Management Accounting Concepts and Practices

VerifiedAdded on 2020/01/07

|15

|4801

|265

Literature Review

AI Summary

This assignment delves into the core concepts and practices of management accounting. It examines the definition, functions, and scope of management accounting within various organizational contexts. Students will analyze real-world examples and case studies to understand how management accounting techniques inform strategic decision-making, performance evaluation, and cost control.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION........................................................................................................................................3

TASK 1.........................................................................................................................................................3

a) Definition of management accounting and there comparison with financial accounting and also

explain the management accounting as a decision-making tools ...........................................................3

b) Types of management accounting system..........................................................................................7

TASK 2.........................................................................................................................................................7

1. Absorption Costing..............................................................................................................................7

2. Marginal costing..................................................................................................................................8

TASK 3.......................................................................................................................................................10

a) Types of budget and there advantages/ dis-advantage......................................................................10

b) Process of preparing budget..............................................................................................................11

c) Pricing strategies................................................................................................................................12

TASK 4.......................................................................................................................................................12

(A) Balance Score card and use of balance score card to identify and responding to financial problems

...............................................................................................................................................................12

1. Use of Balance score card in identifying and responding to financial problems .............................12

2. Use of balance score card in order to improve the financial governance..........................................13

CONCLUSION..........................................................................................................................................13

REFERENCES...........................................................................................................................................15

INTRODUCTION........................................................................................................................................3

TASK 1.........................................................................................................................................................3

a) Definition of management accounting and there comparison with financial accounting and also

explain the management accounting as a decision-making tools ...........................................................3

b) Types of management accounting system..........................................................................................7

TASK 2.........................................................................................................................................................7

1. Absorption Costing..............................................................................................................................7

2. Marginal costing..................................................................................................................................8

TASK 3.......................................................................................................................................................10

a) Types of budget and there advantages/ dis-advantage......................................................................10

b) Process of preparing budget..............................................................................................................11

c) Pricing strategies................................................................................................................................12

TASK 4.......................................................................................................................................................12

(A) Balance Score card and use of balance score card to identify and responding to financial problems

...............................................................................................................................................................12

1. Use of Balance score card in identifying and responding to financial problems .............................12

2. Use of balance score card in order to improve the financial governance..........................................13

CONCLUSION..........................................................................................................................................13

REFERENCES...........................................................................................................................................15

INTRODUCTION

Management accounting is a process which includes all such information which help the

managers to accomplish there goals. It include all the information and decision which is related to the

policy making process, procedures etc. that help the manager to all the funds in an organisation.

Management process includes the managerial functions such as planning, staffing, controlling and

monitoring process that manage all the activity in an organisation. By the help of management

accounting is also make smoothing the activity, so that management accounting is essential for the

business. Inn this research report IMDA Tech (UK) Limited is taken, which is a producer of the different

mobile chargers. There main function is to provide specific charger of the mobile and telephone and also

create different gadgets for the UK retail outlets.

This report describes the role of management accounting by explaining there concept in an

organisation. It also gives the importance of management accounting by comparing with the fiscal

accountancy. It also describes the role of management accounting as a decision making tool in an

organisation. In this report different budget are describes and it also represent the advantage and dis-

advantage of such budget and pricing strategies which affect the organisation's operational activity. By

using the marginal cost and absorption method, it also helps to analysis the cost and net yield of the

IMDA Tech (UK) Ltd. This report also highlight the financial problems and describes the role of

organisation to resolve such problems effectively(Vakalfotis, Ballantine and Wall, 2013.).

TASK 1

a) Definition of management accounting and there comparison with financial accounting and also

explain the management accounting as a decision-making tools

To: Imda Limited, Line Manager

From: Management Accounting Officer

Date: 20 May 2017

Subject: Management accountancy significant and its deviation from the financial accounting

Management accounting includes various managerial functions such as planning, staffing,

organising, controlling and monitoring the activity within the organisation. In this way all this strategies

make the business operations effectively and smoothly. Management accounting also supplies the

information, and facts which are reliable so that it can help the effective work for the organisation.

Difference between Financial and Management Accounting

Basis for Comparison Financial Accounting Management Accounting

Management accounting is a process which includes all such information which help the

managers to accomplish there goals. It include all the information and decision which is related to the

policy making process, procedures etc. that help the manager to all the funds in an organisation.

Management process includes the managerial functions such as planning, staffing, controlling and

monitoring process that manage all the activity in an organisation. By the help of management

accounting is also make smoothing the activity, so that management accounting is essential for the

business. Inn this research report IMDA Tech (UK) Limited is taken, which is a producer of the different

mobile chargers. There main function is to provide specific charger of the mobile and telephone and also

create different gadgets for the UK retail outlets.

This report describes the role of management accounting by explaining there concept in an

organisation. It also gives the importance of management accounting by comparing with the fiscal

accountancy. It also describes the role of management accounting as a decision making tool in an

organisation. In this report different budget are describes and it also represent the advantage and dis-

advantage of such budget and pricing strategies which affect the organisation's operational activity. By

using the marginal cost and absorption method, it also helps to analysis the cost and net yield of the

IMDA Tech (UK) Ltd. This report also highlight the financial problems and describes the role of

organisation to resolve such problems effectively(Vakalfotis, Ballantine and Wall, 2013.).

TASK 1

a) Definition of management accounting and there comparison with financial accounting and also

explain the management accounting as a decision-making tools

To: Imda Limited, Line Manager

From: Management Accounting Officer

Date: 20 May 2017

Subject: Management accountancy significant and its deviation from the financial accounting

Management accounting includes various managerial functions such as planning, staffing,

organising, controlling and monitoring the activity within the organisation. In this way all this strategies

make the business operations effectively and smoothly. Management accounting also supplies the

information, and facts which are reliable so that it can help the effective work for the organisation.

