Management Accounting: Understanding Systems, Reporting Methods, and Integration within Organizational Context - Desklib

VerifiedAdded on 2023/06/18

|19

|5458

|59

AI Summary

This report discusses the concept of management accounting, types of management accounting systems, methods of management accounting reporting, and its integration within Eagle Eye Solutions. It also compares MA planning tools on the basis of their advantages and disadvantages and evaluates the effectiveness of MA in responding to financial problems of the company. The report emphasizes the importance of optimal capital structure, developing management information system, and controlling cost of products. It also explains the difference between marginal and absorption costing and the uses of financial reporting and statement for success and growth of business.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

5 – Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

Understanding Management Accounting....................................................................................3

Essential requirements of MA systems........................................................................................3

Different methods used in MA reporting.....................................................................................4

Principles of MA..........................................................................................................................5

Role of management accounting and management accounting system.......................................6

Income Statement Preparation under marginal and absorption costing.......................................7

Uses of financial reporting and statement for success and growth of business...........................8

Critical evaluation of how MA accounting systems and reporting methods are integrated

within an organizational context..................................................................................................9

Benefits of MA function to Eagle Eye.........................................................................................9

Conclusion of applying MA.........................................................................................................9

PART 2..........................................................................................................................................10

1. Comparison and contrasting three planning tools used in management accounting for

budgetary control with its advantages and disadvantages.........................................................10

2. Comparison of ways in which management accounting is effectively applied within

company in dealing and preventing financial problems............................................................13

CONCLUSION AND RECOMMENDATIONS..........................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

Understanding Management Accounting....................................................................................3

Essential requirements of MA systems........................................................................................3

Different methods used in MA reporting.....................................................................................4

Principles of MA..........................................................................................................................5

Role of management accounting and management accounting system.......................................6

Income Statement Preparation under marginal and absorption costing.......................................7

Uses of financial reporting and statement for success and growth of business...........................8

Critical evaluation of how MA accounting systems and reporting methods are integrated

within an organizational context..................................................................................................9

Benefits of MA function to Eagle Eye.........................................................................................9

Conclusion of applying MA.........................................................................................................9

PART 2..........................................................................................................................................10

1. Comparison and contrasting three planning tools used in management accounting for

budgetary control with its advantages and disadvantages.........................................................10

2. Comparison of ways in which management accounting is effectively applied within

company in dealing and preventing financial problems............................................................13

CONCLUSION AND RECOMMENDATIONS..........................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION

MA is of great importance in making managerial decisions with the help of budgeting,

forecasting and in-depth analysis of business affairs. This report is based on Eagle eye solutions

which is based in UK to provide digital platform for retail businesses. Such platforms are meant

for intelligent and real time connections with customers (Vakhrushina and et.al., 2018). Within

the two parts of this report, concept of MA, types of MA systems, methods of MA reporting and

its integration within Eagle eye has been evaluated. Also, comparison of MA planning tools on

the basis of their advantages and disadvantages has been done in this report. At last,

effectiveness of MA in responding to financial problems of the company will be evaluated here.

MAIN BODY

PART 1

Understanding Management Accounting

As explained and defined by CFI (Corporate Finance Institute), management accounting involves

the process of identifying, measuring, analysing & interpreting the information and data of

financial nature. For instance, financial manager within Eagle Eye can apply MA methods and

system in their organizational context for taking sound and effective financial decision, so that

management can ensure overall efficiency in business's regular operations.

Essential requirements of MA systems

The various MA systems that Eagle Eye is essential required to apply and follow within

its organizational context for greater efficiency and effectiveness are as follows:

Cost accounting system: The system is of great importance as it is concerned with the

categorization of overall cost of the organization into direct and indirect cost (Ax and Greve,

2017). For instance, cost accounting system can be implemented within Eagle eye solutions to

determine how much cost the company is incurring towards maintaining and updating software

from time to time. Accordingly, they can determine how much price they should charge for their

software solutions which is of great importance in ensuring overall profitability of the business.

Inventory management system: This system of MA provides with various procedures for

valuing inventory of the business like FIFO, LIFO and AVCO. For instance, there are many

inventory related issues that can arise within Eagle Eye to ensure smooth flow of inventory

during the process of production. It helps an organization to avoid problems of losses due to

MA is of great importance in making managerial decisions with the help of budgeting,

forecasting and in-depth analysis of business affairs. This report is based on Eagle eye solutions

which is based in UK to provide digital platform for retail businesses. Such platforms are meant

for intelligent and real time connections with customers (Vakhrushina and et.al., 2018). Within

the two parts of this report, concept of MA, types of MA systems, methods of MA reporting and

its integration within Eagle eye has been evaluated. Also, comparison of MA planning tools on

the basis of their advantages and disadvantages has been done in this report. At last,

effectiveness of MA in responding to financial problems of the company will be evaluated here.

MAIN BODY

PART 1

Understanding Management Accounting

As explained and defined by CFI (Corporate Finance Institute), management accounting involves

the process of identifying, measuring, analysing & interpreting the information and data of

financial nature. For instance, financial manager within Eagle Eye can apply MA methods and

system in their organizational context for taking sound and effective financial decision, so that

management can ensure overall efficiency in business's regular operations.

Essential requirements of MA systems

The various MA systems that Eagle Eye is essential required to apply and follow within

its organizational context for greater efficiency and effectiveness are as follows:

Cost accounting system: The system is of great importance as it is concerned with the

categorization of overall cost of the organization into direct and indirect cost (Ax and Greve,

2017). For instance, cost accounting system can be implemented within Eagle eye solutions to

determine how much cost the company is incurring towards maintaining and updating software

from time to time. Accordingly, they can determine how much price they should charge for their

software solutions which is of great importance in ensuring overall profitability of the business.

Inventory management system: This system of MA provides with various procedures for

valuing inventory of the business like FIFO, LIFO and AVCO. For instance, there are many

inventory related issues that can arise within Eagle Eye to ensure smooth flow of inventory

during the process of production. It helps an organization to avoid problems of losses due to

breakage and theft. Accordingly, ordering of stock in a required quantity become possible at the

right time (Bento, Mertins and White, 2018). Also, with the help of efficient inventory

management system, identification and responding to trends can be possible. So that, customer's

warning can be fulfilled without getting delay and facing any shortages.

Job costing system: This system involves assignment of costs that an organization has incurred

to difference job and services performed within the organizational context. For example, Eagle

eye can implement this system to allocate overall costs to difference jobs such as hardware

solutions, software solutions, etc. By doing business can determine how much profitable each

different job is and whether to continue with the job or not. The system should be such through

which it can be identified that what is the cost of materials associated with each different jobs.

Price – optimization system: This system is very useful for the companies in deciding the right

price for their products by giving consideration to the demand of the company's products and

services in the market (Pedroso, Gomes and Yasin, 2020). To determine the right price for the

products, management within the company always spend enough time towards arriving at the

right price to sell their products in quick manner. It is the strategy helps a company in reaching

at a desired profitability levels by gaining insights on how sensitive their clients are to the change

in the price of the products. Through this system of MA, variations in demand can be determined

at different levels of price along with combining cost related data with inventory related

information, so that recommendations can be made on how profits can be improved.

