Management Accounting: Cost of Goods Manufactured, Australian Dairy Products in China, Chinese vs Western Approaches, Sales and Purchase Budgets

VerifiedAdded on 2023/06/14

|15

|3683

|487

AI Summary

This article covers topics related to management accounting such as cost of goods manufactured, Australian dairy products in China, Chinese vs Western approaches, and sales and purchase budgets.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question No 1................................................................................................................2

Answer to Question No 2................................................................................................................3

Australian dairy products benefits and advantages in China.......................................................3

Difference between Chinese and the Western approaches to management accounting..............4

Concepts of guanxi and power distance......................................................................................4

Answer to Question No 3................................................................................................................5

Requirement a..............................................................................................................................5

Requirement b..............................................................................................................................7

Requirement c..............................................................................................................................7

Answer to Question No 4................................................................................................................8

Difference between fixed and variable cost.................................................................................8

Difference between product and period cost...............................................................................9

Answer to Question No 5 (Strategic Management Accounting)...................................................10

Requirement i.............................................................................................................................10

Requirement ii...........................................................................................................................11

Requirement iii..........................................................................................................................11

Answer to Question 5 (Ethics Case Study)....................................................................................12

Reference List................................................................................................................................13

MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question No 1................................................................................................................2

Answer to Question No 2................................................................................................................3

Australian dairy products benefits and advantages in China.......................................................3

Difference between Chinese and the Western approaches to management accounting..............4

Concepts of guanxi and power distance......................................................................................4

Answer to Question No 3................................................................................................................5

Requirement a..............................................................................................................................5

Requirement b..............................................................................................................................7

Requirement c..............................................................................................................................7

Answer to Question No 4................................................................................................................8

Difference between fixed and variable cost.................................................................................8

Difference between product and period cost...............................................................................9

Answer to Question No 5 (Strategic Management Accounting)...................................................10

Requirement i.............................................................................................................................10

Requirement ii...........................................................................................................................11

Requirement iii..........................................................................................................................11

Answer to Question 5 (Ethics Case Study)....................................................................................12

Reference List................................................................................................................................13

2

MANAGEMENT ACCOUNTING

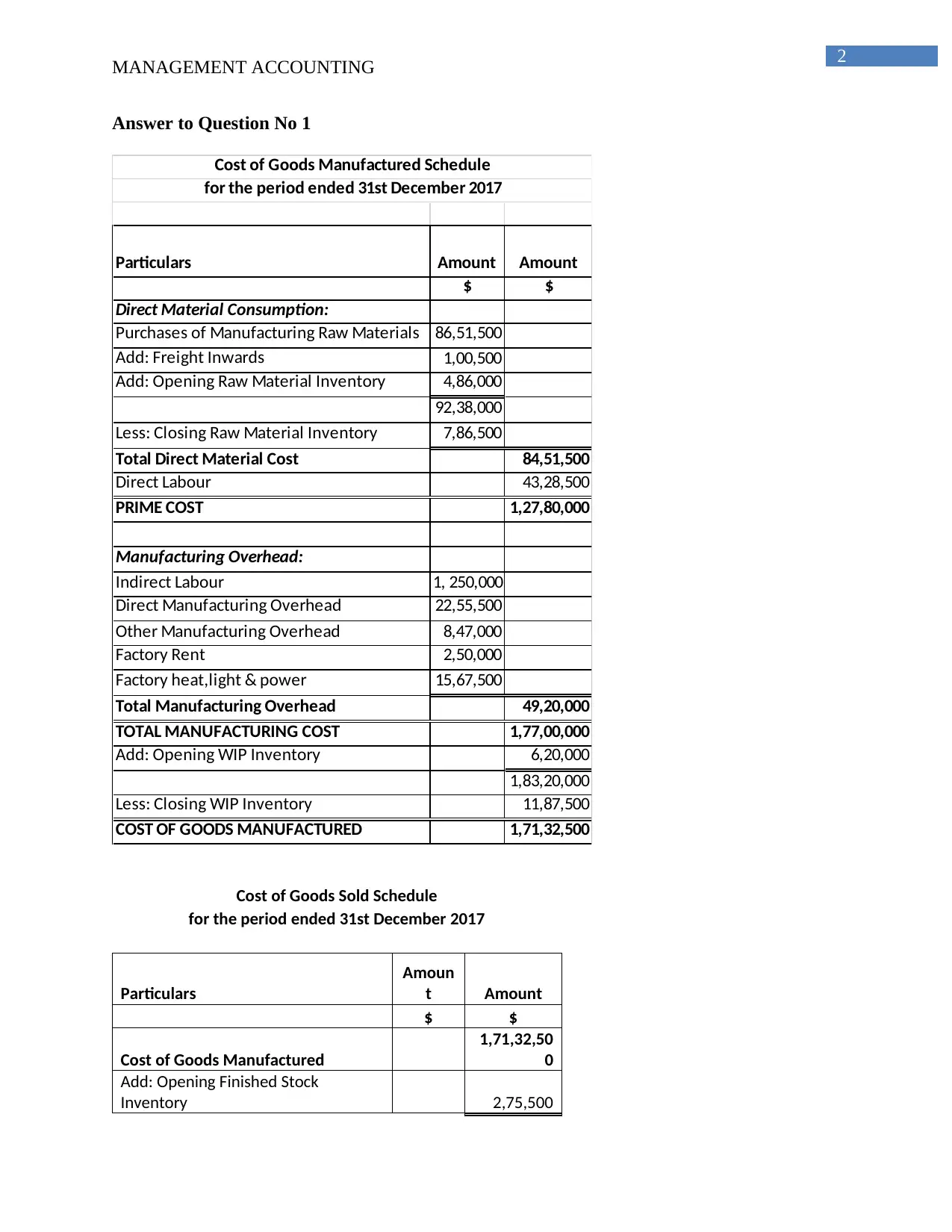

Answer to Question No 1

Particulars Amount Amount

$ $

Direct Material Consumption:

Purchases of Manufacturing Raw Materials 86,51,500

Add: Freight Inwards 1,00,500

Add: Opening Raw Material Inventory 4,86,000

92,38,000

Less: Closing Raw Material Inventory 7,86,500

Total Direct Material Cost 84,51,500

Direct Labour 43,28,500

PRIME COST 1,27,80,000

Manufacturing Overhead:

Indirect Labour 1, 250,000

Direct Manufacturing Overhead 22,55,500

Other Manufacturing Overhead 8,47,000

Factory Rent 2,50,000

Factory heat,light & power 15,67,500

Total Manufacturing Overhead 49,20,000

TOTAL MANUFACTURING COST 1,77,00,000

Add: Opening WIP Inventory 6,20,000

1,83,20,000

Less: Closing WIP Inventory 11,87,500

COST OF GOODS MANUFACTURED 1,71,32,500

Cost of Goods Manufactured Schedule

for the period ended 31st December 2017

Cost of Goods Sold Schedule

for the period ended 31st December 2017

Particulars

Amoun

t Amount

$ $

Cost of Goods Manufactured

1,71,32,50

0

Add: Opening Finished Stock

Inventory 2,75,500

MANAGEMENT ACCOUNTING

Answer to Question No 1

Particulars Amount Amount

$ $

Direct Material Consumption:

Purchases of Manufacturing Raw Materials 86,51,500

Add: Freight Inwards 1,00,500

Add: Opening Raw Material Inventory 4,86,000

92,38,000

Less: Closing Raw Material Inventory 7,86,500

Total Direct Material Cost 84,51,500

Direct Labour 43,28,500

PRIME COST 1,27,80,000

Manufacturing Overhead:

