Management Accounting: Roles, Systems, and Techniques

VerifiedAdded on 2022/11/27

|23

|4180

|467

AI Summary

This document provides a comprehensive overview of management accounting, including its roles, systems, and techniques. It explains how management accounting helps in decision-making, cost evaluation, and financial planning. The document also explores different management accounting systems, such as inventory management, price optimization, cost accounting, and job costing. Additionally, it discusses various techniques used for cost analysis and budgeting. Lastly, it covers the uses of planning tools and how organizations can respond to financial problems using management accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 1

Question-Answers

LO1- Management Accounting

Management Accounting is the procedure of maintaining management reports and accounts that

offer correct and timely financial information that is necessary by managers to take the decisions

such as short term or long terms decisions. The act of translating the financial data into the useful

information helps the managers and officers to take the decision (Business Dictionary, 2018).

Roles of Management Accounting

Management accounting plays the different role in the organization as it is essential to retain the

financial information. The role of management accounting is describing below:

Formulate Financial Strategies- Management accountants can frame financial strategies using;

sales forecasts, job costing techniques, and budgets. It has been seen that the organization

develop the strategies to improve the net profit, gross income, and earning per share. It is

essential for the organisation to analyses the financial data while developing the strategies for the

growth.

Monitor expenses- Gathering financial data of the organization in a single book helps to monitor

all the expenses and incomes.

Maintain Profitability- Company maintains its books and accounts due to which the

profitability of an organization will maintain (Chenhall, and Moers, 2015).

Question-Answers

LO1- Management Accounting

Management Accounting is the procedure of maintaining management reports and accounts that

offer correct and timely financial information that is necessary by managers to take the decisions

such as short term or long terms decisions. The act of translating the financial data into the useful

information helps the managers and officers to take the decision (Business Dictionary, 2018).

Roles of Management Accounting

Management accounting plays the different role in the organization as it is essential to retain the

financial information. The role of management accounting is describing below:

Formulate Financial Strategies- Management accountants can frame financial strategies using;

sales forecasts, job costing techniques, and budgets. It has been seen that the organization

develop the strategies to improve the net profit, gross income, and earning per share. It is

essential for the organisation to analyses the financial data while developing the strategies for the

growth.

Monitor expenses- Gathering financial data of the organization in a single book helps to monitor

all the expenses and incomes.

Maintain Profitability- Company maintains its books and accounts due to which the

profitability of an organization will maintain (Chenhall, and Moers, 2015).

MANAGEMENT ACCOUNTING 2

Management Accounting System

Inventory Management System- In this system, all the transaction related to stock is recorded.

The activity of supply chain is also mentioned in the report as it helps to maintain the stock to

operate smoothly in the market.

Price Optimization System- In this system, the organization set the prices of delivering the

services to consumers.

Cost Accounting System- It is the system that is used by the manufacturing department in order

to record the production events by using the perpetual inventory system.

Job Costing System- In this system, the cost is allocated to the specific job or business involved

in it.

It has been seen that the different management systems have different role in the organization

that helps to operate smoothly in the market. It is essential for the organization to implement

these systems at the workplace to gain the advantage (Kaplan, and Atkinson, 2015).

Methods of managerial accounting reports

There are various ways in which the organization maintains their reports with the accurate

amount and these are as below:

Budget Report- Organisation can prepare the budget by collecting financial data as per the

financial funds. It is useful for the managers to control the cost of every department and reduces

the wastage.

Accounts Receivable Aging Reports- Organization can maintain the account receivable aging

report to uphold the cash flow statement for organisations that spread credits for their customers.

Management Accounting System

Inventory Management System- In this system, all the transaction related to stock is recorded.

The activity of supply chain is also mentioned in the report as it helps to maintain the stock to

operate smoothly in the market.

Price Optimization System- In this system, the organization set the prices of delivering the

services to consumers.

Cost Accounting System- It is the system that is used by the manufacturing department in order

to record the production events by using the perpetual inventory system.

Job Costing System- In this system, the cost is allocated to the specific job or business involved

in it.

It has been seen that the different management systems have different role in the organization

that helps to operate smoothly in the market. It is essential for the organization to implement

these systems at the workplace to gain the advantage (Kaplan, and Atkinson, 2015).

Methods of managerial accounting reports

There are various ways in which the organization maintains their reports with the accurate

amount and these are as below:

Budget Report- Organisation can prepare the budget by collecting financial data as per the

financial funds. It is useful for the managers to control the cost of every department and reduces

the wastage.

Accounts Receivable Aging Reports- Organization can maintain the account receivable aging

report to uphold the cash flow statement for organisations that spread credits for their customers.

MANAGEMENT ACCOUNTING 3

Job Costs Report – The report contain the expenses of a specific project that helps to estimate

the revenue so that the organization can earns the profitability.

