Management Accounting Report: KEF Manufacturing Case Study

VerifiedAdded on 2021/02/19

|20

|4288

|19

Report

AI Summary

This report delves into the realm of management accounting, exploring its core concepts, essential requirements, and various reporting methods. It utilizes Alpha FMC, a London-based consultancy, and its client, Kent Engineering and Foundry (KEF), a loudspeaker manufacturer, as a case study to illustrate the practical application of management accounting systems. The report examines different management accounting systems, including costing, price optimization, inventory management, and job costing systems, assessing their benefits within the context of KEF Manufacturing. Furthermore, it analyzes various management accounting reporting techniques, such as budget reports, performance reports, and job costing reports, and evaluates the integration of management accounting systems and reporting within organizational processes. The report also covers the computation of costs using marginal and absorption costing techniques, the advantages and disadvantages of budgetary control, and compares how organizations adopt management accounting systems in response to financial problems. Finally, it analyzes how management accounting systems aid in resolving financial problems sustainably and evaluates how planning tools help in achieving sustainable success.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1. Concept of Management Accounting and its essential requirements..............................4

P2. Various methods used for management accounting reporting.........................................6

M1. Assessing benefits of MAS in the context of KEF Manufacturing................................8

D1. Critical evaluation of integrating MAS and MAR within organizational processes.......8

TASK 2............................................................................................................................................8

P3. Computation of costs using Marginal and Absorption Costing Techniques....................8

.............................................................................................................................................12

M2. Application of Management Accounting techniques....................................................14

D2. Production of Financial Reports that enable data interpretation of various business

activities................................................................................................................................14

TASK 3..........................................................................................................................................14

P4. Advantages and disadvantages of different kind of planning tools of budgetary control14

M3. Types of planning tools and their application for preparing and forecasting of budgets.16

TASK 4..........................................................................................................................................17

P5. Comparing the ways organisations adopt MAS in response of Financial Problems.....17

Comparing implementation of MAS among different organisations...................................18

M4. Analysis of how management accounting system help in resolution of financial problems

sustainably............................................................................................................................19

D3. Evaluating how Planning tools help in resolution of financial problems to achieve

sustainable success...............................................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1. Concept of Management Accounting and its essential requirements..............................4

P2. Various methods used for management accounting reporting.........................................6

M1. Assessing benefits of MAS in the context of KEF Manufacturing................................8

D1. Critical evaluation of integrating MAS and MAR within organizational processes.......8

TASK 2............................................................................................................................................8

P3. Computation of costs using Marginal and Absorption Costing Techniques....................8

.............................................................................................................................................12

M2. Application of Management Accounting techniques....................................................14

D2. Production of Financial Reports that enable data interpretation of various business

activities................................................................................................................................14

TASK 3..........................................................................................................................................14

P4. Advantages and disadvantages of different kind of planning tools of budgetary control14

M3. Types of planning tools and their application for preparing and forecasting of budgets.16

TASK 4..........................................................................................................................................17

P5. Comparing the ways organisations adopt MAS in response of Financial Problems.....17

Comparing implementation of MAS among different organisations...................................18

M4. Analysis of how management accounting system help in resolution of financial problems

sustainably............................................................................................................................19

D3. Evaluating how Planning tools help in resolution of financial problems to achieve

sustainable success...............................................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

INTRODUCTION

In present day scenario, the business environment has evolved from the preparation of

historic general ledger using a wide variety of book-keeping systems and methods that provide

financial accounting information at a face value (Abdullah and Said, 2015). There has been an

introduction of highly customized business processes as well as systems which ensures that not

only the performance is tracked on a continual basis but also cost-based information helps in

removal of uncertainty so as to facilitate forecasting of future strategic plans of action.

In this context, this report aims to provide an insightful look into the various types of

management accounting systems as well as techniques. For this purpose, Alpha FMC has been

chosen as a consultancy organization that is based in London, UK (Alpha, 2019). It has a wide

variety of clients most of which are small and medium sized enterprises that are operative in

sectors like Manufacturing, Retail, Hospitality or Construction. One such enterprise is Kent

Engineering and Foundry (KEF) which is based out of Maidstone, England and produces as well

as distributes loudspeakers internationally (KEF, 2019). Also, an analysis of planning tools and

techniques has been undertaken to depict how such systems enable decision-making among

organizations.

TASK 1

P1. Concept of Management Accounting and its essential requirements

In the recent years, the concept of Managerial Accounting has gained huge acclamation

from accounting professionals as well as organisations alike. It can be defined as the practice of

taking informed financial as well as non-financial decisions on the basis of information derived

by the managers in regards to a particular business element which helps in successful

achievement of organisational goals. It is important to note that financial reporting forms a

critical part of this field of study (Al-Mawali, 2015). Management accounting is the discipline

including a set of methods or techniques which deal with the collection, process, and

interpretation of qualitative and quantitative information of any business in order to prepare

reports that must be used by decision makers to determine how to find sources of incomes and

how to invest the business resources to fulfil the organization strategy in the most convenient

way.

In present day scenario, the business environment has evolved from the preparation of

historic general ledger using a wide variety of book-keeping systems and methods that provide

financial accounting information at a face value (Abdullah and Said, 2015). There has been an

introduction of highly customized business processes as well as systems which ensures that not

only the performance is tracked on a continual basis but also cost-based information helps in

removal of uncertainty so as to facilitate forecasting of future strategic plans of action.

In this context, this report aims to provide an insightful look into the various types of

management accounting systems as well as techniques. For this purpose, Alpha FMC has been

chosen as a consultancy organization that is based in London, UK (Alpha, 2019). It has a wide

variety of clients most of which are small and medium sized enterprises that are operative in

sectors like Manufacturing, Retail, Hospitality or Construction. One such enterprise is Kent

Engineering and Foundry (KEF) which is based out of Maidstone, England and produces as well

as distributes loudspeakers internationally (KEF, 2019). Also, an analysis of planning tools and

techniques has been undertaken to depict how such systems enable decision-making among

organizations.

TASK 1

P1. Concept of Management Accounting and its essential requirements

In the recent years, the concept of Managerial Accounting has gained huge acclamation

from accounting professionals as well as organisations alike. It can be defined as the practice of

taking informed financial as well as non-financial decisions on the basis of information derived

by the managers in regards to a particular business element which helps in successful

achievement of organisational goals. It is important to note that financial reporting forms a

critical part of this field of study (Al-Mawali, 2015). Management accounting is the discipline

including a set of methods or techniques which deal with the collection, process, and

interpretation of qualitative and quantitative information of any business in order to prepare

reports that must be used by decision makers to determine how to find sources of incomes and

how to invest the business resources to fulfil the organization strategy in the most convenient

way.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

One of the main advantages of it is that it enables accurate forecasting of information

which further enables in planning budgets as well as their comparison to actual performance.

