Management Accounting: Systems, Techniques, and Financial Analysis

VerifiedAdded on 2021/02/19

|18

|5381

|40

Report

AI Summary

This report offers a detailed analysis of management accounting systems and techniques, focusing on their application within a business context. It begins with an introduction to management accounting, emphasizing its role in decision-making and achieving business goals. The report then delves into various management accounting systems, including inventory management, cost accounting, and price optimization. It explores different methods of management accounting reporting, such as inventory reports, performance reports, and cost accounting reports. The core of the report involves the preparation of income statements using both absorption and marginal costing methods, providing a comparative analysis of their impacts. Furthermore, it examines the advantages and disadvantages of planning tools used in budgetary control and analyzes how management accounting systems can be adapted to address financial problems, culminating in a critical evaluation of strategies to reduce financial issues and achieve sustainable success. The report uses KEF manufacturing company as a case study throughout.

Management

Accounting, systems and

techniques

Accounting, systems and

techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Management accounting system and essential requirement of different kind of accounting

systems........................................................................................................................................3

P2: Different kind of methods of management accounting reporting.........................................4

M1 Benefit of management accounting system. ........................................................................6

D1. Management accounting system and accounting reports are integrated within

organisational processes..............................................................................................................7

TASK 2............................................................................................................................................7

P3: Preparation of income statements with the use of absorption and marginal costing method

.....................................................................................................................................................7

M2: Various types of management accounting techniques.......................................................11

D2: Critical analyse of data collected from income statements................................................11

TASK 3..........................................................................................................................................11

P4: Advantages and disadvantages of planning tools used in budgetary control.....................11

M3. Analyse the use of different planning tools and their application for preparation and

forecasting budgets:..................................................................................................................13

TASK 4.....................................................................................................................................14

P5: Adaption management accounting system to respond to financial problems.....................14

M4. Responding to financial problems, management accounting can lead organisations to

sustainable success....................................................................................................................15

D3: Critical evaluation to reduce financial issues.....................................................................16

CONCLUSION..............................................................................................................................16

REFRENCES.................................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Management accounting system and essential requirement of different kind of accounting

systems........................................................................................................................................3

P2: Different kind of methods of management accounting reporting.........................................4

M1 Benefit of management accounting system. ........................................................................6

D1. Management accounting system and accounting reports are integrated within

organisational processes..............................................................................................................7

TASK 2............................................................................................................................................7

P3: Preparation of income statements with the use of absorption and marginal costing method

.....................................................................................................................................................7

M2: Various types of management accounting techniques.......................................................11

D2: Critical analyse of data collected from income statements................................................11

TASK 3..........................................................................................................................................11

P4: Advantages and disadvantages of planning tools used in budgetary control.....................11

M3. Analyse the use of different planning tools and their application for preparation and

forecasting budgets:..................................................................................................................13

TASK 4.....................................................................................................................................14

P5: Adaption management accounting system to respond to financial problems.....................14

M4. Responding to financial problems, management accounting can lead organisations to

sustainable success....................................................................................................................15

D3: Critical evaluation to reduce financial issues.....................................................................16

CONCLUSION..............................................................................................................................16

REFRENCES.................................................................................................................................17

INTRODUCTION

Management Accounting is an essential part of management that help to prepare the

business cost as well as operations to make effective decision in order to attain the business goal

significantly. It include accounting information that help the firm to formulate policies in order

to assist day to day business activities and maximise the profit effectively (Rossing, 2013).

Along with that it carry both monetary as well as non monetary information that help in better

performance of business by formulating effective policies. For the better understanding of report

KEF manufacturing company has been selected which is small business and operate within UK.

This report cover following topics such as understanding on management accounting systems.

Determine proper technique to prepare income statement by using marginal and absorption cost.

Moreover, explain the uses of planning tools in management accounting. Further, compare

organisations on the basis of management accounting to respond financial problem.

TASK 1

P1: Management accounting system and essential requirement of different kind of accounting

systems

Management accounting system refer to the financial as well as non financial

information that help the manager to make effective business decision in order to perform day to

day business activity. The main advantage associated with management accounting is that the

management can prepare the effective plan and execute it effective for the better operations of

business. There are various management accounting system some of them are defined below:

Inventory management system: Inventory management system helps in proper

management of stock whether it is in form of raw material, semi finished or finished good

(Clinton and White, 2012). Here decision are made on the basis of purchase of new inventory or

the requirement of warehouse to store the inventory in order to minimise the chances of defects

that leads to wastage. Herein, KEF manufacturing company uses inventory management system

to track the stock and make effective decision.

Cost accounting system: This system helps the company to determine the overall

expenditure incurred to carry out various activity of business. It is an effective system as it helps

to minimise the chances of unnecessary expenditure that saves the cost and enhance the

profitability of firm. In relation to KEF manufacturing company uses cost accounting system to

Management Accounting is an essential part of management that help to prepare the

business cost as well as operations to make effective decision in order to attain the business goal

significantly. It include accounting information that help the firm to formulate policies in order

to assist day to day business activities and maximise the profit effectively (Rossing, 2013).

Along with that it carry both monetary as well as non monetary information that help in better

performance of business by formulating effective policies. For the better understanding of report

KEF manufacturing company has been selected which is small business and operate within UK.

This report cover following topics such as understanding on management accounting systems.

Determine proper technique to prepare income statement by using marginal and absorption cost.

Moreover, explain the uses of planning tools in management accounting. Further, compare

organisations on the basis of management accounting to respond financial problem.

