Management Accounting: Types of Systems, Reporting Methods, Cost Analysis and Budgetary Control

VerifiedAdded on 2023/06/18

|15

|4928

|386

AI Summary

This report discusses the significance of management accounting in decision-making process. It explains the different types of management accounting systems such as cost-accounting system, inventory management system, job costing system and price optimization system. It also outlines the methods adopted for management accounting reporting such as budget report, accounts receivable ageing report, job cost report and inventory and manufacturing report. The report further describes the tools and techniques of cost analysis such as marginal costing and absorption costing system. Finally, it explains the planning tools of budgetary control such as cash budget.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

P1: Types of management accounting systems...........................................................................3

P2: Methods adopted for management accounting reporting.....................................................5

P3: Tools and techniques of cost analysis...................................................................................7

P4: Planning tools of budgetary control .....................................................................................9

P5: Management accounting systems to handle the financial problems...................................10

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

P1: Types of management accounting systems...........................................................................3

P2: Methods adopted for management accounting reporting.....................................................5

P3: Tools and techniques of cost analysis...................................................................................7

P4: Planning tools of budgetary control .....................................................................................9

P5: Management accounting systems to handle the financial problems...................................10

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management Accounting is defined as a procedure where all the financial information is

provided to the top management for decision-making process. In the current times, management

account is highly significant as it helps in identifying, analysing and interpreting the crucial

information to take managerial decisions. The management accounting make use of past

information and forecasts the future to make budgets or reports. The present report is based on

the case scenario of SOLLOTAK (UK) LTD. It deals in designing and manufacturing of

products such as switches, stabilizers, etc. The report will explain the different requirements of

management accounting and the method used for its reporting. Further it will outline the

different techniques and tools of cost analysis and shows which costing system is best for the

company. It will also describe the tools used for budgetary control with the major benefits and

drawbacks. Finally, it will explain that how management accounting system can be used to

handle financial problems.

P1: Types of management accounting systems

Management accounting is defined as a process to identify, analyse and communicate all

the information (financial) to the management to achieve the company's vision and mission.

Types of Management Accounting Systems:

Cost-Accounting System

It is an accounting system which is generally used by producers or manufacturers to

maintain all the production related activities using a particular system. Generally, this system

works by following the raw materials as and when they go to production process and turns into

finished products (Dierkes and Siepelmeyer, 2019). Sollotak Ltd. can also adopt cost-accounting

system to keep up with the production activities and to trace and track the cost of raw materials

and finished products. The system will write down the use of raw materials.

Advantages:

The system fixes standard for everything thereby reducing wastage and losses. It helps in cost reduction because new and better production methods are followed.

Disadvantages:

Management Accounting is defined as a procedure where all the financial information is

provided to the top management for decision-making process. In the current times, management

account is highly significant as it helps in identifying, analysing and interpreting the crucial

information to take managerial decisions. The management accounting make use of past

information and forecasts the future to make budgets or reports. The present report is based on

the case scenario of SOLLOTAK (UK) LTD. It deals in designing and manufacturing of

products such as switches, stabilizers, etc. The report will explain the different requirements of

management accounting and the method used for its reporting. Further it will outline the

different techniques and tools of cost analysis and shows which costing system is best for the

company. It will also describe the tools used for budgetary control with the major benefits and

drawbacks. Finally, it will explain that how management accounting system can be used to

handle financial problems.

P1: Types of management accounting systems

Management accounting is defined as a process to identify, analyse and communicate all

the information (financial) to the management to achieve the company's vision and mission.

Types of Management Accounting Systems:

Cost-Accounting System

It is an accounting system which is generally used by producers or manufacturers to

maintain all the production related activities using a particular system. Generally, this system

works by following the raw materials as and when they go to production process and turns into

finished products (Dierkes and Siepelmeyer, 2019). Sollotak Ltd. can also adopt cost-accounting

system to keep up with the production activities and to trace and track the cost of raw materials

and finished products. The system will write down the use of raw materials.

Advantages:

The system fixes standard for everything thereby reducing wastage and losses. It helps in cost reduction because new and better production methods are followed.

Disadvantages:

Future decisions are taken on the basis of past information.

The cost is calculated on the grounds of full capacity utilization. In case of under-

utilization, the results shown may not be effective.

Inventory Management System:

It can be defined as a system where the businesses record the amount of goods they have

in their warehouses, at their display units or with other distributors. This will help you to

maintain right no. of goods at the right place (Muchaendepi. And et.al., 2019). By adopting the

Inventory management system, Sollotak Ltd. can track down its inventory level. It will assist to

keep the correct no. of goods at correct place and in appropriate quantity.

Advantages:

In the absence of inventory report, the business will not have proper record of sales and

inventory and can mislead the employees. By maintaining the report, the business can pick out the slow moving goods and can take

necessary actions to clear them.

Disadvantages:

This system software is very costly in the market. It is not affordable by small sized

business.

Special training is required to successfully operate this system which is sometimes quite

lengthy and complicated.

Job Costing System:

This type of costing is described as a unique accounting method which is used to record

the expenditure incurred to produce a product. It is the process of collecting and calculating the

cost of materials, overheads and expenses for a particular product (ElMaraghy, and Alami.

2020). Sollotak Ltd., a manufacturing company can easily assign cost to different production

activities and how much expense is incurred for one job.

Advantages:

The system gives freedom of cost controlling because the cost is calculated at every stage

of production process. It is easy to compare the cost of present job with that of the previous job.

The cost is calculated on the grounds of full capacity utilization. In case of under-

utilization, the results shown may not be effective.

Inventory Management System:

It can be defined as a system where the businesses record the amount of goods they have

in their warehouses, at their display units or with other distributors. This will help you to

maintain right no. of goods at the right place (Muchaendepi. And et.al., 2019). By adopting the

Inventory management system, Sollotak Ltd. can track down its inventory level. It will assist to

keep the correct no. of goods at correct place and in appropriate quantity.

Advantages:

In the absence of inventory report, the business will not have proper record of sales and

inventory and can mislead the employees. By maintaining the report, the business can pick out the slow moving goods and can take

necessary actions to clear them.

Disadvantages:

This system software is very costly in the market. It is not affordable by small sized

business.

Special training is required to successfully operate this system which is sometimes quite

lengthy and complicated.

Job Costing System:

This type of costing is described as a unique accounting method which is used to record

the expenditure incurred to produce a product. It is the process of collecting and calculating the

cost of materials, overheads and expenses for a particular product (ElMaraghy, and Alami.

2020). Sollotak Ltd., a manufacturing company can easily assign cost to different production

activities and how much expense is incurred for one job.

Advantages:

The system gives freedom of cost controlling because the cost is calculated at every stage

of production process. It is easy to compare the cost of present job with that of the previous job.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Disadvantages:

Controlling measures are taken only after the costs are incurred. Therefore, no possibility

of cost control. At times of inflation, comparing the cost of a job is pointless.

Price Optimization System:

A system where price is derived from the market database that will give maximum profits

to the company and can optimally meet the company's goals and objectives is known as Price

optimization System (Gupta, and et.al., 2020). Different types of survey data are used such as

consumer surveys, demographic surveys, etc., Sollotak Ltd. with so many product line can make

an effective use of price optimization system by effectively pricing the products.

Advantages:

This system helps to get rid of any manual work and reduces the chances of mistakes. The system studies the consumer's buying pattern and help companies in quoting the

prices in a better way.