Hence, some of the crucial functions played by Management accounting in organisations include

planning, organising, controlling and decision-making. In addition to this, it also acts as a

medium of communication among all the organisational levels and departments. In the context of

KEF, there are various types of Management Accounting Systems (MAS) that are in place for

the business itself, however, it can improve its performance in a sustainable manner if it focuses

on the processes mentioned underneath:

Costing System:

As KEF is a manufacturing entity, it is crucial for it to have a competent system in place

which facilitates cost minimization and quality maximization of the various products it

manufactures and sells to its customers. Such a system consists of investment or expenses

needed to produce a good or deliver a service (Alvesson and Willmott, 2012). Hence, this system

plays an important role. It is a framework which helps in accurate estimation of reimbursements

so as to enable forecasting and planning for the managers that eventually helps in the

enhancement of overall profitability of KEF. Any type of system which helps in deliverance of

such functions to the business managers with least changes made to the existing set-up of such

accounting processes can be treated as an ideal costing system for KEF.

Price-Optimisation System:

It is important to know the correct value of the products and services since it not only

determines the level of revenues generated but also the profitability maintained by an entity over

the course of its life. This system helps in finding the right price that not only delivers cost-

effective and high quality offerings of finished goods to Kent's customers but also maximizes

profits for the company itself. As this system takes into account the overall demand of the

product, level of competition as well as cost of goods manufactured, it can help KEF in bringing

more profit and overcoming competition effectively. One of the essential requirements of this

system is to have a strong analytics back-end that would act as a supportive structure by posing

as a medium of database to the company itself (Arroyo, 2012).

Inventory Management System:

As the name suggests, this system assists in management of inventory that is essentially

related to stocks, products to be sold, raw materials if the business manufactures one or several

which further enables in planning budgets as well as their comparison to actual performance.

Hence, some of the crucial functions played by Management accounting in organisations include

planning, organising, controlling and decision-making. In addition to this, it also acts as a

medium of communication among all the organisational levels and departments. In the context of

KEF, there are various types of Management Accounting Systems (MAS) that are in place for

the business itself, however, it can improve its performance in a sustainable manner if it focuses

on the processes mentioned underneath:

Costing System:

As KEF is a manufacturing entity, it is crucial for it to have a competent system in place

which facilitates cost minimization and quality maximization of the various products it

manufactures and sells to its customers. Such a system consists of investment or expenses

needed to produce a good or deliver a service (Alvesson and Willmott, 2012). Hence, this system

plays an important role. It is a framework which helps in accurate estimation of reimbursements

so as to enable forecasting and planning for the managers that eventually helps in the

enhancement of overall profitability of KEF. Any type of system which helps in deliverance of

such functions to the business managers with least changes made to the existing set-up of such

accounting processes can be treated as an ideal costing system for KEF.

Price-Optimisation System:

It is important to know the correct value of the products and services since it not only

determines the level of revenues generated but also the profitability maintained by an entity over

the course of its life. This system helps in finding the right price that not only delivers cost-

effective and high quality offerings of finished goods to Kent's customers but also maximizes

profits for the company itself. As this system takes into account the overall demand of the

product, level of competition as well as cost of goods manufactured, it can help KEF in bringing

more profit and overcoming competition effectively. One of the essential requirements of this

system is to have a strong analytics back-end that would act as a supportive structure by posing

as a medium of database to the company itself (Arroyo, 2012).

Inventory Management System:

As the name suggests, this system assists in management of inventory that is essentially

related to stocks, products to be sold, raw materials if the business manufactures one or several

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

products, etc. which further helps in preparation of financial reports of the company. In order to

ascertain the correct system for the Kent Engineering, it is important to know how well the

suppliers management is executed through it along with synchronization of marketplaces. Hence,

KEF must internally understand its existing inventory management policy so as to improve them

by bring in more customization to such policies and procedures (Bebbington, Unerman and

O’DWYER, 2014).

Job Costing System:

This type of accounting system is kind of a specific order costing method under which

costs are first accumulated then associated to individual cost-units called 'Jobs'. The main

purpose of this system is to ascertain jobs related to each unit and derive the profit earned from

them individually. It is suitable for those businesses which manufacture customer specific goods

made and delivered. The essential pre-requisites for this system is that an effective production

control system is existent in the organisation along with properly classified, apportioned and

absorption methodologies implemented for overheads. As KEF fulfils these conditions,

implementation of this system can help in improving Kent's performance and profitability.

P2. Various methods used for management accounting reporting

Some of the crucial functions performed by Management Accounting is to act as a means

of communication to both internal as well as external stakeholders of the company (Busco,

Caglio and Scapens, 2015). This is usually done by consolidation of financial and non-financial

information in a manner which gives an overview of the business activities, performance,

profitability and projects that have been undertaken by such enterprise in a given fiscal year. For

this purpose, important financial reports are formulated for a specific time-period. Some of the

important methodologies that are adopted for Management Accounting Reporting (MAR) have

been enlisted below:

Budget Reports:

Preparation of such reports helps in critical assessment of company's performance in

terms of departments, costs as well as the business as a whole. A budget estimate is usually

inclusive of previous experiences along with future contingencies that may arise in relation to the

earnings and expenditures for a given time-period (Franco-Santos, Lucianetti and Bourne, 2012).

Hence, using this report is crucial as it enables proper planning of scarce resources available with

ascertain the correct system for the Kent Engineering, it is important to know how well the

suppliers management is executed through it along with synchronization of marketplaces. Hence,

KEF must internally understand its existing inventory management policy so as to improve them

by bring in more customization to such policies and procedures (Bebbington, Unerman and

O’DWYER, 2014).

Job Costing System:

This type of accounting system is kind of a specific order costing method under which

costs are first accumulated then associated to individual cost-units called 'Jobs'. The main

purpose of this system is to ascertain jobs related to each unit and derive the profit earned from

them individually. It is suitable for those businesses which manufacture customer specific goods

made and delivered. The essential pre-requisites for this system is that an effective production

control system is existent in the organisation along with properly classified, apportioned and

absorption methodologies implemented for overheads. As KEF fulfils these conditions,

implementation of this system can help in improving Kent's performance and profitability.

