Management Accounting: Unilever Case Study and Analysis Report

VerifiedAdded on 2023/01/11

|20

|5605

|98

Report

AI Summary

This report examines the management accounting practices of Unilever, a leading multinational consumer goods company. It provides an overview of management accounting and its essential requirements, focusing on different management accounting systems like cost accounting, inventory management (IMS), and price optimization systems (POS). The report details various methods of management accounting reporting, including budget reports, performance reports, account receivable reports (ARR), and cost reports. It highlights the benefits of each system and integrates them into the organizational process. The analysis includes practical applications and advantages of these systems, offering insights into how Unilever utilizes these tools to enhance its financial management, control costs, and improve decision-making processes. The report also discusses the integration of these systems and reports within the organization's processes.

Management accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

INTRODUCTION

The MA is the arrangement of money related information and exhortation to an

organization for use in association and improvement of its business. This is the way toward

examining business expenses and tasks to plan inward budgetary report, records and reports to

help supervisor's taking specific business decisions for accomplishing business objectives in

successful way. The present report is based on “Unilever” which is British multinational

consumer goods company. The company is largest producer of consumer goods in the world.

The company has 155000 numbers of employees by covering world wide area. That is very

important to manage their account of company in effective manner. In respect of that report will

explain management accounting and give essential requirements of different types of

management accounting system. This will explain the different methods used for management

accounting system. As per that, report will calculate the costs by using appropriate tools of doing

cost analysis to prepare income statement under the different techniques. Report will also explain

advantage and disadvantages of different types of planning tools using budgetary control. Along

with that the report will also highlight comparison of adoption of management accounting

system to respond to financial problems.

LO 1

Explain management accounting and its essential requirement of different management

accounting system.

Management accounting system is also known as managerial accounting system. This is

the way toward giving money related data just as resources to administrator in taking decisions.

This is utilized by interior group of organization and thing that is making it appropriately unique

in relation to financial accounting. In this procedure, monetary data and report, for example,

receipt budget summary is shared with the finance department of the organization with the

correct supervisory group of Unilever (Abernethy and Campbell, 2018). The main objective of

MA which is used to statistical data as well as take the better chances for taking accurate

decision, controlling enterprise, various business activities and development. This is the

application of professional skills and knowledge in preparation of accounting and financial

information in effective and in respective manner. This assists internal management in the

formulation of planning, policies and controls the operations of company.

3

The MA is the arrangement of money related information and exhortation to an

organization for use in association and improvement of its business. This is the way toward

examining business expenses and tasks to plan inward budgetary report, records and reports to

help supervisor's taking specific business decisions for accomplishing business objectives in

successful way. The present report is based on “Unilever” which is British multinational

consumer goods company. The company is largest producer of consumer goods in the world.

The company has 155000 numbers of employees by covering world wide area. That is very

important to manage their account of company in effective manner. In respect of that report will

explain management accounting and give essential requirements of different types of

management accounting system. This will explain the different methods used for management

accounting system. As per that, report will calculate the costs by using appropriate tools of doing

cost analysis to prepare income statement under the different techniques. Report will also explain

advantage and disadvantages of different types of planning tools using budgetary control. Along

with that the report will also highlight comparison of adoption of management accounting

system to respond to financial problems.

LO 1

Explain management accounting and its essential requirement of different management

accounting system.

Management accounting system is also known as managerial accounting system. This is

the way toward giving money related data just as resources to administrator in taking decisions.

This is utilized by interior group of organization and thing that is making it appropriately unique

in relation to financial accounting. In this procedure, monetary data and report, for example,

receipt budget summary is shared with the finance department of the organization with the

correct supervisory group of Unilever (Abernethy and Campbell, 2018). The main objective of

MA which is used to statistical data as well as take the better chances for taking accurate

decision, controlling enterprise, various business activities and development. This is the

application of professional skills and knowledge in preparation of accounting and financial

information in effective and in respective manner. This assists internal management in the

formulation of planning, policies and controls the operations of company.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting system:

The MA framework is significant in light of the fact that it helps to enhance the

profitability and productivity limit of organization in successful way. This procedure is higher

productive and useful for higher market share for their business expansion and growth just as

advancement. There are various accounting system which are explains below:

Cost accounting system:

A cost accounting system is the framework that is used by companies for estimating cost

of products for profitability analysis, cost control and inventory valuation. This helps to

determine the profitability and revenue of Unilever Company by including such activities such as

inventory, work in progress and finished goods. There are different types of cost accounting

which are explains below:

Fixed cost is the cost which is depends on level of production. These are usually thinks

like the mortgage as well as the lease payment on the types of building or equipment.