Indirect Labour 1, 250,000

Direct Manufacturing Overhead 22,55,500

Other Manufacturing Overhead 8,47,000

Factory Rent 2,50,000

Factory heat,light & power 15,67,500

Total Manufacturing Overhead 49,20,000

TOTAL MANUFACTURING COST 1,77,00,000

Add: Opening WIP Inventory 6,20,000

1,83,20,000

Less: Closing WIP Inventory 11,87,500

COST OF GOODS MANUFACTURED 1,71,32,500

Cost of Goods Manufactured Schedule

for the period ended 31st December 2017

Cost of Goods Sold Schedule

for the period ended 31st December 2017

Particulars

Amoun

t Amount

$ $

Cost of Goods Manufactured

1,71,32,50

0

Add: Opening Finished Stock

Inventory 2,75,500

3

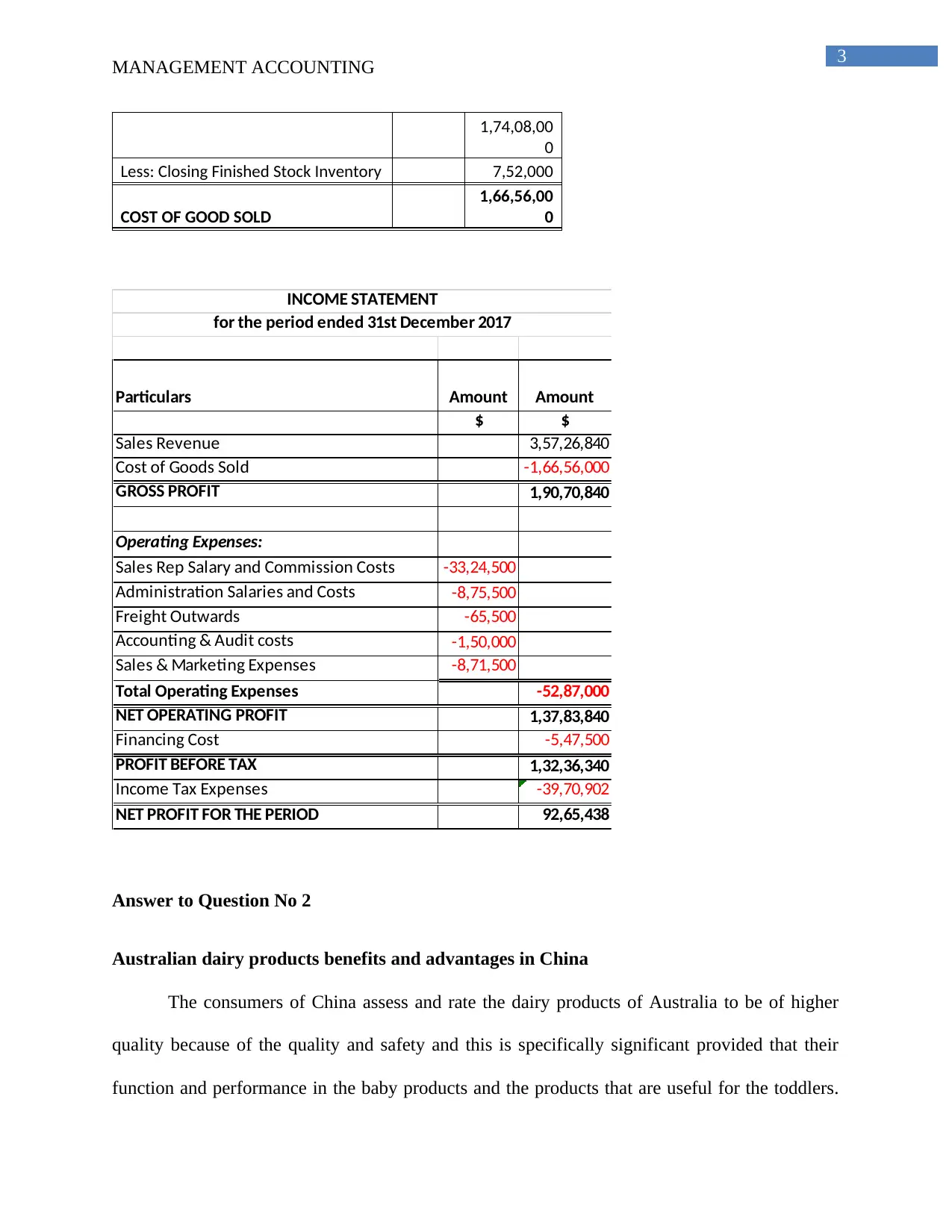

MANAGEMENT ACCOUNTING

1,74,08,00

0

Less: Closing Finished Stock Inventory 7,52,000

COST OF GOOD SOLD

1,66,56,00

0

Particulars Amount Amount

$ $

Sales Revenue 3,57,26,840

Cost of Goods Sold -1,66,56,000

GROSS PROFIT 1,90,70,840

Operating Expenses:

Sales Rep Salary and Commission Costs -33,24,500

Administration Salaries and Costs -8,75,500

Freight Outwards -65,500

Accounting & Audit costs -1,50,000

Sales & Marketing Expenses -8,71,500

Total Operating Expenses -52,87,000

NET OPERATING PROFIT 1,37,83,840

Financing Cost -5,47,500

PROFIT BEFORE TAX 1,32,36,340

Income Tax Expenses -39,70,902

NET PROFIT FOR THE PERIOD 92,65,438

INCOME STATEMENT

for the period ended 31st December 2017

Answer to Question No 2

Australian dairy products benefits and advantages in China

The consumers of China assess and rate the dairy products of Australia to be of higher

quality because of the quality and safety and this is specifically significant provided that their

function and performance in the baby products and the products that are useful for the toddlers.

MANAGEMENT ACCOUNTING

1,74,08,00

0

Less: Closing Finished Stock Inventory 7,52,000

COST OF GOOD SOLD

1,66,56,00

0

Particulars Amount Amount

$ $

Sales Revenue 3,57,26,840

Cost of Goods Sold -1,66,56,000

GROSS PROFIT 1,90,70,840

Operating Expenses:

Sales Rep Salary and Commission Costs -33,24,500

Administration Salaries and Costs -8,75,500

Freight Outwards -65,500

Accounting & Audit costs -1,50,000

Sales & Marketing Expenses -8,71,500

Total Operating Expenses -52,87,000

NET OPERATING PROFIT 1,37,83,840

Financing Cost -5,47,500

PROFIT BEFORE TAX 1,32,36,340

Income Tax Expenses -39,70,902

NET PROFIT FOR THE PERIOD 92,65,438

INCOME STATEMENT

for the period ended 31st December 2017

Answer to Question No 2

Australian dairy products benefits and advantages in China

The consumers of China assess and rate the dairy products of Australia to be of higher

quality because of the quality and safety and this is specifically significant provided that their

function and performance in the baby products and the products that are useful for the toddlers.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

MANAGEMENT ACCOUNTING

This would be helpful in developing and extending the profiles and the accessibility of the dairy

products of Australia. In accordance to the dairy products of Australia, China has become the

point of focus in order to increase their sales (Gray et al., 2016). The expansion and the

development for the desires and the demands for the dairy products in China is leading to an

extensive change in the society of China and create new opportunities for the products that are

ready for the consumers.

Difference between Chinese and the Western approaches to management accounting

In the countries that are located in the West, management accounting is even known as

the cost accounting of their ancestors that has been created after the early 19th century. The

establishment and the creation of management accounting are impacted by the management

science development factor (Deegan, 2017). The process of management accounting in the

western societies is the rational and real implication of the management operations that are

reliant on discipline. However, the implication of management accounting in China is limited by

the society that is existent in China. In order to enhancer and influence the extensive utilisation

of the process of management accounting, the factors related to the society and the culture is

even taken into consideration.

Concepts of guanxi and power distance

It is seen that power distance is the degree with respect to which information is granted

by the community that there is an existence of unequal power distribution. Every entity or an

individual has their authoritative place within the community and culture in case the culture has

extensive level of power distance (Russell et al., 2017). However, on the other hand, the entities

who are within the culture and have very low level of power distance prefers to stay powerful

and younger individuals and do not disclose their status, image and power. The fundamentals of

MANAGEMENT ACCOUNTING

This would be helpful in developing and extending the profiles and the accessibility of the dairy

products of Australia. In accordance to the dairy products of Australia, China has become the

point of focus in order to increase their sales (Gray et al., 2016). The expansion and the

development for the desires and the demands for the dairy products in China is leading to an

extensive change in the society of China and create new opportunities for the products that are

ready for the consumers.

Difference between Chinese and the Western approaches to management accounting

In the countries that are located in the West, management accounting is even known as

the cost accounting of their ancestors that has been created after the early 19th century. The

establishment and the creation of management accounting are impacted by the management

science development factor (Deegan, 2017). The process of management accounting in the

western societies is the rational and real implication of the management operations that are

reliant on discipline. However, the implication of management accounting in China is limited by

the society that is existent in China. In order to enhancer and influence the extensive utilisation

of the process of management accounting, the factors related to the society and the culture is

even taken into consideration.

Concepts of guanxi and power distance

It is seen that power distance is the degree with respect to which information is granted

by the community that there is an existence of unequal power distribution. Every entity or an

individual has their authoritative place within the community and culture in case the culture has

extensive level of power distance (Russell et al., 2017). However, on the other hand, the entities

who are within the culture and have very low level of power distance prefers to stay powerful

and younger individuals and do not disclose their status, image and power. The fundamentals of

5

MANAGEMENT ACCOUNTING

guanxi are looked upon to be another kind of cultural value in China that is a replication of the

Confucianism philosophy.