P2. Various methods used for management accounting reporting

Some of the crucial functions performed by Management Accounting is to act as a means

of communication to both internal as well as external stakeholders of the company (Busco,

Caglio and Scapens, 2015). This is usually done by consolidation of financial and non-financial

information in a manner which gives an overview of the business activities, performance,

profitability and projects that have been undertaken by such enterprise in a given fiscal year. For

this purpose, important financial reports are formulated for a specific time-period. Some of the

important methodologies that are adopted for Management Accounting Reporting (MAR) have

been enlisted below:

Budget Reports:

Preparation of such reports helps in critical assessment of company's performance in

terms of departments, costs as well as the business as a whole. A budget estimate is usually

inclusive of previous experiences along with future contingencies that may arise in relation to the

earnings and expenditures for a given time-period (Franco-Santos, Lucianetti and Bourne, 2012).

Hence, using this report is crucial as it enables proper planning of scarce resources available with

the business that ultimately help in bringing about cost-effectiveness as well as supplier

management practices in the organisation such as Kent Engineering & Foundry.

Performance Reports:

As performance is one of the main determinant of how well a business is doing in its

given internal and external environment, they play an important role in the present day scenario.

These reports help in the communication of inter-departmental, organisational as well as

employee performance which is crucial for the identification of weaknesses and strengths of the

company. On the basis of such reports, employee morale is also maintained by rewarding those

that perform better than their counterparts. Thus, ensuring that a definite level of motivation is

always present among them which is essential from a long-term perspective. KEF can employ

such reports to keep a check on the measures and business activities undertaken by the company

so as to realize their mission in a strategic manner.

Accounts Receivable Ageing Report:

Being a manufacturing business, it is obvious that operations of the company have a

heavy reliance on credit. Hence, preparation of such a report has immense importance for

businesses such as KEF. An Accounts Receivable Ageing Report is one which gives a detailed

view in regards to the amounts owed by external parties to the business for a particular period of

time (Johnson, 2015). Identification of defaulters helps the company know that whether the

credit policies put in place are effective or not. It also helps in ascertaining the amount of bad

debts that have occurred or are likely to occur in the near future. There periodic analysis also

facilitates prevention of overlooking any kind of old debts. The main advantage of this kind of

reports is that they make it easy to prevent the overlooking any kind of old debts and add value

to the financial reports of the business.

Job Costing Report:

Under the Job Costing System, individual profit as well as costs are classified,

apportioned and accumulated in relation to specific activities, usually known as 'job'. Keeping in

track of such earnings and expenditure is also important. These reports enable identification of

profit-making areas of the business which can help in building core competencies for that

particular enterprise. This is true in the case of KEF too which is mainly dealing in

manufacturing and distribution of electronic products.

management practices in the organisation such as Kent Engineering & Foundry.

Performance Reports:

As performance is one of the main determinant of how well a business is doing in its

given internal and external environment, they play an important role in the present day scenario.

These reports help in the communication of inter-departmental, organisational as well as

employee performance which is crucial for the identification of weaknesses and strengths of the

company. On the basis of such reports, employee morale is also maintained by rewarding those

that perform better than their counterparts. Thus, ensuring that a definite level of motivation is

always present among them which is essential from a long-term perspective. KEF can employ

such reports to keep a check on the measures and business activities undertaken by the company

so as to realize their mission in a strategic manner.

Accounts Receivable Ageing Report:

Being a manufacturing business, it is obvious that operations of the company have a

heavy reliance on credit. Hence, preparation of such a report has immense importance for

businesses such as KEF. An Accounts Receivable Ageing Report is one which gives a detailed

view in regards to the amounts owed by external parties to the business for a particular period of

time (Johnson, 2015). Identification of defaulters helps the company know that whether the

credit policies put in place are effective or not. It also helps in ascertaining the amount of bad

debts that have occurred or are likely to occur in the near future. There periodic analysis also

facilitates prevention of overlooking any kind of old debts. The main advantage of this kind of

reports is that they make it easy to prevent the overlooking any kind of old debts and add value

to the financial reports of the business.

Job Costing Report:

Under the Job Costing System, individual profit as well as costs are classified,

apportioned and accumulated in relation to specific activities, usually known as 'job'. Keeping in

track of such earnings and expenditure is also important. These reports enable identification of

profit-making areas of the business which can help in building core competencies for that

particular enterprise. This is true in the case of KEF too which is mainly dealing in

manufacturing and distribution of electronic products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Thus, preparation of such reports is important for a company such as Kent Engineering &

Foundry so as to build economies of scale in a sustainable manner.