Difference between Financial and Management Accounting

Basis for Comparison Financial Accounting Management Accounting

Meaning Fiscal accountancy is a process

which consider all the financial

activity such as preparing the

financial statements such as

profit and loss a/c, balance

sheet , cash flow, ratio analysis

etc.

In management accounting, it

includes all the managerial

functions such as planning,

staffing, controlling and

motivating the workers in an

organisation, so that it can help

the organisation to work with

there great efferents or

accomplish there goals in future.

For example: Such information

which is helpful to decision

making, analysis the cash flow

by using appropriate data etc.

Necessary in organisation For every business organisation,

financial accounting is useful

and essential. For example:

Imda limited also require to

maintain there financial

statement to analysis there actual

position at the end of the

financial year.

But management accounting is

not necessary for every

organisation. As per the need of

the manger or activity,

management accounting can be

done. For example: If Imda

limited's managers wanted to

know the data and information

related to the resources, in this

case they can maintain the

management accounting so that

they can analysis the position of

resources in an organisation.

Objectives/Motives The main motive to make

financial accounting to get the

actual financial position of the

company, so that it will help to

all different kind of interested

This main objective is to make

an effective managerial control

in an organisation. For example:

If Imda Ltd manger want to

analysis the records, than

which consider all the financial

activity such as preparing the

financial statements such as

profit and loss a/c, balance

sheet , cash flow, ratio analysis

etc.

In management accounting, it

includes all the managerial

functions such as planning,

staffing, controlling and

motivating the workers in an

organisation, so that it can help

the organisation to work with

there great efferents or

accomplish there goals in future.

For example: Such information

which is helpful to decision

making, analysis the cash flow

by using appropriate data etc.

Necessary in organisation For every business organisation,

financial accounting is useful

and essential. For example:

Imda limited also require to

maintain there financial

statement to analysis there actual

position at the end of the

financial year.

But management accounting is

not necessary for every

organisation. As per the need of

the manger or activity,

management accounting can be

done. For example: If Imda

limited's managers wanted to

know the data and information

related to the resources, in this

case they can maintain the

management accounting so that

they can analysis the position of

resources in an organisation.

Objectives/Motives The main motive to make

financial accounting to get the

actual financial position of the

company, so that it will help to

all different kind of interested

This main objective is to make

an effective managerial control

in an organisation. For example:

If Imda Ltd manger want to

analysis the records, than

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

parties. For example: If the

shareholders of Imda limited

wanted there financial position

because there motive is that as

per determining the company's

position they can decide how

much capital investment is

beneficial for them(Schaltegger,

Gibassier and Zvezdov, 2013).

managers can use information for

effective business planning.

Information Financial accounting includes

information which is fully based

on monetary term. For example:

If Imda lit choose to take

financial accounting in there

work, than they only includes all

those items in there balance sheet

which are expressed in the

money value.

But in management accounting,

it requires both monetary and

non- monetary value. For

example: In management

accounting, it make full records

of company's all expenses and

income which are expressed in

money term but is also make full

records of resources which are

come and out from the company.

So that such resources are

expressed in non-monetary

value.

Format Financial accounting requires

balance sheet, income statement

such as profit and loss account,

which follow there specific

accounting rules.

In management accounting there

is no specific accounting rules

are followed, because in

management accounting all the

decision are taken by the

managers as per the need. So that

in management accounting there

is no formate provision for

planning process etc.

Users All the statements which are But management accounting is

shareholders of Imda limited

wanted there financial position

because there motive is that as

per determining the company's

position they can decide how

much capital investment is

beneficial for them(Schaltegger,

Gibassier and Zvezdov, 2013).

managers can use information for

effective business planning.

Information Financial accounting includes

information which is fully based

on monetary term. For example:

If Imda lit choose to take

financial accounting in there

work, than they only includes all

those items in there balance sheet

which are expressed in the

money value.

But in management accounting,

it requires both monetary and

non- monetary value. For

example: In management

accounting, it make full records

of company's all expenses and

income which are expressed in

money term but is also make full

records of resources which are

come and out from the company.

So that such resources are

expressed in non-monetary

value.

Format Financial accounting requires

balance sheet, income statement

such as profit and loss account,

which follow there specific

accounting rules.

In management accounting there

is no specific accounting rules

are followed, because in

management accounting all the

decision are taken by the

managers as per the need. So that

in management accounting there

is no formate provision for

planning process etc.

Users All the statements which are But management accounting is

prepared by the financial

accounting are used by all the

internal and outer users. For

example: In internal users it

includes managers, employers

etc. and outer users it includes

Government, Shareholders etc.

only done by the internal parties

of an organisation, so that it is

only used for the employers,

employees and managers etc.

Time Frame Financial accounting are made at

the end of financial year or

accounting year. For example: 1

April to 31 March is considered

as a accounting period of an

organisation(Wajeetongratana,

2016).

Management accounting not

required any time frame for there

operations. Whenever the

manager feels that there is

necessary of making

management report they can use

management accounting in any

time.

Establishment and Auditing

Requirement

There are the provision that

financial accounting must be

published and audited by the

statutory auditor.

In management accounting there

is no requirement to making any

publication and auditing of the

report.

Importance of management accounting information as a decision making tools

Management accounting helps to analysis the cost of each resources so that managers can

determine the actual usage of resources, after that they can allocate the cost in different areas as per the

need of the departments. In this way, managers can minimize there cost so that they can maximize there

profitability. In this case IMDA Limited always check there cost in such a way that it was effective or

not for the organisation.

Management accounting also plays an important role to decide the effective costing techniques.

In this way Imda Ltd can determine the effective costing techniques such that in which manner

resources are buy or sell. In this way company should minimize the cost by using effective techniques

for the costing. So that while making an effective costing techniques, ABC costing is considered by

Imda so that it will help to maximize there profitability of an organisation.

Management accounting provides the data for the managers so that they can analysis each and

every conditions of the business. Such information helps the Imda limited to take effective decision

accounting are used by all the

internal and outer users. For

example: In internal users it

includes managers, employers

etc. and outer users it includes

Government, Shareholders etc.

only done by the internal parties

of an organisation, so that it is

only used for the employers,

employees and managers etc.

