Management Accounting - Tools and Techniques

VerifiedAdded on 2021/02/19

|13

|2255

|37

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

TASK 1 .........................................................................................................................................1

P1- Management accounting and requirements of its different systems.....................................1

P2- Methods of management accounting reporting.....................................................................3

P3- Cost calculation and preparation of income statement using absorption and marginal

costing..........................................................................................................................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

TASK 1 .........................................................................................................................................1

P1- Management accounting and requirements of its different systems.....................................1

P2- Methods of management accounting reporting.....................................................................3

P3- Cost calculation and preparation of income statement using absorption and marginal

costing..........................................................................................................................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

Introduction

Management accounting is a financial analysis technique which is

subordinated by accounting knowledge and financial information disseminated by

accounting professionals to the management body of the organisation in order to

aid the executives in making key critical decisions, designing of programme

structure and evaluating performance of the business (Kaplan, Robert and Anthony,

2015). For drawing better study of management accounting tools and techniques

LSEC Ltd., a newly formed business entity engaged in manufacturing circuit

boards is studied to apply practical and theoretical aspects of management

accounting literature in a real life business situation.

TASK 1

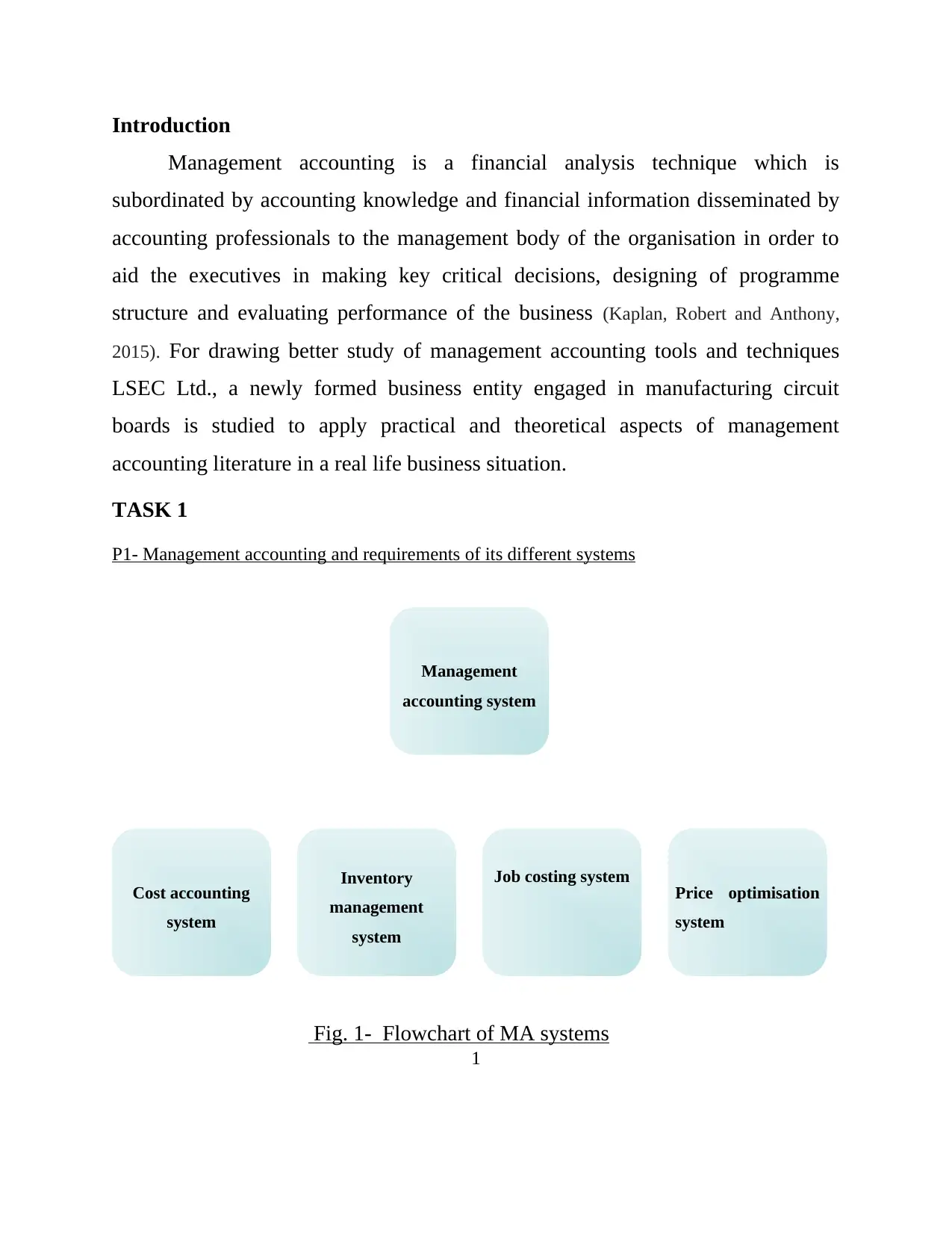

P1- Management accounting and requirements of its different systems

Fig. 1- Flowchart of MA systems

1

Management

accounting system

Cost accounting

system

Inventory

management

system

Job costing system Price optimisation

system

Management accounting is a financial analysis technique which is

subordinated by accounting knowledge and financial information disseminated by

accounting professionals to the management body of the organisation in order to

aid the executives in making key critical decisions, designing of programme

structure and evaluating performance of the business (Kaplan, Robert and Anthony,

2015). For drawing better study of management accounting tools and techniques

LSEC Ltd., a newly formed business entity engaged in manufacturing circuit

boards is studied to apply practical and theoretical aspects of management

accounting literature in a real life business situation.

TASK 1

P1- Management accounting and requirements of its different systems

Fig. 1- Flowchart of MA systems

1

Management

accounting system

Cost accounting

system

Inventory

management

system

Job costing system Price optimisation

system

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management accounting is a systematic flow of important financial data and

