Management Accounting Report: Strategies for Taj Store's Success

VerifiedAdded on 2020/06/05

|16

|4922

|31

Report

AI Summary

This report offers a comprehensive analysis of management accounting principles, specifically tailored for Taj Store, a grocery shop in London. It begins with an introduction to management accounting systems, highlighting their importance in decision-making and financial control. The report then delves into specific areas like inventory management, cost accounting, and job costing, emphasizing their role in optimizing operations. It differentiates between financial and managerial accounting, outlining their respective stakeholders and objectives. The report further explores various management accounting reporting methods, including inventory management, accounts receivable, performance, accounts payable, and budget reporting. A key section contrasts marginal and absorption costing methods in income statements. Finally, the report discusses planning tools used for budgetary control and the adoption of management accounting systems to address financial challenges, providing a holistic view of how these practices can drive business success.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting systems and their essential requirements.................................1

P2. Methods of management accounting reporting ...............................................................4

TASK 2............................................................................................................................................5

P3 Difference between income statement made through marginal and absorption costing...5

TASK 3 ..........................................................................................................................................9

P4 Advantages and disadvantages of planning tools which are used for budgetary control..9

P5 Adopting management accounting systems for responding financial troubles .............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting systems and their essential requirements.................................1

P2. Methods of management accounting reporting ...............................................................4

TASK 2............................................................................................................................................5

P3 Difference between income statement made through marginal and absorption costing...5

TASK 3 ..........................................................................................................................................9

P4 Advantages and disadvantages of planning tools which are used for budgetary control..9

P5 Adopting management accounting systems for responding financial troubles .............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a well defined procedure that helps in analysis of financial

and non-financial data that will be use in crucial decision making that is related to investment

and operational control in firm (Renz, 2016). MA focuses on increasing returns by reduces cost

of various options like production or expenditures. Taj store is a grocery shop that operates their

business in London, United Kingdom. This organisation is working in small level but they start

their business in 1936. This report will asses management accounting with its variants and their

essential use in corporation. Some methods of MA are discussed in this report. This assignment

consist detailed explanation of income statement. Various budgets are also discussed in this

report.

TASK 1

P1. Management accounting systems and their essential requirements

It is compulsory for every organization to make right decision at correct time to ensure

profitability of business. Management accounting helps in the decision making systems because

it has many variants that are able to solve many financial and non-financial problems. Raise

funds for business operations are not easy for small enterprise like Taj Store. They depend on the

loans with low interest rates to raise funds and assign those funds in that areas which enables

high return for firm (Banerjee, 2012). Financial accounting helps in assignment of funds with

help of its other functions like inventory management, cost management etc. Basic focus of MA

is recording transaction that arise in daily operations in corporation. There are various

differences in financial and managerial accounting that are given as below:

Financial Accounting Managerial Accounting

It is made for external stakeholders like

consumers, suppliers, etc.

It is made for internal stakeholders like junior

employees, board members, managers, etc.

Historical data is required in this type and it

does not follow proper time schedule to

prepare.

It is a present year document that is made for

future purpose.

It includes all transactions that happen in

organization as a whole.

It records only particular and specific data.

1

Management accounting is a well defined procedure that helps in analysis of financial

and non-financial data that will be use in crucial decision making that is related to investment

and operational control in firm (Renz, 2016). MA focuses on increasing returns by reduces cost

of various options like production or expenditures. Taj store is a grocery shop that operates their

business in London, United Kingdom. This organisation is working in small level but they start

their business in 1936. This report will asses management accounting with its variants and their

essential use in corporation. Some methods of MA are discussed in this report. This assignment

consist detailed explanation of income statement. Various budgets are also discussed in this

report.

TASK 1

P1. Management accounting systems and their essential requirements

It is compulsory for every organization to make right decision at correct time to ensure

profitability of business. Management accounting helps in the decision making systems because

it has many variants that are able to solve many financial and non-financial problems. Raise

funds for business operations are not easy for small enterprise like Taj Store. They depend on the

loans with low interest rates to raise funds and assign those funds in that areas which enables

high return for firm (Banerjee, 2012). Financial accounting helps in assignment of funds with

help of its other functions like inventory management, cost management etc. Basic focus of MA

is recording transaction that arise in daily operations in corporation. There are various

differences in financial and managerial accounting that are given as below:

Financial Accounting Managerial Accounting

It is made for external stakeholders like

consumers, suppliers, etc.

It is made for internal stakeholders like junior

employees, board members, managers, etc.

Historical data is required in this type and it

does not follow proper time schedule to

prepare.

It is a present year document that is made for

future purpose.

It includes all transactions that happen in

organization as a whole.

It records only particular and specific data.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It focuses only on the financial data. Although it concentrates in financial and non-

financial areas both.

It is mandatory for organization to keep all

financial data to meet legal requirements.

There is no legal boundaries that pressurise to

keep the management accounts.

Small scale companies have limited resources that have to put in that task which can

provide high returns. Management accounting process recognises all mistakes attempted by

managers repeatedly in inventory control and price optimising system. It helps in diminishing the

confusion among various functional levels and it also reduces the time that is taken to make a

call. Cost accounting and job costing are some other kinds of systems that focus on minimising

the expenditure that are associated with production department. Complete explanation is given as

below:

Inventory Management system- If an organization does not manage its raw materials and

keep extra goods in their warehouses that increases cost of carry and enhances overall expenses.

