Management Accounting System and Techniques: Detailed Analysis Report

VerifiedAdded on 2020/12/10

|21

|6229

|444

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and techniques. It begins by defining management accounting and its essential requirements, differentiating it from financial accounting, and outlining key components like cost accounting, price optimization, inventory management, and job costing systems. The report then explores various management accounting reporting methods, including cost managerial accounting, budget reports, performance reports, and accounts receivable aging reports. Furthermore, it evaluates the benefits of management accounting systems within an organizational context, detailing how these systems aid in cost control, price optimization, inventory management, and overall financial planning. The report also delves into calculating costs using marginal and absorption costing, accurately applying accounting techniques, and producing financial reports for various business activities. Finally, it examines the advantages and disadvantages of planning tools, their application in budgeting and forecasting, and how management accounting adapts to and solves financial problems, ultimately leading organizations toward sustainable success.

MANAGEMENT

ACCOUNTING SYSTEM

AND TECHNIQUES

ACCOUNTING SYSTEM

AND TECHNIQUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO 1.................................................................................................................................................1

P1. Explaining management accounting and essential requirements of management ..........1

accounting system..................................................................................................................1

P2. Explaining different methods used for management accounting reporting.....................4

M1. Evaluating benefits of management accounting system and their application ..............5

within an organisational context.............................................................................................5

D1. Critically evaluating how management accounting systems and management .............6

accounting reporting is integrated within organisational processes.......................................6

LO 2.................................................................................................................................................7

P3. Calculate costs using appropriate techniques of cost analysis to prepare an ..................7

income statement using Marginal and Absorption Costs.......................................................7

M2. Accurately apply a range of management accounting techniques and produce ..........10

appropriate financial reporting documents...........................................................................10

D2. Produce financial reports that accurately apply and interpret data for a range of ........10

business activities.................................................................................................................10

LO 3...............................................................................................................................................11

P4. The advantages and disadvantages of different planning tools......................................11

M3. Use and application of different planning tools for preparing and forecasting ...........13

budgets..................................................................................................................................13

D3. Planning tools for accounting respond to solve financial problems..............................14

LO 4...............................................................................................................................................15

P5. Adapting management accounting systems to respond to financial problems...............15

M4. By responding to financial problems' management accounting can lead ....................16

organisation to sustainable success......................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO 1.................................................................................................................................................1

P1. Explaining management accounting and essential requirements of management ..........1

accounting system..................................................................................................................1

P2. Explaining different methods used for management accounting reporting.....................4

M1. Evaluating benefits of management accounting system and their application ..............5

within an organisational context.............................................................................................5

D1. Critically evaluating how management accounting systems and management .............6

accounting reporting is integrated within organisational processes.......................................6

LO 2.................................................................................................................................................7

P3. Calculate costs using appropriate techniques of cost analysis to prepare an ..................7

income statement using Marginal and Absorption Costs.......................................................7

M2. Accurately apply a range of management accounting techniques and produce ..........10

appropriate financial reporting documents...........................................................................10

D2. Produce financial reports that accurately apply and interpret data for a range of ........10

business activities.................................................................................................................10

LO 3...............................................................................................................................................11

P4. The advantages and disadvantages of different planning tools......................................11

M3. Use and application of different planning tools for preparing and forecasting ...........13

budgets..................................................................................................................................13

D3. Planning tools for accounting respond to solve financial problems..............................14

LO 4...............................................................................................................................................15

P5. Adapting management accounting systems to respond to financial problems...............15

M4. By responding to financial problems' management accounting can lead ....................16

organisation to sustainable success......................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting is a term which is concerned with the application of professional

knowledge and abilities in policy formulation, planning and controlling for the undertakings. It is

a process which involves concept of evaluating, identifying and preparing management accounts,

reports and business strategy to provide accurate, fair and timely information related to

financial, managerial and non-financial matter necessary for decision-making & also helps in

interpreting & communicating information to company's stakeholders (Otley, D., 2016). Further

more, the company has used different management accounting techniques for controlling cost,

making budgets. It has also explained that how a company uses different management

accounting tools in solving its financial problem and thereby achieve its organisational goal.

Management Accounting reporting has also been explained which contains material information

about the company's financial position, cost incurred, non monetary information thereby helping

in formulating business plans & strategies, preparing budgets, measuring performance, decision-

making and estimating future profits and cost to be incurred (Otley, D., 2016).

MAIN BODY

LO 1

P1. Explaining management accounting and essential requirements of management

accounting system.

Management accounting is defined as a process or technique of identifying, evaluating,

monitoring, measuring and communicating the financial, non financial, economical and

managerial information to organisation people for better decision-making, defining business

strategies & plans essential for achieving organisational goals and objectives effectively and

thereby generating maximum profits. It emphasises on factors such as planning, controlling and

providing information to the management for internal decision-making. The process of

management accounting is related with preparing management reports and accounts which helps

in providing correct, relevant, accurate and timely financial as well as the statistical information

as required by the management of the organisation to make day-to-day and short-term business

related decisions (Otley, D., 2016).

1

Management accounting is a term which is concerned with the application of professional

knowledge and abilities in policy formulation, planning and controlling for the undertakings. It is

a process which involves concept of evaluating, identifying and preparing management accounts,

reports and business strategy to provide accurate, fair and timely information related to

financial, managerial and non-financial matter necessary for decision-making & also helps in

interpreting & communicating information to company's stakeholders (Otley, D., 2016). Further

more, the company has used different management accounting techniques for controlling cost,

making budgets. It has also explained that how a company uses different management

accounting tools in solving its financial problem and thereby achieve its organisational goal.

Management Accounting reporting has also been explained which contains material information

about the company's financial position, cost incurred, non monetary information thereby helping

in formulating business plans & strategies, preparing budgets, measuring performance, decision-

making and estimating future profits and cost to be incurred (Otley, D., 2016).

MAIN BODY

LO 1

P1. Explaining management accounting and essential requirements of management

accounting system.

Management accounting is defined as a process or technique of identifying, evaluating,

monitoring, measuring and communicating the financial, non financial, economical and

managerial information to organisation people for better decision-making, defining business

strategies & plans essential for achieving organisational goals and objectives effectively and

thereby generating maximum profits. It emphasises on factors such as planning, controlling and

providing information to the management for internal decision-making. The process of

management accounting is related with preparing management reports and accounts which helps

in providing correct, relevant, accurate and timely financial as well as the statistical information

as required by the management of the organisation to make day-to-day and short-term business

related decisions (Otley, D., 2016).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Distinction between Management Accounting and Financial Accounting.

