Management Accounting Systems, Applications, and Analysis: KEF Limited

VerifiedAdded on 2023/01/16

|16

|3237

|57

Report

AI Summary

This report provides a detailed analysis of Management Accounting Systems (MAS) and their practical applications, using KEF Limited as a case study. It explores various types of MAS, including cost accounting, price optimization, stock management, and job order costing, along with the benefits of each system. The report examines different types of management accounting reports such as budget reports, accounts receivable aging reports, performance reports, and inventory reports. It delves into the calculation of production costs using absorption and marginal costing techniques, including the preparation of income statements. The report further discusses budgetary control, its planning tools (operating, capital, and fixed budgets), and their advantages and disadvantages. Finally, the report highlights the importance of these systems in addressing monetary issues within a business context.

Management

Accounting Systems

and its applications

Accounting Systems

and its applications

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..............................................................................................................3

MAIN BODY.......................................................................................................................3

Task 1.............................................................................................................................3

Task 2.............................................................................................................................6

Task 3...........................................................................................................................12

Task 4...........................................................................................................................13

CONCLUSION.................................................................................................................15

REFERENCES................................................................................................................16

INTRODUCTION ..............................................................................................................3

MAIN BODY.......................................................................................................................3

Task 1.............................................................................................................................3

Task 2.............................................................................................................................6

Task 3...........................................................................................................................12

Task 4...........................................................................................................................13

CONCLUSION.................................................................................................................15

REFERENCES................................................................................................................16

INTRODUCTION

The field of accounting is too wide it is not limited till the recording of transaction

of financial aspects. Management accounting is one of the key form of accounting which

is linked to process of helping internal department of business entities by preparing

internal reports (Novas, Alves and Sousa, 2017). Under this accounting all types of data

are gathered and recorded in a systematic form. Main objective of this project report is

to explaining role of this accounting as well as its functions for business entities. In the

report KEF limited company has been chosen which is a medium sized manufacturing

business entity. The report covers detailed information about different types of MA and

reports. As well as various form of planning tools are also mentioned along with

importance of this accounting in sorting monetary issues.

MAIN BODY

Task 1.

Mean of MA and its types.

MA- As above discussed, it is a form of accounting which is aligned with process of

gathering monetary and anti monetary data from different transactions. After that using

this gathered data for preparing internal managerial reports. It consists vital range of

accounting systems which are mentioned below in such manner:

Cost accounting system- It can be defined as a type of accounting system which

starts with process of making projection of future expenditures and costs. The

objective of this prediction of cost is to help finance department of companies in

order to do proper use of available resources and to minimise overall

expenditures (Chiarin and Vagnoni, 2015). It is essential for companies because

by help of this accounting system, managers can assess total number of

expenditures during a particular time period. As well as can evaluate variation

between actual and standard costs. In the KEF limited company, they apply this

accounting system which is helping them in order to control expenses which

occurs in operating different activities and operations.

The field of accounting is too wide it is not limited till the recording of transaction

of financial aspects. Management accounting is one of the key form of accounting which

is linked to process of helping internal department of business entities by preparing

internal reports (Novas, Alves and Sousa, 2017). Under this accounting all types of data

are gathered and recorded in a systematic form. Main objective of this project report is

to explaining role of this accounting as well as its functions for business entities. In the

report KEF limited company has been chosen which is a medium sized manufacturing

business entity. The report covers detailed information about different types of MA and

reports. As well as various form of planning tools are also mentioned along with

importance of this accounting in sorting monetary issues.

MAIN BODY

Task 1.

Mean of MA and its types.

MA- As above discussed, it is a form of accounting which is aligned with process of

gathering monetary and anti monetary data from different transactions. After that using

this gathered data for preparing internal managerial reports. It consists vital range of

accounting systems which are mentioned below in such manner:

Cost accounting system- It can be defined as a type of accounting system which

starts with process of making projection of future expenditures and costs. The

objective of this prediction of cost is to help finance department of companies in

order to do proper use of available resources and to minimise overall

expenditures (Chiarin and Vagnoni, 2015). It is essential for companies because

by help of this accounting system, managers can assess total number of

expenditures during a particular time period. As well as can evaluate variation

between actual and standard costs. In the KEF limited company, they apply this

accounting system which is helping them in order to control expenses which

occurs in operating different activities and operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price optimisation system- In this accounting system, a systematic process of

analysing market demand and situation is followed. Main objective of applying

this process is to evaluate customers' demand for a particular product. It is

essential for companies in order to set prices of products and services as per

market condition. In the aspect of KEF limited company, their sales department

applies this accounting system to set prices of manufactured items.