Disadvantages:

Consumer database does not always produce correct results. Sometimes, they can be

biased and manipulated.

Setting a price in dynamic environment which is constantly changing is a difficult task in

this system.

P2: Methods adopted for management accounting reporting

Reports are very significant for the companies to smoothly handle the daily operations. There are

various methods adopted for reporting the management accounting which are as follows:

Budget report: A company has a report that compares the accomplished results to the

intended budget. The budget report examines what all expenses are incurred on a high level so

that necessary steps can be taken (Church, Kuang, and Liu, 2019). Such tool is often used to

keep a control over the results. Budget report, to a certain extent, can protect the company

against any threats in the future. Budget reports help Sollotak Ltd. in projecting sales or

production levels for the upcoming year. In case of achieving the sales target of £100000 for the

next month, Sollotak Ltd. can either increase their production or can reduce their selling price in

order to attract new customers.

Controlling measures are taken only after the costs are incurred. Therefore, no possibility

of cost control. At times of inflation, comparing the cost of a job is pointless.

Price Optimization System:

A system where price is derived from the market database that will give maximum profits

to the company and can optimally meet the company's goals and objectives is known as Price

optimization System (Gupta, and et.al., 2020). Different types of survey data are used such as

consumer surveys, demographic surveys, etc., Sollotak Ltd. with so many product line can make

an effective use of price optimization system by effectively pricing the products.

Advantages:

This system helps to get rid of any manual work and reduces the chances of mistakes. The system studies the consumer's buying pattern and help companies in quoting the

prices in a better way.

Disadvantages:

Consumer database does not always produce correct results. Sometimes, they can be

biased and manipulated.

Setting a price in dynamic environment which is constantly changing is a difficult task in

this system.

P2: Methods adopted for management accounting reporting

Reports are very significant for the companies to smoothly handle the daily operations. There are

various methods adopted for reporting the management accounting which are as follows:

Budget report: A company has a report that compares the accomplished results to the

intended budget. The budget report examines what all expenses are incurred on a high level so

that necessary steps can be taken (Church, Kuang, and Liu, 2019). Such tool is often used to

keep a control over the results. Budget report, to a certain extent, can protect the company

against any threats in the future. Budget reports help Sollotak Ltd. in projecting sales or

production levels for the upcoming year. In case of achieving the sales target of £100000 for the

next month, Sollotak Ltd. can either increase their production or can reduce their selling price in

order to attract new customers.

Advantages:

All the activities of different departments can be easily co-ordinated with help of

budgeting. The report consist of all the action to be executed. Therefore, through reports, objectives

are translated into actions.

Disadvantages:

If employees are not able to perform up to the standards, such budgets can demotivate the

employees.

The company has to perform within the standards which makes it impossible for the

employees to come up with innovative ideas.

Accounts Receivable Ageing Report: In management accounting, this type of report is

defined as classifying the receivables according to the date on which they become due so that a

calculation can be made about the losses (bad debts) incurred by the company. Receivables

emerge when the company makes the credit sale (Suwantari, Ariana, and Suprapto, 2020). If the

customer is making late payments on a regular basis, its credit worthiness can be assessed from

this report and necessary actions can be taken. Such report helps the business to collect their

balance outstanding on time without any delay. With the help of such report, Sollotak Ltd. can

check whether their debtors are making the payments on time or how much extra time they are

taking to settle the accounts.

Advantages:

Calculating working capital becomes easy as the company has knowledge that when a

customer will make the payment. Maintenance of such reports can relieve the company from debt collection and can focus

on other important areas.

Disadvantages:

Drafting of such a report proves to be costly in case of companies having less finance. Report making is also a complicated work because all the minute details about the debtor

has to be recorded.

Job Cost Report: Here, cost of materials, labour and overhead of a particular job are

gathered. It is a report that records the cost of a project which is in process. In job costing report,

All the activities of different departments can be easily co-ordinated with help of

budgeting. The report consist of all the action to be executed. Therefore, through reports, objectives

are translated into actions.

Disadvantages:

If employees are not able to perform up to the standards, such budgets can demotivate the

employees.

The company has to perform within the standards which makes it impossible for the

employees to come up with innovative ideas.

Accounts Receivable Ageing Report: In management accounting, this type of report is

defined as classifying the receivables according to the date on which they become due so that a

calculation can be made about the losses (bad debts) incurred by the company. Receivables

emerge when the company makes the credit sale (Suwantari, Ariana, and Suprapto, 2020). If the

customer is making late payments on a regular basis, its credit worthiness can be assessed from

this report and necessary actions can be taken. Such report helps the business to collect their

balance outstanding on time without any delay. With the help of such report, Sollotak Ltd. can

check whether their debtors are making the payments on time or how much extra time they are

taking to settle the accounts.

Advantages:

Calculating working capital becomes easy as the company has knowledge that when a

customer will make the payment. Maintenance of such reports can relieve the company from debt collection and can focus

on other important areas.

Disadvantages:

Drafting of such a report proves to be costly in case of companies having less finance. Report making is also a complicated work because all the minute details about the debtor

has to be recorded.

Job Cost Report: Here, cost of materials, labour and overhead of a particular job are

gathered. It is a report that records the cost of a project which is in process. In job costing report,

constructing the correct cost estimates is crucial (Drobyazko, and et.al., 2019). The reason being

if cost estimation is not done appropriately, then the rest of the work will be affected badly.

Sollotak Ltd. With the help of proper cost estimation, can continuously monitor and report the

work so that corrective measure can be taken in case of any deviations.

Advantages:

Efficiency of each job is carefully studied so that a job which is less efficient can be

addressed within the proper time frame. Each job's profitability can be easily measured which supports the company to continue

with a particular job or not.

Disadvantages:

Unwanted and undesirable cost can arise at any time which cannot be eliminated

completely. Such costs will increase the cost of a job.

The employee has to record all the raw material and labour used for a particular job

which is sometimes tedious.

Inventory and Manufacturing Report: Inventory management is very important because it

directly affects the cash flow of the company. Inventory reports maintains accurate information

with all the details about inventory (Muchaendepi, and et.al., 2019). This reports helps the

companies to smoothly perform its operations without any disturbance because the company can

track the inventory. In case of excess inventory, Sollotak Ltd. can clear the stock and in case of

shortage, company can make necessary arrangements to refill the stock. The inventory report is

an all-inclusive report as it precisely includes all the information about a particular transaction.

Advantages:

Inventory reports helps in saving a lot of time as it is can be easily traced which all goods

are in the warehouse and which needs to be produced or procured. It helps to retain the customers by easily fulfilling the demands of customers on time.

Disadvantages:

Inventory report are complex and complicated that they are not easily understandable by

the employees.

In the dynamic and complex business environment, such reports can only reduce the risk

up to a limited extent.

if cost estimation is not done appropriately, then the rest of the work will be affected badly.

Sollotak Ltd. With the help of proper cost estimation, can continuously monitor and report the

work so that corrective measure can be taken in case of any deviations.

Advantages:

Efficiency of each job is carefully studied so that a job which is less efficient can be

addressed within the proper time frame. Each job's profitability can be easily measured which supports the company to continue

with a particular job or not.

Disadvantages:

Unwanted and undesirable cost can arise at any time which cannot be eliminated

completely. Such costs will increase the cost of a job.