S. No. Basis Management Accounting Financial Accounting

1 Nature of Information Financial and Non-financial

Information.

Mainly financial information.

2 Information uses To help in planning,

monitoring, controlling and

decision-making.

To record the financial

performance and position of

the company at the end of the

period and communicating it

to its users.

3 Information users Information is used by Internal

users mainly i.e. by managers,

employees (Otley, D., 2016).

Useful for external users viz.

shareholders, creditors, banks

etc.

4 Time period It emphasises on future

aspects useful for growth of

business.

It considers past transactions

(Otley, D., 2016).

The essential requirements of management accounting system are as follows:

1. Cost Accounting System - The Cost Accounting system is a process which is used by the

company to make estimates, analyses the product cost for ascertaining the profit levels, cost

incurred in carrying on business activities i.e. for manufacturing a product, inventory valuation

and controlling cost (Otley, D., 2016). It has two types:

1. Process Costing Method - It is a cost accounting system which emphasizes on ascertainment

of the operating and manufacturing costs incurred separately for every wok process. It takes into

consideration the products of similar nature useful in such costing method. It is calculated by

totalling of all cost amount and divided by total output for ascertaining cost per unit (Otley, D.,

2016).

2. Job order Costing Method - It is a process which emphasizes on ascertainment of the operating

and manufacturing costs incurred separately for every wok job. It involves collection of cost of

production that is engaged in production of some specific unit or a group. This cost accounting

2

S. No. Basis Management Accounting Financial Accounting

1 Nature of Information Financial and Non-financial

Information.

Mainly financial information.

2 Information uses To help in planning,

monitoring, controlling and

decision-making.

To record the financial

performance and position of

the company at the end of the

period and communicating it

to its users.

3 Information users Information is used by Internal

users mainly i.e. by managers,

employees (Otley, D., 2016).

Useful for external users viz.

shareholders, creditors, banks

etc.

4 Time period It emphasises on future

aspects useful for growth of

business.

It considers past transactions

(Otley, D., 2016).

The essential requirements of management accounting system are as follows:

1. Cost Accounting System - The Cost Accounting system is a process which is used by the

company to make estimates, analyses the product cost for ascertaining the profit levels, cost

incurred in carrying on business activities i.e. for manufacturing a product, inventory valuation

and controlling cost (Otley, D., 2016). It has two types:

1. Process Costing Method - It is a cost accounting system which emphasizes on ascertainment

of the operating and manufacturing costs incurred separately for every wok process. It takes into

consideration the products of similar nature useful in such costing method. It is calculated by

totalling of all cost amount and divided by total output for ascertaining cost per unit (Otley, D.,

2016).

2. Job order Costing Method - It is a process which emphasizes on ascertainment of the operating

and manufacturing costs incurred separately for every wok job. It involves collection of cost of

production that is engaged in production of some specific unit or a group. This cost accounting

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

method is used for costing the unique products and also helps customers in ascertaining exact

cost incurred for producing a product.

2. Price optimisation system - This method of management accounting system helps company in

analysing that how customer will behave towards different price changes with different channels

of its products and services (Otley, D., 2016). It studies the customer response towards different

price. This method helps the company in analysing the best possible price for its product and

services which it can charge from its customers and in-turn will maximize the business profits

and able to achieve its goal and objectives effectively. It also helps in determining the future

profit by studying fluctuation in demand with reference to price changes. It considers three

factors as price elements:

1. Strategy of pricing a product.

2. Product value for both buyer and seller, and

3. Strategies and procedures used for increasing profits level (Otley, D., 2016).

3. Inventory Management System - It is a system of managing inventory, stock levels by

monitoring and tracking goods, products within supply chain and area where business carries out

its operating and manufacturing functions. This method helps company in ensuring the

continuity of workflow, evaluating exact inventory figure and its reorder before stock out

situation arises. The main function of managing inventory is to keep a check on detailed record

of new or returned product when it enters or leaves a warehouse (Otley, D., 2016). This

management accounting system has following two sub types:

1. LIFO - LIFO stands for “Last in, first out”. It is a method of inventory valuation in which last

inventory item purchased is sold first among all the inventory held.

2. FIFO - FIFO stands for “First in, first out”. It is a method in which goods purchased first are

the goods sold first (Otley, D., 2016).

4. Job Costing System - This method is defined as a process in which manufacturing and

operating cost are assign to each and every product and service, so as to monitor and keep a track

of expenses incurred. Cost information associated with the specific product or any business

activity or specific job process is determined for the knowledge of customer which helps them in

3

cost incurred for producing a product.

2. Price optimisation system - This method of management accounting system helps company in

analysing that how customer will behave towards different price changes with different channels

of its products and services (Otley, D., 2016). It studies the customer response towards different

price. This method helps the company in analysing the best possible price for its product and

services which it can charge from its customers and in-turn will maximize the business profits

and able to achieve its goal and objectives effectively. It also helps in determining the future

profit by studying fluctuation in demand with reference to price changes. It considers three

factors as price elements:

1. Strategy of pricing a product.

2. Product value for both buyer and seller, and

3. Strategies and procedures used for increasing profits level (Otley, D., 2016).

3. Inventory Management System - It is a system of managing inventory, stock levels by

monitoring and tracking goods, products within supply chain and area where business carries out

its operating and manufacturing functions. This method helps company in ensuring the

continuity of workflow, evaluating exact inventory figure and its reorder before stock out

situation arises. The main function of managing inventory is to keep a check on detailed record

of new or returned product when it enters or leaves a warehouse (Otley, D., 2016). This

management accounting system has following two sub types:

1. LIFO - LIFO stands for “Last in, first out”. It is a method of inventory valuation in which last

inventory item purchased is sold first among all the inventory held.

2. FIFO - FIFO stands for “First in, first out”. It is a method in which goods purchased first are

the goods sold first (Otley, D., 2016).