Stock management system- It is a type of accounting system which is linked to

assess quantity of various form of material by help of techniques like last in first

out method, first in first out etc. This is essential for companies in order to track

various kinds of goods stored in warehouses such as raw material, finished

goods etc. In the KEF limited company, they apply this accounting system for

evaluating actual quantity of material on a daily basis so that accurate decisions

can be taken by managers.

Job order costing system- This can be defined as an accounting system that

computes the cost of each individual output by help of assessing cost of job

(Maas,Schaltegger and Crutzen, 2016). It is being implemented in those

enterprises in which portfolio of products is higher. This accounting system is

essential for companies in order to minimise cost of job and activities under

control. In the KEF limited company, they apply this accounting system for

evaluating cost of activities separately and for minimising cost of job.

Various kinds of MA reports.

MA reports- These are types of report which are prepared by companies with an aim of

making effective planning, better decision-making and for measuring actual

performance. Accountant of KEF limited company produce below mentioned reports

such as:

Budget report- It is a type of report which is prepared by help of different types of

budgets. Under this information regards to estimated income and expenses is

included along with the value of variation. It contributes to managers in order to

track monetary performance. In the KEF limited company, their accountants

prepare this report for helping managers by providing data of actual performance.

analysing market demand and situation is followed. Main objective of applying

this process is to evaluate customers' demand for a particular product. It is

essential for companies in order to set prices of products and services as per

market condition. In the aspect of KEF limited company, their sales department

applies this accounting system to set prices of manufactured items.

Stock management system- It is a type of accounting system which is linked to

assess quantity of various form of material by help of techniques like last in first

out method, first in first out etc. This is essential for companies in order to track

various kinds of goods stored in warehouses such as raw material, finished

goods etc. In the KEF limited company, they apply this accounting system for

evaluating actual quantity of material on a daily basis so that accurate decisions

can be taken by managers.

Job order costing system- This can be defined as an accounting system that

computes the cost of each individual output by help of assessing cost of job

(Maas,Schaltegger and Crutzen, 2016). It is being implemented in those

enterprises in which portfolio of products is higher. This accounting system is

essential for companies in order to minimise cost of job and activities under

control. In the KEF limited company, they apply this accounting system for

evaluating cost of activities separately and for minimising cost of job.

Various kinds of MA reports.

MA reports- These are types of report which are prepared by companies with an aim of

making effective planning, better decision-making and for measuring actual

performance. Accountant of KEF limited company produce below mentioned reports

such as:

Budget report- It is a type of report which is prepared by help of different types of

budgets. Under this information regards to estimated income and expenses is

included along with the value of variation. It contributes to managers in order to

track monetary performance. In the KEF limited company, their accountants

prepare this report for helping managers by providing data of actual performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounts receivable ageing report- This is form of report which is linked to

gathering key information about those parties whose amount is due. By help of it,

finance manager of business entities can evaluate information regards to those

customers whose payment is due. In the KEF limited company, their accountants

prepare this report which help to finance department in order to manage debts.

Performance report- This is a kinds of report which is prepared by accountants to

provide an appropriate framework to managers in order to take decision about

progress and appraisal of employees (Dekker, 2016). Under it, information

related to actual and estimated outcome is included in a detailed manner. In the

above company, their accountant prepares this report for measurement of actual

level of performance.

Inventory report- It can be defined as a type of report which is produced by

accountants containing information regards to quantity of various form of

material. Under this, information is added in accordance of making proper

analysis by using techniques like LIFO, FIFO and many more. In KEF limited

company, they use this reports' information in order to controlling manufacturing

activities.

Benefits of MAS:

Types of MAS Benefits

Cost accounting

system

This is aligned to process of estimating and tracking overall

costs and expenditures. In KEF limited company, this

accounting system is helping to their finance department in the

context of managing expenditures.

Price optimisation

system

It is related with process of setting prices of products and

services at an effective level. The sales department of KEF

limited company set prices of manufactured items as per the

information provided under this accounting system.

Stock management

system

Under this accounting system valuation of stock quantity is done

by help of different approaches. The production department of

KEF limited company, takes appropriate steps about new

gathering key information about those parties whose amount is due. By help of it,

finance manager of business entities can evaluate information regards to those

customers whose payment is due. In the KEF limited company, their accountants

prepare this report which help to finance department in order to manage debts.

Performance report- This is a kinds of report which is prepared by accountants to

provide an appropriate framework to managers in order to take decision about

progress and appraisal of employees (Dekker, 2016). Under it, information

related to actual and estimated outcome is included in a detailed manner. In the

above company, their accountant prepares this report for measurement of actual

level of performance.