Different methods used in MA reporting

There are various methods within the scope of management accounting that can be used by the

accountants and finance manager of Eagle Eye are as follows:

Budget reports: This kind of reports are useful in setting benchmarks for the performance which

is known as budgeted performance for the future of the company. Through this, expected cost

that may incurred in nearer future of Eagle Eye solution can be determined, so that at the end of

the budgeted period the actual costs are compared with that of budgeted one and accordingly, the

variance between budgeted and actual can be identified (G'iyosov, 2019). For instance, Financial

management team can prepare cash budget to determine how much closing cash balance they are

required to maintain and also can create spending plan for better management of liquidity and

short term solvency.

right time (Bento, Mertins and White, 2018). Also, with the help of efficient inventory

management system, identification and responding to trends can be possible. So that, customer's

warning can be fulfilled without getting delay and facing any shortages.

Job costing system: This system involves assignment of costs that an organization has incurred

to difference job and services performed within the organizational context. For example, Eagle

eye can implement this system to allocate overall costs to difference jobs such as hardware

solutions, software solutions, etc. By doing business can determine how much profitable each

different job is and whether to continue with the job or not. The system should be such through

which it can be identified that what is the cost of materials associated with each different jobs.

Price – optimization system: This system is very useful for the companies in deciding the right

price for their products by giving consideration to the demand of the company's products and

services in the market (Pedroso, Gomes and Yasin, 2020). To determine the right price for the

products, management within the company always spend enough time towards arriving at the

right price to sell their products in quick manner. It is the strategy helps a company in reaching

at a desired profitability levels by gaining insights on how sensitive their clients are to the change

in the price of the products. Through this system of MA, variations in demand can be determined

at different levels of price along with combining cost related data with inventory related

information, so that recommendations can be made on how profits can be improved.

Different methods used in MA reporting

There are various methods within the scope of management accounting that can be used by the

accountants and finance manager of Eagle Eye are as follows:

Budget reports: This kind of reports are useful in setting benchmarks for the performance which

is known as budgeted performance for the future of the company. Through this, expected cost

that may incurred in nearer future of Eagle Eye solution can be determined, so that at the end of

the budgeted period the actual costs are compared with that of budgeted one and accordingly, the

variance between budgeted and actual can be identified (G'iyosov, 2019). For instance, Financial

management team can prepare cash budget to determine how much closing cash balance they are

required to maintain and also can create spending plan for better management of liquidity and

short term solvency.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Performance report: This report is useful in reviewing and analysing various performance

related factors of employees and different departments with the company. Like, Eagle Eye can

prepare performance report to evaluate those employees who are directly linked with the

production process to ensure higher productivity and quality of their IT solutions. With the help

of this report, requirement of providing training and development sessions can be understood.

Account Receivables ageing report: Framing credit policies become possible through this

method of MA along with appropriate cash flow management. The whole receivables balance are

first broken down on the basis of duration within which they are expected to make payments. For

managers, it is of high importance to identify that whether the company is facing any issues in

the process of collecting dues from its customers (Saukkonen, Laine and Suomala, 2018). If yes

and the majority of customers are not able to pay their outstanding balances, then this indicates

that Eagle Eye must tighten their credit policies. Time to time monitoring of account receivables

ageing report allows for looking over debts of the company.

Capital budgeting: This method of MA provides a useful insight about which project os most

profitable and appropriate for the business. For instance, to determine how to get back the

invested amount at the earliest can be facilitated by management accountant of Eagle Eye

through the application of pay back period technique of capital budgeting which is most suitable

for determining how long it will take for the business to get back their invested amount.

Inventory and manufacturing: To make manufacturing process highly efficient, MA accounting

reports can be used by Eagle Eye as these reports provides information regarding hourly labour

costs, per unit overhead costs and inventory wastes (Dierynck and Labro, 2018). With the help of

such information, manager can determine which production line needs improvements and how

bonuses can be linked with employees performance to reduce wastages and costs.

Principles of MA Compiling and designing: Accounting statements, reports, information and records along

with the evidence results related to future, past and present should be compiled and

designed in such a way to meet the needs of the Eagle Eye and resolve their problems

accordingly. Also, design of MA systems should be such that facilitate presentation of

relevant data and accounting information can also be modified to meet managerial

requirements.

related factors of employees and different departments with the company. Like, Eagle Eye can

prepare performance report to evaluate those employees who are directly linked with the

production process to ensure higher productivity and quality of their IT solutions. With the help

of this report, requirement of providing training and development sessions can be understood.

Account Receivables ageing report: Framing credit policies become possible through this

method of MA along with appropriate cash flow management. The whole receivables balance are

first broken down on the basis of duration within which they are expected to make payments. For

managers, it is of high importance to identify that whether the company is facing any issues in

the process of collecting dues from its customers (Saukkonen, Laine and Suomala, 2018). If yes

and the majority of customers are not able to pay their outstanding balances, then this indicates

that Eagle Eye must tighten their credit policies. Time to time monitoring of account receivables

ageing report allows for looking over debts of the company.

Capital budgeting: This method of MA provides a useful insight about which project os most

profitable and appropriate for the business. For instance, to determine how to get back the

invested amount at the earliest can be facilitated by management accountant of Eagle Eye

through the application of pay back period technique of capital budgeting which is most suitable

for determining how long it will take for the business to get back their invested amount.

Inventory and manufacturing: To make manufacturing process highly efficient, MA accounting

reports can be used by Eagle Eye as these reports provides information regarding hourly labour

costs, per unit overhead costs and inventory wastes (Dierynck and Labro, 2018). With the help of

such information, manager can determine which production line needs improvements and how

bonuses can be linked with employees performance to reduce wastages and costs.

Principles of MA Compiling and designing: Accounting statements, reports, information and records along

with the evidence results related to future, past and present should be compiled and

designed in such a way to meet the needs of the Eagle Eye and resolve their problems

accordingly. Also, design of MA systems should be such that facilitate presentation of

relevant data and accounting information can also be modified to meet managerial

requirements.

Relevance: Managers using information for the purpose of making decisions should be

relevant specifically (Vakhrushina and et.al., 2018). For this, management needs to

review organizational requirement on a regular basis to reflect the changes taking in the

business environment. For instance, budget reports must be prepared by utilizing present,

past, future, internal, external, non-financial and financial information to ensure

appropriate forecasting. Management by exception: While presenting reports and information to management,

this particular principle of MA has been followed. It means application of standard

costing techniques and budgetary control system within the framework of MA systems

(Ax and Greve, 2017). With this, the deviation of actual performance from planned

performance can be found out easily and accordingly informed to management to

understand what is going wrong and what actions must be taken by them.

Credibility: The roles and responsibility of all the team members within different

departments must be defined in a structured form. Within Eagle eye ethical rules and

regulations must be followed to reinforce the aspects related to ethics in information

technology professionalism. In this way stake-holder's trust towards the company can be

improvised.

Role of management accounting and management accounting system

The managers of Eagle Eye Solution Ltd is need to fulfil the following role of

management accounting: Maintaining Optimal capital structure: The company need to manage optimal capital

structure within their company which involve debt, equity, loans, bonds etc. Thus it is

advisable to the Eagle Eye company to adopt optimal capital structure because it provide

them high benefits and is available at low cost of acquisition. For this, they can adopt

weighted average cost of capital model (Lyly-Yrjänäinen and et.al., 2017). Developing Management information system: Besides maintaining optimal capital

structure, the company's management also need to develop and implement management

information system. For example, with the application of systems within Eagle Eye

company, the managers are able to process its work more efficiently and error free.