TASK 1

P1: Management accounting system and essential requirement of different kind of accounting

systems

Management accounting system refer to the financial as well as non financial

information that help the manager to make effective business decision in order to perform day to

day business activity. The main advantage associated with management accounting is that the

management can prepare the effective plan and execute it effective for the better operations of

business. There are various management accounting system some of them are defined below:

Inventory management system: Inventory management system helps in proper

management of stock whether it is in form of raw material, semi finished or finished good

(Clinton and White, 2012). Here decision are made on the basis of purchase of new inventory or

the requirement of warehouse to store the inventory in order to minimise the chances of defects

that leads to wastage. Herein, KEF manufacturing company uses inventory management system

to track the stock and make effective decision.

Cost accounting system: This system helps the company to determine the overall

expenditure incurred to carry out various activity of business. It is an effective system as it helps

to minimise the chances of unnecessary expenditure that saves the cost and enhance the

profitability of firm. In relation to KEF manufacturing company uses cost accounting system to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manage the operations of business and make optimum utilisation of resources to control the

overall cost incurred by firm. Thus, it is critical for company to identify the exact cost incurred in

the manufacturing of product due to which the whole system is prepared on the basis of

anticipated amount.

Price optimisation system: It is an effective management accounting system that help

the firm to determine the best suited price of product. This determination is made on the basis of

customer reaction toward the various pricing level. In terms of KEF manufacturing company can

uses this system to identify effective pricing strategy and allocate suitable prices for the different

range of product and services. Thus, company finally lands up setting that price that can help the

firm to meet their objectives like expansion which leads to maximising the operations of

business.

Job costing system: Job costing system is a vital accounting system that help the firm to

determine different activities performed in a business as well as cost associated to carry on

various business activity. It gives brief information regarding the cost of job so that firm can

determine effective decision. In context to KEF manufacturing company, the manager can make

the use of this system to evaluate various cost and perform all the internal activities effectively.

Hence, these system are basically used by KEF manufacturing company to achieve the

desired result by managing the overall system effectively.

P2: Different kind of methods of management accounting reporting

Management accounting report emphasize on the internal information of business which

is received through financial accounting. It is basically used to conduct better planning, make

effective decision and regulate the internal performance. These report are generated via book

keeping and accounting method due to which these report need to be crafted effectively.

Moreover, different company chooses different method to manage the report in order to record

the financial and non financial information suitably (Songini, Gnan, and Malmi, 2013). Herein,

KEF manufacturing company can use various type of accounting report which is determined

below:

Inventory report: Inventory report are prepared to keep all the information associated

with stock. It also include the movement of inventory from one level to another so that company

can track the available stock and manage the flow of inventory. Herein, KEF manufacturing

company can manage physical inventory by using managerial accounting report that help to

overall cost incurred by firm. Thus, it is critical for company to identify the exact cost incurred in

the manufacturing of product due to which the whole system is prepared on the basis of

anticipated amount.

Price optimisation system: It is an effective management accounting system that help

the firm to determine the best suited price of product. This determination is made on the basis of

customer reaction toward the various pricing level. In terms of KEF manufacturing company can

uses this system to identify effective pricing strategy and allocate suitable prices for the different

range of product and services. Thus, company finally lands up setting that price that can help the

firm to meet their objectives like expansion which leads to maximising the operations of

business.

Job costing system: Job costing system is a vital accounting system that help the firm to

determine different activities performed in a business as well as cost associated to carry on

various business activity. It gives brief information regarding the cost of job so that firm can

determine effective decision. In context to KEF manufacturing company, the manager can make

the use of this system to evaluate various cost and perform all the internal activities effectively.

Hence, these system are basically used by KEF manufacturing company to achieve the

desired result by managing the overall system effectively.

P2: Different kind of methods of management accounting reporting

Management accounting report emphasize on the internal information of business which

is received through financial accounting. It is basically used to conduct better planning, make

effective decision and regulate the internal performance. These report are generated via book

keeping and accounting method due to which these report need to be crafted effectively.

Moreover, different company chooses different method to manage the report in order to record

the financial and non financial information suitably (Songini, Gnan, and Malmi, 2013). Herein,

KEF manufacturing company can use various type of accounting report which is determined

below:

Inventory report: Inventory report are prepared to keep all the information associated

with stock. It also include the movement of inventory from one level to another so that company

can track the available stock and manage the flow of inventory. Herein, KEF manufacturing

company can manage physical inventory by using managerial accounting report that help to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manage the manufacturing process efficiently. Hence, it is a suitable method that include

managing the inventory waste and labour cost.

Performance report: These report are prepare to measure the performance of an

employee by setting the desired goal. So it helps to evaluate the key strength of an employee to

attain the benchmark as well as areas where they are lacking to perform effectively. In relation to

KEF manufacturing company usually prepare these report to attain the future decision by

evaluating the performance of an employee successfully. Moreover, it include benchmarking

system based on which employee progress is measured or tracked to enhance the profitability as

well as productivity of firm. Further, it is a detail statement that include annual performance

report which help the employee to determine their success in the completion of project by

adhering the budgetary control.

Job cost accounting report: Job costing report depict the expenses incurred by firm

while carrying on specific project. The firm estimate the revenue in order to evaluate the

profitability gained from the job. Further, these report are widely used in the business to

determine the high earning area and make progressive effort to manage the fund as well as time

of company. In context to KEF manufacturing company can analyses their expenses and manage

the area where business may incur huge expenditure.