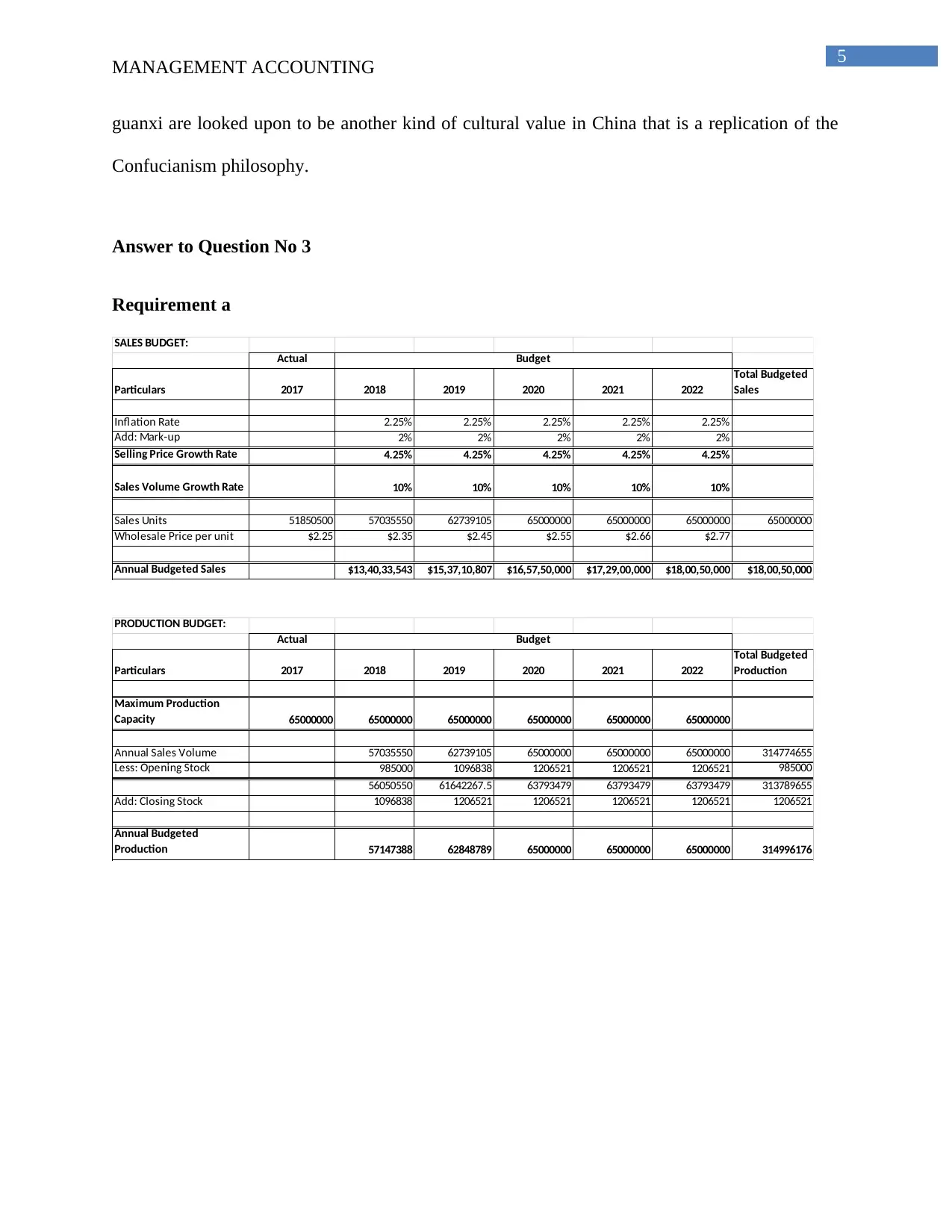

Answer to Question No 3

Requirement a

SALES BUDGET:

Actual

Particulars 2017 2018 2019 2020 2021 2022

Total Budgeted

Sales

Inflation Rate 2.25% 2.25% 2.25% 2.25% 2.25%

Add: Mark-up 2% 2% 2% 2% 2%

Selling Price Growth Rate 4.25% 4.25% 4.25% 4.25% 4.25%

Sales Volume Growth Rate 10% 10% 10% 10% 10%

Sales Units 51850500 57035550 62739105 65000000 65000000 65000000 65000000

Wholesale Price per unit $2.25 $2.35 $2.45 $2.55 $2.66 $2.77

Annual Budgeted Sales $13,40,33,543 $15,37,10,807 $16,57,50,000 $17,29,00,000 $18,00,50,000 $18,00,50,000

Budget

PRODUCTION BUDGET:

Actual

Particulars 2017 2018 2019 2020 2021 2022

Total Budgeted

Production

Maximum Production

Capacity 65000000 65000000 65000000 65000000 65000000 65000000

Annual Sales Volume 57035550 62739105 65000000 65000000 65000000 314774655

Less: Opening Stock 985000 1096838 1206521 1206521 1206521 985000

56050550 61642267.5 63793479 63793479 63793479 313789655

Add: Closing Stock 1096838 1206521 1206521 1206521 1206521 1206521

Annual Budgeted

Production 57147388 62848789 65000000 65000000 65000000 314996176

Budget

MANAGEMENT ACCOUNTING

guanxi are looked upon to be another kind of cultural value in China that is a replication of the

Confucianism philosophy.

Answer to Question No 3

Requirement a

SALES BUDGET:

Actual

Particulars 2017 2018 2019 2020 2021 2022

Total Budgeted

Sales

Inflation Rate 2.25% 2.25% 2.25% 2.25% 2.25%

Add: Mark-up 2% 2% 2% 2% 2%

Selling Price Growth Rate 4.25% 4.25% 4.25% 4.25% 4.25%

Sales Volume Growth Rate 10% 10% 10% 10% 10%

Sales Units 51850500 57035550 62739105 65000000 65000000 65000000 65000000

Wholesale Price per unit $2.25 $2.35 $2.45 $2.55 $2.66 $2.77

Annual Budgeted Sales $13,40,33,543 $15,37,10,807 $16,57,50,000 $17,29,00,000 $18,00,50,000 $18,00,50,000

Budget

PRODUCTION BUDGET:

Actual

Particulars 2017 2018 2019 2020 2021 2022

Total Budgeted

Production

Maximum Production

Capacity 65000000 65000000 65000000 65000000 65000000 65000000

Annual Sales Volume 57035550 62739105 65000000 65000000 65000000 314774655

Less: Opening Stock 985000 1096838 1206521 1206521 1206521 985000

56050550 61642267.5 63793479 63793479 63793479 313789655

Add: Closing Stock 1096838 1206521 1206521 1206521 1206521 1206521

Annual Budgeted

Production 57147388 62848789 65000000 65000000 65000000 314996176

Budget

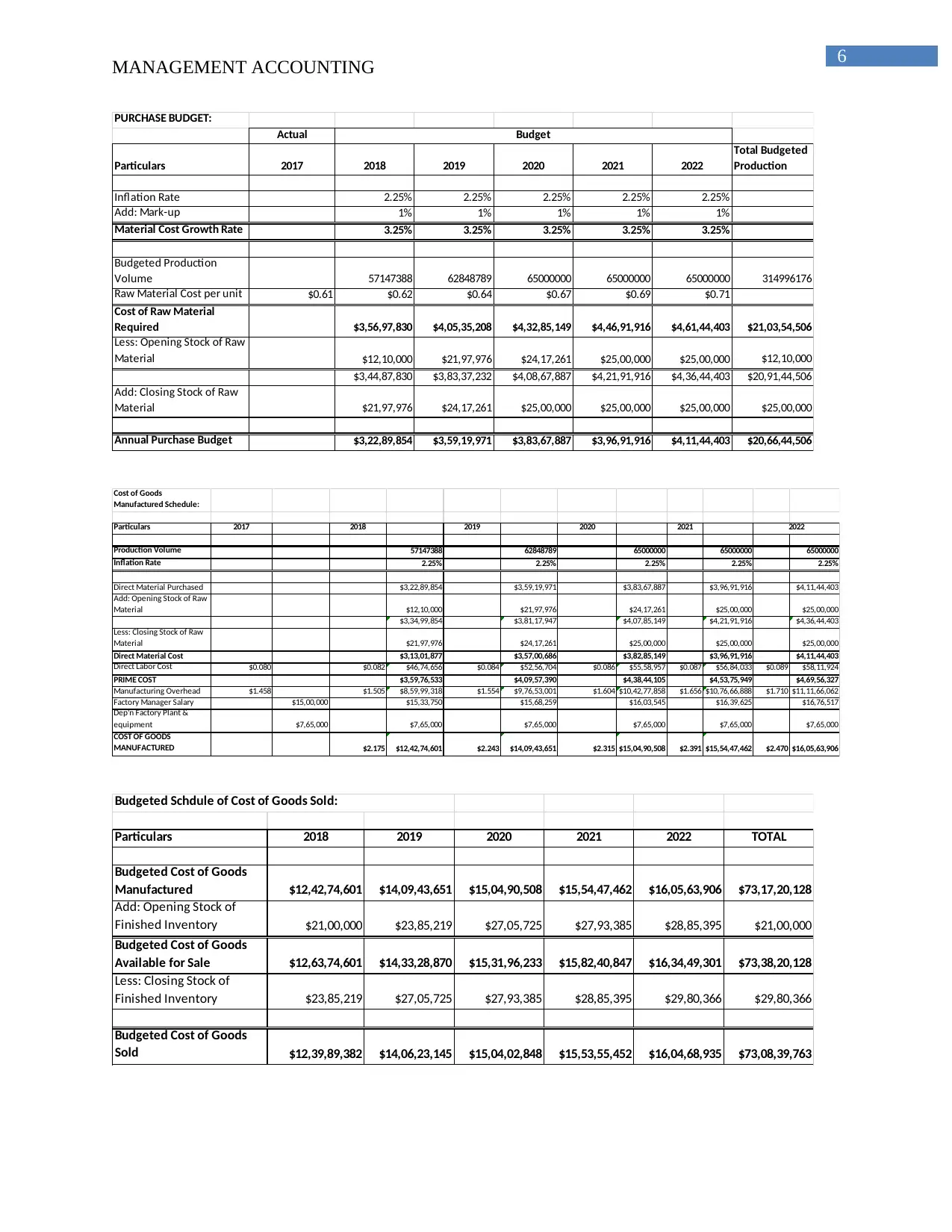

6

MANAGEMENT ACCOUNTING

PURCHASE BUDGET:

Actual

Particulars 2017 2018 2019 2020 2021 2022

Total Budgeted

Production

Inflation Rate 2.25% 2.25% 2.25% 2.25% 2.25%

Add: Mark-up 1% 1% 1% 1% 1%

Material Cost Growth Rate 3.25% 3.25% 3.25% 3.25% 3.25%

Budgeted Production

Volume 57147388 62848789 65000000 65000000 65000000 314996176

Raw Material Cost per unit $0.61 $0.62 $0.64 $0.67 $0.69 $0.71

Cost of Raw Material

Required $3,56,97,830 $4,05,35,208 $4,32,85,149 $4,46,91,916 $4,61,44,403 $21,03,54,506

Less: Opening Stock of Raw

Material $12,10,000 $21,97,976 $24,17,261 $25,00,000 $25,00,000 $12,10,000

$3,44,87,830 $3,83,37,232 $4,08,67,887 $4,21,91,916 $4,36,44,403 $20,91,44,506

Add: Closing Stock of Raw

Material $21,97,976 $24,17,261 $25,00,000 $25,00,000 $25,00,000 $25,00,000

Annual Purchase Budget $3,22,89,854 $3,59,19,971 $3,83,67,887 $3,96,91,916 $4,11,44,403 $20,66,44,506

Budget

Cost of Goods

Manufactured Schedule:

Particulars 2017 2018 2019 2020 2021

Production Volume 57147388 62848789 65000000 65000000 65000000

Inflation Rate 2.25% 2.25% 2.25% 2.25% 2.25%

Direct Material Purchased $3,22,89,854 $3,59,19,971 $3,83,67,887 $3,96,91,916 $4,11,44,403

Add: Opening Stock of Raw

Material $12,10,000 $21,97,976 $24,17,261 $25,00,000 $25,00,000

$3,34,99,854 $3,81,17,947 $4,07,85,149 $4,21,91,916 $4,36,44,403

Less: Closing Stock of Raw

Material $21,97,976 $24,17,261 $25,00,000 $25,00,000 $25,00,000

Direct Material Cost $3,13,01,877 $3,57,00,686 $3,82,85,149 $3,96,91,916 $4,11,44,403

Direct Labor Cost $0.080 $0.082 $46,74,656 $0.084 $52,56,704 $0.086 $55,58,957 $0.087 $56,84,033 $0.089 $58,11,924

PRIME COST $3,59,76,533 $4,09,57,390 $4,38,44,105 $4,53,75,949 $4,69,56,327

Manufacturing Overhead $1.458 $1.505 $8,59,99,318 $1.554 $9,76,53,001 $1.604 $10,42,77,858 $1.656 $10,76,66,888 $1.710 $11,11,66,062

Factory Manager Salary $15,00,000 $15,33,750 $15,68,259 $16,03,545 $16,39,625 $16,76,517

Dep'n Factory Plant &

equipment $7,65,000 $7,65,000 $7,65,000 $7,65,000 $7,65,000 $7,65,000

COST OF GOODS

MANUFACTURED $2.175 $12,42,74,601 $2.243 $14,09,43,651 $2.315 $15,04,90,508 $2.391 $15,54,47,462 $2.470 $16,05,63,906

2022

Particulars 2018 2019 2020 2021 2022 TOTAL

Budgeted Cost of Goods

Manufactured $12,42,74,601 $14,09,43,651 $15,04,90,508 $15,54,47,462 $16,05,63,906 $73,17,20,128

Add: Opening Stock of

Finished Inventory $21,00,000 $23,85,219 $27,05,725 $27,93,385 $28,85,395 $21,00,000

Budgeted Cost of Goods

Available for Sale $12,63,74,601 $14,33,28,870 $15,31,96,233 $15,82,40,847 $16,34,49,301 $73,38,20,128

Less: Closing Stock of

Finished Inventory $23,85,219 $27,05,725 $27,93,385 $28,85,395 $29,80,366 $29,80,366

Budgeted Cost of Goods

Sold $12,39,89,382 $14,06,23,145 $15,04,02,848 $15,53,55,452 $16,04,68,935 $73,08,39,763

Budgeted Schdule of Cost of Goods Sold:

MANAGEMENT ACCOUNTING

PURCHASE BUDGET:

Actual

Particulars 2017 2018 2019 2020 2021 2022

Total Budgeted

Production

Inflation Rate 2.25% 2.25% 2.25% 2.25% 2.25%

Add: Mark-up 1% 1% 1% 1% 1%

Material Cost Growth Rate 3.25% 3.25% 3.25% 3.25% 3.25%

Budgeted Production

Volume 57147388 62848789 65000000 65000000 65000000 314996176

Raw Material Cost per unit $0.61 $0.62 $0.64 $0.67 $0.69 $0.71

Cost of Raw Material

Required $3,56,97,830 $4,05,35,208 $4,32,85,149 $4,46,91,916 $4,61,44,403 $21,03,54,506

Less: Opening Stock of Raw

Material $12,10,000 $21,97,976 $24,17,261 $25,00,000 $25,00,000 $12,10,000

$3,44,87,830 $3,83,37,232 $4,08,67,887 $4,21,91,916 $4,36,44,403 $20,91,44,506

Add: Closing Stock of Raw

Material $21,97,976 $24,17,261 $25,00,000 $25,00,000 $25,00,000 $25,00,000

Annual Purchase Budget $3,22,89,854 $3,59,19,971 $3,83,67,887 $3,96,91,916 $4,11,44,403 $20,66,44,506

Budget

Cost of Goods

Manufactured Schedule:

Particulars 2017 2018 2019 2020 2021

Production Volume 57147388 62848789 65000000 65000000 65000000

Inflation Rate 2.25% 2.25% 2.25% 2.25% 2.25%

Direct Material Purchased $3,22,89,854 $3,59,19,971 $3,83,67,887 $3,96,91,916 $4,11,44,403

Add: Opening Stock of Raw

Material $12,10,000 $21,97,976 $24,17,261 $25,00,000 $25,00,000

$3,34,99,854 $3,81,17,947 $4,07,85,149 $4,21,91,916 $4,36,44,403

Less: Closing Stock of Raw

Material $21,97,976 $24,17,261 $25,00,000 $25,00,000 $25,00,000

Direct Material Cost $3,13,01,877 $3,57,00,686 $3,82,85,149 $3,96,91,916 $4,11,44,403

Direct Labor Cost $0.080 $0.082 $46,74,656 $0.084 $52,56,704 $0.086 $55,58,957 $0.087 $56,84,033 $0.089 $58,11,924

PRIME COST $3,59,76,533 $4,09,57,390 $4,38,44,105 $4,53,75,949 $4,69,56,327

Manufacturing Overhead $1.458 $1.505 $8,59,99,318 $1.554 $9,76,53,001 $1.604 $10,42,77,858 $1.656 $10,76,66,888 $1.710 $11,11,66,062

Factory Manager Salary $15,00,000 $15,33,750 $15,68,259 $16,03,545 $16,39,625 $16,76,517

Dep'n Factory Plant &

equipment $7,65,000 $7,65,000 $7,65,000 $7,65,000 $7,65,000 $7,65,000

COST OF GOODS

MANUFACTURED $2.175 $12,42,74,601 $2.243 $14,09,43,651 $2.315 $15,04,90,508 $2.391 $15,54,47,462 $2.470 $16,05,63,906

2022

Particulars 2018 2019 2020 2021 2022 TOTAL

Budgeted Cost of Goods

Manufactured $12,42,74,601 $14,09,43,651 $15,04,90,508 $15,54,47,462 $16,05,63,906 $73,17,20,128

Add: Opening Stock of

Finished Inventory $21,00,000 $23,85,219 $27,05,725 $27,93,385 $28,85,395 $21,00,000

Budgeted Cost of Goods

Available for Sale $12,63,74,601 $14,33,28,870 $15,31,96,233 $15,82,40,847 $16,34,49,301 $73,38,20,128

Less: Closing Stock of

Finished Inventory $23,85,219 $27,05,725 $27,93,385 $28,85,395 $29,80,366 $29,80,366

Budgeted Cost of Goods

Sold $12,39,89,382 $14,06,23,145 $15,04,02,848 $15,53,55,452 $16,04,68,935 $73,08,39,763

Budgeted Schdule of Cost of Goods Sold:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