That type of payment is depreciated at the fixed as per the monthly rate (Cost accounting,

2020). This can be increase and decrease as per production level.

Variable cost is tied to company level of production. Most of costs into company are

more variable and not fixed due to some changes are required sudden. Like the floral

ramping, some of expenses as well as maintenance charges are also variable within the

company.

Operating cost is associated with day to day operation of business. These costs can be

withering fixed or variable which are depending on situation.

Direct cost is related with producing a product. The direct cost of finish good include the

labour working hours in production department in effective and in respective manner.

Inventory management system (IMS):

IMS is a tool and framework which involves the proper structure as well as establishing

the process and inventory monitoring of the organization. This is the software of tracking

inventory levels, order, sales and deliveries. It is the combination of technology and process

which is oversees monitoring as well as maintenances of stock product. Inventory is the most

important and an important asset or part of the organization and it is necessary to maintain record

of inventory (Ax and Greve, 2017). It is extremely pivotal so as to a foundation for overseeing

and tracking the stock whether it is crude material, work in progress, completed stock in

4

The MA framework is significant in light of the fact that it helps to enhance the

profitability and productivity limit of organization in successful way. This procedure is higher

productive and useful for higher market share for their business expansion and growth just as

advancement. There are various accounting system which are explains below:

Cost accounting system:

A cost accounting system is the framework that is used by companies for estimating cost

of products for profitability analysis, cost control and inventory valuation. This helps to

determine the profitability and revenue of Unilever Company by including such activities such as

inventory, work in progress and finished goods. There are different types of cost accounting

which are explains below:

Fixed cost is the cost which is depends on level of production. These are usually thinks

like the mortgage as well as the lease payment on the types of building or equipment.

That type of payment is depreciated at the fixed as per the monthly rate (Cost accounting,

2020). This can be increase and decrease as per production level.

Variable cost is tied to company level of production. Most of costs into company are

more variable and not fixed due to some changes are required sudden. Like the floral

ramping, some of expenses as well as maintenance charges are also variable within the

company.

Operating cost is associated with day to day operation of business. These costs can be

withering fixed or variable which are depending on situation.

Direct cost is related with producing a product. The direct cost of finish good include the

labour working hours in production department in effective and in respective manner.

Inventory management system (IMS):

IMS is a tool and framework which involves the proper structure as well as establishing

the process and inventory monitoring of the organization. This is the software of tracking

inventory levels, order, sales and deliveries. It is the combination of technology and process

which is oversees monitoring as well as maintenances of stock product. Inventory is the most

important and an important asset or part of the organization and it is necessary to maintain record

of inventory (Ax and Greve, 2017). It is extremely pivotal so as to a foundation for overseeing

and tracking the stock whether it is crude material, work in progress, completed stock in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

distribution centre and showrooms, merchandise sent on credit or products dispatched for

conveyance to merchants or clients. For following its stock, Unilever utilizes software which

encourages the organization to unravel the inquiries of the clients on schedule and furthermore

advises for keeping up the nature of the items. This system has two methods which are help to

maintaining stocks of company. Those methods are explains below:

FIFO; this is stand for the first in first out, the cost which is associated with the inventory

of Unilever was purchased first cost expensed first.

LIFO: this is stand for last in first out, this assumes which is the most recent product

added into company inventory sold first.

Price optimisation system (POS):

POS is a procedure of scientific examination which is gives the best possible data along

with material information. This is about how the interest of an item and administrations are

differed by the variety in cost. This assistance to break down the conduct just as response of the

clients toward the value set that is varies at similar items in various circumstances (Fleischman

and McLean, 2020). It records and orders the data, at that point applies on cost of manufacturing

of stock which is helps the organization in picking the best value that improves the benefit and

consumer loyalty too. So as to gathering the best possible data and watching costumer conduct

on various estimating, different channels are utilized by Unilever. The Company proposed

various arrangements of costs to its all age sections' purchasers and choose right price as per

them.

Those are different management accounting system which is help to maintain the records

of company and its inventory by preparing statements. Those are creating various benefits for

company. Inventory management system is properly helped to company for eliminate shortage

and overstocking. This will also provide facility to manager for finding out right and proper

balance between carrying too much and little inventory (Honggowati and et.al., 2017). On the

other side, cost accounting system is help to disclosure profitability activities for business as well

as unprofitability. This provides effective guidance to Unilever for the future production policies

and to find the exact causes to decrease and increase profit of company.