4. Job Costing System - This method is defined as a process in which manufacturing and

operating cost are assign to each and every product and service, so as to monitor and keep a track

of expenses incurred. Cost information associated with the specific product or any business

activity or specific job process is determined for the knowledge of customer which helps them in

3

getting cost reimbursed under terms and conditions as defined in contract (Otley, D., 2016). It

divides cost into Direct material, labour and overhead costs. By using job costing system, the

company can ascertained cost at any stage of job completed and comparing it with estimated

costs prepared thereby helping in controlling cost and maximizing profits of the business

organisation.

P2. Explaining different methods used for management accounting reporting.

The management accounting reporting is a term which provides detailed information related to

financial, non financial and managerial matters of the company. It helps company in making

decision related to internal processes of the business organisation. This is considered as a process

of planning, monitoring, evaluating and decision making on the basis of material information

provided about the company's financial position, cost incurred thereby helping the company in

formulating business strategies & plans, preparing budgets, measuring performance, estimating

future profits and cost to be incurred (Mohd Fuzi, N. and et.al., 2019).

Different used for management accounting reporting are as follows:

1. Cost Managerial Accounting Report - This report helps in evaluating the cost involved in

manufacturing or producing a specific product, unit or group of units. It helps in realizing the

product cost prices and selling prices and comparing for determining the profit margins. The cost

managerial accounting system distributes the cost into direct raw material costs, direct labour

cost and overhead cost. The total cost figure ascertained is divided by the total number of output

produced for determining the cost per unit of a product or service (Mohd Fuzi, N. and et.al.,

2019).

2. Budget Report - This report helps business organisation in analysing the performance of

various business departments and business operations. It helps company in controlling cost,

business expenses by preparing budgets & business strategies for future period. With the help of

budget report, the company can achieve its objectives with limited budget amount thereby

maximizing profit and minimum cost of production.

3. Performance Report - This report provides detailed information about the success journey of

performance of a business project or of employee performance. It helps the company in

monitoring and reviewing the performance thereby assisting in decision making (Mohd Fuzi, N.

and et.al., 2019). Such reports provide deeper view of the working of business organisation. It is

4

divides cost into Direct material, labour and overhead costs. By using job costing system, the

company can ascertained cost at any stage of job completed and comparing it with estimated

costs prepared thereby helping in controlling cost and maximizing profits of the business

organisation.

P2. Explaining different methods used for management accounting reporting.

The management accounting reporting is a term which provides detailed information related to

financial, non financial and managerial matters of the company. It helps company in making

decision related to internal processes of the business organisation. This is considered as a process

of planning, monitoring, evaluating and decision making on the basis of material information

provided about the company's financial position, cost incurred thereby helping the company in

formulating business strategies & plans, preparing budgets, measuring performance, estimating

future profits and cost to be incurred (Mohd Fuzi, N. and et.al., 2019).

Different used for management accounting reporting are as follows:

1. Cost Managerial Accounting Report - This report helps in evaluating the cost involved in

manufacturing or producing a specific product, unit or group of units. It helps in realizing the

product cost prices and selling prices and comparing for determining the profit margins. The cost

managerial accounting system distributes the cost into direct raw material costs, direct labour

cost and overhead cost. The total cost figure ascertained is divided by the total number of output

produced for determining the cost per unit of a product or service (Mohd Fuzi, N. and et.al.,

2019).

2. Budget Report - This report helps business organisation in analysing the performance of

various business departments and business operations. It helps company in controlling cost,

business expenses by preparing budgets & business strategies for future period. With the help of

budget report, the company can achieve its objectives with limited budget amount thereby

maximizing profit and minimum cost of production.

3. Performance Report - This report provides detailed information about the success journey of

performance of a business project or of employee performance. It helps the company in

monitoring and reviewing the performance thereby assisting in decision making (Mohd Fuzi, N.

and et.al., 2019). Such reports provide deeper view of the working of business organisation. It is

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

important for every company to monitor and keep a track of its strategy & policy developed for

attainment of mission. It is a budget which compares actual and budgeted amounts of cost to be

controlled for a business organisation.

4. Accounts Receivable Aging Reports - The report of Accounts Receivable Aging takes into

consideration the importance of accounts receivables for making crucial management decisions

in the business organisation. This report emphasises on the credit side of the business balance

sheet and income statements. Apart from the credit side amount, any balance remaining helps the

company in identifying the defaulting person of the business organisation. It helps in assessing

the problem coming in cash collection process of the company (Mohd Fuzi, N. and et.al., 2019).

