Management Accounting System and its Application: A Comprehensive Analysis

VerifiedAdded on 2024/05/16

|22

|3674

|331

AI Summary

This report delves into the significance of management accounting in enhancing company performance and decision-making. It explores various types of management accounting systems, including managerial, inventory, and cost accounting, and critically evaluates their benefits and applications within an organizational context. The report further examines the differences between absorption costing and marginal costing, providing illustrative income statements and a reconciliation statement to highlight the discrepancies in profit calculations. Additionally, it compares and contrasts three planning tools used in management accounting: standard costing, budgetary control, and decision making, analyzing their effectiveness in addressing financial problems and guiding organizations towards sustainable success. The report concludes by emphasizing the crucial role of management accounting in navigating financial challenges and achieving long-term organizational goals.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting System and its application

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Section I..........................................................................................................................................3

[P1] Explain why management accounting is important in the decision-making process for

improving the performance of the company...............................................................................3

[P2] Explain three different types of management accounting systems used for

management accounting reporting..............................................................................................5

[P3] Critically evaluate the benefits of types of management accounting systems and their

application within an organizational context..............................................................................6

[P4.(a)] Prepare and present two different income statements under absorption costing and

marginal costing for each of the two quarters............................................................................7

[P4.(b)] Explain with supportive calculations, why the profits under techniques are

different........................................................................................................................................11

[P4.(c)] Produce a reconciliation statement of profit or loss showing the reconciled profits

for the two techniques used previously......................................................................................12

Section II.......................................................................................................................................13

[Part A] Compare and contrast three different planning tools used in management

accounting. Analyse and evaluate how the use of planning tools for accounting respond to

solving financial problems to lead the organization.................................................................13

[Part B] Compare ways in which management accounting is applied. Analyse how, in

responding to financial problems, management accounting can lead organizations to

sustainable success.......................................................................................................................15

Conclusion....................................................................................................................................16

References.....................................................................................................................................17

Section I..........................................................................................................................................3

[P1] Explain why management accounting is important in the decision-making process for

improving the performance of the company...............................................................................3

[P2] Explain three different types of management accounting systems used for

management accounting reporting..............................................................................................5

[P3] Critically evaluate the benefits of types of management accounting systems and their

application within an organizational context..............................................................................6

[P4.(a)] Prepare and present two different income statements under absorption costing and

marginal costing for each of the two quarters............................................................................7

[P4.(b)] Explain with supportive calculations, why the profits under techniques are

different........................................................................................................................................11

[P4.(c)] Produce a reconciliation statement of profit or loss showing the reconciled profits

for the two techniques used previously......................................................................................12

Section II.......................................................................................................................................13

[Part A] Compare and contrast three different planning tools used in management

accounting. Analyse and evaluate how the use of planning tools for accounting respond to

solving financial problems to lead the organization.................................................................13

[Part B] Compare ways in which management accounting is applied. Analyse how, in

responding to financial problems, management accounting can lead organizations to

sustainable success.......................................................................................................................15

Conclusion....................................................................................................................................16

References.....................................................................................................................................17

Section I

[P1] Explain why management accounting is important in the decision-making process for

improving the performance of the company.

Management accounting is a broader concept as it involves various aspects. Each and every

branch of study of management accounting has different implications and aims to achieve

organizational goals and objectives. The formulation and implementation of management

accounting will help all the levels of management working within an organizational structure.

Role and significance of the management accounting in the decision making the process so that

the overall performance of the company can be improved are as follow:

1. The important and prominent feature of management accounting namely, financial accounting, is

used by the top-level management to take various crucial decisions (Ada & Ghaffarzadeh, 2015).

With the proper implementation of financial accounting, the true and actual profitability can be

determined. This will also help to satisfy the requirements of all the stakeholders as they are

always interested in the business affairs of the concerned business enterprise.

2. With the assistance of management accounting, the per unit cost can be determined and

identified. This information relating to per unit cost helps to take crucial decisions regarding cost

control and cost reduction to the extent possible (Guga & Musa, 2015). The management

accounting facilitates to take compare per unit cost with the rival firms operating in the business

environment.

3. The management accounting helps to identify the unprofitable segment or unprofitable

individual product or service as a result of which the overall profit can be achieved. As such,

through management accounting, the top level can focus on core activities so that overall

objectives can be achieved.

4. The implementation of management accounting will help to diversify the business so that it can

prosper and flourish and achieve competitive advantage over its rival firms. As such, the top

[P1] Explain why management accounting is important in the decision-making process for

improving the performance of the company.

Management accounting is a broader concept as it involves various aspects. Each and every

branch of study of management accounting has different implications and aims to achieve

organizational goals and objectives. The formulation and implementation of management

accounting will help all the levels of management working within an organizational structure.

Role and significance of the management accounting in the decision making the process so that

the overall performance of the company can be improved are as follow:

1. The important and prominent feature of management accounting namely, financial accounting, is

used by the top-level management to take various crucial decisions (Ada & Ghaffarzadeh, 2015).

With the proper implementation of financial accounting, the true and actual profitability can be

determined. This will also help to satisfy the requirements of all the stakeholders as they are

always interested in the business affairs of the concerned business enterprise.

2. With the assistance of management accounting, the per unit cost can be determined and

identified. This information relating to per unit cost helps to take crucial decisions regarding cost

control and cost reduction to the extent possible (Guga & Musa, 2015). The management

accounting facilitates to take compare per unit cost with the rival firms operating in the business

environment.

3. The management accounting helps to identify the unprofitable segment or unprofitable

individual product or service as a result of which the overall profit can be achieved. As such,

through management accounting, the top level can focus on core activities so that overall

objectives can be achieved.

4. The implementation of management accounting will help to diversify the business so that it can

prosper and flourish and achieve competitive advantage over its rival firms. As such, the top

level management can take crucial decisions which will help to capture market share in the

market.

5. Under management accounting, different types of budgets are prepared by the all the segments

operating or functioning in the business enterprise (Breuer, et. al., 2013). Preparation of budget

helps to establish standards or benchmarks for every department which it aims to achieve within

a specified time span.

6. The information generated from the application of several costing principles can be analyzed on

the basis of which several decisions can be taken. The application of costing principles need to

be carefully applied by the management to get the accurate and correct result. For this purpose,

the cost accountant should be well skilled and have expert knowledge.

7. The management accounting helps to measure the performance by identifying key performance

indicators. Measuring the actual performance will help in the decision-making process. If the

management is unsatisfied with any particular segment or department, the management can take

suitable and appropriate decision against the responsible officer.

market.

5. Under management accounting, different types of budgets are prepared by the all the segments

operating or functioning in the business enterprise (Breuer, et. al., 2013). Preparation of budget

helps to establish standards or benchmarks for every department which it aims to achieve within

a specified time span.

6. The information generated from the application of several costing principles can be analyzed on

the basis of which several decisions can be taken. The application of costing principles need to

be carefully applied by the management to get the accurate and correct result. For this purpose,

the cost accountant should be well skilled and have expert knowledge.

7. The management accounting helps to measure the performance by identifying key performance

indicators. Measuring the actual performance will help in the decision-making process. If the

management is unsatisfied with any particular segment or department, the management can take

suitable and appropriate decision against the responsible officer.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

[P2] Explain three different types of management accounting systems used for

management accounting reporting.

Under management accounting systems, different types of reports are prepared so as to take

several crucial and strategic decisions. All these reports play a major and dominant role in

management accounting reporting. These reports come under management accounting reporting.

Some of the major three different types of management accounting systems are listed below:

Image 1: Types of management accounting systems used in management accounting reporting

Source: By Author,2018

From the above image, it can be observed that there are three predominant types of management

accounting system implementation of which is crucial in almost every business enterprise be it a

manufacturing concern or a non-profit organization. As such, these are the basic classification of

management accounting system which needs to exist in every organization and industry. These

are explained below one by one:

Managerial accounting: This branch of management accounting is planning concept. As such,

the managerial accounting is implemented at the top level or the strategic level of management.

