Comprehensive Report on Management Accounting for Business Operations

VerifiedAdded on 2020/12/09

|16

|5215

|157

Report

AI Summary

This report delves into the intricacies of management accounting, focusing on its application within the internal management of organizations. It comprehensively examines various accounting systems, including price optimization, inventory management, and cost accounting, and their essential requirements. The report uses L&B Haulage civil engineering contractors limited as a case study to illustrate the practical application of these systems, particularly in construction projects. It details different methods for management accounting reporting, such as budgetary reports, inventory cost reports, performance reports, and cost managerial accounting reports. The report also highlights the benefits of each accounting system and how they integrate within organizational processes. Furthermore, it compares marginal costing and absorption costing methods and their impact on net profit calculations. Overall, the report provides a detailed overview of management accounting principles and practices, emphasizing their significance in financial decision-making and performance evaluation.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Part (A) ........................................................................................................................................1

Part(B)..........................................................................................................................................5

ANNEX (A) Question 2...............................................................................................................5

ANNEX (B)................................................................................................................................6

ACTIVITY 2....................................................................................................................................8

PART(A)......................................................................................................................................8

ANNEX C..................................................................................................................................10

PART (B)...................................................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Part (A) ........................................................................................................................................1

Part(B)..........................................................................................................................................5

ANNEX (A) Question 2...............................................................................................................5

ANNEX (B)................................................................................................................................6

ACTIVITY 2....................................................................................................................................8

PART(A)......................................................................................................................................8

ANNEX C..................................................................................................................................10

PART (B)...................................................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is a type of accounting system that is related to internal

management of the organisations. It consists both kind of information including financial and

non financial. Eventually, management accounting is a wide term which is being used by the

companies to proper management of different functions (Abdelmoneim Mohamed and Jones,

2014). This project report describes in detail about this accounting system including its different

types, their benefits and drawbacks. As well as various planning tools in context to performance

management. Apart from it, report states about the role of management accounting in solving the

financial problems. Herein, the L&B haulage civil engineering contractors limited company is

selected. It was evolved thirty years ago and this company provides services like civil

engineering contracts, recycle and waste management project etc. Majorly this company deals in

construction project.

ACTIVITY 1.

Part (A)

Management accounting system and their essential requirement:

In the context of internal management of the organisations, management accounting plays

a crucial role (Armitage, Webb and Glynn, 2016). This is why because managers use all the

needed information from this accounting system. The basic mean of management accounting

system is the monitoring, analysing, interpreting the financial data in order to take important

decisions. One of the best feature of this accounting system is that it consists monetary and non

monetary information which becomes basis of internal decision making. Additionally, this

accounting system does not require any audit as well as it is not mandatory. The L&B haulage

civil engineering contractors limited implements this accounting system for proper management

of their various kind of civil and construction projects. The management accounting includes a

wide range of accounting systems that are being used by the companies for their different kind of

functions and applications. Herein, the essential requirements of the different accounting systems

are mentioned as below:

Price optimisation system- The price optimisation system is a kind of accounting system

that is related to the determination of right price of different kind of products and services

( Boučková, 2015). As well as this accounting system provides a basis for analysing the

Management accounting is a type of accounting system that is related to internal

management of the organisations. It consists both kind of information including financial and

non financial. Eventually, management accounting is a wide term which is being used by the

companies to proper management of different functions (Abdelmoneim Mohamed and Jones,

2014). This project report describes in detail about this accounting system including its different

types, their benefits and drawbacks. As well as various planning tools in context to performance

management. Apart from it, report states about the role of management accounting in solving the

financial problems. Herein, the L&B haulage civil engineering contractors limited company is

selected. It was evolved thirty years ago and this company provides services like civil

engineering contracts, recycle and waste management project etc. Majorly this company deals in

construction project.

ACTIVITY 1.

Part (A)

Management accounting system and their essential requirement:

In the context of internal management of the organisations, management accounting plays

a crucial role (Armitage, Webb and Glynn, 2016). This is why because managers use all the

needed information from this accounting system. The basic mean of management accounting

system is the monitoring, analysing, interpreting the financial data in order to take important

decisions. One of the best feature of this accounting system is that it consists monetary and non

monetary information which becomes basis of internal decision making. Additionally, this

accounting system does not require any audit as well as it is not mandatory. The L&B haulage

civil engineering contractors limited implements this accounting system for proper management

of their various kind of civil and construction projects. The management accounting includes a

wide range of accounting systems that are being used by the companies for their different kind of

functions and applications. Herein, the essential requirements of the different accounting systems

are mentioned as below:

Price optimisation system- The price optimisation system is a kind of accounting system

that is related to the determination of right price of different kind of products and services

( Boučková, 2015). As well as this accounting system provides a basis for analysing the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

customer reaction on different pricing levels. Due to this companies enables to evaluate

the impact of change in price level. Additionally, price optimisation system helps in

providing guidance in assigning accurate level of price which is suitable for both to the

customers as well as for company. Herein, the context of the L&B haulage civil

engineering contractors limited they use price optimisation system for assigning right

price of different civil projects. Due to this, they analyse their clients reaction on the

different pricing level. Apart from it, price optimisation is majorly required for fixing the

level of price that can satisfy both to the customers and company.

