Management Accounting: Systems, Reports, Cost Calculation and Budgetary Control

VerifiedAdded on 2023/06/17

|17

|3851

|269

AI Summary

This report focuses on the use of management accounting in enhancing the efficiency and effectiveness of ASDA, a retail-based management dealing in groceries. It covers topics such as management accounting systems, reports, cost calculation, and budgetary control. The report also discusses various techniques and tools that can be used for these purposes. Subject: Management Accounting, Course Code: N/A, Course Name: N/A, College/University: N/A

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting systems..........................................................................................1

P2: Management accounting reports............................................................................................3

TASK 2............................................................................................................................................4

P3: Calculation of costs...............................................................................................................4

TASK 3............................................................................................................................................7

P4: Planning tools for Budgetary Control....................................................................................7

TASK 4............................................................................................................................................8

P5: Comparison of organizations.................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting systems..........................................................................................1

P2: Management accounting reports............................................................................................3

TASK 2............................................................................................................................................4

P3: Calculation of costs...............................................................................................................4

TASK 3............................................................................................................................................7

P4: Planning tools for Budgetary Control....................................................................................7

TASK 4............................................................................................................................................8

P5: Comparison of organizations.................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management Accounting termed to the use of a broad variety of methods and tools by

which the appropriate financial analysis will be done and therefore the right determination can be

taken by the managers of a particular organization which can thus help them in managing the

funds quite appropriately and properly (Alabdullah and Ahmed, 2020). Therefore, it is necessary

that the use of Management Accounting should be made so that the enhancement in the overall

level of efficiency and effectiveness level can be done in a right way. For this report, ASDA has

been selected. It is a retail based management that deals in groceries, and other related items. In

this report, there will be a elaborated and specific focussing on the manner in which the usage of

Management Accounting might be made with the aim of enhancing the global field level of

efficiency and effectiveness level within the organization in an appropriate manner so that the

management of the financial needs and requirements can be done.

TASK 1

P1: Management accounting systems

Management accounting is an important concept which is quite helpful for the managers

so that they are able to consider the way in which they can take the decisions which can be quite

useful for the purpose of managing the funds in a right manner (Alhatabat, 2020). Therefore, the

managers of ASDA are required to follows their concentration on its use so that the improvement

in the suitable level can be done in an appropriate way.

There are various types of Management accounting systems which can be used within a

company. These are explained as follows-

Cost Accounting System- It is a system in which a thorough and detailed assessment of

the costs is made (Amirbeyki Langroudi, Kordestani and Reazei, 2020). Hence, in this manner it

can be declared that the utilisation of this section that might be created so that the global term of

efficiency and effectiveness level can be made quite appropriately in a proper manner. ASDA

can use it for properly assessing the costs and determining the future course of action to be taken.

Essential requirements-

It is a system in which there must be identification of the methods and techniques to be

used for the determination of the level of costs in an appropriate manner.

1

Management Accounting termed to the use of a broad variety of methods and tools by

which the appropriate financial analysis will be done and therefore the right determination can be

taken by the managers of a particular organization which can thus help them in managing the

funds quite appropriately and properly (Alabdullah and Ahmed, 2020). Therefore, it is necessary

that the use of Management Accounting should be made so that the enhancement in the overall

level of efficiency and effectiveness level can be done in a right way. For this report, ASDA has

been selected. It is a retail based management that deals in groceries, and other related items. In

this report, there will be a elaborated and specific focussing on the manner in which the usage of

Management Accounting might be made with the aim of enhancing the global field level of

efficiency and effectiveness level within the organization in an appropriate manner so that the

management of the financial needs and requirements can be done.

TASK 1

P1: Management accounting systems

Management accounting is an important concept which is quite helpful for the managers

so that they are able to consider the way in which they can take the decisions which can be quite

useful for the purpose of managing the funds in a right manner (Alhatabat, 2020). Therefore, the

managers of ASDA are required to follows their concentration on its use so that the improvement

in the suitable level can be done in an appropriate way.

There are various types of Management accounting systems which can be used within a

company. These are explained as follows-

Cost Accounting System- It is a system in which a thorough and detailed assessment of

the costs is made (Amirbeyki Langroudi, Kordestani and Reazei, 2020). Hence, in this manner it

can be declared that the utilisation of this section that might be created so that the global term of

efficiency and effectiveness level can be made quite appropriately in a proper manner. ASDA

can use it for properly assessing the costs and determining the future course of action to be taken.

Essential requirements-

It is a system in which there must be identification of the methods and techniques to be

used for the determination of the level of costs in an appropriate manner.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

In this system, the identification of the appropriate steps to be taken so that the needs and

requirements of the organization are managed should be done quite appropriately.

Inventory Management System- In this division, the use of manner and toolsshould be

made for the specific aim of assessing the level of stock effectively and efficiently (Diab, 2020).

Thus, in this way it can be stated that the management of ASDAshould be able to make the use

of this system for managing the stock items appropriately.

Essential requirements-

In this system, a right tracking system must be used which can therefore help a lot in

managing the stock items systematically.

This system should be helpful for maintaining a higher-level of efficiency and

effectiveness in the management of the stock items in the organization.

Job Costing System- In this system, the proper assessment of the various types of job

costs should be made (Dwirandra and ASTIKA, 2020). In The relation of ASDA it can be stated

that this sections is quite essential and useful for determining and controlling the job sections.

Essential requirements-

This system must be able to identify the job costs and therefore ensure that the

appropriate actions can be taken by tracking them.

This system should be able to ensure that the appropriate and right steps should be taken

for enhancing the profitability level.

