Management Accounting Techniques and Reporting for Toyota's Operations

VerifiedAdded on 2020/07/23

|17

|4444

|51

Report

AI Summary

This report provides a detailed analysis of Toyota's management accounting practices. It explores various management accounting systems, including financial accounting, cost accounting, auditing, and taxation, and their application within Toyota's operations. The report delves into different reporting techniques, such as budget reports, account receivable aging, and job cost reports, illustrating their importance in financial management. Furthermore, it examines the integration of these reporting methods within Toyota's business processes, highlighting their impact on decision-making and operational efficiency. The report also covers planning tools and budgetary control systems, including activity-based budgeting, along with their advantages and disadvantages. Through the use of marginal and absorption costing techniques, the report provides income statements and interprets the data for industrial operations. Overall, the report emphasizes how management accounting systems contribute to Toyota's sustainable success by resolving financial obstacles and improving resource utilization.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Determining different kinds of management accounting systems used by Toyota..........1

P 2. Different techniques used by Toyota for management accounting reporting.................3

M1. Analysing the importance of management accounting systems and its application in

Toyota.....................................................................................................................................5

D1. Integration of management accounting reporting in the business process of Toyota.....5

TASK 2............................................................................................................................................5

P3. Providing income statements on the basis of absorption and marginal costing techniques

................................................................................................................................................5

M 2 Application of management accounting techniques and facilitating the financial reporting

documents...............................................................................................................................8

D 2 Interpretation of the data for the range of industrial operations......................................8

TASK 3............................................................................................................................................8

P4. Determining various kinds of planning tools and budgetary control systems with their pros

and cons..................................................................................................................................8

P5. Adoption of management accounting systems to resolve the financial obstacles..........10

M3 Determining the use of planning tools as well as producing the forecasting budgets...11

M4 Resolving the financial issues through management accounting will help in sustainable

success of business...............................................................................................................11

D3 Implementation of planning tools which helps in solving financial problems for

sustainable success of Toyota...............................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Determining different kinds of management accounting systems used by Toyota..........1

P 2. Different techniques used by Toyota for management accounting reporting.................3

M1. Analysing the importance of management accounting systems and its application in

Toyota.....................................................................................................................................5

D1. Integration of management accounting reporting in the business process of Toyota.....5

TASK 2............................................................................................................................................5

P3. Providing income statements on the basis of absorption and marginal costing techniques

................................................................................................................................................5

M 2 Application of management accounting techniques and facilitating the financial reporting

documents...............................................................................................................................8

D 2 Interpretation of the data for the range of industrial operations......................................8

TASK 3............................................................................................................................................8

P4. Determining various kinds of planning tools and budgetary control systems with their pros

and cons..................................................................................................................................8

P5. Adoption of management accounting systems to resolve the financial obstacles..........10

M3 Determining the use of planning tools as well as producing the forecasting budgets...11

M4 Resolving the financial issues through management accounting will help in sustainable

success of business...............................................................................................................11

D3 Implementation of planning tools which helps in solving financial problems for

sustainable success of Toyota...............................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

To have successful business in the long run, there is the need to implement appropriate

management accounting systems in organisation. Thus, with the help of such reporting

techniques, business will be beneficial in making appropriate changes in the industrial activities,

decision making as well as in budgeting a planning for the future operations. In the present

report, there will be discussion based on the management accounting systems, reporting systems

as well as various planning tools for improving the industrial operations of Toyota Inc. The

report will also shed some light over performance appraisals on which they can make appropriate

changes as well as bring innovative ideas to enhance or motivate the workforce.

TASK 1

P1. Determining different kinds of management accounting systems used by Toyota

To improve the operational and financial efficiency of Toyota Inc., managers need to

implement various management accounting techniques. Hence, with the help of such techniques,

business operations will be very effective and produce the profitable returns. However, there

have been various kinds of accounting methods which are being used by the professionals such

as:

1

To have successful business in the long run, there is the need to implement appropriate

management accounting systems in organisation. Thus, with the help of such reporting

techniques, business will be beneficial in making appropriate changes in the industrial activities,

decision making as well as in budgeting a planning for the future operations. In the present

report, there will be discussion based on the management accounting systems, reporting systems

as well as various planning tools for improving the industrial operations of Toyota Inc. The

report will also shed some light over performance appraisals on which they can make appropriate

changes as well as bring innovative ideas to enhance or motivate the workforce.