Explain different methods of MA reporting

MA report is mainly created for undertaking proper and effective planning, controlling

and decision making. This assists in providing specific and useful information to management of

5

conveyance to merchants or clients. For following its stock, Unilever utilizes software which

encourages the organization to unravel the inquiries of the clients on schedule and furthermore

advises for keeping up the nature of the items. This system has two methods which are help to

maintaining stocks of company. Those methods are explains below:

FIFO; this is stand for the first in first out, the cost which is associated with the inventory

of Unilever was purchased first cost expensed first.

LIFO: this is stand for last in first out, this assumes which is the most recent product

added into company inventory sold first.

Price optimisation system (POS):

POS is a procedure of scientific examination which is gives the best possible data along

with material information. This is about how the interest of an item and administrations are

differed by the variety in cost. This assistance to break down the conduct just as response of the

clients toward the value set that is varies at similar items in various circumstances (Fleischman

and McLean, 2020). It records and orders the data, at that point applies on cost of manufacturing

of stock which is helps the organization in picking the best value that improves the benefit and

consumer loyalty too. So as to gathering the best possible data and watching costumer conduct

on various estimating, different channels are utilized by Unilever. The Company proposed

various arrangements of costs to its all age sections' purchasers and choose right price as per

them.

Those are different management accounting system which is help to maintain the records

of company and its inventory by preparing statements. Those are creating various benefits for

company. Inventory management system is properly helped to company for eliminate shortage

and overstocking. This will also provide facility to manager for finding out right and proper

balance between carrying too much and little inventory (Honggowati and et.al., 2017). On the

other side, cost accounting system is help to disclosure profitability activities for business as well

as unprofitability. This provides effective guidance to Unilever for the future production policies

and to find the exact causes to decrease and increase profit of company.

Explain different methods of MA reporting

MA report is mainly created for undertaking proper and effective planning, controlling

and decision making. This assists in providing specific and useful information to management of

5

the company that is further aids for making strategic decision in order to solve issues. There are

various types of management accounting reports which are very useful for Unilever explain

below:

Budget report:

This report is the tool and provides proper details which are used in the evaluation of the

performance evaluation of company in effective manner. This is used for showing indirect

comparison of actual and accurate result of company in order to prepare budget plan for identify

the proper differences between them. This will also used by Unilever for relating the previous

year’s performance with the present one and implement actions and steps in order to gain high

margin of profit (Maas, Schaltegger and Crutzen, 2016). This will likewise incorporate and

included income or cost of Unilever and later work for profit increments. This is the best

possible and viable improvement which helps the organization and its administration for

increasing legitimate information on performance of all the considerable number of departments

just as individual performance inside the association. This report will support Unilever in

effectively managing its work by carrying out the business activities within the given budget.

Performance report:

Performance report is refers with card report that is given to any individual, activity or

procedure. So, that creates usefulness for company to analysis their efforts as well as

productivity of execution can be estimated so as to accomplish their destinations. A foundation

utilizes this report to dissect the capability of its workers, systems and the executives also. This is

uncovers the change between targets which are finished by workers and the targets they expected

to do. The beneficiary of this report is subject to play out the medicinal exercises to improve the

presentation on the off chance that it is required for business. Unilever the board gets ready

execution reports for representatives and exercises with the goal that they might be remunerated,

prepared or change in like manner.

Account receivable report (ARR):

ARR is the receipts which are used by an organization (Hopper and Bui, 2016). That has

not received yet and has a right to attain it in near future. Like: at the point when association

depends about using a loan exchange, it is indispensable for them so as to keep up legitimate

records of data like account holders just as exchange receivables. The ARR refers to the formal

document that contains all the data worry with credit deals, due receipts, development periods,

6

various types of management accounting reports which are very useful for Unilever explain

below:

Budget report:

This report is the tool and provides proper details which are used in the evaluation of the

performance evaluation of company in effective manner. This is used for showing indirect

comparison of actual and accurate result of company in order to prepare budget plan for identify

the proper differences between them. This will also used by Unilever for relating the previous

year’s performance with the present one and implement actions and steps in order to gain high

margin of profit (Maas, Schaltegger and Crutzen, 2016). This will likewise incorporate and

included income or cost of Unilever and later work for profit increments. This is the best

possible and viable improvement which helps the organization and its administration for

increasing legitimate information on performance of all the considerable number of departments

just as individual performance inside the association. This report will support Unilever in

effectively managing its work by carrying out the business activities within the given budget.

