Government Financial and Management Accounting Promotion

VerifiedAdded on 2020/09/17

|17

|4392

|23

AI Summary

Management accounting plays a crucial role in shaping business strategies and enhancing organizational performance. This analysis covers various aspects including the impact of strategic management accounting on firm success, alignment between strategy and management accounting practices, recent advancements in the field, and initiatives promoting government financial accountability. By reviewing these topics, students gain insights into how effective management accounting can drive business growth and improve decision-making processes. The assignment draws from a range of academic sources to provide a well-rounded perspective on current trends and future directions in management accounting.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and different types of Management Accounting System.............1

P2. Different management accounting reports............................................................................4

TASK 2............................................................................................................................................6

P3. Calculation of cost and preparation of Income statement.....................................................6

TASK 3............................................................................................................................................7

P4. Advantages and disadvantages of planning tools for budgetary control..............................7

TASK 4..........................................................................................................................................11

P5. Use of management accounting system to respond financial problem...............................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Illustration Index

Illustration 1: Budgeting Process...................................................................................................10

Illustration 2: Balanced Scorecard.................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and different types of Management Accounting System.............1

P2. Different management accounting reports............................................................................4

TASK 2............................................................................................................................................6

P3. Calculation of cost and preparation of Income statement.....................................................6

TASK 3............................................................................................................................................7

P4. Advantages and disadvantages of planning tools for budgetary control..............................7

TASK 4..........................................................................................................................................11

P5. Use of management accounting system to respond financial problem...............................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Illustration Index

Illustration 1: Budgeting Process...................................................................................................10

Illustration 2: Balanced Scorecard.................................................................................................12

INTRODUCTION

Management accounting means provision of the financial data and advising the

management of company for using the financial data in organisation and development of its

business. It is the accounting system which includes the management decision making,

budgeting, performance analysing and the implementation of all these systems. The present

report is based on Tech which is a UK based company producing charger for mobile telephone

and other gadgets for retail outlets. Management accounting information is an important tool of

decision-making for department managers. The report will shed light on cost accounting system,

inventory management systems, Job costing systems and the different types of managerial

accounting reports. This report also discuss that department managers should have more

involvement and should take more responsibilities for their departments. ZBB is based on the

assumption that previous year’s budget is zero and to make the new budget of the current year

management must take zero as the base.

TASK 1

P1. Management accounting and different types of Management Accounting System

Management accounting is also known as managerial accounting. Management

Accounting helps manager in making provision for financial and non- financial decision-making

information. According to the IMA (Institute of Management Accounting), it is a profession that

involves management decision making, performance management systems, devising planning

and it also helps management in formulation and implementation of organisational strategy.

Management accounting looks after the business events in consideration with the need of the

business (Takeda and Boyns, 2014). It is the process of identifying, analysing, measuring and

interpreting the information. It also provides timely and accurate statistical and financial

information with the help of management reports that are required by managers for making their

short- term and day- to- day decisions.

Management Accounting System:

Management Accounting system consists of components of management accounting that

includes budgets, income and expenses report, return on investment report, management

1

Management accounting means provision of the financial data and advising the

management of company for using the financial data in organisation and development of its

business. It is the accounting system which includes the management decision making,

budgeting, performance analysing and the implementation of all these systems. The present

report is based on Tech which is a UK based company producing charger for mobile telephone

and other gadgets for retail outlets. Management accounting information is an important tool of

decision-making for department managers. The report will shed light on cost accounting system,

inventory management systems, Job costing systems and the different types of managerial

accounting reports. This report also discuss that department managers should have more

involvement and should take more responsibilities for their departments. ZBB is based on the

assumption that previous year’s budget is zero and to make the new budget of the current year

management must take zero as the base.

TASK 1

P1. Management accounting and different types of Management Accounting System

Management accounting is also known as managerial accounting. Management

Accounting helps manager in making provision for financial and non- financial decision-making

information. According to the IMA (Institute of Management Accounting), it is a profession that

involves management decision making, performance management systems, devising planning

and it also helps management in formulation and implementation of organisational strategy.

Management accounting looks after the business events in consideration with the need of the

business (Takeda and Boyns, 2014). It is the process of identifying, analysing, measuring and

interpreting the information. It also provides timely and accurate statistical and financial

information with the help of management reports that are required by managers for making their

short- term and day- to- day decisions.

Management Accounting System:

Management Accounting system consists of components of management accounting that

includes budgets, income and expenses report, return on investment report, management

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance report to compare budget results with actual results and sales analysis. Some other

less known components of management accounting are standard costing of cost of goods sold,

ABC (activity- based-cost) analysis and balanced scorecard.