Inventory management system- Inventory management system is an accounting system

that is related to the proper management of the raw material as well as of finished goods.

Due to this accounting system, companies can check movement of goods in entire supply

chain system. Additionally, it helps in checking the level of raw material and prepared

goods in the ware houses. In the context of L&B haulage civil engineering contractors

limited company this is useful in checking the quantity of raw material and because of

this they can purchase right quantity of material of construction. As well as this

accounting system is required for ensuring the quantity of goods and material so that

company can order for new material accordingly. Eventually, in the absence of this

accounting system companies can not asses the need of purchasing new material and that

can result in lose (Cleary, 2015).

Cost accounting system- As the name assists this accounting system is related to the

calculation of cost of different products and services. The main purpose of this

accounting system is to evaluate the profitability of products and services by comparing

cost with the actual money earned. This accounting system is required for analysing

which products are profitable and which ones are not. L&B haulage civil engineering

contractors limited applies this accounting system to check the cost of different projects

and to evaluate the profitability of each projects. With the help of this accounting system,

in the end of any project, they can check that which civil project is beneficial and which

one is not. Basically, this accounting system includes two accounting systems which are

as follows:

Process costing- This costing system is useful for evaluating the cost at different stages. Like in

the above mentioned company, they can check the cost at different step of construction projects.

the impact of change in price level. Additionally, price optimisation system helps in

providing guidance in assigning accurate level of price which is suitable for both to the

customers as well as for company. Herein, the context of the L&B haulage civil

engineering contractors limited they use price optimisation system for assigning right

price of different civil projects. Due to this, they analyse their clients reaction on the

different pricing level. Apart from it, price optimisation is majorly required for fixing the

level of price that can satisfy both to the customers and company.

Inventory management system- Inventory management system is an accounting system

that is related to the proper management of the raw material as well as of finished goods.

Due to this accounting system, companies can check movement of goods in entire supply

chain system. Additionally, it helps in checking the level of raw material and prepared

goods in the ware houses. In the context of L&B haulage civil engineering contractors

limited company this is useful in checking the quantity of raw material and because of

this they can purchase right quantity of material of construction. As well as this

accounting system is required for ensuring the quantity of goods and material so that

company can order for new material accordingly. Eventually, in the absence of this

accounting system companies can not asses the need of purchasing new material and that

can result in lose (Cleary, 2015).

Cost accounting system- As the name assists this accounting system is related to the

calculation of cost of different products and services. The main purpose of this

accounting system is to evaluate the profitability of products and services by comparing

cost with the actual money earned. This accounting system is required for analysing

which products are profitable and which ones are not. L&B haulage civil engineering

contractors limited applies this accounting system to check the cost of different projects

and to evaluate the profitability of each projects. With the help of this accounting system,

in the end of any project, they can check that which civil project is beneficial and which

one is not. Basically, this accounting system includes two accounting systems which are

as follows:

Process costing- This costing system is useful for evaluating the cost at different stages. Like in

the above mentioned company, they can check the cost at different step of construction projects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job order costing system- Job order costing system is important in calculating cost of each job

involved in any particular activity of product manufacturing or service providing. Herein, the

context of L&B haulage civil engineering contractors limited company, they apply this costing

system for computing cost of each job involved in any particular project (Collis and Hussey,

2017).

Different method for management accounting reporting:

The management accounting reporting is consists various kind of reports which are useful

for both to the internal management and for external stakeholders. Eventually, these accounting

reports are prepared with the use different methods. There are various kind of methods that are

being used by the L&B haulage civil engineering contractors limited company. Some of these

methods are mentioned below:

Budgetary reports - Budgets are also known by the financial plan. It is just estimation of

future income and expenditure. This is very important method for preparation of management

accounting reporting. This is why because it consists different kind of needed financial

information for making the reports. Eventually, it includes two types of informations one is

estimated income and expenditure and another one is actual income, expenditure. If actual

income is more then estimated income then, performance will be best, on the other hand if actual

income is below to the targeted income the, performance will be low. So these types of

informations becomes useful in preparation of the management accounting reporting. Herein, the

context of L&B haulage civil engineering contractors limited company they use this tool for

making their accounting reports (Edwards, 2013).

Inventory cost reports- It is a kind of method which is used for identifying different

assigned cost incurred at particular inventory store. This is helpful in computing overall storage

cost that is assigned in the different stores. Eventually, it is an important method of preparation

of inventory management accounting reports. It provides a base for making strategies and plans

to control storage, caring and ordering cost. It contains all needed cost related informations.

Herein, the aspect of L&B haulage civil engineering contractors limited company they make

these reports to evaluate the inventory costs as well as to check efficiency of inventory system.

Performance reports- Performance reports are used for evaluating the financial and non

financial performance of the organisation (Endenich, 2014). As well as these reports include the

comparison of actual generated income with the actual income earned. Herein, the aspect of

involved in any particular activity of product manufacturing or service providing. Herein, the

context of L&B haulage civil engineering contractors limited company, they apply this costing

system for computing cost of each job involved in any particular project (Collis and Hussey,

2017).

