Alternative Exam Assignment: Management Accounting Solution

VerifiedAdded on 2023/06/10

|12

|2478

|192

Homework Assignment

AI Summary

This document presents a comprehensive solution to a management accounting assignment, addressing key concepts and techniques. The solution begins with an introduction to management accounting, emphasizing its role in financial strategy and operational management. It then delves into specific questions, starting with the application of the high-low method to estimate variable and fixed costs in a hospital setting. The solution calculates operating costs at different occupancy rates. Further, it explores the use of absorption and marginal costing methods for income statement analysis and production cost calculations. The assignment also encompasses variance analysis, including material price and usage variances, labor rate and efficiency variances, and overhead variances. The solution explains the causes behind these variances and their examination in relation to work performance. Additionally, the document provides a detailed analysis of opportunity costs, incremental costs, and make-or-buy decisions, including relevant cost calculations. The conclusion summarizes the key takeaways, highlighting the role of management accounting in informed decision-making and the impact of various factors on cost control and efficiency.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.................................................................................................................................3

Main Body.............................................................................................................................................3

QUESTION 1....................................................................................................................................3

QUESTION 3....................................................................................................................................4

QUESTION 4....................................................................................................................................6

QUESTION 5....................................................................................................................................8

CONCLUSION...................................................................................................................................11

References...........................................................................................................................................12

INTRODUCTION.................................................................................................................................3

Main Body.............................................................................................................................................3

QUESTION 1....................................................................................................................................3

QUESTION 3....................................................................................................................................4

QUESTION 4....................................................................................................................................6

QUESTION 5....................................................................................................................................8

CONCLUSION...................................................................................................................................11

References...........................................................................................................................................12

INTRODUCTION

Management accounting is the procedure of identifying, measuring, analyzing and

interpreting the financial statements. It helps the managers of the business enterprise to make

good financial strategies and manage the day – to- day business operations of the company. It

helps the owners to take long – term as well as short – term decisions. The upcoming report

contains the different tools and techniques that are used by the managers to make appropriate

decisions. In addition to this, it consists the calculation of variable costs and fixed operating

cost using the high – low method. Moreover, it holds the evaluation on the income statement

and production per price by the absorption and marginal costing method. Furthermore, it also

encompasses on the different variance analysis method and explanation on opportunity cost,

incremental cost. Moreover, the report also comprises of the purchase and buy decision based

on the computation.

Main Body

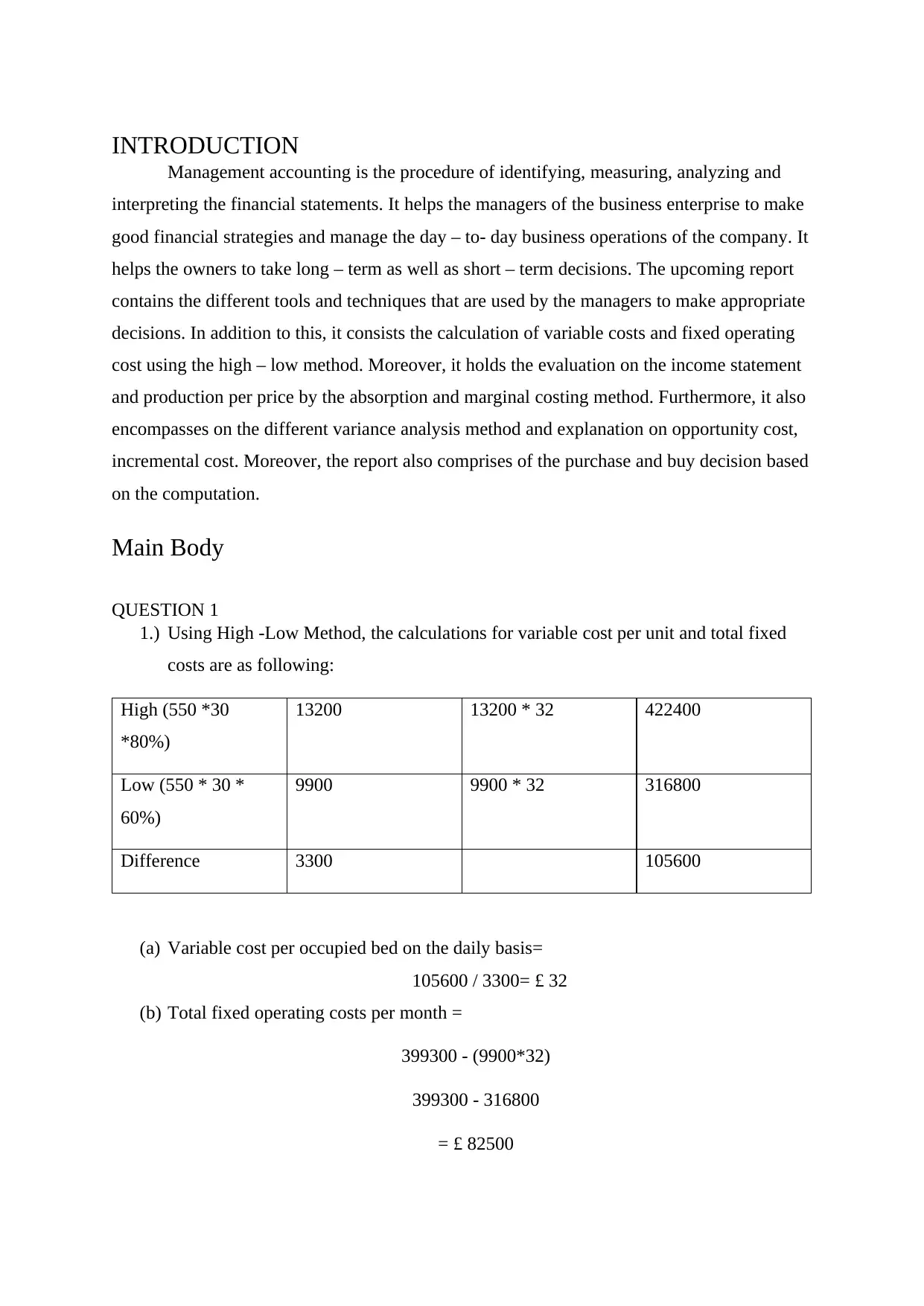

QUESTION 1

1.) Using High -Low Method, the calculations for variable cost per unit and total fixed

costs are as following:

High (550 *30

*80%)

13200 13200 * 32 422400

Low (550 * 30 *

60%)

9900 9900 * 32 316800

Difference 3300 105600

(a) Variable cost per occupied bed on the daily basis=

105600 / 3300= £ 32

(b) Total fixed operating costs per month =

399300 - (9900*32)

399300 - 316800

= £ 82500

Management accounting is the procedure of identifying, measuring, analyzing and

interpreting the financial statements. It helps the managers of the business enterprise to make

good financial strategies and manage the day – to- day business operations of the company. It

helps the owners to take long – term as well as short – term decisions. The upcoming report

contains the different tools and techniques that are used by the managers to make appropriate

decisions. In addition to this, it consists the calculation of variable costs and fixed operating

cost using the high – low method. Moreover, it holds the evaluation on the income statement

and production per price by the absorption and marginal costing method. Furthermore, it also

encompasses on the different variance analysis method and explanation on opportunity cost,

incremental cost. Moreover, the report also comprises of the purchase and buy decision based

on the computation.