Controlling: This is basically one of the most crucial role of management accounting

department as it involve control of cost of products. It require proper communication

relevant specifically (Vakhrushina and et.al., 2018). For this, management needs to

review organizational requirement on a regular basis to reflect the changes taking in the

business environment. For instance, budget reports must be prepared by utilizing present,

past, future, internal, external, non-financial and financial information to ensure

appropriate forecasting. Management by exception: While presenting reports and information to management,

this particular principle of MA has been followed. It means application of standard

costing techniques and budgetary control system within the framework of MA systems

(Ax and Greve, 2017). With this, the deviation of actual performance from planned

performance can be found out easily and accordingly informed to management to

understand what is going wrong and what actions must be taken by them.

Credibility: The roles and responsibility of all the team members within different

departments must be defined in a structured form. Within Eagle eye ethical rules and

regulations must be followed to reinforce the aspects related to ethics in information

technology professionalism. In this way stake-holder's trust towards the company can be

improvised.

Role of management accounting and management accounting system

The managers of Eagle Eye Solution Ltd is need to fulfil the following role of

management accounting: Maintaining Optimal capital structure: The company need to manage optimal capital

structure within their company which involve debt, equity, loans, bonds etc. Thus it is

advisable to the Eagle Eye company to adopt optimal capital structure because it provide

them high benefits and is available at low cost of acquisition. For this, they can adopt

weighted average cost of capital model (Lyly-Yrjänäinen and et.al., 2017). Developing Management information system: Besides maintaining optimal capital

structure, the company's management also need to develop and implement management

information system. For example, with the application of systems within Eagle Eye

company, the managers are able to process its work more efficiently and error free.

Controlling: This is basically one of the most crucial role of management accounting

department as it involve control of cost of products. It require proper communication

among the departments regarding cost related information (Abernethy and Wallis, 2019).

For this, managers of Eagle Eye company need to adopt variance analysis tools to

identify the gap between actual and standard income and expenses.

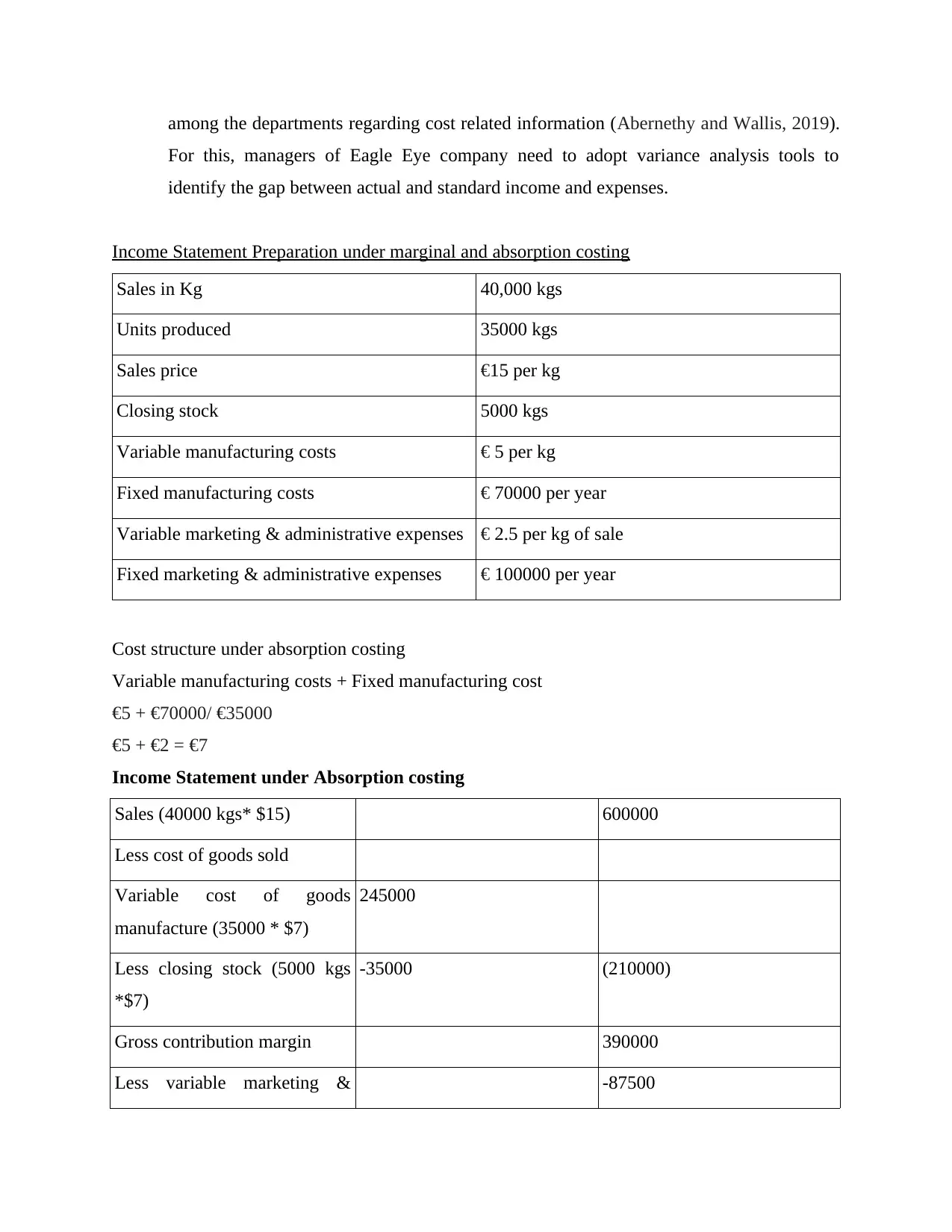

Income Statement Preparation under marginal and absorption costing

Sales in Kg 40,000 kgs

Units produced 35000 kgs

Sales price €15 per kg

Closing stock 5000 kgs

Variable manufacturing costs € 5 per kg

Fixed manufacturing costs € 70000 per year

Variable marketing & administrative expenses € 2.5 per kg of sale

Fixed marketing & administrative expenses € 100000 per year

Cost structure under absorption costing

Variable manufacturing costs + Fixed manufacturing cost

€5 + €70000/ €35000

€5 + €2 = €7

Income Statement under Absorption costing

Sales (40000 kgs* $15) 600000

Less cost of goods sold

Variable cost of goods

manufacture (35000 * $7)

245000

Less closing stock (5000 kgs

*$7)

-35000 (210000)

Gross contribution margin 390000

Less variable marketing & -87500

For this, managers of Eagle Eye company need to adopt variance analysis tools to

identify the gap between actual and standard income and expenses.