Time Frame Financial accounting are made at

the end of financial year or

accounting year. For example: 1

April to 31 March is considered

as a accounting period of an

organisation(Wajeetongratana,

2016).

Management accounting not

required any time frame for there

operations. Whenever the

manager feels that there is

necessary of making

management report they can use

management accounting in any

time.

Establishment and Auditing

Requirement

There are the provision that

financial accounting must be

published and audited by the

statutory auditor.

In management accounting there

is no requirement to making any

publication and auditing of the

report.

Importance of management accounting information as a decision making tools

Management accounting helps to analysis the cost of each resources so that managers can

determine the actual usage of resources, after that they can allocate the cost in different areas as per the

need of the departments. In this way, managers can minimize there cost so that they can maximize there

profitability. In this case IMDA Limited always check there cost in such a way that it was effective or

not for the organisation.

Management accounting also plays an important role to decide the effective costing techniques.

In this way Imda Ltd can determine the effective costing techniques such that in which manner

resources are buy or sell. In this way company should minimize the cost by using effective techniques

for the costing. So that while making an effective costing techniques, ABC costing is considered by

Imda so that it will help to maximize there profitability of an organisation.

Management accounting provides the data for the managers so that they can analysis each and

every conditions of the business. Such information helps the Imda limited to take effective decision

related to there operational activity. In this way by making an effective report of the business by using

the relevant data, it will help the organisation to take effective decision which are best for the company.

As a instrument of determination devising it consider to analyse the magnitude relation, fiscal

perspective of the company, and also aid to prediction in fund such as currency change of location and

there various deviation which is related to the Imda limited.

b) Types of management accounting system

Cost accounting system- Cost accounting system is helpful to determine the actual cost in an

organisation. It is done so because it increases the chances of profitability in the the organisation. There

are various methods which are used in estimating the actual cost. So Imda limited firstly determine the

cost that it is normal, actual or standard(Morales and Lambert, 2013). Normal cost represent that such

cost which are entering into the business having there real value, but in actual cost it includes the actual

market value of the cost. So that to form cost accounting, occupation order of magnitude costing and

process costing can be used so that all this methods can improve the value of report in an organisation.

Inventory management system- It is a computing device - based system which aid the structure

for path the plane of stock, orders, sales etc. It also utilized by making a command of work, invoice for

all the substantial and other representation which is affiliated to the acquisition(Vakalfotis, Ballantine

and Wall, 2013). So that various section can change there reports by carry off there orders, pursuing

there assets, negotiate there services, characteristic there commodity and by optimizing there stock list.

For example: wired chase, radio-relative frequency determination etc. are the instrument of stock

direction scheme.

Job costing system- Job costing are used in an organisation because the products which produce

in a business are different with each other. In this way, business can apply the job costing system so that

they can improve the product quality by using custom equipment so that the quality of each products will

be improved.

Price optimising system- Price optimising system is a system by following such system, producer

can determine the level of satisfaction of the customers with the products which are rendered by the the

company(Lavia López and Hiebl, 2014). In this way, producer should fixed there price by optimising

them, so that it will satisfied the customers demand and also achieve there profitability. For example: If

Imda limited setting there price they go to the help of retail, banking, airlines etc. to maximize there

prices.

the relevant data, it will help the organisation to take effective decision which are best for the company.

As a instrument of determination devising it consider to analyse the magnitude relation, fiscal

perspective of the company, and also aid to prediction in fund such as currency change of location and

there various deviation which is related to the Imda limited.

b) Types of management accounting system

Cost accounting system- Cost accounting system is helpful to determine the actual cost in an

organisation. It is done so because it increases the chances of profitability in the the organisation. There

are various methods which are used in estimating the actual cost. So Imda limited firstly determine the

cost that it is normal, actual or standard(Morales and Lambert, 2013). Normal cost represent that such

cost which are entering into the business having there real value, but in actual cost it includes the actual

market value of the cost. So that to form cost accounting, occupation order of magnitude costing and

process costing can be used so that all this methods can improve the value of report in an organisation.

Inventory management system- It is a computing device - based system which aid the structure

for path the plane of stock, orders, sales etc. It also utilized by making a command of work, invoice for

all the substantial and other representation which is affiliated to the acquisition(Vakalfotis, Ballantine

and Wall, 2013). So that various section can change there reports by carry off there orders, pursuing

there assets, negotiate there services, characteristic there commodity and by optimizing there stock list.

For example: wired chase, radio-relative frequency determination etc. are the instrument of stock

direction scheme.

Job costing system- Job costing are used in an organisation because the products which produce

in a business are different with each other. In this way, business can apply the job costing system so that

they can improve the product quality by using custom equipment so that the quality of each products will

be improved.

Price optimising system- Price optimising system is a system by following such system, producer

can determine the level of satisfaction of the customers with the products which are rendered by the the

company(Lavia López and Hiebl, 2014). In this way, producer should fixed there price by optimising

them, so that it will satisfied the customers demand and also achieve there profitability. For example: If