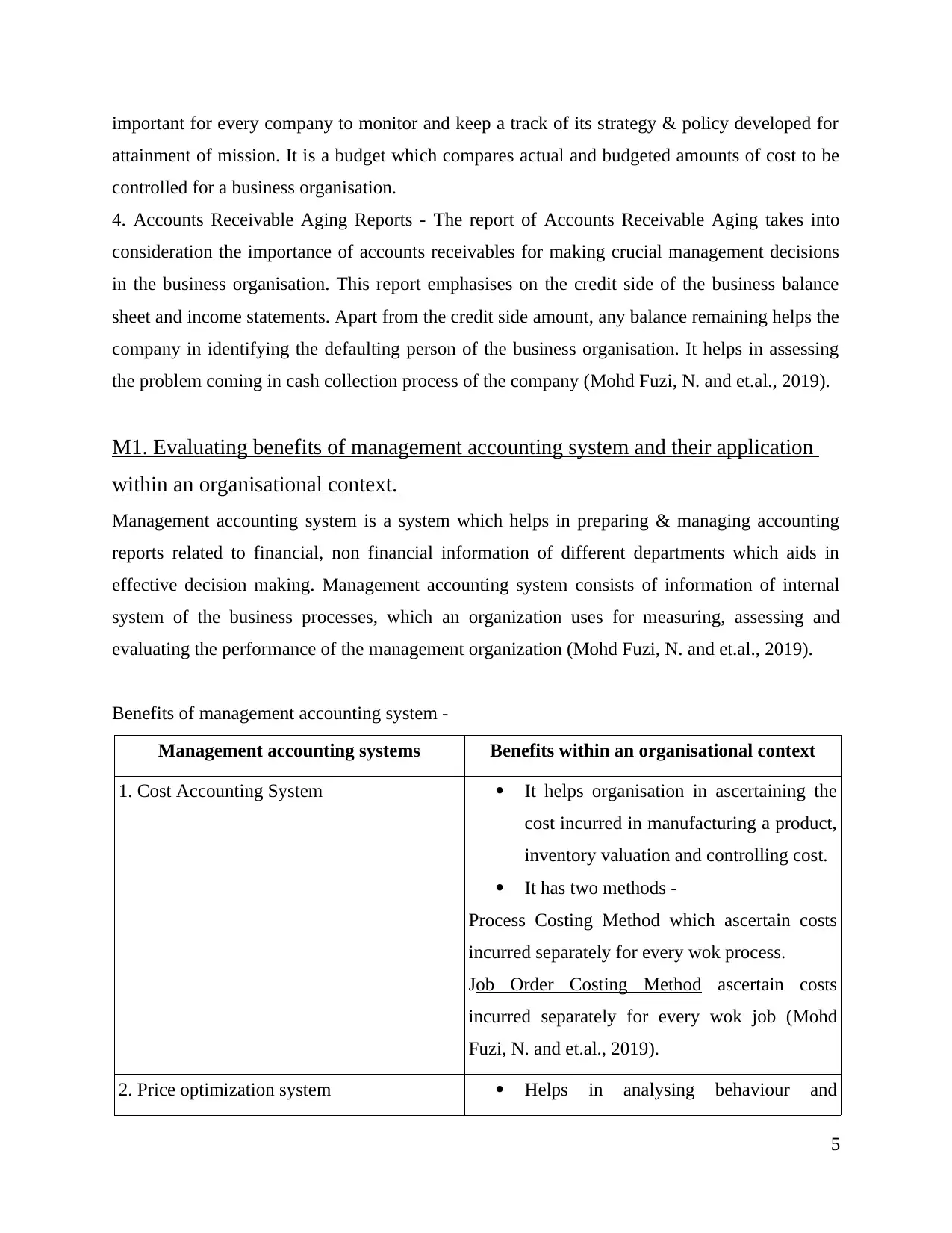

M1. Evaluating benefits of management accounting system and their application

within an organisational context.

Management accounting system is a system which helps in preparing & managing accounting

reports related to financial, non financial information of different departments which aids in

effective decision making. Management accounting system consists of information of internal

system of the business processes, which an organization uses for measuring, assessing and

evaluating the performance of the management organization (Mohd Fuzi, N. and et.al., 2019).

Benefits of management accounting system -

Management accounting systems Benefits within an organisational context

1. Cost Accounting System It helps organisation in ascertaining the

cost incurred in manufacturing a product,

inventory valuation and controlling cost.

It has two methods -

Process Costing Method which ascertain costs

incurred separately for every wok process.

Job Order Costing Method ascertain costs

incurred separately for every wok job (Mohd

Fuzi, N. and et.al., 2019).

2. Price optimization system Helps in analysing behaviour and

5

attainment of mission. It is a budget which compares actual and budgeted amounts of cost to be

controlled for a business organisation.

4. Accounts Receivable Aging Reports - The report of Accounts Receivable Aging takes into

consideration the importance of accounts receivables for making crucial management decisions

in the business organisation. This report emphasises on the credit side of the business balance

sheet and income statements. Apart from the credit side amount, any balance remaining helps the

company in identifying the defaulting person of the business organisation. It helps in assessing

the problem coming in cash collection process of the company (Mohd Fuzi, N. and et.al., 2019).

M1. Evaluating benefits of management accounting system and their application

within an organisational context.

Management accounting system is a system which helps in preparing & managing accounting

reports related to financial, non financial information of different departments which aids in

effective decision making. Management accounting system consists of information of internal

system of the business processes, which an organization uses for measuring, assessing and

evaluating the performance of the management organization (Mohd Fuzi, N. and et.al., 2019).

Benefits of management accounting system -

Management accounting systems Benefits within an organisational context

1. Cost Accounting System It helps organisation in ascertaining the

cost incurred in manufacturing a product,

inventory valuation and controlling cost.

It has two methods -

Process Costing Method which ascertain costs

incurred separately for every wok process.

Job Order Costing Method ascertain costs

incurred separately for every wok job (Mohd

Fuzi, N. and et.al., 2019).

2. Price optimization system Helps in analysing behaviour and

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

response of customer towards different

price changes with different channels of

its products and services (Mohd Fuzi, N.

and et.al., 2019).

It helps in determining future profit by

studying fluctuation in demand with

reference to price changes.