TASK 1

P1. Determining different kinds of management accounting systems used by Toyota

To improve the operational and financial efficiency of Toyota Inc., managers need to

implement various management accounting techniques. Hence, with the help of such techniques,

business operations will be very effective and produce the profitable returns. However, there

have been various kinds of accounting methods which are being used by the professionals such

as:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

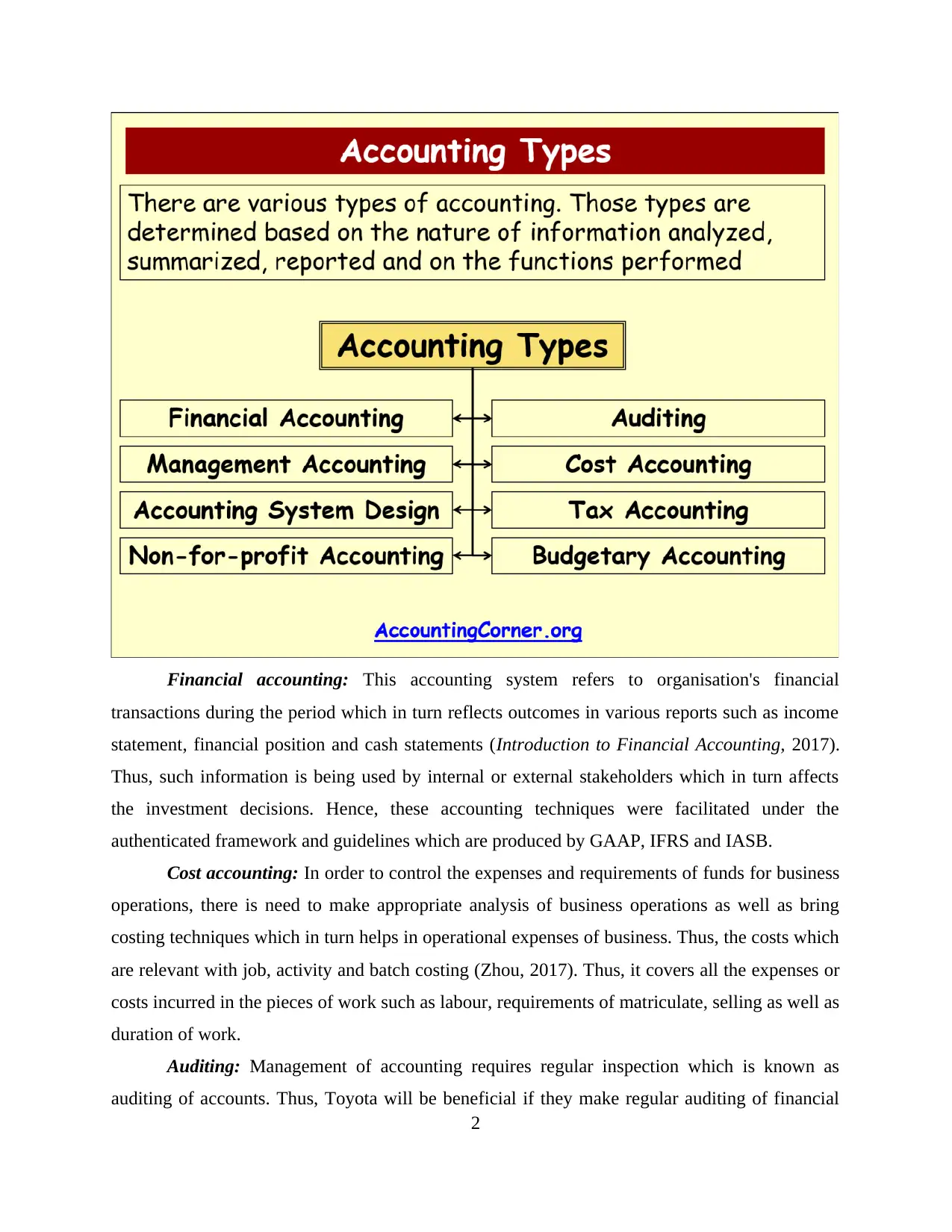

Financial accounting: This accounting system refers to organisation's financial

transactions during the period which in turn reflects outcomes in various reports such as income

statement, financial position and cash statements (Introduction to Financial Accounting, 2017).

Thus, such information is being used by internal or external stakeholders which in turn affects

the investment decisions. Hence, these accounting techniques were facilitated under the

authenticated framework and guidelines which are produced by GAAP, IFRS and IASB.

Cost accounting: In order to control the expenses and requirements of funds for business

operations, there is need to make appropriate analysis of business operations as well as bring

costing techniques which in turn helps in operational expenses of business. Thus, the costs which

are relevant with job, activity and batch costing (Zhou, 2017). Thus, it covers all the expenses or

costs incurred in the pieces of work such as labour, requirements of matriculate, selling as well as

duration of work.

Auditing: Management of accounting requires regular inspection which is known as

auditing of accounts. Thus, Toyota will be beneficial if they make regular auditing of financial

2

transactions during the period which in turn reflects outcomes in various reports such as income

statement, financial position and cash statements (Introduction to Financial Accounting, 2017).