Main Body

QUESTION 1

1.) Using High -Low Method, the calculations for variable cost per unit and total fixed

costs are as following:

High (550 *30

*80%)

13200 13200 * 32 422400

Low (550 * 30 *

60%)

9900 9900 * 32 316800

Difference 3300 105600

(a) Variable cost per occupied bed on the daily basis=

105600 / 3300= £ 32

(b) Total fixed operating costs per month =

399300 - (9900*32)

399300 - 316800

= £ 82500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

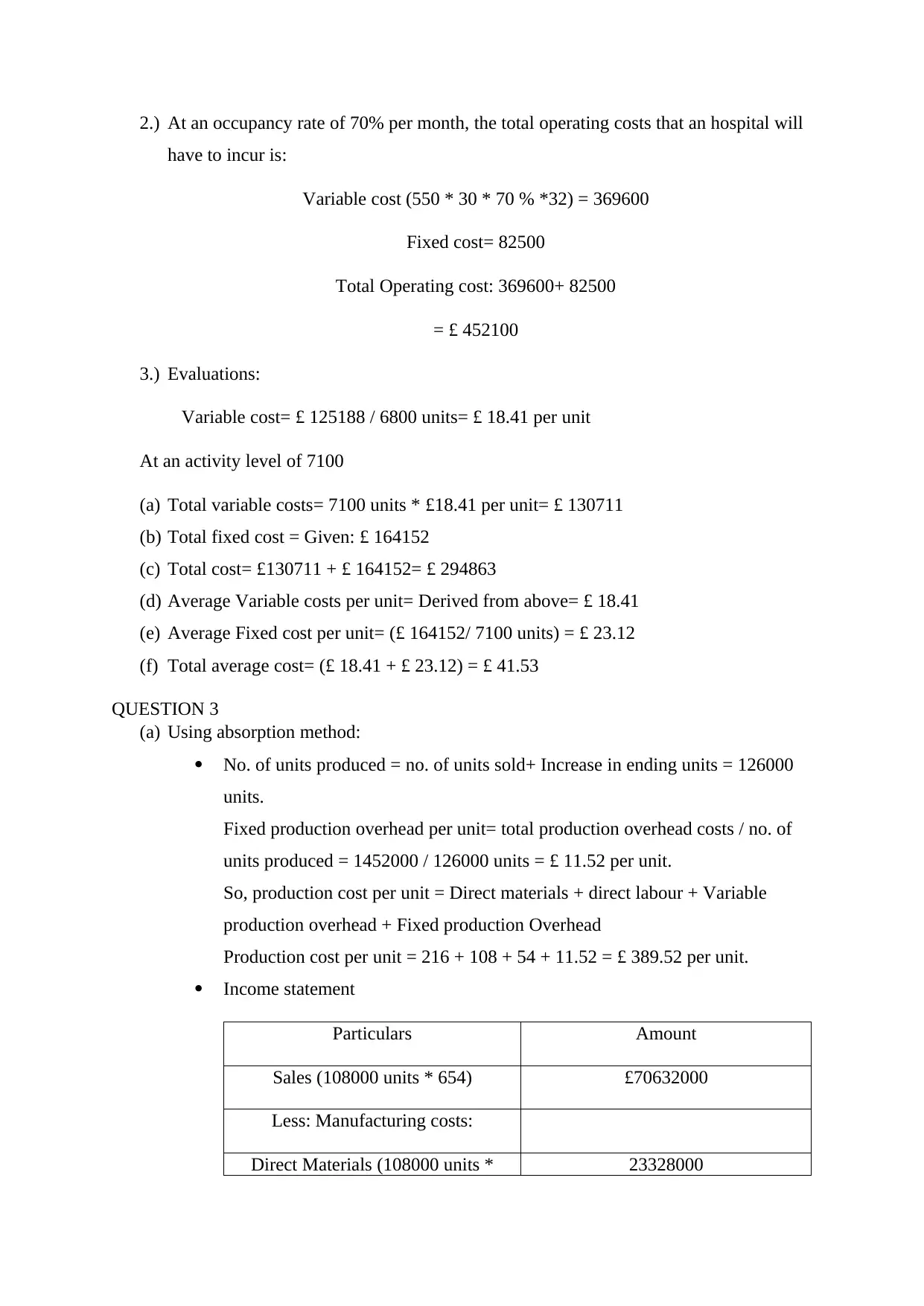

2.) At an occupancy rate of 70% per month, the total operating costs that an hospital will

have to incur is:

Variable cost (550 * 30 * 70 % *32) = 369600

Fixed cost= 82500

Total Operating cost: 369600+ 82500

= £ 452100

3.) Evaluations:

Variable cost= £ 125188 / 6800 units= £ 18.41 per unit

At an activity level of 7100

(a) Total variable costs= 7100 units * £18.41 per unit= £ 130711

(b) Total fixed cost = Given: £ 164152

(c) Total cost= £130711 + £ 164152= £ 294863

(d) Average Variable costs per unit= Derived from above= £ 18.41

(e) Average Fixed cost per unit= (£ 164152/ 7100 units) = £ 23.12

(f) Total average cost= (£ 18.41 + £ 23.12) = £ 41.53

QUESTION 3

(a) Using absorption method:

No. of units produced = no. of units sold+ Increase in ending units = 126000

units.

Fixed production overhead per unit= total production overhead costs / no. of

units produced = 1452000 / 126000 units = £ 11.52 per unit.

So, production cost per unit = Direct materials + direct labour + Variable

production overhead + Fixed production Overhead

Production cost per unit = 216 + 108 + 54 + 11.52 = £ 389.52 per unit.

Income statement

Particulars Amount

Sales (108000 units * 654) £70632000

Less: Manufacturing costs:

Direct Materials (108000 units * 23328000

have to incur is:

Variable cost (550 * 30 * 70 % *32) = 369600

Fixed cost= 82500

Total Operating cost: 369600+ 82500

= £ 452100

3.) Evaluations:

Variable cost= £ 125188 / 6800 units= £ 18.41 per unit

At an activity level of 7100

(a) Total variable costs= 7100 units * £18.41 per unit= £ 130711

(b) Total fixed cost = Given: £ 164152

(c) Total cost= £130711 + £ 164152= £ 294863

(d) Average Variable costs per unit= Derived from above= £ 18.41

(e) Average Fixed cost per unit= (£ 164152/ 7100 units) = £ 23.12

(f) Total average cost= (£ 18.41 + £ 23.12) = £ 41.53

QUESTION 3

(a) Using absorption method:

No. of units produced = no. of units sold+ Increase in ending units = 126000

units.