Importance of Management Accounting System in organisation:

Management accounting system play a critical role in the group learning of the

organisation.

The main purpose of management accounting in an organisation is to help management

in decision making by collecting, communicating and processing information that will

help to plan, control and evaluate the organisational strategy and business processes.

It helps in forecasting the future that aids decision making by giving answers to the

following questions- should investment be made in more equipment? Is there a need of

diversification? Should the company merge or acquire a new company? It forecasts the

future trends by answering all these questions.

It helps in making decision related to the make or buy a product from a third party.

Management accounting helps in forecasting cash flow and its impact on business.

It helps in knowing and understanding the variances and discrepancies in what is actually

achieved and what was predicted. It analyses the expected rate of return to the organisation.

Management Accounting vs Financial Accounting

Basis Management Accounting Financial Accounting

Meaning It provides related information to

the management for decision-

making.

It focuses on preparation on financial

statements for providing financial

information to its users.

Interested parties External as well as Internal parties

like management.

Only External parties like

shareholders, investors, etc.

Format It does not have specified format. It has specified format to present

2

less known components of management accounting are standard costing of cost of goods sold,

ABC (activity- based-cost) analysis and balanced scorecard.

Importance of Management Accounting System in organisation:

Management accounting system play a critical role in the group learning of the

organisation.

The main purpose of management accounting in an organisation is to help management

in decision making by collecting, communicating and processing information that will

help to plan, control and evaluate the organisational strategy and business processes.

It helps in forecasting the future that aids decision making by giving answers to the

following questions- should investment be made in more equipment? Is there a need of

diversification? Should the company merge or acquire a new company? It forecasts the

future trends by answering all these questions.

It helps in making decision related to the make or buy a product from a third party.

Management accounting helps in forecasting cash flow and its impact on business.

It helps in knowing and understanding the variances and discrepancies in what is actually

achieved and what was predicted. It analyses the expected rate of return to the organisation.

Management Accounting vs Financial Accounting

Basis Management Accounting Financial Accounting

Meaning It provides related information to

the management for decision-

making.

It focuses on preparation on financial

statements for providing financial

information to its users.

Interested parties External as well as Internal parties

like management.

Only External parties like

shareholders, investors, etc.

Format It does not have specified format. It has specified format to present

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information.

Time The reports are prepared as per the

need and requirement of the

managers.

It is generally prepared at the end of

financial year.

Audit of reports Audit of management reports are

not to be audited by statutory

auditor.

Audit through statutory auditor is

mandatory.

Types of management accounting system

Different types of management accounting systems are:

Cost accounting system: It is the framework used by management for estimating the

cost of their products and services with the purpose of analysing the profitability, cost

control and inventory valuation. Calculating the accurate cost of products and services is

typical hence the system is critical to operate. Tech Ltd. can use this system in estimating

the cost of its mobile phone charger.

Inventory management system: Inventory management system helps the management

to mange the inventory of the organisation. This includes both types of inventory that is

finished goods and raw material. Inventory management system in the modern era is been

managed by various inventory management software's. Tech Ltd. may use any software

from the available choices of inventory management software's.

Job- costing system: It is the system to assign the variables of manufacturing cost to

different individual products or product batches. It is generally used when manufactured

products have significant difference (Klemstine and Maher, 2014). In the case of identical

products, process costing is used. Tech Ltd. is indulged in manufacturing of various

products so it may use job costing for assigning manufacturing cost to mobile phone

charger.

3

Time The reports are prepared as per the

need and requirement of the

managers.

It is generally prepared at the end of

financial year.

Audit of reports Audit of management reports are

not to be audited by statutory

auditor.

Audit through statutory auditor is

mandatory.

Types of management accounting system

Different types of management accounting systems are:

Cost accounting system: It is the framework used by management for estimating the

cost of their products and services with the purpose of analysing the profitability, cost

control and inventory valuation. Calculating the accurate cost of products and services is

typical hence the system is critical to operate. Tech Ltd. can use this system in estimating

the cost of its mobile phone charger.

Inventory management system: Inventory management system helps the management

to mange the inventory of the organisation. This includes both types of inventory that is

finished goods and raw material. Inventory management system in the modern era is been

managed by various inventory management software's. Tech Ltd. may use any software

from the available choices of inventory management software's.

Job- costing system: It is the system to assign the variables of manufacturing cost to

different individual products or product batches. It is generally used when manufactured

products have significant difference (Klemstine and Maher, 2014). In the case of identical

products, process costing is used. Tech Ltd. is indulged in manufacturing of various

products so it may use job costing for assigning manufacturing cost to mobile phone

charger.