Thus, such information is being used by internal or external stakeholders which in turn affects

the investment decisions. Hence, these accounting techniques were facilitated under the

authenticated framework and guidelines which are produced by GAAP, IFRS and IASB.

Cost accounting: In order to control the expenses and requirements of funds for business

operations, there is need to make appropriate analysis of business operations as well as bring

costing techniques which in turn helps in operational expenses of business. Thus, the costs which

are relevant with job, activity and batch costing (Zhou, 2017). Thus, it covers all the expenses or

costs incurred in the pieces of work such as labour, requirements of matriculate, selling as well as

duration of work.

Auditing: Management of accounting requires regular inspection which is known as

auditing of accounts. Thus, Toyota will be beneficial if they make regular auditing of financial

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reports with the help of accounting professionals as well as auditors of industry (Noordin,

Zainuddin and Mail, 2017). Hence, such operational techniques will help business in making

proper changes as well as suggesting effectual solutions to improves business operations.

Taxation: While planning operating business activities and earning adequate amount of

profitability, it is the prime responsibility of firm to make tax returns. However, in the UK, there

has been taxes levied over industries which are corporate taxes, custom duties and other

transactional taxes such as transportation and various central or state level taxes (Yudi and et.al.,

2016). Hence, these taxes are being collected by HMRC and legal authority of UK.

Budgets: To set an adequate amount of limit over the operational activities of

organisation, budgeting tools will be beneficial such as cash budget, sales and purchase as well

as various operational budgets. Thus, Toyota needs to implement prefect use of such managerial

accounting techniques that will help in the utilisation of resources as well as lower down the

wastage due to such business operations.

Job costing system: This technique will help the managerial professionals in making

proper estimation in relation with improving efficiency of business. However, there can be

analysis which is based on the use of laborious efforts, material and duration in producing the

single unit as well as cost required for the completion of such business operations (Laudon and

Laudon, 2016).

Price optimisation: Rates levied over the commodities produced by organisation are

needed to have appropriate prices which in turn bring profitable returns as well as must be more

than the costs incurred while producing such units. Hence, Toyota as the manufacturing unit can

be beneficial if they optimise the process over vehicle which must be effective.

Inventory management: The initial requirement in order to satisfy the consumer needs is

having proper inventory management (Hopper and Bui, 2016). Thus, Toyota needs to analyse the

market requirements as well as produce commodities which are desired by their consumers.

Hence, this will help in improving the brand image as well as increase industrial efficiency to

meet demands on time.

P2. Different techniques used by Toyota for management accounting reporting

1. Budget report - This report based on company's budget. In this report they define the

budget of organisation then increase their budget will set in effective department. In Toyota,

many employees are working and there are a lot of departments for different tasks. But so some

3

Zainuddin and Mail, 2017). Hence, such operational techniques will help business in making

proper changes as well as suggesting effectual solutions to improves business operations.

Taxation: While planning operating business activities and earning adequate amount of

profitability, it is the prime responsibility of firm to make tax returns. However, in the UK, there

has been taxes levied over industries which are corporate taxes, custom duties and other

transactional taxes such as transportation and various central or state level taxes (Yudi and et.al.,

2016). Hence, these taxes are being collected by HMRC and legal authority of UK.

Budgets: To set an adequate amount of limit over the operational activities of

organisation, budgeting tools will be beneficial such as cash budget, sales and purchase as well

as various operational budgets. Thus, Toyota needs to implement prefect use of such managerial

accounting techniques that will help in the utilisation of resources as well as lower down the

wastage due to such business operations.

Job costing system: This technique will help the managerial professionals in making

proper estimation in relation with improving efficiency of business. However, there can be

analysis which is based on the use of laborious efforts, material and duration in producing the

single unit as well as cost required for the completion of such business operations (Laudon and

Laudon, 2016).

Price optimisation: Rates levied over the commodities produced by organisation are

needed to have appropriate prices which in turn bring profitable returns as well as must be more

than the costs incurred while producing such units. Hence, Toyota as the manufacturing unit can

be beneficial if they optimise the process over vehicle which must be effective.

Inventory management: The initial requirement in order to satisfy the consumer needs is

having proper inventory management (Hopper and Bui, 2016). Thus, Toyota needs to analyse the

market requirements as well as produce commodities which are desired by their consumers.

Hence, this will help in improving the brand image as well as increase industrial efficiency to

meet demands on time.