On the other hand if firm have less than required inventory it delays production and maximise

expenditure of supply chain (Herzig and et. al., 2012). This kind of action will affect demand

meeting negatively and reduces customer base for corporation. Inventory management system is

a software that is used for managing deliveries, recording of available and sold stock, etc. For

making an order, it is necessary to identify accurate number of orders that can be measured by

EOQ i.e. Economic Order Quantity. This software of accounting helps in the decrement of

wastage of resources by tracking all records. It also assures smooth operations of business by

keeping all records regarding inventory which has to be in warehouse for the next production.

Some organizations keep their product’s record on the basis of margin. If an item earns more

profit then it gains more attention of supply chain management system.

2

financial areas both.

It is mandatory for organization to keep all

financial data to meet legal requirements.

There is no legal boundaries that pressurise to

keep the management accounts.

Small scale companies have limited resources that have to put in that task which can

provide high returns. Management accounting process recognises all mistakes attempted by

managers repeatedly in inventory control and price optimising system. It helps in diminishing the

confusion among various functional levels and it also reduces the time that is taken to make a

call. Cost accounting and job costing are some other kinds of systems that focus on minimising

the expenditure that are associated with production department. Complete explanation is given as

below:

Inventory Management system- If an organization does not manage its raw materials and

keep extra goods in their warehouses that increases cost of carry and enhances overall expenses.

On the other hand if firm have less than required inventory it delays production and maximise

expenditure of supply chain (Herzig and et. al., 2012). This kind of action will affect demand

meeting negatively and reduces customer base for corporation. Inventory management system is

a software that is used for managing deliveries, recording of available and sold stock, etc. For

making an order, it is necessary to identify accurate number of orders that can be measured by

EOQ i.e. Economic Order Quantity. This software of accounting helps in the decrement of

wastage of resources by tracking all records. It also assures smooth operations of business by

keeping all records regarding inventory which has to be in warehouse for the next production.

Some organizations keep their product’s record on the basis of margin. If an item earns more

profit then it gains more attention of supply chain management system.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting system: It is a software that manages over costing and stops wastages of

resources. It is an important part of management accounting that checks and manages the cost

that is related to various aspects like wages, manufacturing cost, etc. This function has a wide

scope but generally it is used in the production department. Managers use this as a tool of

identification of profit on specific products. Diminish direct labour cost and material cost are

main areas of focus (DRURY, 2013).

Job costing: This method studies profitability that is related to various jobs and analyse

capacity of these jobs. According to this analysis, if jobs are well doing then management

increases their no to obtain goals in lesser time. This option also expresses tasks and actions that

are generating low benefits and managers can remove these tasks from operations. This is mainly

used at the time when company has specific demands.

Price Optimisation System: Price of a product is very important part that affects its

demand directly in positive and negative manner. It is the responsibility of managerial

accounting to finds out number of high priced products in portfolio of company and check

whether they are generating profit or not (Morales and Lambert, 2013). A customer denies to buy

a product that have high rate and easily buys its substitutes that have low price. Price should not

be that much low that will be reason of company loss but it should not be that much higher that

3

Illustration 1: Inventory Management

(Source: Orendorff, 2017)

resources. It is an important part of management accounting that checks and manages the cost

that is related to various aspects like wages, manufacturing cost, etc. This function has a wide

scope but generally it is used in the production department. Managers use this as a tool of

identification of profit on specific products. Diminish direct labour cost and material cost are

main areas of focus (DRURY, 2013).

Job costing: This method studies profitability that is related to various jobs and analyse

capacity of these jobs. According to this analysis, if jobs are well doing then management

increases their no to obtain goals in lesser time. This option also expresses tasks and actions that

are generating low benefits and managers can remove these tasks from operations. This is mainly

used at the time when company has specific demands.

Price Optimisation System: Price of a product is very important part that affects its

demand directly in positive and negative manner. It is the responsibility of managerial

accounting to finds out number of high priced products in portfolio of company and check

whether they are generating profit or not (Morales and Lambert, 2013). A customer denies to buy

a product that have high rate and easily buys its substitutes that have low price. Price should not

be that much low that will be reason of company loss but it should not be that much higher that

3

Illustration 1: Inventory Management

(Source: Orendorff, 2017)

customer would not purchase it. It must be in correct proportion so that customer will buy goods

and this action will generate profits also. This tool is associated with the price management.

P2. Methods of management accounting reporting

Each and every organizations record their transactions to evaluate their working that they

have done in their past. These are documents that is made for removing drawbacks of past

procedures and will help in successful future plans. These reports have matching criteria that

evaluates current objective with achieved targets. Distinct management accounting reports are

described below:

Inventory management reports: This is made for checking whether stock is properly

managed or not and if it is not what will be the ways of managing this in coming time period.

This action is helpful in removing problems related to stock for e.g. over and under stacking

without wasting time. This report is a presentor of present stock that is available in organization

and how much is needed for accomplishment of demands in particular time. Taj Store can accept

this to decrease its ordering and carrying cost and this method will help in identifying proper

needs of stock which is necessary to fulfil customers’ demands in correct time duration. This

kind of reporting hikes sale of enterprise. Venture is selling various kind of goods and items so

inventory control is mandatory for getting support in recognition of expected quantity of goods

which customer may buy in recent time. This task is done with help of past records and mistakes

(Ward, 2012).