The objective of managerial accounting is to regulate and control the business operations in a

lucid and understandable manner (Guga & Musa, 2015).

Types of management accounting

systems:

Managerial

accounting

Inventory

accounting Cost

accounting

management accounting reporting.

Under management accounting systems, different types of reports are prepared so as to take

several crucial and strategic decisions. All these reports play a major and dominant role in

management accounting reporting. These reports come under management accounting reporting.

Some of the major three different types of management accounting systems are listed below:

Image 1: Types of management accounting systems used in management accounting reporting

Source: By Author,2018

From the above image, it can be observed that there are three predominant types of management

accounting system implementation of which is crucial in almost every business enterprise be it a

manufacturing concern or a non-profit organization. As such, these are the basic classification of

management accounting system which needs to exist in every organization and industry. These

are explained below one by one:

Managerial accounting: This branch of management accounting is planning concept. As such,

the managerial accounting is implemented at the top level or the strategic level of management.

The objective of managerial accounting is to regulate and control the business operations in a

lucid and understandable manner (Guga & Musa, 2015).

Types of management accounting

systems:

Managerial

accounting

Inventory

accounting Cost

accounting

Inventory accounting: The inventory accounting deals with the maintenance of records relating

to stock. Under this branch of study, inventory is classified into various categories namely raw

materials, work in progress, finished goods and spare parts. The inventory accounting can be

done to have a better control on inventory and helps in identification of pilferage or loss of

inventory (Breuer, et. al., 2013).

Cost accounting: The cost accounting deals with the costing principles of products and services

dealt with by the concerned business enterprise. As such, it helps in the determination of actual

cost incurred to produce the products or services.

[P3] Critically evaluate the benefits of types of management accounting systems and their

application within an organizational context.

Benefits of Managerial accounting:

1. The managerial accountant prepares and presents different types of managerial reports including

budget reports, performance reports and cost reports. These reports are strictly meant for the

internal purpose.

2. Under managerial reporting, generally, all the reports prepared the managerial accountant serves

the needs and requirements of the board of directors. This is the major difference between

managerial accounting and financial accounting. In financial accounting, the information is

generated to serve the needs of shareholders (Sukhia, et. al., 2014).

Benefits of Inventory accounting:

1. With the assistance of inventory accounting, the physical verification of inventory can be done

easily. This helps to identify and loophole in the inventory management system.

2. The data and information obtained through inventory management system need to be compared

with the records maintained online or in the books of the store. The difference between the

records and physical verification can arise due to error or mistake in records maintained or

counting during verification (Omotayo, 2015).

to stock. Under this branch of study, inventory is classified into various categories namely raw

materials, work in progress, finished goods and spare parts. The inventory accounting can be

done to have a better control on inventory and helps in identification of pilferage or loss of

inventory (Breuer, et. al., 2013).

Cost accounting: The cost accounting deals with the costing principles of products and services

dealt with by the concerned business enterprise. As such, it helps in the determination of actual

cost incurred to produce the products or services.

[P3] Critically evaluate the benefits of types of management accounting systems and their

application within an organizational context.

Benefits of Managerial accounting:

1. The managerial accountant prepares and presents different types of managerial reports including

budget reports, performance reports and cost reports. These reports are strictly meant for the

internal purpose.

2. Under managerial reporting, generally, all the reports prepared the managerial accountant serves

the needs and requirements of the board of directors. This is the major difference between

managerial accounting and financial accounting. In financial accounting, the information is

generated to serve the needs of shareholders (Sukhia, et. al., 2014).

Benefits of Inventory accounting:

1. With the assistance of inventory accounting, the physical verification of inventory can be done

easily. This helps to identify and loophole in the inventory management system.

2. The data and information obtained through inventory management system need to be compared

with the records maintained online or in the books of the store. The difference between the

records and physical verification can arise due to error or mistake in records maintained or

counting during verification (Omotayo, 2015).

Benefits of Cost accounting:

1. The cost accounting helps to correctly determine the per unit cost of all the products and

services. For this purpose, the allocation of cost needs to be done to the various products. This

can only be done only if the cost accountant has proper knowledge of cost components (Ada &

Ghaffarzadeh, 2015).

2. With the implementation of cost accounting system in the organizational structure in any

business enterprise, the segregation of cost into various parts can be done easily. Cost can be

classified into various categories depending on various factors. For instance, the cost can be

segregated into fixed and variable. Other classification can be manufacturing and selling and

distribution expenses.

1. The cost accounting helps to correctly determine the per unit cost of all the products and

services. For this purpose, the allocation of cost needs to be done to the various products. This

can only be done only if the cost accountant has proper knowledge of cost components (Ada &

Ghaffarzadeh, 2015).

2. With the implementation of cost accounting system in the organizational structure in any

business enterprise, the segregation of cost into various parts can be done easily. Cost can be

classified into various categories depending on various factors. For instance, the cost can be

segregated into fixed and variable. Other classification can be manufacturing and selling and

distribution expenses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

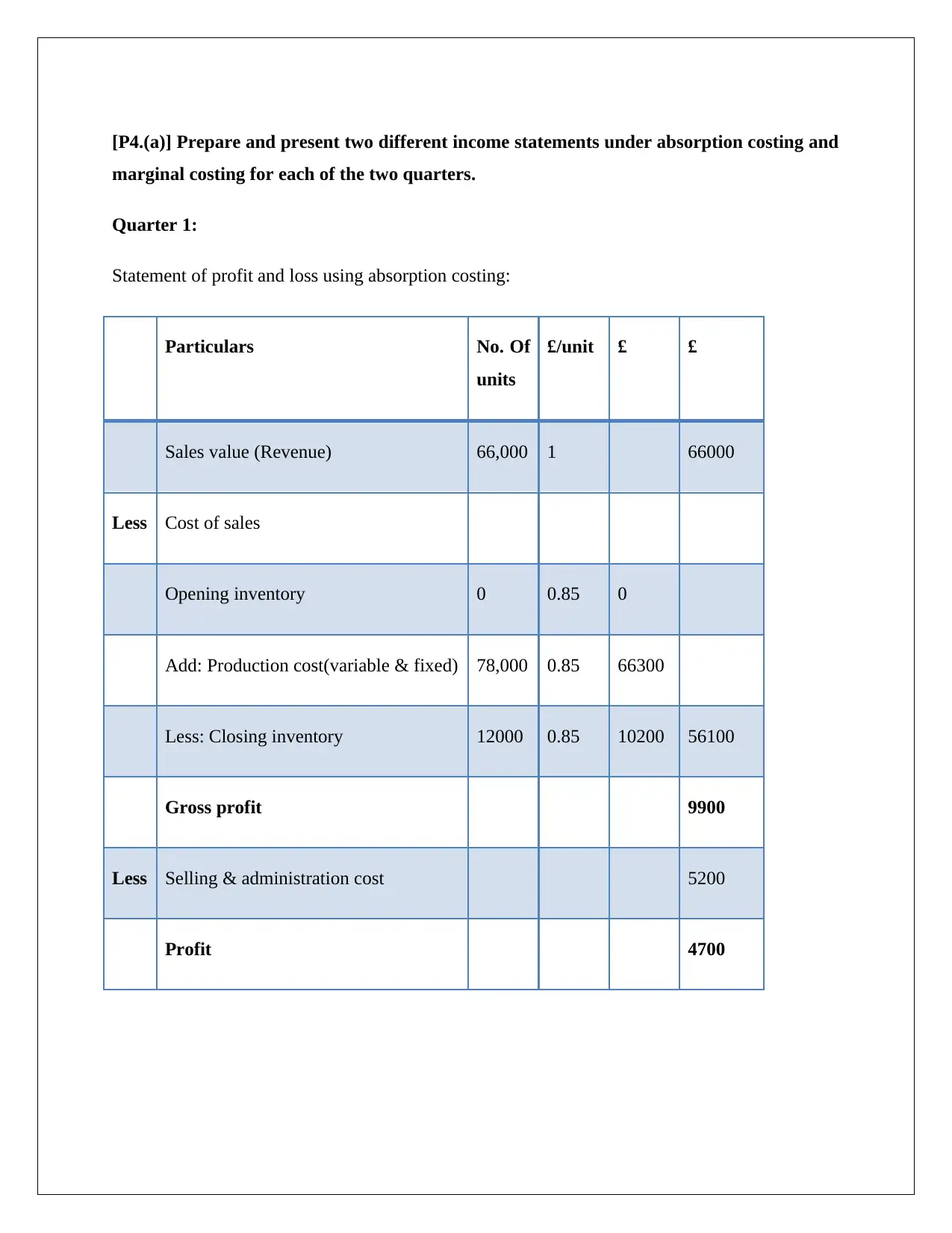

[P4.(a)] Prepare and present two different income statements under absorption costing and

marginal costing for each of the two quarters.