P2. Different techniques used by Toyota for management accounting reporting

1. Budget report - This report based on company's budget. In this report they define the

budget of organisation then increase their budget will set in effective department. In Toyota,

many employees are working and there are a lot of departments for different tasks. But so some

3

department cannot be able to complete the target of the organisation and some units will get the

entire target of the company and they can be able to give their best. Company's half profit is

based on that department's employees who gives their best at workplace (Flynn, 2015). So this all

consideration by the company and set the budget according to department. If the departments

who give their best then next year budget will increase for them, and the department who cannot

be able to get the goals of the company, they will not get the budget. Company can decrease their

budget compare than present budget. So budget report is based on the department who doing well

and who doing not as well as according company.

2. Account receivable aging - This report is based on company’s cash flow and credit of

customers. Company provides credit services to their customers. Their customers getting the

services of credit and company collect the entire data of that customers and make an accounting

report. Some customers can pay their outstanding amount on time and then company mentioned

that information in their record but some time some customers can not be able to pay their

outstanding on time (Das, 2014). Then company send notice to them, but customers will not pay

the credit on that time as well. Further, company can take serious action for their customers who

cannot pay the outstanding amount. Through that action company will borrow the refund of their

credit fund and get the outstanding which not payable by the customers. So this report is based

on cash flow and credit service which given by the company. Toyota company sale cars to their

customers with instalment services. But some time customers can not be able to pay that

instalment on time. Then company can borrow the car in action of company policy.

3. Job cost report - This report shows specific project's expenses. They estimated the

revenue of entire department and then they evaluate the profitability and productivity which

provide by the employees. This report helps identifies higher earning areas and low earning areas

of the company (Wu, and Wang, 2016.). Further, they will stop wasting time on lower earning

areas and start focus on higher earning areas for increasing their strength and get the more profit.

Inventory and manufacturing - When company sale their product and purchase the raw

material then they need to keep record of this entire works. So company can make an inventory

for the data as sales, purchase, sales return, purchase return, profit, loss, delivery report etc. This

report shows the all data to the company when organisation require the most.

4

entire target of the company and they can be able to give their best. Company's half profit is

based on that department's employees who gives their best at workplace (Flynn, 2015). So this all

consideration by the company and set the budget according to department. If the departments

who give their best then next year budget will increase for them, and the department who cannot

be able to get the goals of the company, they will not get the budget. Company can decrease their

budget compare than present budget. So budget report is based on the department who doing well

and who doing not as well as according company.

2. Account receivable aging - This report is based on company’s cash flow and credit of

customers. Company provides credit services to their customers. Their customers getting the

services of credit and company collect the entire data of that customers and make an accounting

report. Some customers can pay their outstanding amount on time and then company mentioned

that information in their record but some time some customers can not be able to pay their

outstanding on time (Das, 2014). Then company send notice to them, but customers will not pay

the credit on that time as well. Further, company can take serious action for their customers who

cannot pay the outstanding amount. Through that action company will borrow the refund of their

credit fund and get the outstanding which not payable by the customers. So this report is based

on cash flow and credit service which given by the company. Toyota company sale cars to their

customers with instalment services. But some time customers can not be able to pay that

instalment on time. Then company can borrow the car in action of company policy.

3. Job cost report - This report shows specific project's expenses. They estimated the

revenue of entire department and then they evaluate the profitability and productivity which

provide by the employees. This report helps identifies higher earning areas and low earning areas

of the company (Wu, and Wang, 2016.). Further, they will stop wasting time on lower earning

areas and start focus on higher earning areas for increasing their strength and get the more profit.

Inventory and manufacturing - When company sale their product and purchase the raw

material then they need to keep record of this entire works. So company can make an inventory

for the data as sales, purchase, sales return, purchase return, profit, loss, delivery report etc. This

report shows the all data to the company when organisation require the most.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1. Analysing the importance of management accounting systems and its application in Toyota

Toyota as the multinational brand has huge business operations. It has many

manufacturing units, showrooms etc. which in turn have wide operational activities. Thus, there

is the need to have appropriate recording of all transactions as well as regular inspection of

accounts which in turn help business in making adequate cost controlling techniques. However,

application of Budgetary and costing techniques as well as various management accounting

methods will help them in making effectual business operations as well as bring adequate

outcomes. Thus, with the help of job costing business will be beneficial in making the adequate

changes in business operations such as improving the efficiency of workforce, optimum

utilisation of resources as well as bring innovative improvements in production, selling,

marketing etc. activities of industry.

D1. Integration of management accounting reporting in the business process of Toyota

To have appropriate outcomes, there is the need to implement reporting techniques in

organisation. Thus, managers or accounting professionals of Toyota will be beneficial in

producing the reports and communicating in internal or external environment of industry. Hence,

it will be beneficial for planning and decision making as well as bringing proper solutions for

business forecasts. Thus, such results are being disclosed in the external environment which are

in turn helpful for business in improving the capital structure as well as revenue gathering. In

terms of having better investment for operational activities of business, this disclosure will be

fruitful for business in terms of inviting investors to analyse profitability of firm as well as take

benefits form dividends.