Income Statement Preparation under marginal and absorption costing

Sales in Kg 40,000 kgs

Units produced 35000 kgs

Sales price €15 per kg

Closing stock 5000 kgs

Variable manufacturing costs € 5 per kg

Fixed manufacturing costs € 70000 per year

Variable marketing & administrative expenses € 2.5 per kg of sale

Fixed marketing & administrative expenses € 100000 per year

Cost structure under absorption costing

Variable manufacturing costs + Fixed manufacturing cost

€5 + €70000/ €35000

€5 + €2 = €7

Income Statement under Absorption costing

Sales (40000 kgs* $15) 600000

Less cost of goods sold

Variable cost of goods

manufacture (35000 * $7)

245000

Less closing stock (5000 kgs

*$7)

-35000 (210000)

Gross contribution margin 390000

Less variable marketing & -87500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

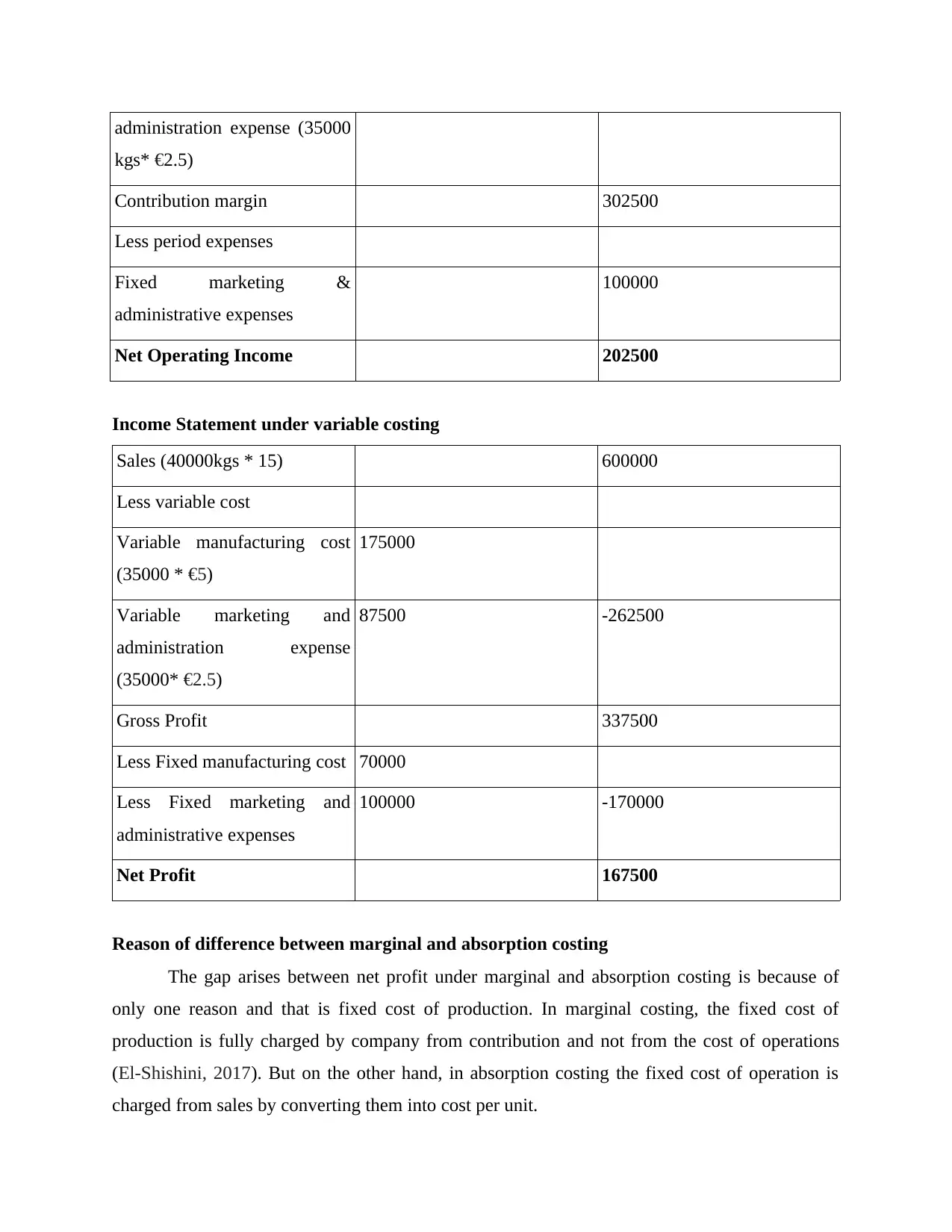

administration expense (35000

kgs* €2.5)

Contribution margin 302500

Less period expenses

Fixed marketing &

administrative expenses

100000

Net Operating Income 202500

Income Statement under variable costing

Sales (40000kgs * 15) 600000

Less variable cost

Variable manufacturing cost

(35000 * €5)

175000

Variable marketing and

administration expense

(35000* €2.5)

87500 -262500

Gross Profit 337500

Less Fixed manufacturing cost 70000

Less Fixed marketing and

administrative expenses

100000 -170000

Net Profit 167500

Reason of difference between marginal and absorption costing

The gap arises between net profit under marginal and absorption costing is because of

only one reason and that is fixed cost of production. In marginal costing, the fixed cost of

production is fully charged by company from contribution and not from the cost of operations

(El-Shishini, 2017). But on the other hand, in absorption costing the fixed cost of operation is

charged from sales by converting them into cost per unit.

kgs* €2.5)

Contribution margin 302500

Less period expenses

Fixed marketing &

administrative expenses

100000

Net Operating Income 202500

Income Statement under variable costing

Sales (40000kgs * 15) 600000

Less variable cost

Variable manufacturing cost

(35000 * €5)

175000

Variable marketing and

administration expense

(35000* €2.5)

87500 -262500

Gross Profit 337500

Less Fixed manufacturing cost 70000

Less Fixed marketing and

administrative expenses

100000 -170000

Net Profit 167500

Reason of difference between marginal and absorption costing

The gap arises between net profit under marginal and absorption costing is because of

only one reason and that is fixed cost of production. In marginal costing, the fixed cost of

production is fully charged by company from contribution and not from the cost of operations

(El-Shishini, 2017). But on the other hand, in absorption costing the fixed cost of operation is

charged from sales by converting them into cost per unit.

Uses of financial reporting and statement for success and growth of business

The financial statements and reporting basically provide real-time analysis using ratio

analysis tool to the Eagle Eye company with the help of which the company can determine its

profitability and liquidity performance. The financial reports is also used by the management of

the company to identify and gauge liquidity position of the company. For example, currently the

Eagle Eye company acquire funds from only equity financing which does not allow them any tax

benefits (Botes and Sharma, 2017). So, if the company really wants to earn more profit with tax

saving they have to adopt the debt financing and equity financing both in 2:1 ratio.

Critical evaluation of how MA accounting systems and reporting methods are integrated within

an organisational context

Both MA systems and reporting methods are helpful for Eagle eye in making better decisions for

enhancing business efficiency. It helps in understanding position at present and analysing it for

identifying future business opportunities. Through integration of inventory management systems,

Eagle eye can determine how much inventory level they should maintain (Bento, Mertins and

White, 2018). For example, Unilever by using JIT method for managing its inventory became a

largest retail company in UK. Also, job cost report are helpful in identifying cost associated with

different jobs to eliminate the one which is not profitable for the business. However, it is always

advisable to first consider the business objective prior to integration of any MA systems or

reporting methods as poor integration may leads to non-accomplishment of goals and also

financial loss for the company.

Benefits of MA function to Eagle Eye

The following are benefits of adopting MA tools and techniques within organizational system:

Marginal analysis is useful for Eagle eye in determining profits from generating revenue

by offering software solutions to customers.

Break-even analysis is useful in determining the minimum level of sales to avoid losses

in business and also helps in setting margin of safety (Pedroso, Gomes and Yasin, 2020).

To identify and report the causes of variance in actual and planned performance to the

management, variance analysis is very necessary.