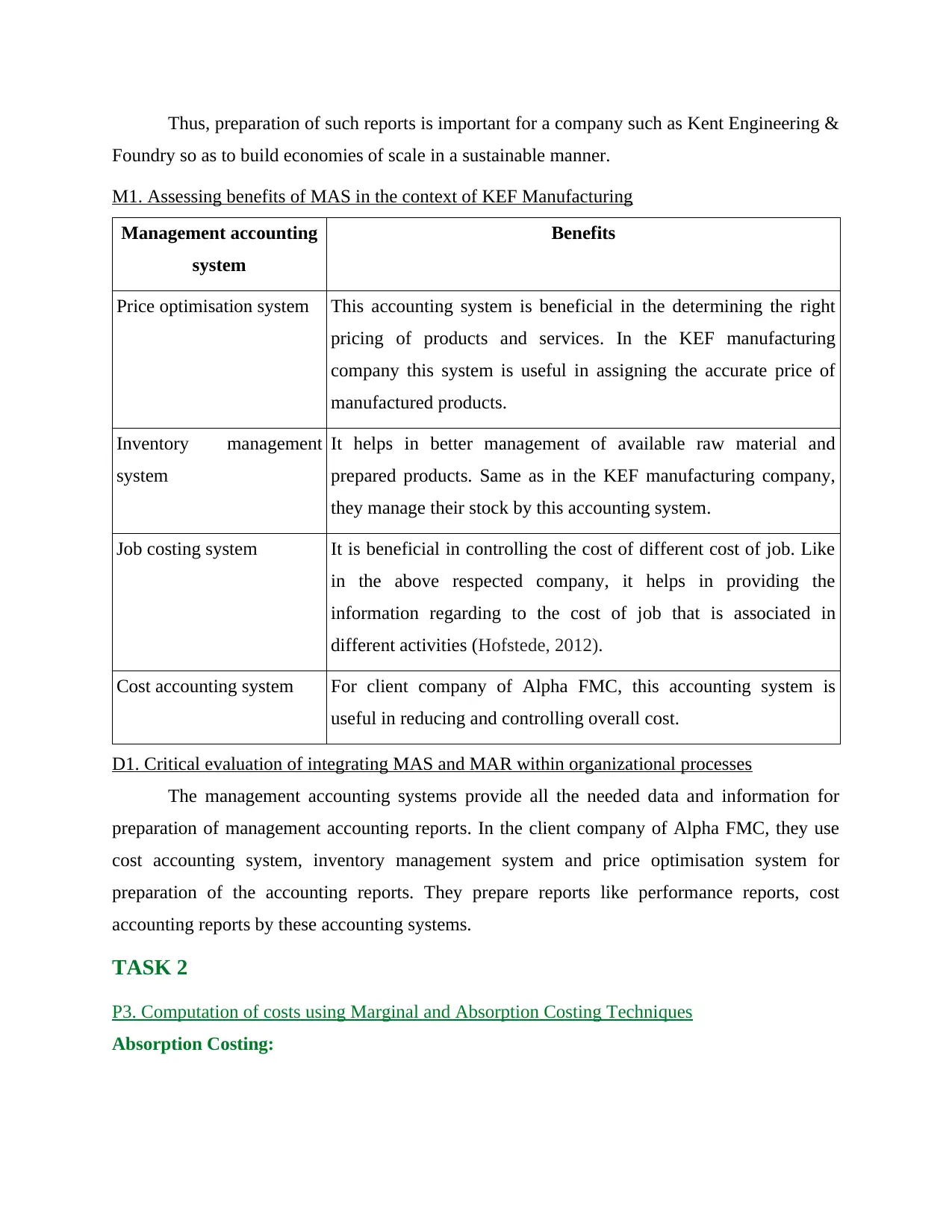

M1. Assessing benefits of MAS in the context of KEF Manufacturing

Management accounting

system

Benefits

Price optimisation system This accounting system is beneficial in the determining the right

pricing of products and services. In the KEF manufacturing

company this system is useful in assigning the accurate price of

manufactured products.

Inventory management

system

It helps in better management of available raw material and

prepared products. Same as in the KEF manufacturing company,

they manage their stock by this accounting system.

Job costing system It is beneficial in controlling the cost of different cost of job. Like

in the above respected company, it helps in providing the

information regarding to the cost of job that is associated in

different activities (Hofstede, 2012).

Cost accounting system For client company of Alpha FMC, this accounting system is

useful in reducing and controlling overall cost.

D1. Critical evaluation of integrating MAS and MAR within organizational processes

The management accounting systems provide all the needed data and information for

preparation of management accounting reports. In the client company of Alpha FMC, they use

cost accounting system, inventory management system and price optimisation system for

preparation of the accounting reports. They prepare reports like performance reports, cost

accounting reports by these accounting systems.

TASK 2

P3. Computation of costs using Marginal and Absorption Costing Techniques

Absorption Costing:

Foundry so as to build economies of scale in a sustainable manner.

M1. Assessing benefits of MAS in the context of KEF Manufacturing

Management accounting

system

Benefits

Price optimisation system This accounting system is beneficial in the determining the right

pricing of products and services. In the KEF manufacturing

company this system is useful in assigning the accurate price of

manufactured products.

Inventory management

system

It helps in better management of available raw material and

prepared products. Same as in the KEF manufacturing company,

they manage their stock by this accounting system.

Job costing system It is beneficial in controlling the cost of different cost of job. Like

in the above respected company, it helps in providing the

information regarding to the cost of job that is associated in

different activities (Hofstede, 2012).

Cost accounting system For client company of Alpha FMC, this accounting system is

useful in reducing and controlling overall cost.

D1. Critical evaluation of integrating MAS and MAR within organizational processes

The management accounting systems provide all the needed data and information for

preparation of management accounting reports. In the client company of Alpha FMC, they use

cost accounting system, inventory management system and price optimisation system for

preparation of the accounting reports. They prepare reports like performance reports, cost

accounting reports by these accounting systems.