The employee has to record all the raw material and labour used for a particular job

which is sometimes tedious.

Inventory and Manufacturing Report: Inventory management is very important because it

directly affects the cash flow of the company. Inventory reports maintains accurate information

with all the details about inventory (Muchaendepi, and et.al., 2019). This reports helps the

companies to smoothly perform its operations without any disturbance because the company can

track the inventory. In case of excess inventory, Sollotak Ltd. can clear the stock and in case of

shortage, company can make necessary arrangements to refill the stock. The inventory report is

an all-inclusive report as it precisely includes all the information about a particular transaction.

Advantages:

Inventory reports helps in saving a lot of time as it is can be easily traced which all goods

are in the warehouse and which needs to be produced or procured. It helps to retain the customers by easily fulfilling the demands of customers on time.

Disadvantages:

Inventory report are complex and complicated that they are not easily understandable by

the employees.

In the dynamic and complex business environment, such reports can only reduce the risk

up to a limited extent.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

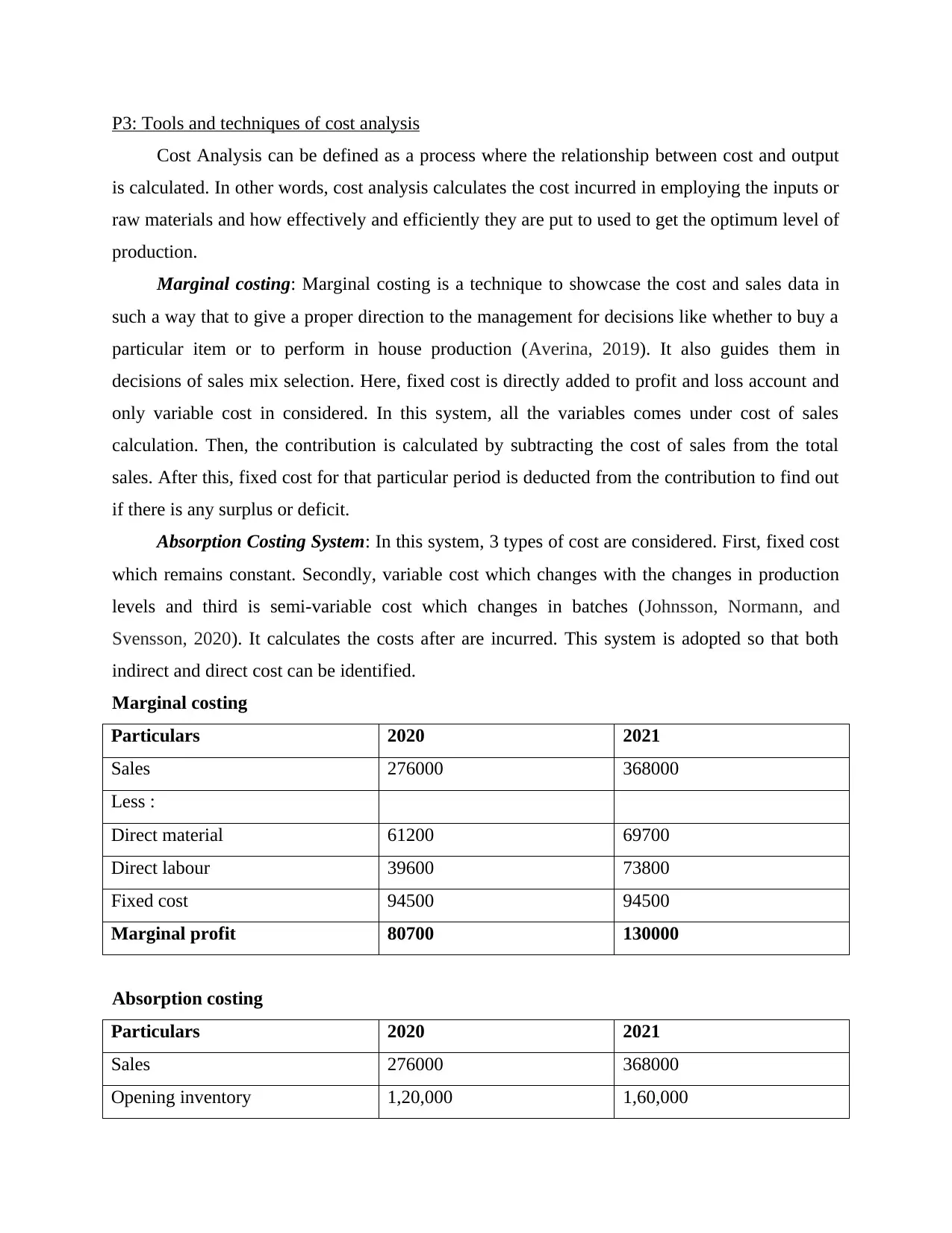

P3: Tools and techniques of cost analysis

Cost Analysis can be defined as a process where the relationship between cost and output

is calculated. In other words, cost analysis calculates the cost incurred in employing the inputs or

raw materials and how effectively and efficiently they are put to used to get the optimum level of

production.

Marginal costing: Marginal costing is a technique to showcase the cost and sales data in

such a way that to give a proper direction to the management for decisions like whether to buy a

particular item or to perform in house production (Averina, 2019). It also guides them in

decisions of sales mix selection. Here, fixed cost is directly added to profit and loss account and

only variable cost in considered. In this system, all the variables comes under cost of sales

calculation. Then, the contribution is calculated by subtracting the cost of sales from the total

sales. After this, fixed cost for that particular period is deducted from the contribution to find out

if there is any surplus or deficit.