Inventory report- It can be defined as a type of report which is produced by

accountants containing information regards to quantity of various form of

material. Under this, information is added in accordance of making proper

analysis by using techniques like LIFO, FIFO and many more. In KEF limited

company, they use this reports' information in order to controlling manufacturing

activities.

Benefits of MAS:

Types of MAS Benefits

Cost accounting

system

This is aligned to process of estimating and tracking overall

costs and expenditures. In KEF limited company, this

accounting system is helping to their finance department in the

context of managing expenditures.

Price optimisation

system

It is related with process of setting prices of products and

services at an effective level. The sales department of KEF

limited company set prices of manufactured items as per the

information provided under this accounting system.

Stock management

system

Under this accounting system valuation of stock quantity is done

by help of different approaches. The production department of

KEF limited company, takes appropriate steps about new

production and purchasing of raw material by help of this

accounting system.

Job order costing

system

This accounting system helps in process of computing cost of

job and produced units. Same as in the above company, it is

helpful for managing overall cost of job.

Integration of MAS and MA reports with business process.

In the aspect of MAS various range of accounting systems are included such as

stock management system, price optimisation system etc. In the KEF limited company,

their production department is integrated to inventory management system as well as

sales department with price optimisation system (Bhimani, 2015). In addition, MA

reports are also aligned to business process. Like in above company, their accounts

department prepares strategies and policies by help of accounts receivable ageing

report.

Task 2.

