Management Accounting Systems and Techniques

21 Pages4404 Words58 Views

Added on 2023-01-04

About This Document

This study focuses on management accounting systems and techniques prevalent in the UK. It explores different methods of management accounting reporting, techniques of cost analysis, and tools used in management accounting. The study aims to provide insights into how these systems and techniques can be implemented to improve financial performance.

Management Accounting Systems and Techniques

Added on 2023-01-04

ShareRelated Documents

MANAGEMENT

ACCOUNTING SYSTEMS

AND TECHNIQUES

ACCOUNTING SYSTEMS

AND TECHNIQUES

Table of Contents

INTRODUCTION...........................................................................................................................3

P1 Management Accounting Systems.............................................................................................3

P2 Different methods of Management Accounting Reporting..........................................5

P3 Techniques of cost analysis........................................................................................................6

P4 Tools and techniques used in management accounting............................................................10

P5 Comparison of companies responding to financial problems using management accounting.12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

P1 Management Accounting Systems.............................................................................................3

P2 Different methods of Management Accounting Reporting..........................................5

P3 Techniques of cost analysis........................................................................................................6

P4 Tools and techniques used in management accounting............................................................10

P5 Comparison of companies responding to financial problems using management accounting.12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

The study focuses on management accounting and its systems prevalent in UK. Management Accounting refers to

the accounting system used by business managers for preparation of reports related to business activities and

analysing, interpreting, measuring, identifying the goals to be achieved by the business. The study will relate to the

management accounting techniques in UK firm and its implementation to better financial performance. It will focus

light on various planning tools and techniques to solve financial problems existing within the company.

P1 Management Accounting Systems

Management accounting is the accounting system used by business managers to prepare financial reports, rectifying

the errors and identifying with analyzation the best method to achieve the financial goals (Alborov and et.al.,

2017). It helps managers in decision-making of short term and long-term goals. It helps in making decisions like:

a) Forecasting: It involves decision-making in terms of matters like whether to buy an equipment or not,

whether it would be correct to diversify the business and if it would be correct to partner in a company or a

merger.

b) It keeps in account what to buy keeping in mind the operational costs and budget strategy.

c) Cash flows can be judged as to what amount should go to each section within the organisation and budget

planning can be done accordingly.

d) It helps understand variances in performance of the company as to what goal was set and how much is

achieved plus where the strategy was lacking.

e) The rate of return is also analysed as to which project would be best suiting for investment.

Requirements of different types of management accounting

There are five types of broad-based accounting:

a) Margin Analysis: Managerial accounting uses incremental analysis on production and thus gauges the

break-even point to calculate the minimum production required to achieve the investment cost of the

business (Burritt and et.al.,2019). In context of Capital joinery, the break even will help it know when the

business has covered up its initial investment cost and the minimum production required to reach the

required stage. Company can accordingly allocate its production budget and also have an idea of EOQ

which is Economic Order Quantity. This will help to order the right amount of inventory required for further

production thus saving up inventory costs. The increment of unit after break even will decide success and

profit for the business.

b) Constraint Analysis: The constraints occurring within sales or production and its reflection on cash flow,

profit and revenue is estimated by management accounting. Capital Joinery will be able to find out the

section it may be lacking in by managerial accounting finding out the key aspect (Alborov and et.al., 2017).

The study focuses on management accounting and its systems prevalent in UK. Management Accounting refers to

the accounting system used by business managers for preparation of reports related to business activities and

analysing, interpreting, measuring, identifying the goals to be achieved by the business. The study will relate to the

management accounting techniques in UK firm and its implementation to better financial performance. It will focus

light on various planning tools and techniques to solve financial problems existing within the company.

P1 Management Accounting Systems

Management accounting is the accounting system used by business managers to prepare financial reports, rectifying

the errors and identifying with analyzation the best method to achieve the financial goals (Alborov and et.al.,

2017). It helps managers in decision-making of short term and long-term goals. It helps in making decisions like:

a) Forecasting: It involves decision-making in terms of matters like whether to buy an equipment or not,

whether it would be correct to diversify the business and if it would be correct to partner in a company or a

merger.

b) It keeps in account what to buy keeping in mind the operational costs and budget strategy.

c) Cash flows can be judged as to what amount should go to each section within the organisation and budget

planning can be done accordingly.

d) It helps understand variances in performance of the company as to what goal was set and how much is

achieved plus where the strategy was lacking.

e) The rate of return is also analysed as to which project would be best suiting for investment.