Imda limited setting there price they go to the help of retail, banking, airlines etc. to maximize there

prices.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

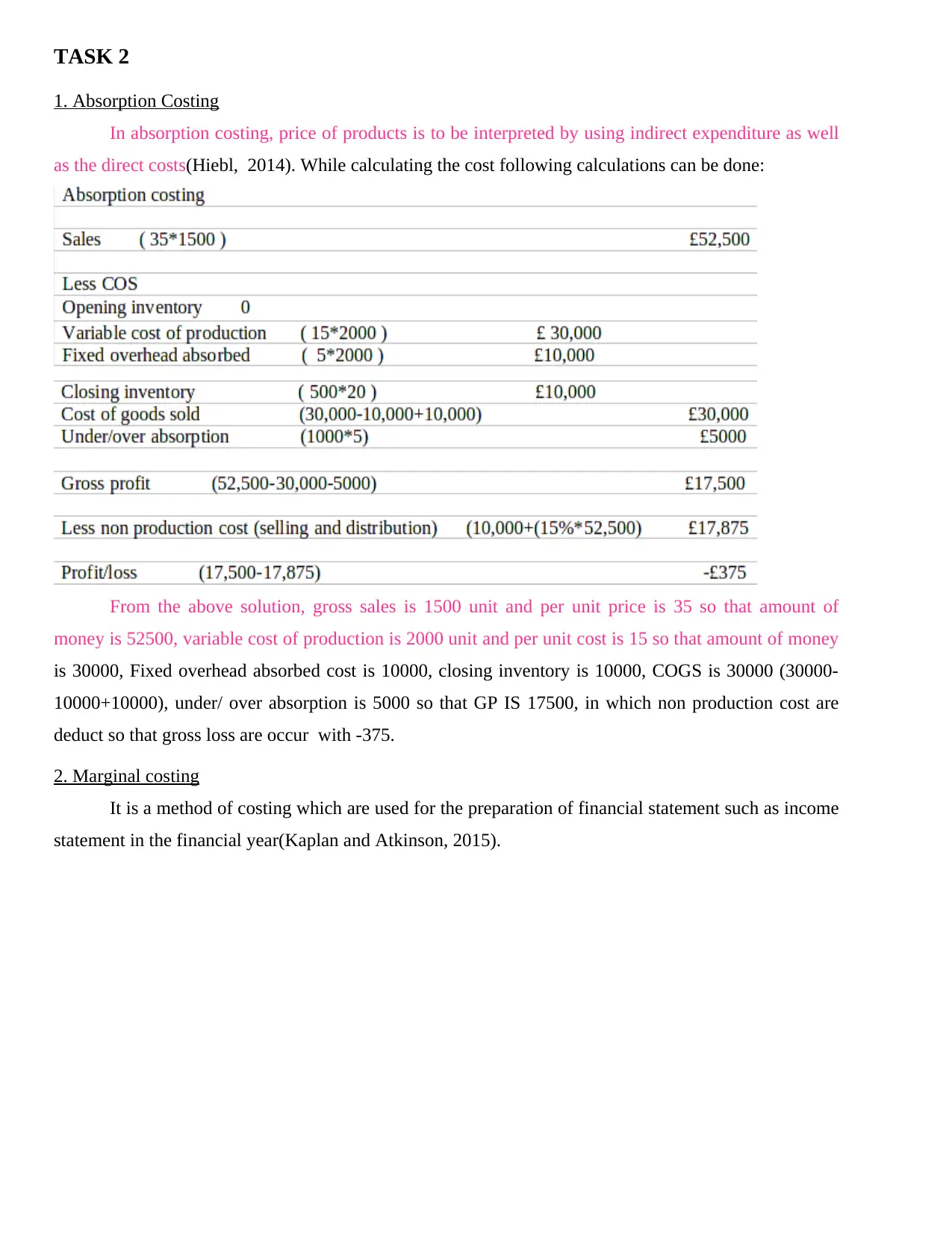

1. Absorption Costing

In absorption costing, price of products is to be interpreted by using indirect expenditure as well

as the direct costs(Hiebl, 2014). While calculating the cost following calculations can be done:

From the above solution, gross sales is 1500 unit and per unit price is 35 so that amount of

money is 52500, variable cost of production is 2000 unit and per unit cost is 15 so that amount of money

is 30000, Fixed overhead absorbed cost is 10000, closing inventory is 10000, COGS is 30000 (30000-

10000+10000), under/ over absorption is 5000 so that GP IS 17500, in which non production cost are

deduct so that gross loss are occur with -375.

2. Marginal costing

It is a method of costing which are used for the preparation of financial statement such as income

statement in the financial year(Kaplan and Atkinson, 2015).

1. Absorption Costing

In absorption costing, price of products is to be interpreted by using indirect expenditure as well

as the direct costs(Hiebl, 2014). While calculating the cost following calculations can be done:

From the above solution, gross sales is 1500 unit and per unit price is 35 so that amount of

money is 52500, variable cost of production is 2000 unit and per unit cost is 15 so that amount of money

is 30000, Fixed overhead absorbed cost is 10000, closing inventory is 10000, COGS is 30000 (30000-

10000+10000), under/ over absorption is 5000 so that GP IS 17500, in which non production cost are

deduct so that gross loss are occur with -375.

2. Marginal costing

It is a method of costing which are used for the preparation of financial statement such as income

statement in the financial year(Kaplan and Atkinson, 2015).

