Pricing and Cost Control Strategies

VerifiedAdded on 2020/06/06

|14

|4065

|43

AI Summary

This assignment delves into the crucial aspects of pricing strategy and cost control within a business context. The report aims to analyze various approaches to setting prices that ensure profitability while remaining competitive. Furthermore, it examines different cost control techniques to minimize expenses and maximize operational efficiency. The analysis is supported by academic references and explores the evolving landscape of management accounting practices.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

P1 (a) Management accounting and requirement of management accounting system...............2

P2 (b) Presenting financial Information......................................................................................4

TASK 2 .........................................................................................................................................5

P3 Calculation of profit as per marginal and absorption costing................................................5

TASK 3............................................................................................................................................7

P4 (a) Different type of budgets and their disadvantage and advantages...................................7

P4 (b) Process of preparing budgets by using various costing system.......................................9

P4 (c) Importance of budget as a tool of planning and control purpose.....................................9

TASK 4..........................................................................................................................................10

P5 Balanced scorecard approach...............................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

1

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

P1 (a) Management accounting and requirement of management accounting system...............2

P2 (b) Presenting financial Information......................................................................................4

TASK 2 .........................................................................................................................................5

P3 Calculation of profit as per marginal and absorption costing................................................5

TASK 3............................................................................................................................................7

P4 (a) Different type of budgets and their disadvantage and advantages...................................7

P4 (b) Process of preparing budgets by using various costing system.......................................9

P4 (c) Importance of budget as a tool of planning and control purpose.....................................9

TASK 4..........................................................................................................................................10

P5 Balanced scorecard approach...............................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

1

INTRODUCTION

Management and accounting is a tool to operate and manage the financial, accounting

and performance records in an ethical and effective manner (Lennox, Francis and Wang, 2011).

Accounting is a method which is used to keep records and information in figures and numbers.

At present, accounting tools are widely used by organisations to make an effective and

systematic structure of businesses. This is a report to be submitted to finance director in Tech

(UK). It is a company which provides special charger for mobile telephone and other carry on

gadgets for retail industries in UK. There are different management accounting reports and

difference between management accounting and financing accounting explained in this report.

Different types of budgets are explained and differentiated in this report as well.

TASK 1

P1 (a) Management accounting and requirement of management accounting system

Accounting was basically used in maintaining records and information which is collected

from multiple departments of organisation. Now, the accounting methods and techniques are

used as management perspectives too. Managers and directors use accounting reports and

information in decision making and strategic planning process. Being an involvement of

managers and directors in accounting process, this is also known as managerial accounting.

Management accounting contains rules and regulations, accounting standards. GAAP (Generally

Accepted Accounting Principles) provide rules and regulations regarding keeping records and

information in particular formats.

Difference between management accounting and financial accounting

Management Accounting Financial accounting

This accounting is known as managerial

accounting system which is used by the

managers, directors and stakeholders, investors

and financiers of company.

This accounting system is used to form the

financial records properly. This is known as

historical approach which is made up of

multiple rules, guidelines and standards of

finance.

This remain focused upon future events and

incidents. It helps the managers to analyse risk

There are various financial records maintained

like cash flow statement, balance sheets, cost

2

Management and accounting is a tool to operate and manage the financial, accounting

and performance records in an ethical and effective manner (Lennox, Francis and Wang, 2011).

Accounting is a method which is used to keep records and information in figures and numbers.

At present, accounting tools are widely used by organisations to make an effective and

systematic structure of businesses. This is a report to be submitted to finance director in Tech

(UK). It is a company which provides special charger for mobile telephone and other carry on

gadgets for retail industries in UK. There are different management accounting reports and

difference between management accounting and financing accounting explained in this report.

Different types of budgets are explained and differentiated in this report as well.

TASK 1

P1 (a) Management accounting and requirement of management accounting system

Accounting was basically used in maintaining records and information which is collected

from multiple departments of organisation. Now, the accounting methods and techniques are

used as management perspectives too. Managers and directors use accounting reports and

information in decision making and strategic planning process. Being an involvement of

managers and directors in accounting process, this is also known as managerial accounting.

Management accounting contains rules and regulations, accounting standards. GAAP (Generally

Accepted Accounting Principles) provide rules and regulations regarding keeping records and

information in particular formats.

Difference between management accounting and financial accounting

Management Accounting Financial accounting

This accounting is known as managerial

accounting system which is used by the

managers, directors and stakeholders, investors

and financiers of company.

This accounting system is used to form the

financial records properly. This is known as

historical approach which is made up of

multiple rules, guidelines and standards of

finance.

This remain focused upon future events and

incidents. It helps the managers to analyse risk

There are various financial records maintained

like cash flow statement, balance sheets, cost

2

factors and future opportunities. of capital, fund flow statement, ratio analysis,

etc.