Price Optimization System- In this section, the management of the costs should be done

so that the suitable cost that are selected for the particular aim of ensuring that the section of

profits can be enhanced (Golyagina and Valuckas, 2020). Hence, it is quite necessary that the

business like ASDA are capable to make its usage for ascertaining the prices in a proper way.

Essential requirements-

This system should allow for forecasting of the different types of prices so that the prices

can be set according to the level of demand.

This system must be helpful for setting such prices so that the profits in the organization

can increase which will help the people within the organization.

P2: Management accounting reports

Management accounting reports are such reports that are quite helpful and helpful for the

particular purpose of ensuring that the analysis and interpretation can be carried out in an

2

requirements of the organization are managed should be done quite appropriately.

Inventory Management System- In this division, the use of manner and toolsshould be

made for the specific aim of assessing the level of stock effectively and efficiently (Diab, 2020).

Thus, in this way it can be stated that the management of ASDAshould be able to make the use

of this system for managing the stock items appropriately.

Essential requirements-

In this system, a right tracking system must be used which can therefore help a lot in

managing the stock items systematically.

This system should be helpful for maintaining a higher-level of efficiency and

effectiveness in the management of the stock items in the organization.

Job Costing System- In this system, the proper assessment of the various types of job

costs should be made (Dwirandra and ASTIKA, 2020). In The relation of ASDA it can be stated

that this sections is quite essential and useful for determining and controlling the job sections.

Essential requirements-

This system must be able to identify the job costs and therefore ensure that the

appropriate actions can be taken by tracking them.

This system should be able to ensure that the appropriate and right steps should be taken

for enhancing the profitability level.

Price Optimization System- In this section, the management of the costs should be done

so that the suitable cost that are selected for the particular aim of ensuring that the section of

profits can be enhanced (Golyagina and Valuckas, 2020). Hence, it is quite necessary that the

business like ASDA are capable to make its usage for ascertaining the prices in a proper way.

Essential requirements-

This system should allow for forecasting of the different types of prices so that the prices

can be set according to the level of demand.

This system must be helpful for setting such prices so that the profits in the organization

can increase which will help the people within the organization.

P2: Management accounting reports

Management accounting reports are such reports that are quite helpful and helpful for the

particular purpose of ensuring that the analysis and interpretation can be carried out in an

2

appropriate way (Hutahayan, 2020). Therefore, it can be declared that the use of such manner

that is quite essential and supportable for the particular purpose of ensuring that the right reason

and recommendations that might be derived which will be helpful in taking decisions. The

Management Accounting Reports that can be used by ASDA are mentioned below -

Job Costing Reports- These reports are highly helpful and useful for the determination

of the job costs in an appropriate way (Isoh, 2020). It is therefore crucial to make sure that the

determination of the job costs should be done through making an use of these reports. ASDA

managers should be able to make their use for the analysis of job costs and therefore determining

the approach to be taken for decreasing the job costs so that the profitability level can be

enhanced.

Inventory Management Reports- These reports are necessary for ensuring that the

management of the stock level can be done appropriately (Johnstone, 2020). Hence, it might be

stated that it is quite necessary and important to make their use so that the global level of ratio

and affectivity that are raising. In the relation of ASDA it should be ensured that the use of these

reports is done for the particular purpose of appropriate management of the different types of

stock point so that the accomplishment of the score and objectives can be through with it.

Departmental Reports- In these reports, the assessment of the performance level of the

departments is required to be made which will therefore help in identifying the appropriate

decisions to be taken for the future. Thus, it can be stated that through these reports the track of

the work done by the departments can be made. For ASDA it is necessary that the use of these

reports should be made so that the overall level of efficiency and effectiveness can be enhanced.

Performance Reports- In these reports, it is highly necessary that the performance

assessment is carried out which will be helpful for the purpose of taking the right steps in the

future. Therefore, it can be stated that through using these reports the performance level can be

increased. ASDA managers should be able to use them for ensuring that the deviations and

variations in the performance are assessed and thus the corrective actions are taken effectively

and efficiently.

3

that is quite essential and supportable for the particular purpose of ensuring that the right reason

and recommendations that might be derived which will be helpful in taking decisions. The

Management Accounting Reports that can be used by ASDA are mentioned below -

Job Costing Reports- These reports are highly helpful and useful for the determination

of the job costs in an appropriate way (Isoh, 2020). It is therefore crucial to make sure that the

determination of the job costs should be done through making an use of these reports. ASDA

managers should be able to make their use for the analysis of job costs and therefore determining

the approach to be taken for decreasing the job costs so that the profitability level can be

enhanced.

Inventory Management Reports- These reports are necessary for ensuring that the

management of the stock level can be done appropriately (Johnstone, 2020). Hence, it might be

stated that it is quite necessary and important to make their use so that the global level of ratio

and affectivity that are raising. In the relation of ASDA it should be ensured that the use of these

reports is done for the particular purpose of appropriate management of the different types of

stock point so that the accomplishment of the score and objectives can be through with it.

Departmental Reports- In these reports, the assessment of the performance level of the

departments is required to be made which will therefore help in identifying the appropriate

decisions to be taken for the future. Thus, it can be stated that through these reports the track of

the work done by the departments can be made. For ASDA it is necessary that the use of these

reports should be made so that the overall level of efficiency and effectiveness can be enhanced.

Performance Reports- In these reports, it is highly necessary that the performance

assessment is carried out which will be helpful for the purpose of taking the right steps in the

future. Therefore, it can be stated that through using these reports the performance level can be

increased. ASDA managers should be able to use them for ensuring that the deviations and

variations in the performance are assessed and thus the corrective actions are taken effectively

and efficiently.