Different method for management accounting reporting:

The management accounting reporting is consists various kind of reports which are useful

for both to the internal management and for external stakeholders. Eventually, these accounting

reports are prepared with the use different methods. There are various kind of methods that are

being used by the L&B haulage civil engineering contractors limited company. Some of these

methods are mentioned below:

Budgetary reports - Budgets are also known by the financial plan. It is just estimation of

future income and expenditure. This is very important method for preparation of management

accounting reporting. This is why because it consists different kind of needed financial

information for making the reports. Eventually, it includes two types of informations one is

estimated income and expenditure and another one is actual income, expenditure. If actual

income is more then estimated income then, performance will be best, on the other hand if actual

income is below to the targeted income the, performance will be low. So these types of

informations becomes useful in preparation of the management accounting reporting. Herein, the

context of L&B haulage civil engineering contractors limited company they use this tool for

making their accounting reports (Edwards, 2013).

Inventory cost reports- It is a kind of method which is used for identifying different

assigned cost incurred at particular inventory store. This is helpful in computing overall storage

cost that is assigned in the different stores. Eventually, it is an important method of preparation

of inventory management accounting reports. It provides a base for making strategies and plans

to control storage, caring and ordering cost. It contains all needed cost related informations.

Herein, the aspect of L&B haulage civil engineering contractors limited company they make

these reports to evaluate the inventory costs as well as to check efficiency of inventory system.

Performance reports- Performance reports are used for evaluating the financial and non

financial performance of the organisation (Endenich, 2014). As well as these reports include the

comparison of actual generated income with the actual income earned. Herein, the aspect of

L&B haulage civil engineering contractors limited company they make these reports to check the

financial performance of different engineering projects. Due to this they can evaluate the

efficiency of their projects by comparing the earned revenue with the estimated income level.

Eventually, this report helps them in changing the policies and plans if performance is low.

Cost managerial accounting reports- These accounting reports are those reports which

consist information regarding to the cost. In broad sense, these types of accounting reports

includes raw material cost, labour cost, overhead etc. Eventually, cost managerial accounting

reports help in evaluating the cost so that organisations can make suitable decisions if cost occurs

high. The L&B haulage civil engineering contractors limited company makes this accounting

report for analysing the cost of different projects. As well as it contains the information regarding

to the cost in broad sense. This detailed information helps in keeping an extra sight of eye on the

cost of construction projects.

Benefits of different accounting systems and their application in context to organisational

process:

The various method of management accounting system have their own importance in

aspect of different companies. Eventually, it all depends on the nature of organisation that how

can it helps them. Herein, the aspect of L&B haulage civil engineering contractors limited

company they are using some management accounting systems which are as follows.

Benefits of price optimisation system- It is useful in determination of accurate price of

products and services (Grabner and Moers, 2013). This accounting system is helpful for

above selected company as it helps in assigning right price of various kind of engineering

and construction projects. As well as it also important for them in evaluating their

customers reaction on different pricing levels.

Benefits of inventory management system- The inventory management system is useful

in tracking the movement of goods in entire supply chain. As well as checking the

quantity of raw material in the warehouses. In the aspect of L&B haulage civil

engineering contractors limited company, it is helpful in checking the quantity of raw

material for construction projects.

Benefits of cost accounting system- Cost accounting system is important in calculating

overall cost of production. In the L&B haulage civil engineering contractors limited

financial performance of different engineering projects. Due to this they can evaluate the

efficiency of their projects by comparing the earned revenue with the estimated income level.

Eventually, this report helps them in changing the policies and plans if performance is low.

Cost managerial accounting reports- These accounting reports are those reports which

consist information regarding to the cost. In broad sense, these types of accounting reports

includes raw material cost, labour cost, overhead etc. Eventually, cost managerial accounting

reports help in evaluating the cost so that organisations can make suitable decisions if cost occurs

high. The L&B haulage civil engineering contractors limited company makes this accounting

report for analysing the cost of different projects. As well as it contains the information regarding

to the cost in broad sense. This detailed information helps in keeping an extra sight of eye on the

cost of construction projects.

Benefits of different accounting systems and their application in context to organisational

process:

The various method of management accounting system have their own importance in

aspect of different companies. Eventually, it all depends on the nature of organisation that how

can it helps them. Herein, the aspect of L&B haulage civil engineering contractors limited

company they are using some management accounting systems which are as follows.

Benefits of price optimisation system- It is useful in determination of accurate price of

products and services (Grabner and Moers, 2013). This accounting system is helpful for

above selected company as it helps in assigning right price of various kind of engineering

and construction projects. As well as it also important for them in evaluating their

customers reaction on different pricing levels.

Benefits of inventory management system- The inventory management system is useful

in tracking the movement of goods in entire supply chain. As well as checking the

quantity of raw material in the warehouses. In the aspect of L&B haulage civil

engineering contractors limited company, it is helpful in checking the quantity of raw

material for construction projects.

Benefits of cost accounting system- Cost accounting system is important in calculating

overall cost of production. In the L&B haulage civil engineering contractors limited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company, it is useful in computing total cost of different civil engineering projects. As

well as with the help of this accounting system, they can evaluate the efficiency of

various projects (Holsapple, 2013).