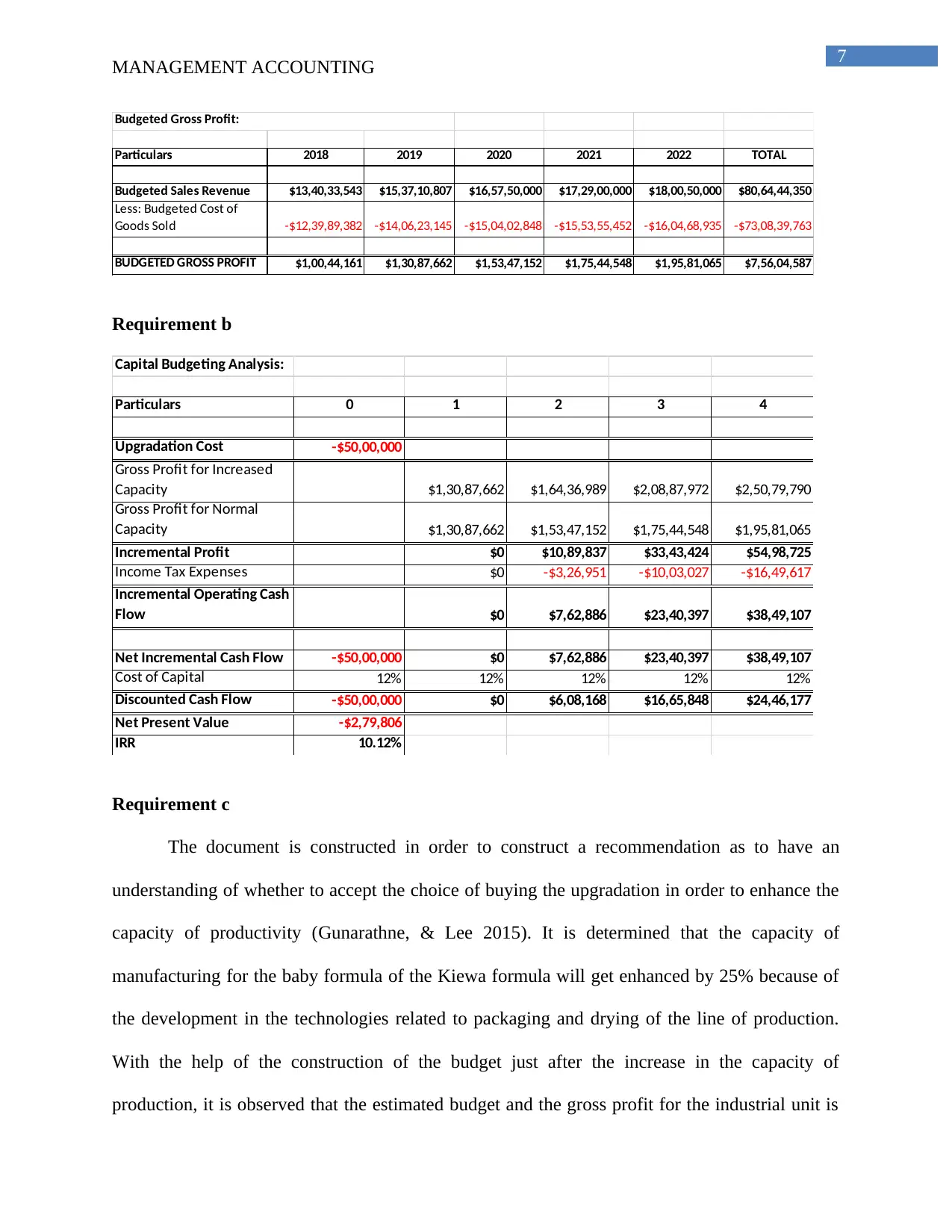

7

MANAGEMENT ACCOUNTING

Particulars 2018 2019 2020 2021 2022 TOTAL

Budgeted Sales Revenue $13,40,33,543 $15,37,10,807 $16,57,50,000 $17,29,00,000 $18,00,50,000 $80,64,44,350

Less: Budgeted Cost of

Goods Sold -$12,39,89,382 -$14,06,23,145 -$15,04,02,848 -$15,53,55,452 -$16,04,68,935 -$73,08,39,763

BUDGETED GROSS PROFIT $1,00,44,161 $1,30,87,662 $1,53,47,152 $1,75,44,548 $1,95,81,065 $7,56,04,587

Budgeted Gross Profit:

Requirement b

Capital Budgeting Analysis:

Particulars 0 1 2 3 4

Upgradation Cost -$50,00,000

Gross Profit for Increased

Capacity $1,30,87,662 $1,64,36,989 $2,08,87,972 $2,50,79,790

Gross Profit for Normal

Capacity $1,30,87,662 $1,53,47,152 $1,75,44,548 $1,95,81,065

Incremental Profit $0 $10,89,837 $33,43,424 $54,98,725

Income Tax Expenses $0 -$3,26,951 -$10,03,027 -$16,49,617

Incremental Operating Cash

Flow $0 $7,62,886 $23,40,397 $38,49,107

Net Incremental Cash Flow -$50,00,000 $0 $7,62,886 $23,40,397 $38,49,107

Cost of Capital 12% 12% 12% 12% 12%

Discounted Cash Flow -$50,00,000 $0 $6,08,168 $16,65,848 $24,46,177

Net Present Value -$2,79,806

IRR 10.12%

Requirement c

The document is constructed in order to construct a recommendation as to have an

understanding of whether to accept the choice of buying the upgradation in order to enhance the

capacity of productivity (Gunarathne, & Lee 2015). It is determined that the capacity of

manufacturing for the baby formula of the Kiewa formula will get enhanced by 25% because of

the development in the technologies related to packaging and drying of the line of production.

With the help of the construction of the budget just after the increase in the capacity of

production, it is observed that the estimated budget and the gross profit for the industrial unit is

MANAGEMENT ACCOUNTING

Particulars 2018 2019 2020 2021 2022 TOTAL

Budgeted Sales Revenue $13,40,33,543 $15,37,10,807 $16,57,50,000 $17,29,00,000 $18,00,50,000 $80,64,44,350

Less: Budgeted Cost of

Goods Sold -$12,39,89,382 -$14,06,23,145 -$15,04,02,848 -$15,53,55,452 -$16,04,68,935 -$73,08,39,763

BUDGETED GROSS PROFIT $1,00,44,161 $1,30,87,662 $1,53,47,152 $1,75,44,548 $1,95,81,065 $7,56,04,587

Budgeted Gross Profit:

Requirement b

Capital Budgeting Analysis:

Particulars 0 1 2 3 4

Upgradation Cost -$50,00,000

Gross Profit for Increased

Capacity $1,30,87,662 $1,64,36,989 $2,08,87,972 $2,50,79,790

Gross Profit for Normal

Capacity $1,30,87,662 $1,53,47,152 $1,75,44,548 $1,95,81,065

Incremental Profit $0 $10,89,837 $33,43,424 $54,98,725

Income Tax Expenses $0 -$3,26,951 -$10,03,027 -$16,49,617

Incremental Operating Cash

Flow $0 $7,62,886 $23,40,397 $38,49,107

Net Incremental Cash Flow -$50,00,000 $0 $7,62,886 $23,40,397 $38,49,107

Cost of Capital 12% 12% 12% 12% 12%

Discounted Cash Flow -$50,00,000 $0 $6,08,168 $16,65,848 $24,46,177

Net Present Value -$2,79,806

IRR 10.12%

Requirement c

The document is constructed in order to construct a recommendation as to have an

understanding of whether to accept the choice of buying the upgradation in order to enhance the

capacity of productivity (Gunarathne, & Lee 2015). It is determined that the capacity of

manufacturing for the baby formula of the Kiewa formula will get enhanced by 25% because of

the development in the technologies related to packaging and drying of the line of production.

With the help of the construction of the budget just after the increase in the capacity of

production, it is observed that the estimated budget and the gross profit for the industrial unit is

8

MANAGEMENT ACCOUNTING

rising. On the other hand, when implicating the process and the technique of the assessment of

capital budgeting, it is observed that the net present value of the project is -$279806 and thereby

can be said that the value is negative. Hence, the present value of the cash flow of the future is

negative and thereby upgradation and innovation in the drying line of production and packaging

should not be initiated. Additionally, the required return rate or the cost of capital in order to

upgrade the line of production and packaging is 12%. The overall internal rate of return value

has been found to be 10.12%. It is viewed that the internal rate of return is significantly more

than the cost of capital and thereby explaining that the innovation and the development of the

line of product should be initiated (Gray et al., 2017). It is even essential to look at the precise

and the authentic strategic financial risk, which is related to the concerned project. It is viewed

that the real budgeted gross profit is rising each and every year and it is practicable to initiate the

business without enhancing limitations related to production. However, it is necessary to look

into the overall strategic risks and the benefits when constructing a decision in order to go ahead

with a project. When an innovative practice or process is related, one of the distinct issues is the

risk related to operations (Roberts, & Wallace 2015). The concerned project has essential level of

implications of cost if it has an effect on the central activities of the business or in the product

quality.