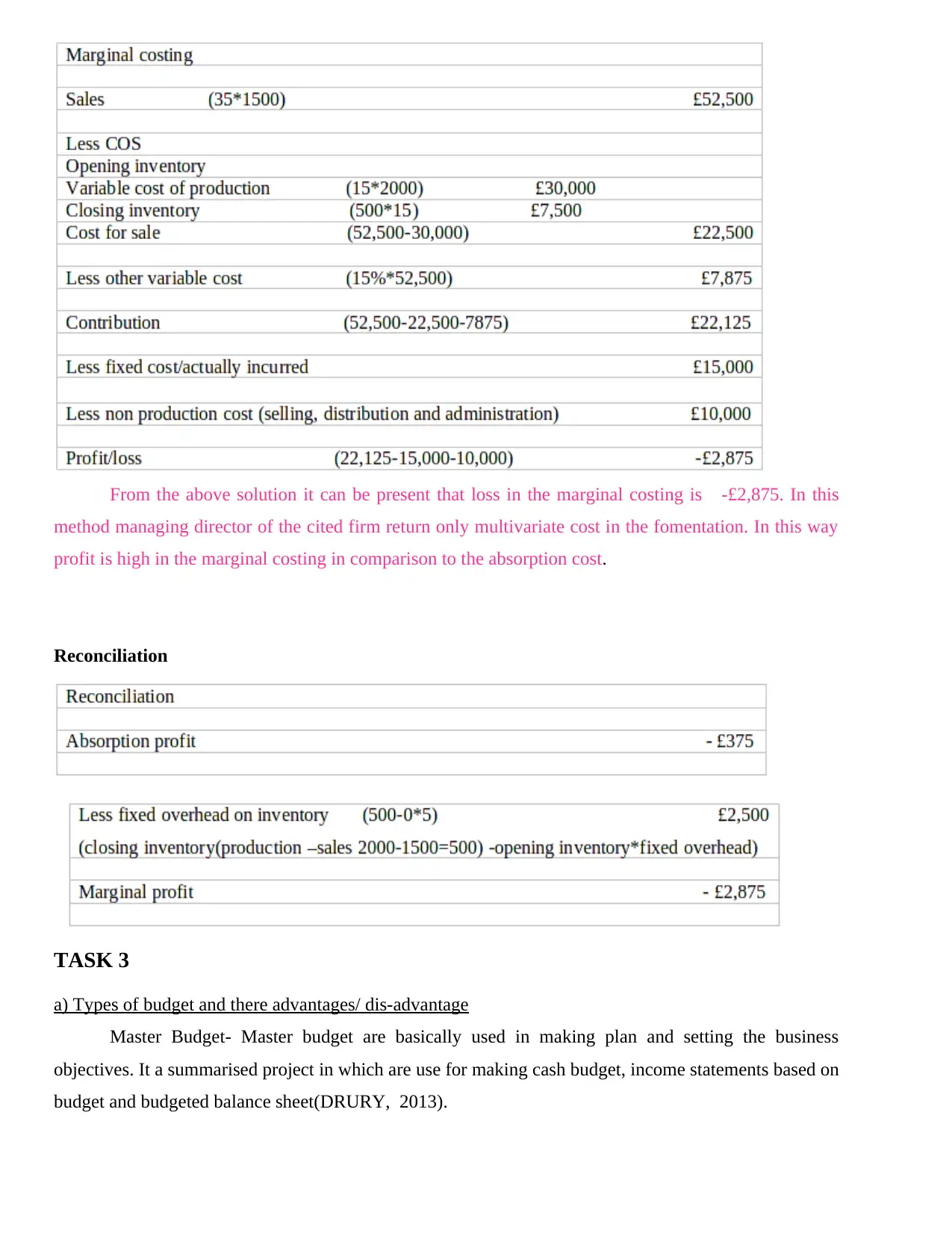

From the above solution it can be present that loss in the marginal costing is -£2,875. In this

method managing director of the cited firm return only multivariate cost in the fomentation. In this way

profit is high in the marginal costing in comparison to the absorption cost.

Reconciliation

TASK 3

a) Types of budget and there advantages/ dis-advantage

Master Budget- Master budget are basically used in making plan and setting the business

objectives. It a summarised project in which are use for making cash budget, income statements based on

budget and budgeted balance sheet(DRURY, 2013).

method managing director of the cited firm return only multivariate cost in the fomentation. In this way

profit is high in the marginal costing in comparison to the absorption cost.

Reconciliation

TASK 3

a) Types of budget and there advantages/ dis-advantage

Master Budget- Master budget are basically used in making plan and setting the business

objectives. It a summarised project in which are use for making cash budget, income statements based on

budget and budgeted balance sheet(DRURY, 2013).

Operational budget- Operational budget relates to the operational activity of the business. It

includes the day- to- day revenues and expenses such as all type of overheads, cost, expenses etc. In this

budget, manager use this information to compare the results throughout the year. All the inflows and

outflows are compared with each other, in this case any variance are generated in revenue can be

adjusted in this type of budget.

Cash flow budget- This budget mainly focus on the net cash inflow and outflow during the

accounting year. On the basis of such estimation, cash requirement in a business is estimated at a specific

time duration(Cooper, Ezzamel and Qu, 2017).

Financial budget- Financial budget mainly prepare to determine the financial requirement in a

business. It analysis that how much funds are used in the operational activity and how much fund are

required in the future.

Advantages of budget

Budget provide the sufficient information about the business operational activity.

It also help to find out the strength and weakness of the organization.

It also assist to identify the business performance in future.

It is a best techniques which help to maximize the resources so that such resources can use

effectively.

Budgets also increases the profitability of the company.

It is considered as a best tool to allocate the funds and assets in an organisation.

Dis-advantages of budget

By making wrong estimation of the budget it make negative impact in financial preparation and

dealing of a business.

Budgets are successful as per the estimation of past and forthcoming events. Such events are

unpredictable so that it is hard to make an effective management of business.

By making budget in a business, it is very time consuming and costly process done by the

manager.

b) Process of preparing budget

Gather Information- The first step is the collecting the information related to all type of expenses

and income during the year. In this way, Imda limited prepare a statements of bills, loans etc. which are

incurred during the year.

Recording all the sources of income- Imda limited should record all the sources of income such

as income from investment, income from sale etc. In this way, company should record all the sources so

that manger can estimate the budget for accomplishment of the operational activity.

includes the day- to- day revenues and expenses such as all type of overheads, cost, expenses etc. In this

budget, manager use this information to compare the results throughout the year. All the inflows and

outflows are compared with each other, in this case any variance are generated in revenue can be

adjusted in this type of budget.

Cash flow budget- This budget mainly focus on the net cash inflow and outflow during the

accounting year. On the basis of such estimation, cash requirement in a business is estimated at a specific

time duration(Cooper, Ezzamel and Qu, 2017).

Financial budget- Financial budget mainly prepare to determine the financial requirement in a

business. It analysis that how much funds are used in the operational activity and how much fund are

required in the future.

Advantages of budget

Budget provide the sufficient information about the business operational activity.

It also help to find out the strength and weakness of the organization.

It also assist to identify the business performance in future.