Cost accounting report: Such report helps the business to examine the activities

associated with cash outflow. It provides the detail information regarding various activity and

minimise the expenses of business effectively to gain better result (Chan, Tong and Zhang,

2012). These report are effective for manufacturing firm as they get the detail information

regarding the operation done in various business activity to get planned result. Hence, cost

accounting report determine various cost associated with project, processes as well as product to

display the fair amount in financing statement. It further leads to indulgence in planning as well

as controlling activity that help in the preparation of desirable result.

Account receivable ageing report: These report are crafted to provide the detail

information regarding the debtors as well as total amount payable by the company. Along with

that this help the firm to manage the cash-flow and attain the purpose of company significantly.

Thus, it is a critical tool used by KEF company to extend the credit amount for the supplier as

well as customer without shopping the operations of firms. Although it is risky to pay credit but

at times company need to make credit transaction as well to maintain the smooth business

managing the inventory waste and labour cost.

Performance report: These report are prepare to measure the performance of an

employee by setting the desired goal. So it helps to evaluate the key strength of an employee to

attain the benchmark as well as areas where they are lacking to perform effectively. In relation to

KEF manufacturing company usually prepare these report to attain the future decision by

evaluating the performance of an employee successfully. Moreover, it include benchmarking

system based on which employee progress is measured or tracked to enhance the profitability as

well as productivity of firm. Further, it is a detail statement that include annual performance

report which help the employee to determine their success in the completion of project by

adhering the budgetary control.

Job cost accounting report: Job costing report depict the expenses incurred by firm

while carrying on specific project. The firm estimate the revenue in order to evaluate the

profitability gained from the job. Further, these report are widely used in the business to

determine the high earning area and make progressive effort to manage the fund as well as time

of company. In context to KEF manufacturing company can analyses their expenses and manage

the area where business may incur huge expenditure.

Cost accounting report: Such report helps the business to examine the activities

associated with cash outflow. It provides the detail information regarding various activity and

minimise the expenses of business effectively to gain better result (Chan, Tong and Zhang,

2012). These report are effective for manufacturing firm as they get the detail information

regarding the operation done in various business activity to get planned result. Hence, cost

accounting report determine various cost associated with project, processes as well as product to

display the fair amount in financing statement. It further leads to indulgence in planning as well

as controlling activity that help in the preparation of desirable result.

Account receivable ageing report: These report are crafted to provide the detail

information regarding the debtors as well as total amount payable by the company. Along with

that this help the firm to manage the cash-flow and attain the purpose of company significantly.

Thus, it is a critical tool used by KEF company to extend the credit amount for the supplier as

well as customer without shopping the operations of firms. Although it is risky to pay credit but

at times company need to make credit transaction as well to maintain the smooth business

process. Hence, account receivable ageing periodically analyse the collection amount and

maintain the record of cash and non cash transaction.