3

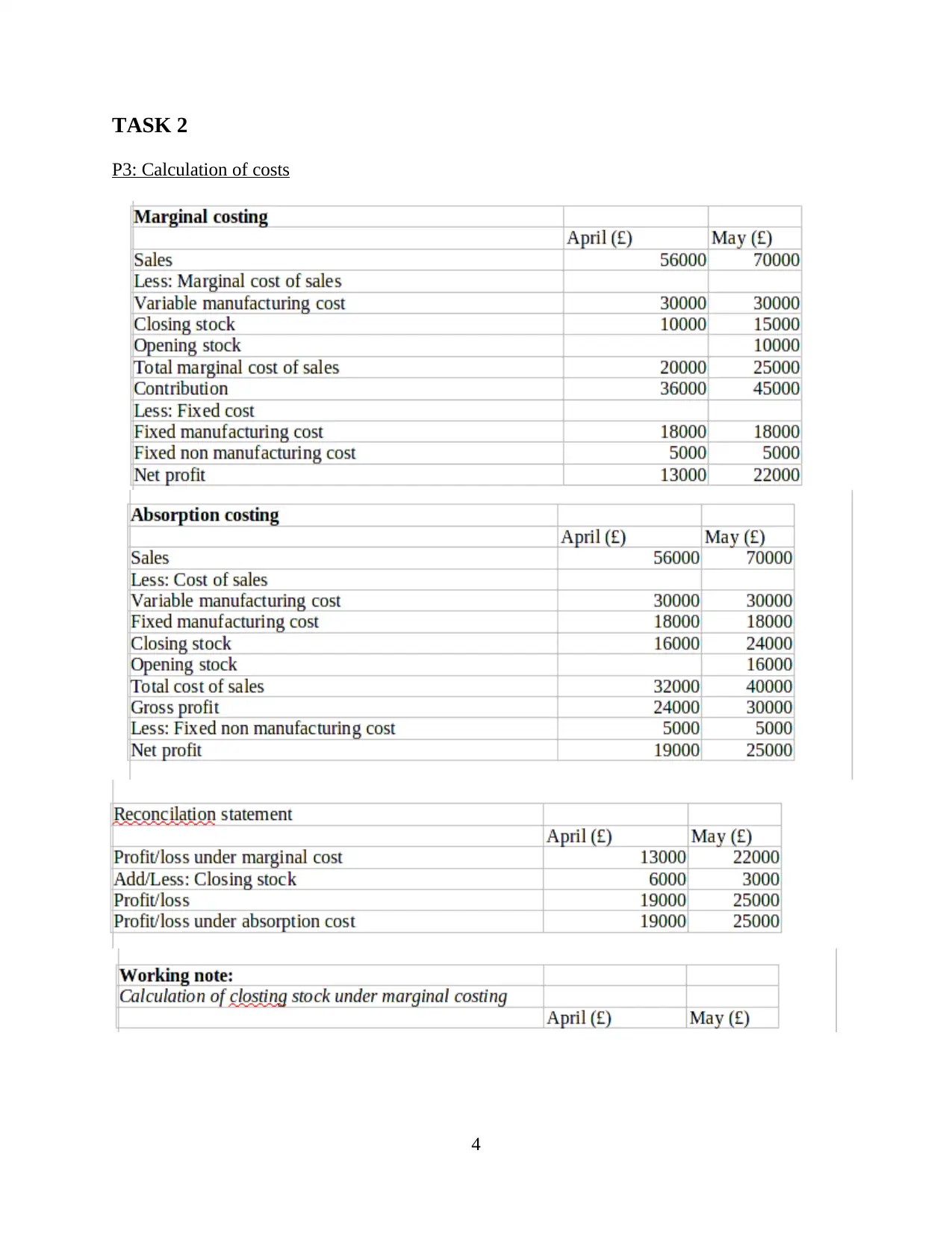

TASK 2

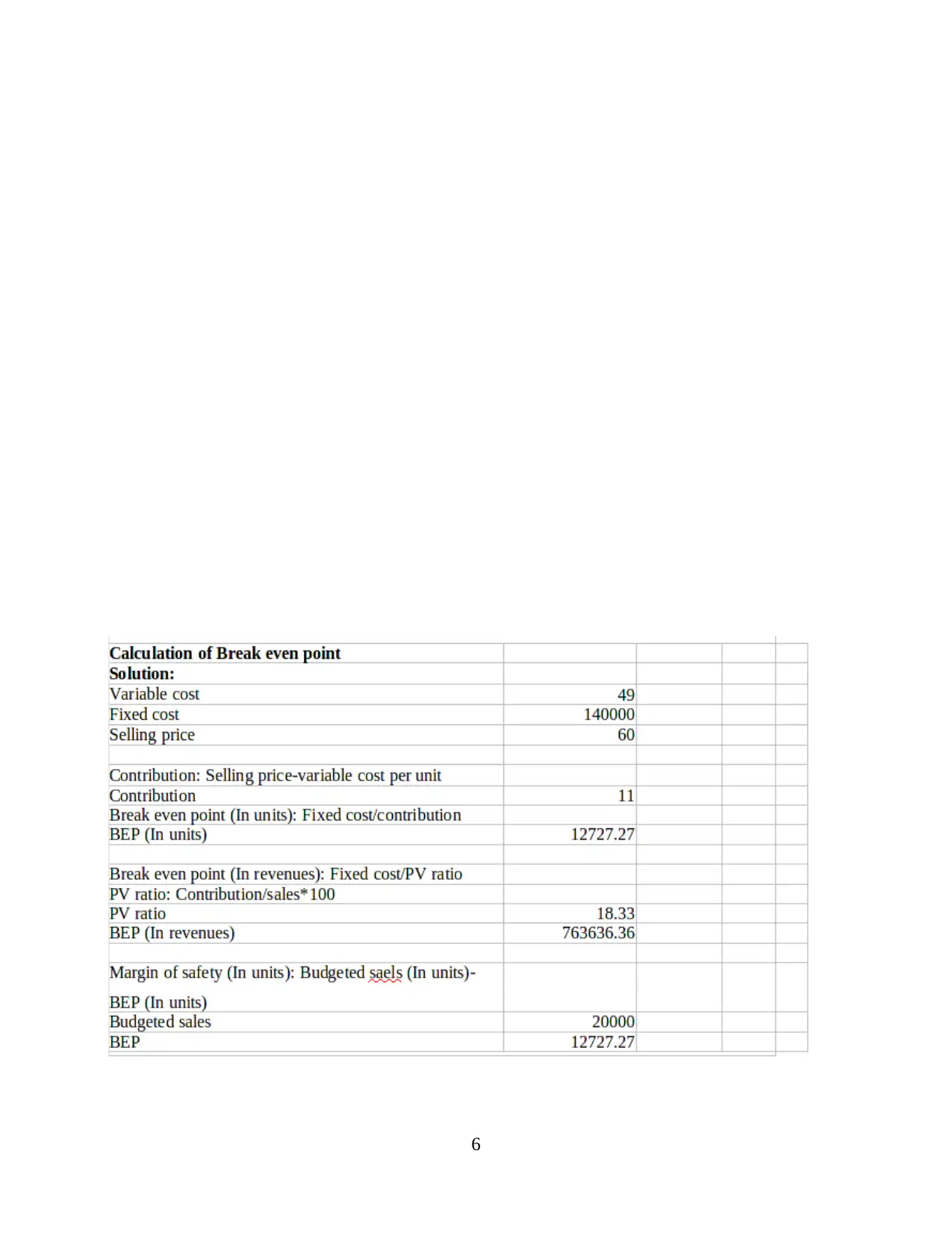

P3: Calculation of costs

4

P3: Calculation of costs

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

6

It is necessary that the appropriate assessment of the different type of costs is made

within an organization. For this purpose, the important techniques are required to be used. These

techniques are explained as follows-

Marginal Costing-

It is a section in which the variable cost is charged from the divisions and the fixed cost is

written off as against to the contribution (Kumarasinghe and Haleem, 2020). Hence, it might be

stated that this special method is helpful in ensuring that the right purpose of the profits can be

made in the company which will thus support it a lot in the future. Hence, it is required that the

managers of ASDA are able to ensure that they can make the right utilisation of this method for

determining the profitability level.

Advantages-

It is quite simple to use and therefore in this way the people in the organization are able

to easily learn about its application. Thus, it can be easily applied within the organization

and its processes.

It is helpful for the purpose of decision-making in the organization and therefore this can

lead towards better decisions. Thus, the managers can take the right decisions which will

thus help them a lot.

Disadvantages-

When the use of this technique is made, the segregation of the various types of overheads

in the organization becomes difficult.

As this technique excludes the fixed overheads from the costs it can therefore lead

towards wrong conclusions.

Absorption Costing-

It is a system by which the classification of the costs can be made and hence the right

course of activities are to be taken for further determination (Legaspi, 2020). Therefore, it can be

stated that the right use of this particular system has to be created so that the business of the

appropriate needs and wants can be made quite effectively and efficiently. It will thus lead

towards improvement of the level of net income. For the managers of ASDA it is important that

7

within an organization. For this purpose, the important techniques are required to be used. These

techniques are explained as follows-

Marginal Costing-

It is a section in which the variable cost is charged from the divisions and the fixed cost is