It is a best techniques which help to maximize the resources so that such resources can use

effectively.

Budgets also increases the profitability of the company.

It is considered as a best tool to allocate the funds and assets in an organisation.

Dis-advantages of budget

By making wrong estimation of the budget it make negative impact in financial preparation and

dealing of a business.

Budgets are successful as per the estimation of past and forthcoming events. Such events are

unpredictable so that it is hard to make an effective management of business.

By making budget in a business, it is very time consuming and costly process done by the

manager.

b) Process of preparing budget

Gather Information- The first step is the collecting the information related to all type of expenses

and income during the year. In this way, Imda limited prepare a statements of bills, loans etc. which are

incurred during the year.

Recording all the sources of income- Imda limited should record all the sources of income such

as income from investment, income from sale etc. In this way, company should record all the sources so

that manger can estimate the budget for accomplishment of the operational activity.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Create a list of monthly expenses- A company should create a complete records of all the

expenses such as salaries, wages, bonus, repair and maintenance expenditure, selling expenses,

administration expenses etc. In this way Imda limited UK, make a complete records of all the expenses

in the form of income statement, so that manager can determine such records for estimation of future

budget.

Break expenses into categories- To preparing a budget, company should divide all the expenses

into there sub- categories such as fixed expenses and variable expenses(Brandau, Endenich, Trapp and

Hoffjan, 2013). Fixed expenses are such expenses which are same from every month, for example: fixed

loan repayment, mortgage etc. Variable expenses are those expenses which are fluctuating over the

month. For example: Gifts, vacations expenses etc.

Available funding- After estimating all the expenses and income or determining the budget

assumptions, the next step it to secure the available funds. This step is do so because by estimating the

funds, managers can determine the actual need of fund in a company. As per the available fund, it is

helpful to the company to allocate the resources in such an areas which is required for the funds.

Receiving income prediction and section fund- Later creating a budget accumulation, income and

role in departments can be prediction in this phase. For foretelling the division fund, Imda cover can

form a judgement which are successful for performance. Successful financial gain of the section and

here the performance can-full modification in it. Aside set up a activity program are helpful for effectual

apportionment of assets and beginning(Fullerton, Kennedy and Widener, 2014). Therefore, away move

ahead preceding each path a appropriate fund can be successful for Imda Limited for here flourishing

plan of action.

c) Evaluation strategies:-

Administration controller of the Imda limited setting here product's price by there production

and distribution system. A business can use various type of pricing strategies to sell there products and

services. This price is set up by the accountant to secure the business's profitability. In this way, pricing

is a best way to create a demand of the products in a market. Effective pricing strategies attract there

customers so that they can buy the products in a company. In this race, Imda Limited always try to set-

up there price by using different pricing model. Company can use absorption pricing, high-low pricing,

terminal point pricing, minimum cost pricing, odd number pricing, cost plus evaluation and premium

pricing model to set there product's price.

In absorption pricing, company can use the variable cost of each unit in there products but in

high-low pricing they should maintain there price higher in case of competition but in condition of

promotion time, they should reduce there product's price in the market. In case of limit pricing, company

expenses such as salaries, wages, bonus, repair and maintenance expenditure, selling expenses,

administration expenses etc. In this way Imda limited UK, make a complete records of all the expenses

in the form of income statement, so that manager can determine such records for estimation of future

budget.

Break expenses into categories- To preparing a budget, company should divide all the expenses

into there sub- categories such as fixed expenses and variable expenses(Brandau, Endenich, Trapp and

Hoffjan, 2013). Fixed expenses are such expenses which are same from every month, for example: fixed

loan repayment, mortgage etc. Variable expenses are those expenses which are fluctuating over the

month. For example: Gifts, vacations expenses etc.

Available funding- After estimating all the expenses and income or determining the budget

assumptions, the next step it to secure the available funds. This step is do so because by estimating the

funds, managers can determine the actual need of fund in a company. As per the available fund, it is

helpful to the company to allocate the resources in such an areas which is required for the funds.

Receiving income prediction and section fund- Later creating a budget accumulation, income and

role in departments can be prediction in this phase. For foretelling the division fund, Imda cover can

form a judgement which are successful for performance. Successful financial gain of the section and

here the performance can-full modification in it. Aside set up a activity program are helpful for effectual

apportionment of assets and beginning(Fullerton, Kennedy and Widener, 2014). Therefore, away move

ahead preceding each path a appropriate fund can be successful for Imda Limited for here flourishing

plan of action.

c) Evaluation strategies:-

Administration controller of the Imda limited setting here product's price by there production

and distribution system. A business can use various type of pricing strategies to sell there products and

services. This price is set up by the accountant to secure the business's profitability. In this way, pricing

is a best way to create a demand of the products in a market. Effective pricing strategies attract there

customers so that they can buy the products in a company. In this race, Imda Limited always try to set-

up there price by using different pricing model. Company can use absorption pricing, high-low pricing,

terminal point pricing, minimum cost pricing, odd number pricing, cost plus evaluation and premium

pricing model to set there product's price.

In absorption pricing, company can use the variable cost of each unit in there products but in

high-low pricing they should maintain there price higher in case of competition but in condition of

promotion time, they should reduce there product's price in the market. In case of limit pricing, company

should limit there price so that they can reduce the entry of new firm in the monopolist situation. In cost

plus pricing, company set there products and services prices in a cost based method. Furthermore, Imda

Tech Ltd can also go with skimming pricing strategy. In this way, company can set-up there prices as per

the market and customer condition, so that they can earn profit with giving customer satisfaction.

TASK 4

(A) Equilibrium Rating card and usage of scale rating card to identify and state to financial problems:-

Equilibrium Rating card is the theoretical account thet is used to evidence and negotiate the

business organisation fit. It about rarely exploited to carry plan of action of entity to existence and assist

into organise the plan of action crosswise the business firm (Miller and Kelber, 2015).