The financial statements and reporting basically provide real-time analysis using ratio

analysis tool to the Eagle Eye company with the help of which the company can determine its

profitability and liquidity performance. The financial reports is also used by the management of

the company to identify and gauge liquidity position of the company. For example, currently the

Eagle Eye company acquire funds from only equity financing which does not allow them any tax

benefits (Botes and Sharma, 2017). So, if the company really wants to earn more profit with tax

saving they have to adopt the debt financing and equity financing both in 2:1 ratio.

Critical evaluation of how MA accounting systems and reporting methods are integrated within

an organisational context

Both MA systems and reporting methods are helpful for Eagle eye in making better decisions for

enhancing business efficiency. It helps in understanding position at present and analysing it for

identifying future business opportunities. Through integration of inventory management systems,

Eagle eye can determine how much inventory level they should maintain (Bento, Mertins and

White, 2018). For example, Unilever by using JIT method for managing its inventory became a

largest retail company in UK. Also, job cost report are helpful in identifying cost associated with

different jobs to eliminate the one which is not profitable for the business. However, it is always

advisable to first consider the business objective prior to integration of any MA systems or

reporting methods as poor integration may leads to non-accomplishment of goals and also

financial loss for the company.

Benefits of MA function to Eagle Eye

The following are benefits of adopting MA tools and techniques within organizational system:

Marginal analysis is useful for Eagle eye in determining profits from generating revenue

by offering software solutions to customers.

Break-even analysis is useful in determining the minimum level of sales to avoid losses

in business and also helps in setting margin of safety (Pedroso, Gomes and Yasin, 2020).

To identify and report the causes of variance in actual and planned performance to the

management, variance analysis is very necessary.

Conclusion of applying MA

To enhance motivation among employees and profitability of business, adoption of MA

systems and reporting methods is necessary. The tools, functions and benefits of MA and its

implementation within Eagle Eye has been evaluated in this report. Also, MA helps in improving

reliability and cost transparency within Eagle eye along with building brand image and

expanding to global level.

PART 2

1. Comparison and contrasting three planning tools used in management accounting for

budgetary control with its advantages and disadvantages

Planning tools of management accounting (MA) helps the Eagle Eye solution Ltd to

solve its financial issues with the preparation of budgets and forecast. The various planning tools

available to the Eagle Eye company are as follows:

Budgetary Control: This is a planning tool which is used to plan and control the

production and selling of goods and services of company. The main purpose of budgetary

control is promoting communication and coordination among departments along with

motivating managers and evaluating performance (Sedevich-Fons, 2018). For example,

the Purchase department of Eagle Eye solution Ltd need to continuously communicate

with the Production department in order to know about the quantity of raw material and

equipment required to purchased. This require preparation of budgets such as cash, sales,

purchase, production budgets etc.

Advantage and disadvantage of Budgetary control

Budgetary Control

Advantage Disadvantage

This tools is helpful for companies to

maintain coordinates activities among

various departments.

For example, if all the departments of

the Eagle Eye company clarified and

justified request of each other by using

In case if the application of budgets

within the Eagle Eye company are

done rigidly and mechanically than it

causes major problem to the company.

To enhance motivation among employees and profitability of business, adoption of MA

systems and reporting methods is necessary. The tools, functions and benefits of MA and its

implementation within Eagle Eye has been evaluated in this report. Also, MA helps in improving

reliability and cost transparency within Eagle eye along with building brand image and

expanding to global level.

PART 2

1. Comparison and contrasting three planning tools used in management accounting for

budgetary control with its advantages and disadvantages

Planning tools of management accounting (MA) helps the Eagle Eye solution Ltd to

solve its financial issues with the preparation of budgets and forecast. The various planning tools

available to the Eagle Eye company are as follows:

Budgetary Control: This is a planning tool which is used to plan and control the

production and selling of goods and services of company. The main purpose of budgetary

control is promoting communication and coordination among departments along with

motivating managers and evaluating performance (Sedevich-Fons, 2018). For example,

the Purchase department of Eagle Eye solution Ltd need to continuously communicate

with the Production department in order to know about the quantity of raw material and

equipment required to purchased. This require preparation of budgets such as cash, sales,

purchase, production budgets etc.

Advantage and disadvantage of Budgetary control

Budgetary Control

Advantage Disadvantage

This tools is helpful for companies to

maintain coordinates activities among

various departments.

For example, if all the departments of

the Eagle Eye company clarified and

justified request of each other by using

In case if the application of budgets

within the Eagle Eye company are

done rigidly and mechanically than it

causes major problem to the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

this tool, than their resources

allocation will automatically get

improve (Sedevich-Fons, 2018).

It is also helps in enhancing

communication with the employees

and the impact of which the specific

resources, revenue and activities

required to carry out business are get

to know by company managers.

Sometime the lack of employees

engagement in the preparation of

budgets cause demotivation.

For example, while preparing budgets

if managers of Eagle Eye company do

not provide information about

particular expenditures to employees,

than they will not be committed to

them.

With the help of reallocation tool the

managers of the company take proper

and appropriate corrective actions.

Their may be chance of increase in

perception of unfairness and rigid

budgets create difficulty to company to

obtain money from any new source

and ideas (Sedevich-Fons, 2018).

Cost Volume Profit analysis: This is basically most significant management planning

tool that help the company in analysing the effect of sales volume and product cost over

its operating profit (Abernethy and Wallis, 2019). For example, Eagle Eye solution

company with the help of cost volume profit analysis can estimate the income and

expenses figure and than compare it with the actual one. The variance and break-even

analysis is a tool used for computing the gap between standard and actual amount and no

loss and no profit sales point.

Advantages and disadvantage of cost volume profit analysis

Cost Volume Profit Analysis

Advantages Disadvantages

It is very easy to calculate the

estimated figures using the standard

The disadvantage of the break-even

analysis tool is that it assume that all

allocation will automatically get

improve (Sedevich-Fons, 2018).

It is also helps in enhancing

communication with the employees

and the impact of which the specific

resources, revenue and activities

required to carry out business are get

to know by company managers.

Sometime the lack of employees

engagement in the preparation of

budgets cause demotivation.

For example, while preparing budgets

if managers of Eagle Eye company do

not provide information about

particular expenditures to employees,

than they will not be committed to

them.

With the help of reallocation tool the

managers of the company take proper

and appropriate corrective actions.

Their may be chance of increase in

perception of unfairness and rigid

budgets create difficulty to company to

obtain money from any new source

and ideas (Sedevich-Fons, 2018).

Cost Volume Profit analysis: This is basically most significant management planning

tool that help the company in analysing the effect of sales volume and product cost over

its operating profit (Abernethy and Wallis, 2019). For example, Eagle Eye solution

company with the help of cost volume profit analysis can estimate the income and

expenses figure and than compare it with the actual one. The variance and break-even

analysis is a tool used for computing the gap between standard and actual amount and no

loss and no profit sales point.

Advantages and disadvantage of cost volume profit analysis

Cost Volume Profit Analysis

Advantages Disadvantages

It is very easy to calculate the

estimated figures using the standard

The disadvantage of the break-even

analysis tool is that it assume that all

formulas which get easily changes as

per the change in variables.

The variance among the estimation

and actual are also easily analysed by

the managers of Eagle Eye company

with the use of this planning tool of

management accounting (Abernethy

and Wallis, 2019).

their fixed cost remain fixed all over

the time.

But it is not possible in reality because

there is no fixed cost in real world.

The break-even analysis helps the

Eagle Eye company in planning their

future sales which they have sale for

earning profits.

For example, in case if the company's

sales are not increasing than they need

to make changes in their products and

service prices using pricing strategy.

