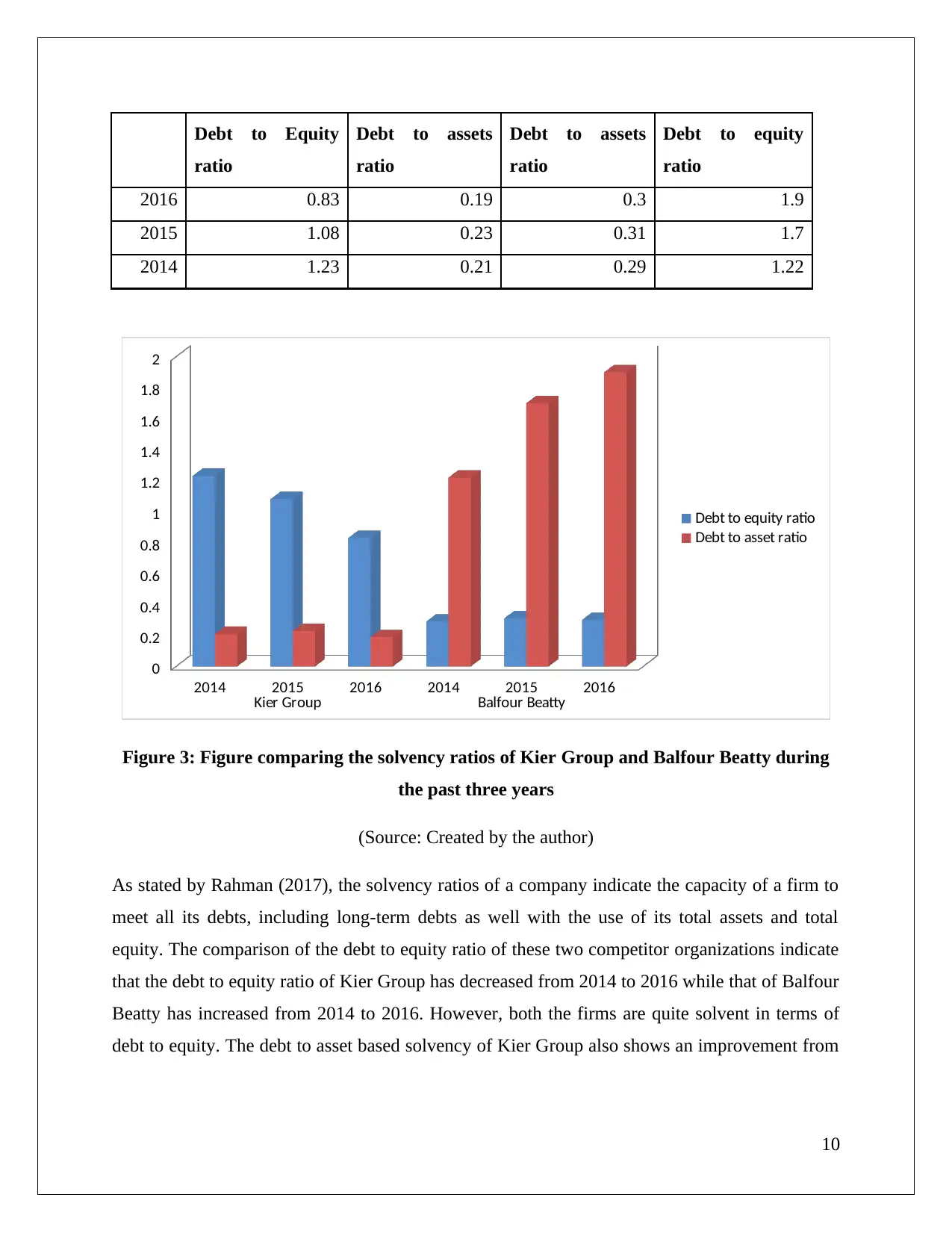

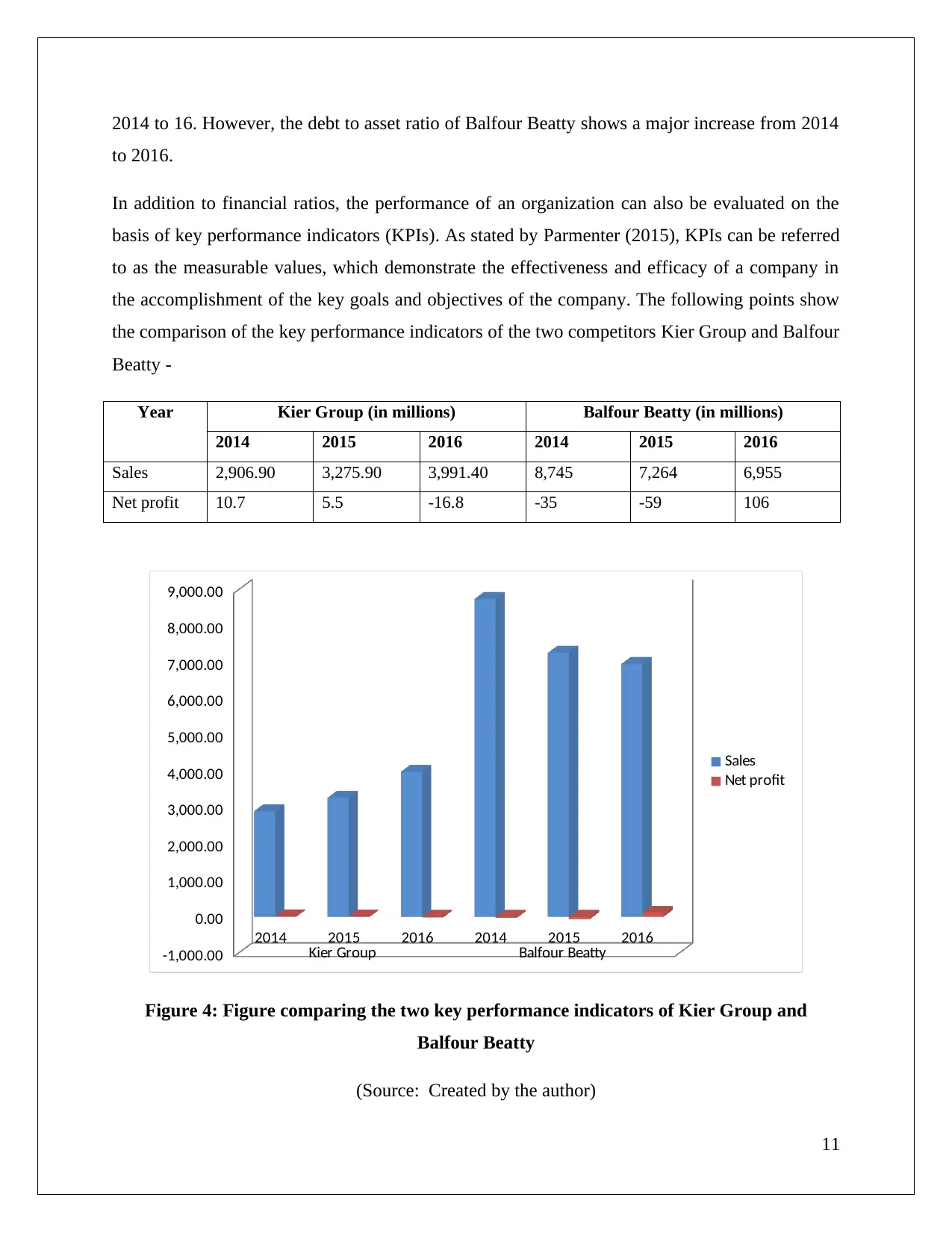

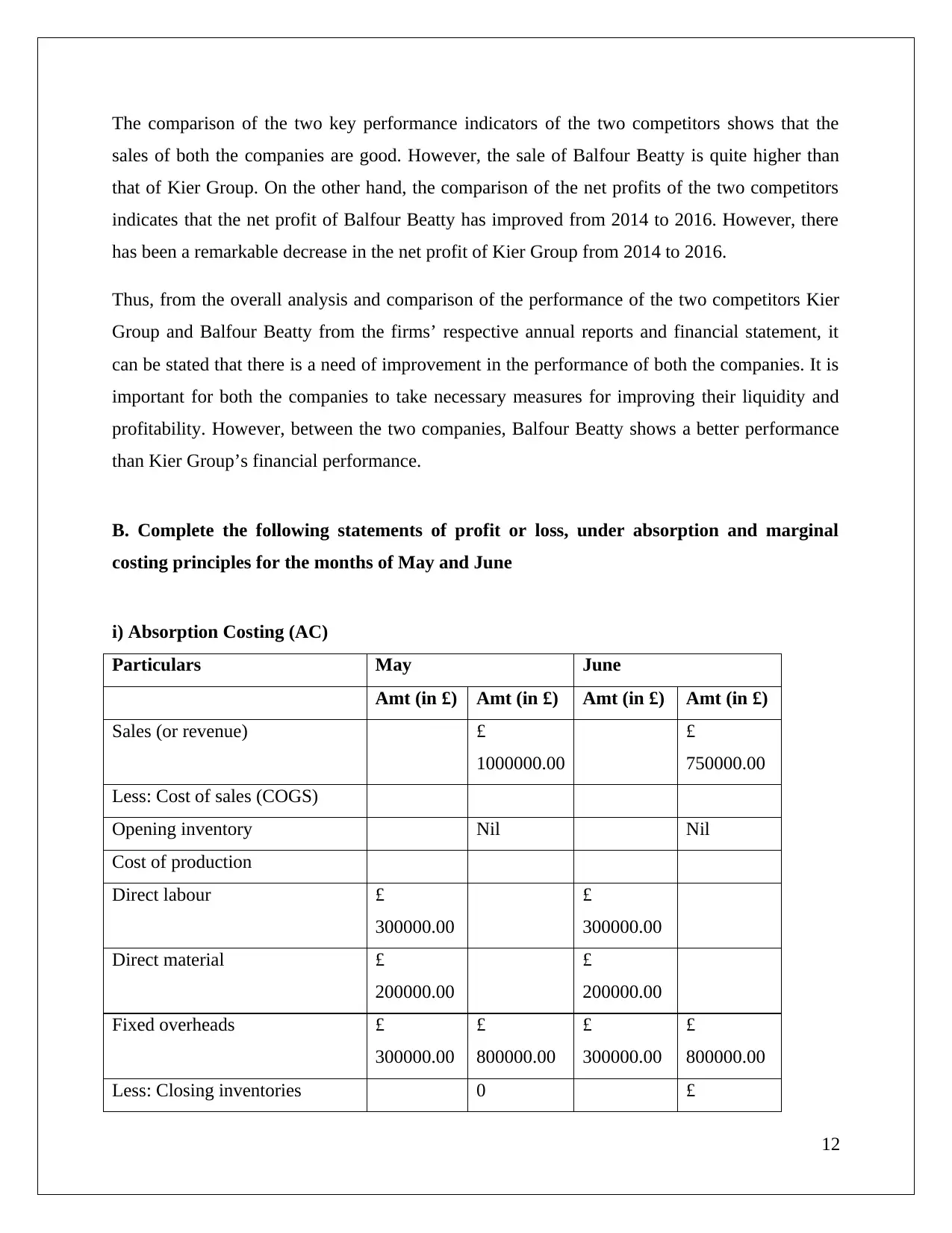

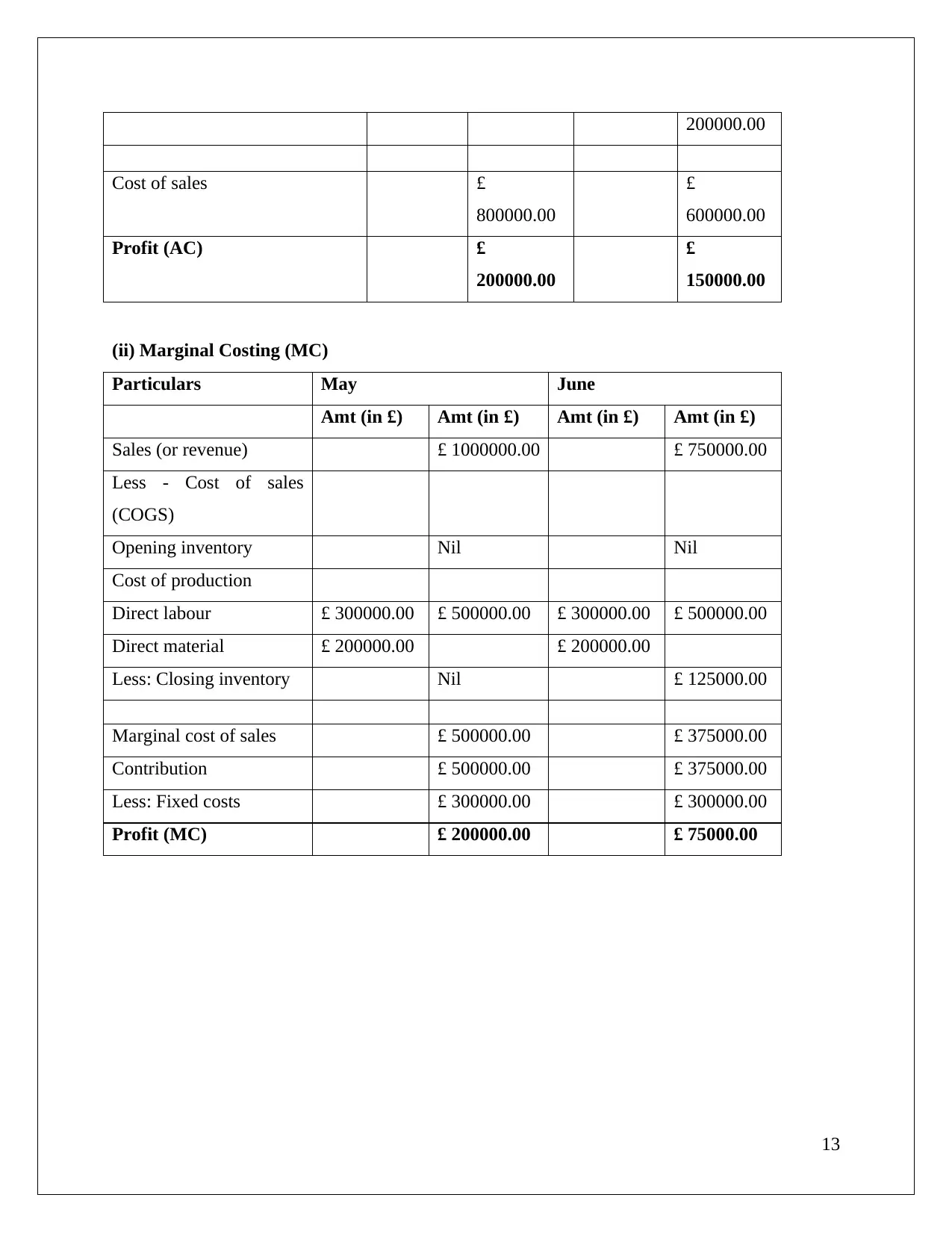

This report delves into the crucial role of management accounting in modern organizations, exploring its various systems and their integration within a company. It examines the benefits of management accounting, including its contribution to planning, controlling, decision-making, and performance evaluation. The report further analyzes the financial performance of two competitor organizations, Kier Group and Balfour Beatty, using key performance indicators and financial ratios. It also provides a detailed comparison of three planning tools commonly used in management accounting: budgeting, variance analysis, and standard costing, highlighting their effectiveness in addressing financial challenges. This comprehensive analysis demonstrates the vital role of management accounting in achieving organizational success.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)