Fixed production overhead per unit= total production overhead costs / no. of

units produced = 1452000 / 126000 units = £ 11.52 per unit.

So, production cost per unit = Direct materials + direct labour + Variable

production overhead + Fixed production Overhead

Production cost per unit = 216 + 108 + 54 + 11.52 = £ 389.52 per unit.

Income statement

Particulars Amount

Sales (108000 units * 654) £70632000

Less: Manufacturing costs:

Direct Materials (108000 units * 23328000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

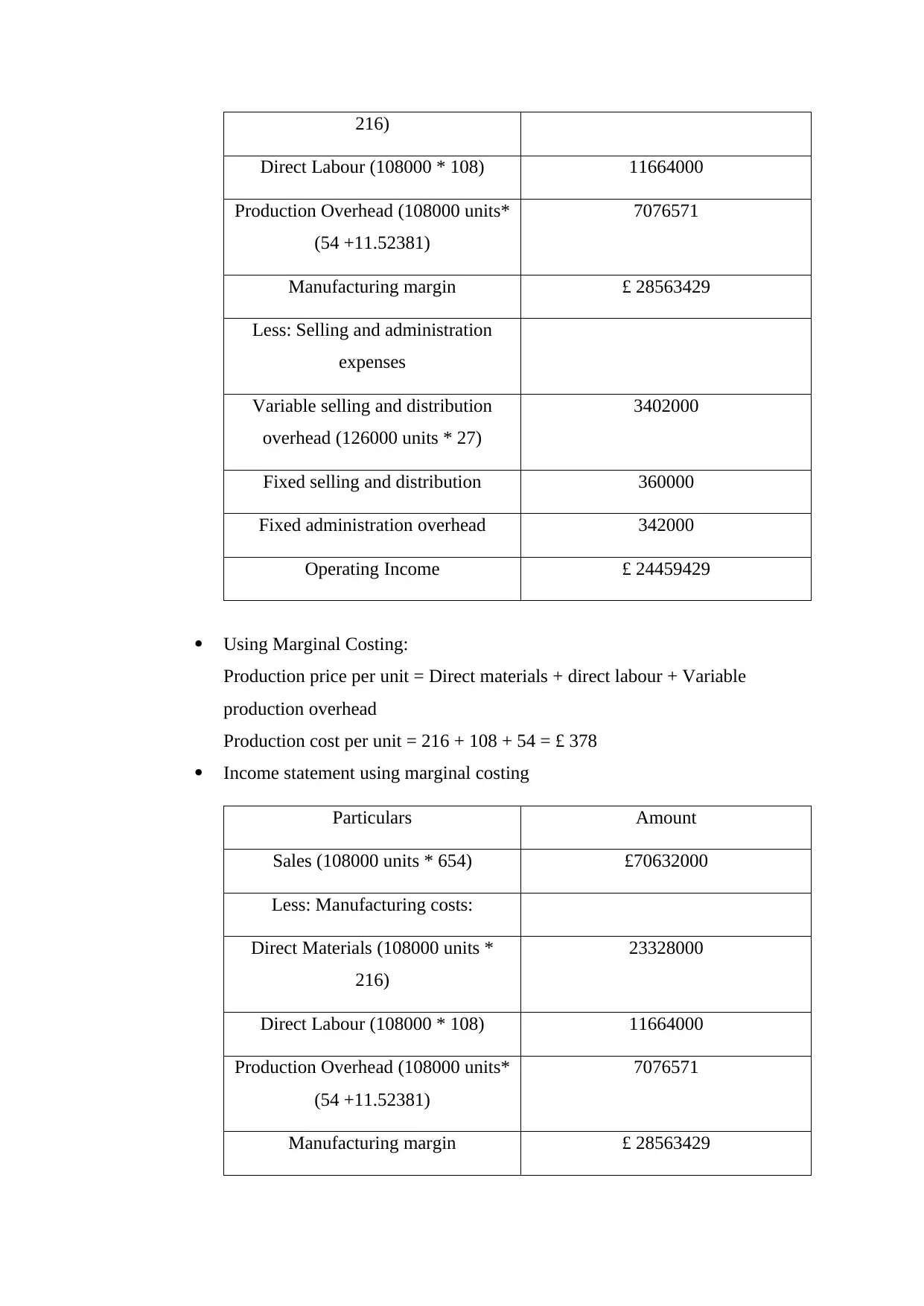

216)

Direct Labour (108000 * 108) 11664000

Production Overhead (108000 units*

(54 +11.52381)

7076571

Manufacturing margin £ 28563429

Less: Selling and administration

expenses

Variable selling and distribution

overhead (126000 units * 27)

3402000

Fixed selling and distribution 360000

Fixed administration overhead 342000

Operating Income £ 24459429

Using Marginal Costing:

Production price per unit = Direct materials + direct labour + Variable

production overhead

Production cost per unit = 216 + 108 + 54 = £ 378

Income statement using marginal costing

Particulars Amount

Sales (108000 units * 654) £70632000

Less: Manufacturing costs:

Direct Materials (108000 units *

216)

23328000

Direct Labour (108000 * 108) 11664000

Production Overhead (108000 units*

(54 +11.52381)

7076571

Manufacturing margin £ 28563429

Direct Labour (108000 * 108) 11664000

Production Overhead (108000 units*

(54 +11.52381)

7076571

Manufacturing margin £ 28563429

Less: Selling and administration

expenses

Variable selling and distribution

overhead (126000 units * 27)

3402000

Fixed selling and distribution 360000

Fixed administration overhead 342000

Operating Income £ 24459429

Using Marginal Costing:

Production price per unit = Direct materials + direct labour + Variable

production overhead

Production cost per unit = 216 + 108 + 54 = £ 378

Income statement using marginal costing

Particulars Amount

Sales (108000 units * 654) £70632000

Less: Manufacturing costs:

Direct Materials (108000 units *

216)

23328000

Direct Labour (108000 * 108) 11664000

Production Overhead (108000 units*

(54 +11.52381)

7076571

Manufacturing margin £ 28563429

Less: Selling and administration

expenses

Variable selling and distribution

overhead (126000 units * 27)