TASK 2

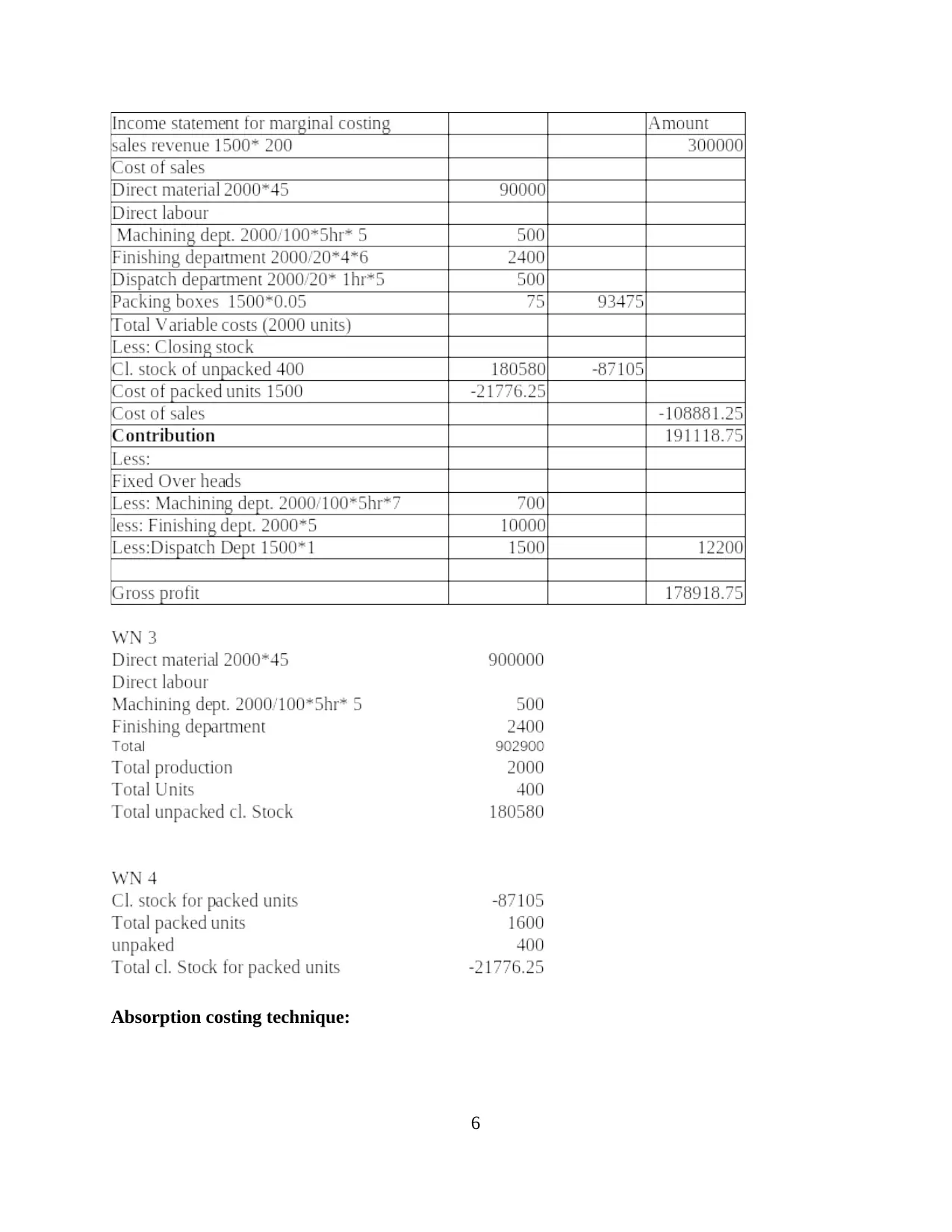

P3. Providing income statements on the basis of absorption and marginal costing techniques

Marginal costing technique:

5

Toyota as the multinational brand has huge business operations. It has many

manufacturing units, showrooms etc. which in turn have wide operational activities. Thus, there

is the need to have appropriate recording of all transactions as well as regular inspection of

accounts which in turn help business in making adequate cost controlling techniques. However,

application of Budgetary and costing techniques as well as various management accounting

methods will help them in making effectual business operations as well as bring adequate

outcomes. Thus, with the help of job costing business will be beneficial in making the adequate

changes in business operations such as improving the efficiency of workforce, optimum

utilisation of resources as well as bring innovative improvements in production, selling,

marketing etc. activities of industry.