Management accounting contains annual

reports, financial reports and performance

score card.

There are different law boards and institutions

made which provide guidelines to retain the

records in a proper manner. These are (GAAP),

IFRS (International Financial Reporting

Standards) and ISAB (International

Accounting Standards Board).

Data and information which are provided

though management accounting reports are

used in making plans and strategies.

This is a part of internal reporting which is

used by finance manager to make finance and

investment plans as well as procurement of

funds.

Importance of management accounting as a decision making tool

Decision making is a process used to make future plans regarding growth and

development of organisation (Grabner and Moers, 2013). Business environment is full of

competitors and rivals. Effective operations and management are the only factors which can

separate organisation from competitors and provide competitive advantage. Management

accounting is a combination of multiple accounting and management system which provides a

large area to analyse overall performance of organisation. Versatile nature and dynamic scope

make management accounting more continent and flexible. Information and data remain accurate

which helps in making straight to the point strategies and plans for further growth and

development.

Management accounting systems are useful and essential for all the types of

organisations. There are various types of activity based costing techniques used in management

accounting. It helps in analysing the cost of product at particular stage or activity. Management

accounting information is mostly used in the manufacturing process. It provides required sources

which remain essential in the manufacturing of product.

Cost accounting system

Cost management and cost accounting; both are important parts of management

accounting. This accounting method is used to analyse the manufacturing cost and control extra

3

etc.

Management accounting contains annual

reports, financial reports and performance

score card.

There are different law boards and institutions

made which provide guidelines to retain the

records in a proper manner. These are (GAAP),

IFRS (International Financial Reporting

Standards) and ISAB (International

Accounting Standards Board).

Data and information which are provided

though management accounting reports are

used in making plans and strategies.

This is a part of internal reporting which is

used by finance manager to make finance and

investment plans as well as procurement of

funds.

Importance of management accounting as a decision making tool

Decision making is a process used to make future plans regarding growth and

development of organisation (Grabner and Moers, 2013). Business environment is full of

competitors and rivals. Effective operations and management are the only factors which can

separate organisation from competitors and provide competitive advantage. Management

accounting is a combination of multiple accounting and management system which provides a

large area to analyse overall performance of organisation. Versatile nature and dynamic scope

make management accounting more continent and flexible. Information and data remain accurate

which helps in making straight to the point strategies and plans for further growth and

development.

Management accounting systems are useful and essential for all the types of

organisations. There are various types of activity based costing techniques used in management

accounting. It helps in analysing the cost of product at particular stage or activity. Management

accounting information is mostly used in the manufacturing process. It provides required sources

which remain essential in the manufacturing of product.

Cost accounting system

Cost management and cost accounting; both are important parts of management

accounting. This accounting method is used to analyse the manufacturing cost and control extra

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

cost. This accounting system is used in manufacturing industry which deals in product and

services. It helps in deciding the base price of product. This cost is considered as gross

manufacturing cost. Managers of Tech (UK) would help the cost accounting system to analyse

the manufacturing cost of making special chargers for retail industry. Relevant cost analysis is

one of the essential components of cost accounting system which remain focused upon

controlling the cost of marketing and advertisement cost.

Inventory management system

This is one of the management systems which is used by organisation to manage the

quantity of stock and storing them in a secured place (Pärl, 2012). Stock can be found in the form

of raw material, work in progress, finished goods, etc. Inventories are categorised on a priority

basis according to their importance in manufacturing process. ABC inventory system is a

common approach which is used in managing the stock as per their preciousness.

Job costing

In large organisation, manufacturing process remains divided in multiple sections and

divisions. Finished product from one process become raw material for another process. Job

costing method help to track the cost of product at particular batch or section. It differentiates the

profitability at every job. A job can be elaborated as a project done for one customer or a single

unit of product. Bifurcation of jobs and section depends upon various types of direct expenses as

direct labour, raw material, factory expenses, overheads and costs. A job profitability report

shows the overall profit and loss statement for organisation.

P2 (b) Presenting financial Information

Different types of management accounting reports

Management reports are beneficial to managers and directors at management level.

Various type of management reports provides wide range of measurement and overview to sort

out and form strategic plans. Below are some management reports are described:

Cost reports – these are the reports which provide data and information regarding analyse

the cost and expensed for a particular time duration (Michalak, 2013). Cost reports contains

different type of cost analysis as marginal costs, absorption costs, process costs, labour and

material costs, job and batch cost. All these cost are integrated in one single format and presented

to managers and directors.