3402000

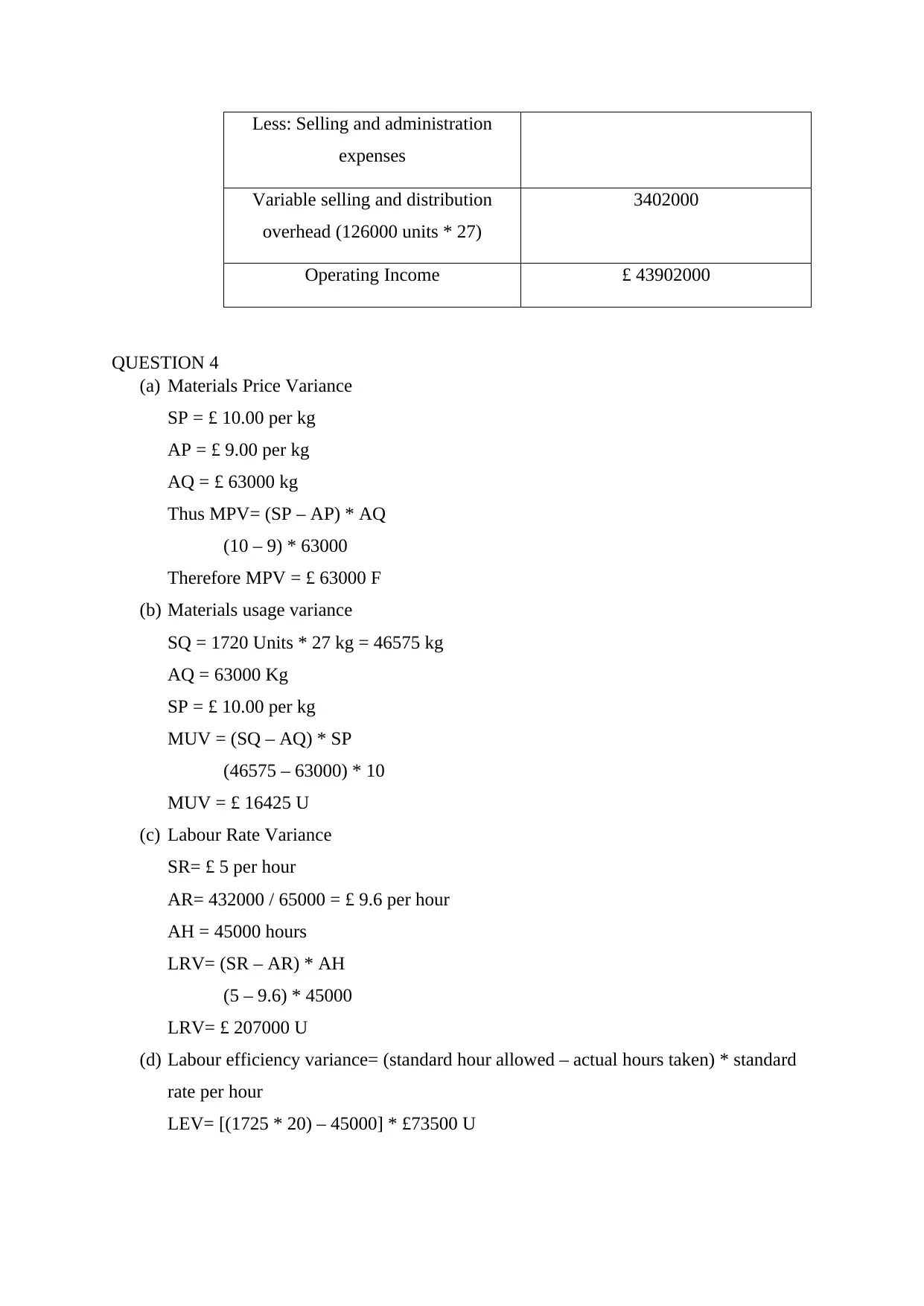

Operating Income £ 43902000

QUESTION 4

(a) Materials Price Variance

SP = £ 10.00 per kg

AP = £ 9.00 per kg

AQ = £ 63000 kg

Thus MPV= (SP – AP) * AQ

(10 – 9) * 63000

Therefore MPV = £ 63000 F

(b) Materials usage variance

SQ = 1720 Units * 27 kg = 46575 kg

AQ = 63000 Kg

SP = £ 10.00 per kg

MUV = (SQ – AQ) * SP

(46575 – 63000) * 10

MUV = £ 16425 U

(c) Labour Rate Variance

SR= £ 5 per hour

AR= 432000 / 65000 = £ 9.6 per hour

AH = 45000 hours

LRV= (SR – AR) * AH

(5 – 9.6) * 45000

LRV= £ 207000 U

(d) Labour efficiency variance= (standard hour allowed – actual hours taken) * standard

rate per hour

LEV= [(1725 * 20) – 45000] * £73500 U

expenses

Variable selling and distribution

overhead (126000 units * 27)

3402000

Operating Income £ 43902000

QUESTION 4

(a) Materials Price Variance

SP = £ 10.00 per kg

AP = £ 9.00 per kg

AQ = £ 63000 kg

Thus MPV= (SP – AP) * AQ

(10 – 9) * 63000

Therefore MPV = £ 63000 F

(b) Materials usage variance

SQ = 1720 Units * 27 kg = 46575 kg

AQ = 63000 Kg

SP = £ 10.00 per kg

MUV = (SQ – AQ) * SP

(46575 – 63000) * 10

MUV = £ 16425 U

(c) Labour Rate Variance

SR= £ 5 per hour

AR= 432000 / 65000 = £ 9.6 per hour

AH = 45000 hours

LRV= (SR – AR) * AH

(5 – 9.6) * 45000

LRV= £ 207000 U

(d) Labour efficiency variance= (standard hour allowed – actual hours taken) * standard