D1. Integration of management accounting reporting in the business process of Toyota

To have appropriate outcomes, there is the need to implement reporting techniques in

organisation. Thus, managers or accounting professionals of Toyota will be beneficial in

producing the reports and communicating in internal or external environment of industry. Hence,

it will be beneficial for planning and decision making as well as bringing proper solutions for

business forecasts. Thus, such results are being disclosed in the external environment which are

in turn helpful for business in improving the capital structure as well as revenue gathering. In

terms of having better investment for operational activities of business, this disclosure will be

fruitful for business in terms of inviting investors to analyse profitability of firm as well as take

benefits form dividends.

TASK 2

P3. Providing income statements on the basis of absorption and marginal costing techniques

Marginal costing technique:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption costing technique:

6

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

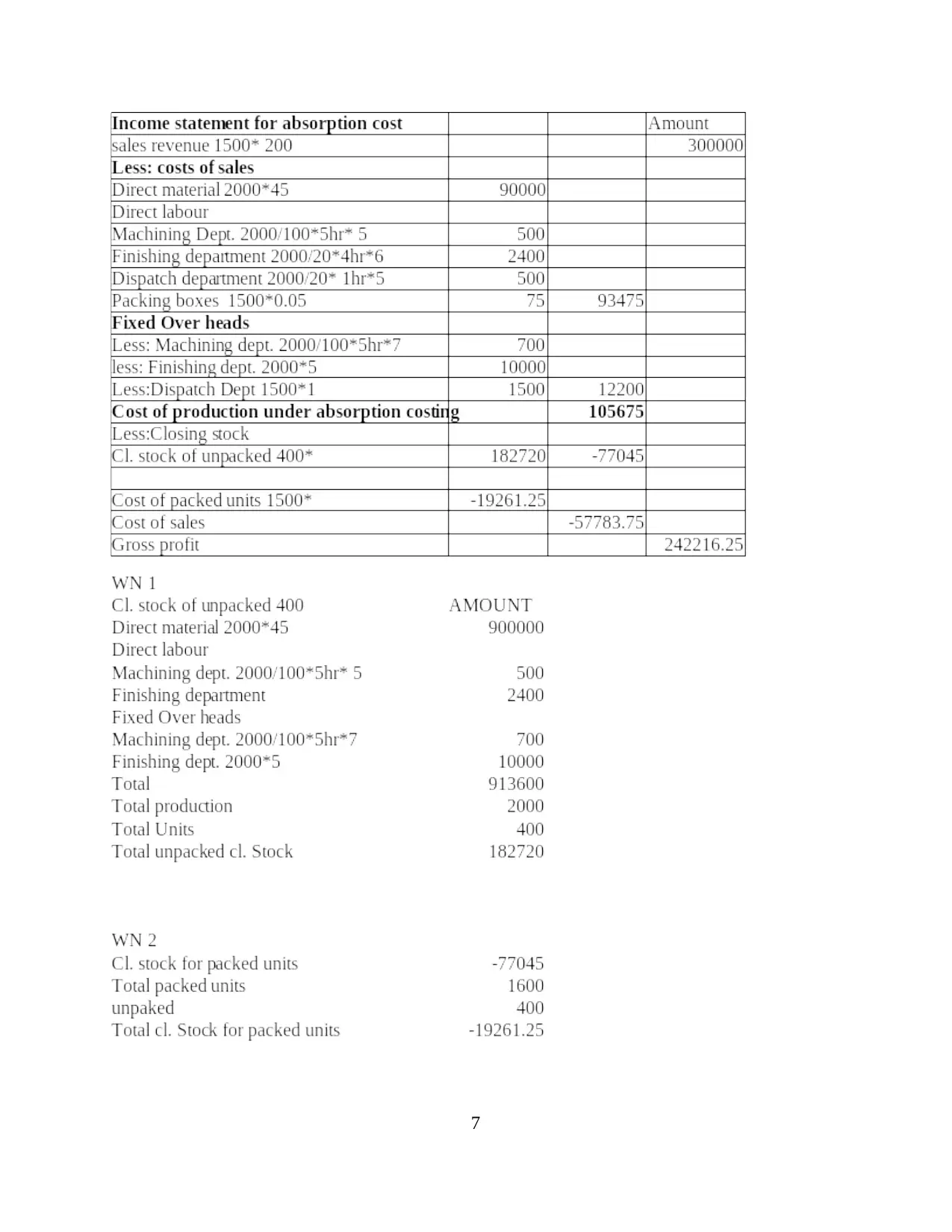

M2 Application of management accounting techniques and facilitating the financial reporting

documents

The management accounting techniques are used to analyse the financial profitability of

the firm. They maximize the amount of the profit which need to be earned by the company. On

the basis of marginal cost and absorption cost they need to calculate the income or total revenue

of the firm.