valuable financial information related to a specific fiscal period of LSEC Ltd. To

the managerial personnel. The information is highly regarded as a foundation layer

to draw decisive inferences from and help the business grow in a positive direction.

Management accounting is quite different from financial accounting as per their

fundamental use and objectives. Financial information is dedicated towards the

general public. Firms provide financial statements for open public to see and know

about the profitability situation of the business. Generally, stakeholders are

concerned about the financial information and for the preparation of statements,

help of financial accounting is taken, whereas management accounting is purely

internal and used only by the management (Chiwamit, Modell and Yang, 2014). It is

assisted by various sub sets called as management accounting systems. These

systems provide sectoral data which is merged in a single management information

system. Some key systems are as follows:

Price optimisation system: It is a combination of various quantitative

models used to understand demand fluctuations at different price levels. The

information is further processed using costing and inventory levels to optimise

price structure to lowest possible (Brewer, Garrison and Noreen, 2015). This system

helps in keeping prices competitive, initial pricing, promotional pricing and

deciding value proposition. Company uses this technique to identify the pricing

sweet spot and hitting it, or trying to maximise profits through increasing

consumers willingness to pay.

Inventory management system: It is related with the use of technological

software to track the inflow and outflow of goods, inventory laying at the

2

valuable financial information related to a specific fiscal period of LSEC Ltd. To

the managerial personnel. The information is highly regarded as a foundation layer

to draw decisive inferences from and help the business grow in a positive direction.

Management accounting is quite different from financial accounting as per their

fundamental use and objectives. Financial information is dedicated towards the

general public. Firms provide financial statements for open public to see and know

about the profitability situation of the business. Generally, stakeholders are

concerned about the financial information and for the preparation of statements,

help of financial accounting is taken, whereas management accounting is purely

internal and used only by the management (Chiwamit, Modell and Yang, 2014). It is

assisted by various sub sets called as management accounting systems. These

systems provide sectoral data which is merged in a single management information

system. Some key systems are as follows:

Price optimisation system: It is a combination of various quantitative

models used to understand demand fluctuations at different price levels. The

information is further processed using costing and inventory levels to optimise

price structure to lowest possible (Brewer, Garrison and Noreen, 2015). This system

helps in keeping prices competitive, initial pricing, promotional pricing and

deciding value proposition. Company uses this technique to identify the pricing

sweet spot and hitting it, or trying to maximise profits through increasing

consumers willingness to pay.