4

services. It helps in deciding the base price of product. This cost is considered as gross

manufacturing cost. Managers of Tech (UK) would help the cost accounting system to analyse

the manufacturing cost of making special chargers for retail industry. Relevant cost analysis is

one of the essential components of cost accounting system which remain focused upon

controlling the cost of marketing and advertisement cost.

Inventory management system

This is one of the management systems which is used by organisation to manage the

quantity of stock and storing them in a secured place (Pärl, 2012). Stock can be found in the form

of raw material, work in progress, finished goods, etc. Inventories are categorised on a priority

basis according to their importance in manufacturing process. ABC inventory system is a

common approach which is used in managing the stock as per their preciousness.

Job costing

In large organisation, manufacturing process remains divided in multiple sections and

divisions. Finished product from one process become raw material for another process. Job

costing method help to track the cost of product at particular batch or section. It differentiates the

profitability at every job. A job can be elaborated as a project done for one customer or a single

unit of product. Bifurcation of jobs and section depends upon various types of direct expenses as

direct labour, raw material, factory expenses, overheads and costs. A job profitability report

shows the overall profit and loss statement for organisation.

P2 (b) Presenting financial Information

Different types of management accounting reports

Management reports are beneficial to managers and directors at management level.

Various type of management reports provides wide range of measurement and overview to sort

out and form strategic plans. Below are some management reports are described:

Cost reports – these are the reports which provide data and information regarding analyse

the cost and expensed for a particular time duration (Michalak, 2013). Cost reports contains

different type of cost analysis as marginal costs, absorption costs, process costs, labour and

material costs, job and batch cost. All these cost are integrated in one single format and presented

to managers and directors.

4

Budgetary reports – Analysation of future cost and events are considered in budgetary

reports. Budgets are made on the basis of past records and information. This reports help in

forming and casting the plans for better operation in near future. Budgetary reports are the

projected score card which defines that how much amount of material, labour and overheads to

be implemented in manufacturing process for upcoming year.

Performance reports – These are the reports which are made by leaders subject to their

functional departments (Dumitru and et. al. 2011). Leaders peruse the performance of every

individual and integrate the report in single format and submit the reports to managers. All the

performance report provided by leaders are categorised by managers and they prepare a

conclusive and summarised report. These reports help in analysing overall performance of

organisation.

Other reports – All other reports which are used as supportive tools considered in other

reports (Zamora, 2011). These reports are used to get additional sources to rectify and rephrase

the final reports. All these reports are known as subsidiary reports or supportive reports.

Why systematic presentation of information is required

Systematic presentation of reports help to understand the data and information easily. In

corporates and businesses functions management reporting help in bifurcate the data and figures.

It provides a convenient path to explain and sort out the informations in summarised way to

form the plans and business projects. Management accounting system divided the cost in two

ways first is internal cost and second is external cost of management.

TASK 2

P3 Calculation of profit as per marginal and absorption costing

Marginal costing

Calculation of profit by using marginal costing

technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

5

reports. Budgets are made on the basis of past records and information. This reports help in

forming and casting the plans for better operation in near future. Budgetary reports are the

projected score card which defines that how much amount of material, labour and overheads to

be implemented in manufacturing process for upcoming year.

Performance reports – These are the reports which are made by leaders subject to their

functional departments (Dumitru and et. al. 2011). Leaders peruse the performance of every

individual and integrate the report in single format and submit the reports to managers. All the

performance report provided by leaders are categorised by managers and they prepare a

conclusive and summarised report. These reports help in analysing overall performance of

organisation.

Other reports – All other reports which are used as supportive tools considered in other

reports (Zamora, 2011). These reports are used to get additional sources to rectify and rephrase

the final reports. All these reports are known as subsidiary reports or supportive reports.

Why systematic presentation of information is required

Systematic presentation of reports help to understand the data and information easily. In

corporates and businesses functions management reporting help in bifurcate the data and figures.

It provides a convenient path to explain and sort out the informations in summarised way to

form the plans and business projects. Management accounting system divided the cost in two

ways first is internal cost and second is external cost of management.

TASK 2

P3 Calculation of profit as per marginal and absorption costing

Marginal costing

Calculation of profit by using marginal costing

technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

5

Direct material 16000

Variable production overheads 4000

Less: cost of closing inventory (500*15) -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

Absorption costing

Calculation of profit by using absorption costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling and distribution

expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

6

Variable production overheads 4000

Less: cost of closing inventory (500*15) -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

Absorption costing

Calculation of profit by using absorption costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling and distribution

expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4 (a) Different type of budgets and their disadvantage and advantages

There are various budgets are prepared to forecasting and analysing the cost for further

events and incidents.1. Finance Budge – An organisation need finance requirement to operate its business

functions and activities. Finance is sources which work as a blood in organisation to

boost the functions and operations subject to business projects and goals (Gullkvist,