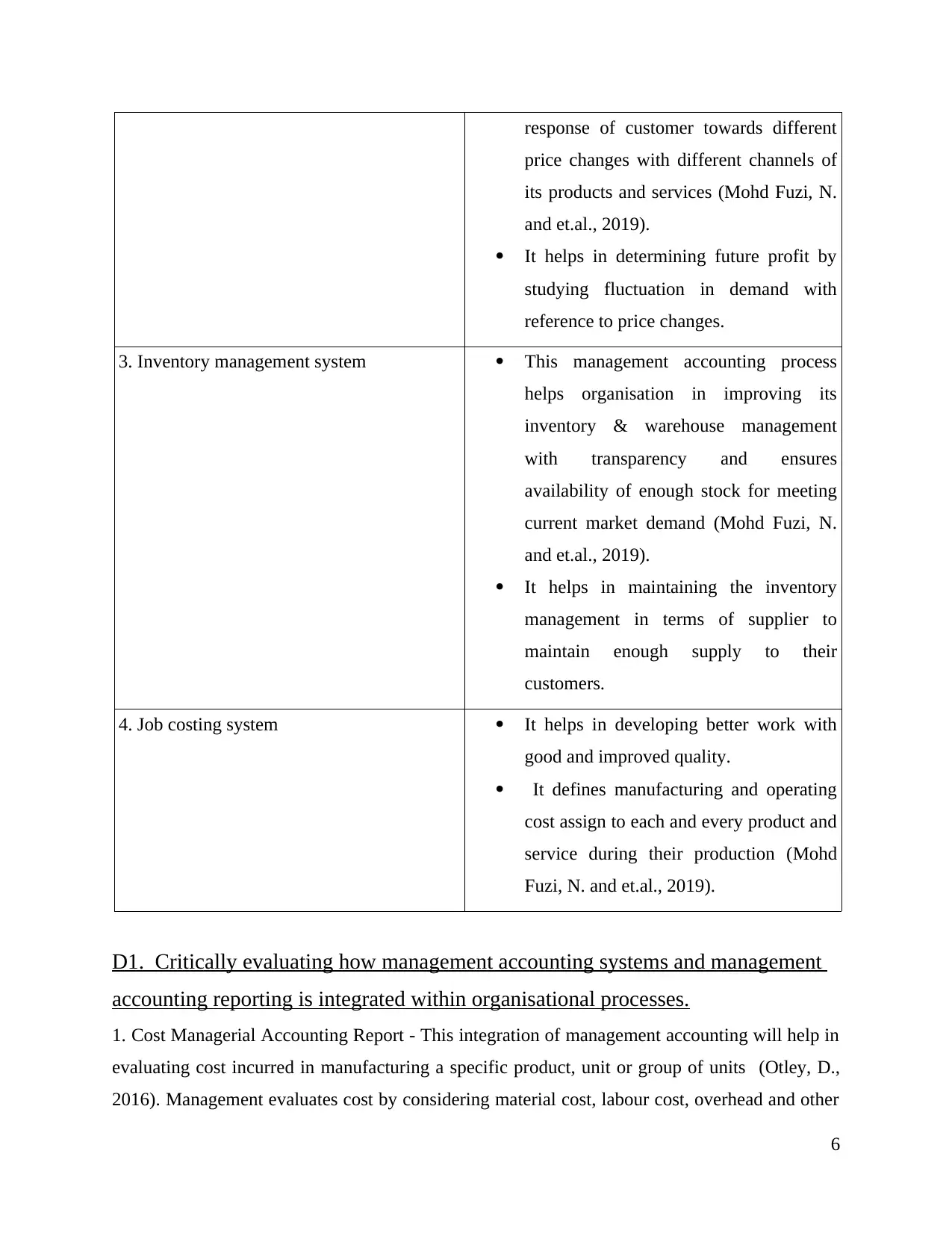

3. Inventory management system This management accounting process

helps organisation in improving its

inventory & warehouse management

with transparency and ensures

availability of enough stock for meeting

current market demand (Mohd Fuzi, N.

and et.al., 2019).

It helps in maintaining the inventory

management in terms of supplier to

maintain enough supply to their

customers.

4. Job costing system It helps in developing better work with

good and improved quality.

It defines manufacturing and operating

cost assign to each and every product and

service during their production (Mohd

Fuzi, N. and et.al., 2019).

D1. Critically evaluating how management accounting systems and management

accounting reporting is integrated within organisational processes.

1. Cost Managerial Accounting Report - This integration of management accounting will help in

evaluating cost incurred in manufacturing a specific product, unit or group of units (Otley, D.,

2016). Management evaluates cost by considering material cost, labour cost, overhead and other

6

price changes with different channels of

its products and services (Mohd Fuzi, N.

and et.al., 2019).

It helps in determining future profit by

studying fluctuation in demand with

reference to price changes.

3. Inventory management system This management accounting process

helps organisation in improving its

inventory & warehouse management

with transparency and ensures

availability of enough stock for meeting

current market demand (Mohd Fuzi, N.

and et.al., 2019).

It helps in maintaining the inventory

management in terms of supplier to

maintain enough supply to their

customers.

4. Job costing system It helps in developing better work with

good and improved quality.

It defines manufacturing and operating

cost assign to each and every product and

service during their production (Mohd

Fuzi, N. and et.al., 2019).

D1. Critically evaluating how management accounting systems and management

accounting reporting is integrated within organisational processes.

1. Cost Managerial Accounting Report - This integration of management accounting will help in

evaluating cost incurred in manufacturing a specific product, unit or group of units (Otley, D.,

2016). Management evaluates cost by considering material cost, labour cost, overhead and other

6

cost. It helps in determining the product cost prices and selling prices and comparing for

determining the profit margins.

2. Budget report - With the help of this management accounting report the organisation is able to

maximizing profit and minimize its cost of production with the availability of limited budgeted

amount and resources as the budget is prepared by management for meeting future expenses. It

helps in controlling cost expense by preparing future budget (Otley, D., 2016).

3. Performance report - By this integration of management accounting, the company is able to

develop business plans & strategies, budgets for achieving the goals and objectives of business

organisation timely and effectively by minimizing cost of production and maximizing profits.

This report will also help the manager of business organisation in analysing the performance &

market position of business (Otley, D., 2016).

4. Account Receivable Aging report - This integration in the management accounting helps the

organisation in collecting the account receivable due on time. It helps the company in identifying

the defaulting person of the business organisation. It also supports company in assessing the

problem faced in cash collection process of the company (Otley, D., 2016).