Accounts receivables reporting - Taj store is running their business since long time in

United Kingdom. They have many customers that use to buy goods on credit basis and make

payments on schedule basis not at every time. This report concerns these kind of customers and

manages their records. This reporting includes data of record of data related to money that is a

receivable for company. Some corporations make this report on weekly, monthly and yearly

basis and some other firm do not focus on time period but they are concerned about total money

that are receivable from debtors. Taj store makes this report on their convenience but they are

very good in making and keeping this report in their venture. Main purpose of making this report

is that it reduces debt of organization. They will use this report in best way as they can and they

can make strict rules for those who are weak in payment and secures their payment with help of

this tool.

4

and this action will generate profits also. This tool is associated with the price management.

P2. Methods of management accounting reporting

Each and every organizations record their transactions to evaluate their working that they

have done in their past. These are documents that is made for removing drawbacks of past

procedures and will help in successful future plans. These reports have matching criteria that

evaluates current objective with achieved targets. Distinct management accounting reports are

described below:

Inventory management reports: This is made for checking whether stock is properly

managed or not and if it is not what will be the ways of managing this in coming time period.

This action is helpful in removing problems related to stock for e.g. over and under stacking

without wasting time. This report is a presentor of present stock that is available in organization

and how much is needed for accomplishment of demands in particular time. Taj Store can accept

this to decrease its ordering and carrying cost and this method will help in identifying proper

needs of stock which is necessary to fulfil customers’ demands in correct time duration. This

kind of reporting hikes sale of enterprise. Venture is selling various kind of goods and items so

inventory control is mandatory for getting support in recognition of expected quantity of goods

which customer may buy in recent time. This task is done with help of past records and mistakes

(Ward, 2012).

Accounts receivables reporting - Taj store is running their business since long time in

United Kingdom. They have many customers that use to buy goods on credit basis and make

payments on schedule basis not at every time. This report concerns these kind of customers and

manages their records. This reporting includes data of record of data related to money that is a

receivable for company. Some corporations make this report on weekly, monthly and yearly

basis and some other firm do not focus on time period but they are concerned about total money

that are receivable from debtors. Taj store makes this report on their convenience but they are

very good in making and keeping this report in their venture. Main purpose of making this report

is that it reduces debt of organization. They will use this report in best way as they can and they

can make strict rules for those who are weak in payment and secures their payment with help of