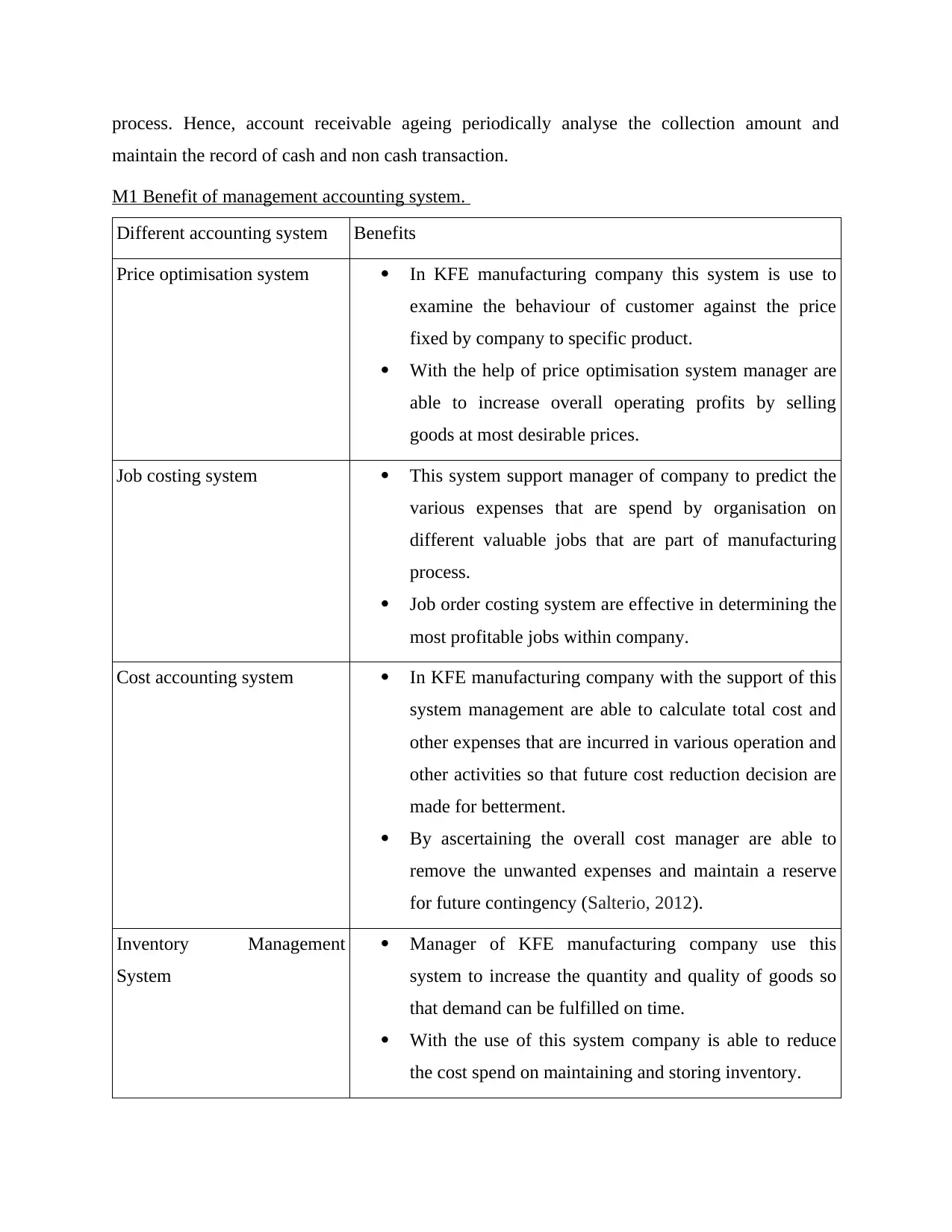

M1 Benefit of management accounting system.

Different accounting system Benefits

Price optimisation system In KFE manufacturing company this system is use to

examine the behaviour of customer against the price

fixed by company to specific product.

With the help of price optimisation system manager are

able to increase overall operating profits by selling

goods at most desirable prices.

Job costing system This system support manager of company to predict the

various expenses that are spend by organisation on

different valuable jobs that are part of manufacturing

process.

Job order costing system are effective in determining the

most profitable jobs within company.

Cost accounting system In KFE manufacturing company with the support of this

system management are able to calculate total cost and

other expenses that are incurred in various operation and

other activities so that future cost reduction decision are

made for betterment.

By ascertaining the overall cost manager are able to

remove the unwanted expenses and maintain a reserve

for future contingency (Salterio, 2012).

Inventory Management

System

Manager of KFE manufacturing company use this

system to increase the quantity and quality of goods so

that demand can be fulfilled on time.

With the use of this system company is able to reduce

the cost spend on maintaining and storing inventory.

maintain the record of cash and non cash transaction.

M1 Benefit of management accounting system.

Different accounting system Benefits

Price optimisation system In KFE manufacturing company this system is use to

examine the behaviour of customer against the price

fixed by company to specific product.

With the help of price optimisation system manager are

able to increase overall operating profits by selling

goods at most desirable prices.

Job costing system This system support manager of company to predict the

various expenses that are spend by organisation on

different valuable jobs that are part of manufacturing

process.

Job order costing system are effective in determining the

most profitable jobs within company.

Cost accounting system In KFE manufacturing company with the support of this

system management are able to calculate total cost and

other expenses that are incurred in various operation and

other activities so that future cost reduction decision are

made for betterment.

By ascertaining the overall cost manager are able to

remove the unwanted expenses and maintain a reserve

for future contingency (Salterio, 2012).

Inventory Management

System

Manager of KFE manufacturing company use this

system to increase the quantity and quality of goods so

that demand can be fulfilled on time.

With the use of this system company is able to reduce

the cost spend on maintaining and storing inventory.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D1. Management accounting system and accounting reports are integrated within organisational

processes

In business scenario, management accounting reports and systems are equally

interrelated with each other in different ways. As it is also stated that accounting systems are so

much essential as it help to formulate vital accounting reports so that business decisions are

made to overcome uncertain condition within workplace (Novas, Alves and Sousa, 2017).

Managers of KFE manufacturing company set account receivable reports with the support of

price optimisation system which so that product at suitable price can be sold to large number of

customer on credit basis.

TASK 2

P3: Preparation of income statements with the use of absorption and marginal costing method

Marginal costing method: Marginal costing is an essential method that helps in

preparation of income system as it include variable cost which are categorised as product cost.

Whereas, within this method fixed cost is categorised as cost incurred within specific period.

Here profit is calculated with the use of profit volume ratio and is presented to outline the total

contribution made by company.

Absorption costing: Absorption costing method is different from marginal costing as it

categorise both variable as well as fixed cost as product cost. It is basically used for reporting

purpose in terms of tax as well as financial reporting. As fixed cost is taken within product cost

due to which the profit gets minimised (Boyns, Edwards and Nikitin, 2013).

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production 4000 4000

processes

In business scenario, management accounting reports and systems are equally

interrelated with each other in different ways. As it is also stated that accounting systems are so

much essential as it help to formulate vital accounting reports so that business decisions are

made to overcome uncertain condition within workplace (Novas, Alves and Sousa, 2017).

Managers of KFE manufacturing company set account receivable reports with the support of

price optimisation system which so that product at suitable price can be sold to large number of

customer on credit basis.

TASK 2

P3: Preparation of income statements with the use of absorption and marginal costing method

Marginal costing method: Marginal costing is an essential method that helps in

preparation of income system as it include variable cost which are categorised as product cost.

Whereas, within this method fixed cost is categorised as cost incurred within specific period.

Here profit is calculated with the use of profit volume ratio and is presented to outline the total

contribution made by company.

Absorption costing: Absorption costing method is different from marginal costing as it

categorise both variable as well as fixed cost as product cost. It is basically used for reporting

purpose in terms of tax as well as financial reporting. As fixed cost is taken within product cost

due to which the profit gets minimised (Boyns, Edwards and Nikitin, 2013).