Inventory management system: It is related with the use of technological

software to track the inflow and outflow of goods, inventory laying at the

2

warehouse and in the transit (Ward, 2012). Through this system, a proper check on

the movement of goods can be traced which helps in eliminating wastage risks,

reducing over stocking or under stocking and ensuring easy availability of goods.

Job costing system: It is a system of cost information accumulation related

to specific service job or manufacturing function. The information is forwarded for

the use of the management to provide it to the client in contract for cost

reimbursement (Wickramasinghe and Alawattage, 2012). Typically, a job costing system

assimilates three major types costs known as direct materials, direct labour, and

overheads.

Cost accounting system: This system is related with intense study of costs

associated with the production of goods. This system evaluates every cost incurred

during production process to keep a cost control check, reduce wastage and help in

deciding prices for the final products (Trucco, 2015). The two internal costing

technique as a part of this system are job order costing and process costing.

P2- Methods of management accounting reporting

Based on the analysis and insights drawn from systems, reports are prepared

to evaluate the performances of the systems, concerned departments, their

processes, deviations between budgeted situations to the actual situations to help

the management in identifying internal problems and drawing their possible

solutions (Modell, 2014). LSEC Ltd. analysts prepare various reports provided to

executives for decision-making which are discussed here as follows:

3

the movement of goods can be traced which helps in eliminating wastage risks,

reducing over stocking or under stocking and ensuring easy availability of goods.

Job costing system: It is a system of cost information accumulation related

to specific service job or manufacturing function. The information is forwarded for

the use of the management to provide it to the client in contract for cost

reimbursement (Wickramasinghe and Alawattage, 2012). Typically, a job costing system

assimilates three major types costs known as direct materials, direct labour, and

overheads.

Cost accounting system: This system is related with intense study of costs

associated with the production of goods. This system evaluates every cost incurred

during production process to keep a cost control check, reduce wastage and help in

deciding prices for the final products (Trucco, 2015). The two internal costing

technique as a part of this system are job order costing and process costing.

P2- Methods of management accounting reporting

Based on the analysis and insights drawn from systems, reports are prepared

to evaluate the performances of the systems, concerned departments, their

processes, deviations between budgeted situations to the actual situations to help

the management in identifying internal problems and drawing their possible

solutions (Modell, 2014). LSEC Ltd. analysts prepare various reports provided to

executives for decision-making which are discussed here as follows:

3

Job cost report: This report contains the ongoing costs accredited with the

production process. It enlists the current state of jobs functioning on the production

and all other job costs which were incurred during the previous years. It helps in

performance evaluation and cost control mechanism. Jobbing is a technique often

used in manufacturing firms to identify each single unit of factor production

engaged in manufacturing process. Assigning cost to each factorial helps in

deciding final price for the business.

Inventory report: This report includes detailed descriptions about the

inventory levels at various warehouses and storage units, total production level,

raw material entered, goods in production and goods in transit etc. it is a mixture of

many small reports which forms a part of final inventory report (Morden, 2016).

generally businesses take loans by mortgaging minimum volume of stock at a time.

This system helps the firm in maintaining requisite level of inventory at all times to

abide to the loan terms.

4

Management

accounting

reports

Job cost reports Inventory reports

Account

receivable and

aging reports

Performance

management

reports

production process. It enlists the current state of jobs functioning on the production

and all other job costs which were incurred during the previous years. It helps in

performance evaluation and cost control mechanism. Jobbing is a technique often

used in manufacturing firms to identify each single unit of factor production

engaged in manufacturing process. Assigning cost to each factorial helps in

deciding final price for the business.