Performance report:

Performance report is refers with card report that is given to any individual, activity or

procedure. So, that creates usefulness for company to analysis their efforts as well as

productivity of execution can be estimated so as to accomplish their destinations. A foundation

utilizes this report to dissect the capability of its workers, systems and the executives also. This is

uncovers the change between targets which are finished by workers and the targets they expected

to do. The beneficiary of this report is subject to play out the medicinal exercises to improve the

presentation on the off chance that it is required for business. Unilever the board gets ready

execution reports for representatives and exercises with the goal that they might be remunerated,

prepared or change in like manner.

Account receivable report (ARR):

ARR is the receipts which are used by an organization (Hopper and Bui, 2016). That has

not received yet and has a right to attain it in near future. Like: at the point when association

depends about using a loan exchange, it is indispensable for them so as to keep up legitimate

records of data like account holders just as exchange receivables. The ARR refers to the formal

document that contains all the data worry with credit deals, due receipts, development periods,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

due enthusiasm on late instalments, credit approaches, contact subtleties of the borrowers,

arrangements for awful obligations, and so on. The administration of Unilever keep up this report

so that due sum can be gotten convenient, indebted person turnover proportion and liquidity of

the firm can be improved and credit approaches can be refreshed normally. Thus, it will assist

Unilever in meeting with the uncertain future events that can be dangerous for the company.

Cost report:

Cost report is the financial report that is help to identify cost and charges those are

generate through various activities happens within the company. This provides the complete

information about the cost accounting of company and business (Collis and Hussey, 2017). This

covers all the information about the all those transactions which are related to the cost expense

and revenue. Cost report is help to determine the cost elements and activity of organization that

includes product, services, manufacturing process, distribution and other various elements. This

helped to management of Unilever for keeping a watch on every cost of company. It is

effectively help in putting control on the cost element of the company in respect to various

business activities.

M1 benefits of management accounting system.

Management Accounting

(MA) System

Benefits

Cost Accounting (CA)

System

This CA system is assist management for identifying the

activities which are unwanted and just incurring cost for

the company.

Through this, company can work on reducing the cost

associated with manufacturing, improving efficiency and

saving time.

It assists Unilever in determining the profitability

attached to the individual product.

IMS This will assist Unilever in effectively managing its

inventory resulting in improved customer satisfaction.

(Maas, Schaltegger and Crutzen, 2016).

The system controls over cost of inventory stock as well

7

arrangements for awful obligations, and so on. The administration of Unilever keep up this report

so that due sum can be gotten convenient, indebted person turnover proportion and liquidity of

the firm can be improved and credit approaches can be refreshed normally. Thus, it will assist

Unilever in meeting with the uncertain future events that can be dangerous for the company.

Cost report:

Cost report is the financial report that is help to identify cost and charges those are

generate through various activities happens within the company. This provides the complete

information about the cost accounting of company and business (Collis and Hussey, 2017). This

covers all the information about the all those transactions which are related to the cost expense

and revenue. Cost report is help to determine the cost elements and activity of organization that

includes product, services, manufacturing process, distribution and other various elements. This

helped to management of Unilever for keeping a watch on every cost of company. It is

effectively help in putting control on the cost element of the company in respect to various

business activities.

M1 benefits of management accounting system.

Management Accounting

(MA) System

Benefits

Cost Accounting (CA)

System

This CA system is assist management for identifying the

activities which are unwanted and just incurring cost for

the company.

Through this, company can work on reducing the cost

associated with manufacturing, improving efficiency and

saving time.

It assists Unilever in determining the profitability

attached to the individual product.

IMS This will assist Unilever in effectively managing its

inventory resulting in improved customer satisfaction.

(Maas, Schaltegger and Crutzen, 2016).

The system controls over cost of inventory stock as well

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as provide an informational transparency.

This also help the organization in exercising control over

the cost that is incurred on managing the inventory by

determining the right level of stock.

Price Optimisation System Price optimisation system is helps for improving the

nature of items as per client prerequisites.

Firm may fix the cost so as to get most extreme benefit

with least expense.

The price is determined based on the demand of the

product and the consumers willingness to pay for that

product.

D1 integration of management accounting system and management accounting report into

organization process.