Management accounting system and reporting are integrated within the organisational processes.

The management accounting system and management accounting reporting are

interrelated with the organisational processes (Maskell, Baggaley and Grasso, 2016). This is why

because management accounting system includes different accounting systems like inventory

management system, price optimisation system etc. All these accounting systems are linked up

with the preparation of management accounting reports because needed information comes from

these accounting systems. In the absence of this link, it would be difficult to prepare the

accounting reports. Herein, the context of L&B haulage civil engineering contractors limited

company they use a wide range of management accounting systems(inventory management

system, price optimisation system, cost accounting system) in their projects. Due to these

accounting systems they get all needed information for preparation of accounting reports like

budgetary reports, inventory cost reports, cost managerial reports and performance reports.

Overall this link between management accounting system and accounting reports is interrelated

with the organisational process.

Part(B)

ANNEX (A) Question 2.

Marginal costing method- This costing method is a kind of costing method in which

variable costs are considered as the unit cost (Morden, 2016). On the other hand, fixed costs are

written off against the contribution.

Absorption costing method- Absorption costing method considers all the cost which

occurs in the production including the fixed and variable cost (Schaltegger, Burritt and Petersen,

2017). This costing method is required for income tax reporting and external financing reporting.

Calculating of net profit with MARGINAL COSTING

PARTICULARS AMOUNT

SALES 427500 427500

well as with the help of this accounting system, they can evaluate the efficiency of

various projects (Holsapple, 2013).

Management accounting system and reporting are integrated within the organisational processes.

The management accounting system and management accounting reporting are

interrelated with the organisational processes (Maskell, Baggaley and Grasso, 2016). This is why

because management accounting system includes different accounting systems like inventory

management system, price optimisation system etc. All these accounting systems are linked up

with the preparation of management accounting reports because needed information comes from

these accounting systems. In the absence of this link, it would be difficult to prepare the

accounting reports. Herein, the context of L&B haulage civil engineering contractors limited

company they use a wide range of management accounting systems(inventory management

system, price optimisation system, cost accounting system) in their projects. Due to these

accounting systems they get all needed information for preparation of accounting reports like

budgetary reports, inventory cost reports, cost managerial reports and performance reports.

Overall this link between management accounting system and accounting reports is interrelated

with the organisational process.

Part(B)

ANNEX (A) Question 2.

Marginal costing method- This costing method is a kind of costing method in which

variable costs are considered as the unit cost (Morden, 2016). On the other hand, fixed costs are

written off against the contribution.

Absorption costing method- Absorption costing method considers all the cost which

occurs in the production including the fixed and variable cost (Schaltegger, Burritt and Petersen,

2017). This costing method is required for income tax reporting and external financing reporting.