Inventory and Manufacturing – Organization that has the physical inventory can also maintain

the inventory and manufacturing report to create their manufacturing process efficient or

effective (Cooper, Ezzamel, and Qu, 2017).

Advantages of systems of management accounting with an organization

There are numerous assistances of system of management accounting that improves the

operations and overall profitability. The assistances of management accounting system are

discussed below:

Reduce expenses- Maintaining the management accounting report with the different systems

helps to maintain the balance between the expenses and revenues. Budget report of the

organization helps to allocate the cost as per the requirement of the departments due to which the

expenses will control.

Improve cash flows- It has been seen that the accounts receivable aging report is maintain that

supports to compare the cash flow statement. This system is mainly roll up into the company

total master budget that helps to save the money by analyzing the expenditure with the revenue.

Maintaining balance between the expenditure and revenue improves the cash flow statement of

the organization.

Business Decisions-

Job Costs Report – The report contain the expenses of a specific project that helps to estimate

the revenue so that the organization can earns the profitability.

Inventory and Manufacturing – Organization that has the physical inventory can also maintain

the inventory and manufacturing report to create their manufacturing process efficient or

effective (Cooper, Ezzamel, and Qu, 2017).

Advantages of systems of management accounting with an organization

There are numerous assistances of system of management accounting that improves the

operations and overall profitability. The assistances of management accounting system are

discussed below:

Reduce expenses- Maintaining the management accounting report with the different systems

helps to maintain the balance between the expenses and revenues. Budget report of the

organization helps to allocate the cost as per the requirement of the departments due to which the

expenses will control.

Improve cash flows- It has been seen that the accounts receivable aging report is maintain that

supports to compare the cash flow statement. This system is mainly roll up into the company

total master budget that helps to save the money by analyzing the expenditure with the revenue.

Maintaining balance between the expenditure and revenue improves the cash flow statement of

the organization.

Business Decisions-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 4

Preparing the accounts and reports of management accounting supports the organization to take

the accurate decision. Management accounting assistances to analyses the quantitative with the

qualitative to take the decision appropriately (Thomas, 2016).

Increase Financial Returns

Management accounting also supports to prepare the financial forecasts in order to increase the

consumers demand and potential sales due to which the company financial returns is increases.

LO2- Techniques of Management Accounting

Evaluation of cost using suitable techniques of cost analysis

Cost- It is a monetary value that the organisation has spent in order to gain somewhat in return or

produce something. In the organization, cost symbolizes the money amount that the organisation

spends the amount in producing something (Labro, 2019).

Differentiation Classification Cost

There is various costs that are spent by the organization in order to producing something. These

are given below:

Fixed Cost- The cost that remains constant and cannot change with the change of output level

or sales revenue.

Variable Cost- It is the cost that can be differs from the production volume or services provided.

Direct Cost-The amount that can be spent on the production of specific goods or services.

Indirect Cost- Indirect Cost is the cost that is not straight liable to a cost object. It can be fixed

or variable in nature but particular overhead cost can be directly credited to a project.

Preparing the accounts and reports of management accounting supports the organization to take

the accurate decision. Management accounting assistances to analyses the quantitative with the

qualitative to take the decision appropriately (Thomas, 2016).

Increase Financial Returns

Management accounting also supports to prepare the financial forecasts in order to increase the

consumers demand and potential sales due to which the company financial returns is increases.

LO2- Techniques of Management Accounting

Evaluation of cost using suitable techniques of cost analysis

Cost- It is a monetary value that the organisation has spent in order to gain somewhat in return or

produce something. In the organization, cost symbolizes the money amount that the organisation

spends the amount in producing something (Labro, 2019).

Differentiation Classification Cost

There is various costs that are spent by the organization in order to producing something. These

are given below:

Fixed Cost- The cost that remains constant and cannot change with the change of output level

or sales revenue.

Variable Cost- It is the cost that can be differs from the production volume or services provided.

Direct Cost-The amount that can be spent on the production of specific goods or services.

Indirect Cost- Indirect Cost is the cost that is not straight liable to a cost object. It can be fixed

or variable in nature but particular overhead cost can be directly credited to a project.

MANAGEMENT ACCOUNTING 5

Material Cost- It is the cost of production material that can be easily found with the unit of

production. It can also be said that it is the cost of direct material.

Labor Cost- This cost includes the wages that are incurred while producing the goods or

delivering the specific services to consumers (Quattrone, 2016).

Different Costing System

There is various costing system that can be used by the organizations to assess the cost and these

are given below:

Absorption Costing System

Variable costing is the methodology which is only assigned the variable cost to inventory. In this

system, all overhead costs are considered as the expenses in the period while variable overhead

cost and direct material are allocated as an inventory of the organisation. It has been evaluated

that there is no uses of the variable costing in the financial reports since the accounting

frameworks implement at the workplace (Babu, and Masum, 2019).