this tool.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

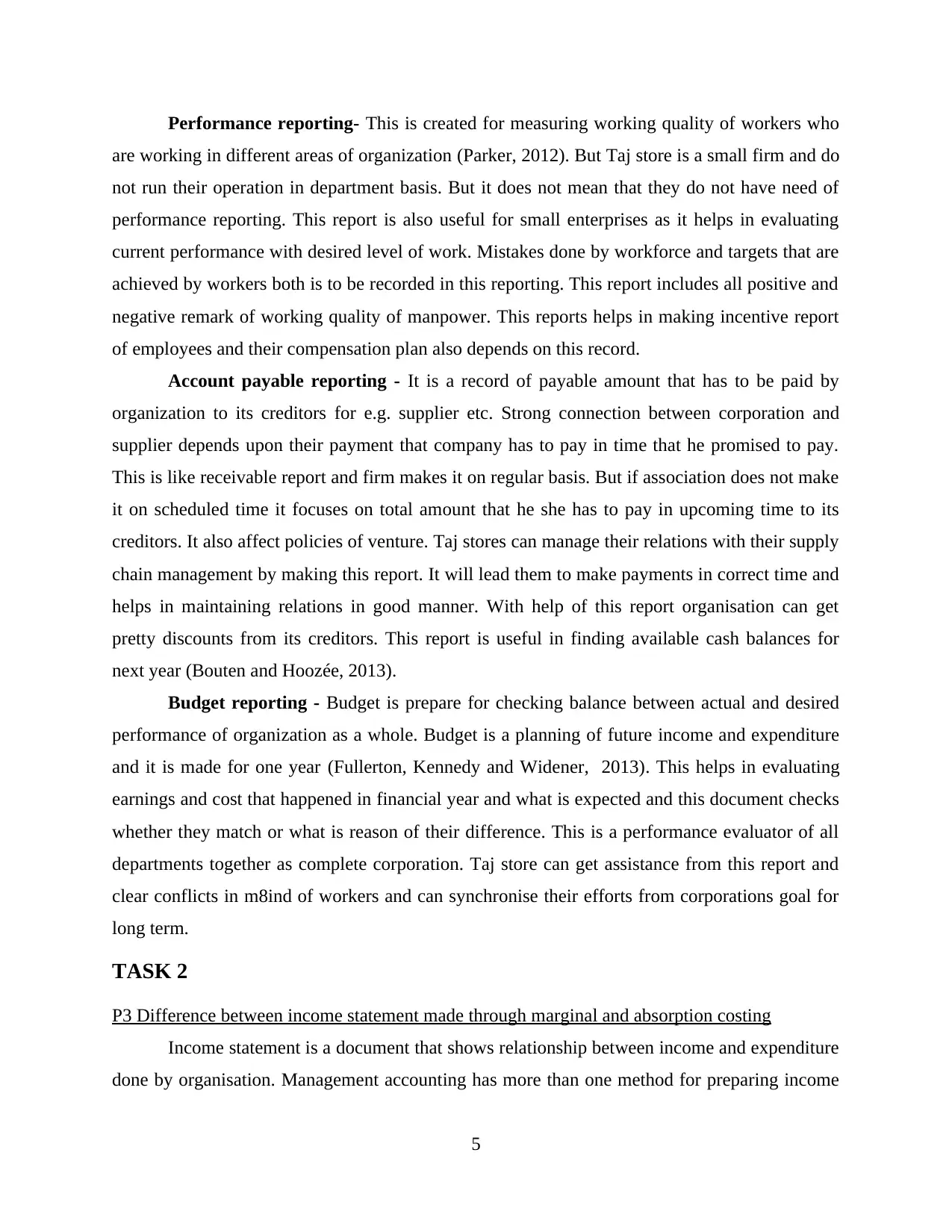

Performance reporting- This is created for measuring working quality of workers who

are working in different areas of organization (Parker, 2012). But Taj store is a small firm and do

not run their operation in department basis. But it does not mean that they do not have need of

performance reporting. This report is also useful for small enterprises as it helps in evaluating

current performance with desired level of work. Mistakes done by workforce and targets that are

achieved by workers both is to be recorded in this reporting. This report includes all positive and

negative remark of working quality of manpower. This reports helps in making incentive report

of employees and their compensation plan also depends on this record.

Account payable reporting - It is a record of payable amount that has to be paid by

organization to its creditors for e.g. supplier etc. Strong connection between corporation and

supplier depends upon their payment that company has to pay in time that he promised to pay.

This is like receivable report and firm makes it on regular basis. But if association does not make

it on scheduled time it focuses on total amount that he she has to pay in upcoming time to its

creditors. It also affect policies of venture. Taj stores can manage their relations with their supply

chain management by making this report. It will lead them to make payments in correct time and

helps in maintaining relations in good manner. With help of this report organisation can get

pretty discounts from its creditors. This report is useful in finding available cash balances for

next year (Bouten and Hoozée, 2013).

Budget reporting - Budget is prepare for checking balance between actual and desired

performance of organization as a whole. Budget is a planning of future income and expenditure

and it is made for one year (Fullerton, Kennedy and Widener, 2013). This helps in evaluating

earnings and cost that happened in financial year and what is expected and this document checks

whether they match or what is reason of their difference. This is a performance evaluator of all

departments together as complete corporation. Taj store can get assistance from this report and

clear conflicts in m8ind of workers and can synchronise their efforts from corporations goal for

long term.