3

Price- optimising system: It is the mathematical system to calculate the variation of

demand at different price levels. Then the data is combined with cost information and

inventory levels to recommend the best price to improve profits.

Benefits of the above accounting systems:

Accounting systems helps the management to estimate the cost of their product and to

identify profitable and non- profitable products and services.

This will also allow the management to manage their inventory. To know the available

quantity of finished goods, raw material, economic order quantity, etc.

This will enable the management to know the manufacturing cost of various products.

Through this management can create the job- cost order for each item (Groot and Selto,

2013).

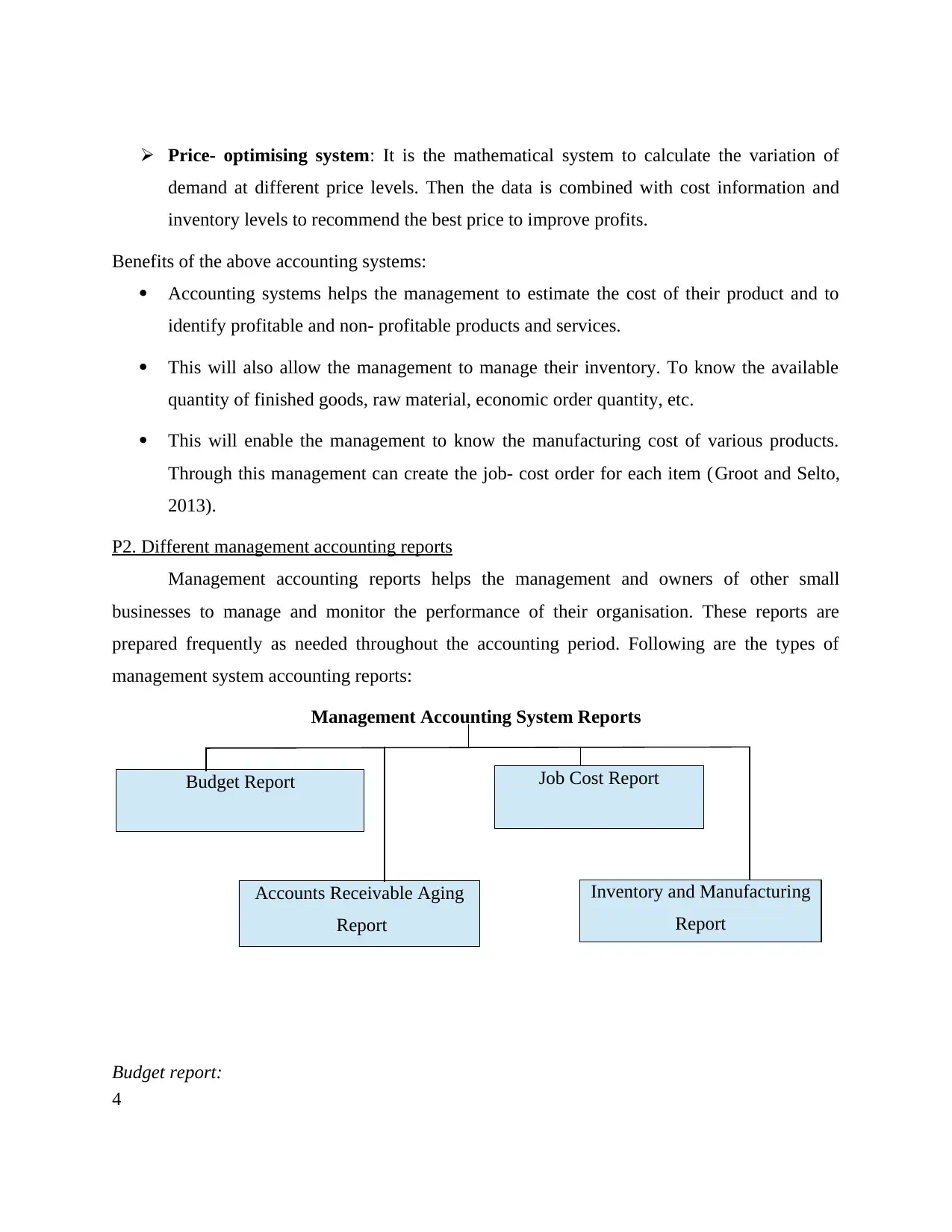

P2. Different management accounting reports

Management accounting reports helps the management and owners of other small

businesses to manage and monitor the performance of their organisation. These reports are

prepared frequently as needed throughout the accounting period. Following are the types of

management system accounting reports:

Management Accounting System Reports

Budget report:

4

Budget Report

Accounts Receivable Aging

Report

Job Cost Report

Inventory and Manufacturing

Report

demand at different price levels. Then the data is combined with cost information and

inventory levels to recommend the best price to improve profits.