Inventory report: This report includes detailed descriptions about the

inventory levels at various warehouses and storage units, total production level,

raw material entered, goods in production and goods in transit etc. it is a mixture of

many small reports which forms a part of final inventory report (Morden, 2016).

generally businesses take loans by mortgaging minimum volume of stock at a time.

This system helps the firm in maintaining requisite level of inventory at all times to

abide to the loan terms.

4

Management

accounting

reports

Job cost reports Inventory reports

Account

receivable and

aging reports

Performance

management

reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance report: This report includes details about performance

evaluation of various business segments like personnels, strategies, departments,

market standing, products etc. the variations between the budgeted figures to the

actual figures helps management in identifying solutions to the problems. These

reports are prepared with the help of techniques and models offered by eminent

management thinkers to evaluate performance using various mathematical and

behavioural models. Performances are subjective in nature so are the models.

Models rates every factor based on various factors which gives a comprehensive

view of various parameters.

Account receivable report: This report contains periodic details of the

creditors and debtors, bills to be received, due dates, funds in circulation, interest

rates, and other terms and conditions associated with credit policy of the business

(Suomala and Lyly-Yrjänäinen, 2012). This report helps in tracking funds flow,

managing money better and reducing financial losses. This report also includes

total amount of funds received and paid in a year which helps the management in

identifying liquidity situation of the firm.

P3- Cost calculation and preparation of income statement using absorption and

marginal costing

Cost Analysis: This analysis is used to establish a positive relationship

between cost and output. Costs incurred on production should result in fruitful

outcomes. The management uses this technique to identify various possible

solutions to adapt correct inputs and use those inputs in production for maximum

benefits (Schaltegger and Csutora, 2012).

5

evaluation of various business segments like personnels, strategies, departments,

market standing, products etc. the variations between the budgeted figures to the

actual figures helps management in identifying solutions to the problems. These

reports are prepared with the help of techniques and models offered by eminent

management thinkers to evaluate performance using various mathematical and

behavioural models. Performances are subjective in nature so are the models.

Models rates every factor based on various factors which gives a comprehensive

view of various parameters.

Account receivable report: This report contains periodic details of the

creditors and debtors, bills to be received, due dates, funds in circulation, interest

rates, and other terms and conditions associated with credit policy of the business

(Suomala and Lyly-Yrjänäinen, 2012). This report helps in tracking funds flow,

managing money better and reducing financial losses. This report also includes

total amount of funds received and paid in a year which helps the management in

identifying liquidity situation of the firm.

P3- Cost calculation and preparation of income statement using absorption and

marginal costing

Cost Analysis: This analysis is used to establish a positive relationship

between cost and output. Costs incurred on production should result in fruitful

outcomes. The management uses this technique to identify various possible

solutions to adapt correct inputs and use those inputs in production for maximum

benefits (Schaltegger and Csutora, 2012).

5

Income statement: This statement is one of the financial statements

prepared to determine the financial health of the business. This statement is

prepared in dedicated format which contains lists of profits and losses occurred

during a period, It is prepared by deducting expenses from the income earned

during the period to identify net loss or profits. It tells the operating health of the

firm (Yalcin, 2012).

Absorption costing: This costing system undertakes all fixed and variable

costs into account during the production (Strauss, Kristandl and Quinn, 2015). It

undertakes all overhead as well as direct costs incidental to the production into

account and then allocates them to individual accounts. This method is fruitful in

calculation of inventory levels as it contains all costs such as variable, fixed and

overheads costs in one head.

Marginal costing: Under this method, total cost is ascertained as a result of

change in total cost due to addition in cost as an effect of increase in one additional

unit of production. It includes the incremental value of the cost, not all costs.

Marginal costs for goods which are customised are pretty high as compared to

goods which are produced in large volumes as it reduces the variable cost per unit

element.