2013). There three type of budgets are prepared to bifurcate the information and data as

per capital and revenue nature. Financial budget is a combination of Cash budgets, capital

expenditure budgets and balance sheet budgets. All the inflows and outflow of cash are

considered in cash budget. Any kind of expenditure as purchase of new plant and

machinery, equipment, land and building are considered as capital expenditure and are

considered in capital expenditure budget. Balance sheet budget helps in managing and

balance the assets and liabilities of organisation.2. Cash flow budget – this budget is prepared to analyse the further requirement of cash for

accessing the task requirements. This is one of the essential requirement for business and

organisations to analyse cash requirement for future.3. Master budget- this budget helps to analyse the cash budget in order to determine

estimated income and expenditure of organisation. It assist managers and accountants

subject to interrelated different budgets.4. Operating Budget – Activities and transaction which are made on regular basis are

considered as operating activities and operating expenses. All the operating transactions

are considered in income and expenditure account of company. These the expensed

which are incurred to execute operations known as operating expenses or indirect

expenses (Moser, 2012). Operating budget support to analyse the cost and consumptions

of resources in adjustment of operating expenses during the year. It provides an

estimation that how much amount of finance and cash to be utilised in operations and

business activities in upcoming years. Sales revenue budgets, expense budgets, project

budgets are the part of operating budgets. All the selling, advertising, marketing and

promotional expenses are considered in sales budgets. Expenses which remain related to

administration, stationary and newspapers expenditure, petty expenses are adjusted in

7

P4 (a) Different type of budgets and their disadvantage and advantages

There are various budgets are prepared to forecasting and analysing the cost for further

events and incidents.1. Finance Budge – An organisation need finance requirement to operate its business

functions and activities. Finance is sources which work as a blood in organisation to

boost the functions and operations subject to business projects and goals (Gullkvist,

2013). There three type of budgets are prepared to bifurcate the information and data as

per capital and revenue nature. Financial budget is a combination of Cash budgets, capital

expenditure budgets and balance sheet budgets. All the inflows and outflow of cash are

considered in cash budget. Any kind of expenditure as purchase of new plant and

machinery, equipment, land and building are considered as capital expenditure and are

considered in capital expenditure budget. Balance sheet budget helps in managing and

balance the assets and liabilities of organisation.2. Cash flow budget – this budget is prepared to analyse the further requirement of cash for

accessing the task requirements. This is one of the essential requirement for business and

organisations to analyse cash requirement for future.3. Master budget- this budget helps to analyse the cash budget in order to determine

estimated income and expenditure of organisation. It assist managers and accountants

subject to interrelated different budgets.4. Operating Budget – Activities and transaction which are made on regular basis are

considered as operating activities and operating expenses. All the operating transactions

are considered in income and expenditure account of company. These the expensed

which are incurred to execute operations known as operating expenses or indirect

expenses (Moser, 2012). Operating budget support to analyse the cost and consumptions

of resources in adjustment of operating expenses during the year. It provides an

estimation that how much amount of finance and cash to be utilised in operations and

business activities in upcoming years. Sales revenue budgets, expense budgets, project

budgets are the part of operating budgets. All the selling, advertising, marketing and

promotional expenses are considered in sales budgets. Expenses which remain related to

administration, stationary and newspapers expenditure, petty expenses are adjusted in

7

expense budget. All other expenditures which are incurred to frame and design of plans

and strategies considered in project budget.5. Non-monetary budgets – Contingent liabilities and assets which remain uncertain and

can not be countable in money are considered in non-monetary budgets. These budgets

help in identifying the non-monetary incomes and expenditure to prepare an projected

budget. For example goodwill is one of the non-monetary income and asset which is

estimated in these type of budget.

6. Fixed and variable budgets – the are the budgets which bifurcate the cost as per their

type and nature (Leitner, 2013). There are two types of cost found in organisational

context fixed and variable cost. There are some costs which remain uncontrollable and

constant that are considered in fixed cost. Variable cost vary in respect of change of cost

with the change in per unit. Fixed cost remain same and constant while making budgets

and plans. Semi variable cost is one of the type of cost which remain fixed at certain level

and then after change in proportion of quantity, amount or size. Fixed cost budgets are

used to control cost and analyse the cost for upcoming year.

Advantages and disadvantage of various type of budgets

Advantage Disadvantage

Budgets provides a path to predict the future

situations and opportunities and frame growth

and development plans.

It is a process which contains high cost and

investment.

It helps in identifying the amount of resources

as finance, labour, material and wages to be

utilised in future.

Budgets are prepared on the basis of last years'

informations and records which are used

contains income statement, profit and loss and

fund flow statements.