Requirements of different types of management accounting

There are five types of broad-based accounting:

a) Margin Analysis: Managerial accounting uses incremental analysis on production and thus gauges the

break-even point to calculate the minimum production required to achieve the investment cost of the

business (Burritt and et.al.,2019). In context of Capital joinery, the break even will help it know when the

business has covered up its initial investment cost and the minimum production required to reach the

required stage. Company can accordingly allocate its production budget and also have an idea of EOQ

which is Economic Order Quantity. This will help to order the right amount of inventory required for further

production thus saving up inventory costs. The increment of unit after break even will decide success and

profit for the business.

b) Constraint Analysis: The constraints occurring within sales or production and its reflection on cash flow,

profit and revenue is estimated by management accounting. Capital Joinery will be able to find out the

section it may be lacking in by managerial accounting finding out the key aspect (Alborov and et.al., 2017).

It may be production where higher technique may be required to manufacture joinery items. Company will

have to bring in superior technology for this and hence accordingly a budget allocation will have to be

made. This will help company in removing constraints and improve production and revenue. Cash flow will

get affected on both sides as superior technology will demand more investment but it will be balanced by

sales increase due to better product quality and profit may come up after some time.

c) Capital Budgeting: The investment of a certain amount of capital on a project, equipment etc. is decided

and factors of time value of money and rate of return are taken into consideration. It also reviews the

demand of products and services and sets a financial chart for their purchase (Honggowati and et.al., 2017).

Capital Joinery will be able to make decision on project or investment on equipment which will be suitable

for the company to put their finances in. Methods used in management accounting of time value of money

and rate of return will help in making long term and short-term decisions. The demand of products from

suppliers and customers will also get in picture for the company and accordingly production can be done

thus saving excess costs.

d) Trend Analysis: Factors like historical pricing, sales volumes, demographic trends of customers,

geographical locations are taken into consideration. Capital Joinery can hugely benefit from these factors as

the demand and supply chart with revenue generation all will come up in statistical terms thus making it

easy to allocate budget for varied products according to the demand per se.

e) Product Costing: It helps in determining the cost of product making involving factor of raw materials,

production costs, overhead costs etc. Costs associated with inventory and their storage are also made

according to inventory taking up per square foot space. Capital Joinery through management accounting

will be able to price its products better after calculating all the production, material and overhead costs.

Excess costs in inventory management will too be accounted helping in gauging cash flow better.

P2 Different methods of Management Accounting Reporting

Management Accounting is reported in the following ways:

a) Budget Reporting: Budget consists of all the company’s earnings and expenditures upcoming in a

financial year. The various sections of organisation viz. marketing, HR, systems, finance are covered up

in it. Allotment of money is done seeing the previous budget allocated, the response achieved through it

and the current demands of the organisation (Burritt and et.al.,2019). A company tries to achieve its

goals in staying within the budgeted norms. Seeing the circumstances change in future, usually a

separate provision is added in the budget. Capital Joinery will get pre-estimate of how much to allocate

finance in which section, cost cutting can take place where managers feel excess amount is being used.

b) Account Receivables Report: An organisation has to extend credit in some orders as every order does

not generate instant payment. This is booked as account receivables in which money is pending for the

have to bring in superior technology for this and hence accordingly a budget allocation will have to be

made. This will help company in removing constraints and improve production and revenue. Cash flow will

get affected on both sides as superior technology will demand more investment but it will be balanced by

sales increase due to better product quality and profit may come up after some time.

c) Capital Budgeting: The investment of a certain amount of capital on a project, equipment etc. is decided

and factors of time value of money and rate of return are taken into consideration. It also reviews the

demand of products and services and sets a financial chart for their purchase (Honggowati and et.al., 2017).

Capital Joinery will be able to make decision on project or investment on equipment which will be suitable

for the company to put their finances in. Methods used in management accounting of time value of money

and rate of return will help in making long term and short-term decisions. The demand of products from

suppliers and customers will also get in picture for the company and accordingly production can be done

thus saving excess costs.

d) Trend Analysis: Factors like historical pricing, sales volumes, demographic trends of customers,

geographical locations are taken into consideration. Capital Joinery can hugely benefit from these factors as

the demand and supply chart with revenue generation all will come up in statistical terms thus making it

easy to allocate budget for varied products according to the demand per se.

e) Product Costing: It helps in determining the cost of product making involving factor of raw materials,

production costs, overhead costs etc. Costs associated with inventory and their storage are also made

according to inventory taking up per square foot space. Capital Joinery through management accounting

will be able to price its products better after calculating all the production, material and overhead costs.

Excess costs in inventory management will too be accounted helping in gauging cash flow better.