written off as against to the contribution (Kumarasinghe and Haleem, 2020). Hence, it might be

stated that this special method is helpful in ensuring that the right purpose of the profits can be

made in the company which will thus support it a lot in the future. Hence, it is required that the

managers of ASDA are able to ensure that they can make the right utilisation of this method for

determining the profitability level.

Advantages-

It is quite simple to use and therefore in this way the people in the organization are able

to easily learn about its application. Thus, it can be easily applied within the organization

and its processes.

It is helpful for the purpose of decision-making in the organization and therefore this can

lead towards better decisions. Thus, the managers can take the right decisions which will

thus help them a lot.

Disadvantages-

When the use of this technique is made, the segregation of the various types of overheads

in the organization becomes difficult.

As this technique excludes the fixed overheads from the costs it can therefore lead

towards wrong conclusions.

Absorption Costing-

It is a system by which the classification of the costs can be made and hence the right

course of activities are to be taken for further determination (Legaspi, 2020). Therefore, it can be

stated that the right use of this particular system has to be created so that the business of the

appropriate needs and wants can be made quite effectively and efficiently. It will thus lead

towards improvement of the level of net income. For the managers of ASDA it is important that

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the use of this particular method is made so that the attainment of the future goals and objectives

can be carried out.

Advantages-

The analysis of the level of overheads within the organization can be made appropriately

when the use of this particular technique is made. Thus, the control on the level of

overheads can be kept in this way which will be quite useful in controlling the overheads

in an appropriate manner.

Through the use of this technique the apportionment and allocation of the overheads can

be done in a much better way. Thus, the identification of the overheads of the various

departments in the organization can be carried out in a right manner.

Disadvantages-

It is not useful for the purpose of decision-making and therefore in this way it can create

an impact on the organizations.