It supports the management committee in

decision making and strategic planning.

Innovative ideas and creation remain lack

behind while making budgets.

Budgets make the organisational structure

strong and stable to deal with challenges

positive attributes.

Budgets are based on predictions and

estimation which are not the guarantee of

hundred percent success.

8

and strategies considered in project budget.5. Non-monetary budgets – Contingent liabilities and assets which remain uncertain and

can not be countable in money are considered in non-monetary budgets. These budgets

help in identifying the non-monetary incomes and expenditure to prepare an projected

budget. For example goodwill is one of the non-monetary income and asset which is

estimated in these type of budget.

6. Fixed and variable budgets – the are the budgets which bifurcate the cost as per their

type and nature (Leitner, 2013). There are two types of cost found in organisational

context fixed and variable cost. There are some costs which remain uncontrollable and

constant that are considered in fixed cost. Variable cost vary in respect of change of cost

with the change in per unit. Fixed cost remain same and constant while making budgets

and plans. Semi variable cost is one of the type of cost which remain fixed at certain level

and then after change in proportion of quantity, amount or size. Fixed cost budgets are

used to control cost and analyse the cost for upcoming year.

Advantages and disadvantage of various type of budgets

Advantage Disadvantage

Budgets provides a path to predict the future

situations and opportunities and frame growth

and development plans.

It is a process which contains high cost and

investment.

It helps in identifying the amount of resources

as finance, labour, material and wages to be

utilised in future.

Budgets are prepared on the basis of last years'

informations and records which are used

contains income statement, profit and loss and

fund flow statements.

It supports the management committee in

decision making and strategic planning.

Innovative ideas and creation remain lack

behind while making budgets.

Budgets make the organisational structure

strong and stable to deal with challenges

positive attributes.

Budgets are based on predictions and

estimation which are not the guarantee of

hundred percent success.

8

P4 (b) Process of preparing budgets by using various costing system

Below are some basic steps defined to frame and design the budgets as

General information – there are some general informations and data are collected form all the

departments. These data may be related to operational costs, payment receipts, bills etc.

Source of income – this is the second step which help in find out the source of income to

generate the finance and cash. Find out the payback period of getting payments are the main

sectors of this step.

Make a list of monthly expenses – All the payments and incomes are recorded in books of

accounts (Bennett and James, 2017). There is a list prepared to sort out the monthly expenses.

For example how much expenses are made on monthly purchase and manufacturing process are

counted in this method.

Break even analysis – how much amount of sale is required to generate minimum profit are

calculated by this method. It is one of the prominent and convenient method for managers

perspective. This method help in analysing the profit volume and sales ratio after adjustment of

variable and fixed cost.

Pricing strategies – this strategy is used to ascertain the cost and profit margin on product and

services of company. This step help in managing the cost and deciding the price of product.

Implementation – After making strategies and plan there is a practical analysis done by

implementation them in departments and functions of organisation.

Analysation – this steps indicates towards the measurement the performance of organisation

subject to proposed budget and plan.

Various type of pricing systems are used such as

Price skimming: this is the system which is used to analyse price subject to enhancing

profitability of organisation. Prices and sales prices are decided at initial stage.

Economic pricing: this system is used to determine optimum price of product in order to

earn optimum returns form operations.

P4 (c) Importance of budget as a tool of planning and control purpose

Budgeting and planning tools are considered as essential in organisational context.

Budgetary-control is one of the planning tool which helps in making cost effective budgets and

plans (Lachmann, Knauer and Trapp, 2013). Budgetary-control process system is implemented

in organisation to control the cost and set the margin of profit. Budgets and plans are made to

9

Below are some basic steps defined to frame and design the budgets as

General information – there are some general informations and data are collected form all the

departments. These data may be related to operational costs, payment receipts, bills etc.

Source of income – this is the second step which help in find out the source of income to

generate the finance and cash. Find out the payback period of getting payments are the main

sectors of this step.

Make a list of monthly expenses – All the payments and incomes are recorded in books of

accounts (Bennett and James, 2017). There is a list prepared to sort out the monthly expenses.

For example how much expenses are made on monthly purchase and manufacturing process are

counted in this method.

Break even analysis – how much amount of sale is required to generate minimum profit are

calculated by this method. It is one of the prominent and convenient method for managers

perspective. This method help in analysing the profit volume and sales ratio after adjustment of

variable and fixed cost.

Pricing strategies – this strategy is used to ascertain the cost and profit margin on product and

services of company. This step help in managing the cost and deciding the price of product.

Implementation – After making strategies and plan there is a practical analysis done by

implementation them in departments and functions of organisation.

Analysation – this steps indicates towards the measurement the performance of organisation

subject to proposed budget and plan.