Answer to Question No 4

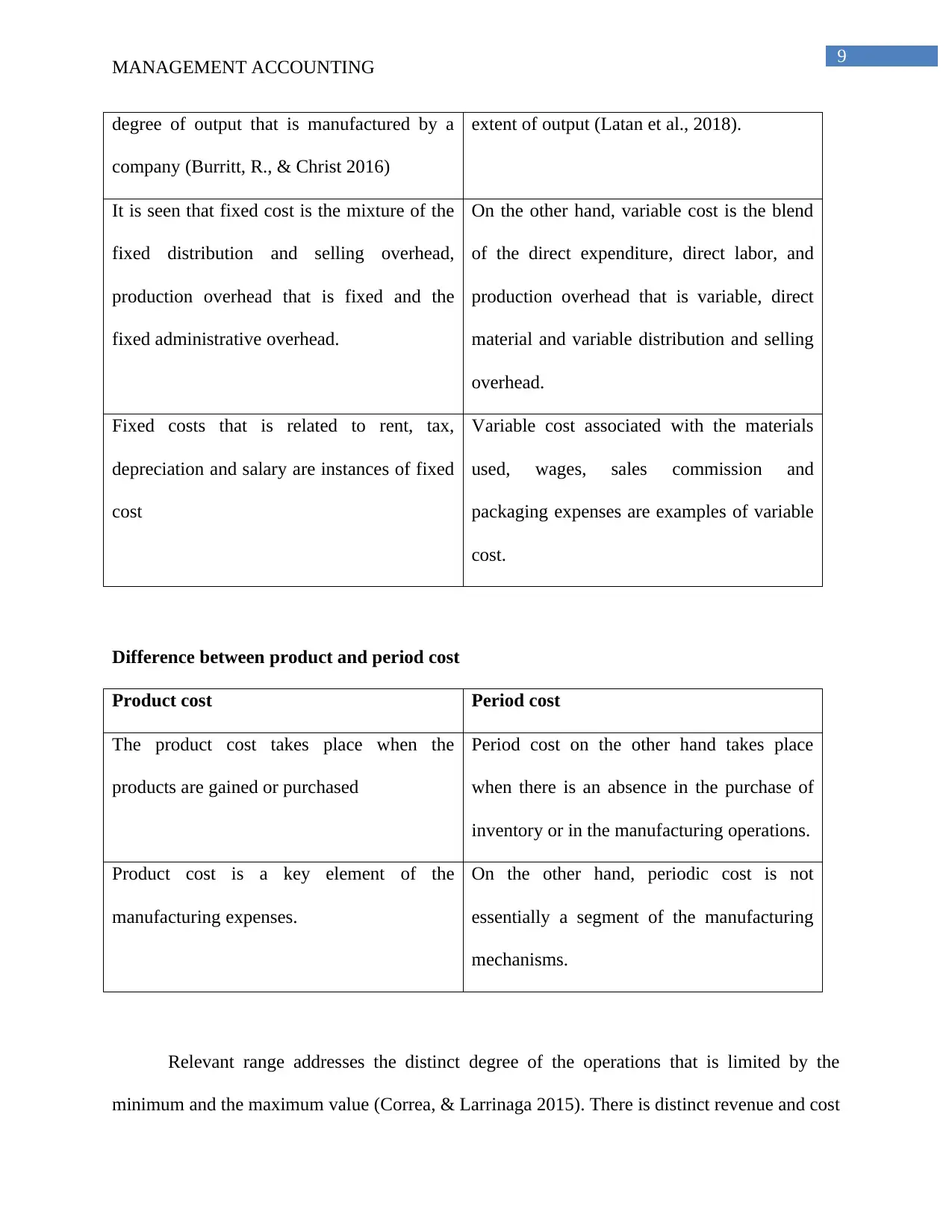

Difference between fixed and variable cost

Fixed cost Variable cost

Fixed cost refers to the cost or the expenses

that is always fixed without considering

On the other hand, the variable cost is the

expense that is variable and will alter the

MANAGEMENT ACCOUNTING

rising. On the other hand, when implicating the process and the technique of the assessment of

capital budgeting, it is observed that the net present value of the project is -$279806 and thereby

can be said that the value is negative. Hence, the present value of the cash flow of the future is

negative and thereby upgradation and innovation in the drying line of production and packaging

should not be initiated. Additionally, the required return rate or the cost of capital in order to

upgrade the line of production and packaging is 12%. The overall internal rate of return value

has been found to be 10.12%. It is viewed that the internal rate of return is significantly more

than the cost of capital and thereby explaining that the innovation and the development of the

line of product should be initiated (Gray et al., 2017). It is even essential to look at the precise

and the authentic strategic financial risk, which is related to the concerned project. It is viewed

that the real budgeted gross profit is rising each and every year and it is practicable to initiate the

business without enhancing limitations related to production. However, it is necessary to look

into the overall strategic risks and the benefits when constructing a decision in order to go ahead

with a project. When an innovative practice or process is related, one of the distinct issues is the

risk related to operations (Roberts, & Wallace 2015). The concerned project has essential level of

implications of cost if it has an effect on the central activities of the business or in the product

quality.

Answer to Question No 4

Difference between fixed and variable cost

Fixed cost Variable cost

Fixed cost refers to the cost or the expenses

that is always fixed without considering

On the other hand, the variable cost is the

expense that is variable and will alter the

9

MANAGEMENT ACCOUNTING

degree of output that is manufactured by a

company (Burritt, R., & Christ 2016)

extent of output (Latan et al., 2018).

It is seen that fixed cost is the mixture of the

fixed distribution and selling overhead,

production overhead that is fixed and the

fixed administrative overhead.

On the other hand, variable cost is the blend

of the direct expenditure, direct labor, and

production overhead that is variable, direct

material and variable distribution and selling

overhead.

Fixed costs that is related to rent, tax,

depreciation and salary are instances of fixed

cost

Variable cost associated with the materials

used, wages, sales commission and

packaging expenses are examples of variable

cost.

Difference between product and period cost

Product cost Period cost

The product cost takes place when the

products are gained or purchased

Period cost on the other hand takes place

when there is an absence in the purchase of

inventory or in the manufacturing operations.

Product cost is a key element of the

manufacturing expenses.

On the other hand, periodic cost is not

essentially a segment of the manufacturing

mechanisms.

Relevant range addresses the distinct degree of the operations that is limited by the

minimum and the maximum value (Correa, & Larrinaga 2015). There is distinct revenue and cost

MANAGEMENT ACCOUNTING

degree of output that is manufactured by a

company (Burritt, R., & Christ 2016)

extent of output (Latan et al., 2018).

It is seen that fixed cost is the mixture of the

fixed distribution and selling overhead,

production overhead that is fixed and the

fixed administrative overhead.

On the other hand, variable cost is the blend

of the direct expenditure, direct labor, and

production overhead that is variable, direct

material and variable distribution and selling

overhead.

Fixed costs that is related to rent, tax,

depreciation and salary are instances of fixed

cost

Variable cost associated with the materials

used, wages, sales commission and

packaging expenses are examples of variable

cost.

Difference between product and period cost

Product cost Period cost

The product cost takes place when the

products are gained or purchased

Period cost on the other hand takes place

when there is an absence in the purchase of

inventory or in the manufacturing operations.

Product cost is a key element of the

manufacturing expenses.

On the other hand, periodic cost is not

essentially a segment of the manufacturing

mechanisms.

Relevant range addresses the distinct degree of the operations that is limited by the

minimum and the maximum value (Correa, & Larrinaga 2015). There is distinct revenue and cost

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

MANAGEMENT ACCOUNTING

extent that is likely to take place within the specified boundaries is shown by the relevant range.

The revenues and the costs are looked upon to differ from the anticipated value that is outside the

relevant range. Relevant range is looked upon as the essential qualifier when assigning the

budgeted fixed expenses.

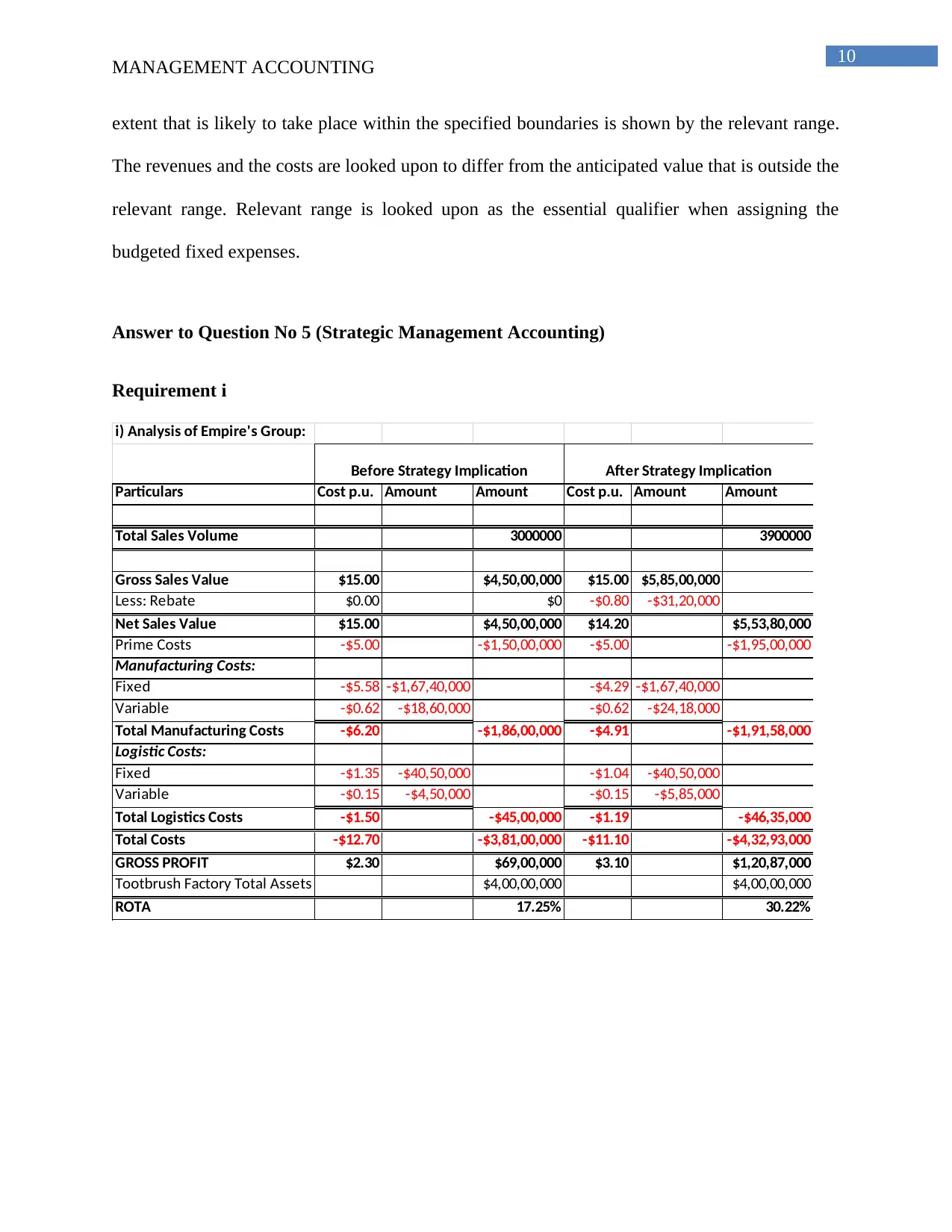

Answer to Question No 5 (Strategic Management Accounting)