TASK 2

P3. Computation of costs using Marginal and Absorption Costing Techniques

Absorption Costing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

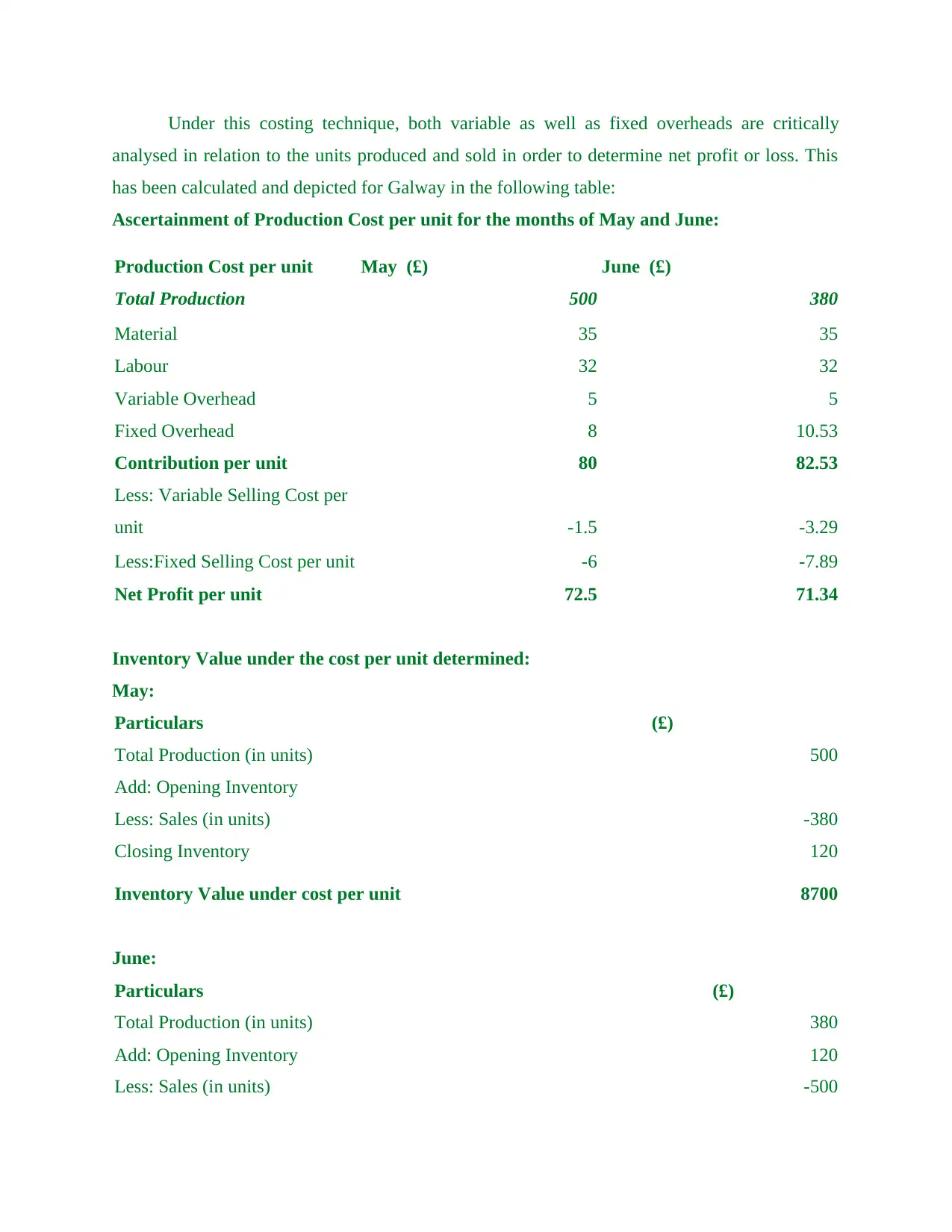

Under this costing technique, both variable as well as fixed overheads are critically

analysed in relation to the units produced and sold in order to determine net profit or loss. This

has been calculated and depicted for Galway in the following table:

Ascertainment of Production Cost per unit for the months of May and June:

Production Cost per unit May (£) June (£)

Total Production 500 380

Material 35 35

Labour 32 32

Variable Overhead 5 5

Fixed Overhead 8 10.53

Contribution per unit 80 82.53

Less: Variable Selling Cost per

unit -1.5 -3.29

Less:Fixed Selling Cost per unit -6 -7.89

Net Profit per unit 72.5 71.34

Inventory Value under the cost per unit determined:

May:

Particulars (£)

Total Production (in units) 500

Add: Opening Inventory

Less: Sales (in units) -380

Closing Inventory 120

Inventory Value under cost per unit 8700

June:

Particulars (£)

Total Production (in units) 380

Add: Opening Inventory 120

Less: Sales (in units) -500

analysed in relation to the units produced and sold in order to determine net profit or loss. This

has been calculated and depicted for Galway in the following table:

Ascertainment of Production Cost per unit for the months of May and June:

Production Cost per unit May (£) June (£)

Total Production 500 380

Material 35 35

Labour 32 32

Variable Overhead 5 5

Fixed Overhead 8 10.53

Contribution per unit 80 82.53

Less: Variable Selling Cost per

unit -1.5 -3.29

Less:Fixed Selling Cost per unit -6 -7.89

Net Profit per unit 72.5 71.34

Inventory Value under the cost per unit determined:

May:

Particulars (£)

Total Production (in units) 500

Add: Opening Inventory

Less: Sales (in units) -380

Closing Inventory 120

Inventory Value under cost per unit 8700

June:

Particulars (£)

Total Production (in units) 380

Add: Opening Inventory 120

Less: Sales (in units) -500

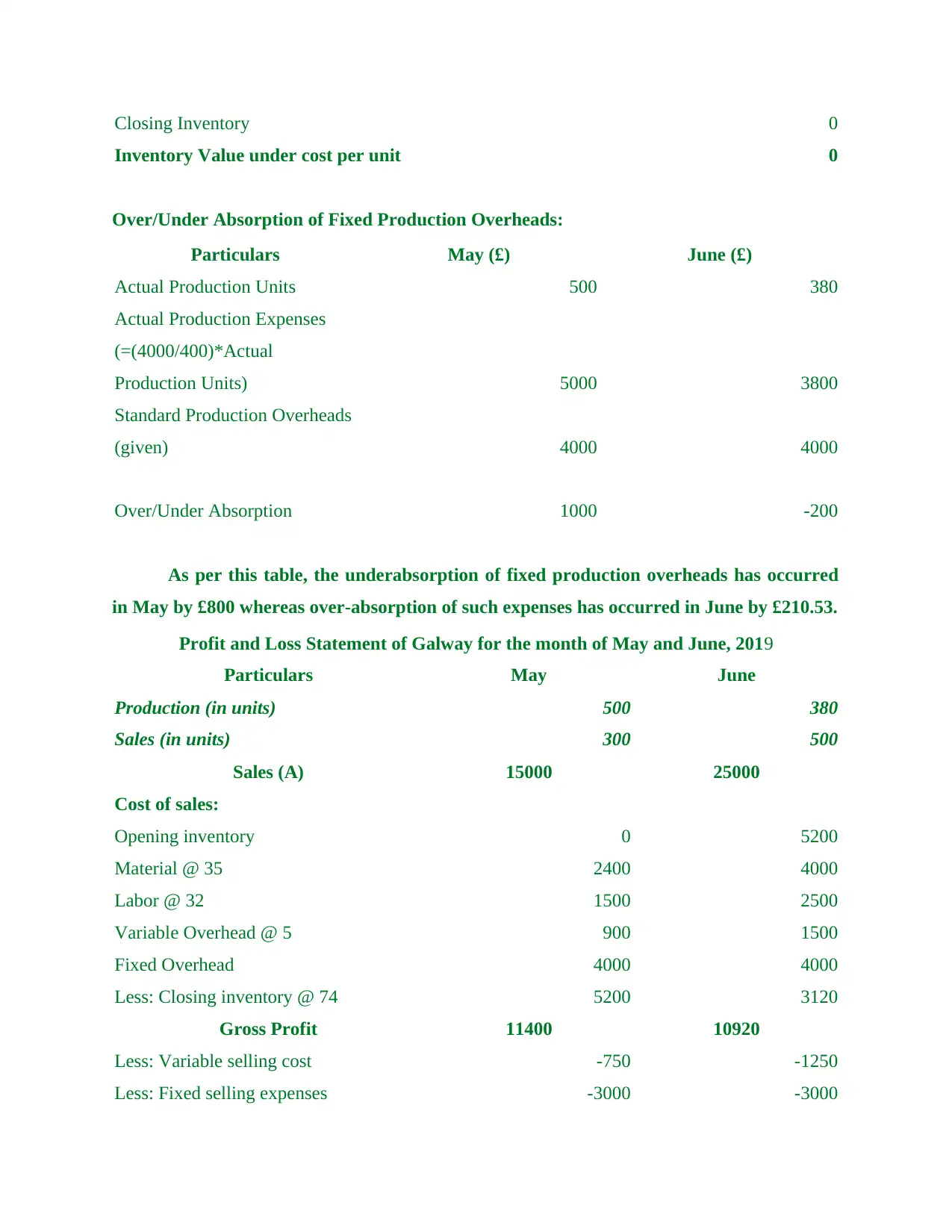

Closing Inventory 0

Inventory Value under cost per unit 0

Over/Under Absorption of Fixed Production Overheads:

Particulars May (£) June (£)

Actual Production Units 500 380

Actual Production Expenses

(=(4000/400)*Actual

Production Units) 5000 3800

Standard Production Overheads

(given) 4000 4000

Over/Under Absorption 1000 -200

As per this table, the underabsorption of fixed production overheads has occurred

in May by £800 whereas over-absorption of such expenses has occurred in June by £210.53.