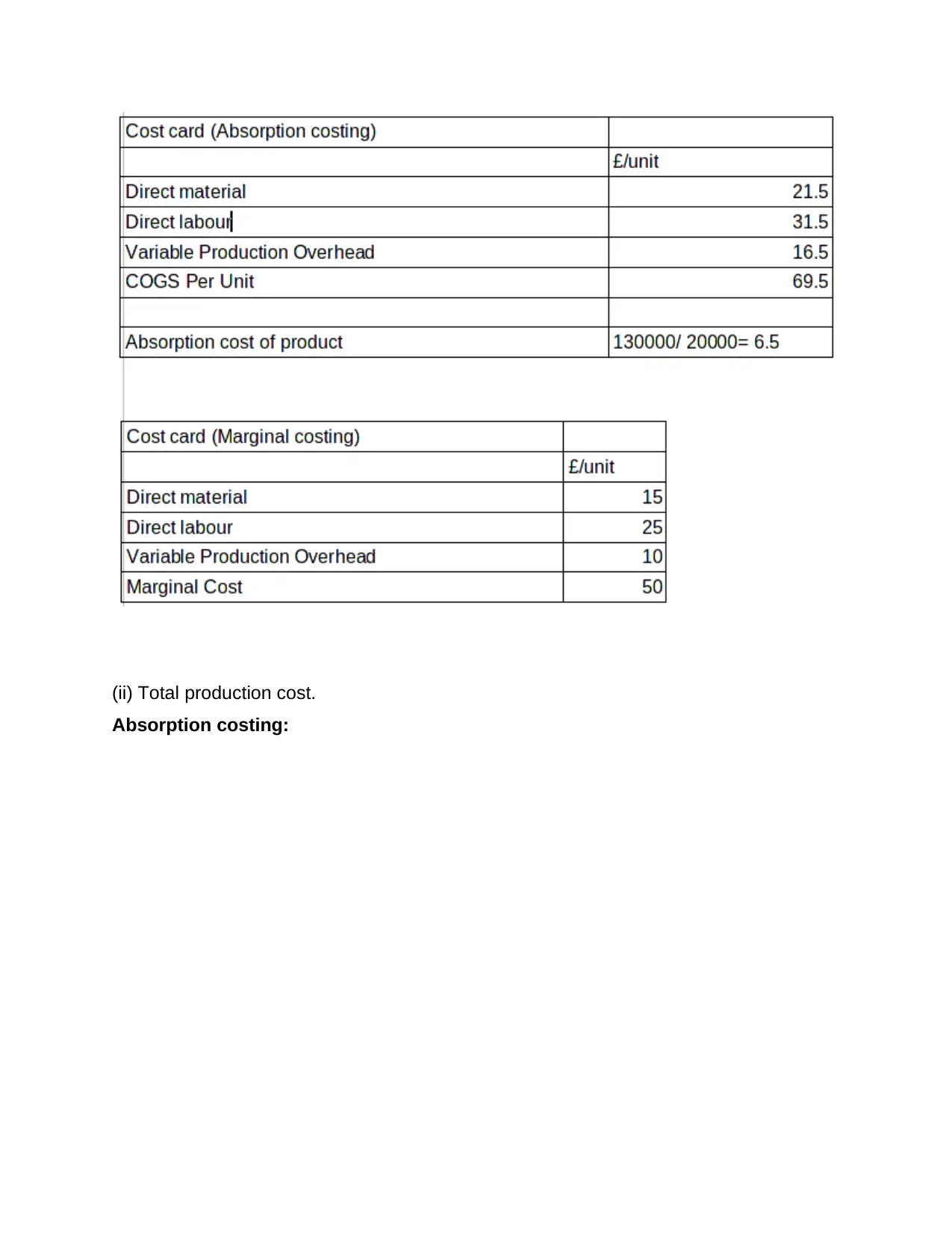

I) Calculation of cost of production per unit.

accounting system.

Job order costing

system

This accounting system helps in process of computing cost of

job and produced units. Same as in the above company, it is

helpful for managing overall cost of job.

Integration of MAS and MA reports with business process.

In the aspect of MAS various range of accounting systems are included such as

stock management system, price optimisation system etc. In the KEF limited company,

their production department is integrated to inventory management system as well as

sales department with price optimisation system (Bhimani, 2015). In addition, MA

reports are also aligned to business process. Like in above company, their accounts

department prepares strategies and policies by help of accounts receivable ageing

report.

Task 2.

I) Calculation of cost of production per unit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