Requirement i

i) Analysis of Empire's Group:

Particulars Cost p.u. Amount Amount Cost p.u. Amount Amount

Total Sales Volume 3000000 3900000

Gross Sales Value $15.00 $4,50,00,000 $15.00 $5,85,00,000

Less: Rebate $0.00 $0 -$0.80 -$31,20,000

Net Sales Value $15.00 $4,50,00,000 $14.20 $5,53,80,000

Prime Costs -$5.00 -$1,50,00,000 -$5.00 -$1,95,00,000

Manufacturing Costs:

Fixed -$5.58 -$1,67,40,000 -$4.29 -$1,67,40,000

Variable -$0.62 -$18,60,000 -$0.62 -$24,18,000

Total Manufacturing Costs -$6.20 -$1,86,00,000 -$4.91 -$1,91,58,000

Logistic Costs:

Fixed -$1.35 -$40,50,000 -$1.04 -$40,50,000

Variable -$0.15 -$4,50,000 -$0.15 -$5,85,000

Total Logistics Costs -$1.50 -$45,00,000 -$1.19 -$46,35,000

Total Costs -$12.70 -$3,81,00,000 -$11.10 -$4,32,93,000

GROSS PROFIT $2.30 $69,00,000 $3.10 $1,20,87,000

Tootbrush Factory Total Assets $4,00,00,000 $4,00,00,000

ROTA 17.25% 30.22%

Before Strategy Implication After Strategy Implication

MANAGEMENT ACCOUNTING

extent that is likely to take place within the specified boundaries is shown by the relevant range.

The revenues and the costs are looked upon to differ from the anticipated value that is outside the

relevant range. Relevant range is looked upon as the essential qualifier when assigning the

budgeted fixed expenses.

Answer to Question No 5 (Strategic Management Accounting)

Requirement i

i) Analysis of Empire's Group:

Particulars Cost p.u. Amount Amount Cost p.u. Amount Amount

Total Sales Volume 3000000 3900000

Gross Sales Value $15.00 $4,50,00,000 $15.00 $5,85,00,000

Less: Rebate $0.00 $0 -$0.80 -$31,20,000

Net Sales Value $15.00 $4,50,00,000 $14.20 $5,53,80,000

Prime Costs -$5.00 -$1,50,00,000 -$5.00 -$1,95,00,000

Manufacturing Costs:

Fixed -$5.58 -$1,67,40,000 -$4.29 -$1,67,40,000

Variable -$0.62 -$18,60,000 -$0.62 -$24,18,000

Total Manufacturing Costs -$6.20 -$1,86,00,000 -$4.91 -$1,91,58,000

Logistic Costs:

Fixed -$1.35 -$40,50,000 -$1.04 -$40,50,000

Variable -$0.15 -$4,50,000 -$0.15 -$5,85,000

Total Logistics Costs -$1.50 -$45,00,000 -$1.19 -$46,35,000

Total Costs -$12.70 -$3,81,00,000 -$11.10 -$4,32,93,000

GROSS PROFIT $2.30 $69,00,000 $3.10 $1,20,87,000

Tootbrush Factory Total Assets $4,00,00,000 $4,00,00,000

ROTA 17.25% 30.22%

Before Strategy Implication After Strategy Implication

11

MANAGEMENT ACCOUNTING

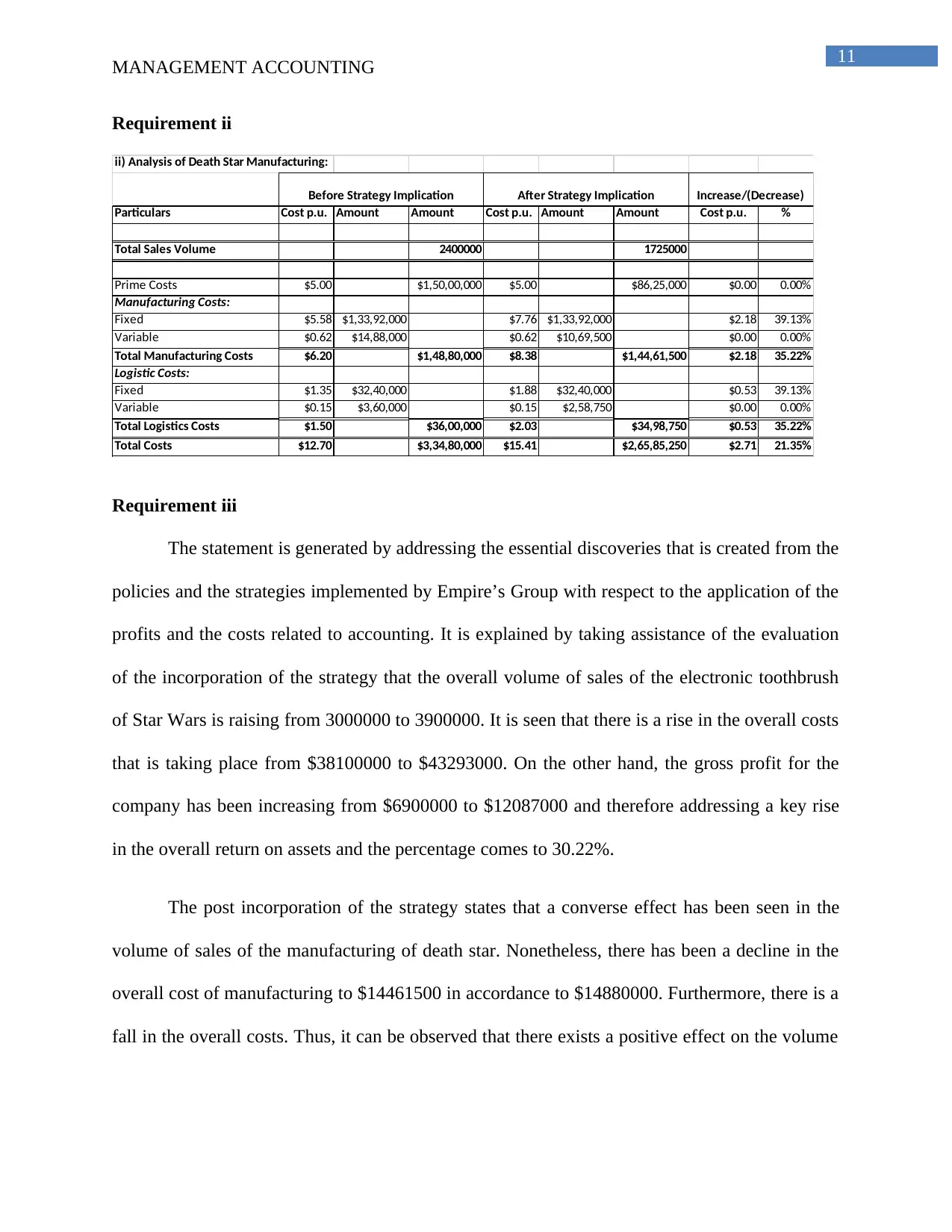

Requirement ii

ii) Analysis of Death Star Manufacturing:

Particulars Cost p.u. Amount Amount Cost p.u. Amount Amount Cost p.u. %

Total Sales Volume 2400000 1725000

Prime Costs $5.00 $1,50,00,000 $5.00 $86,25,000 $0.00 0.00%

Manufacturing Costs:

Fixed $5.58 $1,33,92,000 $7.76 $1,33,92,000 $2.18 39.13%

Variable $0.62 $14,88,000 $0.62 $10,69,500 $0.00 0.00%

Total Manufacturing Costs $6.20 $1,48,80,000 $8.38 $1,44,61,500 $2.18 35.22%

Logistic Costs:

Fixed $1.35 $32,40,000 $1.88 $32,40,000 $0.53 39.13%

Variable $0.15 $3,60,000 $0.15 $2,58,750 $0.00 0.00%

Total Logistics Costs $1.50 $36,00,000 $2.03 $34,98,750 $0.53 35.22%

Total Costs $12.70 $3,34,80,000 $15.41 $2,65,85,250 $2.71 21.35%

Before Strategy Implication After Strategy Implication Increase/(Decrease)

Requirement iii

The statement is generated by addressing the essential discoveries that is created from the

policies and the strategies implemented by Empire’s Group with respect to the application of the

profits and the costs related to accounting. It is explained by taking assistance of the evaluation

of the incorporation of the strategy that the overall volume of sales of the electronic toothbrush

of Star Wars is raising from 3000000 to 3900000. It is seen that there is a rise in the overall costs

that is taking place from $38100000 to $43293000. On the other hand, the gross profit for the

company has been increasing from $6900000 to $12087000 and therefore addressing a key rise

in the overall return on assets and the percentage comes to 30.22%.