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production 4000 4000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

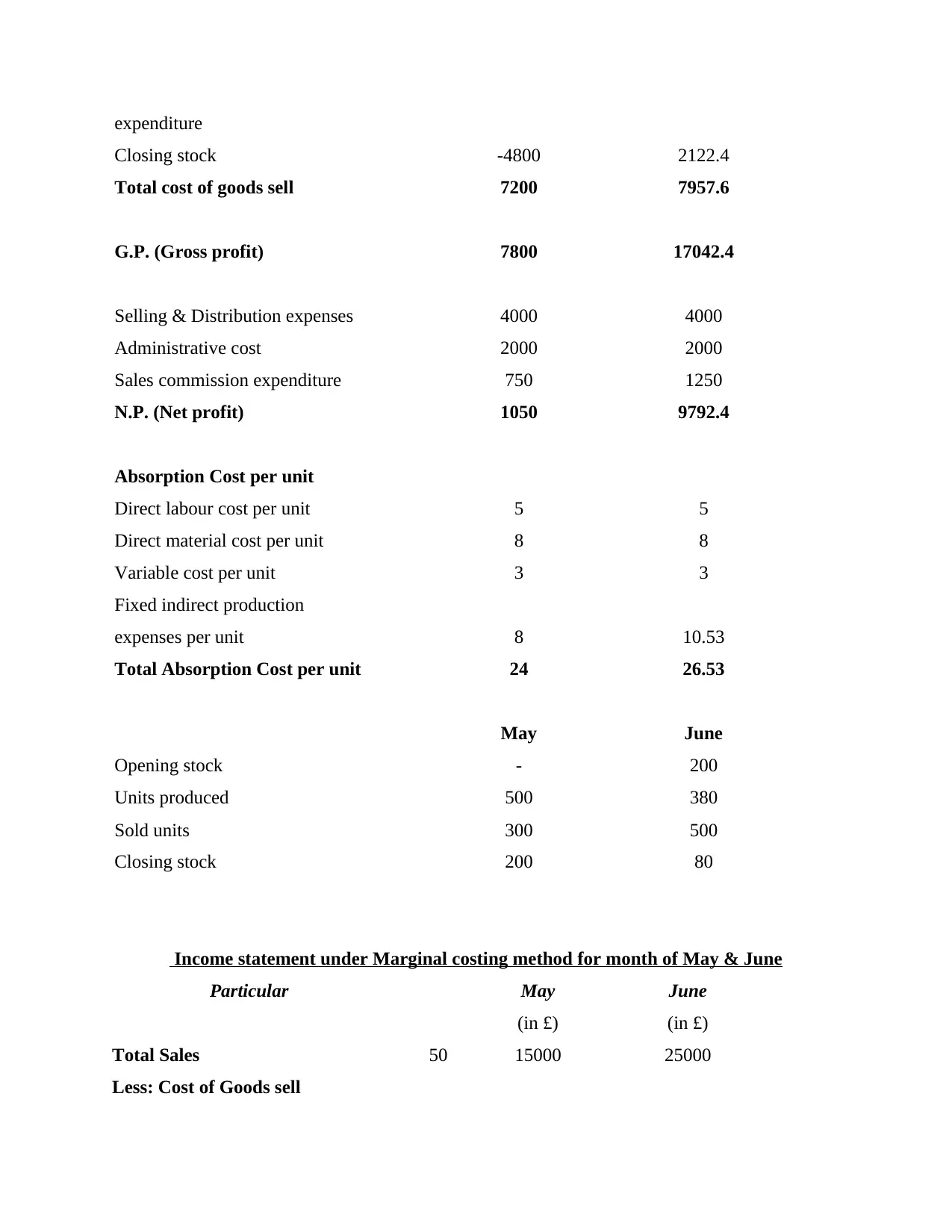

expenditure

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production

expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: Cost of Goods sell

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production

expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