The highlighting of certain costs is not done when this technique is used and therefore

this affects the organizations.

Therefore, it can be stated that the use of both of these techniques is quite

accommodating for the specific intention of taking of the right decisions which are related with

enhancing the general division of efficiency and effectiveness in a better manner. Therefore, the

managers of ASDA should be able to ensure that they must be able to appropriately use these

particular techniques which will help them in identifying the future course of decision which has

to be taken. This will help in targeting a particular increase in the general level of net income in

the future for the organization.

TASK 3

P4: Planning tools for Budgetary Control

Budgetary Control is a technique in which the preparation of the Budgets is done so that

the necessary course of action can be taken. Therefore, in this way it is helpful for the

management of the funds within the organization. The managers of ASDA should make its use

for ensuring that the use of forecasts can be made correctly and appropriately.

Different types of Budgets can be prepared within the organizations. An explanation of

some of these Budgets can be provided as follows-

8

can be carried out.

Advantages-

The analysis of the level of overheads within the organization can be made appropriately

when the use of this particular technique is made. Thus, the control on the level of

overheads can be kept in this way which will be quite useful in controlling the overheads

in an appropriate manner.

Through the use of this technique the apportionment and allocation of the overheads can

be done in a much better way. Thus, the identification of the overheads of the various

departments in the organization can be carried out in a right manner.

Disadvantages-

It is not useful for the purpose of decision-making and therefore in this way it can create

an impact on the organizations.

The highlighting of certain costs is not done when this technique is used and therefore

this affects the organizations.

Therefore, it can be stated that the use of both of these techniques is quite

accommodating for the specific intention of taking of the right decisions which are related with

enhancing the general division of efficiency and effectiveness in a better manner. Therefore, the

managers of ASDA should be able to ensure that they must be able to appropriately use these

particular techniques which will help them in identifying the future course of decision which has

to be taken. This will help in targeting a particular increase in the general level of net income in

the future for the organization.

TASK 3

P4: Planning tools for Budgetary Control

Budgetary Control is a technique in which the preparation of the Budgets is done so that

the necessary course of action can be taken. Therefore, in this way it is helpful for the

management of the funds within the organization. The managers of ASDA should make its use

for ensuring that the use of forecasts can be made correctly and appropriately.

Different types of Budgets can be prepared within the organizations. An explanation of

some of these Budgets can be provided as follows-

8

Cash Budget-

It is a Budget in which the insure of the cash receipts and expending is made. It is

therefore necessary that its preparation can be done so that the social control of the cash can be

done in a correct manner (Lueg, 2020). Therefore, it is important for the management of ASDA

that they make the use of this budget.

Advantages-

Through its preparation, the cash can be managed so that the decisions can be taken in

quite an appropriate way.

This budget is required to be prepared so that the necessary control on the cash receipts

and expenditures can be kept.

Disadvantages-

Its preparation can affect the level of flexibility in the organizations which is related with

cash expenditures.

Its preparation is quite time-consuming and costly and therefore in this way this affects

the organizations.

Sales Budget-

It is a forecast of the sales of a particular organization over a specific period of time. Therefore, it

is quite important that the management of the sales revenues of the organization can be done

through making an appropriate use of this particular budget (Massicotte and Henri, 2020). In the

context of ASDAit is necessary that its preparation should be made for ensuring a right

management of the sales effectively and efficiently.

Advantages-

It is a Budget through which the comparison of the actual sales data with the previous

sales data can be carried out. This can therefore help the management to be able to draw

conclusions and recommendations which are useful.

It is a Budget through which the determination of the actions to be taken for the future

can be done which will be useful for the purpose of taking the right decisions effectively

and efficiently.

Disadvantages-

A Sales Budget which is prepared by the higher authorities may not be acceptable to all

the people in the organization. Thus, in this way it can impact the level of operations.

9

It is a Budget in which the insure of the cash receipts and expending is made. It is

therefore necessary that its preparation can be done so that the social control of the cash can be

done in a correct manner (Lueg, 2020). Therefore, it is important for the management of ASDA

that they make the use of this budget.

Advantages-

Through its preparation, the cash can be managed so that the decisions can be taken in

quite an appropriate way.

This budget is required to be prepared so that the necessary control on the cash receipts

and expenditures can be kept.

Disadvantages-

Its preparation can affect the level of flexibility in the organizations which is related with

cash expenditures.

Its preparation is quite time-consuming and costly and therefore in this way this affects

the organizations.

Sales Budget-

It is a forecast of the sales of a particular organization over a specific period of time. Therefore, it

is quite important that the management of the sales revenues of the organization can be done

through making an appropriate use of this particular budget (Massicotte and Henri, 2020). In the

context of ASDAit is necessary that its preparation should be made for ensuring a right

management of the sales effectively and efficiently.

Advantages-

It is a Budget through which the comparison of the actual sales data with the previous

sales data can be carried out. This can therefore help the management to be able to draw

conclusions and recommendations which are useful.

It is a Budget through which the determination of the actions to be taken for the future

can be done which will be useful for the purpose of taking the right decisions effectively

and efficiently.

Disadvantages-

A Sales Budget which is prepared by the higher authorities may not be acceptable to all

the people in the organization. Thus, in this way it can impact the level of operations.

9

Its preparation is quite time-consuming and costly. Therefore, in this way it affects the

organizations.

Master Budget-

It is a Budget which is prepared for the purpose of managing the overall level of needs

and requirements of the organizations which are related with the Budgeting process (Mayndarto

and Agustine, 2021). Its preparation helps the firms in keeping a tight control on their expenses

and ensuring that the decisions can be taken smoothly.

