gain by using them. Different tools are also such as zero based, operating budget etc. to

control budget which makes positive impact on overall profitability of an organisation.

REFERENCES

Books and Journals

Bekkers, V., Dijkstra, G. and Fenger, M., 2016. Governance and the democratic deficit:

Assessing the democratic legitimacy of governance practices. Routledge.

Danoshana, S. and Ravivathani, T., 2019. The impact of the corporate governance on firm

performance: A study on financial institutions in Sri Lanka. SAARJ Journal on Banking

& Insurance Research .8(1). pp.62-67.

Kustiyo, K. and et. al., 2015. Annual Forest Monitoring as part of Indonesia's National Carbon

Accounting System. The International Archives of Photogrammetry, Remote Sensing

and Spatial Information Sciences .40(7). p.441.

Lunkes, R.J. And et. al., 2019. Study on the Adoption of Management Accounting Practices in

Hotel Companies in Florianópolis, SC, Brazil. Turismo em Análise .29(2).

Ng, F. and Li, I., 2016. Case-mix accounting beyond the hospital: Foundations for a customer-

perspective in accounting for healthcare. Pacific Accounting Review .28(4). pp.373-385.

Nwonyuku, K., 2015. Behavioral Implications of Management Accounting Practices: A

Contemporary Issue in Management Accounting. Available at SSRN 2656521.

Ruiz, J.L. and Sirvent, I., 2016. Common benchmarking and ranking of units with DEA.

Omega .65. pp.1-9.

Simmie, J.M. and Somers, K.P., 2015. Benchmarking compound methods (CBS-QB3, CBS-

APNO, G3, G4, W1BD) against the active thermochemical tables: A litmus test for

cost-effective molecular formation enthalpies. The Journal of Physical Chemistry

A .119(28). pp.7235-7246.

Smith, D. and Driscoll, T., 2017. Partnering with data scientists for management accounting

success: management accountants have the opportunity to drive value creation by

working with industry experts to integrate data science. Strategic Finance .98(11).

pp.70-72.

Spiering, T. and et. al., 2015. Energy efficiency benchmarking for injection moulding processes.

Robotics and Computer-Integrated Manufacturing .36. pp.45-59.

Trucco, S., 2015. Financial Accounting and Alignment to Management Accounting in the Italian

Context. In Financial Accounting (pp. 83-132). Springer, Cham.

Wouters, M. and Pelz, M., 2018. Fostering corporate innovation by living apart together:

Management accounting information exchange in the Bosch startup platform. In

Accounting, Innovation and Inter-Organisational Relationships(pp. 82-103). Routledge.

Books and Journals

Bekkers, V., Dijkstra, G. and Fenger, M., 2016. Governance and the democratic deficit:

Assessing the democratic legitimacy of governance practices. Routledge.

Danoshana, S. and Ravivathani, T., 2019. The impact of the corporate governance on firm

performance: A study on financial institutions in Sri Lanka. SAARJ Journal on Banking

& Insurance Research .8(1). pp.62-67.

Kustiyo, K. and et. al., 2015. Annual Forest Monitoring as part of Indonesia's National Carbon

Accounting System. The International Archives of Photogrammetry, Remote Sensing

and Spatial Information Sciences .40(7). p.441.

Lunkes, R.J. And et. al., 2019. Study on the Adoption of Management Accounting Practices in

Hotel Companies in Florianópolis, SC, Brazil. Turismo em Análise .29(2).

Ng, F. and Li, I., 2016. Case-mix accounting beyond the hospital: Foundations for a customer-

perspective in accounting for healthcare. Pacific Accounting Review .28(4). pp.373-385.

Nwonyuku, K., 2015. Behavioral Implications of Management Accounting Practices: A

Contemporary Issue in Management Accounting. Available at SSRN 2656521.

Ruiz, J.L. and Sirvent, I., 2016. Common benchmarking and ranking of units with DEA.

Omega .65. pp.1-9.

Simmie, J.M. and Somers, K.P., 2015. Benchmarking compound methods (CBS-QB3, CBS-

APNO, G3, G4, W1BD) against the active thermochemical tables: A litmus test for

cost-effective molecular formation enthalpies. The Journal of Physical Chemistry

A .119(28). pp.7235-7246.

Smith, D. and Driscoll, T., 2017. Partnering with data scientists for management accounting

success: management accountants have the opportunity to drive value creation by

working with industry experts to integrate data science. Strategic Finance .98(11).

pp.70-72.

Spiering, T. and et. al., 2015. Energy efficiency benchmarking for injection moulding processes.

Robotics and Computer-Integrated Manufacturing .36. pp.45-59.

Trucco, S., 2015. Financial Accounting and Alignment to Management Accounting in the Italian

Context. In Financial Accounting (pp. 83-132). Springer, Cham.

Wouters, M. and Pelz, M., 2018. Fostering corporate innovation by living apart together:

Management accounting information exchange in the Bosch startup platform. In

Accounting, Innovation and Inter-Organisational Relationships(pp. 82-103). Routledge.

1 out of 13

Related Documents

![Management Accounting Table of Content [pic]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fcb%2F8d835dc5046f43b1b3c649176e00fab1.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.