Management accounting system and report are very important and essential part of

company and its management accounting process. This provides the proper policies

implementation, procedure and structure for announcing process. Without keeping up the best

possible bookkeeping framework, that is beyond the realm of imagination to expect to gather and

arranged information and data in such unique and efficient manner that administration can use

that. Additionally, various reports are providing variances and reasons behind the reports and

management allows supervision for direct at the various functional units of the association for

create effective system (Messner, 2016). For understanding in better manner, here is taking

example: the inventory management (IM) is not working appropriately, then it is problematic to

keep records of stock and exact changes cannot be measures in inventory system. In the case,

report framework won't give exact data to framework, the executives not ready to settle inquiries

of clients. Hence, that it is must for Unilever must keep up both the framework and reporting

process together for survive in industry.

8

This also help the organization in exercising control over

the cost that is incurred on managing the inventory by

determining the right level of stock.

Price Optimisation System Price optimisation system is helps for improving the

nature of items as per client prerequisites.

Firm may fix the cost so as to get most extreme benefit

with least expense.

The price is determined based on the demand of the

product and the consumers willingness to pay for that

product.

D1 integration of management accounting system and management accounting report into

organization process.

Management accounting system and report are very important and essential part of

company and its management accounting process. This provides the proper policies

implementation, procedure and structure for announcing process. Without keeping up the best

possible bookkeeping framework, that is beyond the realm of imagination to expect to gather and

arranged information and data in such unique and efficient manner that administration can use

that. Additionally, various reports are providing variances and reasons behind the reports and

management allows supervision for direct at the various functional units of the association for

create effective system (Messner, 2016). For understanding in better manner, here is taking

example: the inventory management (IM) is not working appropriately, then it is problematic to

keep records of stock and exact changes cannot be measures in inventory system. In the case,

report framework won't give exact data to framework, the executives not ready to settle inquiries

of clients. Hence, that it is must for Unilever must keep up both the framework and reporting

process together for survive in industry.

8

LO 2

P3 Application of various management accounting techniques

With the increasing complexity in the management of financial information, there is

requirement of various types of MA techniques which can be useful in carrying out cost analysis.

Marginal Costing System (MCS)

The marginal costing is the coting method which is used by for the purpose of calculating

the per unit cost of the additional product manufactured (Collis and Hussey, 2017). It takes into

consideration only the variable cost in respect to evaluating the cost of production while the

fixed cost is taken as period cost and which is then set off against the contribution amount

derived of the product.

Absorption Costing System (ACS)

This approach of cost analysis takes into account all the production cost and expenses

incurred on the product irrespective of the fact whether it is fixed or variable cost (Hamamura,

2018). Therefore, the cost of production involves all the direct material and labour cost and the

fixed and variable overhead expenses. This method is used under GAAP and is also used for

external financial reporting.

Unilever is producing a new set of healthcare product which is completely organic. The cost

related to its production is attached in the Appendix.

Analysis and interpretation: It can be interpreted from the computation that under MCS, the

fixed cost is subtracted from the contribution whereas in AC system, the fixed expenses is taken

into account for determining the cost of production. This is the reason why the final outcome is

different under both the methods. In the context of Unilever, there is a profit under marginal

costing which is £28000 and in absorption costing there is a profit of £40000 because marginal

costing only considers variable cost in cost of production in contrast to it in ACS, the fixed cost

involved in the production is taken into account which lead to better results. Thus, absorption

costing is more preferred.

Marginal Costing System Absorption Costing System

It assumes only variable cost of production as

the product cost.

It assumes both fixed and variable cost as the

product cost.

It determines cost of additional unit. It identifies cost of each unit.

9

P3 Application of various management accounting techniques

With the increasing complexity in the management of financial information, there is

requirement of various types of MA techniques which can be useful in carrying out cost analysis.

Marginal Costing System (MCS)

The marginal costing is the coting method which is used by for the purpose of calculating

the per unit cost of the additional product manufactured (Collis and Hussey, 2017). It takes into

consideration only the variable cost in respect to evaluating the cost of production while the

fixed cost is taken as period cost and which is then set off against the contribution amount

derived of the product.

Absorption Costing System (ACS)

This approach of cost analysis takes into account all the production cost and expenses

incurred on the product irrespective of the fact whether it is fixed or variable cost (Hamamura,

2018). Therefore, the cost of production involves all the direct material and labour cost and the

fixed and variable overhead expenses. This method is used under GAAP and is also used for

external financial reporting.

Unilever is producing a new set of healthcare product which is completely organic. The cost

related to its production is attached in the Appendix.