Quarter 1:

Statement of profit and loss using absorption costing:

Particulars No. Of

units

£/unit £ £

Sales value (Revenue) 66,000 1 66000

Less Cost of sales

Opening inventory 0 0.85 0

Add: Production cost(variable & fixed) 78,000 0.85 66300

Less: Closing inventory 12000 0.85 10200 56100

Gross profit 9900

Less Selling & administration cost 5200

Profit 4700

marginal costing for each of the two quarters.

Quarter 1:

Statement of profit and loss using absorption costing:

Particulars No. Of

units

£/unit £ £

Sales value (Revenue) 66,000 1 66000

Less Cost of sales

Opening inventory 0 0.85 0

Add: Production cost(variable & fixed) 78,000 0.85 66300

Less: Closing inventory 12000 0.85 10200 56100

Gross profit 9900

Less Selling & administration cost 5200

Profit 4700

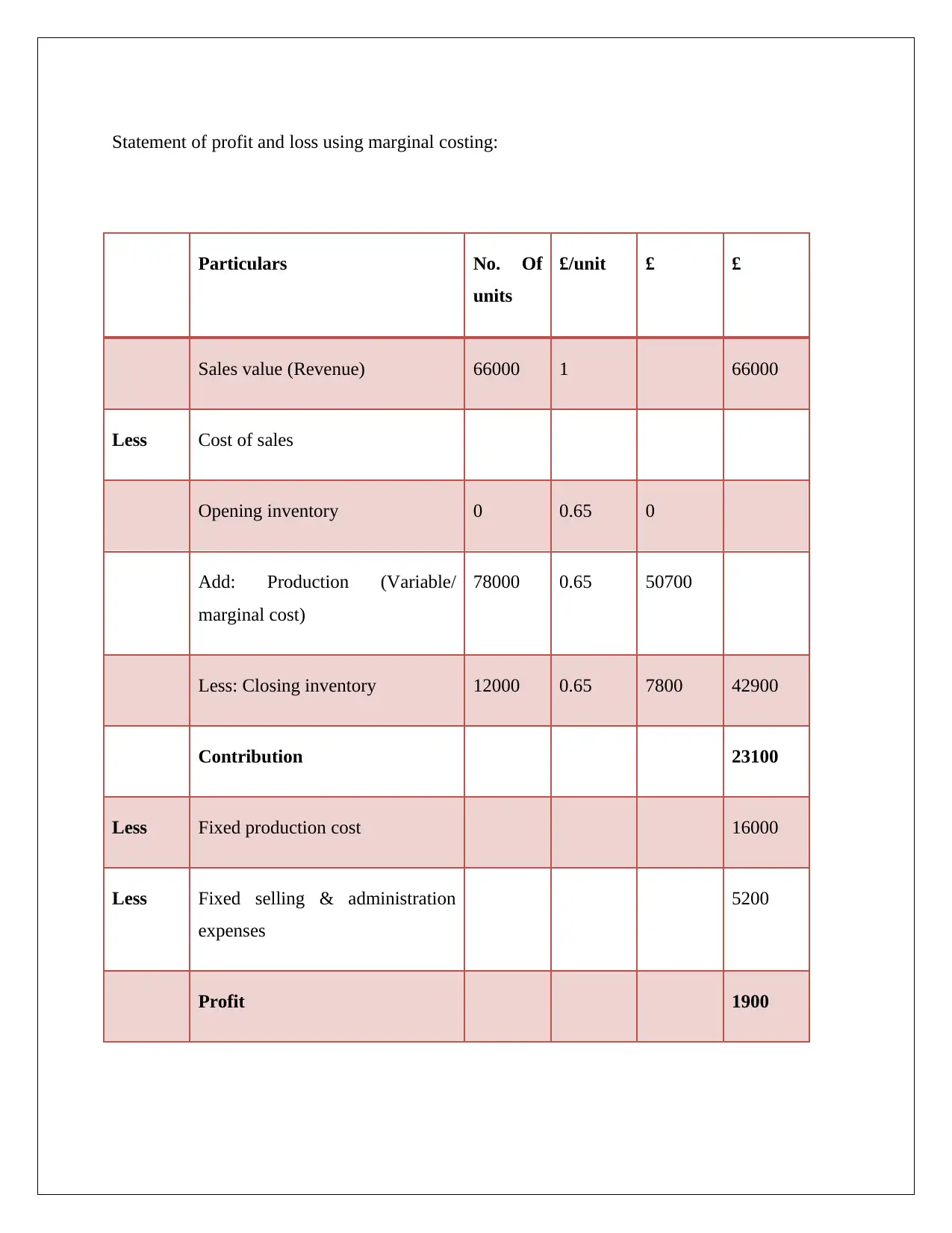

Statement of profit and loss using marginal costing:

Particulars No. Of

units

£/unit £ £

Sales value (Revenue) 66000 1 66000

Less Cost of sales

Opening inventory 0 0.65 0

Add: Production (Variable/

marginal cost)

78000 0.65 50700

Less: Closing inventory 12000 0.65 7800 42900

Contribution 23100

Less Fixed production cost 16000

Less Fixed selling & administration

expenses

5200

Profit 1900

Particulars No. Of

units

£/unit £ £

Sales value (Revenue) 66000 1 66000

Less Cost of sales

Opening inventory 0 0.65 0

Add: Production (Variable/

marginal cost)