The accuracy of this planning tool is

not 100% correct because it is based

on the assumption that variable cost

remain constant all level of sales level.

This is not correct and along with that

sometime separation between variable

and fixed cost is became difficult for

company (Abernethy and Wallis,

2019).

It is also helpful for the company to

calculate the margin of safety where

the company's contribution is higher

than its fixed cost.

With this, the managers of Eagle Eye

company can adopt strategy to reduce

its fixed as well as variable cost.

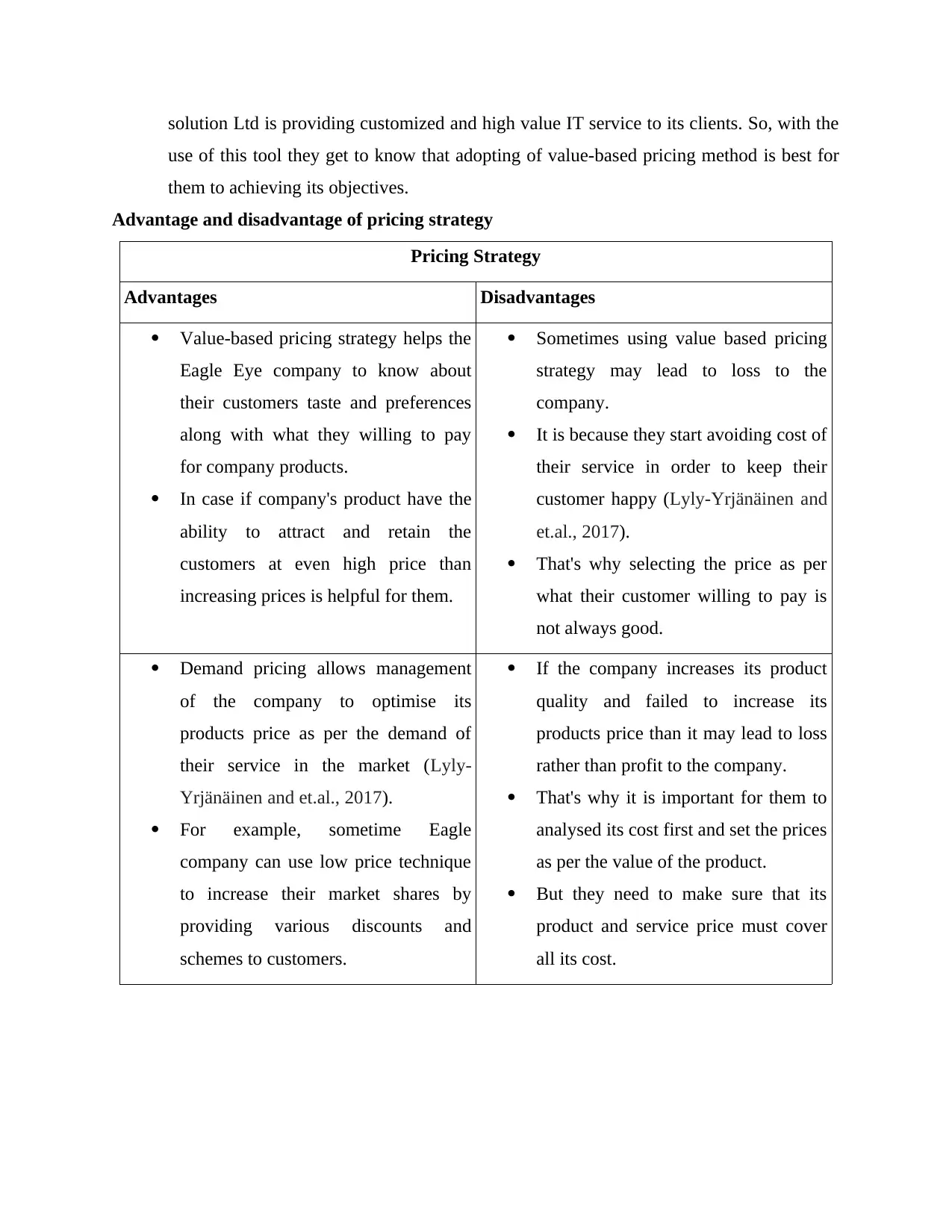

Pricing Strategy: The pricing strategy is a planning tool which require adoption of

appropriate pricing policies such as value-based, premium, penetration and skimming

pricing (Lyly-Yrjänäinen and et.al., 2017). This further help the company in achieving its

pricing and business objectives such as survival, high quality product and service,

maximizing profit and market share etc. For example, the main objective of Eagle Eye

per the change in variables.

The variance among the estimation

and actual are also easily analysed by

the managers of Eagle Eye company

with the use of this planning tool of

management accounting (Abernethy

and Wallis, 2019).

their fixed cost remain fixed all over

the time.

But it is not possible in reality because

there is no fixed cost in real world.

The break-even analysis helps the

Eagle Eye company in planning their

future sales which they have sale for

earning profits.

For example, in case if the company's

sales are not increasing than they need

to make changes in their products and

service prices using pricing strategy.

The accuracy of this planning tool is

not 100% correct because it is based

on the assumption that variable cost

remain constant all level of sales level.

This is not correct and along with that

sometime separation between variable

and fixed cost is became difficult for

company (Abernethy and Wallis,

2019).

It is also helpful for the company to

calculate the margin of safety where

the company's contribution is higher

than its fixed cost.

With this, the managers of Eagle Eye

company can adopt strategy to reduce

its fixed as well as variable cost.

Pricing Strategy: The pricing strategy is a planning tool which require adoption of

appropriate pricing policies such as value-based, premium, penetration and skimming

pricing (Lyly-Yrjänäinen and et.al., 2017). This further help the company in achieving its

pricing and business objectives such as survival, high quality product and service,

maximizing profit and market share etc. For example, the main objective of Eagle Eye

solution Ltd is providing customized and high value IT service to its clients. So, with the

use of this tool they get to know that adopting of value-based pricing method is best for

them to achieving its objectives.

Advantage and disadvantage of pricing strategy

Pricing Strategy

Advantages Disadvantages

Value-based pricing strategy helps the

Eagle Eye company to know about

their customers taste and preferences

along with what they willing to pay

for company products.

In case if company's product have the

ability to attract and retain the

customers at even high price than

increasing prices is helpful for them.

Sometimes using value based pricing

strategy may lead to loss to the

company.

It is because they start avoiding cost of

their service in order to keep their

customer happy (Lyly-Yrjänäinen and

et.al., 2017).

That's why selecting the price as per

what their customer willing to pay is

not always good.

Demand pricing allows management

of the company to optimise its

products price as per the demand of

their service in the market (Lyly-

Yrjänäinen and et.al., 2017).

For example, sometime Eagle

company can use low price technique

to increase their market shares by

providing various discounts and

schemes to customers.

If the company increases its product

quality and failed to increase its

products price than it may lead to loss

rather than profit to the company.

That's why it is important for them to

analysed its cost first and set the prices

as per the value of the product.

But they need to make sure that its

product and service price must cover

all its cost.

use of this tool they get to know that adopting of value-based pricing method is best for

them to achieving its objectives.

Advantage and disadvantage of pricing strategy

Pricing Strategy

Advantages Disadvantages

Value-based pricing strategy helps the

Eagle Eye company to know about

their customers taste and preferences

along with what they willing to pay

for company products.