Selling Price £273

Production Unit 4000 Units

Total Cost of manufacturing a Circuit Board £210

Direct Material £70

6

prepared to determine the financial health of the business. This statement is

prepared in dedicated format which contains lists of profits and losses occurred

during a period, It is prepared by deducting expenses from the income earned

during the period to identify net loss or profits. It tells the operating health of the

firm (Yalcin, 2012).

Absorption costing: This costing system undertakes all fixed and variable

costs into account during the production (Strauss, Kristandl and Quinn, 2015). It

undertakes all overhead as well as direct costs incidental to the production into

account and then allocates them to individual accounts. This method is fruitful in

calculation of inventory levels as it contains all costs such as variable, fixed and

overheads costs in one head.

Marginal costing: Under this method, total cost is ascertained as a result of

change in total cost due to addition in cost as an effect of increase in one additional

unit of production. It includes the incremental value of the cost, not all costs.

Marginal costs for goods which are customised are pretty high as compared to

goods which are produced in large volumes as it reduces the variable cost per unit

element.

Selling Price £273

Production Unit 4000 Units

Total Cost of manufacturing a Circuit Board £210

Direct Material £70

6

Direct Labour £90

Direct Expenses £30

Employees in the manufacturing department are to be paid £9 per hour

Fixed Admin Costs £20000

Other Overhead £60000

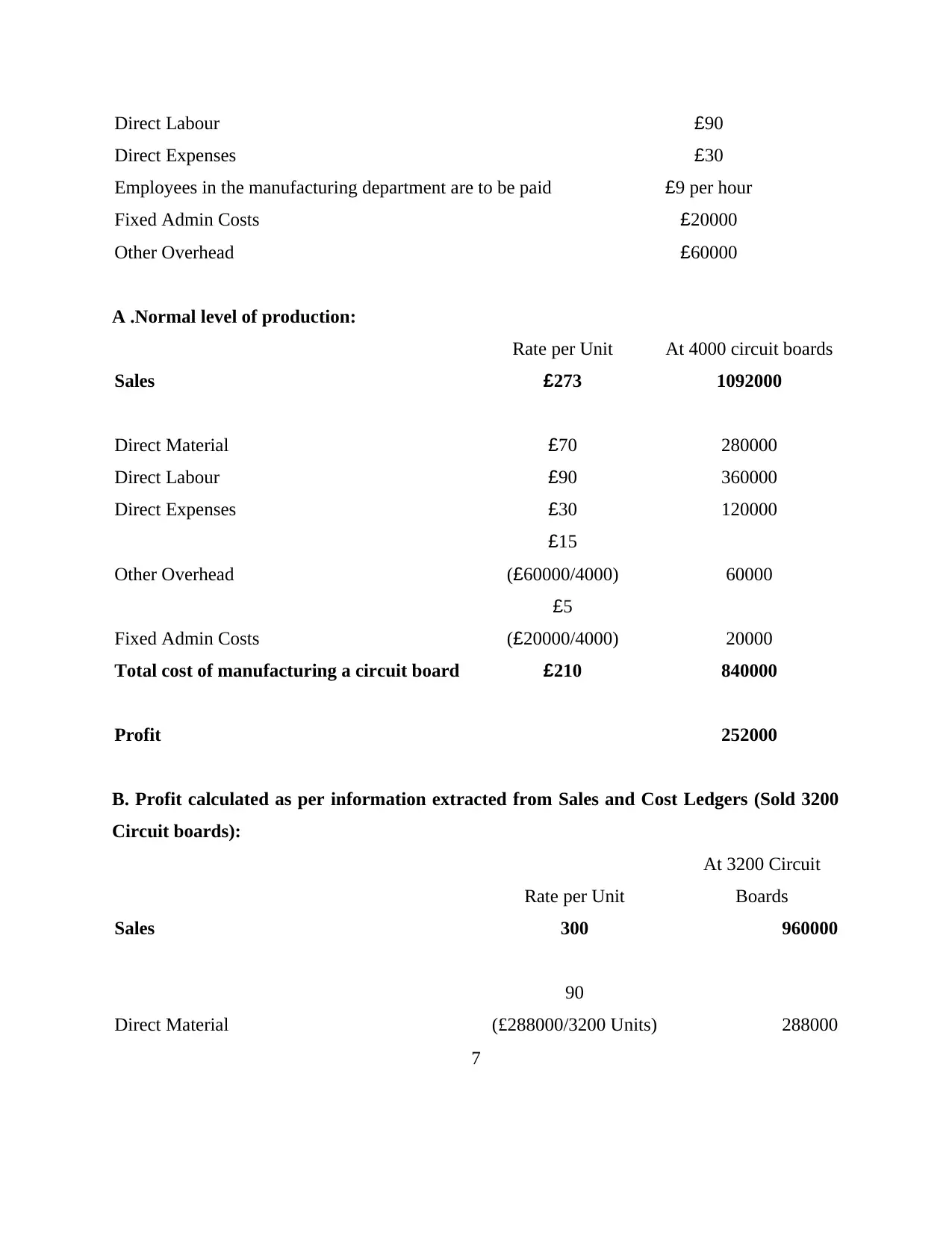

A .Normal level of production:

Rate per Unit At 4000 circuit boards

Sales £273 1092000

Direct Material £70 280000

Direct Labour £90 360000

Direct Expenses £30 120000

Other Overhead

£15

(£60000/4000) 60000

Fixed Admin Costs

£5

(£20000/4000) 20000

Total cost of manufacturing a circuit board £210 840000

Profit 252000

B. Profit calculated as per information extracted from Sales and Cost Ledgers (Sold 3200

Circuit boards):

Rate per Unit

At 3200 Circuit

Boards

Sales 300 960000

Direct Material

90

(£288000/3200 Units) 288000

7

Direct Expenses £30

Employees in the manufacturing department are to be paid £9 per hour

Fixed Admin Costs £20000

Other Overhead £60000

A .Normal level of production:

Rate per Unit At 4000 circuit boards

Sales £273 1092000

Direct Material £70 280000

Direct Labour £90 360000

Direct Expenses £30 120000

Other Overhead

£15

(£60000/4000) 60000

Fixed Admin Costs

£5

(£20000/4000) 20000

Total cost of manufacturing a circuit board £210 840000

Profit 252000

B. Profit calculated as per information extracted from Sales and Cost Ledgers (Sold 3200

Circuit boards):