78000 0.65 50700

Less: Closing inventory 12000 0.65 7800 42900

Contribution 23100

Less Fixed production cost 16000

Less Fixed selling & administration

expenses

5200

Profit 1900

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

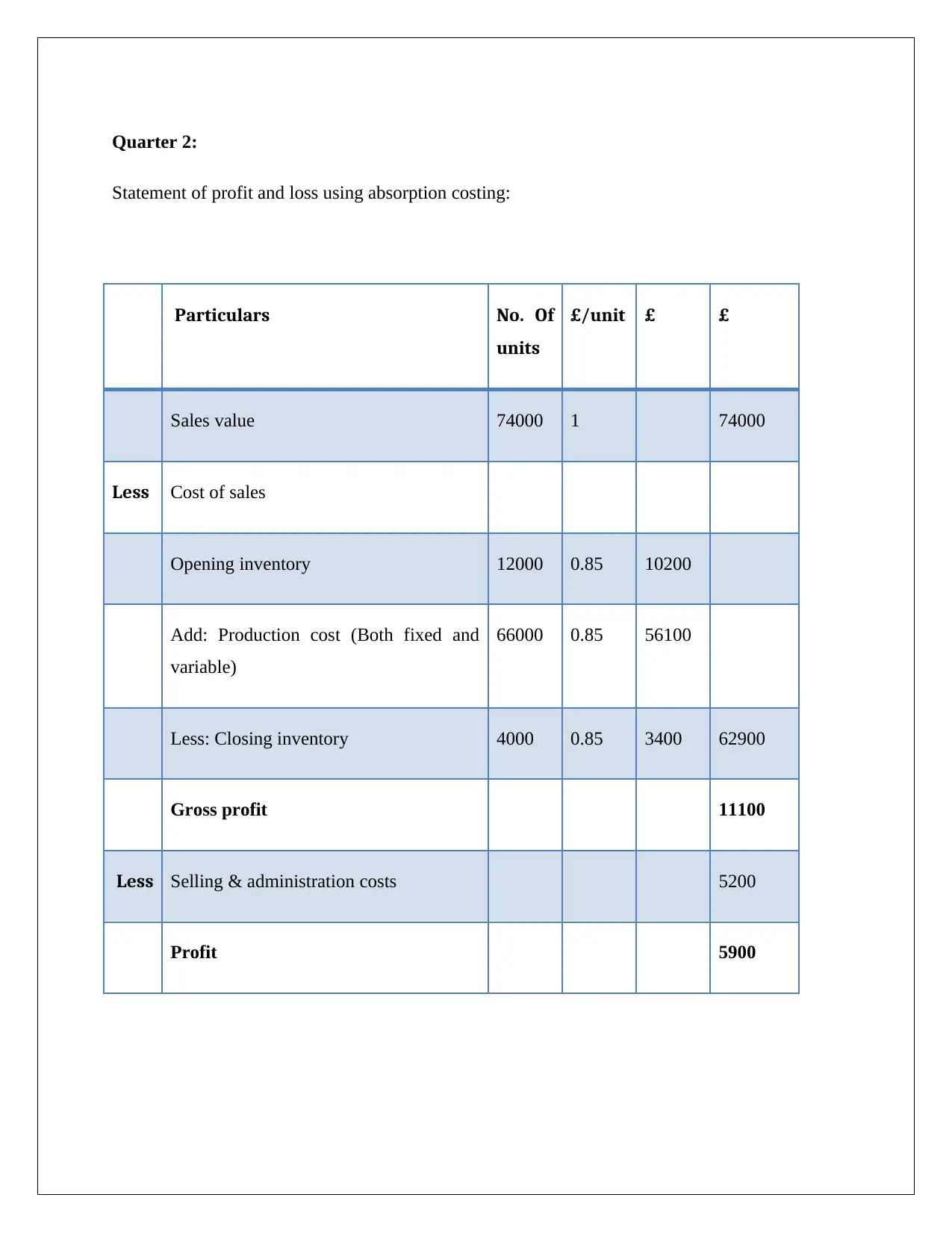

Quarter 2:

Statement of profit and loss using absorption costing:

Particulars No. Of

units

£/unit £ £

Sales value 74000 1 74000

Less Cost of sales

Opening inventory 12000 0.85 10200

Add: Production cost (Both fixed and

variable)

66000 0.85 56100

Less: Closing inventory 4000 0.85 3400 62900

Gross profit 11100

Less Selling & administration costs 5200

Profit 5900

Statement of profit and loss using absorption costing:

Particulars No. Of

units

£/unit £ £

Sales value 74000 1 74000

Less Cost of sales

Opening inventory 12000 0.85 10200

Add: Production cost (Both fixed and

variable)

66000 0.85 56100

Less: Closing inventory 4000 0.85 3400 62900

Gross profit 11100

Less Selling & administration costs 5200

Profit 5900

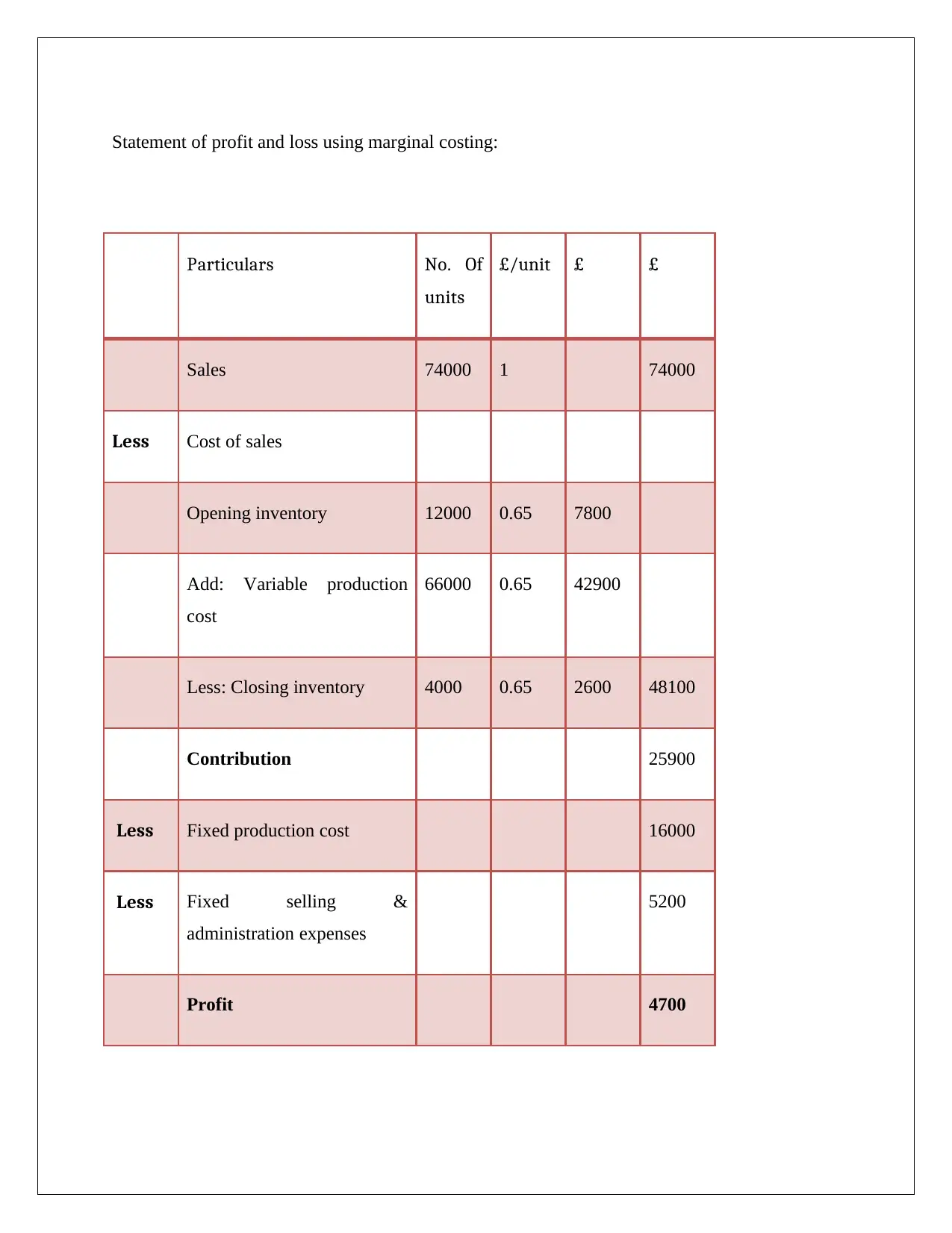

Statement of profit and loss using marginal costing:

Particulars No. Of

units

£/unit £ £

Sales 74000 1 74000

Less Cost of sales

Opening inventory 12000 0.65 7800

Add: Variable production

cost

66000 0.65 42900

Less: Closing inventory 4000 0.65 2600 48100

Contribution 25900

Less Fixed production cost 16000

Less Fixed selling &

administration expenses

5200

Profit 4700

Particulars No. Of

units

£/unit £ £

Sales 74000 1 74000

Less Cost of sales

Opening inventory 12000 0.65 7800

Add: Variable production

cost

66000 0.65 42900

Less: Closing inventory 4000 0.65 2600 48100

Contribution 25900

Less Fixed production cost 16000

Less Fixed selling &

administration expenses

5200

Profit 4700

[P4.(b)] Explain with supportive calculations, why the profits under techniques are

different.

The costing income statement can be prepared either as per absorption costing or as per marginal

costing. However, the income computed as per both the costing approach will be different. This

is because the costs are classified according to different criteria or perspective under both the

costing approach (Sukhia, et. al., 2014).