Analysis and interpretation: It can be interpreted from the computation that under MCS, the

fixed cost is subtracted from the contribution whereas in AC system, the fixed expenses is taken

into account for determining the cost of production. This is the reason why the final outcome is

different under both the methods. In the context of Unilever, there is a profit under marginal

costing which is £28000 and in absorption costing there is a profit of £40000 because marginal

costing only considers variable cost in cost of production in contrast to it in ACS, the fixed cost

involved in the production is taken into account which lead to better results. Thus, absorption

costing is more preferred.

Marginal Costing System Absorption Costing System

It assumes only variable cost of production as

the product cost.

It assumes both fixed and variable cost as the

product cost.

It determines cost of additional unit. It identifies cost of each unit.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

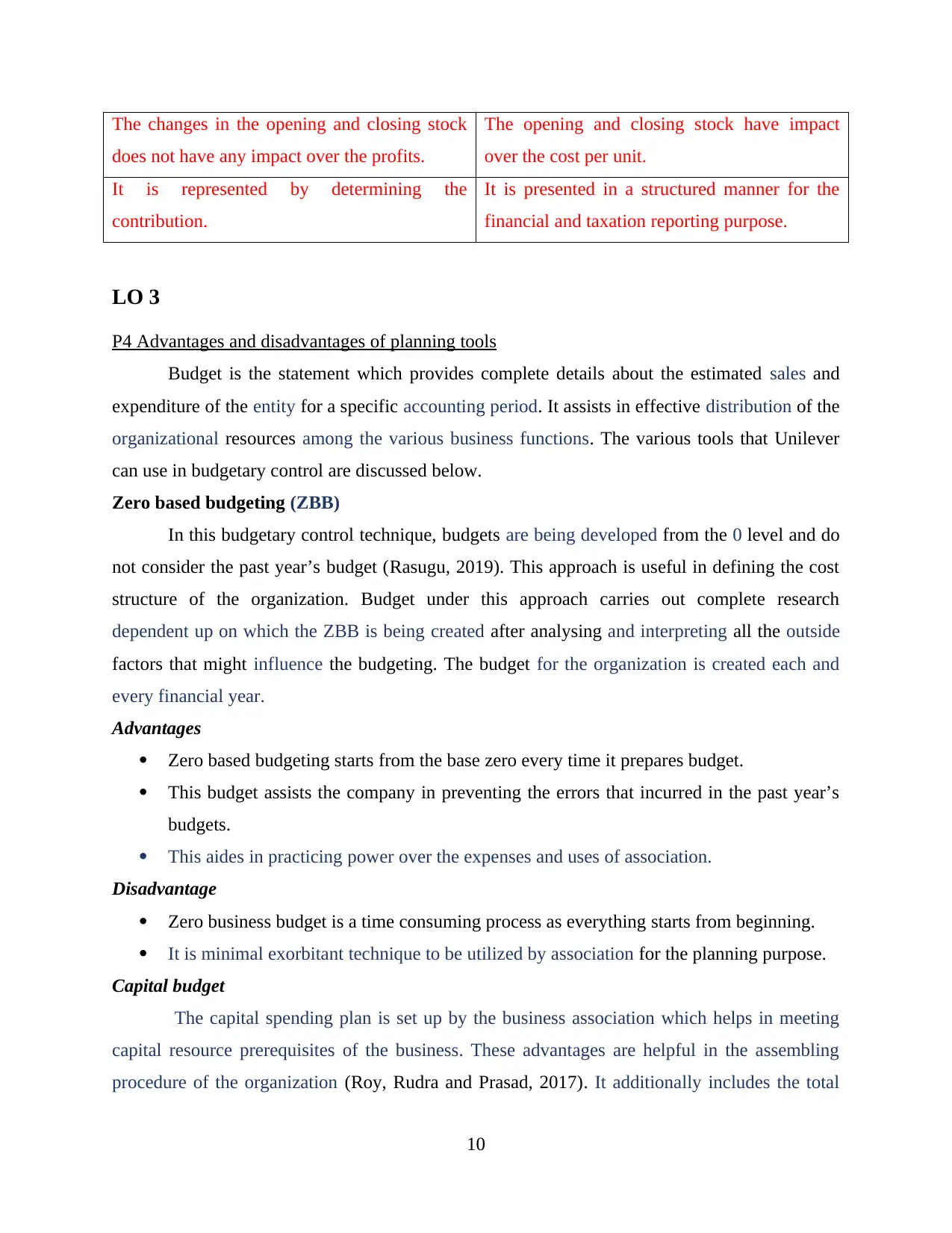

The changes in the opening and closing stock

does not have any impact over the profits.

The opening and closing stock have impact

over the cost per unit.

It is represented by determining the

contribution.