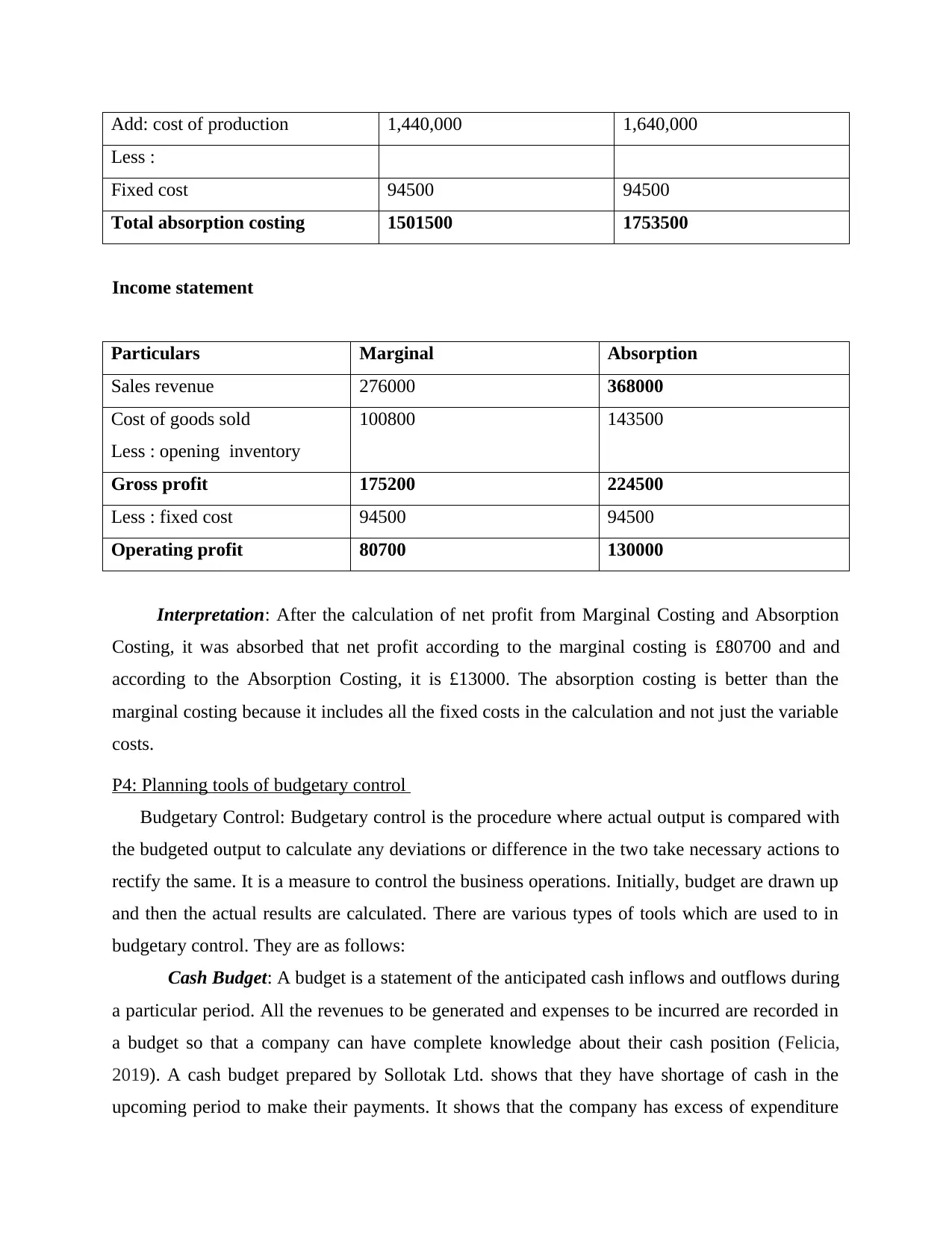

Absorption Costing System: In this system, 3 types of cost are considered. First, fixed cost

which remains constant. Secondly, variable cost which changes with the changes in production

levels and third is semi-variable cost which changes in batches (Johnsson, Normann, and

Svensson, 2020). It calculates the costs after are incurred. This system is adopted so that both

indirect and direct cost can be identified.

Marginal costing

Particulars 2020 2021

Sales 276000 368000

Less :

Direct material 61200 69700

Direct labour 39600 73800

Fixed cost 94500 94500

Marginal profit 80700 130000

Absorption costing

Particulars 2020 2021

Sales 276000 368000

Opening inventory 1,20,000 1,60,000

Cost Analysis can be defined as a process where the relationship between cost and output

is calculated. In other words, cost analysis calculates the cost incurred in employing the inputs or

raw materials and how effectively and efficiently they are put to used to get the optimum level of

production.

Marginal costing: Marginal costing is a technique to showcase the cost and sales data in

such a way that to give a proper direction to the management for decisions like whether to buy a

particular item or to perform in house production (Averina, 2019). It also guides them in

decisions of sales mix selection. Here, fixed cost is directly added to profit and loss account and

only variable cost in considered. In this system, all the variables comes under cost of sales

calculation. Then, the contribution is calculated by subtracting the cost of sales from the total

sales. After this, fixed cost for that particular period is deducted from the contribution to find out

if there is any surplus or deficit.

Absorption Costing System: In this system, 3 types of cost are considered. First, fixed cost

which remains constant. Secondly, variable cost which changes with the changes in production

levels and third is semi-variable cost which changes in batches (Johnsson, Normann, and

Svensson, 2020). It calculates the costs after are incurred. This system is adopted so that both

indirect and direct cost can be identified.

Marginal costing

Particulars 2020 2021

Sales 276000 368000

Less :

Direct material 61200 69700

Direct labour 39600 73800

Fixed cost 94500 94500

Marginal profit 80700 130000

Absorption costing

Particulars 2020 2021

Sales 276000 368000

Opening inventory 1,20,000 1,60,000

Add: cost of production 1,440,000 1,640,000

Less :

Fixed cost 94500 94500

Total absorption costing 1501500 1753500

Income statement

Particulars Marginal Absorption

Sales revenue 276000 368000

Cost of goods sold

Less : opening inventory

100800 143500

Gross profit 175200 224500

Less : fixed cost 94500 94500

Operating profit 80700 130000

Interpretation: After the calculation of net profit from Marginal Costing and Absorption

Costing, it was absorbed that net profit according to the marginal costing is £80700 and and

according to the Absorption Costing, it is £13000. The absorption costing is better than the

marginal costing because it includes all the fixed costs in the calculation and not just the variable

costs.

P4: Planning tools of budgetary control

Budgetary Control: Budgetary control is the procedure where actual output is compared with

the budgeted output to calculate any deviations or difference in the two take necessary actions to

rectify the same. It is a measure to control the business operations. Initially, budget are drawn up

and then the actual results are calculated. There are various types of tools which are used to in

budgetary control. They are as follows:

Cash Budget: A budget is a statement of the anticipated cash inflows and outflows during

a particular period. All the revenues to be generated and expenses to be incurred are recorded in

a budget so that a company can have complete knowledge about their cash position (Felicia,

2019). A cash budget prepared by Sollotak Ltd. shows that they have shortage of cash in the

upcoming period to make their payments. It shows that the company has excess of expenditure

Less :

Fixed cost 94500 94500

Total absorption costing 1501500 1753500

Income statement

Particulars Marginal Absorption

Sales revenue 276000 368000

Cost of goods sold

Less : opening inventory

100800 143500

Gross profit 175200 224500

Less : fixed cost 94500 94500

Operating profit 80700 130000

Interpretation: After the calculation of net profit from Marginal Costing and Absorption

Costing, it was absorbed that net profit according to the marginal costing is £80700 and and

according to the Absorption Costing, it is £13000. The absorption costing is better than the

marginal costing because it includes all the fixed costs in the calculation and not just the variable

costs.

P4: Planning tools of budgetary control

Budgetary Control: Budgetary control is the procedure where actual output is compared with

the budgeted output to calculate any deviations or difference in the two take necessary actions to

rectify the same. It is a measure to control the business operations. Initially, budget are drawn up

and then the actual results are calculated. There are various types of tools which are used to in

budgetary control. They are as follows:

Cash Budget: A budget is a statement of the anticipated cash inflows and outflows during

a particular period. All the revenues to be generated and expenses to be incurred are recorded in

a budget so that a company can have complete knowledge about their cash position (Felicia,

2019). A cash budget prepared by Sollotak Ltd. shows that they have shortage of cash in the

upcoming period to make their payments. It shows that the company has excess of expenditure

over revenues. In such a case they can request for a short term loan from a bank to ensure cash

availability at that time. Preparation of cash budget helps the Sollotak Ltd. to generate the cash

flows without any interruptions. The major advantages of cash budget is that the company never

runs out of the cash and can make the arrangements well before time. But at the same time, the

cash budget is just an estimation based on the past results which cannot be always accurate.