rate per hour

LEV= [(1725 * 20) – 45000] * £73500 U

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

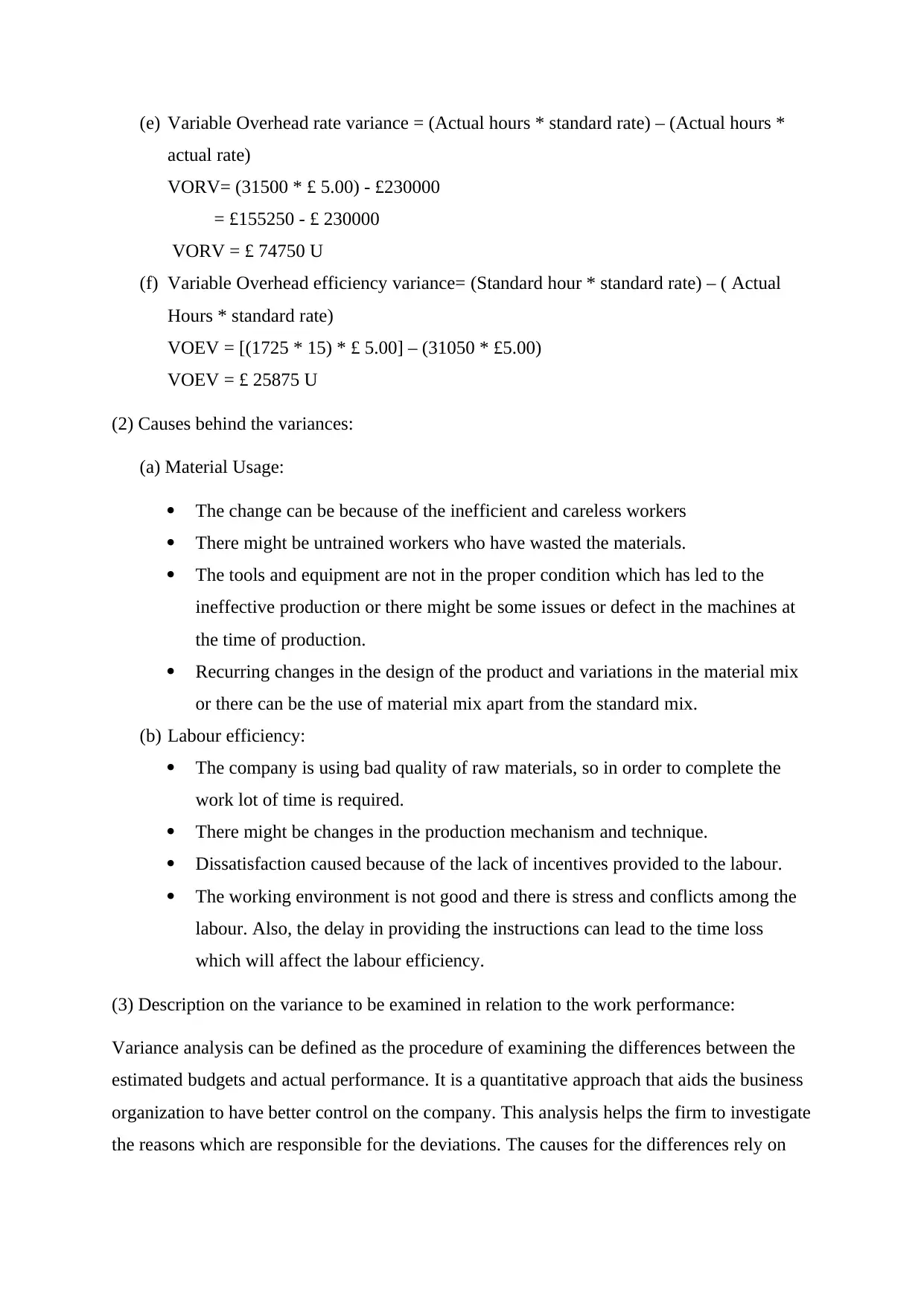

(e) Variable Overhead rate variance = (Actual hours * standard rate) – (Actual hours *

actual rate)

VORV= (31500 * £ 5.00) - £230000

= £155250 - £ 230000

VORV = £ 74750 U

(f) Variable Overhead efficiency variance= (Standard hour * standard rate) – ( Actual

Hours * standard rate)

VOEV = [(1725 * 15) * £ 5.00] – (31050 * £5.00)

VOEV = £ 25875 U

(2) Causes behind the variances:

(a) Material Usage:

The change can be because of the inefficient and careless workers

There might be untrained workers who have wasted the materials.

The tools and equipment are not in the proper condition which has led to the

ineffective production or there might be some issues or defect in the machines at

the time of production.

Recurring changes in the design of the product and variations in the material mix

or there can be the use of material mix apart from the standard mix.

(b) Labour efficiency:

The company is using bad quality of raw materials, so in order to complete the

work lot of time is required.

There might be changes in the production mechanism and technique.

Dissatisfaction caused because of the lack of incentives provided to the labour.

The working environment is not good and there is stress and conflicts among the

labour. Also, the delay in providing the instructions can lead to the time loss

which will affect the labour efficiency.

(3) Description on the variance to be examined in relation to the work performance:

Variance analysis can be defined as the procedure of examining the differences between the

estimated budgets and actual performance. It is a quantitative approach that aids the business

organization to have better control on the company. This analysis helps the firm to investigate

the reasons which are responsible for the deviations. The causes for the differences rely on

actual rate)

VORV= (31500 * £ 5.00) - £230000

= £155250 - £ 230000

VORV = £ 74750 U

(f) Variable Overhead efficiency variance= (Standard hour * standard rate) – ( Actual

Hours * standard rate)

VOEV = [(1725 * 15) * £ 5.00] – (31050 * £5.00)

VOEV = £ 25875 U

(2) Causes behind the variances:

(a) Material Usage:

The change can be because of the inefficient and careless workers

There might be untrained workers who have wasted the materials.

The tools and equipment are not in the proper condition which has led to the

ineffective production or there might be some issues or defect in the machines at

the time of production.

Recurring changes in the design of the product and variations in the material mix

or there can be the use of material mix apart from the standard mix.

(b) Labour efficiency:

The company is using bad quality of raw materials, so in order to complete the

work lot of time is required.

There might be changes in the production mechanism and technique.

Dissatisfaction caused because of the lack of incentives provided to the labour.

The working environment is not good and there is stress and conflicts among the

labour. Also, the delay in providing the instructions can lead to the time loss

which will affect the labour efficiency.

(3) Description on the variance to be examined in relation to the work performance:

Variance analysis can be defined as the procedure of examining the differences between the

estimated budgets and actual performance. It is a quantitative approach that aids the business

organization to have better control on the company. This analysis helps the firm to investigate

the reasons which are responsible for the deviations. The causes for the differences rely on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the components like market conditions, labour variances, overhead variances, budget

standards. The following shall be examined:

Variable Overhead spending: It can be done by excluding the standard overhead cost

per unit with the actual cost obtained and then multiplying it with the total quantity of

output.

Purchase price variance: This can be measured by considering the payment made for

actual price of raw material and subtracting the standard cost.

Labour rate variance: It centres on the wages that are paid to the labour and is referred

to the difference actual cost incurred for the direct labour and cost that was mentioned

in the budget.

Material Yield variance: It is defined as the distinction between the actual and

standard output of the production process.

Fixed overhead spending variance: If the difference is unfavourable then it means that

the fixed overhead expenses are more than the budgeted one. If favourable, then they

are less than the budgeted one.