It is presented in a structured manner for the

financial and taxation reporting purpose.

LO 3

P4 Advantages and disadvantages of planning tools

Budget is the statement which provides complete details about the estimated sales and

expenditure of the entity for a specific accounting period. It assists in effective distribution of the

organizational resources among the various business functions. The various tools that Unilever

can use in budgetary control are discussed below.

Zero based budgeting (ZBB)

In this budgetary control technique, budgets are being developed from the 0 level and do

not consider the past year’s budget (Rasugu, 2019). This approach is useful in defining the cost

structure of the organization. Budget under this approach carries out complete research

dependent up on which the ZBB is being created after analysing and interpreting all the outside

factors that might influence the budgeting. The budget for the organization is created each and

every financial year.

Advantages

Zero based budgeting starts from the base zero every time it prepares budget.

This budget assists the company in preventing the errors that incurred in the past year’s

budgets.

This aides in practicing power over the expenses and uses of association.

Disadvantage

Zero business budget is a time consuming process as everything starts from beginning.

It is minimal exorbitant technique to be utilized by association for the planning purpose.

Capital budget

The capital spending plan is set up by the business association which helps in meeting

capital resource prerequisites of the business. These advantages are helpful in the assembling

procedure of the organization (Roy, Rudra and Prasad, 2017). It additionally includes the total

10

does not have any impact over the profits.

The opening and closing stock have impact

over the cost per unit.

It is represented by determining the

contribution.

It is presented in a structured manner for the

financial and taxation reporting purpose.

LO 3

P4 Advantages and disadvantages of planning tools

Budget is the statement which provides complete details about the estimated sales and

expenditure of the entity for a specific accounting period. It assists in effective distribution of the

organizational resources among the various business functions. The various tools that Unilever

can use in budgetary control are discussed below.

Zero based budgeting (ZBB)

In this budgetary control technique, budgets are being developed from the 0 level and do

not consider the past year’s budget (Rasugu, 2019). This approach is useful in defining the cost

structure of the organization. Budget under this approach carries out complete research

dependent up on which the ZBB is being created after analysing and interpreting all the outside

factors that might influence the budgeting. The budget for the organization is created each and

every financial year.

Advantages

Zero based budgeting starts from the base zero every time it prepares budget.

This budget assists the company in preventing the errors that incurred in the past year’s

budgets.

This aides in practicing power over the expenses and uses of association.

Disadvantage

Zero business budget is a time consuming process as everything starts from beginning.

It is minimal exorbitant technique to be utilized by association for the planning purpose.

Capital budget

The capital spending plan is set up by the business association which helps in meeting

capital resource prerequisites of the business. These advantages are helpful in the assembling

procedure of the organization (Roy, Rudra and Prasad, 2017). It additionally includes the total

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

examination of the speculation with the assistance of the capital planning methods which helps in

deciding the feasibility of the ventures and capital undertakings.

Advantages

This budget helps the organization in analysing the prerequisite of the capital assets for

manufacturing process.

This budget supports in analysing the capital requirements of the business. It helps in knowing the profitability and feasibility related to the investment plan which

the corporate is willing to make an investment.

Disadvantages

This budget may not be able to provide accurate information with respect to investment.

It is completely based on the estimation of the cash inflow that will be generated from the

investment and if it is gone wrong then it will affect the business and may incur losses.

Activity Based Budgeting (ABB)

This is form of budgeting method the business firms create the budget which depends on

the exercises embraced by the association. It depends on the estimation made in regard to the

assets to be used and apportioned alongside the degree of income it will produce (Seetharaman

and et.al, 2016). It doesn't consider the earlier year's spending plan for the purpose of preparing

the current year’s budget. This budgetary tool helps in determining the costs and expenses

attached to the various business activities which are being utilized in the manufacturing process.

The activity based budgeting helps in recognizing the inconsistency in the production framework

which results into determining the costs and the wastages in the process so ideal moves can be

made so as to deal with the circumstance.

Advantages

This budgetary tool is very simple and easy to execute in the firm as it requires exercising

less time and efforts.

This ABB instrument gives assistance to the association in deciding any disparity in the

creation exercises and the creation procedure also.

It does not consider previous year budget which reduces the chances of errors.

Disadvantages

It requires highly professional personnel with relevant skills and knowledge.

This tool is very costly for implementation in the business entity.

11

deciding the feasibility of the ventures and capital undertakings.

Advantages

This budget helps the organization in analysing the prerequisite of the capital assets for

manufacturing process.

