Management Accounting Assignment: ACFI 2003 Analysis and Solution

VerifiedAdded on 2023/01/13

|4

|769

|52

Homework Assignment

AI Summary

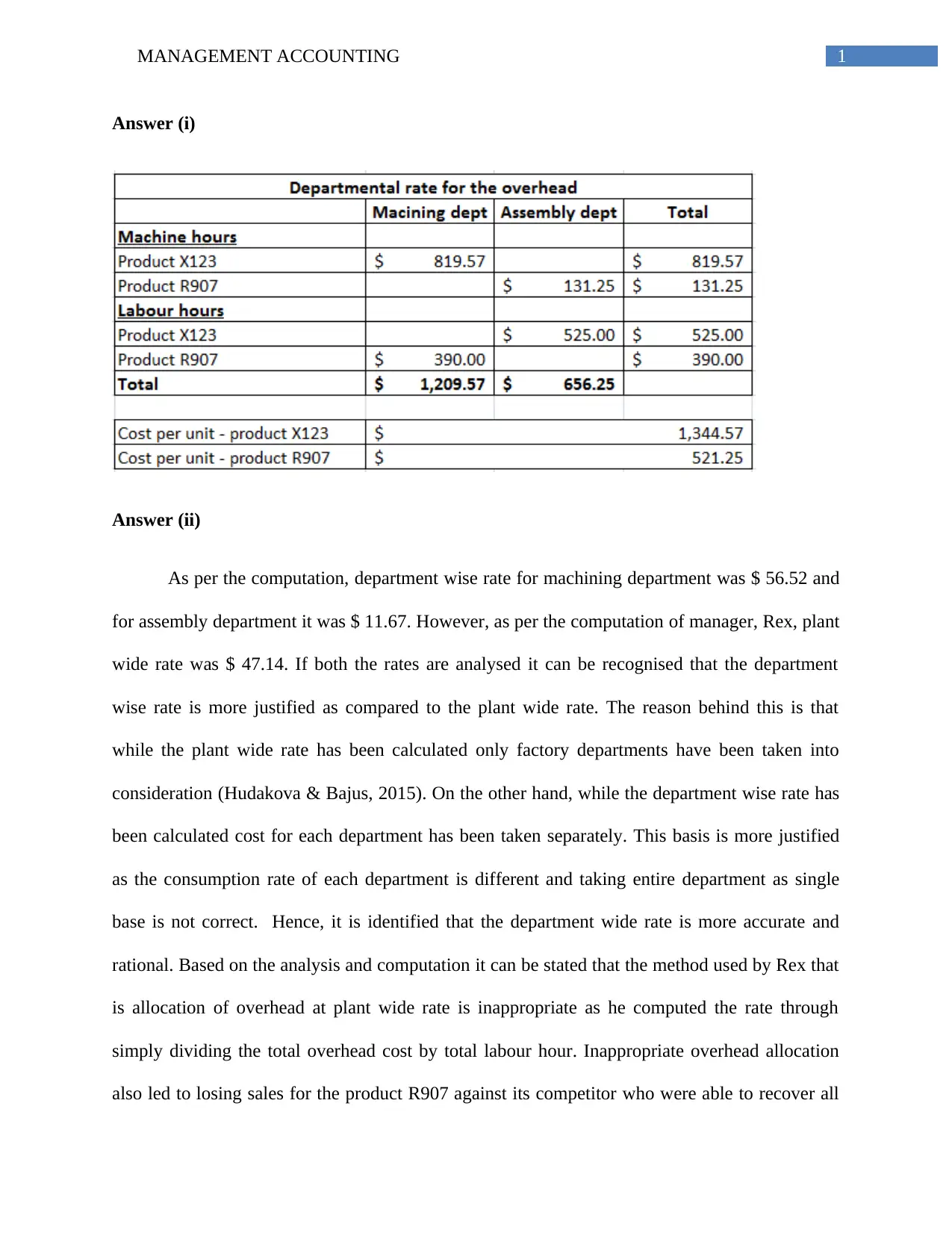

This document presents a solution for a management accounting assignment, likely for an undergraduate course like ACFI 2003. The solution addresses overhead allocation methods, comparing department-wise and plant-wide rates, and advocating for the use of department-wise rates as more accurate. It explains the limitations of the plant-wide rate, which led to lost sales. Furthermore, the solution details the Activity-Based Costing (ABC) method, highlighting its advantages over traditional methods in terms of accuracy and efficiency in costing and pricing, emphasizing its role in identifying and reducing unnecessary costs, and improving overall production processes. The assignment includes calculations for overhead allocation for different products, recommending specific cost figures for each. The solution also references relevant academic literature to support its arguments.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.