Calculating of net profit with MARGINAL COSTING

PARTICULARS AMOUNT

SALES 427500 427500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

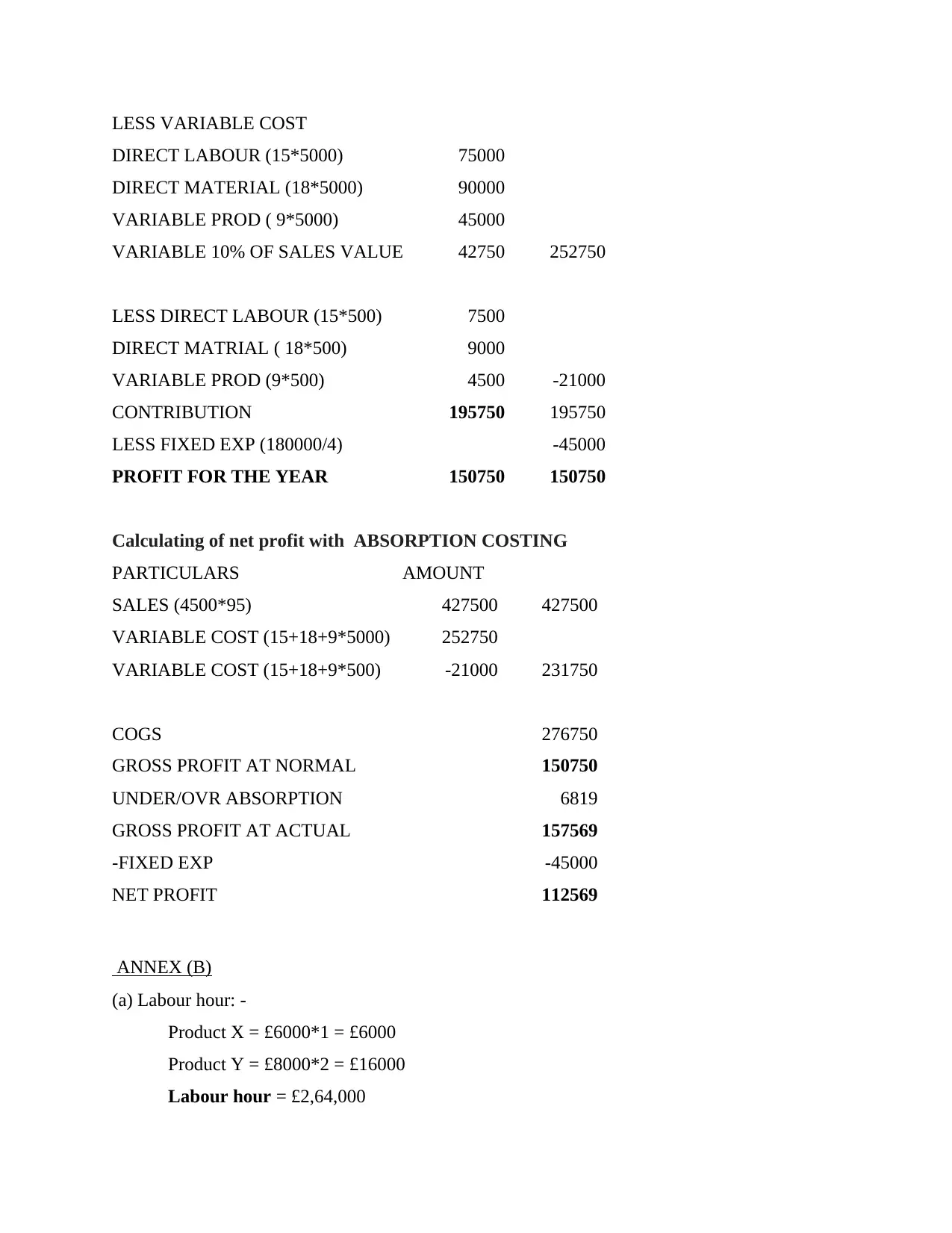

LESS VARIABLE COST

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Calculating of net profit with ABSORPTION COSTING

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

VARIABLE COST (15+18+9*5000) 252750

VARIABLE COST (15+18+9*500) -21000 231750

COGS 276750

GROSS PROFIT AT NORMAL 150750

UNDER/OVR ABSORPTION 6819

GROSS PROFIT AT ACTUAL 157569

-FIXED EXP -45000

NET PROFIT 112569

ANNEX (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Calculating of net profit with ABSORPTION COSTING