Advantages-

It is a budget which details the estimations in a proper manner within the organizations.

Therefore this is helpful for the firms.

This budget is quite useful for ensuring that the management of the level of expenditures

can be made in the organizations. In this way it can help the organization in a proper way.

Disadvantages-

This budget does not offers specialization and therefore it is difficult to analyse and

interpret a particular area through its use.

This budget is quite difficult to read and update. Therefore, in this way it affects the

different types of organizations.

TASK 4

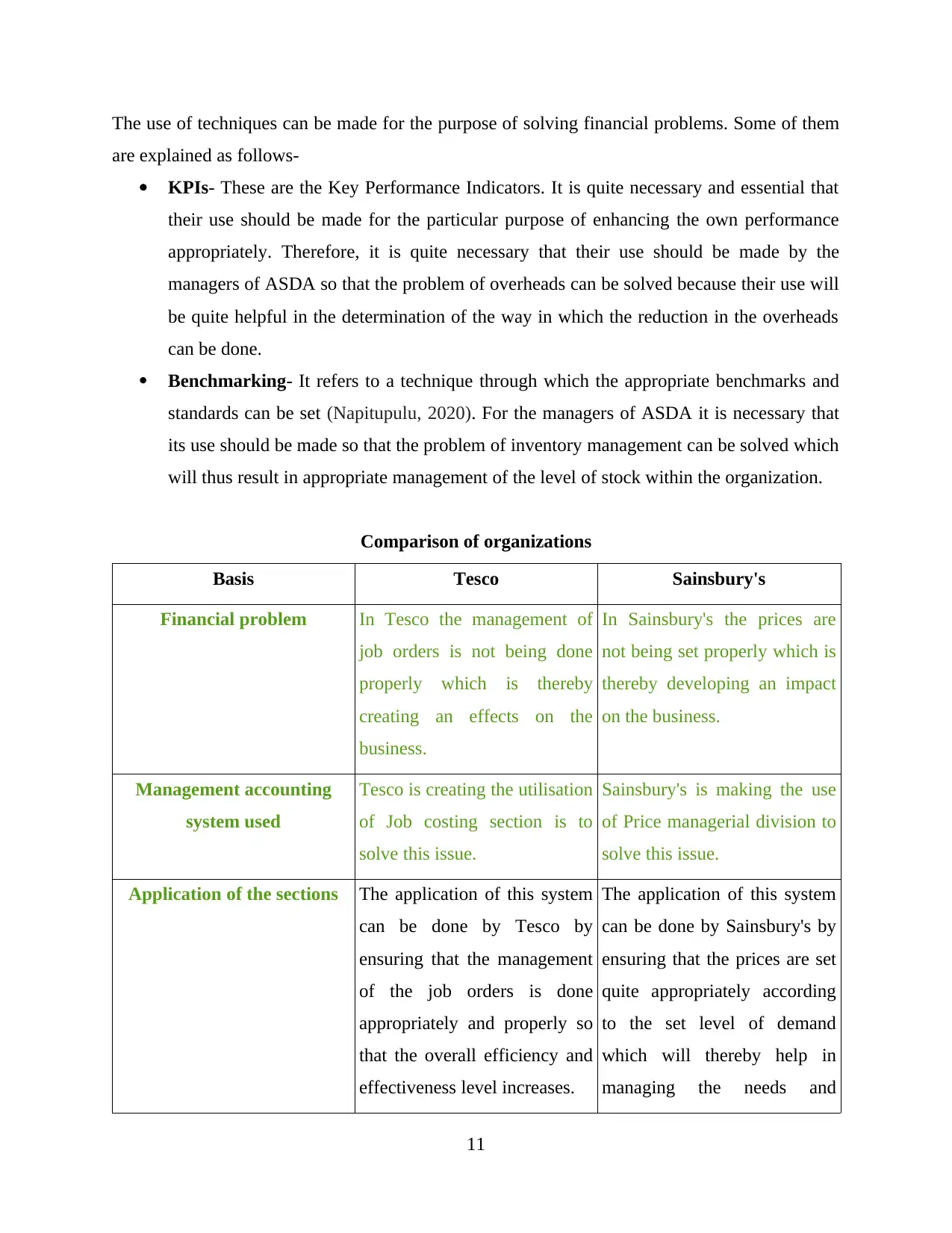

P5: Comparison of organizations

Financial problem- This refers to a condition in which the business faces the financial

trouble and therefore it creates an impact on its position of funds. Such as other management

such as, ASDA also faces financial issues. Some of the problems that are being faced by it are as

follows-

Increase in overheads- The overheads of the organization have been increasing

constantly and therefore this is increasing the costs and lowering the level of profits.

Thus, this is affecting the financial problem of the organizations.

Improper inventory management- The inventory products in the business are not being

maintained as appropriately and thus this is developing its effects on the firm. Therefore,

this is impacting the financial situation of the organization.

10

organizations.

Master Budget-

It is a Budget which is prepared for the purpose of managing the overall level of needs

and requirements of the organizations which are related with the Budgeting process (Mayndarto

and Agustine, 2021). Its preparation helps the firms in keeping a tight control on their expenses

and ensuring that the decisions can be taken smoothly.

Advantages-

It is a budget which details the estimations in a proper manner within the organizations.

Therefore this is helpful for the firms.

This budget is quite useful for ensuring that the management of the level of expenditures

can be made in the organizations. In this way it can help the organization in a proper way.

Disadvantages-

This budget does not offers specialization and therefore it is difficult to analyse and

interpret a particular area through its use.