TASK 2

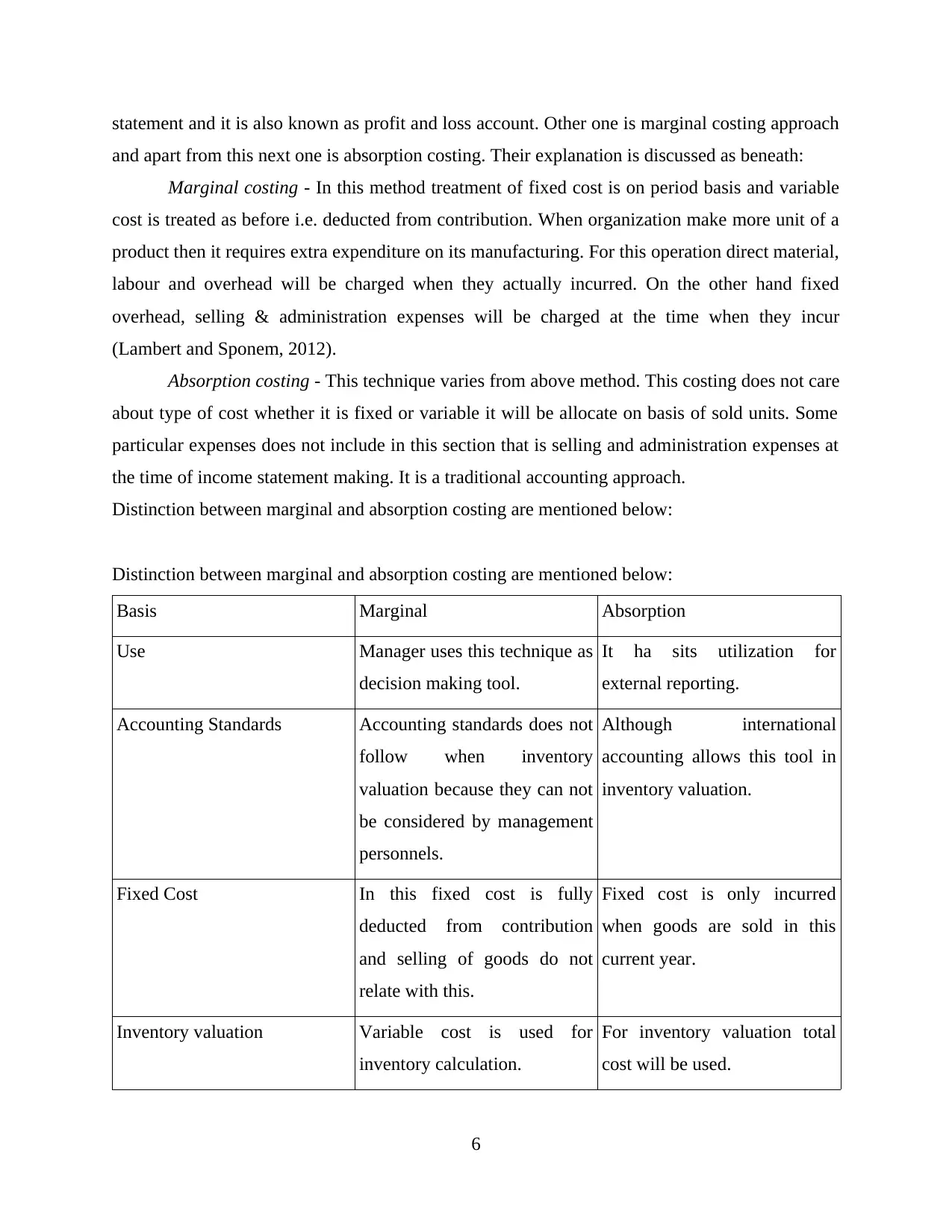

P3 Difference between income statement made through marginal and absorption costing

Income statement is a document that shows relationship between income and expenditure

done by organisation. Management accounting has more than one method for preparing income

5

are working in different areas of organization (Parker, 2012). But Taj store is a small firm and do

not run their operation in department basis. But it does not mean that they do not have need of

performance reporting. This report is also useful for small enterprises as it helps in evaluating

current performance with desired level of work. Mistakes done by workforce and targets that are

achieved by workers both is to be recorded in this reporting. This report includes all positive and

negative remark of working quality of manpower. This reports helps in making incentive report

of employees and their compensation plan also depends on this record.

Account payable reporting - It is a record of payable amount that has to be paid by

organization to its creditors for e.g. supplier etc. Strong connection between corporation and

supplier depends upon their payment that company has to pay in time that he promised to pay.

This is like receivable report and firm makes it on regular basis. But if association does not make

it on scheduled time it focuses on total amount that he she has to pay in upcoming time to its

creditors. It also affect policies of venture. Taj stores can manage their relations with their supply

chain management by making this report. It will lead them to make payments in correct time and

helps in maintaining relations in good manner. With help of this report organisation can get

pretty discounts from its creditors. This report is useful in finding available cash balances for

next year (Bouten and Hoozée, 2013).

Budget reporting - Budget is prepare for checking balance between actual and desired

performance of organization as a whole. Budget is a planning of future income and expenditure

and it is made for one year (Fullerton, Kennedy and Widener, 2013). This helps in evaluating

earnings and cost that happened in financial year and what is expected and this document checks

whether they match or what is reason of their difference. This is a performance evaluator of all

departments together as complete corporation. Taj store can get assistance from this report and

clear conflicts in m8ind of workers and can synchronise their efforts from corporations goal for

long term.

TASK 2

P3 Difference between income statement made through marginal and absorption costing

Income statement is a document that shows relationship between income and expenditure

done by organisation. Management accounting has more than one method for preparing income

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statement and it is also known as profit and loss account. Other one is marginal costing approach

and apart from this next one is absorption costing. Their explanation is discussed as beneath:

Marginal costing - In this method treatment of fixed cost is on period basis and variable

cost is treated as before i.e. deducted from contribution. When organization make more unit of a

product then it requires extra expenditure on its manufacturing. For this operation direct material,

labour and overhead will be charged when they actually incurred. On the other hand fixed

overhead, selling & administration expenses will be charged at the time when they incur

(Lambert and Sponem, 2012).

Absorption costing - This technique varies from above method. This costing does not care

about type of cost whether it is fixed or variable it will be allocate on basis of sold units. Some

particular expenses does not include in this section that is selling and administration expenses at

the time of income statement making. It is a traditional accounting approach.

Distinction between marginal and absorption costing are mentioned below:

Distinction between marginal and absorption costing are mentioned below:

Basis Marginal Absorption

Use Manager uses this technique as

decision making tool.

It ha sits utilization for

external reporting.

Accounting Standards Accounting standards does not

follow when inventory

valuation because they can not

be considered by management

personnels.

Although international

accounting allows this tool in

inventory valuation.

Fixed Cost In this fixed cost is fully

deducted from contribution

and selling of goods do not

relate with this.

Fixed cost is only incurred

when goods are sold in this

current year.

Inventory valuation Variable cost is used for

inventory calculation.

For inventory valuation total

cost will be used.

6

and apart from this next one is absorption costing. Their explanation is discussed as beneath:

Marginal costing - In this method treatment of fixed cost is on period basis and variable

cost is treated as before i.e. deducted from contribution. When organization make more unit of a

product then it requires extra expenditure on its manufacturing. For this operation direct material,

labour and overhead will be charged when they actually incurred. On the other hand fixed

overhead, selling & administration expenses will be charged at the time when they incur

(Lambert and Sponem, 2012).