The post incorporation of the strategy states that a converse effect has been seen in the

volume of sales of the manufacturing of death star. Nonetheless, there has been a decline in the

overall cost of manufacturing to $14461500 in accordance to $14880000. Furthermore, there is a

fall in the overall costs. Thus, it can be observed that there exists a positive effect on the volume

MANAGEMENT ACCOUNTING

Requirement ii

ii) Analysis of Death Star Manufacturing:

Particulars Cost p.u. Amount Amount Cost p.u. Amount Amount Cost p.u. %

Total Sales Volume 2400000 1725000

Prime Costs $5.00 $1,50,00,000 $5.00 $86,25,000 $0.00 0.00%

Manufacturing Costs:

Fixed $5.58 $1,33,92,000 $7.76 $1,33,92,000 $2.18 39.13%

Variable $0.62 $14,88,000 $0.62 $10,69,500 $0.00 0.00%

Total Manufacturing Costs $6.20 $1,48,80,000 $8.38 $1,44,61,500 $2.18 35.22%

Logistic Costs:

Fixed $1.35 $32,40,000 $1.88 $32,40,000 $0.53 39.13%

Variable $0.15 $3,60,000 $0.15 $2,58,750 $0.00 0.00%

Total Logistics Costs $1.50 $36,00,000 $2.03 $34,98,750 $0.53 35.22%

Total Costs $12.70 $3,34,80,000 $15.41 $2,65,85,250 $2.71 21.35%

Before Strategy Implication After Strategy Implication Increase/(Decrease)

Requirement iii

The statement is generated by addressing the essential discoveries that is created from the

policies and the strategies implemented by Empire’s Group with respect to the application of the

profits and the costs related to accounting. It is explained by taking assistance of the evaluation

of the incorporation of the strategy that the overall volume of sales of the electronic toothbrush

of Star Wars is raising from 3000000 to 3900000. It is seen that there is a rise in the overall costs

that is taking place from $38100000 to $43293000. On the other hand, the gross profit for the

company has been increasing from $6900000 to $12087000 and therefore addressing a key rise

in the overall return on assets and the percentage comes to 30.22%.

The post incorporation of the strategy states that a converse effect has been seen in the

volume of sales of the manufacturing of death star. Nonetheless, there has been a decline in the

overall cost of manufacturing to $14461500 in accordance to $14880000. Furthermore, there is a

fall in the overall costs. Thus, it can be observed that there exists a positive effect on the volume

12

MANAGEMENT ACCOUNTING

of sales and the return on the total assets of electronic toothbrush of star war. Thus, it is advisable

to the strategic committee to move forward with the alterations that have been planned.

Answer to Question 5 (Ethics Case Study)

It can be suggested to Burdon to undertake the objectivity that is anticipated from the

management accountant in accordance to the responsibilities for conveying the data in a precise

manner even though these data is not favourable for the one who is asking for it (Al-Shaer et al.,

2017). Hence, Burdon requires to be recommended to address the treatment of accounting to the

management at the top level.

Burdon is advised to undertake the following steps:

It is essential that Burdon ascertains the fact of the scenario and discovering the ethical

problems related with the condition

Values associated to the condition needs to be recognised

Alternate action course needs to be identified \

Probable outcomes of every action course needs to be recognised

MANAGEMENT ACCOUNTING

of sales and the return on the total assets of electronic toothbrush of star war. Thus, it is advisable

to the strategic committee to move forward with the alterations that have been planned.

Answer to Question 5 (Ethics Case Study)

It can be suggested to Burdon to undertake the objectivity that is anticipated from the

management accountant in accordance to the responsibilities for conveying the data in a precise

manner even though these data is not favourable for the one who is asking for it (Al-Shaer et al.,

2017). Hence, Burdon requires to be recommended to address the treatment of accounting to the

management at the top level.

Burdon is advised to undertake the following steps:

It is essential that Burdon ascertains the fact of the scenario and discovering the ethical

problems related with the condition

Values associated to the condition needs to be recognised

Alternate action course needs to be identified \

Probable outcomes of every action course needs to be recognised

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

MANAGEMENT ACCOUNTING

Reference List

Al-Shaer, H., Salama, A., & Toms, S. (2017). Audit committees and financial reporting quality:

Evidence from uk environmental accounting disclosures. Journal of Applied Accounting

Research, 18(1), 2-21.

Burritt, R., & Christ, K. (2016). Industry 4.0 and environmental accounting: a new

revolution?. Asian Journal of Sustainability and Social Responsibility, 1(1), 23-38.

Correa, C., & Larrinaga, C. (2015). Engagement research in social and environmental

accounting. Sustainability Accounting, Management and Policy Journal, 6(1), 5-28.

Deegan, C. (2017). Twenty five years of social and environmental accounting research within

Critical Perspectives of Accounting: Hits, misses and ways forward. Critical Perspectives

on Accounting, 43, 65-87.

Gray, R., Bebbington, J., & Gray, S. (2017). Social and environmental accounting. Vol. I (Los

Angeles, London, New Delhi, Singapore, Washington, 41-56: Sage, 210).

Gray, R., O’Dochartaigh, A., & Rannou, C. (2016). Organisational Effectiveness and Social and

Environmental Accounting: Through the Past Darkly. In Pioneers of Critical

Accounting (pp. 53-71). Palgrave Macmillan, London.

Gunarathne, N., & Lee, K. H. (2015). Environmental Management Accounting (EMA) for

environmental management and organizational change: An eco-control approach. Journal

of Accounting & Organizational Change, 11(3), 362-383.

Latan, H., Jabbour, C. J. C., de Sousa Jabbour, A. B. L., Wamba, S. F., & Shahbaz, M. (2018).

Effects of environmental strategy, environmental uncertainty and top management's

MANAGEMENT ACCOUNTING

Reference List

Al-Shaer, H., Salama, A., & Toms, S. (2017). Audit committees and financial reporting quality:

Evidence from uk environmental accounting disclosures. Journal of Applied Accounting

Research, 18(1), 2-21.

Burritt, R., & Christ, K. (2016). Industry 4.0 and environmental accounting: a new

revolution?. Asian Journal of Sustainability and Social Responsibility, 1(1), 23-38.

Correa, C., & Larrinaga, C. (2015). Engagement research in social and environmental

accounting. Sustainability Accounting, Management and Policy Journal, 6(1), 5-28.

Deegan, C. (2017). Twenty five years of social and environmental accounting research within

Critical Perspectives of Accounting: Hits, misses and ways forward. Critical Perspectives

on Accounting, 43, 65-87.

Gray, R., Bebbington, J., & Gray, S. (2017). Social and environmental accounting. Vol. I (Los

Angeles, London, New Delhi, Singapore, Washington, 41-56: Sage, 210).

Gray, R., O’Dochartaigh, A., & Rannou, C. (2016). Organisational Effectiveness and Social and

Environmental Accounting: Through the Past Darkly. In Pioneers of Critical

Accounting (pp. 53-71). Palgrave Macmillan, London.

Gunarathne, N., & Lee, K. H. (2015). Environmental Management Accounting (EMA) for

environmental management and organizational change: An eco-control approach. Journal

of Accounting & Organizational Change, 11(3), 362-383.

Latan, H., Jabbour, C. J. C., de Sousa Jabbour, A. B. L., Wamba, S. F., & Shahbaz, M. (2018).

Effects of environmental strategy, environmental uncertainty and top management's

14

MANAGEMENT ACCOUNTING

commitment on corporate environmental performance: The role of environmental

management accounting. Journal of Cleaner Production, 180, 297-306.

Roberts, R. W., & Wallace, D. M. (2015). Sustaining diversity in social and environmental

accounting research. Critical Perspectives on Accounting, 32, 78-87.

Russell, S., Milne, M. J., & Dey, C. (2017). Accounts of Nature and the Nature of Accounts:

Critical reflections on environmental accounting and propositions for ecologically

informed accounting. Accounting, Auditing & Accountability Journal, 30(7), 1426-1458.

MANAGEMENT ACCOUNTING

commitment on corporate environmental performance: The role of environmental

management accounting. Journal of Cleaner Production, 180, 297-306.

Roberts, R. W., & Wallace, D. M. (2015). Sustaining diversity in social and environmental

accounting research. Critical Perspectives on Accounting, 32, 78-87.

Russell, S., Milne, M. J., & Dey, C. (2017). Accounts of Nature and the Nature of Accounts:

Critical reflections on environmental accounting and propositions for ecologically

informed accounting. Accounting, Auditing & Accountability Journal, 30(7), 1426-1458.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.