Under absorption costing approach, the costs are classified into production and other operations,

for instance, selling and distribution costs. Accordingly, all the production cost, whether fixed

and variable will be included in the production cost. As a result, the stocks are valued at

production cost (Omotayo, 2015).

Similarly, under marginal costing, costs are classified into the variable and fixed cost. Under

variable costing, all the marginal costs covering both the production related and selling expenses

are added. Stocks under marginal costing are valued at variable cost, including both production

cost and variable cost.

different.

The costing income statement can be prepared either as per absorption costing or as per marginal

costing. However, the income computed as per both the costing approach will be different. This

is because the costs are classified according to different criteria or perspective under both the

costing approach (Sukhia, et. al., 2014).

Under absorption costing approach, the costs are classified into production and other operations,

for instance, selling and distribution costs. Accordingly, all the production cost, whether fixed

and variable will be included in the production cost. As a result, the stocks are valued at

production cost (Omotayo, 2015).

Similarly, under marginal costing, costs are classified into the variable and fixed cost. Under

variable costing, all the marginal costs covering both the production related and selling expenses

are added. Stocks under marginal costing are valued at variable cost, including both production

cost and variable cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

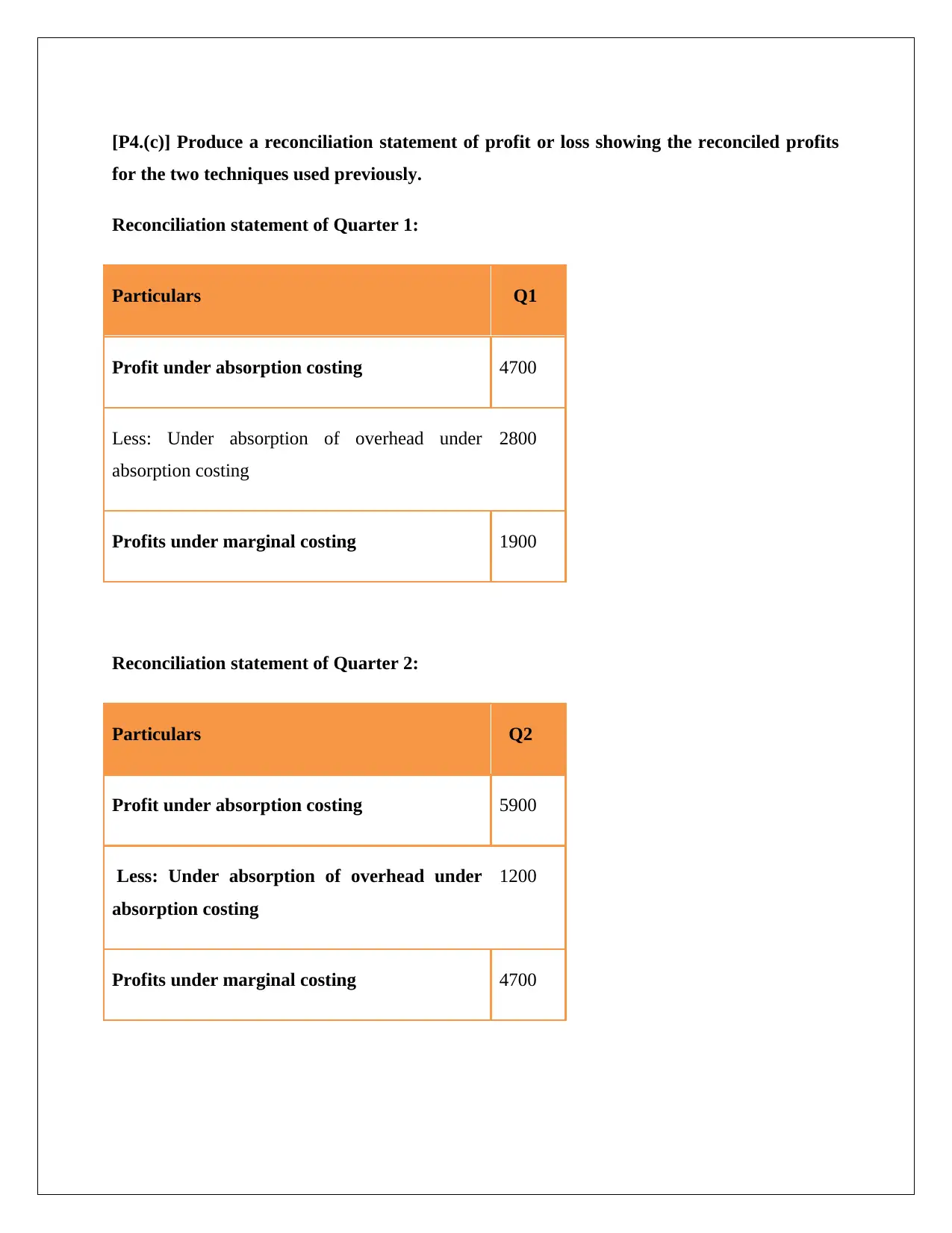

[P4.(c)] Produce a reconciliation statement of profit or loss showing the reconciled profits

for the two techniques used previously.

Reconciliation statement of Quarter 1:

Particulars Q1

Profit under absorption costing 4700

Less: Under absorption of overhead under

absorption costing

2800

Profits under marginal costing 1900

Reconciliation statement of Quarter 2:

Particulars Q2

Profit under absorption costing 5900

Less: Under absorption of overhead under

absorption costing

1200

Profits under marginal costing 4700

for the two techniques used previously.

Reconciliation statement of Quarter 1:

Particulars Q1

Profit under absorption costing 4700

Less: Under absorption of overhead under

absorption costing

2800

Profits under marginal costing 1900

Reconciliation statement of Quarter 2:

Particulars Q2

Profit under absorption costing 5900

Less: Under absorption of overhead under

absorption costing

1200

Profits under marginal costing 4700

The above reconciliation statements of both the quarters explain the difference between the

income computed as per absorption costing and marginal costing. It can be observed that in both

the quarters the difference arises because of the under absorption of overhead under absorption

costing.

income computed as per absorption costing and marginal costing. It can be observed that in both

the quarters the difference arises because of the under absorption of overhead under absorption

costing.

Section II

[Part A] Compare and contrast three different planning tools used in management

accounting. Analyse and evaluate how the use of planning tools for accounting respond to

solving financial problems to lead the organization.