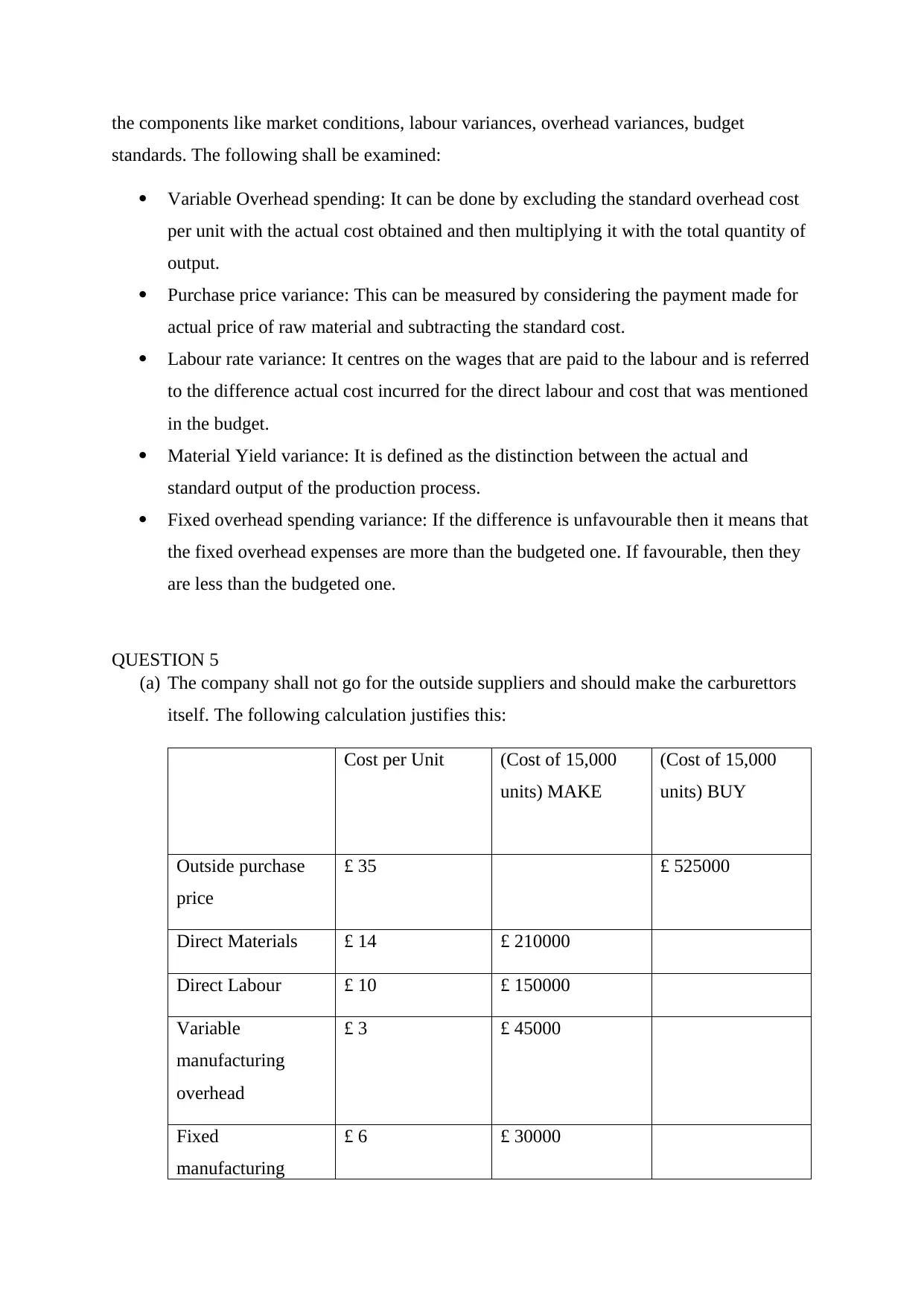

QUESTION 5

(a) The company shall not go for the outside suppliers and should make the carburettors

itself. The following calculation justifies this:

Cost per Unit (Cost of 15,000

units) MAKE

(Cost of 15,000

units) BUY

Outside purchase

price

£ 35 £ 525000

Direct Materials £ 14 £ 210000

Direct Labour £ 10 £ 150000

Variable

manufacturing

overhead

£ 3 £ 45000

Fixed

manufacturing

£ 6 £ 30000

standards. The following shall be examined:

Variable Overhead spending: It can be done by excluding the standard overhead cost

per unit with the actual cost obtained and then multiplying it with the total quantity of

output.

Purchase price variance: This can be measured by considering the payment made for

actual price of raw material and subtracting the standard cost.

Labour rate variance: It centres on the wages that are paid to the labour and is referred

to the difference actual cost incurred for the direct labour and cost that was mentioned

in the budget.

Material Yield variance: It is defined as the distinction between the actual and

standard output of the production process.

Fixed overhead spending variance: If the difference is unfavourable then it means that

the fixed overhead expenses are more than the budgeted one. If favourable, then they

are less than the budgeted one.

QUESTION 5

(a) The company shall not go for the outside suppliers and should make the carburettors

itself. The following calculation justifies this:

Cost per Unit (Cost of 15,000

units) MAKE

(Cost of 15,000

units) BUY

Outside purchase

price

£ 35 £ 525000

Direct Materials £ 14 £ 210000

Direct Labour £ 10 £ 150000

Variable

manufacturing

overhead

£ 3 £ 45000

Fixed

manufacturing

£ 6 £ 30000

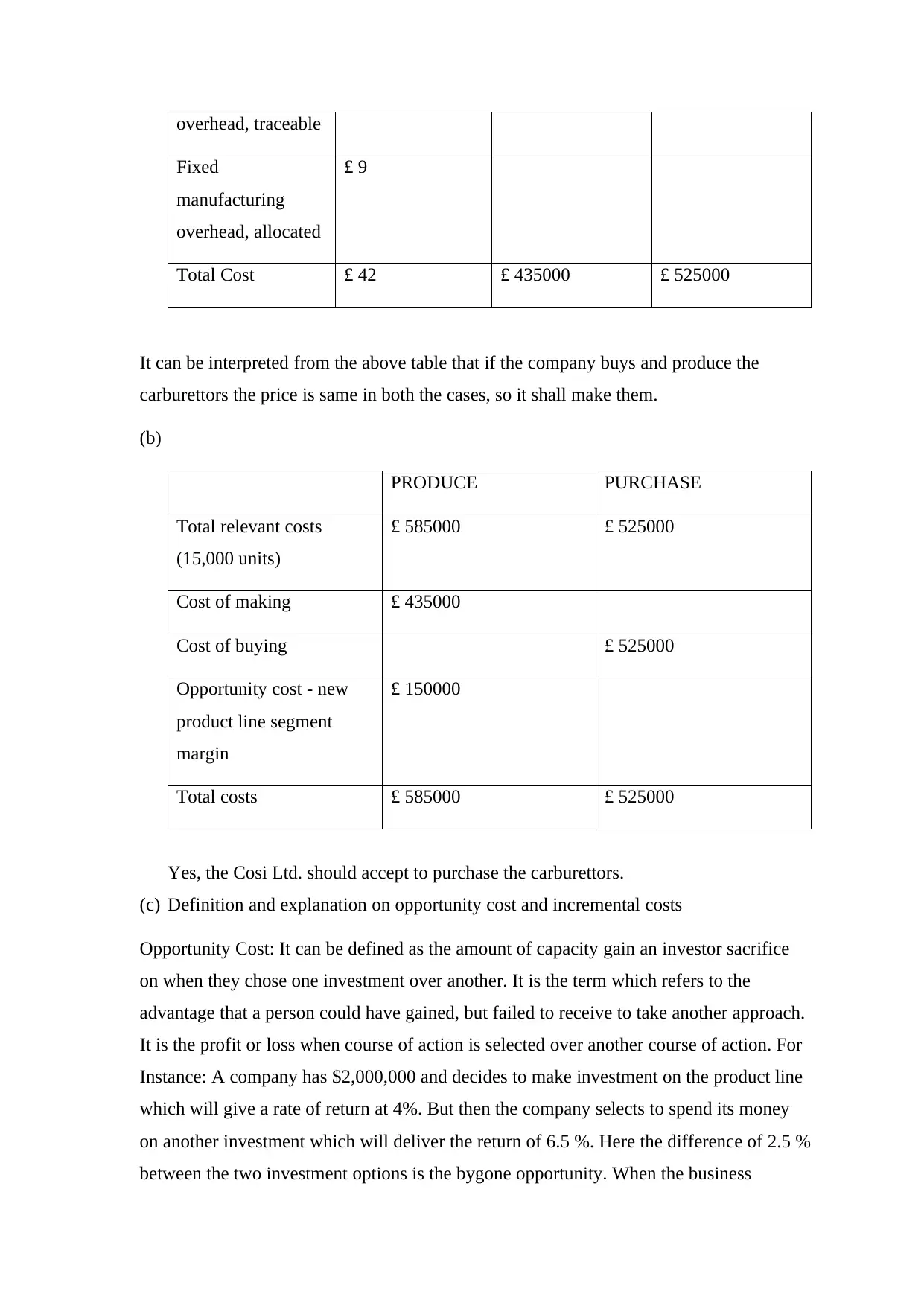

overhead, traceable

Fixed

manufacturing

overhead, allocated

£ 9

Total Cost £ 42 £ 435000 £ 525000

It can be interpreted from the above table that if the company buys and produce the

carburettors the price is same in both the cases, so it shall make them.

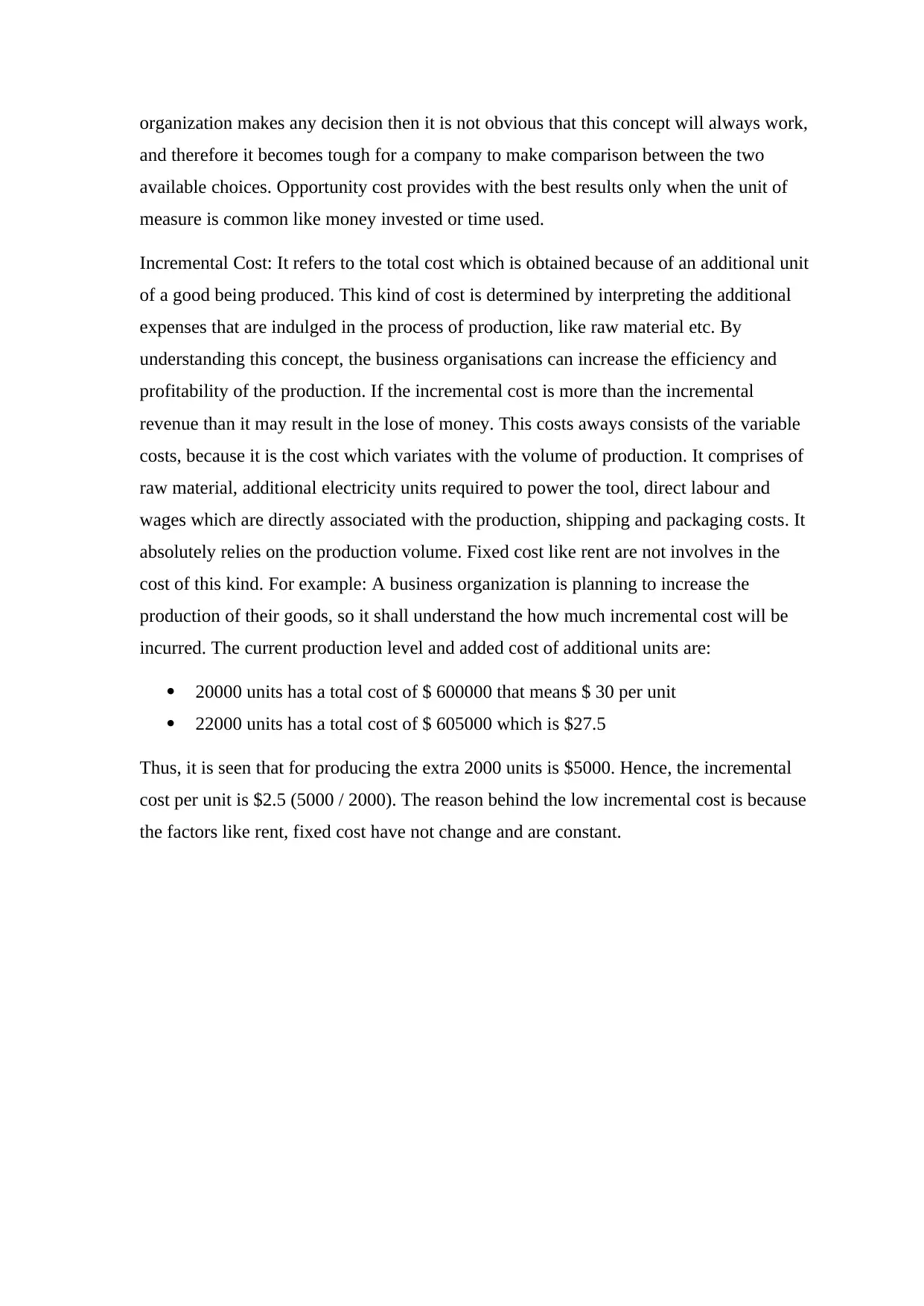

(b)

PRODUCE PURCHASE

Total relevant costs

(15,000 units)

£ 585000 £ 525000

Cost of making £ 435000

Cost of buying £ 525000

Opportunity cost - new

product line segment

margin

£ 150000

Total costs £ 585000 £ 525000

Yes, the Cosi Ltd. should accept to purchase the carburettors.

(c) Definition and explanation on opportunity cost and incremental costs

Opportunity Cost: It can be defined as the amount of capacity gain an investor sacrifice

on when they chose one investment over another. It is the term which refers to the

advantage that a person could have gained, but failed to receive to take another approach.

It is the profit or loss when course of action is selected over another course of action. For

Instance: A company has $2,000,000 and decides to make investment on the product line

which will give a rate of return at 4%. But then the company selects to spend its money

on another investment which will deliver the return of 6.5 %. Here the difference of 2.5 %

between the two investment options is the bygone opportunity. When the business

Fixed

manufacturing

overhead, allocated

£ 9

Total Cost £ 42 £ 435000 £ 525000

It can be interpreted from the above table that if the company buys and produce the

carburettors the price is same in both the cases, so it shall make them.

(b)

PRODUCE PURCHASE

Total relevant costs

(15,000 units)

£ 585000 £ 525000

Cost of making £ 435000

Cost of buying £ 525000

Opportunity cost - new

product line segment

margin

£ 150000

Total costs £ 585000 £ 525000

Yes, the Cosi Ltd. should accept to purchase the carburettors.