P2 Different methods of Management Accounting Reporting

Management Accounting is reported in the following ways:

a) Budget Reporting: Budget consists of all the company’s earnings and expenditures upcoming in a

financial year. The various sections of organisation viz. marketing, HR, systems, finance are covered up

in it. Allotment of money is done seeing the previous budget allocated, the response achieved through it

and the current demands of the organisation (Burritt and et.al.,2019). A company tries to achieve its

goals in staying within the budgeted norms. Seeing the circumstances change in future, usually a

separate provision is added in the budget. Capital Joinery will get pre-estimate of how much to allocate

finance in which section, cost cutting can take place where managers feel excess amount is being used.

b) Account Receivables Report: An organisation has to extend credit in some orders as every order does

not generate instant payment. This is booked as account receivables in which money is pending for the

business. Management accounting helps to find out the clients in this process who are yet to make

payment as well as the defaulters. Too many defaulters can affect cash flow and credit norms need to be

changed for maintaining working capital. Capital Joinery must be having pending payments to be

received, thus it will help them keep a track of distributors and suppliers who are yet to make payment.

It will also help them track defaulters and change their credit terms accordingly.

c) Cost managerial reports: It involves chalking out all the costs associated with production such as raw

materials, labour costs, overhead costs etc. and after their summation divide by the total quantity

produced (Honggowati and et.al., 2017). It helps the company in pricing of the products to its suppliers

with a profit margin. It helps in thus determining selling price for the company and a record of costs

involved. Capital Joinery will be benefitted by maintaining a cost book in which all the summation of

goods manufactured will be there. It can therefore price its goods and profit margin accordingly to the

market conditions. Inventory costs are also then known and help manage the next batch of inventory

accordingly.

d) Performance reports: In the end, performance of every department is measured through accounting

methods. It is seen which department has progressed from the previous year or quarter and an analysis is

done where the department is lacking. Accordingly, the measures are taken for improvement in key

areas (Hiebl and Richter, 2018). Capital Joinery will be able to gauge its budget allocation success for

each department and the key indicators of performance as well as the areas where company has not been

able to reach its goals or if more budget needs to be allocated to a particular stream.

e) Other Managerial Accounting Reports: Order information consisting report, reports on project,

analysis of competitors in the market are the other managerial accounting reports from which a business

can benefit from. Capital Joinery can get detailed specific information on how much order and purchase

cost has gone per order, which project has given a better rate of return and the costs involved initially.

Analysis of other competitors performing in the market, their profit margins and selling prices also will

help the company build a competitive strategy in the market.

P3 Techniques of cost analysis

Marginal Costing

Marginal cost is the change in cost which occurs when producing an incremental unit in production. It is the cost of

producing an extra unit after company has achieved break-even. Marginal cost is used to judge the impact of

variable costs on the production. It does not consider the fixed costs. It involves expenses of direct labour, direct

expenses, direct material and variable overheads.

payment as well as the defaulters. Too many defaulters can affect cash flow and credit norms need to be

changed for maintaining working capital. Capital Joinery must be having pending payments to be

received, thus it will help them keep a track of distributors and suppliers who are yet to make payment.

It will also help them track defaulters and change their credit terms accordingly.

c) Cost managerial reports: It involves chalking out all the costs associated with production such as raw

materials, labour costs, overhead costs etc. and after their summation divide by the total quantity

produced (Honggowati and et.al., 2017). It helps the company in pricing of the products to its suppliers

with a profit margin. It helps in thus determining selling price for the company and a record of costs

involved. Capital Joinery will be benefitted by maintaining a cost book in which all the summation of

goods manufactured will be there. It can therefore price its goods and profit margin accordingly to the

market conditions. Inventory costs are also then known and help manage the next batch of inventory

accordingly.

d) Performance reports: In the end, performance of every department is measured through accounting

methods. It is seen which department has progressed from the previous year or quarter and an analysis is

done where the department is lacking. Accordingly, the measures are taken for improvement in key

areas (Hiebl and Richter, 2018). Capital Joinery will be able to gauge its budget allocation success for

each department and the key indicators of performance as well as the areas where company has not been

able to reach its goals or if more budget needs to be allocated to a particular stream.

e) Other Managerial Accounting Reports: Order information consisting report, reports on project,

analysis of competitors in the market are the other managerial accounting reports from which a business

can benefit from. Capital Joinery can get detailed specific information on how much order and purchase

cost has gone per order, which project has given a better rate of return and the costs involved initially.

Analysis of other competitors performing in the market, their profit margins and selling prices also will

help the company build a competitive strategy in the market.

P3 Techniques of cost analysis

Marginal Costing

Marginal cost is the change in cost which occurs when producing an incremental unit in production. It is the cost of

producing an extra unit after company has achieved break-even. Marginal cost is used to judge the impact of

variable costs on the production. It does not consider the fixed costs. It involves expenses of direct labour, direct

expenses, direct material and variable overheads.