Zero-Based Budgeting: It is a procedure where a budget or statement is made from the

start. The previous budgets are not considered in zero based budgeting. Here, each and every

expense requires a justification before including it in the final budget. If a particular expense

does not entertain the company, it can be excluded. Sollotak Ltd. can make use of ZBB to make

a decision of buy or make (Beredugo, 2019). Zero based budgeting is very beneficial because all

the items and expenses are justified and more profitable items can be included in the budget. It

also helps in cost reduction. Conversely, zero based budgets are complicated and time-

consuming because it has to be created every time a new item is added.

Activity Based Budgeting: ABB is a budgeting tool which recognizes and analyses the

activities and direct cost associated with it. Once the activities are identified, then the cost

associated with each activity is calculated. Sollotak Ltd. can also adopt this budgeting by

identifying the crucial activities and allocating cost to that activity. The key benefits are that

there is no wastage of resources. Each activity is carefully studied before applying cost to it.

Secondly, incompetent activities can be ignored and which improves the operational efficiency

of the business. However, it requires a thorough understanding of the activities which is,

sometimes, lacked by the employees. ABB is a costly and complicated tool to be adopted.

P5: Management accounting systems to handle the financial problems

Running the company smoothly is not an easy job. It comes with all difficulties and

challenges at every step. Financial stability must be maintained in the company otherwise it can

incur huge losses. There can be problems of insufficient capital or wasting the money on too

much promotion or any other unnecessary expenses. The company now-a-days are adopting the

management accounting systems to solve such financial problems which are as follows:

Benchmarking: Benchmarking is a procedure where standards are set and the company's

performance is reviewed against the other group of organization with similar business operations

(Anthopoulos, Janssen and Weerakkody, 2019). Benchmarking can also be done with the

company by comparing the present performance with the past performance of the company. For

availability at that time. Preparation of cash budget helps the Sollotak Ltd. to generate the cash

flows without any interruptions. The major advantages of cash budget is that the company never

runs out of the cash and can make the arrangements well before time. But at the same time, the

cash budget is just an estimation based on the past results which cannot be always accurate.

Zero-Based Budgeting: It is a procedure where a budget or statement is made from the

start. The previous budgets are not considered in zero based budgeting. Here, each and every

expense requires a justification before including it in the final budget. If a particular expense

does not entertain the company, it can be excluded. Sollotak Ltd. can make use of ZBB to make

a decision of buy or make (Beredugo, 2019). Zero based budgeting is very beneficial because all

the items and expenses are justified and more profitable items can be included in the budget. It

also helps in cost reduction. Conversely, zero based budgets are complicated and time-

consuming because it has to be created every time a new item is added.

Activity Based Budgeting: ABB is a budgeting tool which recognizes and analyses the

activities and direct cost associated with it. Once the activities are identified, then the cost

associated with each activity is calculated. Sollotak Ltd. can also adopt this budgeting by

identifying the crucial activities and allocating cost to that activity. The key benefits are that

there is no wastage of resources. Each activity is carefully studied before applying cost to it.

Secondly, incompetent activities can be ignored and which improves the operational efficiency

of the business. However, it requires a thorough understanding of the activities which is,

sometimes, lacked by the employees. ABB is a costly and complicated tool to be adopted.

P5: Management accounting systems to handle the financial problems

Running the company smoothly is not an easy job. It comes with all difficulties and

challenges at every step. Financial stability must be maintained in the company otherwise it can

incur huge losses. There can be problems of insufficient capital or wasting the money on too

much promotion or any other unnecessary expenses. The company now-a-days are adopting the

management accounting systems to solve such financial problems which are as follows:

Benchmarking: Benchmarking is a procedure where standards are set and the company's

performance is reviewed against the other group of organization with similar business operations

(Anthopoulos, Janssen and Weerakkody, 2019). Benchmarking can also be done with the

company by comparing the present performance with the past performance of the company. For

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

example, the business can take past years’ average sales and can set it as a benchmark to evaluate

how efficiently they are generating their sales for this year. Sollotak Ltd. can make a good use of

benchmarking technique to analyse and improve its performance. Sollotak Ltd. can set their

competitors as a benchmark and can set targets accordingly.

Advantages Disadvantages

a) The company can keep a close check that

where they are lacking and can improve their

performance.

b) By setting the benchmarks, the company can

see where they are standing in the market and

can deliver better results and enhance their

position in the market.

a) Sometimes the company gathers wrong or

insufficient information and set standards

accordingly. It results in heavy losses to the

company.

b) It is not always true that benchmarking helps

in enhancing the business performance and

position as it helped the other companies to be

in top positions.

Key Performance Indicators: KPIs are the standards or the barometer that give useful

information about the financial position of the company. KPIs are generally the relationship or

ratio between any two components such as current asset to current liability ratio or the

profitability ratios (Haber and Schryver, 2019). The Sollotak Ltd. can check its solvency by

computing the current ratio. The company can easily check how efficiently they can pay their

obligations and can maintain credibility in the market. Suppose the company is having current

assets of $90000 and its total current liabilities of $30000 then, its current ratio will be 3:1. But

the ideal current ratio should be 2:1. The can set KPI of 2:1. It means the company has enough

liquidity to pay their dues on time. But even after clearing all their dues, there are still funds

which are kept idle by the company. Such funds can be invested by Sollotak Ltd. in more

productive uses. The company can make use of Key Performance Indicators to track their

performance and growth and cut down their costs.

Advantages Disadvantages

a) KPIs provide results with perfect accuracy

which are measurable and can be tracked to

a) Employees are focused to complete the task

without focusing on the quality. KPIs may

how efficiently they are generating their sales for this year. Sollotak Ltd. can make a good use of

benchmarking technique to analyse and improve its performance. Sollotak Ltd. can set their

competitors as a benchmark and can set targets accordingly.

Advantages Disadvantages

a) The company can keep a close check that

where they are lacking and can improve their

performance.

b) By setting the benchmarks, the company can

see where they are standing in the market and

can deliver better results and enhance their

position in the market.

a) Sometimes the company gathers wrong or

insufficient information and set standards

accordingly. It results in heavy losses to the

company.

b) It is not always true that benchmarking helps

in enhancing the business performance and

position as it helped the other companies to be

in top positions.

Key Performance Indicators: KPIs are the standards or the barometer that give useful

information about the financial position of the company. KPIs are generally the relationship or

ratio between any two components such as current asset to current liability ratio or the

profitability ratios (Haber and Schryver, 2019). The Sollotak Ltd. can check its solvency by

computing the current ratio. The company can easily check how efficiently they can pay their

obligations and can maintain credibility in the market. Suppose the company is having current

assets of $90000 and its total current liabilities of $30000 then, its current ratio will be 3:1. But

the ideal current ratio should be 2:1. The can set KPI of 2:1. It means the company has enough

liquidity to pay their dues on time. But even after clearing all their dues, there are still funds

which are kept idle by the company. Such funds can be invested by Sollotak Ltd. in more

productive uses. The company can make use of Key Performance Indicators to track their

performance and growth and cut down their costs.

Advantages Disadvantages

a) KPIs provide results with perfect accuracy

which are measurable and can be tracked to

a) Employees are focused to complete the task

without focusing on the quality. KPIs may

achieve the goal.

b) Each employee knows well in advance

about the goals to be achieved. So, they move

in same direction without any chaos.

prove to be effective to achieve the short term

goals and does not prove to be beneficial in the

long term.

b) The information provided by the KPI is not

proficient enough to be executed.

Variance Analysis: Variance Analysis is a control measure to determine the difference

between standard budgets and the actual results. A trend line can be constructed to view any

variance from the set standards and necessary actions can be taken to get back on the track.