Various type of pricing systems are used such as

Price skimming: this is the system which is used to analyse price subject to enhancing

profitability of organisation. Prices and sales prices are decided at initial stage.

Economic pricing: this system is used to determine optimum price of product in order to

earn optimum returns form operations.

P4 (c) Importance of budget as a tool of planning and control purpose

Budgeting and planning tools are considered as essential in organisational context.

Budgetary-control is one of the planning tool which helps in making cost effective budgets and

plans (Lachmann, Knauer and Trapp, 2013). Budgetary-control process system is implemented

in organisation to control the cost and set the margin of profit. Budgets and plans are made to

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

attain objectives and aims of organisation. Budgetary-control procedures enhanced the scope of

management accounting in organisational context.

In manufacturing and service providing organisations budgetary control process helps to

ascertain the targets and goals with available resources. Budgets shows the strength of

organisation in respect of analysing and forecasting the future events and incidents.

At managerial level budgets are used to make strategies and plans for better orations. It

provides a relevant data and functions regarding examine the position of organisation in market.

TASK 4

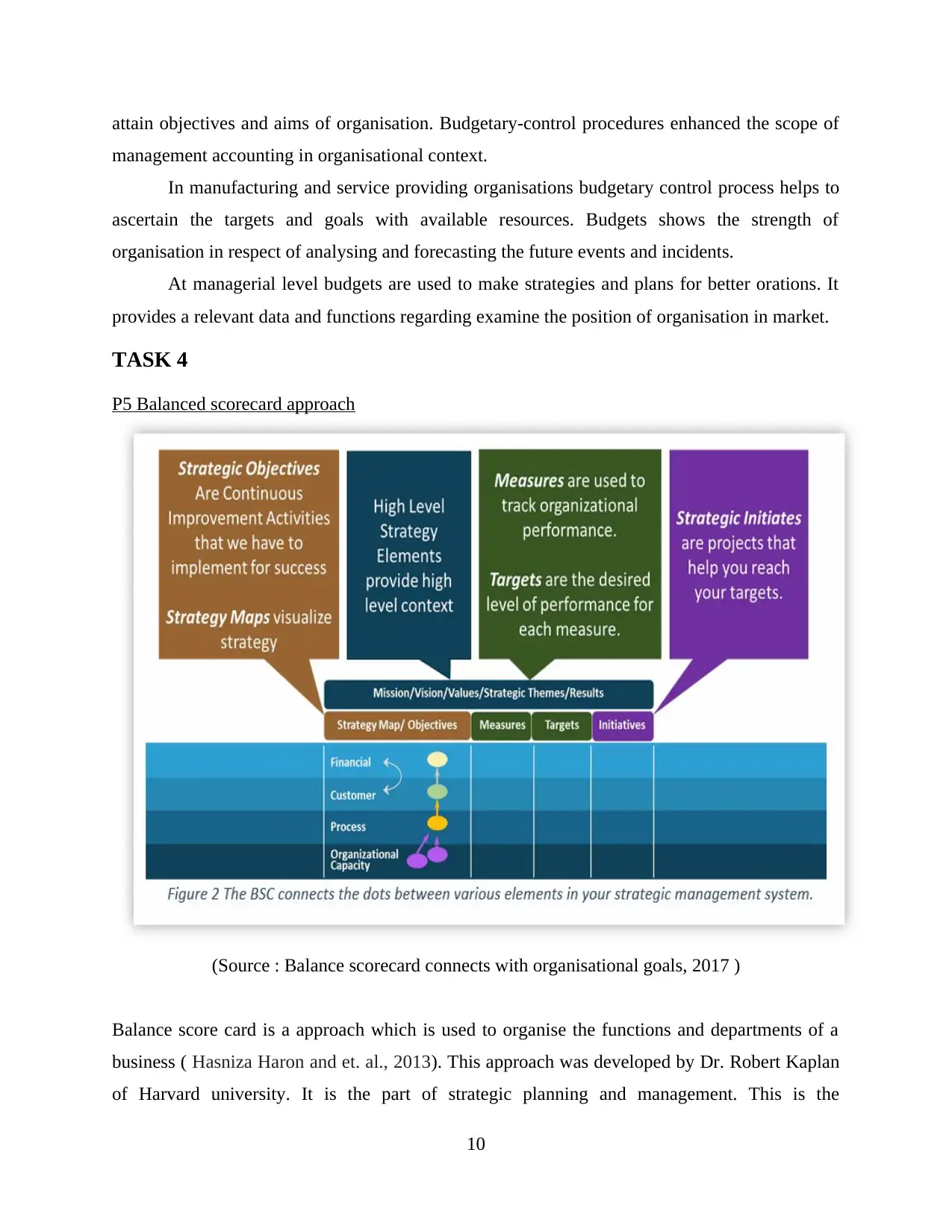

P5 Balanced scorecard approach

(Source : Balance scorecard connects with organisational goals, 2017 )

Balance score card is a approach which is used to organise the functions and departments of a

business ( Hasniza Haron and et. al., 2013). This approach was developed by Dr. Robert Kaplan

of Harvard university. It is the part of strategic planning and management. This is the

10

management accounting in organisational context.