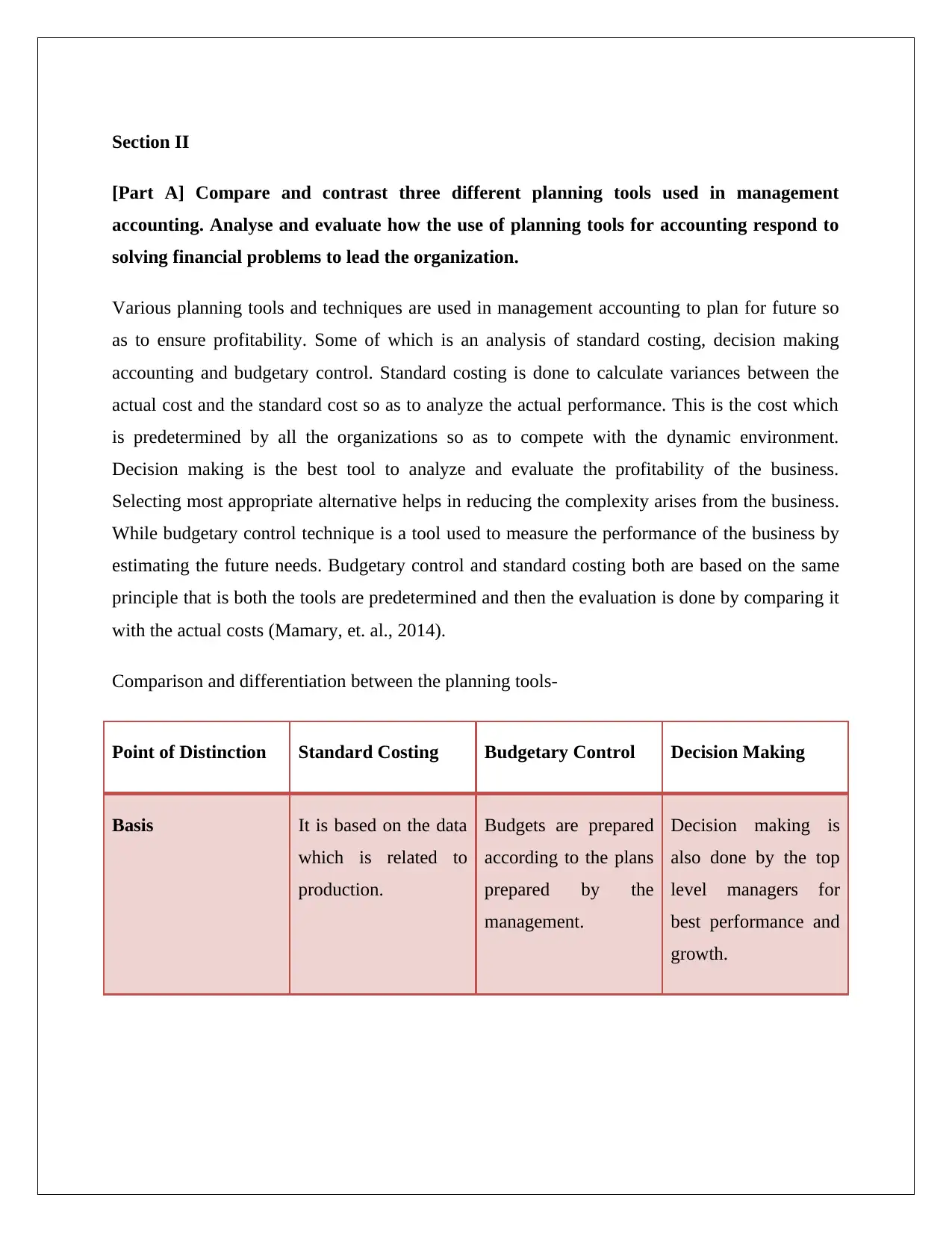

Various planning tools and techniques are used in management accounting to plan for future so

as to ensure profitability. Some of which is an analysis of standard costing, decision making

accounting and budgetary control. Standard costing is done to calculate variances between the

actual cost and the standard cost so as to analyze the actual performance. This is the cost which

is predetermined by all the organizations so as to compete with the dynamic environment.

Decision making is the best tool to analyze and evaluate the profitability of the business.

Selecting most appropriate alternative helps in reducing the complexity arises from the business.

While budgetary control technique is a tool used to measure the performance of the business by

estimating the future needs. Budgetary control and standard costing both are based on the same

principle that is both the tools are predetermined and then the evaluation is done by comparing it

with the actual costs (Mamary, et. al., 2014).

Comparison and differentiation between the planning tools-

Point of Distinction Standard Costing Budgetary Control Decision Making

Basis It is based on the data

which is related to

production.

Budgets are prepared

according to the plans

prepared by the

management.

Decision making is

also done by the top

level managers for

best performance and

growth.

[Part A] Compare and contrast three different planning tools used in management

accounting. Analyse and evaluate how the use of planning tools for accounting respond to

solving financial problems to lead the organization.

Various planning tools and techniques are used in management accounting to plan for future so

as to ensure profitability. Some of which is an analysis of standard costing, decision making

accounting and budgetary control. Standard costing is done to calculate variances between the

actual cost and the standard cost so as to analyze the actual performance. This is the cost which

is predetermined by all the organizations so as to compete with the dynamic environment.

Decision making is the best tool to analyze and evaluate the profitability of the business.

Selecting most appropriate alternative helps in reducing the complexity arises from the business.

While budgetary control technique is a tool used to measure the performance of the business by

estimating the future needs. Budgetary control and standard costing both are based on the same

principle that is both the tools are predetermined and then the evaluation is done by comparing it

with the actual costs (Mamary, et. al., 2014).

Comparison and differentiation between the planning tools-

Point of Distinction Standard Costing Budgetary Control Decision Making

Basis It is based on the data

which is related to

production.

Budgets are prepared

according to the plans

prepared by the

management.

Decision making is

also done by the top

level managers for

best performance and

growth.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

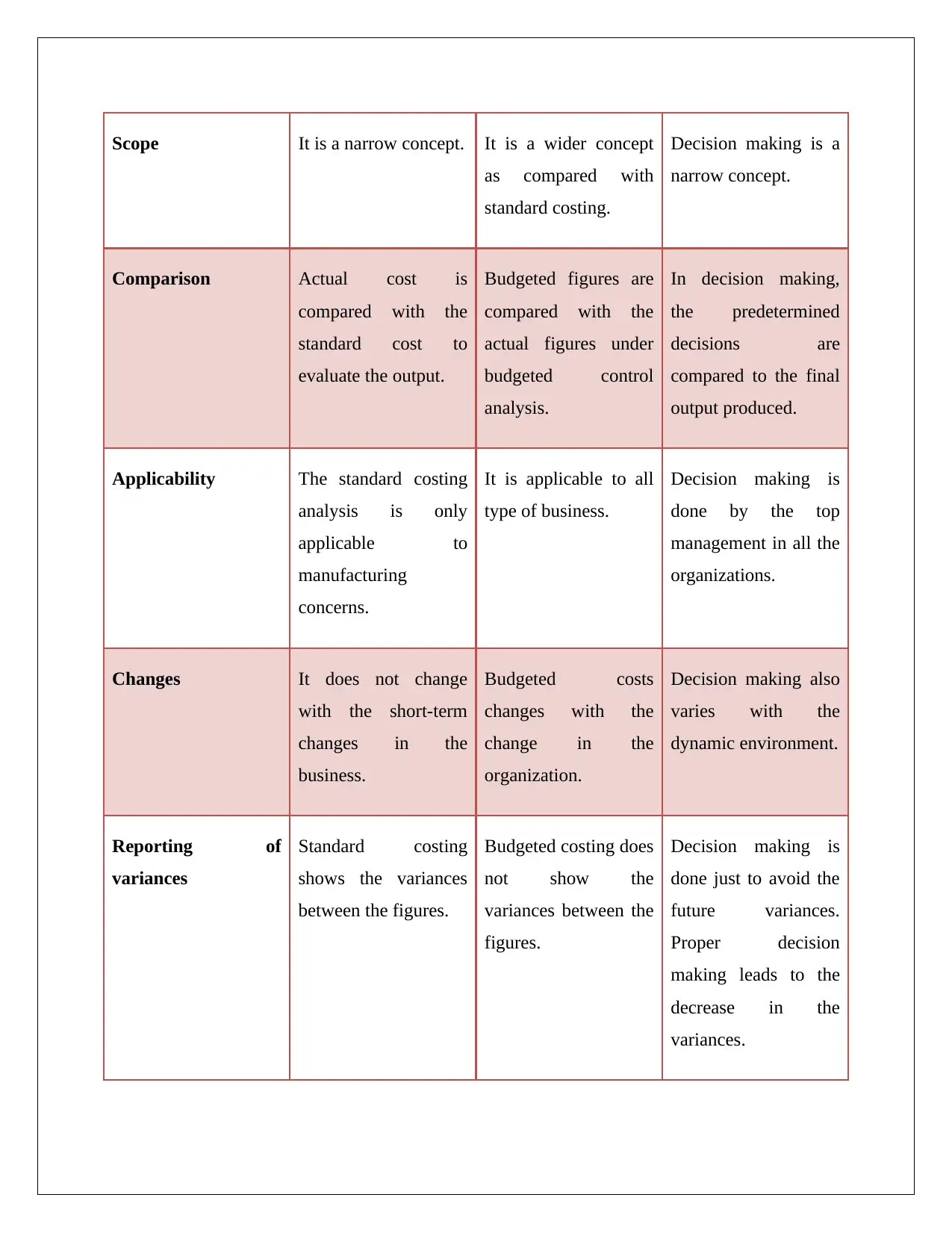

Scope It is a narrow concept. It is a wider concept

as compared with

standard costing.