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

VARIABLE COST (15+18+9*5000) 252750

VARIABLE COST (15+18+9*500) -21000 231750

COGS 276750

GROSS PROFIT AT NORMAL 150750

UNDER/OVR ABSORPTION 6819

GROSS PROFIT AT ACTUAL 157569

-FIXED EXP -45000

NET PROFIT 112569

ANNEX (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

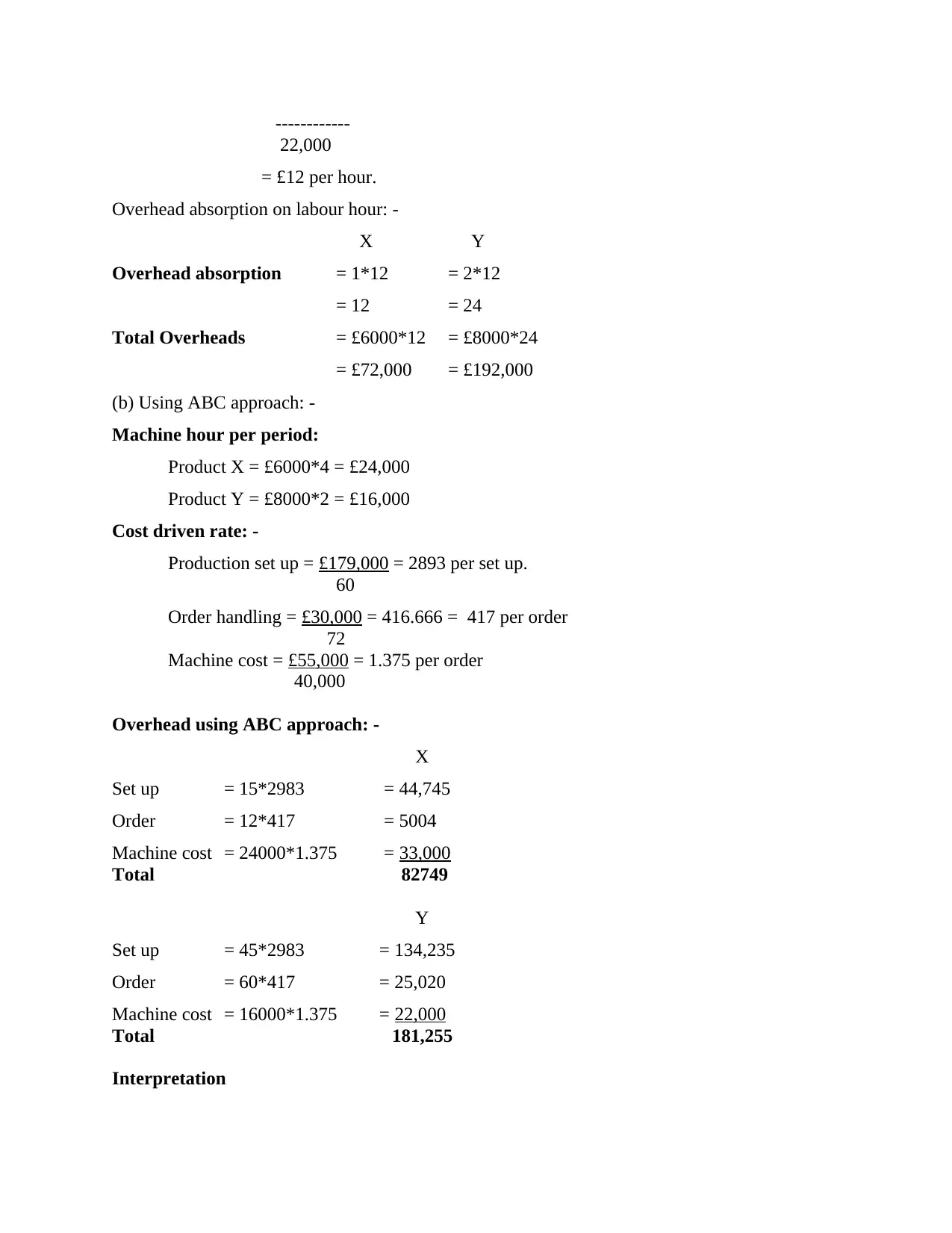

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

Interpretation

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

Interpretation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From above solved numerical it has been analysed that both products X and Y are

incurring different level of costs in the conventional absorption costing method. Product X is

incurring £72,000 cost, on the other hand product Y is occurring the cost of £192,000. In the

activity based costing approach, the machine hour rate per period in product X is of £24,000 and

in product Y is of £16,000. As well as overheads are also different in activity based

costing(ABC) system. The product X is incurring the cost of £82749 and product Y is occurring

cost of £181,255.

ACTIVITY 2.

PART(A)

Planning tools and their advantage- disadvantage.

Budget: This is an estimation of budget which is used in organisation to get fixed amount

of income and expenses in order to run a business speedily. It helps to get estimate of available

resources, expenses and revenues during a particular period of time that shows a interpretation of

future financial goals and situations. Any organisation sets a budget before start a business

activities that gives ideas how much needs to invest to achieve the goals which is decided by the

business concern in order to increase the turnover (Takeda and Boyns, 2014).

Planning tools: Planning tools are the techniques of the organisation that is used to

control the budget and increase profit margin by controlling the cost of the enterprises. L&B

haulage used different types of planning tools for ascertaining the cost of the oragnisation and

make it profitable by overcoming the cost.

Budgetary control: This is the process of defining budgeted results with actual results

for an enterprise. It helps to control the excess budget after comparing budgeted results with

actual results in a fixed period of time. Manager of L&B haulage company prepare an estimation

and compares with actual results for the future period. It helps to make planning and

coordinating with the employees of the organisation. In other words, it is called end results of the

enterprises that focuses on controlling the cost by preparing the budget and performing the

responsibility. Manager of L&B haulage uses this process to control the budget and prepares

budgetary reports that is used to construct high profile building in reasonable budget. Thus,

incurring different level of costs in the conventional absorption costing method. Product X is

incurring £72,000 cost, on the other hand product Y is occurring the cost of £192,000. In the

activity based costing approach, the machine hour rate per period in product X is of £24,000 and

in product Y is of £16,000. As well as overheads are also different in activity based

costing(ABC) system. The product X is incurring the cost of £82749 and product Y is occurring

cost of £181,255.

ACTIVITY 2.

PART(A)

Planning tools and their advantage- disadvantage.

Budget: This is an estimation of budget which is used in organisation to get fixed amount

of income and expenses in order to run a business speedily. It helps to get estimate of available

resources, expenses and revenues during a particular period of time that shows a interpretation of

future financial goals and situations. Any organisation sets a budget before start a business

activities that gives ideas how much needs to invest to achieve the goals which is decided by the

business concern in order to increase the turnover (Takeda and Boyns, 2014).

Planning tools: Planning tools are the techniques of the organisation that is used to

control the budget and increase profit margin by controlling the cost of the enterprises. L&B

haulage used different types of planning tools for ascertaining the cost of the oragnisation and

make it profitable by overcoming the cost.

Budgetary control: This is the process of defining budgeted results with actual results

for an enterprise. It helps to control the excess budget after comparing budgeted results with

actual results in a fixed period of time. Manager of L&B haulage company prepare an estimation

and compares with actual results for the future period. It helps to make planning and

coordinating with the employees of the organisation. In other words, it is called end results of the

enterprises that focuses on controlling the cost by preparing the budget and performing the

responsibility. Manager of L&B haulage uses this process to control the budget and prepares

budgetary reports that is used to construct high profile building in reasonable budget. Thus,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budgetary control is an important aspect of the company that helps to save time and money by

preparing budget estimation. The company is using different types of budget such as-

Zero base budget: This is the most important tool whi9ch is used to control the budget

by preparing the budget from the zero base. It contains re evaluating of the budget that shows

cash flow statement by defining all the expenses. Therefore, zero base budgeting is used to set

the budget where all expenses are started with new period and new budget which are occurred in

the organisation. The manager of L&B haulage can use this tool to know the actual amount of

revenues and expenses that incurred in reality. In this method each activity need to be justified

clearly that involves actual cost of the company (.Zoni, Dossi and Morelli, 2012).