In manufacturing and service providing organisations budgetary control process helps to

ascertain the targets and goals with available resources. Budgets shows the strength of

organisation in respect of analysing and forecasting the future events and incidents.

At managerial level budgets are used to make strategies and plans for better orations. It

provides a relevant data and functions regarding examine the position of organisation in market.

TASK 4

P5 Balanced scorecard approach

(Source : Balance scorecard connects with organisational goals, 2017 )

Balance score card is a approach which is used to organise the functions and departments of a

business ( Hasniza Haron and et. al., 2013). This approach was developed by Dr. Robert Kaplan

of Harvard university. It is the part of strategic planning and management. This is the

10

management tool which is used to connect and communicate organisational goals and objectives

to managers and employees. It provides a path to plan day to day process and activities subject to

task and projects. This management tool is used by large business entities, government, non

profit and social organisations. This approach remain divided in five steps;

Perspective – it provides a view to develop vision and objectives of organisation. There are some

measures KPIs, targets and initiatives are considered in this approach. Financial, customer/stake

holders, internal process, organisational capacity are the factors which are used in making

perspective.

Strategic objectives – This approach remain focused on continuous growth and development.

Break downs are the most common virtues which affect the process of framing vision and

mission of organisation. Selecting the options and take actions are the key sources in strategic

objectives.

Strategy mapping – there is a visual representation is made in strategic mapping which help to

execute the plans and strategies within the organisation. There are different type of performance

management graphs made on the basis of logical concepts and assumptions.

Measures – Some Key Performance Indicators are used to measure the performance and actions

of departments of organisation (Mahesha and Akash, 2013). Providing aims and objectives to

monitor the works and actions, focus the attention of employees towards the desired success,

deciding a common goal and communication level and reduce the intangible and uncertain

factors are the key points which are considered in this step.

Cascading – this is the step which remain divided in three levels as Tier 1, Tier 2, Tier 3.

cascading strategy help entire organisation to line up the tasks and projects subject to

organisational goals and objectives.

As per above given scenario Tech UK gain a loss of 1.5 billions which need to settle with

proper appropriation. Organisation need to analyse the use of management accounting system for

better administration and advancement. It is required to identify key financial indicators such as

liquidity, profitability and solvency ratio. Managers need to control operating expenses and

reduce non operating expenses in order to increase profitability of organisation.

CONCLUSION

Accounting and management both are essential and important aspect in organisational

context. An organisational structure depends upon effective plans and strategies. Management

11

to managers and employees. It provides a path to plan day to day process and activities subject to

task and projects. This management tool is used by large business entities, government, non

profit and social organisations. This approach remain divided in five steps;

Perspective – it provides a view to develop vision and objectives of organisation. There are some

measures KPIs, targets and initiatives are considered in this approach. Financial, customer/stake

holders, internal process, organisational capacity are the factors which are used in making

perspective.

Strategic objectives – This approach remain focused on continuous growth and development.

Break downs are the most common virtues which affect the process of framing vision and

mission of organisation. Selecting the options and take actions are the key sources in strategic

objectives.

Strategy mapping – there is a visual representation is made in strategic mapping which help to

execute the plans and strategies within the organisation. There are different type of performance

management graphs made on the basis of logical concepts and assumptions.

Measures – Some Key Performance Indicators are used to measure the performance and actions

of departments of organisation (Mahesha and Akash, 2013). Providing aims and objectives to

monitor the works and actions, focus the attention of employees towards the desired success,

deciding a common goal and communication level and reduce the intangible and uncertain

factors are the key points which are considered in this step.

Cascading – this is the step which remain divided in three levels as Tier 1, Tier 2, Tier 3.

cascading strategy help entire organisation to line up the tasks and projects subject to

organisational goals and objectives.

As per above given scenario Tech UK gain a loss of 1.5 billions which need to settle with

proper appropriation. Organisation need to analyse the use of management accounting system for

better administration and advancement. It is required to identify key financial indicators such as

liquidity, profitability and solvency ratio. Managers need to control operating expenses and

reduce non operating expenses in order to increase profitability of organisation.