Rate per Unit

At 3200 Circuit

Boards

Sales 300 960000

Direct Material

90

(£288000/3200 Units) 288000

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

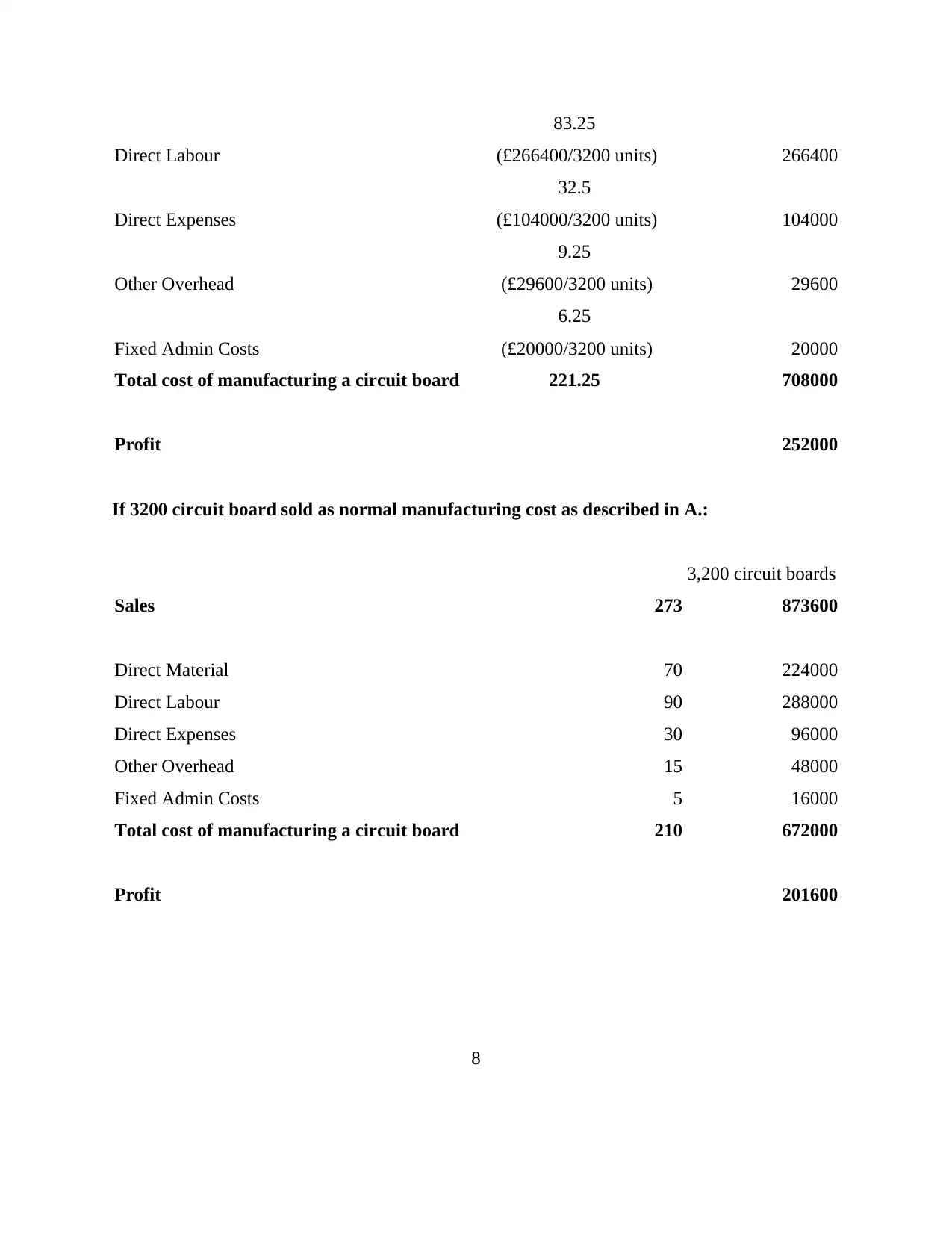

Direct Labour

83.25

(£266400/3200 units) 266400

Direct Expenses

32.5

(£104000/3200 units) 104000

Other Overhead

9.25

(£29600/3200 units) 29600

Fixed Admin Costs

6.25

(£20000/3200 units) 20000

Total cost of manufacturing a circuit board 221.25 708000

Profit 252000

If 3200 circuit board sold as normal manufacturing cost as described in A.:

3,200 circuit boards

Sales 273 873600

Direct Material 70 224000

Direct Labour 90 288000

Direct Expenses 30 96000

Other Overhead 15 48000

Fixed Admin Costs 5 16000

Total cost of manufacturing a circuit board 210 672000

Profit 201600

8

83.25

(£266400/3200 units) 266400

Direct Expenses

32.5

(£104000/3200 units) 104000

Other Overhead

9.25

(£29600/3200 units) 29600

Fixed Admin Costs

6.25

(£20000/3200 units) 20000

Total cost of manufacturing a circuit board 221.25 708000

Profit 252000

If 3200 circuit board sold as normal manufacturing cost as described in A.:

3,200 circuit boards

Sales 273 873600

Direct Material 70 224000

Direct Labour 90 288000

Direct Expenses 30 96000

Other Overhead 15 48000

Fixed Admin Costs 5 16000

Total cost of manufacturing a circuit board 210 672000

Profit 201600

8

Findings: From the above calculations taken two scenarios of A and B into

account. Scenario B where per unit cost is taken as 300 per unit is profitable

for the business as compared to the sales rate per unit at 273 for the same

amount of unit. Looking as per the feasibility analysis the firm should long

for option B price band.