Benefits of the above accounting systems:

Accounting systems helps the management to estimate the cost of their product and to

identify profitable and non- profitable products and services.

This will also allow the management to manage their inventory. To know the available

quantity of finished goods, raw material, economic order quantity, etc.

This will enable the management to know the manufacturing cost of various products.

Through this management can create the job- cost order for each item (Groot and Selto,

2013).

P2. Different management accounting reports

Management accounting reports helps the management and owners of other small

businesses to manage and monitor the performance of their organisation. These reports are

prepared frequently as needed throughout the accounting period. Following are the types of

management system accounting reports:

Management Accounting System Reports

Budget report:

4

Budget Report

Accounts Receivable Aging

Report

Job Cost Report

Inventory and Manufacturing

Report

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

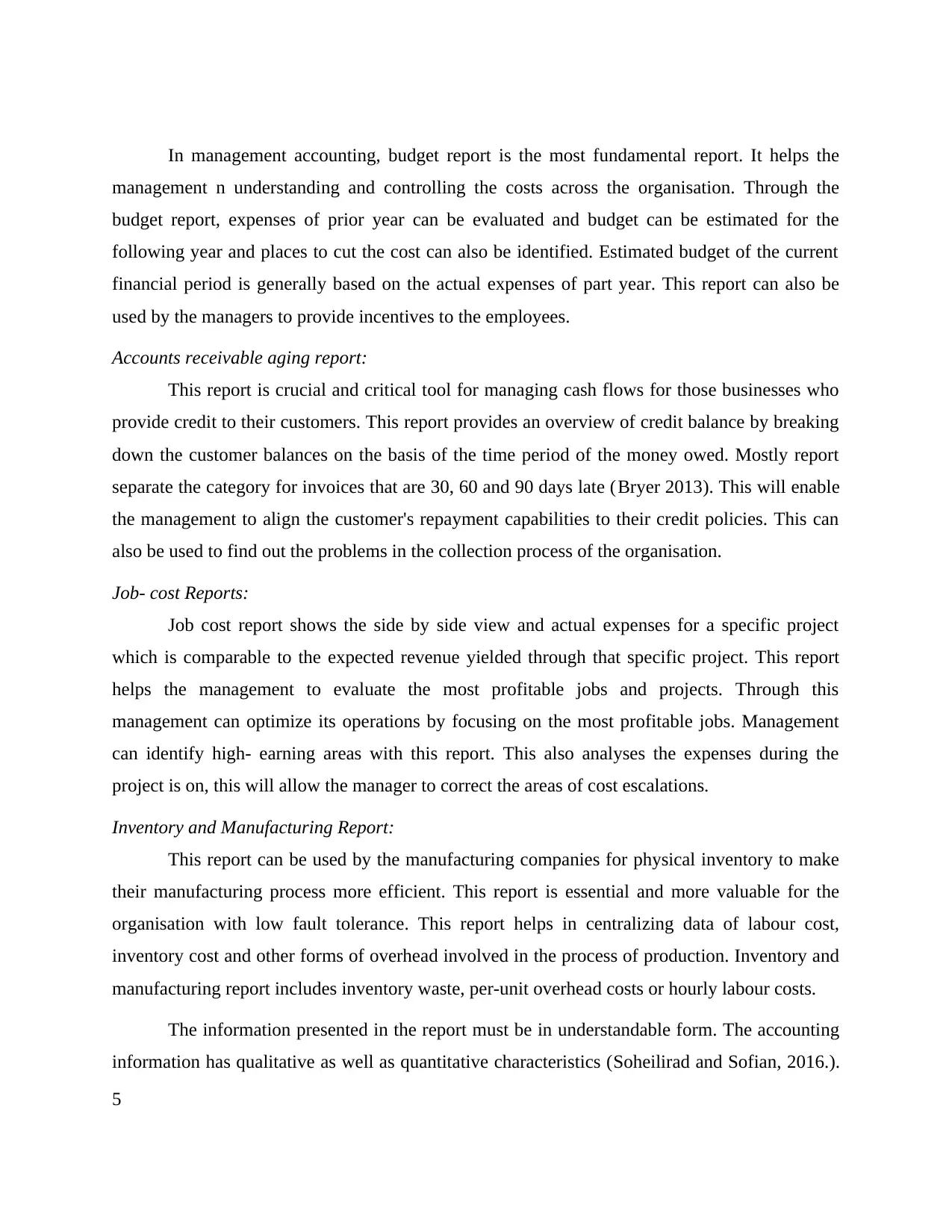

In management accounting, budget report is the most fundamental report. It helps the

management n understanding and controlling the costs across the organisation. Through the

budget report, expenses of prior year can be evaluated and budget can be estimated for the

following year and places to cut the cost can also be identified. Estimated budget of the current

financial period is generally based on the actual expenses of part year. This report can also be

used by the managers to provide incentives to the employees.