In case if company's product have the

ability to attract and retain the

customers at even high price than

increasing prices is helpful for them.

Sometimes using value based pricing

strategy may lead to loss to the

company.

It is because they start avoiding cost of

their service in order to keep their

customer happy (Lyly-Yrjänäinen and

et.al., 2017).

That's why selecting the price as per

what their customer willing to pay is

not always good.

Demand pricing allows management

of the company to optimise its

products price as per the demand of

their service in the market (Lyly-

Yrjänäinen and et.al., 2017).

For example, sometime Eagle

company can use low price technique

to increase their market shares by

providing various discounts and

schemes to customers.

If the company increases its product

quality and failed to increase its

products price than it may lead to loss

rather than profit to the company.

That's why it is important for them to

analysed its cost first and set the prices

as per the value of the product.

But they need to make sure that its

product and service price must cover

all its cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Comparison of ways in which management accounting is effectively applied within company

in dealing and preventing financial problems

The different management accounting tools and techniques uses by various companies in

order to deal with the financial problems and also to solve it are as follows:

Benchmarking:

This is basically the best tool of measuring the performance of the company's products

and services along with the processes with that of its competitors. This means that, with the help

of benchmarking the company can able to change the scope of the service they offer to its

customers. For example, in Eagle Eye company their main issue is related with the competitive

advantage which they are not able to gain in UK market. That's why to deal with this issue the

company decided to adopt the Benchmarking techniques as it is helpful for encouraging team

building and cooperation (Johnstone, 2018). After application of this technique the Eagle Eye

company able to became one of highly competitive information technology service provider

company in the UK market.

Inventory Management systems:

This is a technique which help the company to know about the stock level that every

company need to be ordered at a point of time in order to avoid shortage of inventory. For

example, in Tesco company they mainly faces issues related to supply of stock to its supermarket

and stores all around the world on time (Drury, 2018). So, for this they have decided to use Just-

in-time inventory management tool and the impact of which they started ordering 90% of their

stock directly to supermarkets and only 10% to the warehouse. After application of inventory

management technique, the company is able to manage its inventory and timely fulfilment of

customers requirement related to products and services.

Investment appraisal techniques:

This helps the company to know about the investment project which can provide them

higher returns using the various method of capital budgeting. Some methods basically consider

the time value of money such as NPV and IRR that's why is more advisable to the company. For

example, in Pharmacy2U company they faces issues related to high profitability investment

projects. This means that company have the ability to acquire the funds at low cost but face

difficulty in investing the fund in profitable projects (Petera, P., Wagner, J. and Šoljaková, L.,

2020). So, in order to solve this financial issue the company has decided to adopt the Net Present

in dealing and preventing financial problems

The different management accounting tools and techniques uses by various companies in

order to deal with the financial problems and also to solve it are as follows:

Benchmarking:

This is basically the best tool of measuring the performance of the company's products

and services along with the processes with that of its competitors. This means that, with the help

of benchmarking the company can able to change the scope of the service they offer to its

customers. For example, in Eagle Eye company their main issue is related with the competitive

advantage which they are not able to gain in UK market. That's why to deal with this issue the

company decided to adopt the Benchmarking techniques as it is helpful for encouraging team

building and cooperation (Johnstone, 2018). After application of this technique the Eagle Eye

company able to became one of highly competitive information technology service provider

company in the UK market.

Inventory Management systems:

This is a technique which help the company to know about the stock level that every

company need to be ordered at a point of time in order to avoid shortage of inventory. For

example, in Tesco company they mainly faces issues related to supply of stock to its supermarket

and stores all around the world on time (Drury, 2018). So, for this they have decided to use Just-

in-time inventory management tool and the impact of which they started ordering 90% of their

stock directly to supermarkets and only 10% to the warehouse. After application of inventory

management technique, the company is able to manage its inventory and timely fulfilment of

customers requirement related to products and services.

Investment appraisal techniques:

This helps the company to know about the investment project which can provide them

higher returns using the various method of capital budgeting. Some methods basically consider

the time value of money such as NPV and IRR that's why is more advisable to the company. For

example, in Pharmacy2U company they faces issues related to high profitability investment

projects. This means that company have the ability to acquire the funds at low cost but face

difficulty in investing the fund in profitable projects (Petera, P., Wagner, J. and Šoljaková, L.,

2020). So, in order to solve this financial issue the company has decided to adopt the Net Present

Value method to select the investment projects. After the adoption of this technique the company

is able to select the most profitable assets and equipment for investment purpose.

Break-even Analysis:

The break-even analysis technique of management accounting help the company to

understand its no-loss and no-profit sales point. Along with that they can also compute its margin

of safety of the company's products and services. For example, In Verdant Leisure company the

managers has viewed that company are suffering losses and identifying its reason is difficult for

company. So, they decided to adopt the break-even analysis tool of marginal costing to identify

the reason behind company's product losses. After adoption of this MA technique, the company

now able to earn a continuous profit as they able to identify whether the reason of no profit is

products fixed cost, variable cost or selling price (Dahal, 2019). That's why it is also advisable to

the Eagle Eye company that they need to adopt this techniques for the success and growth of its

business to both local and international level.

CONCLUSION AND RECOMMENDATIONS

The report has concluded the various planning tools and techniques of management

accounting along with their advantage and disadvantage. The impact of which the report has

concluded the tools that Eagle Eye company need to incorporate within the business so that they

can achieve its business operational and financial objectives. Further, the report has concluded

the real world example of companies which are using MA techniques within its company to

solve financial problems. The roles and principles of management accounting techniques are also

concluded in this project along with its integration and benefits to Eagle Eye solution Ltd. The

recommendations on methods of MA that is available to the Eagle Eye company with the help of

which they can achieve sustainable business success are as follows:

It is recommended to the Eagle Eye company's managers that if they want to identify its

liquidity position than they need to adopt the budgeting techniques and prepare monthly

cash budgets or cash flow statements (Botes and Sharma, 2017). This also help them in

ensuring its cash needs for their business expansion and development purpose.

In order to expand its business, the company can also able to fulfil their cash needs by

acquiring funds from different sources such as debt and equity. Thus is advisable to the

is able to select the most profitable assets and equipment for investment purpose.

Break-even Analysis:

The break-even analysis technique of management accounting help the company to

understand its no-loss and no-profit sales point. Along with that they can also compute its margin

of safety of the company's products and services. For example, In Verdant Leisure company the

managers has viewed that company are suffering losses and identifying its reason is difficult for

company. So, they decided to adopt the break-even analysis tool of marginal costing to identify

the reason behind company's product losses. After adoption of this MA technique, the company

now able to earn a continuous profit as they able to identify whether the reason of no profit is

products fixed cost, variable cost or selling price (Dahal, 2019). That's why it is also advisable to

the Eagle Eye company that they need to adopt this techniques for the success and growth of its

business to both local and international level.

CONCLUSION AND RECOMMENDATIONS

The report has concluded the various planning tools and techniques of management

accounting along with their advantage and disadvantage. The impact of which the report has

concluded the tools that Eagle Eye company need to incorporate within the business so that they

can achieve its business operational and financial objectives. Further, the report has concluded

the real world example of companies which are using MA techniques within its company to

solve financial problems. The roles and principles of management accounting techniques are also

concluded in this project along with its integration and benefits to Eagle Eye solution Ltd. The

recommendations on methods of MA that is available to the Eagle Eye company with the help of

which they can achieve sustainable business success are as follows:

It is recommended to the Eagle Eye company's managers that if they want to identify its

liquidity position than they need to adopt the budgeting techniques and prepare monthly

cash budgets or cash flow statements (Botes and Sharma, 2017). This also help them in

ensuring its cash needs for their business expansion and development purpose.