CONCLUSION

From this report, it can be concluded that management accounting is a great

source for the management to form policies and strategy framework for the future.

Management accounting practices at LSEC Ltd. Has evolved into a precise set of

structural decision-making system which has enabled the firm in achieving growth

figures. Using various systems, reports, tools and techniques offered by

management accounting literature has empowered the business with technical

adaptabilities and problem solving mechanism.

9

account. Scenario B where per unit cost is taken as 300 per unit is profitable

for the business as compared to the sales rate per unit at 273 for the same

amount of unit. Looking as per the feasibility analysis the firm should long

for option B price band.

CONCLUSION

From this report, it can be concluded that management accounting is a great

source for the management to form policies and strategy framework for the future.

Management accounting practices at LSEC Ltd. Has evolved into a precise set of

structural decision-making system which has enabled the firm in achieving growth

figures. Using various systems, reports, tools and techniques offered by

management accounting literature has empowered the business with technical

adaptabilities and problem solving mechanism.

9

REFERENCES

Books and Journals:

Brewer, P. C., Garrison, R. H. and Noreen, E. W., 2015. Introduction to managerial accounting.

McGraw-Hill Education.

Chiwamit, P., Modell, S. and Yang, C. L., 2014. The societal relevance of management

accounting innovations: economic value added and institutional work in the fields of

Chinese and Thai state-owned enterprises. Accounting and Business Research. 44(2).

pp.144-180.

Kaplan, Robert S., and Anthony A., 2015. Advanced management accounting. PHI Learning.

Modell, S., 2014. The societal relevance of management accounting: an introduction to the

special issue. Accounting and Business Research. 44(2). pp.83-103.

Morden, T., 2016. Principles of strategic management. Routledge.

Schaltegger, S. and Csutora, M., 2012. Carbon accounting for sustainability and management.

Status quo and challenges. Journal of Cleaner Production. 36. pp.1-16.

Strauss, E., Kristandl, G. and Quinn, M., 2015. The effects of cloud technology on management

accounting and decision-making. Management and Financial Accounting Report. 10(6).

Suomala, P. and Lyly-Yrjänäinen, J., 2012. Management accounting research in practice:

Lessons learned from an interventionist approach. Routledge.

Trucco, S., 2015. Financial accounting: development paths and alignment to management

accounting in the Italian context. Springer.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

Yalcin, S., 2012. Adoption and benefits of management accounting practices: an inter-country

comparison. Accounting in Europe. 9(1). pp.95-110.

Books and Journals:

Brewer, P. C., Garrison, R. H. and Noreen, E. W., 2015. Introduction to managerial accounting.

McGraw-Hill Education.

Chiwamit, P., Modell, S. and Yang, C. L., 2014. The societal relevance of management

accounting innovations: economic value added and institutional work in the fields of

Chinese and Thai state-owned enterprises. Accounting and Business Research. 44(2).

pp.144-180.

Kaplan, Robert S., and Anthony A., 2015. Advanced management accounting. PHI Learning.

Modell, S., 2014. The societal relevance of management accounting: an introduction to the

special issue. Accounting and Business Research. 44(2). pp.83-103.

Morden, T., 2016. Principles of strategic management. Routledge.

Schaltegger, S. and Csutora, M., 2012. Carbon accounting for sustainability and management.

Status quo and challenges. Journal of Cleaner Production. 36. pp.1-16.

Strauss, E., Kristandl, G. and Quinn, M., 2015. The effects of cloud technology on management

accounting and decision-making. Management and Financial Accounting Report. 10(6).

Suomala, P. and Lyly-Yrjänäinen, J., 2012. Management accounting research in practice:

Lessons learned from an interventionist approach. Routledge.

Trucco, S., 2015. Financial accounting: development paths and alignment to management

accounting in the Italian context. Springer.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

Yalcin, S., 2012. Adoption and benefits of management accounting practices: an inter-country

comparison. Accounting in Europe. 9(1). pp.95-110.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.