Advantages: It helps to provides an accurate information about revenues and incomes

that is used to compute the operation cost. It is used to allocate the resources efficiently in L&B

haulage organisation that helps to make profits.

Disadvantages: To apply this tool needs to face challenges such as there is required high

man power who can work extra and need to expertise person. So it may be a drawback for L&B

haulage to hire large number of employees that should be highly experienced.

Incremental budget: This budget is used to prepare current year's budget by changing in

the past year's budget. It is basis on the previous year's budget that helps to give ideas about

current year's budget. The manager of L&B haulage used this tool to prepare incremental budget

with the helps to past year's budget. Such as L&B company finds that there is require to more

expenses in order to build a building then it can make changes in past year's budget.

Advantages: It helps to ignore the wasteful expenses with the help of previous year's

budget. It gives an estimation of expenses and revenues that is used to get estimation of profits

and can control the upcoming risk in L&B haulage organisation. Moreover, it is easy to prepare

because it does not need any specific qualification (Hasniza Haron, Kamal Abdul Rahmanand

Smith, 2013).

Disadvantages: It has demerits also such as manager need to spend more during business

activities. It may be wrong because it depends on past year's information. At the time of

preparing incremental budget there may be chances of risk because of high spendings.

Rolling budget: This means ongoing budget which is used to show the waves ashore on

the beach. Anew waves comes and replace this with last waves that helps to set the financial

plans. Moreover, rolling budget is used to replacing the old budget with new budget by using

preparing budget estimation. The company is using different types of budget such as-

Zero base budget: This is the most important tool whi9ch is used to control the budget

by preparing the budget from the zero base. It contains re evaluating of the budget that shows

cash flow statement by defining all the expenses. Therefore, zero base budgeting is used to set

the budget where all expenses are started with new period and new budget which are occurred in

the organisation. The manager of L&B haulage can use this tool to know the actual amount of

revenues and expenses that incurred in reality. In this method each activity need to be justified

clearly that involves actual cost of the company (.Zoni, Dossi and Morelli, 2012).

Advantages: It helps to provides an accurate information about revenues and incomes

that is used to compute the operation cost. It is used to allocate the resources efficiently in L&B

haulage organisation that helps to make profits.

Disadvantages: To apply this tool needs to face challenges such as there is required high

man power who can work extra and need to expertise person. So it may be a drawback for L&B

haulage to hire large number of employees that should be highly experienced.

Incremental budget: This budget is used to prepare current year's budget by changing in

the past year's budget. It is basis on the previous year's budget that helps to give ideas about

current year's budget. The manager of L&B haulage used this tool to prepare incremental budget

with the helps to past year's budget. Such as L&B company finds that there is require to more

expenses in order to build a building then it can make changes in past year's budget.

Advantages: It helps to ignore the wasteful expenses with the help of previous year's

budget. It gives an estimation of expenses and revenues that is used to get estimation of profits

and can control the upcoming risk in L&B haulage organisation. Moreover, it is easy to prepare

because it does not need any specific qualification (Hasniza Haron, Kamal Abdul Rahmanand

Smith, 2013).

Disadvantages: It has demerits also such as manager need to spend more during business

activities. It may be wrong because it depends on past year's information. At the time of

preparing incremental budget there may be chances of risk because of high spendings.

Rolling budget: This means ongoing budget which is used to show the waves ashore on

the beach. Anew waves comes and replace this with last waves that helps to set the financial

plans. Moreover, rolling budget is used to replacing the old budget with new budget by using

budgeting system. The Management of L&B haulage prepares the rolling budget that allows to

allocate the funds among performing and non performing business activities.

Advantages: It helps L&B haulage to prevents from creation of debt and critical

situation that can be arise in business organisation. Moreover, it helps to save the funds and

reduce the inefficiencies by maintaining rolling budget.

Disadvantages: It is time consuming process that takes too much time to understand and

preparing the rolling budget. And it requires highly skilled and experienced person who can

replace old budget with new budget.

Analysis the use of different planning tools and their application for preparing and forecasting

the budget

Planning tools are very useful in any organisation which helps to prepare and forecasting

the budget that gives suggestion what need to do and when need to do in order to make make

profitable organisation by reducing cost. Through application of above mentioned planning tools

such as zero base budget, rolling budget and incremental budget an organisation can perform

well and can make future budgeting that helps to get information about future planning of the

enterprises. Such as L&B haulage uses zero base budget that helps to give information about

actual cost and incomes which helps to maintain profits. By application of rolling budget L&B

can replace the old budget and with new budget that will helps to give information about new

budget with the help of past budget. Moreover, any organisation can use incremental budget that

helps to make more profits by making some changes in the budget that helps to control over the

excess budget in the organisation that leads to future forecasting.