In order to expand its business, the company can also able to fulfil their cash needs by

acquiring funds from different sources such as debt and equity. Thus is advisable to the

Eagle Eye company that they have to acquire the fund in optimal and ideal ratio i.e., 2:1

from debt and equity financing.

For identifying its non-profitable service process, it is advisable to the company that they

have to adopt the process and service based costing. This helps the managers of Eagle

Eye company to identify the process which incur high cost but do not deliver any profit to

the company (El-Shishini, 2017). Then such process have to be dissolve by the company.

At the time when Eagle Eye company wants to invest their funds on purchase of any

assets and equipment, then it is recommended to the company use NPV or IRR method of

capital budgeting. It is because this method consider the time value of money and provide

best and profitable investment plan out of various alternatives.

Along with that in order to determine the profitable and optimal level of output or

service, the company can use CVP or Break-even analysis (Napitupulu, 2020). This help

the company to know about its profitable output level and also identify about the poor

and lower performance of the employees of the company.

from debt and equity financing.

For identifying its non-profitable service process, it is advisable to the company that they

have to adopt the process and service based costing. This helps the managers of Eagle

Eye company to identify the process which incur high cost but do not deliver any profit to

the company (El-Shishini, 2017). Then such process have to be dissolve by the company.

At the time when Eagle Eye company wants to invest their funds on purchase of any

assets and equipment, then it is recommended to the company use NPV or IRR method of

capital budgeting. It is because this method consider the time value of money and provide

best and profitable investment plan out of various alternatives.

Along with that in order to determine the profitable and optimal level of output or

service, the company can use CVP or Break-even analysis (Napitupulu, 2020). This help

the company to know about its profitable output level and also identify about the poor

and lower performance of the employees of the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and journals

Sedevich-Fons, L., 2018. Linking strategic management accounting and quality management

systems. Business Process Management Journal.

Abernethy, M. A. and Wallis, M. S., 2019. Critique on the “manager effects” research and

implications for management accounting research. Journal of Management Accounting

Research. 31(1). pp.3-40.

Lyly-Yrjänäinen, J. and et.al., 2017. Interventionist management accounting research: theory

contributions with societal impact. Routledge.

Johnstone, L., 2018. Theorising and modelling social control in environmental management

accounting research. Social and Environmental Accountability Journal. 38(1). pp.30-48.

Drury, C., 2018. Cost and management accounting. Cengage Learning.

Petera, P., Wagner, J. and Šoljaková, L., 2020. Strategic management accounting and strategic

management: The mediating effect of performance evaluation and

rewarding. International Journal of Industrial Engineering and Management. 11(2).

pp.116-132.

Dahal, R. K., 2019. Changing role of management accounting in 21st Century. Review Pub

Administration Manag. 7(3). pp.1-8.

Botes, V. L. and Sharma, U., 2017. A gap in management accounting education: fact or

fiction. Pacific Accounting Review.

Napitupulu, I. H., 2020. Internal control, manager’s competency, management accounting

information systems and good corporate governance: Evidence from rural banks in

Indonesia. Global Business Review, p.0972150920919845.

El-Shishini, H. M., 2017. The use of management accounting techniques at hotels in

Bahrain. Review of Integrative Business and Economics Research. 6(2). p.78.

Vakhrushina, M. A., and et.al., 2018. Integrated management accounting in the financial

management system. Research Journal of Pharmaceutical, Biological and Chemical

Sciences, 9(3), pp.808-813.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research, 34,

pp.59-74.

Bento, R. F., Mertins, L. and White, L. F., 2018. Risk management and internal control: A study

of management accounting practice. In Advances in Management Accounting. Emerald

Publishing Limited.

Pedroso, E., Gomes, C. F. and Yasin, M. M., 2020. Management accounting systems: an

organizational competitive performance perspective. Benchmarking: An International

Journal.

G'iyosov, I. K., 2019. THE THEORICAL FEATURES OF THE ORGANIZATION OF THE

STRATEGIC MANAGEMENT ACCOUNTING IN BUSINESS. Theoretical & Applied

Science, (9), pp.260-266.

Saukkonen, N., Laine, T. and Suomala, P., 2018. Utilizing management accounting information

for decision-making: Limitations stemming from the process structure and the actors

involved. Qualitative Research in Accounting & Management.

1

Books and journals

Sedevich-Fons, L., 2018. Linking strategic management accounting and quality management

systems. Business Process Management Journal.

Abernethy, M. A. and Wallis, M. S., 2019. Critique on the “manager effects” research and

implications for management accounting research. Journal of Management Accounting

Research. 31(1). pp.3-40.

Lyly-Yrjänäinen, J. and et.al., 2017. Interventionist management accounting research: theory

contributions with societal impact. Routledge.

Johnstone, L., 2018. Theorising and modelling social control in environmental management

accounting research. Social and Environmental Accountability Journal. 38(1). pp.30-48.

Drury, C., 2018. Cost and management accounting. Cengage Learning.

Petera, P., Wagner, J. and Šoljaková, L., 2020. Strategic management accounting and strategic

management: The mediating effect of performance evaluation and

rewarding. International Journal of Industrial Engineering and Management. 11(2).

pp.116-132.

Dahal, R. K., 2019. Changing role of management accounting in 21st Century. Review Pub

Administration Manag. 7(3). pp.1-8.

Botes, V. L. and Sharma, U., 2017. A gap in management accounting education: fact or

fiction. Pacific Accounting Review.

Napitupulu, I. H., 2020. Internal control, manager’s competency, management accounting

information systems and good corporate governance: Evidence from rural banks in

Indonesia. Global Business Review, p.0972150920919845.

El-Shishini, H. M., 2017. The use of management accounting techniques at hotels in

Bahrain. Review of Integrative Business and Economics Research. 6(2). p.78.

Vakhrushina, M. A., and et.al., 2018. Integrated management accounting in the financial

management system. Research Journal of Pharmaceutical, Biological and Chemical

Sciences, 9(3), pp.808-813.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research, 34,

pp.59-74.

Bento, R. F., Mertins, L. and White, L. F., 2018. Risk management and internal control: A study

of management accounting practice. In Advances in Management Accounting. Emerald

Publishing Limited.

Pedroso, E., Gomes, C. F. and Yasin, M. M., 2020. Management accounting systems: an

organizational competitive performance perspective. Benchmarking: An International

Journal.

G'iyosov, I. K., 2019. THE THEORICAL FEATURES OF THE ORGANIZATION OF THE

STRATEGIC MANAGEMENT ACCOUNTING IN BUSINESS. Theoretical & Applied

Science, (9), pp.260-266.

Saukkonen, N., Laine, T. and Suomala, P., 2018. Utilizing management accounting information

for decision-making: Limitations stemming from the process structure and the actors

involved. Qualitative Research in Accounting & Management.

1

Dierynck, B. and Labro, E., 2018. Management accounting information properties and

operations management. Foundations and Trends in Technology, Information and

Operations Management (2018), 12(1), pp.1-114.

2

operations management. Foundations and Trends in Technology, Information and

Operations Management (2018), 12(1), pp.1-114.

2

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.