Profit and Loss Statement of Galway for the month of May and June, 2019

Particulars May June

Production (in units) 500 380

Sales (in units) 300 500

Sales (A) 15000 25000

Cost of sales:

Opening inventory 0 5200

Material @ 35 2400 4000

Labor @ 32 1500 2500

Variable Overhead @ 5 900 1500

Fixed Overhead 4000 4000

Less: Closing inventory @ 74 5200 3120

Gross Profit 11400 10920

Less: Variable selling cost -750 -1250

Less: Fixed selling expenses -3000 -3000

Inventory Value under cost per unit 0

Over/Under Absorption of Fixed Production Overheads:

Particulars May (£) June (£)

Actual Production Units 500 380

Actual Production Expenses

(=(4000/400)*Actual

Production Units) 5000 3800

Standard Production Overheads

(given) 4000 4000

Over/Under Absorption 1000 -200

As per this table, the underabsorption of fixed production overheads has occurred

in May by £800 whereas over-absorption of such expenses has occurred in June by £210.53.

Profit and Loss Statement of Galway for the month of May and June, 2019

Particulars May June

Production (in units) 500 380

Sales (in units) 300 500

Sales (A) 15000 25000

Cost of sales:

Opening inventory 0 5200

Material @ 35 2400 4000

Labor @ 32 1500 2500

Variable Overhead @ 5 900 1500

Fixed Overhead 4000 4000

Less: Closing inventory @ 74 5200 3120

Gross Profit 11400 10920

Less: Variable selling cost -750 -1250

Less: Fixed selling expenses -3000 -3000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

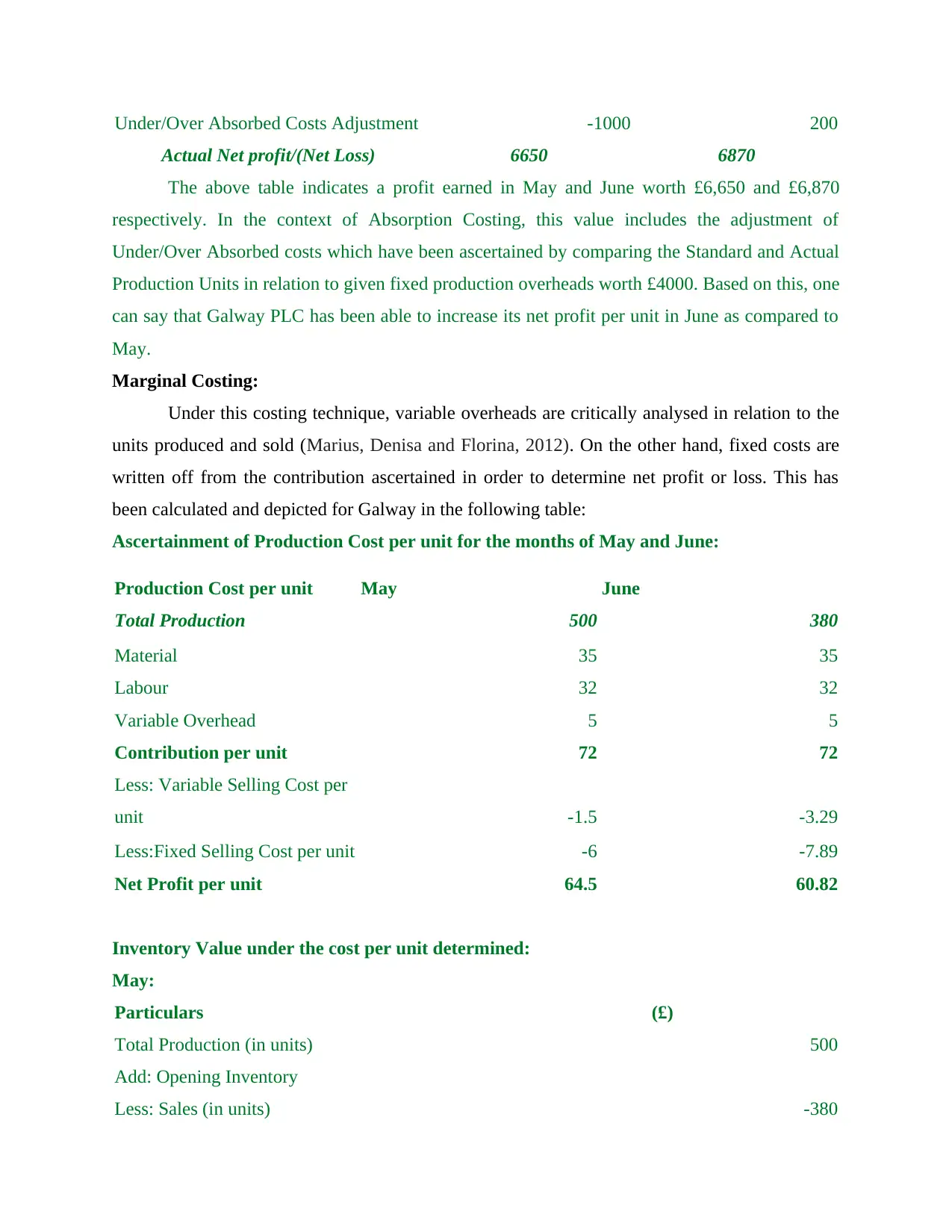

Under/Over Absorbed Costs Adjustment -1000 200

Actual Net profit/(Net Loss) 6650 6870

The above table indicates a profit earned in May and June worth £6,650 and £6,870

respectively. In the context of Absorption Costing, this value includes the adjustment of

Under/Over Absorbed costs which have been ascertained by comparing the Standard and Actual

Production Units in relation to given fixed production overheads worth £4000. Based on this, one

can say that Galway PLC has been able to increase its net profit per unit in June as compared to

May.