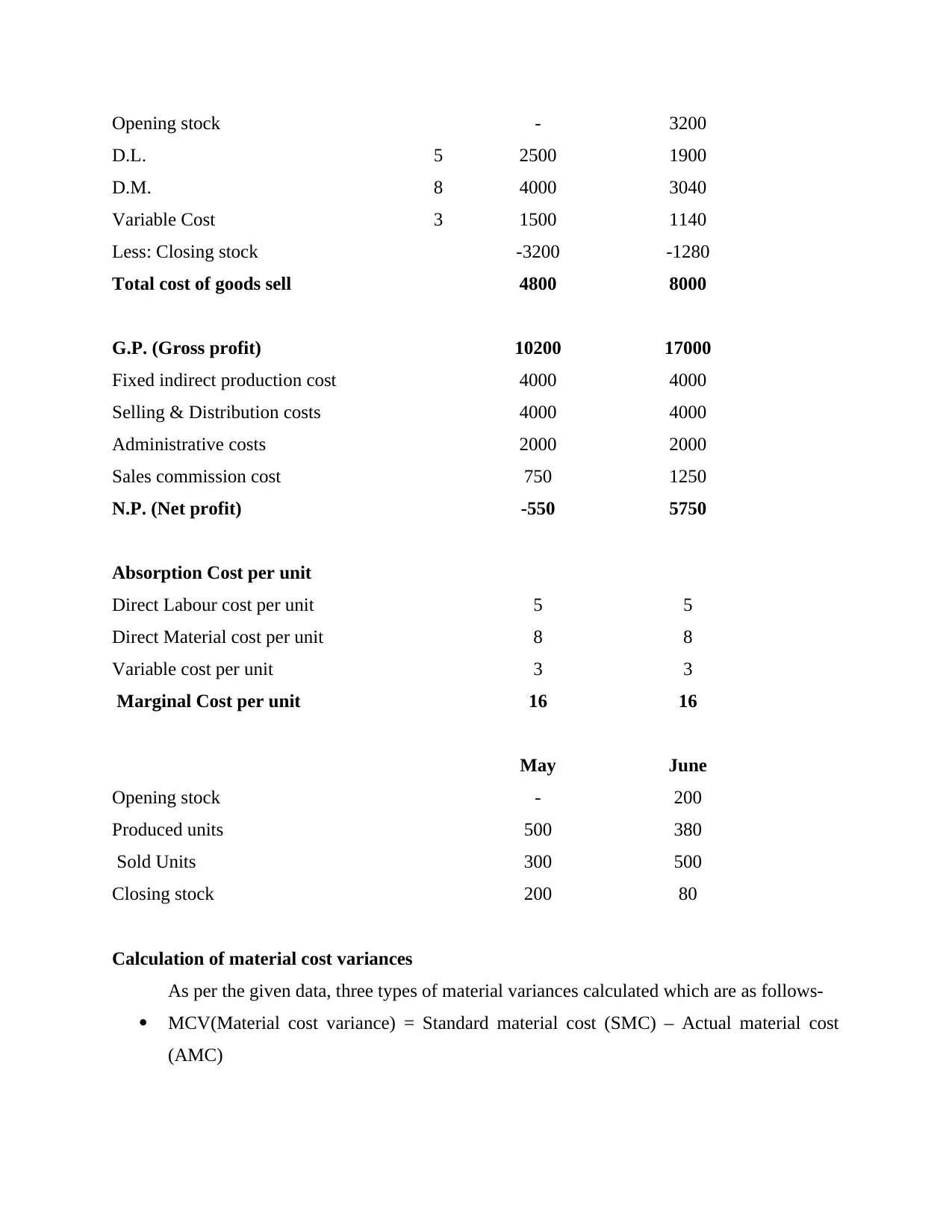

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: Cost of Goods sell

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total cost of goods sell 4800 8000

G.P. (Gross profit) 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

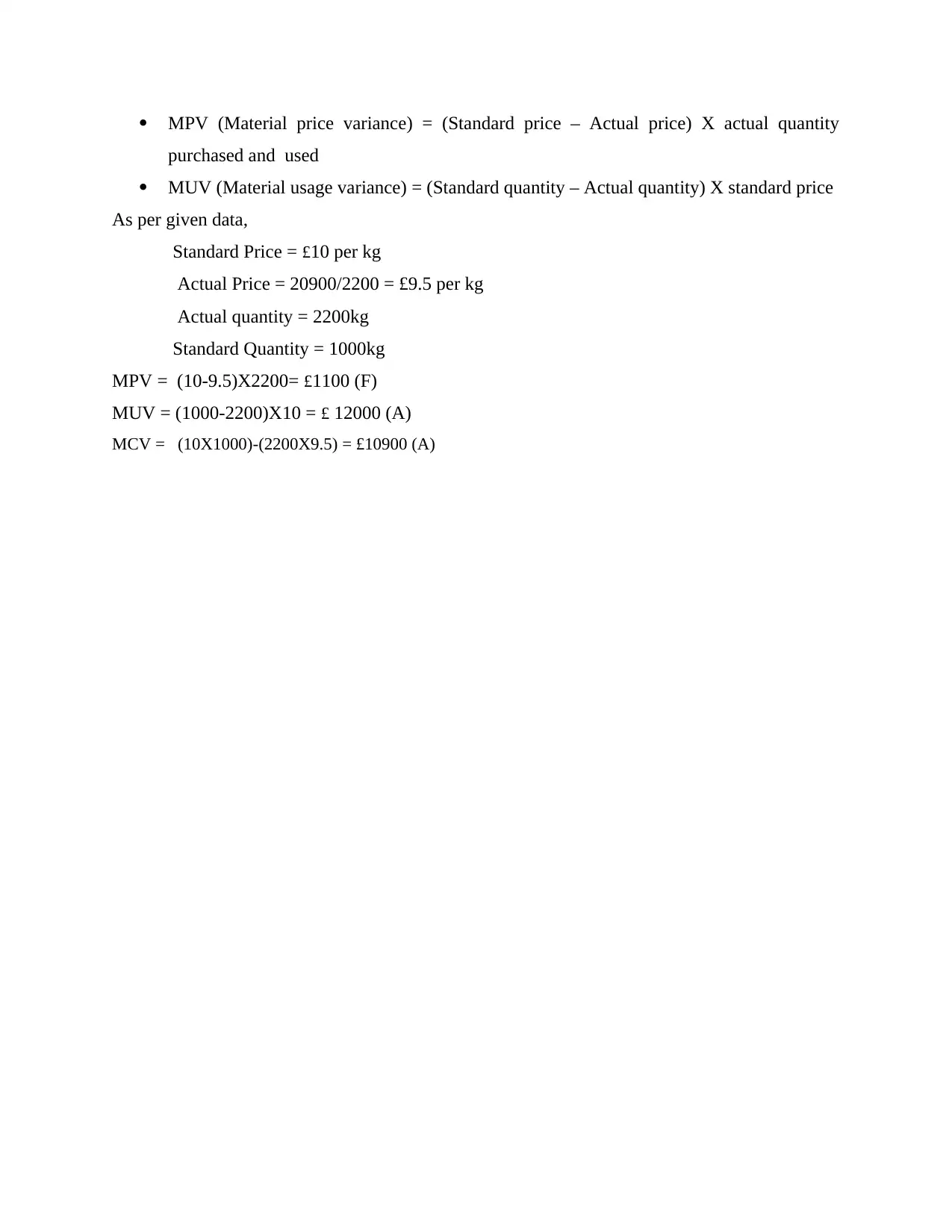

Calculation of material cost variances

As per the given data, three types of material variances calculated which are as follows-