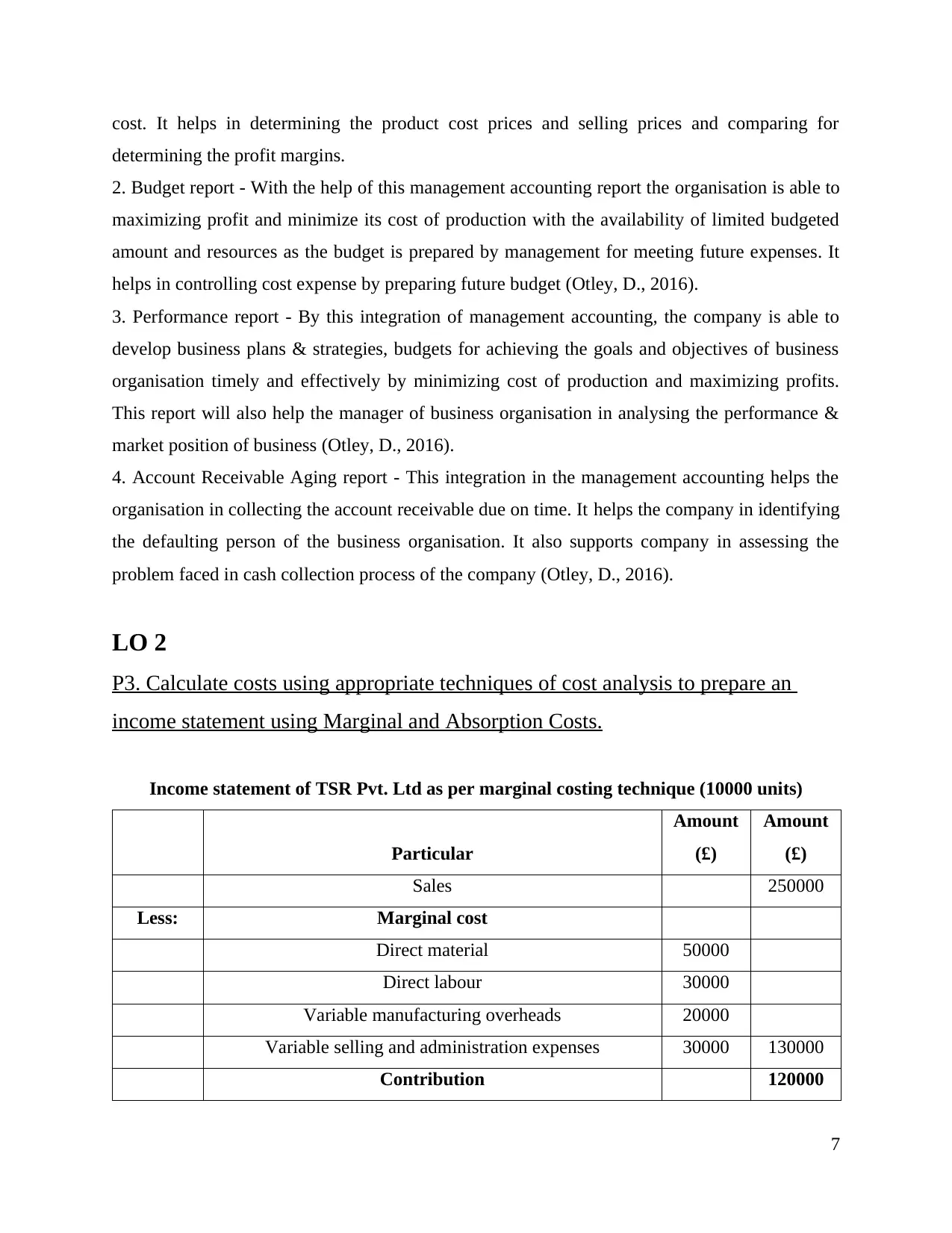

LO 2

P3. Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using Marginal and Absorption Costs.

Income statement of TSR Pvt. Ltd as per marginal costing technique (10000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 50000

Direct labour 30000

Variable manufacturing overheads 20000

Variable selling and administration expenses 30000 130000

Contribution 120000

7

determining the profit margins.

2. Budget report - With the help of this management accounting report the organisation is able to

maximizing profit and minimize its cost of production with the availability of limited budgeted

amount and resources as the budget is prepared by management for meeting future expenses. It

helps in controlling cost expense by preparing future budget (Otley, D., 2016).

3. Performance report - By this integration of management accounting, the company is able to

develop business plans & strategies, budgets for achieving the goals and objectives of business

organisation timely and effectively by minimizing cost of production and maximizing profits.

This report will also help the manager of business organisation in analysing the performance &

market position of business (Otley, D., 2016).

4. Account Receivable Aging report - This integration in the management accounting helps the

organisation in collecting the account receivable due on time. It helps the company in identifying

the defaulting person of the business organisation. It also supports company in assessing the

problem faced in cash collection process of the company (Otley, D., 2016).

LO 2

P3. Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using Marginal and Absorption Costs.

Income statement of TSR Pvt. Ltd as per marginal costing technique (10000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 50000