D2 Interpretation of the data for the range of industrial operations

The net profit of the firm is calculated as 314846 and the gross profit is about 315846 of

the firm. The company is selling about 1500 units at the price of 200 and then total revenue of

30000. The and total contribution expense is about 299000 and the net profit earned by the firm

is about 292000.

TASK 3

P4. Determining various kinds of planning tools and budgetary control systems with their pros

and cons

Activity based budgeting: In this budgeting method, manager allocates cost on the basis

of cost driver. In this, all the overhead expenses incurred by the firm are highly associated with

the activities performed (Downes, von Trapp and Nicol, 2017). Hence, such modern technique of

budgeting provides high level of assistance in allocating financial expenses in an appropriate

manner. Such method of budgeting has following advantages and disadvantages such as:

Advantages

ABB tool of budgeting provides assistance in identifying redundant activities. Hence, by

undertaking such technique Toyota can control wastage and would become to generate

high margin.

It facilitates optimal allocation of financial resources and helps in attaining higher

margin (Activity Based Budgeting: advantages and disadvantages, 2017).

By using such technique, business unit can enhance operational efficiency to a great

extent.

Disadvantages:

Along with the benefits, there are some cons that affect significance of ABB. On the basis

of ABB, to set competent budgeting framework firm requires highly skilled and talented

8

documents

The management accounting techniques are used to analyse the financial profitability of

the firm. They maximize the amount of the profit which need to be earned by the company. On

the basis of marginal cost and absorption cost they need to calculate the income or total revenue

of the firm.

D2 Interpretation of the data for the range of industrial operations

The net profit of the firm is calculated as 314846 and the gross profit is about 315846 of

the firm. The company is selling about 1500 units at the price of 200 and then total revenue of

30000. The and total contribution expense is about 299000 and the net profit earned by the firm

is about 292000.

TASK 3

P4. Determining various kinds of planning tools and budgetary control systems with their pros

and cons

Activity based budgeting: In this budgeting method, manager allocates cost on the basis

of cost driver. In this, all the overhead expenses incurred by the firm are highly associated with

the activities performed (Downes, von Trapp and Nicol, 2017). Hence, such modern technique of

budgeting provides high level of assistance in allocating financial expenses in an appropriate

manner. Such method of budgeting has following advantages and disadvantages such as:

Advantages

ABB tool of budgeting provides assistance in identifying redundant activities. Hence, by

undertaking such technique Toyota can control wastage and would become to generate

high margin.

It facilitates optimal allocation of financial resources and helps in attaining higher

margin (Activity Based Budgeting: advantages and disadvantages, 2017).

By using such technique, business unit can enhance operational efficiency to a great

extent.

Disadvantages:

Along with the benefits, there are some cons that affect significance of ABB. On the basis

of ABB, to set competent budgeting framework firm requires highly skilled and talented

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

personnel (Sperfeld and et.al., 2016). In the absence of having talented personnel Toyota would

not become able to set budget in accordance with ABB. Along with this, high time intensity is

considered as another main limitations of activity based budgeting.

Zero based budgeting: Under ZBB, manager of the business unit starts with zero base for

preparing new budget. It may be served as a reform over the traditional tools because in this

manager completely avoids past financial plan or framework. In accordance with such technique,

by taking zero base, finding and justifying all the cost effective ways of performing activities

manager sets new plan (McCartney, Pierce and Mackie, 2016). Hence, manager of Toyota should

consider following advantages and drawbacks while preparing budgeting framework as per ZBB.

Advantages

ZBB method helps in developing appropriate work and making optimal allocation of

financial resources.

It improves co-ordination among different departments to a great extent.

ZBB helps in avoiding wastage and enhances profit margin significantly.

Disadvantages

In the case of having lack of expertise among the personnel Toyota would not become

able to develop suitable financial plan (Zero Based Budgeting Disadvantages, 2017). \ For preparing budget as per ZBB, business unit requires high manpower as well as time.

Responsibility budgeting: On the basis of responsibility budgeting, by preparing various

responsibility centre such as cost, profit, sales etc. In accordance with such technique,

management team takes input from the managers of each responsibility centre. Considering such

input manager can develop suitable framework for the upcoming time period. Along with this,

responsibility manager also gives specific reasons due to which they failed to get the desired

level of outcome or success (Oyigbo and Ugwu, 2017). This in turn helps firm in developing

suitable framework for the upcoming time period.

Advantages

Helps in taking suitable decision about funds as manager provides their suggestions

regarding the same

Facilitates delegation of roles as well as responsibilities and encourage personnel in

relation to making their best efforts.

Disadvantages

9

not become able to set budget in accordance with ABB. Along with this, high time intensity is

considered as another main limitations of activity based budgeting.