MCV(Material cost variance) = Standard material cost (SMC) – Actual material cost

(AMC)

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total cost of goods sell 4800 8000

G.P. (Gross profit) 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Calculation of material cost variances

As per the given data, three types of material variances calculated which are as follows-

MCV(Material cost variance) = Standard material cost (SMC) – Actual material cost

(AMC)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MPV (Material price variance) = (Standard price – Actual price) X actual quantity

purchased and used

MUV (Material usage variance) = (Standard quantity – Actual quantity) X standard price

As per given data,

Standard Price = £10 per kg

Actual Price = 20900/2200 = £9.5 per kg

Actual quantity = 2200kg

Standard Quantity = 1000kg

MPV = (10-9.5)X2200= £1100 (F)

MUV = (1000-2200)X10 = £ 12000 (A)

MCV = (10X1000)-(2200X9.5) = £10900 (A)

purchased and used

MUV (Material usage variance) = (Standard quantity – Actual quantity) X standard price

As per given data,

Standard Price = £10 per kg

Actual Price = 20900/2200 = £9.5 per kg

Actual quantity = 2200kg

Standard Quantity = 1000kg

MPV = (10-9.5)X2200= £1100 (F)

MUV = (1000-2200)X10 = £ 12000 (A)

MCV = (10X1000)-(2200X9.5) = £10900 (A)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

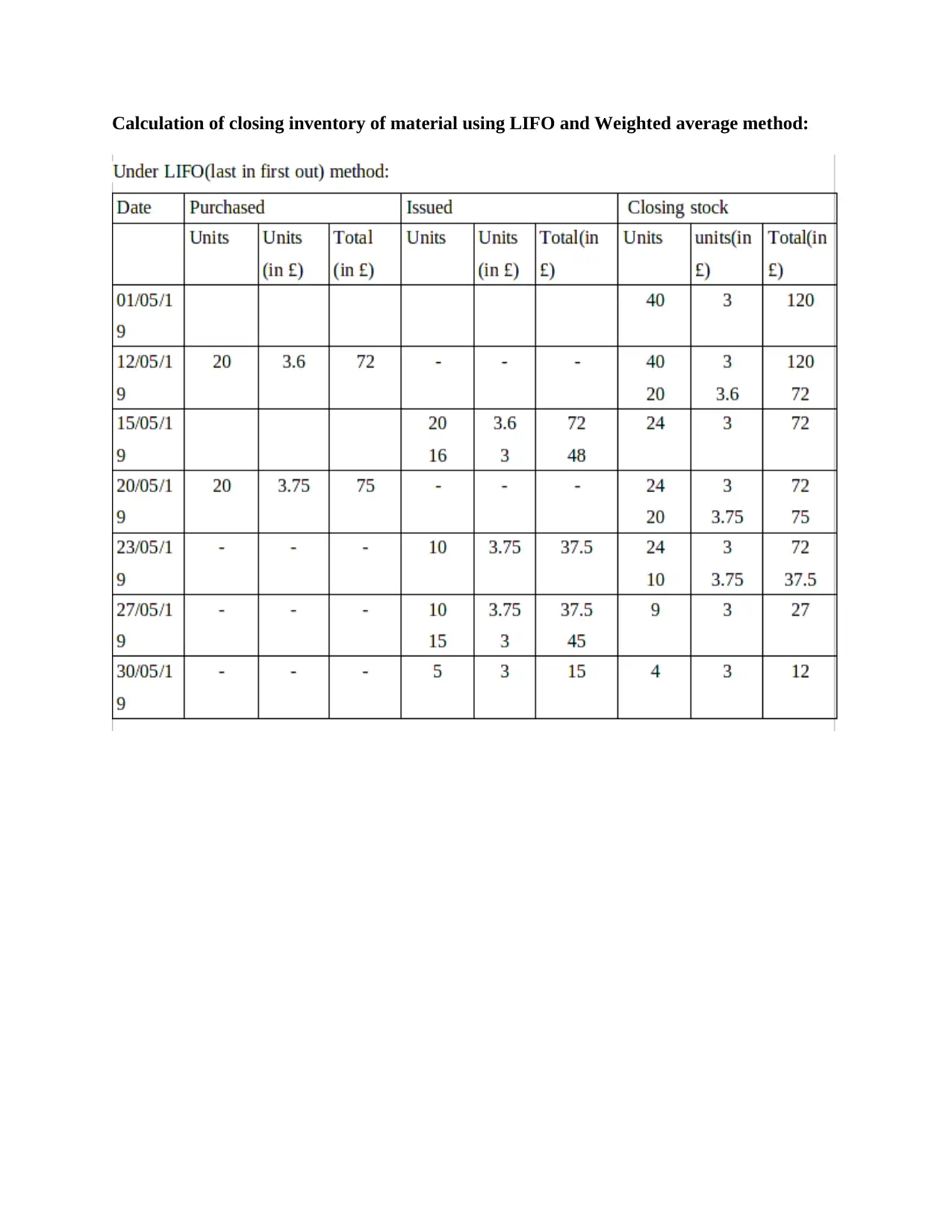

Calculation of closing inventory of material using LIFO and Weighted average method:

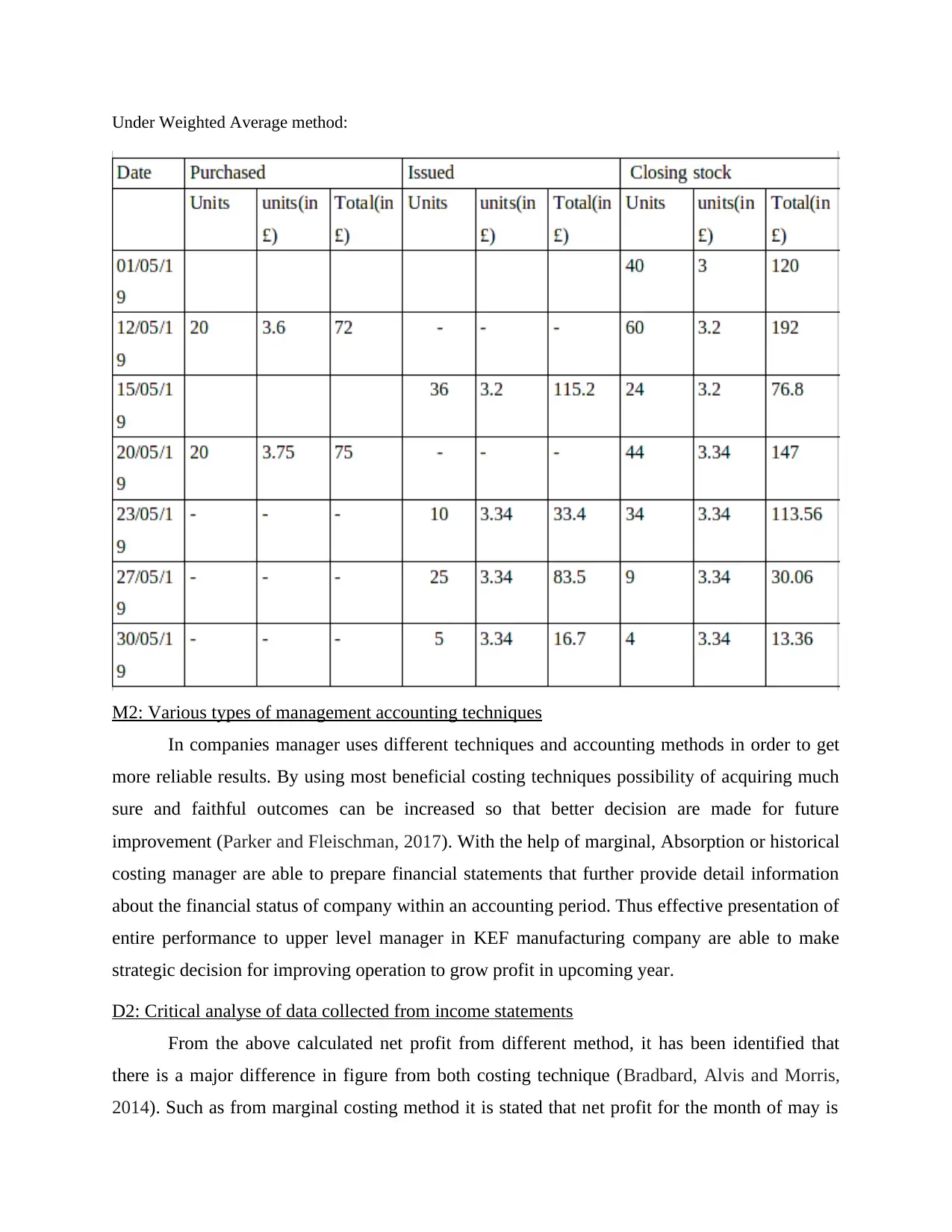

Under Weighted Average method:

M2: Various types of management accounting techniques

In companies manager uses different techniques and accounting methods in order to get

more reliable results. By using most beneficial costing techniques possibility of acquiring much

sure and faithful outcomes can be increased so that better decision are made for future

improvement (Parker and Fleischman, 2017). With the help of marginal, Absorption or historical

costing manager are able to prepare financial statements that further provide detail information

about the financial status of company within an accounting period. Thus effective presentation of

entire performance to upper level manager in KEF manufacturing company are able to make

strategic decision for improving operation to grow profit in upcoming year.

D2: Critical analyse of data collected from income statements

From the above calculated net profit from different method, it has been identified that

there is a major difference in figure from both costing technique (Bradbard, Alvis and Morris,

2014). Such as from marginal costing method it is stated that net profit for the month of may is

M2: Various types of management accounting techniques

In companies manager uses different techniques and accounting methods in order to get

more reliable results. By using most beneficial costing techniques possibility of acquiring much

sure and faithful outcomes can be increased so that better decision are made for future

improvement (Parker and Fleischman, 2017). With the help of marginal, Absorption or historical

costing manager are able to prepare financial statements that further provide detail information

about the financial status of company within an accounting period. Thus effective presentation of

entire performance to upper level manager in KEF manufacturing company are able to make

strategic decision for improving operation to grow profit in upcoming year.

D2: Critical analyse of data collected from income statements

From the above calculated net profit from different method, it has been identified that

there is a major difference in figure from both costing technique (Bradbard, Alvis and Morris,

2014). Such as from marginal costing method it is stated that net profit for the month of may is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.