This budget is quite difficult to read and update. Therefore, in this way it affects the

different types of organizations.

TASK 4

P5: Comparison of organizations

Financial problem- This refers to a condition in which the business faces the financial

trouble and therefore it creates an impact on its position of funds. Such as other management

such as, ASDA also faces financial issues. Some of the problems that are being faced by it are as

follows-

Increase in overheads- The overheads of the organization have been increasing

constantly and therefore this is increasing the costs and lowering the level of profits.

Thus, this is affecting the financial problem of the organizations.

Improper inventory management- The inventory products in the business are not being

maintained as appropriately and thus this is developing its effects on the firm. Therefore,

this is impacting the financial situation of the organization.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The use of techniques can be made for the purpose of solving financial problems. Some of them

are explained as follows-

KPIs- These are the Key Performance Indicators. It is quite necessary and essential that

their use should be made for the particular purpose of enhancing the own performance

appropriately. Therefore, it is quite necessary that their use should be made by the

managers of ASDA so that the problem of overheads can be solved because their use will

be quite helpful in the determination of the way in which the reduction in the overheads

can be done.

Benchmarking- It refers to a technique through which the appropriate benchmarks and

standards can be set (Napitupulu, 2020). For the managers of ASDA it is necessary that

its use should be made so that the problem of inventory management can be solved which

will thus result in appropriate management of the level of stock within the organization.

Comparison of organizations

Basis Tesco Sainsbury's

Financial problem In Tesco the management of

job orders is not being done

properly which is thereby

creating an effects on the

business.

In Sainsbury's the prices are

not being set properly which is

thereby developing an impact

on the business.

Management accounting

system used

Tesco is creating the utilisation

of Job costing section is to

solve this issue.

Sainsbury's is making the use

of Price managerial division to

solve this issue.

Application of the sections The application of this system

can be done by Tesco by

ensuring that the management

of the job orders is done

appropriately and properly so

that the overall efficiency and

effectiveness level increases.

The application of this system

can be done by Sainsbury's by

ensuring that the prices are set

quite appropriately according

to the set level of demand

which will thereby help in

managing the needs and

11

are explained as follows-

KPIs- These are the Key Performance Indicators. It is quite necessary and essential that

their use should be made for the particular purpose of enhancing the own performance

appropriately. Therefore, it is quite necessary that their use should be made by the

managers of ASDA so that the problem of overheads can be solved because their use will

be quite helpful in the determination of the way in which the reduction in the overheads

can be done.

Benchmarking- It refers to a technique through which the appropriate benchmarks and

standards can be set (Napitupulu, 2020). For the managers of ASDA it is necessary that

its use should be made so that the problem of inventory management can be solved which

will thus result in appropriate management of the level of stock within the organization.

Comparison of organizations

Basis Tesco Sainsbury's

Financial problem In Tesco the management of

job orders is not being done

properly which is thereby

creating an effects on the

business.

In Sainsbury's the prices are

not being set properly which is

thereby developing an impact

on the business.

Management accounting

system used

Tesco is creating the utilisation

of Job costing section is to

solve this issue.

Sainsbury's is making the use

of Price managerial division to

solve this issue.

Application of the sections The application of this system

can be done by Tesco by

ensuring that the management

of the job orders is done

appropriately and properly so

that the overall efficiency and

effectiveness level increases.

The application of this system

can be done by Sainsbury's by

ensuring that the prices are set

quite appropriately according

to the set level of demand

which will thereby help in

managing the needs and

11

requirements.

From the above discussion, it can be stated that the managers of ASDA should find out

from the managers of Tesco and Sainsbury's and thus ensure that the suitable activities that are

taken for solving financial issues. Hence, the business of the organization can develop the use of

Cost accounting system to resolve the issues of overheads and Inventory management sections

to solve the issues of inventory. Therefore, in this way the company will be able to bring

smoothness in its level of operations and it will also be able to make sure that it can maintain its

financial health in the right way so that the goals and objectives in the future are attained.

CONCLUSION

From the above report, it can be concluded that Management Accounting termed to the

utilisation of the manner and tools by which the management quite suitably. Thus, for the

managers of an organization it becomes necessary that they use it for the purpose of taking of

various types of necessary decisions. Therefore, it is necessary that it should be used by the

managers of the organization so that the financial facts and information can be used to facilitate

decision-making. Thus, in this manner the business will be capable to ensure that they are

capable to increase the global section of efficiency and effectiveness in quite an suitable manner.

12

From the above discussion, it can be stated that the managers of ASDA should find out

from the managers of Tesco and Sainsbury's and thus ensure that the suitable activities that are

taken for solving financial issues. Hence, the business of the organization can develop the use of

Cost accounting system to resolve the issues of overheads and Inventory management sections

to solve the issues of inventory. Therefore, in this way the company will be able to bring

smoothness in its level of operations and it will also be able to make sure that it can maintain its

financial health in the right way so that the goals and objectives in the future are attained.

CONCLUSION

From the above report, it can be concluded that Management Accounting termed to the

utilisation of the manner and tools by which the management quite suitably. Thus, for the

managers of an organization it becomes necessary that they use it for the purpose of taking of

various types of necessary decisions. Therefore, it is necessary that it should be used by the

managers of the organization so that the financial facts and information can be used to facilitate

decision-making. Thus, in this manner the business will be capable to ensure that they are

capable to increase the global section of efficiency and effectiveness in quite an suitable manner.

12

REFERENCES

Books and Journals:

Alabdullah, T. T. Y. and Ahmed, E. R., 2020. Audit committee impact on corporate profitability

in Oman companies: an auditing and management accounting perspective. Riset

Akuntansi dan Keuangan Indonesia. 5(2). pp.121-128.