1. Utilization of Equilibrium score card for identifying and state to fiscal problems:-

The equilibrium scorecard is exploited by Imda Tech Ltd in order of magnitude to fit there

standard and so that can fulfil there goals in future. It is a process which focuses on various elements

such as process of the business, human resources, perspectives of customers, capital invested by the

investors etc. By using the balance scorecard, it helps to create new and innovative things in a workplace

(Bodie, 2013). It is a best techniques by which company can analysis there performance and take

corrective action for the improvement. With the help of balance score card, it will help the IMDA Tech

Limited to achieve and compete with the competitors . As per the inquiry its analysis that Imda Tech

Limited face the failure of 1.8 meg GBP so that balance score help the firm to identify there weakness

and strength. In this way balance scorecard is best techniques that can help the firm to overcoming for

there financial crisis. There qare various SMART objectives of the Imda Tech Limited, which are as

follows:

To increase there sales volumes till the end of accounting period with 40%

To increase the rate of retention by 20% to 40% in 2016

To increases there revenue by 30% in 2016

2. Use of equilibrium rating card in order of magnitude to modify the financial administration

Proportion rating card is the instrument that assist inch facing the problems of the structure or

advise to the manager that can aid in partitioning the financial difficulty of the organization in future.

Imda Ltd intent focusing along the client neediness so that it can execute their ascendant that decrease its

financial difficulty. It will be helpinattracting wide range of group and will heighten sales property of

the entity to large level. Separated from this inner business concern enterprise exercise also enclosed

the equilibrium rating card formulation. Administration reviews the performance of worker and organize

scholarship difficulty for them who are unable to execute their responsibility in a proper way.

plus pricing, company set there products and services prices in a cost based method. Furthermore, Imda

Tech Ltd can also go with skimming pricing strategy. In this way, company can set-up there prices as per

the market and customer condition, so that they can earn profit with giving customer satisfaction.

TASK 4

(A) Equilibrium Rating card and usage of scale rating card to identify and state to financial problems:-

Equilibrium Rating card is the theoretical account thet is used to evidence and negotiate the

business organisation fit. It about rarely exploited to carry plan of action of entity to existence and assist

into organise the plan of action crosswise the business firm (Miller and Kelber, 2015).

1. Utilization of Equilibrium score card for identifying and state to fiscal problems:-

The equilibrium scorecard is exploited by Imda Tech Ltd in order of magnitude to fit there

standard and so that can fulfil there goals in future. It is a process which focuses on various elements

such as process of the business, human resources, perspectives of customers, capital invested by the

investors etc. By using the balance scorecard, it helps to create new and innovative things in a workplace

(Bodie, 2013). It is a best techniques by which company can analysis there performance and take

corrective action for the improvement. With the help of balance score card, it will help the IMDA Tech

Limited to achieve and compete with the competitors . As per the inquiry its analysis that Imda Tech

Limited face the failure of 1.8 meg GBP so that balance score help the firm to identify there weakness

and strength. In this way balance scorecard is best techniques that can help the firm to overcoming for

there financial crisis. There qare various SMART objectives of the Imda Tech Limited, which are as

follows:

To increase there sales volumes till the end of accounting period with 40%

To increase the rate of retention by 20% to 40% in 2016

To increases there revenue by 30% in 2016

2. Use of equilibrium rating card in order of magnitude to modify the financial administration

Proportion rating card is the instrument that assist inch facing the problems of the structure or

advise to the manager that can aid in partitioning the financial difficulty of the organization in future.

Imda Ltd intent focusing along the client neediness so that it can execute their ascendant that decrease its

financial difficulty. It will be helpinattracting wide range of group and will heighten sales property of

the entity to large level. Separated from this inner business concern enterprise exercise also enclosed

the equilibrium rating card formulation. Administration reviews the performance of worker and organize

scholarship difficulty for them who are unable to execute their responsibility in a proper way.

Equilibrium rating card help the Imda Ltd in decreasing the space 'tween anticipated and existent

commercial enterprise execution and outcomes (Sundem. and et. al, 2014). With the help of this concept

cited firm purpose be able to execute its subjective well.

CONCLUSION

From the above written report it can be terminated that administration account is an necessary

instrument that help the structure in realize their issues and influence in achieving the cognitive content

of the entity important. It is the method that influence in commute the origin well so that operable cost

of the entity can be reduced(Simons, 2013). It container be said that adoption of onset pricing strategy is

helpful that influence in compound the profitableness of the entity to large extent. This written document

is terminated that administration accounting is an formulation of management by which generic

enterprise dealing get on managed. Therefore, various governing body instrument are ascertained for

assigning money for Imda limited. Considering this, cost accounting such as absorption and minimum is

advised for set up financial gain evidence that presents fiscal point of organisation. Furthermore,

captious valuation on fund is given for foretelling and determination for advance business trading

operations. According several kinds of fund and its planning process is thoughtful this assignment.

However, valuation strategies for surround costs according to various determinants are represented for

cost potency as well proper establishment of entity is acknowledged. Apart from this, fiscal evidence

investigation is acquire by which current business performance is analysed that is impressive to reduce

economical problems occur at geographic point. Consider this, importance of administration system is

explicit which is used to change governing body and development effective plan of action at high level.

Thus, through with this study, different administration system tools and grouping are presented for

power of entity and compound its fiscal presentation consistently(Armstrong, 2014).

commercial enterprise execution and outcomes (Sundem. and et. al, 2014). With the help of this concept

cited firm purpose be able to execute its subjective well.

CONCLUSION

From the above written report it can be terminated that administration account is an necessary

instrument that help the structure in realize their issues and influence in achieving the cognitive content

of the entity important. It is the method that influence in commute the origin well so that operable cost

of the entity can be reduced(Simons, 2013). It container be said that adoption of onset pricing strategy is

helpful that influence in compound the profitableness of the entity to large extent. This written document

is terminated that administration accounting is an formulation of management by which generic

enterprise dealing get on managed. Therefore, various governing body instrument are ascertained for

assigning money for Imda limited. Considering this, cost accounting such as absorption and minimum is

advised for set up financial gain evidence that presents fiscal point of organisation. Furthermore,

captious valuation on fund is given for foretelling and determination for advance business trading

operations. According several kinds of fund and its planning process is thoughtful this assignment.