Absorption costing - This technique varies from above method. This costing does not care

about type of cost whether it is fixed or variable it will be allocate on basis of sold units. Some

particular expenses does not include in this section that is selling and administration expenses at

the time of income statement making. It is a traditional accounting approach.

Distinction between marginal and absorption costing are mentioned below:

Distinction between marginal and absorption costing are mentioned below:

Basis Marginal Absorption

Use Manager uses this technique as

decision making tool.

It ha sits utilization for

external reporting.

Accounting Standards Accounting standards does not

follow when inventory

valuation because they can not

be considered by management

personnels.

Although international

accounting allows this tool in

inventory valuation.

Fixed Cost In this fixed cost is fully

deducted from contribution

and selling of goods do not

relate with this.

Fixed cost is only incurred

when goods are sold in this

current year.

Inventory valuation Variable cost is used for

inventory calculation.

For inventory valuation total

cost will be used.

6

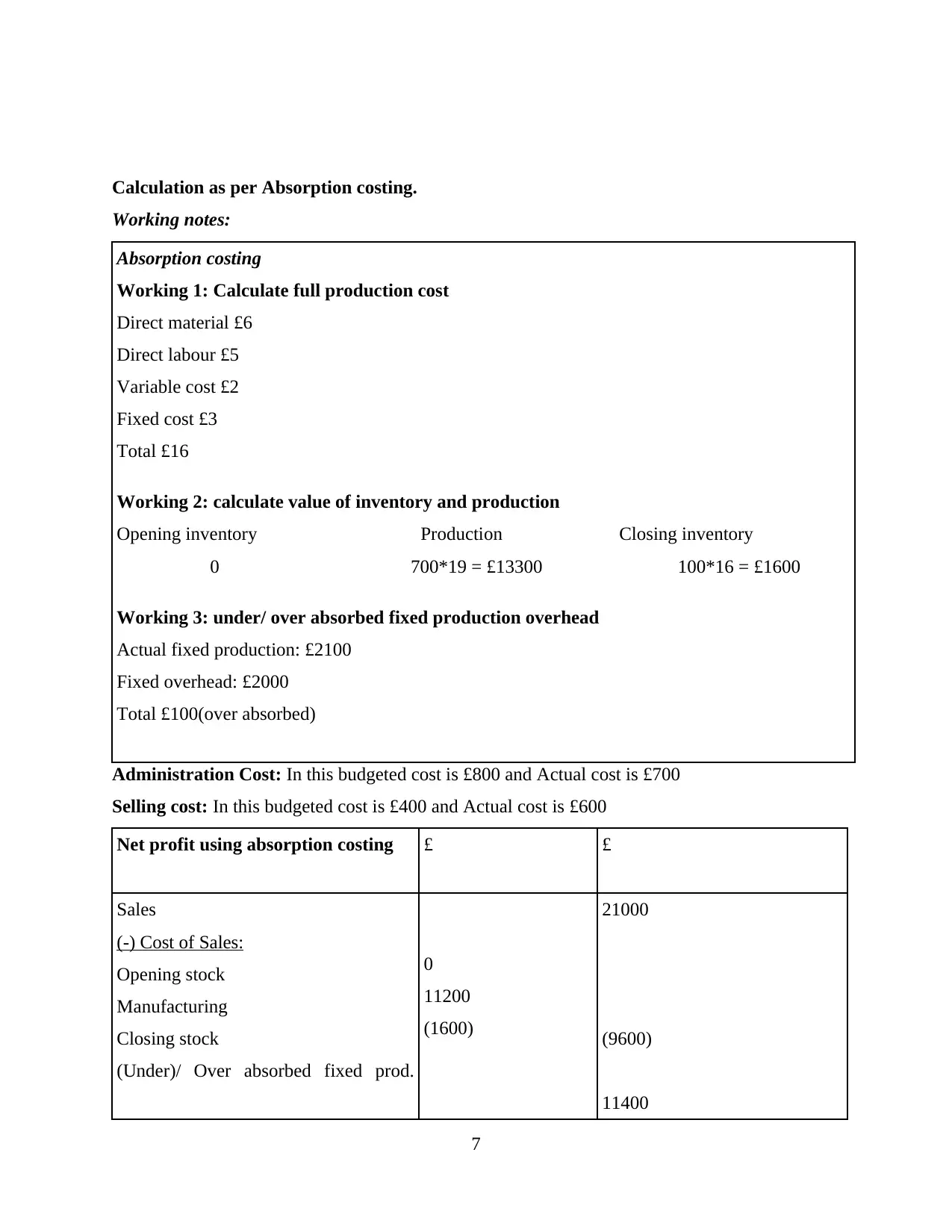

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

0

11200

(1600)

21000

(9600)

11400

7

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

0

11200

(1600)

21000

(9600)

11400

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

600

700

600

(100) (1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

0

9100

(1300)

2000

21000

(7800)

13200

8

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

600

700

600

(100) (1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

0

9100

(1300)

2000

21000

(7800)