Accounts receivable aging report:

This report is crucial and critical tool for managing cash flows for those businesses who

provide credit to their customers. This report provides an overview of credit balance by breaking

down the customer balances on the basis of the time period of the money owed. Mostly report

separate the category for invoices that are 30, 60 and 90 days late (Bryer 2013). This will enable

the management to align the customer's repayment capabilities to their credit policies. This can

also be used to find out the problems in the collection process of the organisation.

Job- cost Reports:

Job cost report shows the side by side view and actual expenses for a specific project

which is comparable to the expected revenue yielded through that specific project. This report

helps the management to evaluate the most profitable jobs and projects. Through this

management can optimize its operations by focusing on the most profitable jobs. Management

can identify high- earning areas with this report. This also analyses the expenses during the

project is on, this will allow the manager to correct the areas of cost escalations.

Inventory and Manufacturing Report:

This report can be used by the manufacturing companies for physical inventory to make

their manufacturing process more efficient. This report is essential and more valuable for the

organisation with low fault tolerance. This report helps in centralizing data of labour cost,

inventory cost and other forms of overhead involved in the process of production. Inventory and

manufacturing report includes inventory waste, per-unit overhead costs or hourly labour costs.

The information presented in the report must be in understandable form. The accounting

information has qualitative as well as quantitative characteristics (Soheilirad and Sofian, 2016.).

5

management n understanding and controlling the costs across the organisation. Through the

budget report, expenses of prior year can be evaluated and budget can be estimated for the

following year and places to cut the cost can also be identified. Estimated budget of the current

financial period is generally based on the actual expenses of part year. This report can also be

used by the managers to provide incentives to the employees.

Accounts receivable aging report:

This report is crucial and critical tool for managing cash flows for those businesses who

provide credit to their customers. This report provides an overview of credit balance by breaking

down the customer balances on the basis of the time period of the money owed. Mostly report

separate the category for invoices that are 30, 60 and 90 days late (Bryer 2013). This will enable

the management to align the customer's repayment capabilities to their credit policies. This can

also be used to find out the problems in the collection process of the organisation.

Job- cost Reports:

Job cost report shows the side by side view and actual expenses for a specific project

which is comparable to the expected revenue yielded through that specific project. This report

helps the management to evaluate the most profitable jobs and projects. Through this

management can optimize its operations by focusing on the most profitable jobs. Management

can identify high- earning areas with this report. This also analyses the expenses during the

project is on, this will allow the manager to correct the areas of cost escalations.

Inventory and Manufacturing Report:

This report can be used by the manufacturing companies for physical inventory to make

their manufacturing process more efficient. This report is essential and more valuable for the

organisation with low fault tolerance. This report helps in centralizing data of labour cost,

inventory cost and other forms of overhead involved in the process of production. Inventory and

manufacturing report includes inventory waste, per-unit overhead costs or hourly labour costs.

The information presented in the report must be in understandable form. The accounting

information has qualitative as well as quantitative characteristics (Soheilirad and Sofian, 2016.).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business reports are used to make various important decisions of the organisation therefore, the

information must be appropriate as inappropriate information can hamper the decisions or it may

provide wrong assessment to the managers. An appropriate report must have following features: Understandable: The information in the report must be understandable as it is the

important qualitative characteristic of financial information. Financial information is

technical and hard to be understood by anyone. For making the information of the report

more understandable, management should appoint the accountant with good skills. A

report that cannot be understood is of no use for the internal as well as external users of

the report. Relevant: the information in the report must be relevant i.e. the information must relate to

the specific time period. While reviewing the financial information, management should

often conduct trend analysis. For example, cost of goods sold would be irrelevant for

inventory management report.

Reliability: The information used in the report must be reliable and not hypothetical. This

will ensure the management that the accounting information presents the accurate picture

of the organisation.