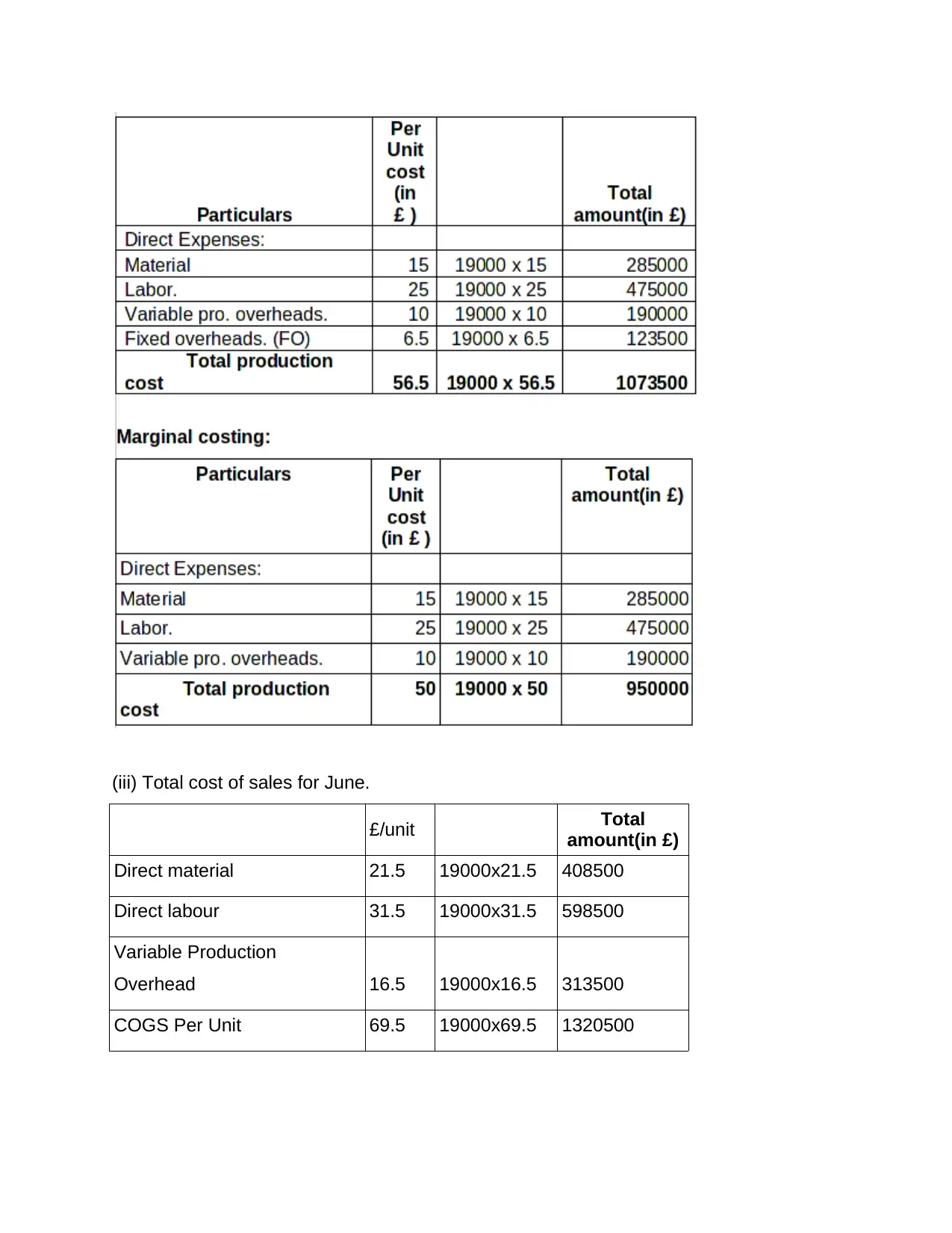

(ii) Total production cost.

Absorption costing:

Absorption costing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(iii) Total cost of sales for June.

£/unit Total

amount(in £)

Direct material 21.5 19000x21.5 408500

Direct labour 31.5 19000x31.5 598500

Variable Production

Overhead 16.5 19000x16.5 313500

COGS Per Unit 69.5 19000x69.5 1320500

£/unit Total

amount(in £)

Direct material 21.5 19000x21.5 408500

Direct labour 31.5 19000x31.5 598500

Variable Production

Overhead 16.5 19000x16.5 313500

COGS Per Unit 69.5 19000x69.5 1320500

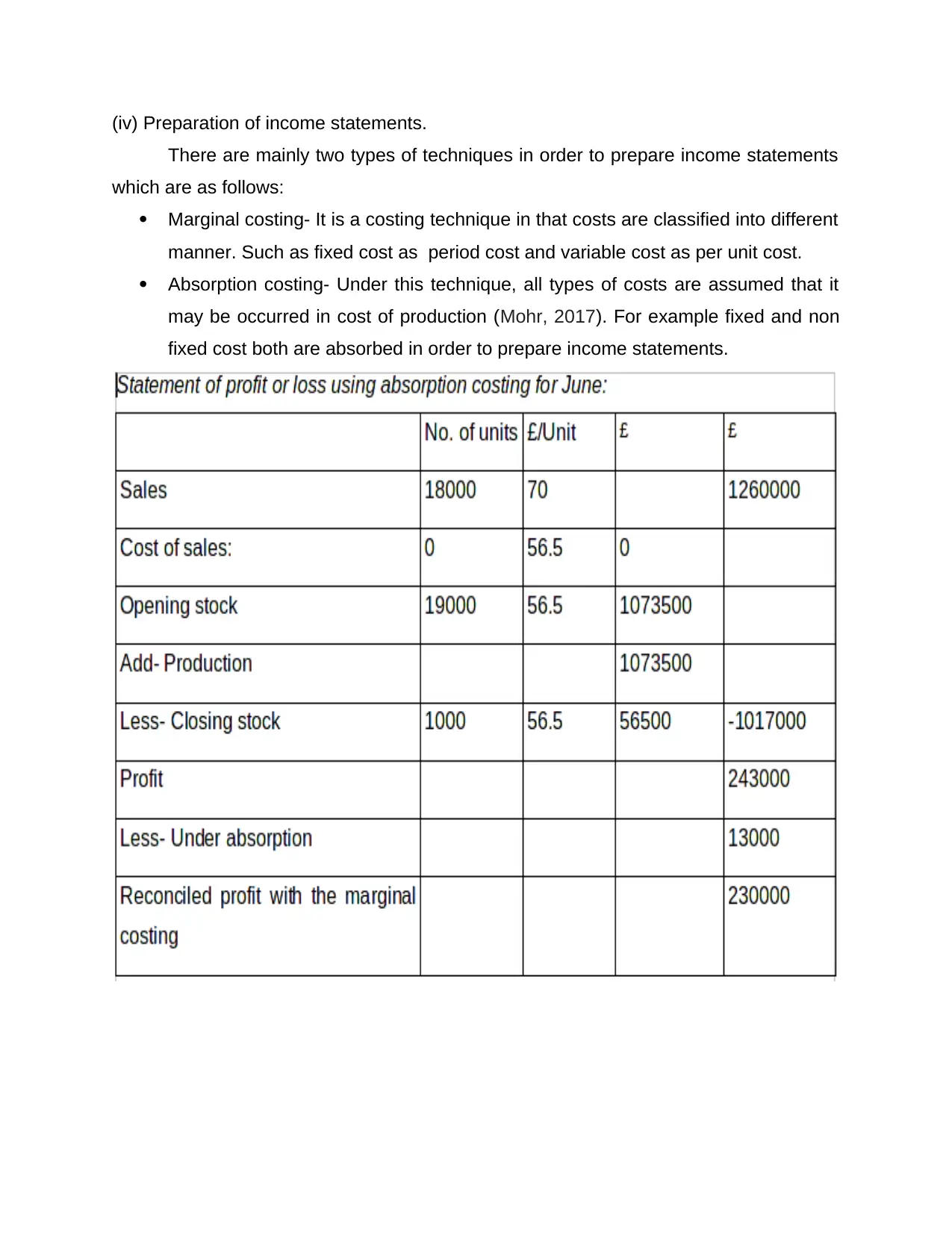

(iv) Preparation of income statements.