Direct labour 30000

Variable manufacturing overheads 20000

Variable selling and administration expenses 30000 130000

Contribution 120000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

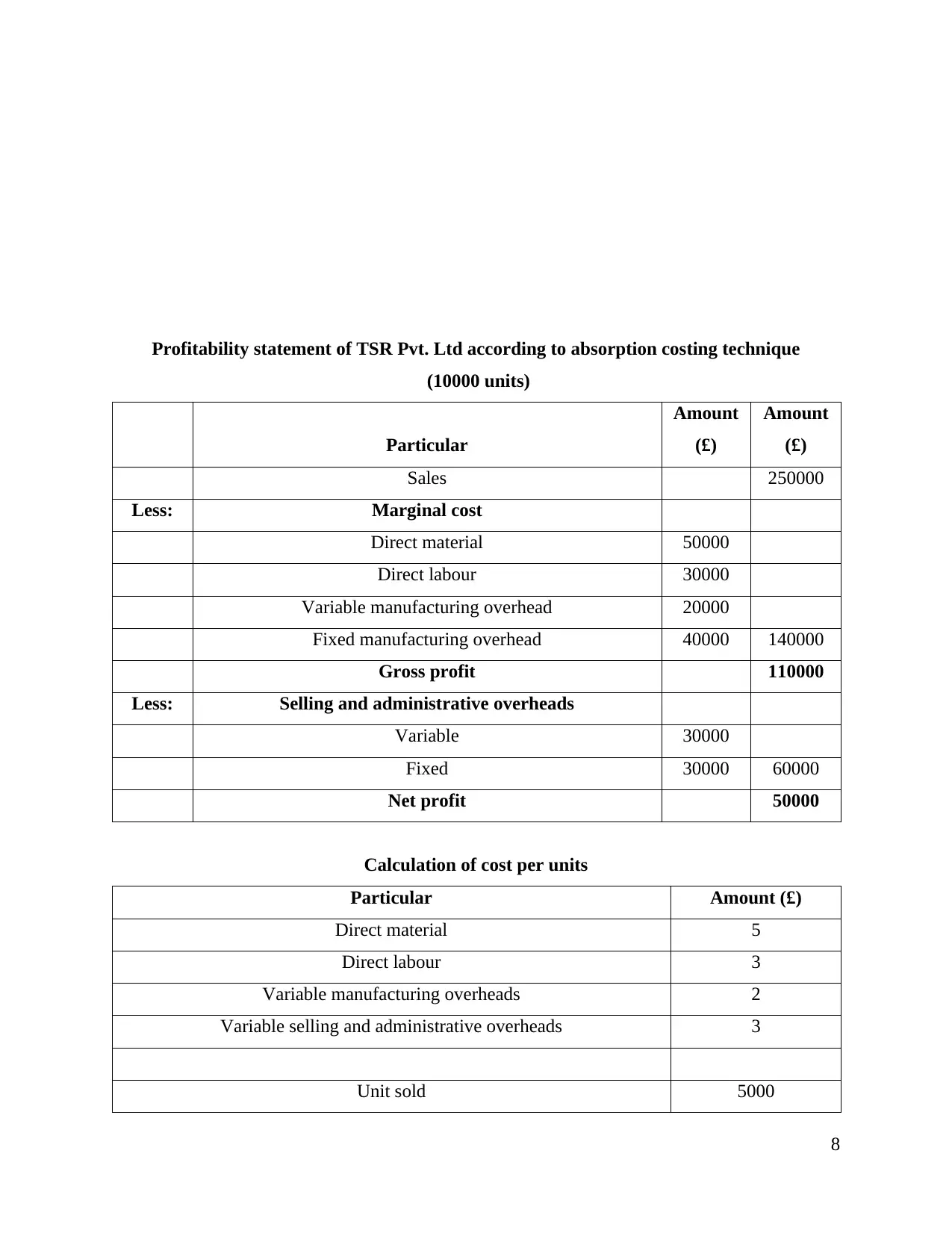

Profitability statement of TSR Pvt. Ltd according to absorption costing technique

(10000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 50000

Direct labour 30000

Variable manufacturing overhead 20000

Fixed manufacturing overhead 40000 140000

Gross profit 110000

Less: Selling and administrative overheads

Variable 30000

Fixed 30000 60000

Net profit 50000

Calculation of cost per units

Particular Amount (£)

Direct material 5

Direct labour 3

Variable manufacturing overheads 2

Variable selling and administrative overheads 3

Unit sold 5000

8

(10000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 50000

Direct labour 30000

Variable manufacturing overhead 20000

Fixed manufacturing overhead 40000 140000

Gross profit 110000

Less: Selling and administrative overheads

Variable 30000

Fixed 30000 60000

Net profit 50000

Calculation of cost per units

Particular Amount (£)

Direct material 5

Direct labour 3

Variable manufacturing overheads 2

Variable selling and administrative overheads 3

Unit sold 5000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

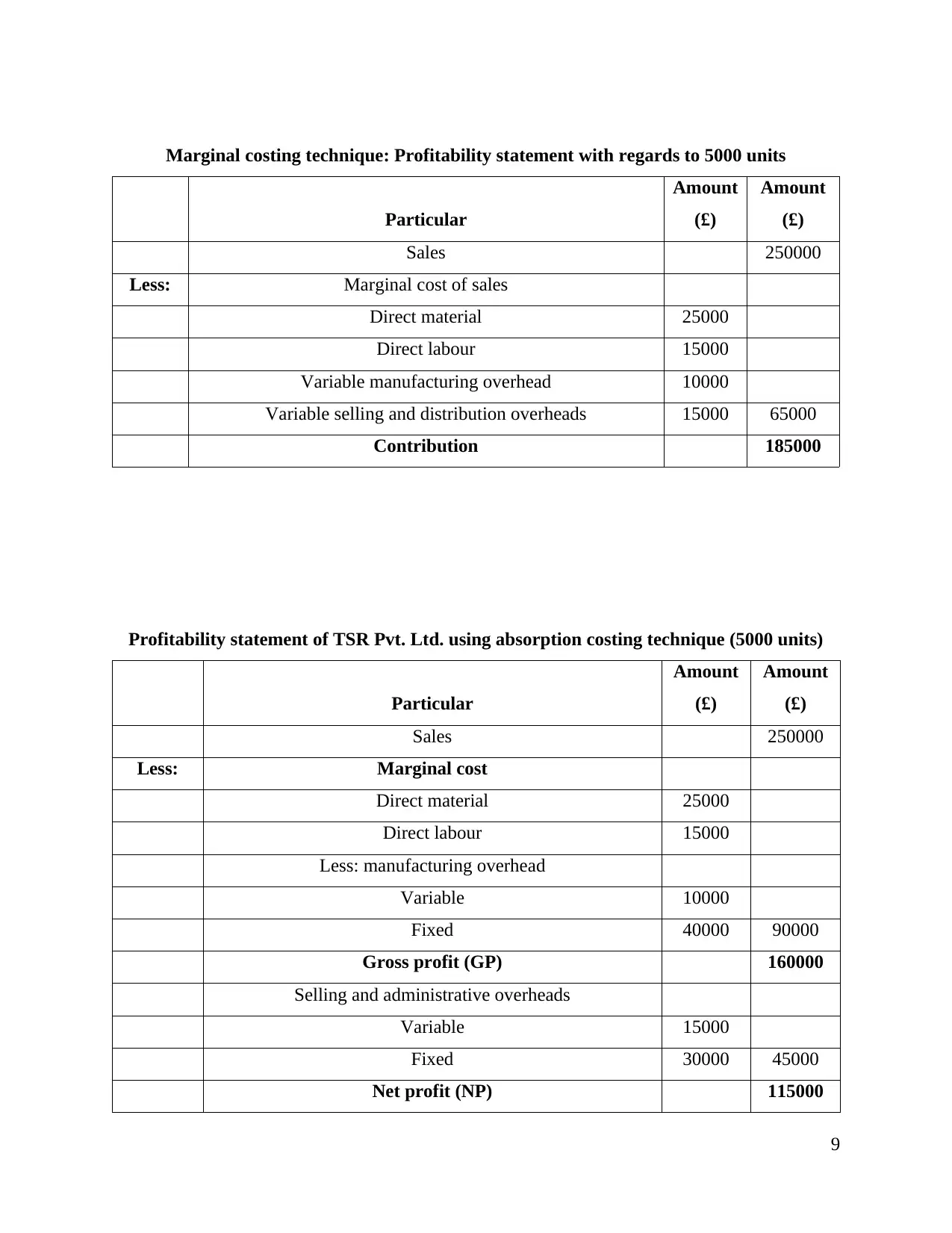

Marginal costing technique: Profitability statement with regards to 5000 units

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost of sales

Direct material 25000

Direct labour 15000

Variable manufacturing overhead 10000

Variable selling and distribution overheads 15000 65000

Contribution 185000

Profitability statement of TSR Pvt. Ltd. using absorption costing technique (5000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 25000