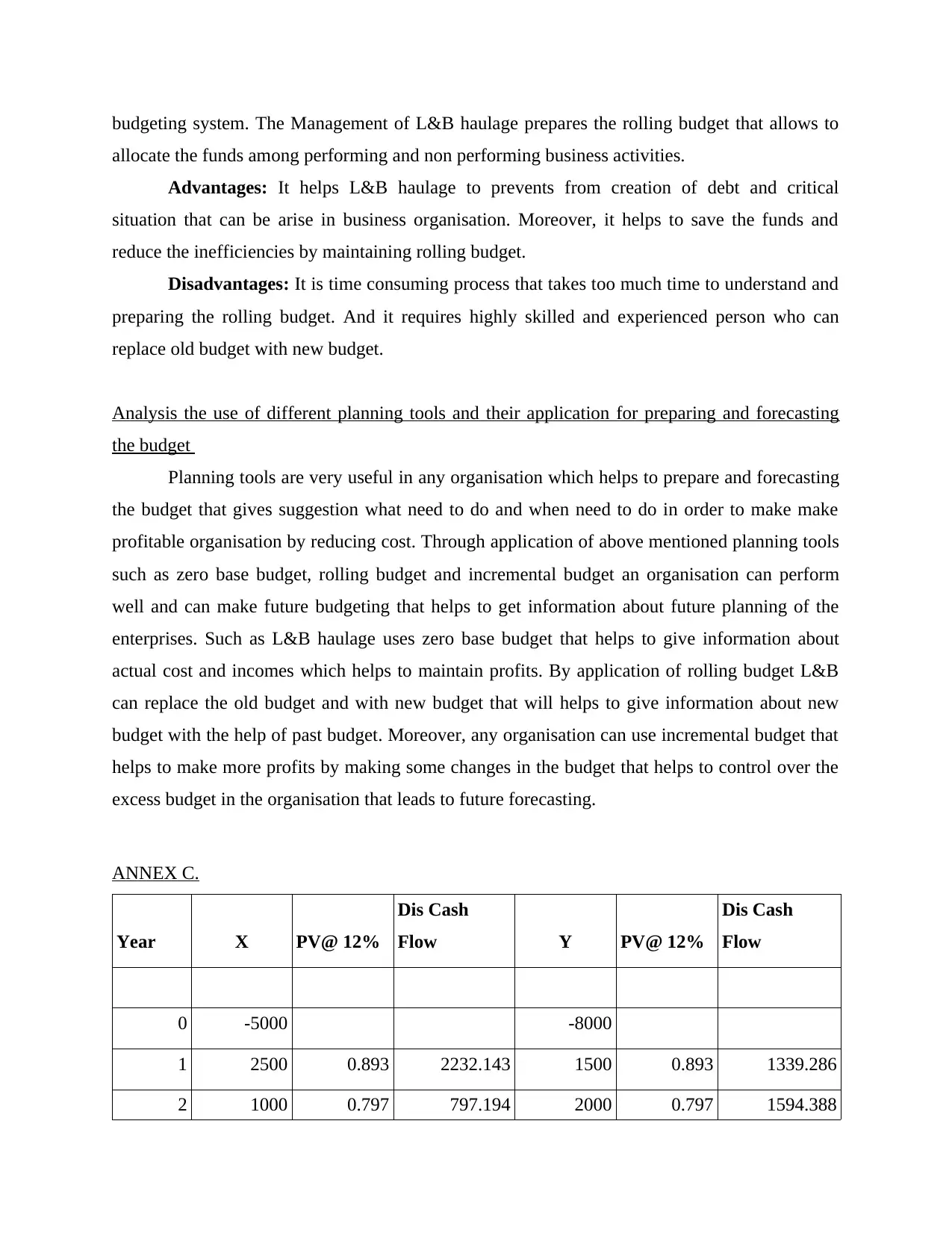

ANNEX C.

Year X PV@ 12%

Dis Cash

Flow Y PV@ 12%

Dis Cash

Flow

0 -5000 -8000

1 2500 0.893 2232.143 1500 0.893 1339.286

2 1000 0.797 797.194 2000 0.797 1594.388

allocate the funds among performing and non performing business activities.

Advantages: It helps L&B haulage to prevents from creation of debt and critical

situation that can be arise in business organisation. Moreover, it helps to save the funds and

reduce the inefficiencies by maintaining rolling budget.

Disadvantages: It is time consuming process that takes too much time to understand and

preparing the rolling budget. And it requires highly skilled and experienced person who can

replace old budget with new budget.

Analysis the use of different planning tools and their application for preparing and forecasting

the budget

Planning tools are very useful in any organisation which helps to prepare and forecasting

the budget that gives suggestion what need to do and when need to do in order to make make

profitable organisation by reducing cost. Through application of above mentioned planning tools

such as zero base budget, rolling budget and incremental budget an organisation can perform

well and can make future budgeting that helps to get information about future planning of the

enterprises. Such as L&B haulage uses zero base budget that helps to give information about

actual cost and incomes which helps to maintain profits. By application of rolling budget L&B

can replace the old budget and with new budget that will helps to give information about new

budget with the help of past budget. Moreover, any organisation can use incremental budget that

helps to make more profits by making some changes in the budget that helps to control over the

excess budget in the organisation that leads to future forecasting.

ANNEX C.

Year X PV@ 12%

Dis Cash

Flow Y PV@ 12%

Dis Cash

Flow

0 -5000 -8000

1 2500 0.893 2232.143 1500 0.893 1339.286

2 1000 0.797 797.194 2000 0.797 1594.388

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.