Decision making is a

narrow concept.

Comparison Actual cost is

compared with the

standard cost to

evaluate the output.

Budgeted figures are

compared with the

actual figures under

budgeted control

analysis.

In decision making,

the predetermined

decisions are

compared to the final

output produced.

Applicability The standard costing

analysis is only

applicable to

manufacturing

concerns.

It is applicable to all

type of business.

Decision making is

done by the top

management in all the

organizations.

Changes It does not change

with the short-term

changes in the

business.

Budgeted costs

changes with the

change in the

organization.

Decision making also

varies with the

dynamic environment.

Reporting of

variances

Standard costing

shows the variances

between the figures.

Budgeted costing does

not show the

variances between the

figures.

Decision making is

done just to avoid the

future variances.

Proper decision

making leads to the

decrease in the

variances.

as compared with

standard costing.

Decision making is a

narrow concept.

Comparison Actual cost is

compared with the

standard cost to

evaluate the output.

Budgeted figures are

compared with the

actual figures under

budgeted control

analysis.

In decision making,

the predetermined

decisions are

compared to the final

output produced.

Applicability The standard costing

analysis is only

applicable to

manufacturing

concerns.

It is applicable to all

type of business.

Decision making is

done by the top

management in all the

organizations.

Changes It does not change

with the short-term

changes in the

business.

Budgeted costs

changes with the

change in the

organization.

Decision making also

varies with the

dynamic environment.

Reporting of

variances

Standard costing

shows the variances

between the figures.

Budgeted costing does

not show the

variances between the

figures.

Decision making is

done just to avoid the

future variances.

Proper decision

making leads to the

decrease in the

variances.

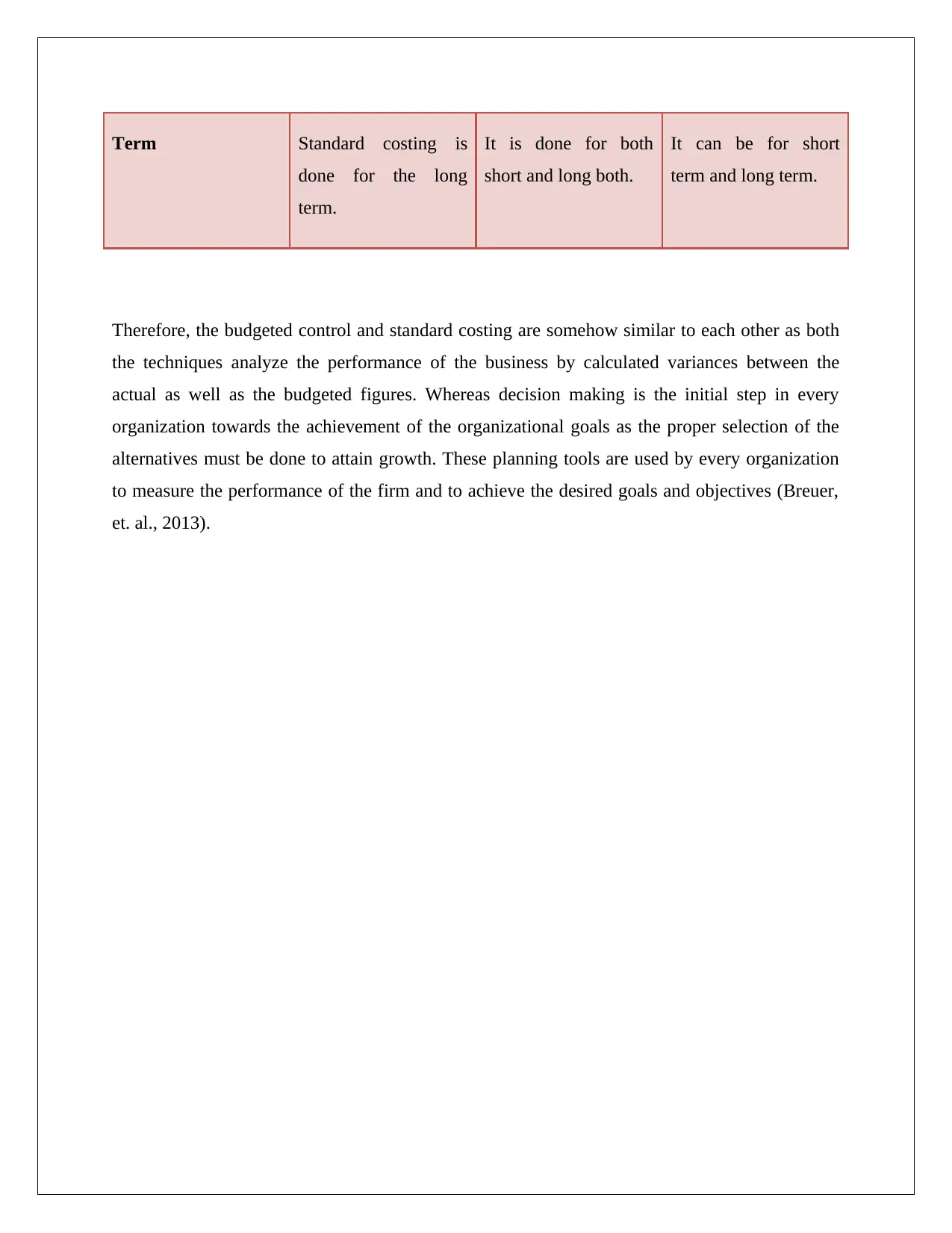

Term Standard costing is

done for the long

term.

It is done for both

short and long both.

It can be for short

term and long term.

Therefore, the budgeted control and standard costing are somehow similar to each other as both

the techniques analyze the performance of the business by calculated variances between the

actual as well as the budgeted figures. Whereas decision making is the initial step in every

organization towards the achievement of the organizational goals as the proper selection of the

alternatives must be done to attain growth. These planning tools are used by every organization

to measure the performance of the firm and to achieve the desired goals and objectives (Breuer,

et. al., 2013).

done for the long

term.

It is done for both

short and long both.

It can be for short

term and long term.

Therefore, the budgeted control and standard costing are somehow similar to each other as both

the techniques analyze the performance of the business by calculated variances between the

actual as well as the budgeted figures. Whereas decision making is the initial step in every

organization towards the achievement of the organizational goals as the proper selection of the

alternatives must be done to attain growth. These planning tools are used by every organization

to measure the performance of the firm and to achieve the desired goals and objectives (Breuer,

et. al., 2013).

[Part B] Compare ways in which management accounting is applied. Analyse how, in

responding to financial problems, management accounting can lead organizations to

sustainable success.

Application of the management accounting is the way through which the organizations can face

the challenges in the environment and which will help the organizations to get rid of the financial

problems. With the implementation of the management accounting, the quality of the decision

making and the effectiveness will lead to superior performance. Strategic planning is done to

analyze the current and the future allocation of the resources. Organisations use various tools to

deal with the financial problems (Mamary, et. al., 2014).

Benchmarks are set to compare the performance of the products and services. It comprises of two

things to be considered while implementing the benchmark these are finding the appropriate one

and ensuring that the benchmark is valuable so that it can be easily compared. KPI’s is another

tool to respond to financial problems as this implies how the organization is competing with the

external environment according to the plan. These can be both financial as well as nonfinancial.

Financial KPI’s include cost, revenue, and profits whereas nonfinancial KPI’s include reliability,

flexibility, innovation, and performance (Mamary, et. al., 2014).