Direct labour 15000

Less: manufacturing overhead

Variable 10000

Fixed 40000 90000

Gross profit (GP) 160000

Selling and administrative overheads

Variable 15000

Fixed 30000 45000

Net profit (NP) 115000

9

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost of sales

Direct material 25000

Direct labour 15000

Variable manufacturing overhead 10000

Variable selling and distribution overheads 15000 65000

Contribution 185000

Profitability statement of TSR Pvt. Ltd. using absorption costing technique (5000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 25000

Direct labour 15000

Less: manufacturing overhead

Variable 10000

Fixed 40000 90000

Gross profit (GP) 160000

Selling and administrative overheads

Variable 15000

Fixed 30000 45000

Net profit (NP) 115000

9

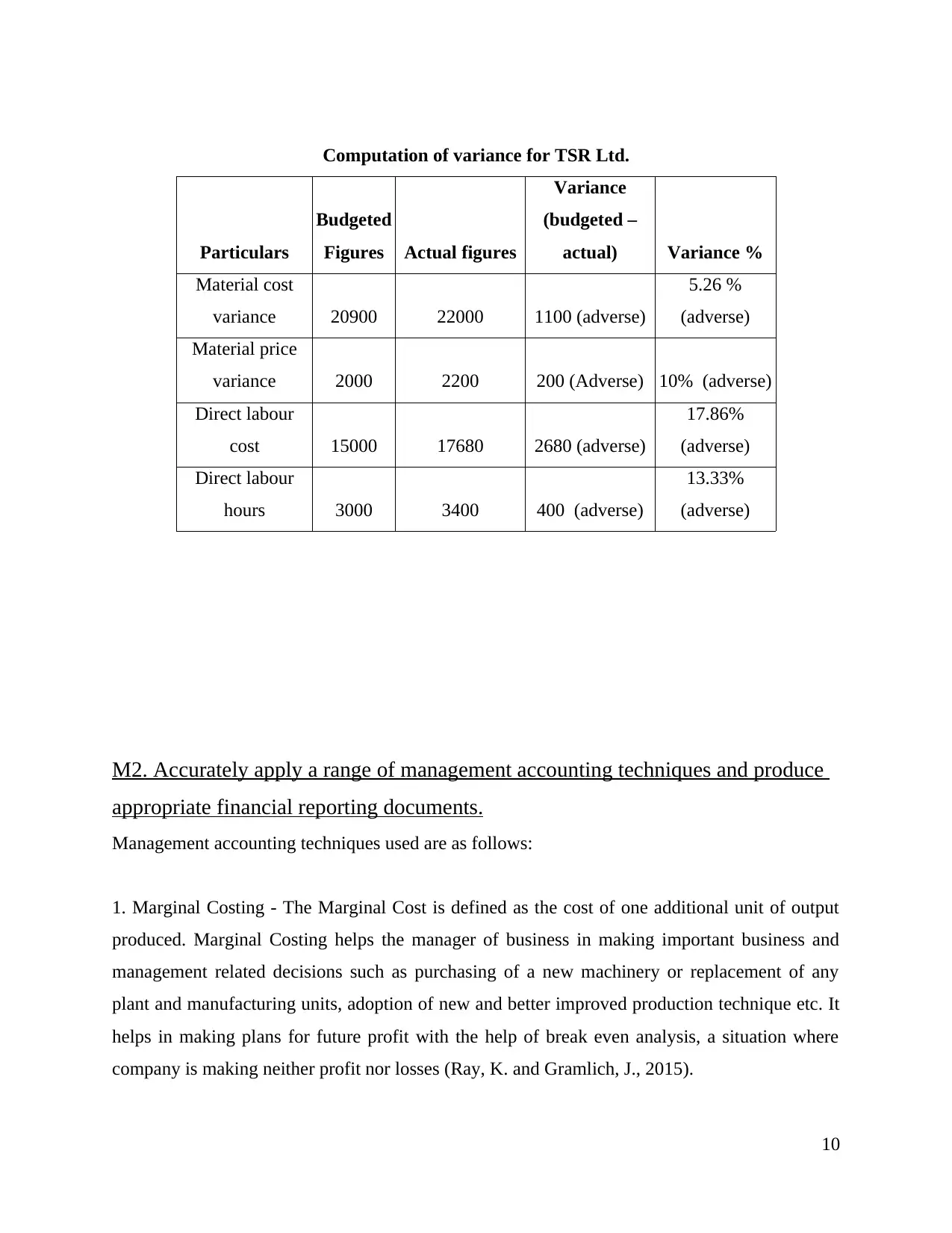

Computation of variance for TSR Ltd.

Particulars

Budgeted

Figures Actual figures

Variance

(budgeted –

actual) Variance %

Material cost

variance 20900 22000 1100 (adverse)

5.26 %

(adverse)

Material price

variance 2000 2200 200 (Adverse) 10% (adverse)

Direct labour

cost 15000 17680 2680 (adverse)

17.86%

(adverse)

Direct labour

hours 3000 3400 400 (adverse)

13.33%

(adverse)

M2. Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents.

Management accounting techniques used are as follows:

1. Marginal Costing - The Marginal Cost is defined as the cost of one additional unit of output

produced. Marginal Costing helps the manager of business in making important business and

management related decisions such as purchasing of a new machinery or replacement of any

plant and manufacturing units, adoption of new and better improved production technique etc. It

helps in making plans for future profit with the help of break even analysis, a situation where

company is making neither profit nor losses (Ray, K. and Gramlich, J., 2015).

10

Particulars

Budgeted

Figures Actual figures

Variance

(budgeted –

actual) Variance %

Material cost

variance 20900 22000 1100 (adverse)

5.26 %

(adverse)

Material price

variance 2000 2200 200 (Adverse) 10% (adverse)

Direct labour

cost 15000 17680 2680 (adverse)

17.86%

(adverse)

Direct labour

hours 3000 3400 400 (adverse)

13.33%

(adverse)

M2. Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents.

Management accounting techniques used are as follows:

1. Marginal Costing - The Marginal Cost is defined as the cost of one additional unit of output

produced. Marginal Costing helps the manager of business in making important business and

management related decisions such as purchasing of a new machinery or replacement of any

plant and manufacturing units, adoption of new and better improved production technique etc. It

helps in making plans for future profit with the help of break even analysis, a situation where

company is making neither profit nor losses (Ray, K. and Gramlich, J., 2015).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21