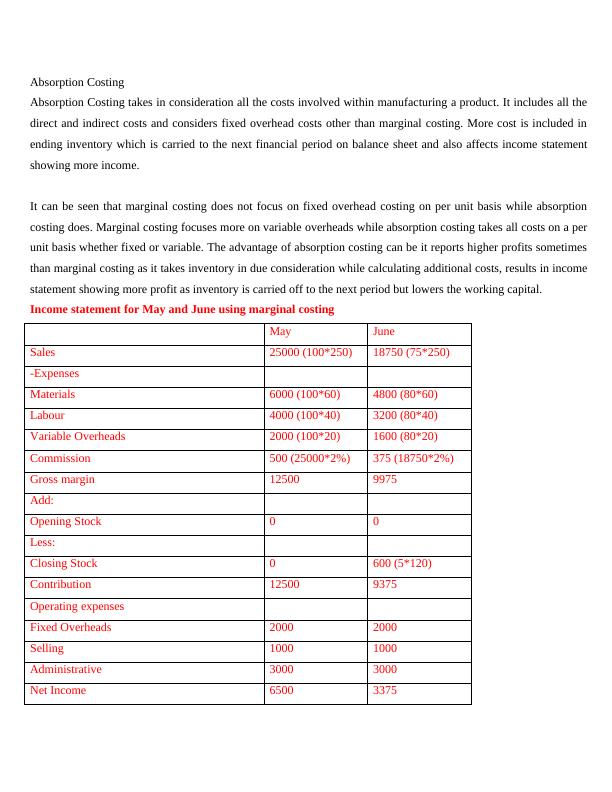

Absorption Costing

Absorption Costing takes in consideration all the costs involved within manufacturing a product. It includes all the

direct and indirect costs and considers fixed overhead costs other than marginal costing. More cost is included in

ending inventory which is carried to the next financial period on balance sheet and also affects income statement

showing more income.

It can be seen that marginal costing does not focus on fixed overhead costing on per unit basis while absorption

costing does. Marginal costing focuses more on variable overheads while absorption costing takes all costs on a per

unit basis whether fixed or variable. The advantage of absorption costing can be it reports higher profits sometimes

than marginal costing as it takes inventory in due consideration while calculating additional costs, results in income

statement showing more profit as inventory is carried off to the next period but lowers the working capital.

Income statement for May and June using marginal costing

May June

Sales 25000 (100*250) 18750 (75*250)

-Expenses

Materials 6000 (100*60) 4800 (80*60)

Labour 4000 (100*40) 3200 (80*40)

Variable Overheads 2000 (100*20) 1600 (80*20)

Commission 500 (25000*2%) 375 (18750*2%)

Gross margin 12500 9975

Add:

Opening Stock 0 0

Less:

Closing Stock 0 600 (5*120)

Contribution 12500 9375

Operating expenses

Fixed Overheads 2000 2000

Selling 1000 1000

Administrative 3000 3000

Net Income 6500 3375

Absorption Costing takes in consideration all the costs involved within manufacturing a product. It includes all the

direct and indirect costs and considers fixed overhead costs other than marginal costing. More cost is included in

ending inventory which is carried to the next financial period on balance sheet and also affects income statement

showing more income.

It can be seen that marginal costing does not focus on fixed overhead costing on per unit basis while absorption

costing does. Marginal costing focuses more on variable overheads while absorption costing takes all costs on a per

unit basis whether fixed or variable. The advantage of absorption costing can be it reports higher profits sometimes

than marginal costing as it takes inventory in due consideration while calculating additional costs, results in income

statement showing more profit as inventory is carried off to the next period but lowers the working capital.

Income statement for May and June using marginal costing

May June

Sales 25000 (100*250) 18750 (75*250)

-Expenses

Materials 6000 (100*60) 4800 (80*60)

Labour 4000 (100*40) 3200 (80*40)

Variable Overheads 2000 (100*20) 1600 (80*20)

Commission 500 (25000*2%) 375 (18750*2%)

Gross margin 12500 9975

Add:

Opening Stock 0 0

Less:

Closing Stock 0 600 (5*120)

Contribution 12500 9375

Operating expenses

Fixed Overheads 2000 2000

Selling 1000 1000

Administrative 3000 3000

Net Income 6500 3375

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting Systems and Techniqueslg...

|16

|4111

|65

Accounting for Management Decision | Reportlg...

|12

|2135

|17

Management Accounting: Types, Methods, and Benefitslg...

|17

|2691

|27

Management Accounting Systems and Techniqueslg...

|18

|4854

|45

Management Accounting Systems & Techniqueslg...

|17

|4852

|91

Management Accounting and Reporting Techniqueslg...

|22

|5891

|91