Zero based budgeting: Under ZBB, manager of the business unit starts with zero base for

preparing new budget. It may be served as a reform over the traditional tools because in this

manager completely avoids past financial plan or framework. In accordance with such technique,

by taking zero base, finding and justifying all the cost effective ways of performing activities

manager sets new plan (McCartney, Pierce and Mackie, 2016). Hence, manager of Toyota should

consider following advantages and drawbacks while preparing budgeting framework as per ZBB.

Advantages

ZBB method helps in developing appropriate work and making optimal allocation of

financial resources.

It improves co-ordination among different departments to a great extent.

ZBB helps in avoiding wastage and enhances profit margin significantly.

Disadvantages

In the case of having lack of expertise among the personnel Toyota would not become

able to develop suitable financial plan (Zero Based Budgeting Disadvantages, 2017). \ For preparing budget as per ZBB, business unit requires high manpower as well as time.

Responsibility budgeting: On the basis of responsibility budgeting, by preparing various

responsibility centre such as cost, profit, sales etc. In accordance with such technique,

management team takes input from the managers of each responsibility centre. Considering such

input manager can develop suitable framework for the upcoming time period. Along with this,

responsibility manager also gives specific reasons due to which they failed to get the desired

level of outcome or success (Oyigbo and Ugwu, 2017). This in turn helps firm in developing

suitable framework for the upcoming time period.

Advantages

Helps in taking suitable decision about funds as manager provides their suggestions

regarding the same

Facilitates delegation of roles as well as responsibilities and encourage personnel in

relation to making their best efforts.

Disadvantages

9

It is highly time consuming process because in this high involvement of personnel are

required.

It also places negatively impacts employee motivation.

Incremental budgeting: This is stated to be yet another well-known method of budgeting as a

planning tool in which, the previous year’s budget is taken into consideration for making the

present year’s budget. It thereby works as a base to plan for the current year to avoid any

mistakes of previous year. This involves making small rectifications in the current year’s budget

where it is assistive in terms of reducing any state of uncertainty in the successive year’s budget.

Although, it is also associated with some major pros and cons, that are as listed below-

Advantages-

o A foremost benefit of this method is its simplicity where it is also easy to prepare

in no time in comparison to other identified methods.

o Apart from this, it is also referred to be one of the easiest method for the

allocation of budget and by together responding to any required change.

o As a result, to which, this particular method of budgeting assists in funding, as

and when required. Disadvantages-

o This method also consists of some major drawbacks which includes non-

identification of any ineffective resource.

o It is sometimes considered to be a non-economical measure that requires spending

huge amount for the preparation of budget using this particular tool.

P5. Adoption of management accounting systems to resolve the financial obstacles

While operating in the market, several kinds of issues and obstacles come into

consideration which directly create negative impact on the business. Therefore, it is mandatory to

make solution of such issues in an appropriate manner so that, Toyota able to boost up its

financial performance (Quinn and et.al., 2017). The current section focuses on financial problems

which are like reducing income and profit, declining return on investment, improve cost,

expenses etc., (Dewa and et.al., 2016). Further, management of Toyota is considering different

systems of MA in order to make solution of such financial issue take place at the workplace.

Moreover, these all the systems or approaches are mentioned below:

10

required.

It also places negatively impacts employee motivation.

Incremental budgeting: This is stated to be yet another well-known method of budgeting as a

planning tool in which, the previous year’s budget is taken into consideration for making the

present year’s budget. It thereby works as a base to plan for the current year to avoid any

mistakes of previous year. This involves making small rectifications in the current year’s budget

where it is assistive in terms of reducing any state of uncertainty in the successive year’s budget.

Although, it is also associated with some major pros and cons, that are as listed below-

Advantages-

o A foremost benefit of this method is its simplicity where it is also easy to prepare

in no time in comparison to other identified methods.

o Apart from this, it is also referred to be one of the easiest method for the

allocation of budget and by together responding to any required change.

o As a result, to which, this particular method of budgeting assists in funding, as

and when required. Disadvantages-

o This method also consists of some major drawbacks which includes non-

identification of any ineffective resource.

o It is sometimes considered to be a non-economical measure that requires spending

huge amount for the preparation of budget using this particular tool.

P5. Adoption of management accounting systems to resolve the financial obstacles

While operating in the market, several kinds of issues and obstacles come into

consideration which directly create negative impact on the business. Therefore, it is mandatory to

make solution of such issues in an appropriate manner so that, Toyota able to boost up its

financial performance (Quinn and et.al., 2017). The current section focuses on financial problems

which are like reducing income and profit, declining return on investment, improve cost,

expenses etc., (Dewa and et.al., 2016). Further, management of Toyota is considering different

systems of MA in order to make solution of such financial issue take place at the workplace.

Moreover, these all the systems or approaches are mentioned below:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.