Suppose the Sollotak Ltd. has drafted a budget for sales to be £150000 but the actual sales

counted to £110000 only. A variance analysis gives a deviation of $40000. After proper

scrutinization, it was found that there are close substitutes of the company's product. The

company has to take necessary actions like increasing the promotional activity or to have some

innovation in the products to induce the sale.

Advantages Disadvantages

a) Necessary actions can be taken immediately

after finding any deviations so that the

company's operations ran smoothly.

b) A particular department or an employee can

be responsible for particular deviation instead

of fixing it to the entire organization.

a) With technological advancements and

changes in the methods of production on a

frequent basis, a new budget is to be made

every time which requires a lot of time and

energy.

b) the company can sometime manipulate the

data to get favourable results or to avoid the

negative deviations.

Balance Scorecard: Balance scorecard is a strategical tool which connects the all the

objectives, goals, and targets to the main vision of the organization. All the financial and non-

financial objectives are recognized and the priorities are given to each objective. The BSC allows

the senior management to consider four perspectives of the company. First is, the customer's

b) Each employee knows well in advance

about the goals to be achieved. So, they move

in same direction without any chaos.

prove to be effective to achieve the short term

goals and does not prove to be beneficial in the

long term.

b) The information provided by the KPI is not

proficient enough to be executed.

Variance Analysis: Variance Analysis is a control measure to determine the difference

between standard budgets and the actual results. A trend line can be constructed to view any

variance from the set standards and necessary actions can be taken to get back on the track.

Suppose the Sollotak Ltd. has drafted a budget for sales to be £150000 but the actual sales

counted to £110000 only. A variance analysis gives a deviation of $40000. After proper

scrutinization, it was found that there are close substitutes of the company's product. The

company has to take necessary actions like increasing the promotional activity or to have some

innovation in the products to induce the sale.

Advantages Disadvantages

a) Necessary actions can be taken immediately

after finding any deviations so that the

company's operations ran smoothly.

b) A particular department or an employee can

be responsible for particular deviation instead

of fixing it to the entire organization.

a) With technological advancements and

changes in the methods of production on a

frequent basis, a new budget is to be made

every time which requires a lot of time and

energy.

b) the company can sometime manipulate the

data to get favourable results or to avoid the

negative deviations.

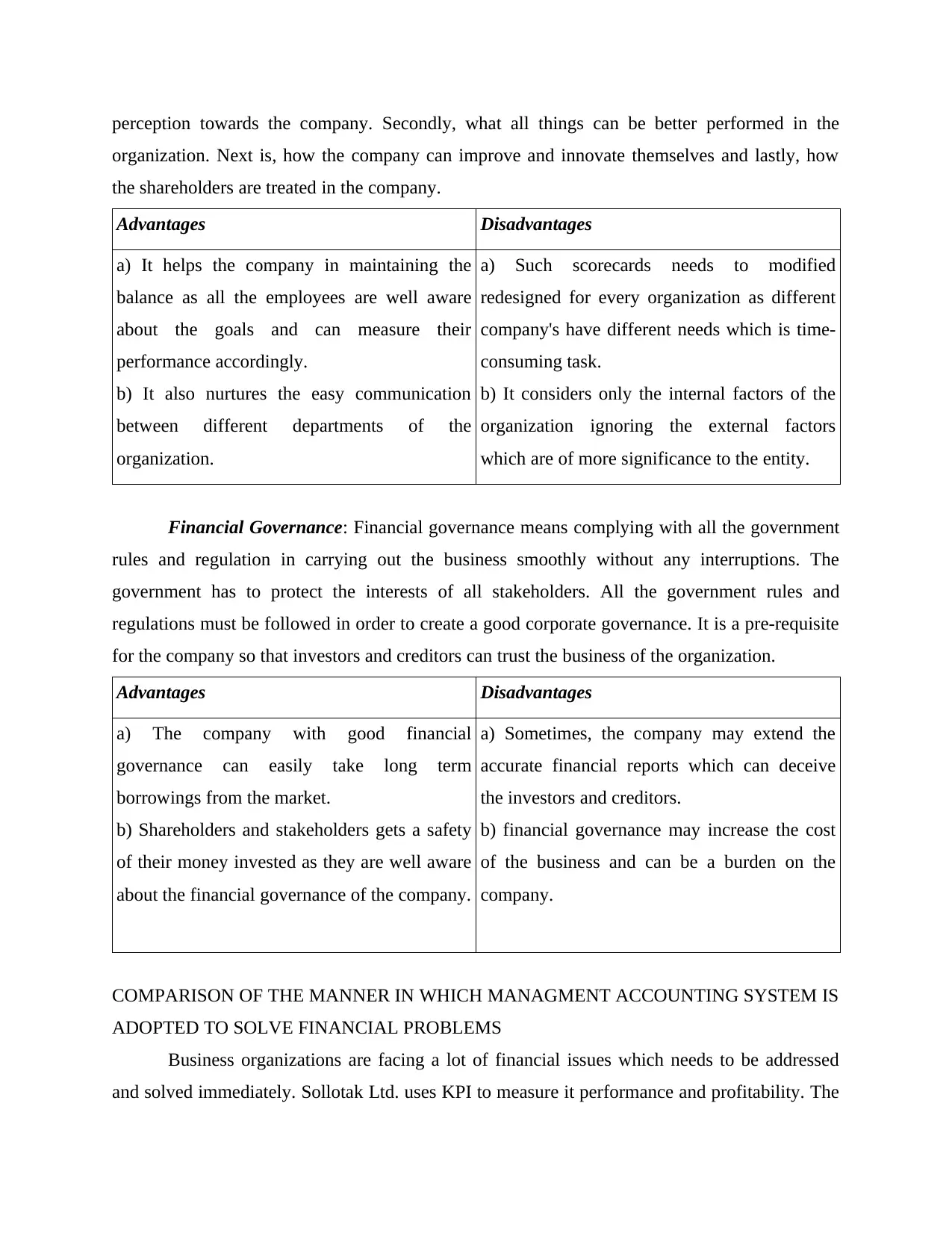

Balance Scorecard: Balance scorecard is a strategical tool which connects the all the

objectives, goals, and targets to the main vision of the organization. All the financial and non-

financial objectives are recognized and the priorities are given to each objective. The BSC allows

the senior management to consider four perspectives of the company. First is, the customer's

perception towards the company. Secondly, what all things can be better performed in the

organization. Next is, how the company can improve and innovate themselves and lastly, how

the shareholders are treated in the company.

Advantages Disadvantages

a) It helps the company in maintaining the

balance as all the employees are well aware

about the goals and can measure their

performance accordingly.

b) It also nurtures the easy communication

between different departments of the

organization.

a) Such scorecards needs to modified

redesigned for every organization as different

company's have different needs which is time-

consuming task.

b) It considers only the internal factors of the

organization ignoring the external factors

which are of more significance to the entity.