Financial governance can also be used as a tool because it is concerned with the financial

decision which helps to attain accountability. In the manufacturing industries application of the

management accounting is important as with this the earnings per share and the profit after tax

can easily be evaluated whereas in the real estate sector it is required to calculate the production

cost and the cost incurred in producing the particular product with that it also implies the value

of work in progress (Ada & Ghaffarzadeh, 2015). This disclosure will lead to the effective

decision making and ensure the increase in performance. To achieve the sustainable growth and

respond appropriately to financial problem, organizations adopt various strategies and business

models so that the social and economic challenges can be faced. Many companies agreed that

they have various skills to compete in the challenging environment.

According to the survey conducted sixty-seven agreed that combining of social and

environmental factors into decision-making process leads to the financial benefits. Companies

responding to financial problems, management accounting can lead organizations to

sustainable success.

Application of the management accounting is the way through which the organizations can face

the challenges in the environment and which will help the organizations to get rid of the financial

problems. With the implementation of the management accounting, the quality of the decision

making and the effectiveness will lead to superior performance. Strategic planning is done to

analyze the current and the future allocation of the resources. Organisations use various tools to

deal with the financial problems (Mamary, et. al., 2014).

Benchmarks are set to compare the performance of the products and services. It comprises of two

things to be considered while implementing the benchmark these are finding the appropriate one

and ensuring that the benchmark is valuable so that it can be easily compared. KPI’s is another

tool to respond to financial problems as this implies how the organization is competing with the

external environment according to the plan. These can be both financial as well as nonfinancial.

Financial KPI’s include cost, revenue, and profits whereas nonfinancial KPI’s include reliability,

flexibility, innovation, and performance (Mamary, et. al., 2014).

Financial governance can also be used as a tool because it is concerned with the financial

decision which helps to attain accountability. In the manufacturing industries application of the

management accounting is important as with this the earnings per share and the profit after tax

can easily be evaluated whereas in the real estate sector it is required to calculate the production

cost and the cost incurred in producing the particular product with that it also implies the value

of work in progress (Ada & Ghaffarzadeh, 2015). This disclosure will lead to the effective

decision making and ensure the increase in performance. To achieve the sustainable growth and

respond appropriately to financial problem, organizations adopt various strategies and business

models so that the social and economic challenges can be faced. Many companies agreed that

they have various skills to compete in the challenging environment.

According to the survey conducted sixty-seven agreed that combining of social and

environmental factors into decision-making process leads to the financial benefits. Companies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which use sustainability concerns believe that support strategic decision making is excessively

used by the organizations as compared with the risk management decisions (Guga & Musa,

2015). Through risk management decisions the firms can easily predict the risk factor and the

operational issues involved. However, with the adaptation of this decision making the

organizations will implement the risk-free decision-making strategies so as to respond to

financial problems faced due to the economic factors.

Development of the KPI’s and the setting or the using of benchmark will help in achieving the

strategic and the sustainable growth. Senior management is responsible for the long-term

sustainable success with the goal to manage change and generate value for shareholders. This

will identify the opportunities for managing the costs and risk (Guga & Musa, 2015). So this can

be seen that with the adoption of the sustainability the companies can evaluate the overall

performance and with that practice, the effectiveness of the management accounting functions

can be achieved. Management accounting is important for taking strategic decisions. Therefore,

the management accounting is essential to deal with the financial problems prevailing in the

business.

used by the organizations as compared with the risk management decisions (Guga & Musa,

2015). Through risk management decisions the firms can easily predict the risk factor and the

operational issues involved. However, with the adaptation of this decision making the

organizations will implement the risk-free decision-making strategies so as to respond to

financial problems faced due to the economic factors.

Development of the KPI’s and the setting or the using of benchmark will help in achieving the

strategic and the sustainable growth. Senior management is responsible for the long-term

sustainable success with the goal to manage change and generate value for shareholders. This

will identify the opportunities for managing the costs and risk (Guga & Musa, 2015). So this can

be seen that with the adoption of the sustainability the companies can evaluate the overall

performance and with that practice, the effectiveness of the management accounting functions

can be achieved. Management accounting is important for taking strategic decisions. Therefore,

the management accounting is essential to deal with the financial problems prevailing in the

business.

Conclusion

From the discussion throughout the report, it can be concluded that management accounting is

essential for every business enterprise. The report also covers the income statement as per

absorption costing and marginal costing. This is done to find out the difference in income

statements prepared as per two costing approaches. Besides, an attempt has been made to

understand the different types of management accounting. Understanding of these aspects will

help to find the solution to various financial problems being faced by any business enterprise.

Accordingly, the report deals with the implication of management accounting in responding to

financial problems. This will help to retain existing customers as well as attract or entice new

customers.

From the discussion throughout the report, it can be concluded that management accounting is

essential for every business enterprise. The report also covers the income statement as per

absorption costing and marginal costing. This is done to find out the difference in income

statements prepared as per two costing approaches. Besides, an attempt has been made to

understand the different types of management accounting. Understanding of these aspects will

help to find the solution to various financial problems being faced by any business enterprise.

Accordingly, the report deals with the implication of management accounting in responding to

financial problems. This will help to retain existing customers as well as attract or entice new

customers.

References

Ada, S., & Ghaffarzadeh, M., 2015. Decision Making Based On Management

Information System And Decision Support System. International Journal of Economics,

Commerce, and Management.

Amirya, M., Djamhuri, A., & Ludigdo, U., 2014. Development of Accounting and

Budget System of General Services Board in Universitas Brawijaya: Study of

Interpretive. International Journal of Humanities and Social Science.

Anna, A., 2015. Strategic Management Tools and Techniques and Organizational

Performance: Findings from the Czech Republic. Journal of Competitiveness.

Breuer, A., Frunmusanu, M. L., & Manciu, A., 2013. The role of management

accounting in the decision-making process: case study caraş Severin county.

Annales Universitatis.

Guga, E., & Musa, O., 2015. Inventory management through EOQ model. International

Journal of Economics, Commerce, and Management.

Mamary, Y. H. A., Aziati, N., & Shamsuddin, A., 2014. The Meaning of Management

Information Systems and its Role in Telecommunication Companies in Yemen. American

Journal of Software Engineering.

Omotayo, F.O., 2015. Knowledge Management as an important tool in Organisational

Management: A Review of Literature. University of Nebraska – Lincoln.

Sukhia, K.N., Khan, A.A., & Bano, M., 2014. Introducing Economic Order Quantity

Model for Inventory Control in Web-based Point of Sale Applications and Comparative

Analysis of Techniques for Demand Forecasting in Inventory Management. International

Journal of Computer Applications.

Ada, S., & Ghaffarzadeh, M., 2015. Decision Making Based On Management

Information System And Decision Support System. International Journal of Economics,

Commerce, and Management.

Amirya, M., Djamhuri, A., & Ludigdo, U., 2014. Development of Accounting and

Budget System of General Services Board in Universitas Brawijaya: Study of

Interpretive. International Journal of Humanities and Social Science.

Anna, A., 2015. Strategic Management Tools and Techniques and Organizational

Performance: Findings from the Czech Republic. Journal of Competitiveness.

Breuer, A., Frunmusanu, M. L., & Manciu, A., 2013. The role of management

accounting in the decision-making process: case study caraş Severin county.

Annales Universitatis.

Guga, E., & Musa, O., 2015. Inventory management through EOQ model. International

Journal of Economics, Commerce, and Management.

Mamary, Y. H. A., Aziati, N., & Shamsuddin, A., 2014. The Meaning of Management

Information Systems and its Role in Telecommunication Companies in Yemen. American

Journal of Software Engineering.

Omotayo, F.O., 2015. Knowledge Management as an important tool in Organisational

Management: A Review of Literature. University of Nebraska – Lincoln.

Sukhia, K.N., Khan, A.A., & Bano, M., 2014. Introducing Economic Order Quantity

Model for Inventory Control in Web-based Point of Sale Applications and Comparative

Analysis of Techniques for Demand Forecasting in Inventory Management. International

Journal of Computer Applications.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.