(c) Definition and explanation on opportunity cost and incremental costs

Opportunity Cost: It can be defined as the amount of capacity gain an investor sacrifice

on when they chose one investment over another. It is the term which refers to the

advantage that a person could have gained, but failed to receive to take another approach.

It is the profit or loss when course of action is selected over another course of action. For

Instance: A company has $2,000,000 and decides to make investment on the product line

which will give a rate of return at 4%. But then the company selects to spend its money

on another investment which will deliver the return of 6.5 %. Here the difference of 2.5 %

between the two investment options is the bygone opportunity. When the business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization makes any decision then it is not obvious that this concept will always work,

and therefore it becomes tough for a company to make comparison between the two

available choices. Opportunity cost provides with the best results only when the unit of

measure is common like money invested or time used.

Incremental Cost: It refers to the total cost which is obtained because of an additional unit

of a good being produced. This kind of cost is determined by interpreting the additional

expenses that are indulged in the process of production, like raw material etc. By

understanding this concept, the business organisations can increase the efficiency and

profitability of the production. If the incremental cost is more than the incremental

revenue than it may result in the lose of money. This costs aways consists of the variable

costs, because it is the cost which variates with the volume of production. It comprises of

raw material, additional electricity units required to power the tool, direct labour and

wages which are directly associated with the production, shipping and packaging costs. It

absolutely relies on the production volume. Fixed cost like rent are not involves in the

cost of this kind. For example: A business organization is planning to increase the

production of their goods, so it shall understand the how much incremental cost will be

incurred. The current production level and added cost of additional units are:

20000 units has a total cost of $ 600000 that means $ 30 per unit

22000 units has a total cost of $ 605000 which is $27.5

Thus, it is seen that for producing the extra 2000 units is $5000. Hence, the incremental

cost per unit is $2.5 (5000 / 2000). The reason behind the low incremental cost is because

the factors like rent, fixed cost have not change and are constant.

and therefore it becomes tough for a company to make comparison between the two

available choices. Opportunity cost provides with the best results only when the unit of

measure is common like money invested or time used.

Incremental Cost: It refers to the total cost which is obtained because of an additional unit

of a good being produced. This kind of cost is determined by interpreting the additional

expenses that are indulged in the process of production, like raw material etc. By

understanding this concept, the business organisations can increase the efficiency and

profitability of the production. If the incremental cost is more than the incremental

revenue than it may result in the lose of money. This costs aways consists of the variable

costs, because it is the cost which variates with the volume of production. It comprises of

raw material, additional electricity units required to power the tool, direct labour and

wages which are directly associated with the production, shipping and packaging costs. It

absolutely relies on the production volume. Fixed cost like rent are not involves in the

cost of this kind. For example: A business organization is planning to increase the

production of their goods, so it shall understand the how much incremental cost will be

incurred. The current production level and added cost of additional units are:

20000 units has a total cost of $ 600000 that means $ 30 per unit

22000 units has a total cost of $ 605000 which is $27.5

Thus, it is seen that for producing the extra 2000 units is $5000. Hence, the incremental

cost per unit is $2.5 (5000 / 2000). The reason behind the low incremental cost is because

the factors like rent, fixed cost have not change and are constant.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report it can be concluded that the management accounting provides

with the different mechanisms to make appropriate decisions. Labour efficiency and material

usage are affected by the disruptions in machinery, inefficient workforce etc are the causes

behind the variations. It also gives the clear representation that opportunity cost is the amount

sacrificed to choose one product over another and incremental analysis does not involve the

fixed cost factor.

From the above report it can be concluded that the management accounting provides

with the different mechanisms to make appropriate decisions. Labour efficiency and material

usage are affected by the disruptions in machinery, inefficient workforce etc are the causes

behind the variations. It also gives the clear representation that opportunity cost is the amount

sacrificed to choose one product over another and incremental analysis does not involve the

fixed cost factor.

References

Books & Journals

Gunarathne, A.N., Lee, K.H. and Hitigala Kaluarachchilage. p.K., 2021. Institutional pressures,

environmental management strategy, and organizational performance: The role of

environmental management accounting. Business Strategy and the

Environment. 30(2). pp.825-839.

Hiebl, M.R. and Richter, J.F., 2018. Response rates in management accounting survey

research. Journal of Management Accounting Research. 30(2). pp.59-79.

Samuel, S., 2018. A conceptual framework for teaching management accounting. Journal of

Accounting Education. 44. pp.25-34.

Johnstone, L., 2018. Theorising and modelling social control in environmental management

accounting research. Social and Environmental Accountability Journal. 38(1). pp.30-

48.

Mariina, E. and Tjahjadi, B., 2020. Strategic management accounting and university performance:

a critical review. Academy of Strategic Management Journal. 19(2). pp.1-5.

Jakobsen, M. and et.al., 2019. Educating management accountants as business partners: Pragmatic

constructivism as an alternative pedagogical paradigm for teaching management

accounting at master’s level. Qualitative Research in Accounting & Management.

Bogt, H.J.T. and Scapens, R.W., 2019. Institutions, situated rationality and agency in management

accounting: A research note extending the Burns and Scapens

framework. Accounting, Auditing & Accountability Journal. 32(6). pp.1801-1825.

Mohamed, R. and Jamil, C.Z.M., 2020. The influence of environmental management accounting

practices on environmental performance in small-medium manufacturing in

Malaysia. International Journal of Environment and Sustainable Development.

19(4). pp.378-392.

Books & Journals

Gunarathne, A.N., Lee, K.H. and Hitigala Kaluarachchilage. p.K., 2021. Institutional pressures,

environmental management strategy, and organizational performance: The role of

environmental management accounting. Business Strategy and the

Environment. 30(2). pp.825-839.

Hiebl, M.R. and Richter, J.F., 2018. Response rates in management accounting survey

research. Journal of Management Accounting Research. 30(2). pp.59-79.

Samuel, S., 2018. A conceptual framework for teaching management accounting. Journal of

Accounting Education. 44. pp.25-34.

Johnstone, L., 2018. Theorising and modelling social control in environmental management

accounting research. Social and Environmental Accountability Journal. 38(1). pp.30-

48.

Mariina, E. and Tjahjadi, B., 2020. Strategic management accounting and university performance:

a critical review. Academy of Strategic Management Journal. 19(2). pp.1-5.

Jakobsen, M. and et.al., 2019. Educating management accountants as business partners: Pragmatic

constructivism as an alternative pedagogical paradigm for teaching management

accounting at master’s level. Qualitative Research in Accounting & Management.

Bogt, H.J.T. and Scapens, R.W., 2019. Institutions, situated rationality and agency in management

accounting: A research note extending the Burns and Scapens

framework. Accounting, Auditing & Accountability Journal. 32(6). pp.1801-1825.

Mohamed, R. and Jamil, C.Z.M., 2020. The influence of environmental management accounting

practices on environmental performance in small-medium manufacturing in

Malaysia. International Journal of Environment and Sustainable Development.

19(4). pp.378-392.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.