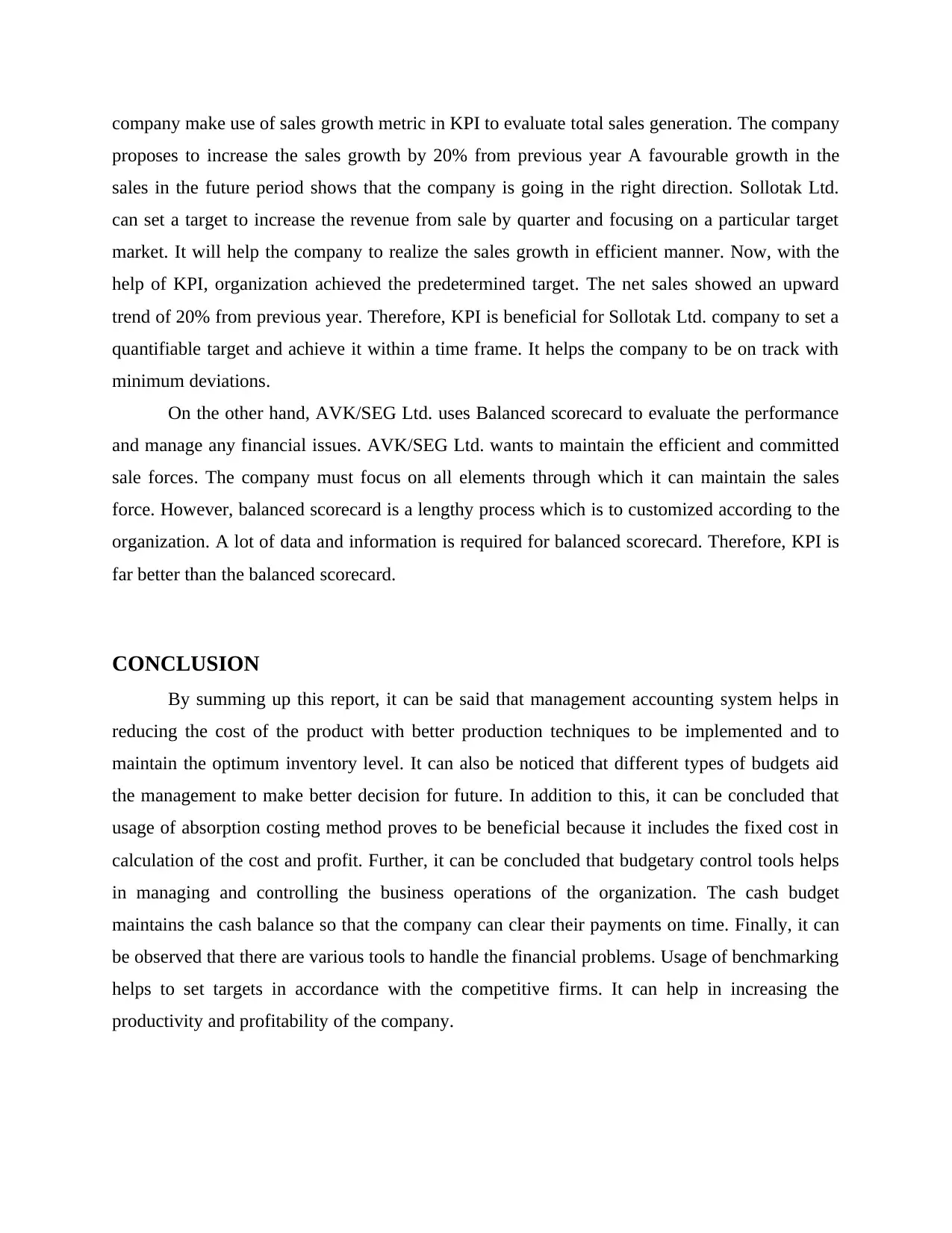

Financial Governance: Financial governance means complying with all the government

rules and regulation in carrying out the business smoothly without any interruptions. The

government has to protect the interests of all stakeholders. All the government rules and

regulations must be followed in order to create a good corporate governance. It is a pre-requisite

for the company so that investors and creditors can trust the business of the organization.

Advantages Disadvantages

a) The company with good financial

governance can easily take long term

borrowings from the market.

b) Shareholders and stakeholders gets a safety

of their money invested as they are well aware

about the financial governance of the company.

a) Sometimes, the company may extend the

accurate financial reports which can deceive

the investors and creditors.

b) financial governance may increase the cost

of the business and can be a burden on the

company.

COMPARISON OF THE MANNER IN WHICH MANAGMENT ACCOUNTING SYSTEM IS

ADOPTED TO SOLVE FINANCIAL PROBLEMS

Business organizations are facing a lot of financial issues which needs to be addressed

and solved immediately. Sollotak Ltd. uses KPI to measure it performance and profitability. The

organization. Next is, how the company can improve and innovate themselves and lastly, how

the shareholders are treated in the company.

Advantages Disadvantages

a) It helps the company in maintaining the

balance as all the employees are well aware

about the goals and can measure their

performance accordingly.

b) It also nurtures the easy communication

between different departments of the

organization.

a) Such scorecards needs to modified

redesigned for every organization as different

company's have different needs which is time-

consuming task.

b) It considers only the internal factors of the

organization ignoring the external factors

which are of more significance to the entity.

Financial Governance: Financial governance means complying with all the government

rules and regulation in carrying out the business smoothly without any interruptions. The

government has to protect the interests of all stakeholders. All the government rules and

regulations must be followed in order to create a good corporate governance. It is a pre-requisite

for the company so that investors and creditors can trust the business of the organization.

Advantages Disadvantages

a) The company with good financial

governance can easily take long term

borrowings from the market.

b) Shareholders and stakeholders gets a safety

of their money invested as they are well aware

about the financial governance of the company.

a) Sometimes, the company may extend the

accurate financial reports which can deceive

the investors and creditors.

b) financial governance may increase the cost

of the business and can be a burden on the

company.

COMPARISON OF THE MANNER IN WHICH MANAGMENT ACCOUNTING SYSTEM IS

ADOPTED TO SOLVE FINANCIAL PROBLEMS

Business organizations are facing a lot of financial issues which needs to be addressed

and solved immediately. Sollotak Ltd. uses KPI to measure it performance and profitability. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company make use of sales growth metric in KPI to evaluate total sales generation. The company

proposes to increase the sales growth by 20% from previous year A favourable growth in the

sales in the future period shows that the company is going in the right direction. Sollotak Ltd.

can set a target to increase the revenue from sale by quarter and focusing on a particular target

market. It will help the company to realize the sales growth in efficient manner. Now, with the

help of KPI, organization achieved the predetermined target. The net sales showed an upward

trend of 20% from previous year. Therefore, KPI is beneficial for Sollotak Ltd. company to set a

quantifiable target and achieve it within a time frame. It helps the company to be on track with

minimum deviations.

On the other hand, AVK/SEG Ltd. uses Balanced scorecard to evaluate the performance

and manage any financial issues. AVK/SEG Ltd. wants to maintain the efficient and committed

sale forces. The company must focus on all elements through which it can maintain the sales

force. However, balanced scorecard is a lengthy process which is to customized according to the

organization. A lot of data and information is required for balanced scorecard. Therefore, KPI is

far better than the balanced scorecard.