There are mainly two types of techniques in order to prepare income statements

which are as follows:

Marginal costing- It is a costing technique in that costs are classified into different

manner. Such as fixed cost as period cost and variable cost as per unit cost.

Absorption costing- Under this technique, all types of costs are assumed that it

may be occurred in cost of production (Mohr, 2017). For example fixed and non

fixed cost both are absorbed in order to prepare income statements.

There are mainly two types of techniques in order to prepare income statements

which are as follows:

Marginal costing- It is a costing technique in that costs are classified into different

manner. Such as fixed cost as period cost and variable cost as per unit cost.

Absorption costing- Under this technique, all types of costs are assumed that it

may be occurred in cost of production (Mohr, 2017). For example fixed and non

fixed cost both are absorbed in order to prepare income statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

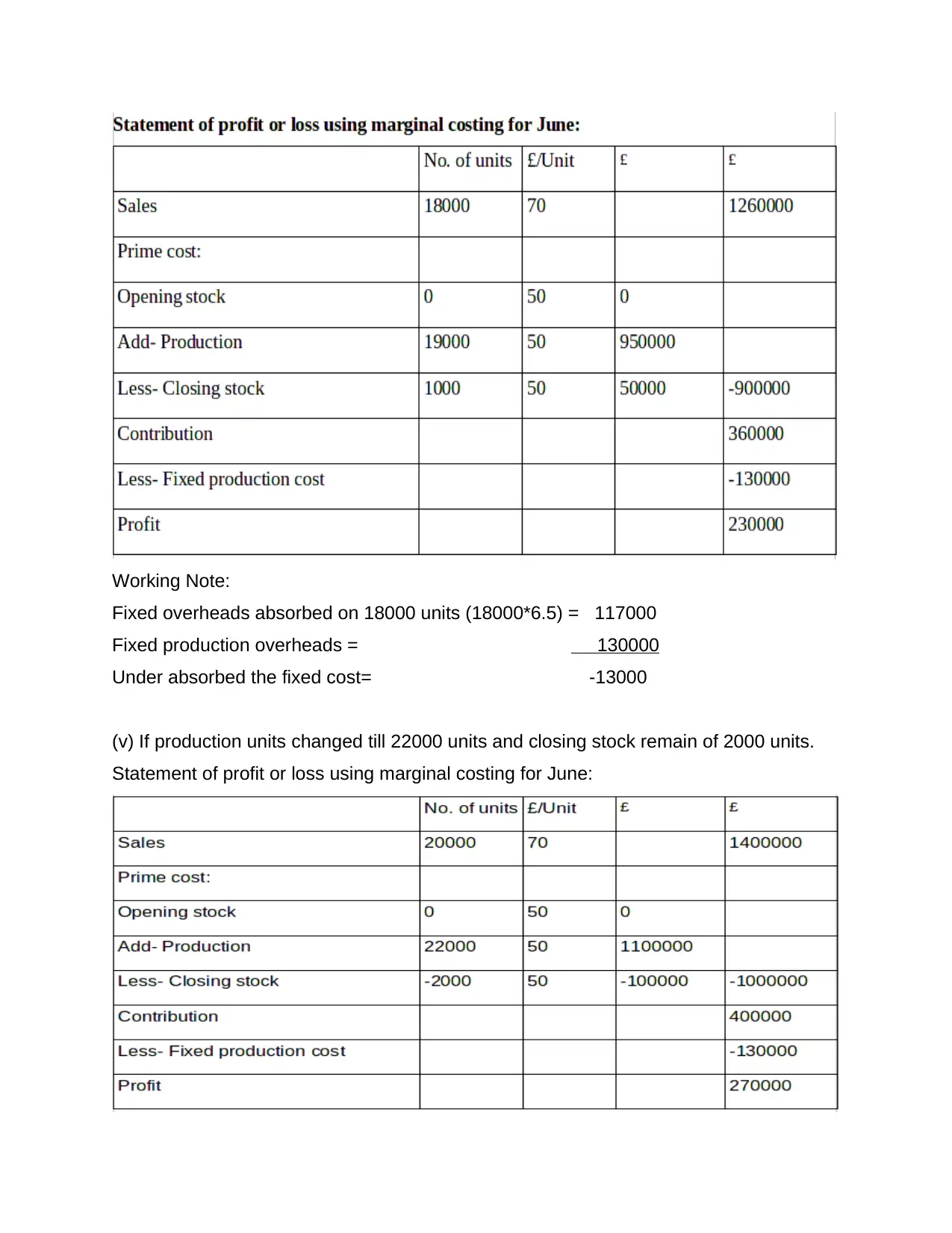

Working Note:

Fixed overheads absorbed on 18000 units (18000*6.5) = 117000

Fixed production overheads = 130000

Under absorbed the fixed cost= -13000

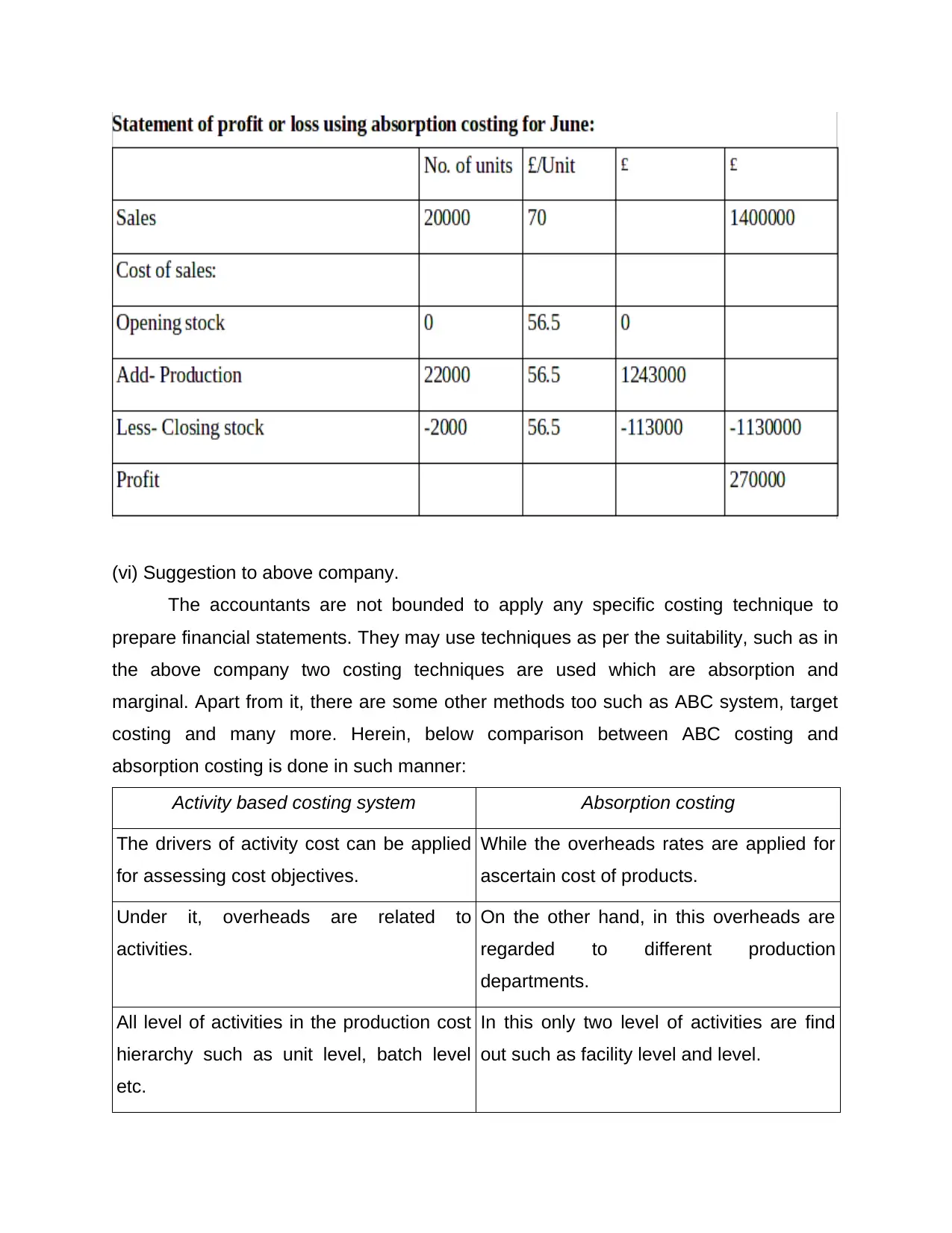

(v) If production units changed till 22000 units and closing stock remain of 2000 units.