CONCLUSION

Accounting and management both are essential and important aspect in organisational

context. An organisational structure depends upon effective plans and strategies. Management

11

and accounting help in storing the informations and data in particular data format. These

informations are used at high authorities level to make effective decision making strategies and

plans for better operations. This report is framed to differentiate the meaning of management

accounting and financial accounting. Different type of management reports are explained which

help in making plans and procedures. Various type of budgets are discussed and their importance

are bifurcated in practical demeanour. Absorption and marginal costing concept is illustrated

with a practical scenario. How budgetary-control process help in deciding the price and control

the cost also explained in this report.

12

informations are used at high authorities level to make effective decision making strategies and

plans for better operations. This report is framed to differentiate the meaning of management

accounting and financial accounting. Different type of management reports are explained which

help in making plans and procedures. Various type of budgets are discussed and their importance

are bifurcated in practical demeanour. Absorption and marginal costing concept is illustrated

with a practical scenario. How budgetary-control process help in deciding the price and control

the cost also explained in this report.

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Dumitru, M. and et. al. 2011. A historical approach of change in management accounting topics

published in Romania. Accounting and Management Information Systems. 10(3). p.375.

Zamora, V. L., 2011. Using a social enterprise service-learning strategy in an introductory

management accounting course. Issues in Accounting Education. 27(1). pp.187-226.

Gullkvist, B. M., 2013. Drivers of change in management accounting practices in an ERP

environment.

Moser, D. V., 2012. Is accounting research stagnant?. Accounting Horizons. 26(4). pp.845-850.

Leitner, S., 2013. Information Quality and Management Accounting: A Simulation Analysis of

Biases in Costing Systems (Vol. 664). Springer Science & Business Media.

Bennett, M. and James, P. eds., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Lachmann, M., Knauer, T. and Trapp, R., 2013. Strategic management accounting practices in

hospitals: Empirical evidence on their dissemination under competitive market

environments. Journal of Accounting & Organizational Change. 9(3). pp.336-369.

Hasniza Haron, N. and et. al., 2013. Management accounting practices and the turnaround

process. Asian Review of Accounting. 21(2). pp.100-112.

Mahesha, V. and Akash, S. B., 2013. Management Accounting Benefits: ERP Environment.

SCMS Journal of Indian Management. 10(3).

Lennox, C. S., Francis, J. R. and Wang, Z., 2011. Selection models in accounting research. The

Accounting Review. 87(2). pp.589-616.

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6). pp.407-419.

Pärl, Ü., 2012. Understanding the role of communication in the management accounting and

control process. Tampere University Press.

Michalak, J., 2013. Management accounting in networks-mapping the research streams. Zeszyty

Teoretyczne Rachunkowosci. 72(128).

Online

Balance scorecard connects with organisational goals, 2017. [Online] Available through

<http://www.balancedscorecard.org/BSC-Basics/About-the-Balanced-Scorecard>

13

Books and Journals

Dumitru, M. and et. al. 2011. A historical approach of change in management accounting topics

published in Romania. Accounting and Management Information Systems. 10(3). p.375.

Zamora, V. L., 2011. Using a social enterprise service-learning strategy in an introductory

management accounting course. Issues in Accounting Education. 27(1). pp.187-226.

Gullkvist, B. M., 2013. Drivers of change in management accounting practices in an ERP

environment.

Moser, D. V., 2012. Is accounting research stagnant?. Accounting Horizons. 26(4). pp.845-850.

Leitner, S., 2013. Information Quality and Management Accounting: A Simulation Analysis of

Biases in Costing Systems (Vol. 664). Springer Science & Business Media.

Bennett, M. and James, P. eds., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Lachmann, M., Knauer, T. and Trapp, R., 2013. Strategic management accounting practices in

hospitals: Empirical evidence on their dissemination under competitive market

environments. Journal of Accounting & Organizational Change. 9(3). pp.336-369.

Hasniza Haron, N. and et. al., 2013. Management accounting practices and the turnaround

process. Asian Review of Accounting. 21(2). pp.100-112.

Mahesha, V. and Akash, S. B., 2013. Management Accounting Benefits: ERP Environment.

SCMS Journal of Indian Management. 10(3).

Lennox, C. S., Francis, J. R. and Wang, Z., 2011. Selection models in accounting research. The

Accounting Review. 87(2). pp.589-616.

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6). pp.407-419.

Pärl, Ü., 2012. Understanding the role of communication in the management accounting and

control process. Tampere University Press.

Michalak, J., 2013. Management accounting in networks-mapping the research streams. Zeszyty

Teoretyczne Rachunkowosci. 72(128).

Online

Balance scorecard connects with organisational goals, 2017. [Online] Available through

<http://www.balancedscorecard.org/BSC-Basics/About-the-Balanced-Scorecard>

13

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.