TASK 2

P3. Calculation of cost and preparation of Income statement

Absorption costing- The methods used by management in calculating the cost of product

or an enterprise by taking both direct and indirect cost into account. Direct cost includes

all cost associated with the manufacturing of product including wages for worker, raw

materials used in producing a product and all overheads costs like utility cost. It is also

called as full cost as including all cost like the fixed overhead as well. The direct cost can

be easily identified by individual cost centres and distribution of overhead among the

department is called apportionment (AbRahman and et.al., 2016). The various methods

for absorption are direct material cost percentage rate, direct labour cost percentage rate,

prime cost percentage rate, labour hour rate and the machine hour rate.

6

information must be appropriate as inappropriate information can hamper the decisions or it may

provide wrong assessment to the managers. An appropriate report must have following features: Understandable: The information in the report must be understandable as it is the

important qualitative characteristic of financial information. Financial information is

technical and hard to be understood by anyone. For making the information of the report

more understandable, management should appoint the accountant with good skills. A

report that cannot be understood is of no use for the internal as well as external users of

the report. Relevant: the information in the report must be relevant i.e. the information must relate to

the specific time period. While reviewing the financial information, management should

often conduct trend analysis. For example, cost of goods sold would be irrelevant for

inventory management report.

Reliability: The information used in the report must be reliable and not hypothetical. This

will ensure the management that the accounting information presents the accurate picture

of the organisation.

TASK 2

P3. Calculation of cost and preparation of Income statement

Absorption costing- The methods used by management in calculating the cost of product

or an enterprise by taking both direct and indirect cost into account. Direct cost includes

all cost associated with the manufacturing of product including wages for worker, raw

materials used in producing a product and all overheads costs like utility cost. It is also

called as full cost as including all cost like the fixed overhead as well. The direct cost can

be easily identified by individual cost centres and distribution of overhead among the

department is called apportionment (AbRahman and et.al., 2016). The various methods

for absorption are direct material cost percentage rate, direct labour cost percentage rate,

prime cost percentage rate, labour hour rate and the machine hour rate.