Alhatabat, Z., 2020. The impact of ERP system's adoption on management accounting practices

in the Jordanian manufacturing companies. International Journal of Business

Information Systems. 33(2). pp.267-284.

Amirbeyki Langroudi, H., Kordestani, G. and Reazei, F., 2020. Assessment of Management

Accounting Model for Sustainable Development. Journal of Management Accounting

and Auditing Knowledge. 9(33). pp.239-259.

Diab, A. A., 2020. The relationship between informality and the formal management accounting

and control process: a case study from Egypt. Academy of Accounting and Financial

Studies Journal. 24(4).

Dwirandra, A. A. N. B. and ASTIKA, I. B. P., 2020. Impact of Environmental Uncertainty, Trust

and Information Technology on User Behavior of Accounting Information Systems. The

Journal of Asian Finance, Economics, and Business. 7(12). pp.1215-1224.

Golyagina, A. and Valuckas, D., 2020. Boundary-work in management accounting: The case of

hybrid professionalism. The British Accounting Review. 52(2). p.100841.

Hutahayan, B., 2020. The mediating role of human capital and management accounting

information system in the relationship between innovation strategy and internal process

performance and the impact on corporate financial performance. Benchmarking: An

International Journal.

Isoh, A. V. N., 2020. Relationship between accounting benefits and ERP user satisfaction in the

context of the fourth industrial revolution. International Journal of Scientific Research

and Management (IJSRM). 8(2).

Johnstone, L., 2020. A systematic analysis of environmental management systems in SMEs:

Possible research directions from a management accounting and control stance. Journal

of Cleaner Production. 244. p.118802.

Kumarasinghe, W. S. L. and Haleem, A., 2020. The impact of digitalization on business models

with special reference to management accounting in small and medium enterprises in

Colombo district.

Legaspi, J. L. R., 2020. What business strategy does and what management accounting is

pursuing: A logistic regression analysis.

Lueg, R., 2020. Customer accounting and free return policies of retailers.

Massicotte, S. and Henri, J. F., 2020. The use of management accounting information by boards

of directors to oversee strategy implementation. The British Accounting Review,

p.100953.

Mayndarto, E. C. and Agustine, Y., 2021. The Efffect of Environmental Management

Accounting, Environmental Strategy on Environmental Performance and Financial

Performance Moderated by Managerial Commitment. International Journal of Science,

Technology & Management. 2(1). pp.112-119.

Napitupulu, I. H., 2020. Internal control, manager’s competency, management accounting

information systems and good corporate governance: Evidence from rural banks in

Indonesia. Global Business Review. p.0972150920919845.

13

Books and Journals:

Alabdullah, T. T. Y. and Ahmed, E. R., 2020. Audit committee impact on corporate profitability

in Oman companies: an auditing and management accounting perspective. Riset

Akuntansi dan Keuangan Indonesia. 5(2). pp.121-128.

Alhatabat, Z., 2020. The impact of ERP system's adoption on management accounting practices

in the Jordanian manufacturing companies. International Journal of Business

Information Systems. 33(2). pp.267-284.

Amirbeyki Langroudi, H., Kordestani, G. and Reazei, F., 2020. Assessment of Management

Accounting Model for Sustainable Development. Journal of Management Accounting

and Auditing Knowledge. 9(33). pp.239-259.

Diab, A. A., 2020. The relationship between informality and the formal management accounting

and control process: a case study from Egypt. Academy of Accounting and Financial

Studies Journal. 24(4).

Dwirandra, A. A. N. B. and ASTIKA, I. B. P., 2020. Impact of Environmental Uncertainty, Trust

and Information Technology on User Behavior of Accounting Information Systems. The

Journal of Asian Finance, Economics, and Business. 7(12). pp.1215-1224.

Golyagina, A. and Valuckas, D., 2020. Boundary-work in management accounting: The case of

hybrid professionalism. The British Accounting Review. 52(2). p.100841.

Hutahayan, B., 2020. The mediating role of human capital and management accounting

information system in the relationship between innovation strategy and internal process

performance and the impact on corporate financial performance. Benchmarking: An

International Journal.

Isoh, A. V. N., 2020. Relationship between accounting benefits and ERP user satisfaction in the

context of the fourth industrial revolution. International Journal of Scientific Research

and Management (IJSRM). 8(2).

Johnstone, L., 2020. A systematic analysis of environmental management systems in SMEs:

Possible research directions from a management accounting and control stance. Journal

of Cleaner Production. 244. p.118802.

Kumarasinghe, W. S. L. and Haleem, A., 2020. The impact of digitalization on business models

with special reference to management accounting in small and medium enterprises in

Colombo district.

Legaspi, J. L. R., 2020. What business strategy does and what management accounting is

pursuing: A logistic regression analysis.

Lueg, R., 2020. Customer accounting and free return policies of retailers.

Massicotte, S. and Henri, J. F., 2020. The use of management accounting information by boards

of directors to oversee strategy implementation. The British Accounting Review,

p.100953.

Mayndarto, E. C. and Agustine, Y., 2021. The Efffect of Environmental Management

Accounting, Environmental Strategy on Environmental Performance and Financial

Performance Moderated by Managerial Commitment. International Journal of Science,

Technology & Management. 2(1). pp.112-119.

Napitupulu, I. H., 2020. Internal control, manager’s competency, management accounting

information systems and good corporate governance: Evidence from rural banks in

Indonesia. Global Business Review. p.0972150920919845.

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

14

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.