13200

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

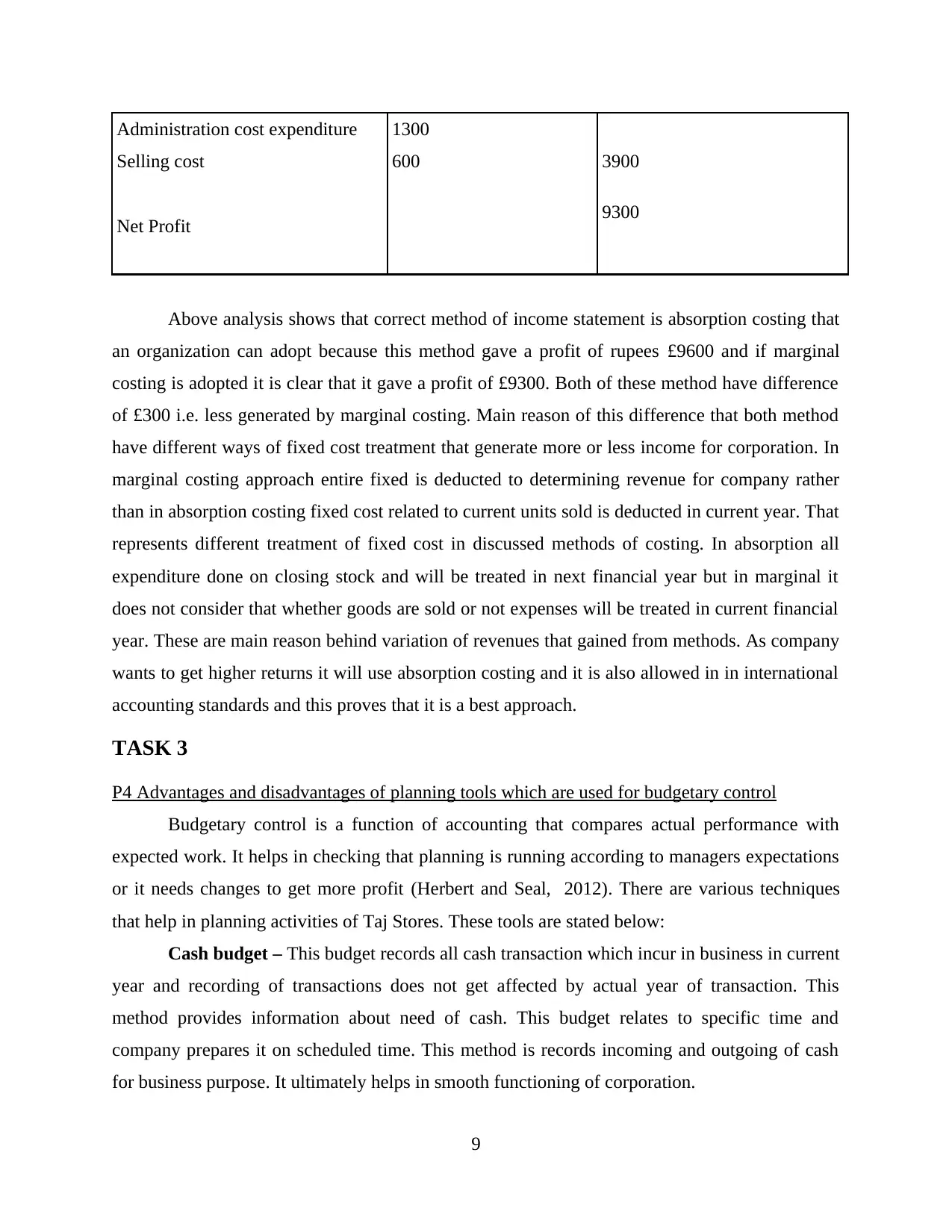

Administration cost expenditure

Selling cost

Net Profit

1300

600 3900

9300

Above analysis shows that correct method of income statement is absorption costing that

an organization can adopt because this method gave a profit of rupees £9600 and if marginal

costing is adopted it is clear that it gave a profit of £9300. Both of these method have difference

of £300 i.e. less generated by marginal costing. Main reason of this difference that both method

have different ways of fixed cost treatment that generate more or less income for corporation. In

marginal costing approach entire fixed is deducted to determining revenue for company rather

than in absorption costing fixed cost related to current units sold is deducted in current year. That

represents different treatment of fixed cost in discussed methods of costing. In absorption all

expenditure done on closing stock and will be treated in next financial year but in marginal it

does not consider that whether goods are sold or not expenses will be treated in current financial

year. These are main reason behind variation of revenues that gained from methods. As company

wants to get higher returns it will use absorption costing and it is also allowed in in international

accounting standards and this proves that it is a best approach.

TASK 3

P4 Advantages and disadvantages of planning tools which are used for budgetary control

Budgetary control is a function of accounting that compares actual performance with

expected work. It helps in checking that planning is running according to managers expectations

or it needs changes to get more profit (Herbert and Seal, 2012). There are various techniques

that help in planning activities of Taj Stores. These tools are stated below:

Cash budget – This budget records all cash transaction which incur in business in current

year and recording of transactions does not get affected by actual year of transaction. This

method provides information about need of cash. This budget relates to specific time and

company prepares it on scheduled time. This method is records incoming and outgoing of cash

for business purpose. It ultimately helps in smooth functioning of corporation.