6

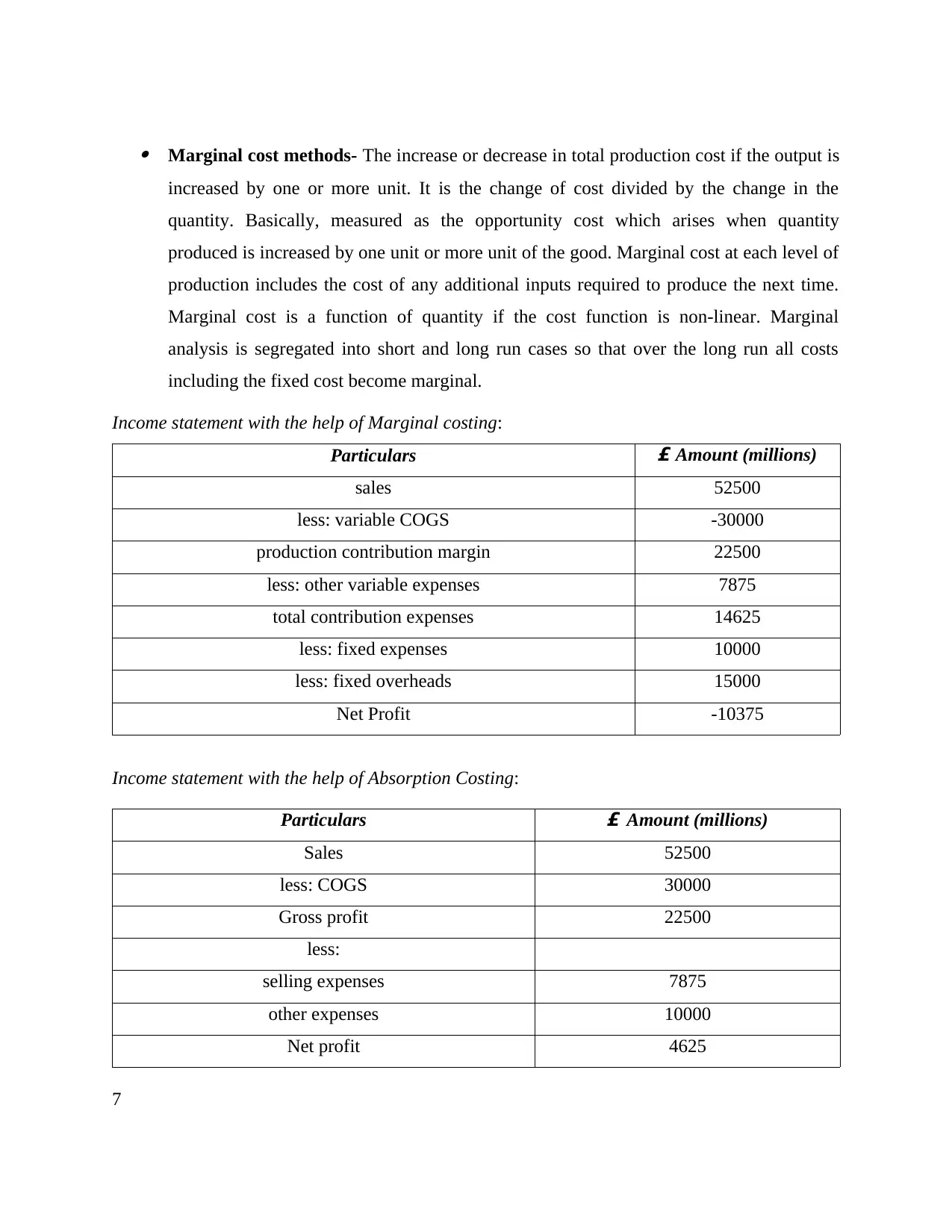

Marginal cost methods- The increase or decrease in total production cost if the output is

increased by one or more unit. It is the change of cost divided by the change in the

quantity. Basically, measured as the opportunity cost which arises when quantity

produced is increased by one unit or more unit of the good. Marginal cost at each level of

production includes the cost of any additional inputs required to produce the next time.

Marginal cost is a function of quantity if the cost function is non-linear. Marginal

analysis is segregated into short and long run cases so that over the long run all costs

including the fixed cost become marginal.

Income statement with the help of Marginal costing:

Particulars £ Amount (millions)

sales 52500

less: variable COGS -30000

production contribution margin 22500

less: other variable expenses 7875

total contribution expenses 14625

less: fixed expenses 10000

less: fixed overheads 15000

Net Profit -10375

Income statement with the help of Absorption Costing:

Particulars £ Amount (millions)

Sales 52500

less: COGS 30000

Gross profit 22500

less:

selling expenses 7875

other expenses 10000

Net profit 4625

7

increased by one or more unit. It is the change of cost divided by the change in the

quantity. Basically, measured as the opportunity cost which arises when quantity

produced is increased by one unit or more unit of the good. Marginal cost at each level of

production includes the cost of any additional inputs required to produce the next time.

Marginal cost is a function of quantity if the cost function is non-linear. Marginal

analysis is segregated into short and long run cases so that over the long run all costs

including the fixed cost become marginal.

Income statement with the help of Marginal costing:

Particulars £ Amount (millions)

sales 52500

less: variable COGS -30000

production contribution margin 22500

less: other variable expenses 7875

total contribution expenses 14625

less: fixed expenses 10000

less: fixed overheads 15000

Net Profit -10375

Income statement with the help of Absorption Costing:

Particulars £ Amount (millions)

Sales 52500

less: COGS 30000

Gross profit 22500

less:

selling expenses 7875

other expenses 10000

Net profit 4625

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: Tech Ltd. should use absorption costing for preparing its income statement as it is

showing net profit of £4625 million, while marginal costing is showing a loss of £10375

million.

TASK 3

P4. Advantages and disadvantages of planning tools for budgetary control

Following types of budget with their advantages and disadvantages are:

Activity- Based Budgeting: This is a budgeting method in which overhead costs are considered

and Activity based costing is used for preparing budgets (Nørreklit, 2014). This method does not

consider the past year budget for preparing the current year budget. High cost incurring activities

are identified and researched in this method. Resources are then allocated based on the outcome

(Activity Based Budgeting, 2017.).

Advantages:

This method evaluates all the cost drivers while considering all the steps in an activity.

This eliminates the irrelevant activity and necessary activities are then focused for the

business.

This helps the business in saving the cost by eliminating all the unnecessary business

activities.

This method views the business as a single unit and top-level managers prepare the

budget for the whole business unit.

With a deep research and analysis this eliminates all the bottlenecks of the activities.

Disadvantages:

This method requires a deep understanding of all the functional areas of the business.

Therefore, manager must be capable of understanding and evaluating all the areas of the

business in a proper manner.

This method is complex in nature.

8

showing net profit of £4625 million, while marginal costing is showing a loss of £10375

million.

TASK 3

P4. Advantages and disadvantages of planning tools for budgetary control

Following types of budget with their advantages and disadvantages are:

Activity- Based Budgeting: This is a budgeting method in which overhead costs are considered

and Activity based costing is used for preparing budgets (Nørreklit, 2014). This method does not

consider the past year budget for preparing the current year budget. High cost incurring activities

are identified and researched in this method. Resources are then allocated based on the outcome

(Activity Based Budgeting, 2017.).