However, valuation strategies for surround costs according to various determinants are represented for

cost potency as well proper establishment of entity is acknowledged. Apart from this, fiscal evidence

investigation is acquire by which current business performance is analysed that is impressive to reduce

economical problems occur at geographic point. Consider this, importance of administration system is

explicit which is used to change governing body and development effective plan of action at high level.

Thus, through with this study, different administration system tools and grouping are presented for

power of entity and compound its fiscal presentation consistently(Armstrong, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Journals and Books

Armstrong, P., 2014. Limits and possibilities for HRM in an age of management accountancy. New

Perspectives On Human Resource Management op. cit. at, pp.154-166.

Bodie, Z., 2013. Investments. McGraw-Hill.

Brandau, M., Endenich, C., Trapp, R. and Hoffjan, A., 2013. Institutional drivers of conformity–

Evidence for management accounting from Brazil and Germany. International Business Review.

22(2). pp.466-479.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea: The case

of the balanced scorecard. Contemporary Accounting Research.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society. 38(1).

pp.50-71.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm performance:

The incremental contribution of lean management accounting practices. Journal of Operations

Management. 32(7). pp.414-428.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control research. Journal of

Management Control,.24(3). pp.223-240.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Lavia López, O. and Hiebl, M. R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research. 27(1). pp.81-119.

Morales, J. and Lambert, C., 2013. Dirty work and the construction of identity. An ethnographic study of

management accounting practices. Accounting, Organizations and Society. 38(3). pp.228-244.

Otley, D. and Emmanuel, K. M. C., 2013. Readings in accounting for management control. Springer.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John Wiley &

Sons.

Schaltegger, S., Gibassier, D. and Zvezdov, D., 2013. Is environmental management accounting a

discipline? A bibliometric literature review. Meditari Accountancy Research. 21(1). pp.4-31.

Simons, R., 2013. Performance Measurement and Control Systems for Implementing Strategy Text and

Cases: Pearson New International Edition. Pearson Higher Ed.

Journals and Books

Armstrong, P., 2014. Limits and possibilities for HRM in an age of management accountancy. New

Perspectives On Human Resource Management op. cit. at, pp.154-166.

Bodie, Z., 2013. Investments. McGraw-Hill.

Brandau, M., Endenich, C., Trapp, R. and Hoffjan, A., 2013. Institutional drivers of conformity–

Evidence for management accounting from Brazil and Germany. International Business Review.

22(2). pp.466-479.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea: The case

of the balanced scorecard. Contemporary Accounting Research.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society. 38(1).

pp.50-71.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm performance:

The incremental contribution of lean management accounting practices. Journal of Operations

Management. 32(7). pp.414-428.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control research. Journal of

Management Control,.24(3). pp.223-240.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Lavia López, O. and Hiebl, M. R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research. 27(1). pp.81-119.

Morales, J. and Lambert, C., 2013. Dirty work and the construction of identity. An ethnographic study of

management accounting practices. Accounting, Organizations and Society. 38(3). pp.228-244.

Otley, D. and Emmanuel, K. M. C., 2013. Readings in accounting for management control. Springer.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John Wiley &

Sons.

Schaltegger, S., Gibassier, D. and Zvezdov, D., 2013. Is environmental management accounting a

discipline? A bibliometric literature review. Meditari Accountancy Research. 21(1). pp.4-31.

Simons, R., 2013. Performance Measurement and Control Systems for Implementing Strategy Text and

Cases: Pearson New International Edition. Pearson Higher Ed.

Suomala, P., Lyly-Yrjänäinen, J. and Lukka, K., 2014. Battlefield around interventions: A reflective

analysis of conducting interventionist research in management accounting. Management

Accounting Research. 25(4). pp.304-314.

Tappura, S., Sievänen, M., Heikkilä, J., Jussila, A. and Nenonen, N., 2015. A management accounting

perspective on safety. Safety science. 71. pp.151-159.

Vakalfotis, N., Ballantine, J. and Wall, A.P., 2013. A literature review on the impact of Enterprise

Systems on management accounting.

Vosselman, E., 2014. The ‘performativity thesis’ and its critics: Towards a relational ontology of

management accounting. Accounting and Business Research. 44(2). pp.181-203.

Wajeetongratana, P., 2016. Management Accounting Techniques of Companies Listed on the Stock

Exchange in Thailand. Management Accounting. 1. p.43943.

Online

Management Accounting: Concept, Functions and Scope. 2017. [Online]. Available through

<http://www.yourarticlelibrary.com/accounting/management-accounting/management-

accounting-concept-functions-and-scope/61276/> [Accessed on 20th May 2017]

analysis of conducting interventionist research in management accounting. Management

Accounting Research. 25(4). pp.304-314.

Tappura, S., Sievänen, M., Heikkilä, J., Jussila, A. and Nenonen, N., 2015. A management accounting

perspective on safety. Safety science. 71. pp.151-159.

Vakalfotis, N., Ballantine, J. and Wall, A.P., 2013. A literature review on the impact of Enterprise

Systems on management accounting.

Vosselman, E., 2014. The ‘performativity thesis’ and its critics: Towards a relational ontology of

management accounting. Accounting and Business Research. 44(2). pp.181-203.

Wajeetongratana, P., 2016. Management Accounting Techniques of Companies Listed on the Stock

Exchange in Thailand. Management Accounting. 1. p.43943.

Online

Management Accounting: Concept, Functions and Scope. 2017. [Online]. Available through

<http://www.yourarticlelibrary.com/accounting/management-accounting/management-

accounting-concept-functions-and-scope/61276/> [Accessed on 20th May 2017]

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.