9

Selling cost

Net Profit

1300

600 3900

9300

Above analysis shows that correct method of income statement is absorption costing that

an organization can adopt because this method gave a profit of rupees £9600 and if marginal

costing is adopted it is clear that it gave a profit of £9300. Both of these method have difference

of £300 i.e. less generated by marginal costing. Main reason of this difference that both method

have different ways of fixed cost treatment that generate more or less income for corporation. In

marginal costing approach entire fixed is deducted to determining revenue for company rather

than in absorption costing fixed cost related to current units sold is deducted in current year. That

represents different treatment of fixed cost in discussed methods of costing. In absorption all

expenditure done on closing stock and will be treated in next financial year but in marginal it

does not consider that whether goods are sold or not expenses will be treated in current financial

year. These are main reason behind variation of revenues that gained from methods. As company

wants to get higher returns it will use absorption costing and it is also allowed in in international

accounting standards and this proves that it is a best approach.

TASK 3

P4 Advantages and disadvantages of planning tools which are used for budgetary control

Budgetary control is a function of accounting that compares actual performance with

expected work. It helps in checking that planning is running according to managers expectations

or it needs changes to get more profit (Herbert and Seal, 2012). There are various techniques

that help in planning activities of Taj Stores. These tools are stated below:

Cash budget – This budget records all cash transaction which incur in business in current

year and recording of transactions does not get affected by actual year of transaction. This

method provides information about need of cash. This budget relates to specific time and

company prepares it on scheduled time. This method is records incoming and outgoing of cash

for business purpose. It ultimately helps in smooth functioning of corporation.

9

Advantages – This tool diminish bad debts risk and it ensures that company should pay

its due amounts in promised time and also must receive payments from organisation's debtors

and this will bring strong relationship of firm with its external stakeholder (Contrafatto and

Burns, 2013).

Disadvantages – Maintain accuracy of this budget is very difficult task for accountants

because cash is a very fluctuating element in venture. And its exact need can not be found.

Manager prepares cash budget on the basis of previous year but these are very flexible points that

ensure inaccuracy of this tool.

Master Budget – Main task of this budget is to allocate various resources to different

functional areas of business. This budget is made for obtaining organizational goal rather than

focusing on individual targets. It is a combination of all budget that a business entity generally

made.

Advantages – Optimum utilization of resources can be done with help of this budget.

Master budget can decrease cost of operations in firm and bring all levels at same place in

organisation. It removes all kind of dilemmas from mind of employees of Taj stores and guides

them a clear way which they can follow for their goal achievement.

Disadvantages – Use of this method is very expensive for any business. Taj store can not

afford to invest their fund in this which is not so important for them because they are a small

enterprise and they can deal with their conflicts on small level (Taipaleenmäki and Ikäheimo,

2013).

Capital expenditure budget – Purchase of capital assets is not an easy task because it

requires higher amount of cash and more analytical time to made these expenses in an adequate

manner. Capital expenditures use more financial resources that is not affordable for Taj Stores.

Capital expenditure includes purchase of new land and building, plant & machinery, furniture

and fixture etc. Requirement of fund for these expenditure is main area of focus of this budget.

Every organisation made this budget whether it is small or big association.

Advantages – This budget analysis major risks that are associated with investments

decisions. It helps in recognition of higher return of applied investment decisions in corporation.

Expenses can be controlled in better way that uses large amount of cash.

Disadvantages – This is made for long term purpose because capital expenditure does not

incur on regular basis. They generally have to made for more than five year of duration. This is

10

its due amounts in promised time and also must receive payments from organisation's debtors

and this will bring strong relationship of firm with its external stakeholder (Contrafatto and

Burns, 2013).

Disadvantages – Maintain accuracy of this budget is very difficult task for accountants

because cash is a very fluctuating element in venture. And its exact need can not be found.

Manager prepares cash budget on the basis of previous year but these are very flexible points that

ensure inaccuracy of this tool.

Master Budget – Main task of this budget is to allocate various resources to different

functional areas of business. This budget is made for obtaining organizational goal rather than

focusing on individual targets. It is a combination of all budget that a business entity generally

made.

Advantages – Optimum utilization of resources can be done with help of this budget.

Master budget can decrease cost of operations in firm and bring all levels at same place in

organisation. It removes all kind of dilemmas from mind of employees of Taj stores and guides

them a clear way which they can follow for their goal achievement.

Disadvantages – Use of this method is very expensive for any business. Taj store can not

afford to invest their fund in this which is not so important for them because they are a small

enterprise and they can deal with their conflicts on small level (Taipaleenmäki and Ikäheimo,

2013).

Capital expenditure budget – Purchase of capital assets is not an easy task because it

requires higher amount of cash and more analytical time to made these expenses in an adequate

manner. Capital expenditures use more financial resources that is not affordable for Taj Stores.

Capital expenditure includes purchase of new land and building, plant & machinery, furniture

and fixture etc. Requirement of fund for these expenditure is main area of focus of this budget.

Every organisation made this budget whether it is small or big association.

Advantages – This budget analysis major risks that are associated with investments

decisions. It helps in recognition of higher return of applied investment decisions in corporation.

Expenses can be controlled in better way that uses large amount of cash.

Disadvantages – This is made for long term purpose because capital expenditure does not

incur on regular basis. They generally have to made for more than five year of duration. This is

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.