Advantages:

This method evaluates all the cost drivers while considering all the steps in an activity.

This eliminates the irrelevant activity and necessary activities are then focused for the

business.

This helps the business in saving the cost by eliminating all the unnecessary business

activities.

This method views the business as a single unit and top-level managers prepare the

budget for the whole business unit.

With a deep research and analysis this eliminates all the bottlenecks of the activities.

Disadvantages:

This method requires a deep understanding of all the functional areas of the business.

Therefore, manager must be capable of understanding and evaluating all the areas of the

business in a proper manner.

This method is complex in nature.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity- based budgeting consumes lot of resources of the organisation, like highly

trained employees to conduct this method.

Zero- Based Budgeting: Unlike other methods of budgeting, this method assumes prior year

budget base as zero and not the past year expenses and prepares new budget for the next period

from the scratch (Tucker and Parker, 2014). For example, if the past year expenses of the

production department of Tech Ltd. were £5000, then the management cannot claim the £5000

amount for the current year budget. All the expenses need to be justified by the management

before claiming any amount for the budget (Zero-based Budgeting (ZBB), 2012).

Advantages:

It is based on needs, requirements and benefits therefore, effective allocation of

resources.

Cost effective ways can be identified to improve operations.

Increases coordination and communication within the organisation.

Identification and elimination of obsolete and wasteful resources.

Disadvantages:

Difficult to justify expenses for obtaining the amount of budget.

Time consuming as it needs to define decision packages and decision units. Includes all levels therefore, should be understood clearly by various level managers for

successful implementation.

Incremental Budgeting: As per this method to arrive at new budget, small changes are made in

the existing budget. Current fiscal year's budget becomes the base for preparing the budget for

forthcoming year (Khodzytska and Ivchenko, 2014). The management operates at the current

level of budget and in case when needed an additional amount is added to arrive at the budget of

next year.

Advantages:

Very easy to implement and doesn't require complex calculations.

9

trained employees to conduct this method.

Zero- Based Budgeting: Unlike other methods of budgeting, this method assumes prior year

budget base as zero and not the past year expenses and prepares new budget for the next period

from the scratch (Tucker and Parker, 2014). For example, if the past year expenses of the

production department of Tech Ltd. were £5000, then the management cannot claim the £5000

amount for the current year budget. All the expenses need to be justified by the management

before claiming any amount for the budget (Zero-based Budgeting (ZBB), 2012).

Advantages:

It is based on needs, requirements and benefits therefore, effective allocation of

resources.

Cost effective ways can be identified to improve operations.

Increases coordination and communication within the organisation.

Identification and elimination of obsolete and wasteful resources.

Disadvantages:

Difficult to justify expenses for obtaining the amount of budget.

Time consuming as it needs to define decision packages and decision units. Includes all levels therefore, should be understood clearly by various level managers for

successful implementation.

Incremental Budgeting: As per this method to arrive at new budget, small changes are made in

the existing budget. Current fiscal year's budget becomes the base for preparing the budget for

forthcoming year (Khodzytska and Ivchenko, 2014). The management operates at the current

level of budget and in case when needed an additional amount is added to arrive at the budget of

next year.

Advantages:

Very easy to implement and doesn't require complex calculations.

9

No detailed analysis is required and ensures continuity of funding.

Provides immediate reflection of the impact of change.

Simple to understand and prepare.

Disadvantages:

No incentives are provided in innovation and development.

Encourages more spending for the budget.

Doesn't eliminate non-effective operations.

There can be three phases of budgeting process. Tech Ltd. may use the following budget

preparation process:

Illustration 1: Budgeting Process

1. Obtaining the estimates: The company should obtain the estimates regarding to its sales,

expected cost, production level and availability of resources. Department heads are

required to provide future estimates of the activities that can have an impact on the

company.

2. Coordinating the Estimates: Various plans of the different organisational units are

evaluated by the budget committees in the organisation for the determination of

potentiality of the plans.

10

Provides immediate reflection of the impact of change.

Simple to understand and prepare.

Disadvantages:

No incentives are provided in innovation and development.

Encourages more spending for the budget.

Doesn't eliminate non-effective operations.

There can be three phases of budgeting process. Tech Ltd. may use the following budget

preparation process:

Illustration 1: Budgeting Process

1. Obtaining the estimates: The company should obtain the estimates regarding to its sales,

expected cost, production level and availability of resources. Department heads are

required to provide future estimates of the activities that can have an impact on the

company.

2. Coordinating the Estimates: Various plans of the different organisational units are

evaluated by the budget committees in the organisation for the determination of

potentiality of the plans.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.