Statement of profit or loss using marginal costing for June:

Fixed overheads absorbed on 18000 units (18000*6.5) = 117000

Fixed production overheads = 130000

Under absorbed the fixed cost= -13000

(v) If production units changed till 22000 units and closing stock remain of 2000 units.

Statement of profit or loss using marginal costing for June:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(vi) Suggestion to above company.

The accountants are not bounded to apply any specific costing technique to

prepare financial statements. They may use techniques as per the suitability, such as in

the above company two costing techniques are used which are absorption and

marginal. Apart from it, there are some other methods too such as ABC system, target

costing and many more. Herein, below comparison between ABC costing and

absorption costing is done in such manner:

Activity based costing system Absorption costing

The drivers of activity cost can be applied

for assessing cost objectives.

While the overheads rates are applied for

ascertain cost of products.

Under it, overheads are related to

activities.

On the other hand, in this overheads are

regarded to different production

departments.

All level of activities in the production cost

hierarchy such as unit level, batch level

etc.

In this only two level of activities are find

out such as facility level and level.

The accountants are not bounded to apply any specific costing technique to

prepare financial statements. They may use techniques as per the suitability, such as in

the above company two costing techniques are used which are absorption and

marginal. Apart from it, there are some other methods too such as ABC system, target

costing and many more. Herein, below comparison between ABC costing and

absorption costing is done in such manner:

Activity based costing system Absorption costing

The drivers of activity cost can be applied

for assessing cost objectives.

While the overheads rates are applied for

ascertain cost of products.

Under it, overheads are related to

activities.

On the other hand, in this overheads are

regarded to different production

departments.

All level of activities in the production cost

hierarchy such as unit level, batch level

etc.

In this only two level of activities are find

out such as facility level and level.

On the basis of above discussion, this can be stated that activity based costing is much

more better in compare to absorption costing technique.

Task 3.

Benefits and drawbacks of planning tools of budgetary control.

Budgetary control- It can be defined as a process of determining different actual

outcomes by help of budgeted figures for business entities for upcoming time period

(Hosseinzadeh and Davar, 2018). Basically, this technique is being used by companies

in order to controlling overall monetary performance of various kinds of aspects. It

consists range of planning tools and some of them are as follows:

Operating budget – This is a type of budget which is prepared on an annual basis

and consists information regards to estimated operational expenditures & income

during a particular time frame. The main objective of this budget is to minimise

operational expenditures and to gain higher operating income. In the KEF limited

company, they prepare this budget for operating their operations and functions in

an effective manner.

Benefits- Main benefit of this budget is that it provides direction to business in order to

gain higher monetary success.

Drawback- It has some common drawbacks such as it consumes too much time and

cost.

Capital budget- It can be defined as a type of technique which is related to

process of determining efficiency of any capital expenditure. Some common

example of capital expenditure are construction of building, purchasing of new

machinery etc. In KEF limited company, they make futuristic investment in

accordance of guidance of this budget.

Benefits- This is beneficial for companies in order to take wise decisions regards to long

term strategic investments.

Drawback- This budget's prediction for long term investments can be wrong in future

time period because of change in economical conditions.

more better in compare to absorption costing technique.

Task 3.

Benefits and drawbacks of planning tools of budgetary control.

Budgetary control- It can be defined as a process of determining different actual

outcomes by help of budgeted figures for business entities for upcoming time period

(Hosseinzadeh and Davar, 2018). Basically, this technique is being used by companies

in order to controlling overall monetary performance of various kinds of aspects. It

consists range of planning tools and some of them are as follows:

Operating budget – This is a type of budget which is prepared on an annual basis

and consists information regards to estimated operational expenditures & income

during a particular time frame. The main objective of this budget is to minimise

operational expenditures and to gain higher operating income. In the KEF limited

company, they prepare this budget for operating their operations and functions in

an effective manner.

Benefits- Main benefit of this budget is that it provides direction to business in order to

gain higher monetary success.

Drawback- It has some common drawbacks such as it consumes too much time and

cost.

Capital budget- It can be defined as a type of technique which is related to

process of determining efficiency of any capital expenditure. Some common

example of capital expenditure are construction of building, purchasing of new

machinery etc. In KEF limited company, they make futuristic investment in

accordance of guidance of this budget.

Benefits- This is beneficial for companies in order to take wise decisions regards to long

term strategic investments.

Drawback- This budget's prediction for long term investments can be wrong in future

time period because of change in economical conditions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.