Marginal Costing:

Under this costing technique, variable overheads are critically analysed in relation to the

units produced and sold (Marius, Denisa and Florina, 2012). On the other hand, fixed costs are

written off from the contribution ascertained in order to determine net profit or loss. This has

been calculated and depicted for Galway in the following table:

Ascertainment of Production Cost per unit for the months of May and June:

Production Cost per unit May June

Total Production 500 380

Material 35 35

Labour 32 32

Variable Overhead 5 5

Contribution per unit 72 72

Less: Variable Selling Cost per

unit -1.5 -3.29

Less:Fixed Selling Cost per unit -6 -7.89

Net Profit per unit 64.5 60.82

Inventory Value under the cost per unit determined:

May:

Particulars (£)

Total Production (in units) 500

Add: Opening Inventory

Less: Sales (in units) -380

Actual Net profit/(Net Loss) 6650 6870

The above table indicates a profit earned in May and June worth £6,650 and £6,870

respectively. In the context of Absorption Costing, this value includes the adjustment of

Under/Over Absorbed costs which have been ascertained by comparing the Standard and Actual

Production Units in relation to given fixed production overheads worth £4000. Based on this, one

can say that Galway PLC has been able to increase its net profit per unit in June as compared to

May.

Marginal Costing:

Under this costing technique, variable overheads are critically analysed in relation to the

units produced and sold (Marius, Denisa and Florina, 2012). On the other hand, fixed costs are

written off from the contribution ascertained in order to determine net profit or loss. This has

been calculated and depicted for Galway in the following table:

Ascertainment of Production Cost per unit for the months of May and June:

Production Cost per unit May June

Total Production 500 380

Material 35 35

Labour 32 32

Variable Overhead 5 5

Contribution per unit 72 72

Less: Variable Selling Cost per

unit -1.5 -3.29

Less:Fixed Selling Cost per unit -6 -7.89

Net Profit per unit 64.5 60.82

Inventory Value under the cost per unit determined:

May:

Particulars (£)

Total Production (in units) 500

Add: Opening Inventory

Less: Sales (in units) -380

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Closing Inventory 120

Inventory Value under cost per unit 7740

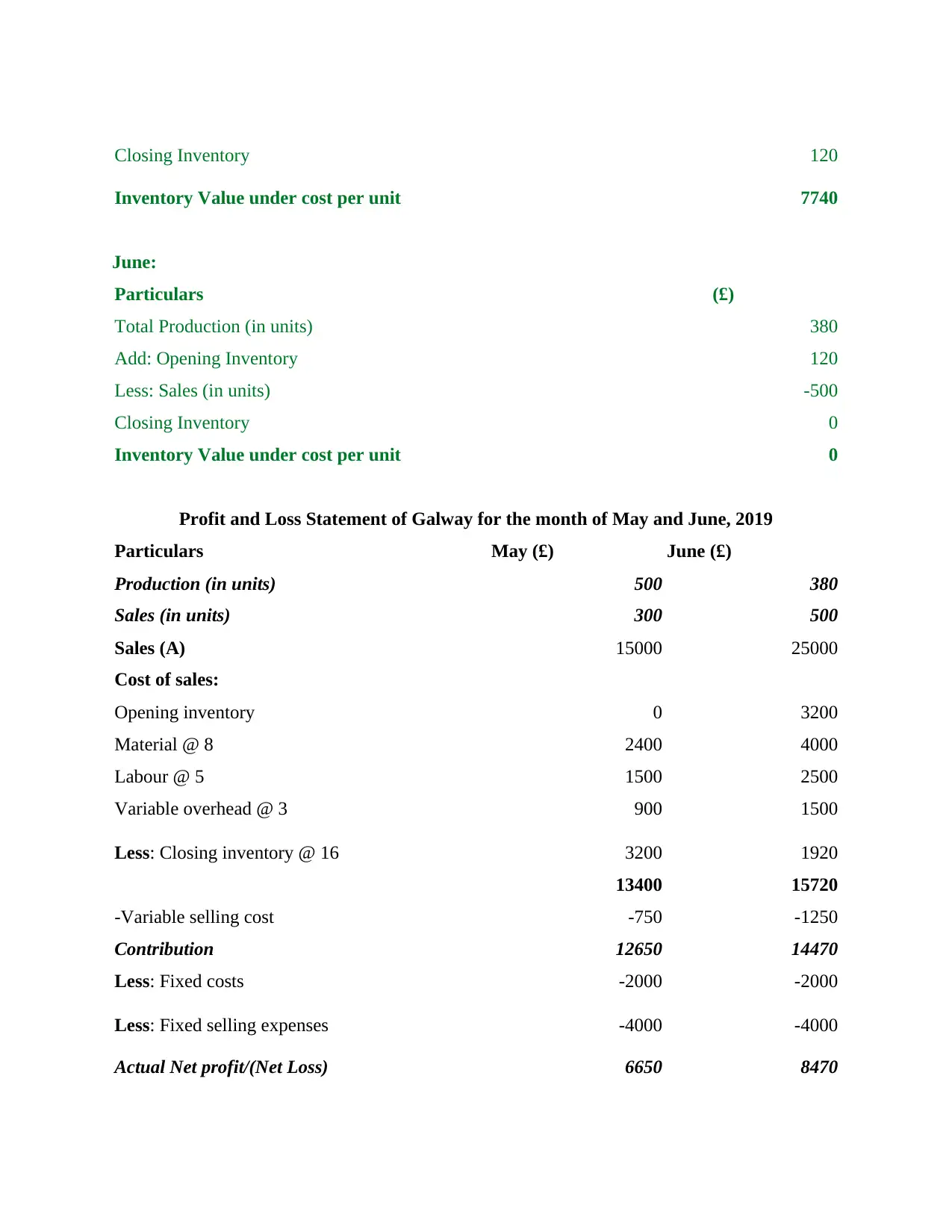

June:

Particulars (£)

Total Production (in units) 380

Add: Opening Inventory 120

Less: Sales (in units) -500

Closing Inventory 0

Inventory Value under cost per unit 0

Profit and Loss Statement of Galway for the month of May and June, 2019

Particulars May (£) June (£)

Production (in units) 500 380

Sales (in units) 300 500

Sales (A) 15000 25000

Cost of sales:

Opening inventory 0 3200

Material @ 8 2400 4000

Labour @ 5 1500 2500

Variable overhead @ 3 900 1500

Less: Closing inventory @ 16 3200 1920

13400 15720

-Variable selling cost -750 -1250

Contribution 12650 14470

Less: Fixed costs -2000 -2000

Less: Fixed selling expenses -4000 -4000

Actual Net profit/(Net Loss) 6650 8470

Inventory Value under cost per unit 7740

June:

Particulars (£)

Total Production (in units) 380

Add: Opening Inventory 120

Less: Sales (in units) -500

Closing Inventory 0

Inventory Value under cost per unit 0

Profit and Loss Statement of Galway for the month of May and June, 2019

Particulars May (£) June (£)

Production (in units) 500 380

Sales (in units) 300 500

Sales (A) 15000 25000

Cost of sales:

Opening inventory 0 3200

Material @ 8 2400 4000

Labour @ 5 1500 2500

Variable overhead @ 3 900 1500

Less: Closing inventory @ 16 3200 1920

13400 15720

-Variable selling cost -750 -1250

Contribution 12650 14470

Less: Fixed costs -2000 -2000

Less: Fixed selling expenses -4000 -4000

Actual Net profit/(Net Loss) 6650 8470

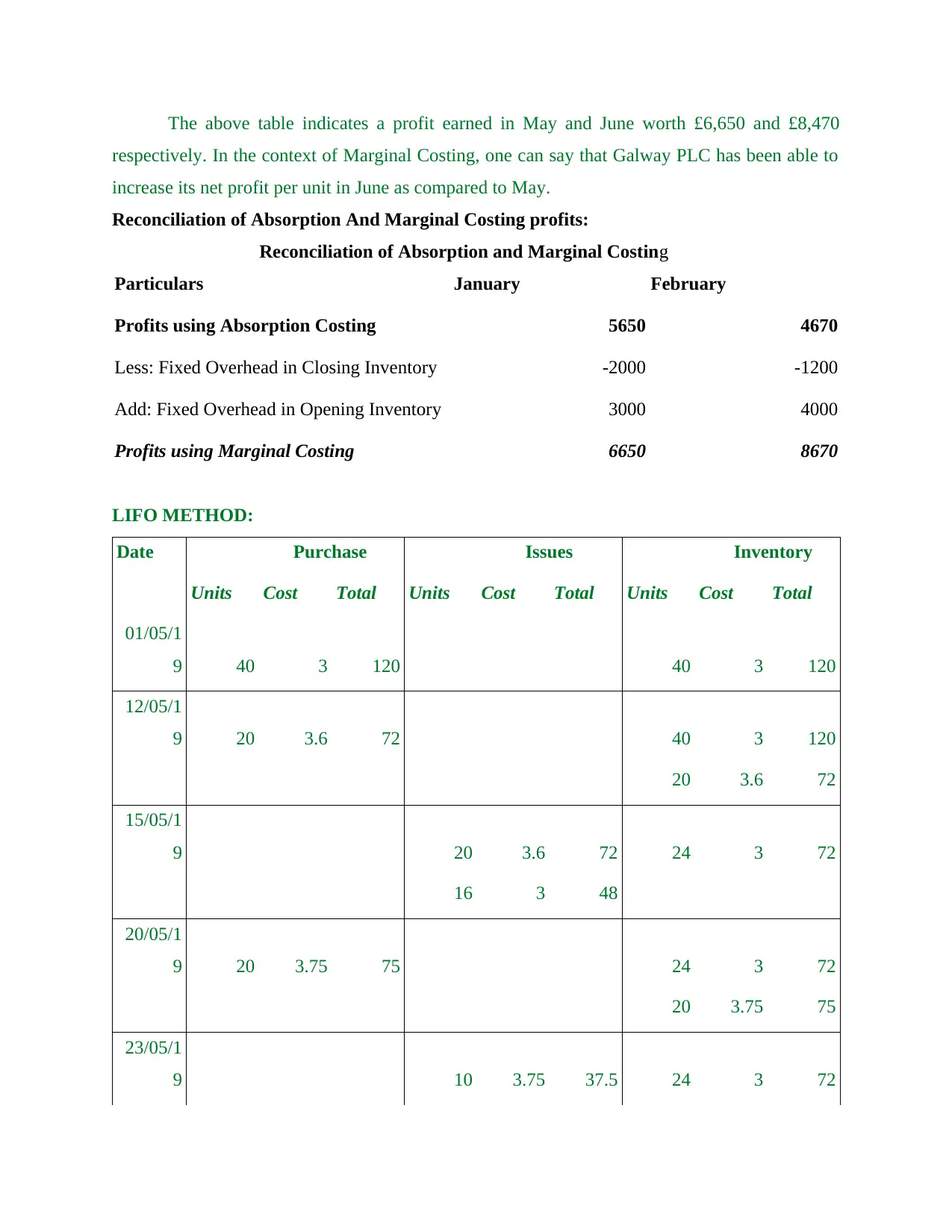

The above table indicates a profit earned in May and June worth £6,650 and £8,470

respectively. In the context of Marginal Costing, one can say that Galway PLC has been able to

increase its net profit per unit in June as compared to May.

Reconciliation of Absorption And Marginal Costing profits:

Reconciliation of Absorption and Marginal Costing

Particulars January February

Profits using Absorption Costing 5650 4670

Less: Fixed Overhead in Closing Inventory -2000 -1200

Add: Fixed Overhead in Opening Inventory 3000 4000

Profits using Marginal Costing 6650 8670

LIFO METHOD:

Date Purchase Issues Inventory

Units Cost Total Units Cost Total Units Cost Total

01/05/1

9 40 3 120 40 3 120

12/05/1

9 20 3.6 72 40 3 120

20 3.6 72

15/05/1

9 20 3.6 72 24 3 72

16 3 48

20/05/1

9 20 3.75 75 24 3 72

20 3.75 75

23/05/1

9 10 3.75 37.5 24 3 72

respectively. In the context of Marginal Costing, one can say that Galway PLC has been able to

increase its net profit per unit in June as compared to May.

Reconciliation of Absorption And Marginal Costing profits:

Reconciliation of Absorption and Marginal Costing

Particulars January February

Profits using Absorption Costing 5650 4670

Less: Fixed Overhead in Closing Inventory -2000 -1200

Add: Fixed Overhead in Opening Inventory 3000 4000

Profits using Marginal Costing 6650 8670

LIFO METHOD:

Date Purchase Issues Inventory

Units Cost Total Units Cost Total Units Cost Total

01/05/1

9 40 3 120 40 3 120

12/05/1

9 20 3.6 72 40 3 120

20 3.6 72

15/05/1

9 20 3.6 72 24 3 72

16 3 48

20/05/1

9 20 3.75 75 24 3 72

20 3.75 75

23/05/1

9 10 3.75 37.5 24 3 72

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.