This budget supports in analysing the capital requirements of the business. It helps in knowing the profitability and feasibility related to the investment plan which

the corporate is willing to make an investment.

Disadvantages

This budget may not be able to provide accurate information with respect to investment.

It is completely based on the estimation of the cash inflow that will be generated from the

investment and if it is gone wrong then it will affect the business and may incur losses.

Activity Based Budgeting (ABB)

This is form of budgeting method the business firms create the budget which depends on

the exercises embraced by the association. It depends on the estimation made in regard to the

assets to be used and apportioned alongside the degree of income it will produce (Seetharaman

and et.al, 2016). It doesn't consider the earlier year's spending plan for the purpose of preparing

the current year’s budget. This budgetary tool helps in determining the costs and expenses

attached to the various business activities which are being utilized in the manufacturing process.

The activity based budgeting helps in recognizing the inconsistency in the production framework

which results into determining the costs and the wastages in the process so ideal moves can be

made so as to deal with the circumstance.

Advantages

This budgetary tool is very simple and easy to execute in the firm as it requires exercising

less time and efforts.

This ABB instrument gives assistance to the association in deciding any disparity in the

creation exercises and the creation procedure also.

It does not consider previous year budget which reduces the chances of errors.

Disadvantages

It requires highly professional personnel with relevant skills and knowledge.

This tool is very costly for implementation in the business entity.

11

Variance analysis

It refers to the difference in the actual figures in comparison to the planned ones. It gives

the clear picture about the performance of the organization like Unilever. This stated in terms of

over performance or underperformance like favourable and unfavourable. An example is stated

in Appendix.

LO 4

P5 compare different management accounting system to respond financial problems.

Financial issues allude as the money related or support related issues. Yet, few of the

issues are which are mainly being come as a challenge by the organization are introduced as

under:

Late imbursement from clients is now a day is biggest financial problem. In that

organization relies that the credit policies of the entity very much and they need to sell their

items and services on credit to clients. At some point clients are from universally and

inadvertently neglects to pay due sum on time which is called as delayed in payment from

customers. It might the reason an enormous and greatest issue for assembling organization like

Unilever it become an ordinary act of clients.

Key performance indicator:

Key performance indicator is known as the KPIs which is measures performance of

establishment. This indicator is used in order to measures competence of both the monetary and

non-monetary operations (Otley, 2016). This is the best planning tool which has whole

concentration on high presentation events those are leads towards achievement of main goal line

and aims of corporation. This KPI pointer is used by upper and top management of Unilever who

are completely responsible for solve all the problems and issues which are related with finance.

The higher-level management of Unilever uses the key performance indicator in other to

recognize monetary issues for unanticipated costs and financial cycle those are significant issue

for organization and association. In that organization need to inspire their workers by giving help

and purchase utilizing proper procedures for accomplish objectives. This technique is significant

and compelling for organization so as to make progress by taking care of issues of organization

in a powerful and in important way. Through this Unilever can take effective steps in analysing

12

It refers to the difference in the actual figures in comparison to the planned ones. It gives

the clear picture about the performance of the organization like Unilever. This stated in terms of

over performance or underperformance like favourable and unfavourable. An example is stated

in Appendix.

LO 4

P5 compare different management accounting system to respond financial problems.

Financial issues allude as the money related or support related issues. Yet, few of the

issues are which are mainly being come as a challenge by the organization are introduced as

under:

Late imbursement from clients is now a day is biggest financial problem. In that

organization relies that the credit policies of the entity very much and they need to sell their

items and services on credit to clients. At some point clients are from universally and

inadvertently neglects to pay due sum on time which is called as delayed in payment from

customers. It might the reason an enormous and greatest issue for assembling organization like

Unilever it become an ordinary act of clients.

Key performance indicator:

Key performance indicator is known as the KPIs which is measures performance of

establishment. This indicator is used in order to measures competence of both the monetary and

non-monetary operations (Otley, 2016). This is the best planning tool which has whole

concentration on high presentation events those are leads towards achievement of main goal line

and aims of corporation. This KPI pointer is used by upper and top management of Unilever who

are completely responsible for solve all the problems and issues which are related with finance.

The higher-level management of Unilever uses the key performance indicator in other to

recognize monetary issues for unanticipated costs and financial cycle those are significant issue

for organization and association. In that organization need to inspire their workers by giving help

and purchase utilizing proper procedures for accomplish objectives. This technique is significant

and compelling for organization so as to make progress by taking care of issues of organization

in a powerful and in important way. Through this Unilever can take effective steps in analysing

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.