CONCLUSION

By summing up this report, it can be said that management accounting system helps in

reducing the cost of the product with better production techniques to be implemented and to

maintain the optimum inventory level. It can also be noticed that different types of budgets aid

the management to make better decision for future. In addition to this, it can be concluded that

usage of absorption costing method proves to be beneficial because it includes the fixed cost in

calculation of the cost and profit. Further, it can be concluded that budgetary control tools helps

in managing and controlling the business operations of the organization. The cash budget

maintains the cash balance so that the company can clear their payments on time. Finally, it can

be observed that there are various tools to handle the financial problems. Usage of benchmarking

helps to set targets in accordance with the competitive firms. It can help in increasing the

productivity and profitability of the company.

proposes to increase the sales growth by 20% from previous year A favourable growth in the

sales in the future period shows that the company is going in the right direction. Sollotak Ltd.

can set a target to increase the revenue from sale by quarter and focusing on a particular target

market. It will help the company to realize the sales growth in efficient manner. Now, with the

help of KPI, organization achieved the predetermined target. The net sales showed an upward

trend of 20% from previous year. Therefore, KPI is beneficial for Sollotak Ltd. company to set a

quantifiable target and achieve it within a time frame. It helps the company to be on track with

minimum deviations.

On the other hand, AVK/SEG Ltd. uses Balanced scorecard to evaluate the performance

and manage any financial issues. AVK/SEG Ltd. wants to maintain the efficient and committed

sale forces. The company must focus on all elements through which it can maintain the sales

force. However, balanced scorecard is a lengthy process which is to customized according to the

organization. A lot of data and information is required for balanced scorecard. Therefore, KPI is

far better than the balanced scorecard.

CONCLUSION

By summing up this report, it can be said that management accounting system helps in

reducing the cost of the product with better production techniques to be implemented and to

maintain the optimum inventory level. It can also be noticed that different types of budgets aid

the management to make better decision for future. In addition to this, it can be concluded that

usage of absorption costing method proves to be beneficial because it includes the fixed cost in

calculation of the cost and profit. Further, it can be concluded that budgetary control tools helps

in managing and controlling the business operations of the organization. The cash budget

maintains the cash balance so that the company can clear their payments on time. Finally, it can

be observed that there are various tools to handle the financial problems. Usage of benchmarking

helps to set targets in accordance with the competitive firms. It can help in increasing the

productivity and profitability of the company.

REFERENCES

Books and Journals

Dierkes, S. and Siepelmeyer, D., 2019. Production and cost theory-based material flow cost

accounting. Journal of Cleaner Production. 235. pp.483-492.

Muchaendepi, W. and et.al., 2019. Inventory management and performance of SMEs in the

manufacturing sector of Harare. Procedia Manufacturing. 33. pp.454-461.

ElMaraghy, W. and Alami, D., 2020. Activity Based Aggregate Job Costing Model for

Reconfigurable Manufacturing Systems. International Journal of Industry and

Sustainable Development. 1(2). pp.1-19.

Gupta, N. and et.al., 2020. Price Optimization for Revenue Maximization at Scale. SMU Data

Science Review. 3(3). p.4.

Church, B. K., Kuang, X. J. and Liu, Y. S., 2019. The effects of measurement basis and slack

benefits on honesty in budget reporting. Accounting, Organizations and Society. 72.

pp.74-84.

Suwantari, N. P., Ariana, I. M. and Suprapto, P. A., 2020. Accounting Analysis in Accounts

Receivable Management to Minimize the Risk of Uncollectible Receivables at ALS

Hotel and Resort. Journal of Applied Sciences in Accounting, Finance, and Tax. 3(2).

pp.117-124.

Drobyazko, S. and et.al., 2019. Formation of hybrid costing system accounting model at the

enterprise. Academy of Accounting and Financial Studies Journal. 23(6). pp.1-6.

Muchaendepi, W. and et.al., 2019. Inventory management and performance of SMEs in the

manufacturing sector of Harare. Procedia Manufacturing. 33. pp.454-461.

Averina, I., 2019. EVOLUTIONS OF COSTING SYSTEMS: A REVIEW OF TRADITIONAL

AND MODERN COSTING SYSTEMS. RUSSIAN ECONOMY: GOALS,

CHALLENGES AND ACHIEVMENTS, pp.34-36.

Johnsson, F., Normann, F. and Svensson, E., 2020. Marginal abatement cost curve of industrial

CO2 capture and storage–a Swedish case study. Frontiers in Energy Research. 8. p.175.

Felicia, C. M., 2019. Aspects Regarding The Size Of Romania'S Cash Budget Deficit. Annals-

Economy Series. 3. pp.115-121.

Anthopoulos, L., Janssen, M. and Weerakkody, V., 2019. A Unified Smart City Model (USCM)

for smart city conceptualization and benchmarking. Smart cities and smart spaces:

Concepts, methodologies, tools, and applications, pp.247-264.

Haber, J. and Schryver, C., 2019. How to create key performance indicators. The CPA Journal.

89(4). pp.24-30.

Online

[Online]. Available through: <>

[Online]. Available through: <>

[Online]. Available through: <>

Books and Journals

Dierkes, S. and Siepelmeyer, D., 2019. Production and cost theory-based material flow cost

accounting. Journal of Cleaner Production. 235. pp.483-492.

Muchaendepi, W. and et.al., 2019. Inventory management and performance of SMEs in the

manufacturing sector of Harare. Procedia Manufacturing. 33. pp.454-461.

ElMaraghy, W. and Alami, D., 2020. Activity Based Aggregate Job Costing Model for

Reconfigurable Manufacturing Systems. International Journal of Industry and

Sustainable Development. 1(2). pp.1-19.

Gupta, N. and et.al., 2020. Price Optimization for Revenue Maximization at Scale. SMU Data

Science Review. 3(3). p.4.

Church, B. K., Kuang, X. J. and Liu, Y. S., 2019. The effects of measurement basis and slack

benefits on honesty in budget reporting. Accounting, Organizations and Society. 72.

pp.74-84.

Suwantari, N. P., Ariana, I. M. and Suprapto, P. A., 2020. Accounting Analysis in Accounts

Receivable Management to Minimize the Risk of Uncollectible Receivables at ALS

Hotel and Resort. Journal of Applied Sciences in Accounting, Finance, and Tax. 3(2).

pp.117-124.

Drobyazko, S. and et.al., 2019. Formation of hybrid costing system accounting model at the

enterprise. Academy of Accounting and Financial Studies Journal. 23(6). pp.1-6.

Muchaendepi, W. and et.al., 2019. Inventory management and performance of SMEs in the

manufacturing sector of Harare. Procedia Manufacturing. 33. pp.454-461.

Averina, I., 2019. EVOLUTIONS OF COSTING SYSTEMS: A REVIEW OF TRADITIONAL

AND MODERN COSTING SYSTEMS. RUSSIAN ECONOMY: GOALS,

CHALLENGES AND ACHIEVMENTS, pp.34-36.

Johnsson, F., Normann, F. and Svensson, E., 2020. Marginal abatement cost curve of industrial

CO2 capture and storage–a Swedish case study. Frontiers in Energy Research. 8. p.175.

Felicia, C. M., 2019. Aspects Regarding The Size Of Romania'S Cash Budget Deficit. Annals-

Economy Series. 3. pp.115-121.

Anthopoulos, L., Janssen, M. and Weerakkody, V., 2019. A Unified Smart City Model (USCM)

for smart city conceptualization and benchmarking. Smart cities and smart spaces:

Concepts, methodologies, tools, and applications, pp.247-264.

Haber, J. and Schryver, C., 2019. How to create key performance indicators. The CPA Journal.

89(4). pp.24-30.

Online

[Online]. Available through: <>

[Online]. Available through: <>

[Online]. Available through: <>

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.