Marginal Costing System

It is a cost that will incurred on one additional unit of output. It is used by the organisations to

evaluate the optimum production quantity. The company who operates the business within the

sweet spot helps to maximize the profits. This concept is used to measure the product pricing

which is essential for the organisation to measure the price while consumers request the lowest

possible price.

Job Costing System

Material Cost- It is the cost of production material that can be easily found with the unit of

production. It can also be said that it is the cost of direct material.

Labor Cost- This cost includes the wages that are incurred while producing the goods or

delivering the specific services to consumers (Quattrone, 2016).

Different Costing System

There is various costing system that can be used by the organizations to assess the cost and these

are given below:

Absorption Costing System

Variable costing is the methodology which is only assigned the variable cost to inventory. In this

system, all overhead costs are considered as the expenses in the period while variable overhead

cost and direct material are allocated as an inventory of the organisation. It has been evaluated

that there is no uses of the variable costing in the financial reports since the accounting

frameworks implement at the workplace (Babu, and Masum, 2019).

Marginal Costing System

It is a cost that will incurred on one additional unit of output. It is used by the organisations to

evaluate the optimum production quantity. The company who operates the business within the

sweet spot helps to maximize the profits. This concept is used to measure the product pricing

which is essential for the organisation to measure the price while consumers request the lowest

possible price.

Job Costing System

MANAGEMENT ACCOUNTING 6

A job costing system contains the process of collecting the data that is relative to the cost of a

specific production or services. The data and facts gathered in this system is also used to evaluate

the accuracy of the valuing system of the organisation. This system is used to allocate the

inventoriable costs to manufactured goods (Labro, 2019).

Process Costing System

The process costing system supports to collect the cost when a huge number of matching units

are being shaped. It is the greatest efficient system to gather the costs that an aggregate level for

a great batch of products.

LO3- Uses of planning tools

Advantages and Disadvantages of planning tools that are used for budgetary control

Budget - Budget is a report in which the valuation of revenue and expenses is considered for a

specified future. The report is prepared on the periodic basis or for a specified period.

Budgetary control- It is a system of management control describes the situation in which the

actual incomes and spending amount are associated with the planned income and spending

amount in order to control the expense (Otley, 2016).

Different types of Budgets

There are numerous types of budget that are necessary to maintain by the organization in order to

earn the high profit. These are given below:

Capital Budget-Capital Budget is the procedure in which the organization evaluates the

expenses or investments that are huge in amount.

A job costing system contains the process of collecting the data that is relative to the cost of a

specific production or services. The data and facts gathered in this system is also used to evaluate

the accuracy of the valuing system of the organisation. This system is used to allocate the

inventoriable costs to manufactured goods (Labro, 2019).

Process Costing System

The process costing system supports to collect the cost when a huge number of matching units

are being shaped. It is the greatest efficient system to gather the costs that an aggregate level for

a great batch of products.

LO3- Uses of planning tools

Advantages and Disadvantages of planning tools that are used for budgetary control

Budget - Budget is a report in which the valuation of revenue and expenses is considered for a

specified future. The report is prepared on the periodic basis or for a specified period.

Budgetary control- It is a system of management control describes the situation in which the

actual incomes and spending amount are associated with the planned income and spending

amount in order to control the expense (Otley, 2016).

Different types of Budgets

There are numerous types of budget that are necessary to maintain by the organization in order to

earn the high profit. These are given below:

Capital Budget-Capital Budget is the procedure in which the organization evaluates the

expenses or investments that are huge in amount.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 7

Operational Budgeting- The Company estimated all the incomes and expenses that are rely on

the future estimation report for the given period of time.

Financial Budget- Financial budget is the process in which the assets, cash flow, incomes and

expenses are estimated that are used to managing the strategy (Cools, Stouthuysen, and Van den

Abbeele, 2017).

Advantage and Disadvantage of Budgeting

Advantages

Forecasting- Preparing budget not only supports the company to sustain the heavy expenses but

also helps to estimate the cost which will occur in the coming future. It is beneficial for the

organisation to forecast the cost in terms of saving the money.

Price setting- It has been seen that there are various budget reports that helps the organisation to

sustain the market position by setting the prices. The budget of the organisation is developed by

the company by analyzing the market condition such as by analyzing the competitor’s prices in

different parameters. The company analyses the different parameters such as fees, rates, and

prices. Set up prices in the process of budgeting helps to enjoy the competitive advantage in the

market (Arend, Zhao, Song, and Im, 2017).

Credit Procurement- There are various financial institutions that help the organisation in

monetary terms such as banks, suppliers, and the other lenders. These financial institutions

provide the money on credit by analyzing the financial situation of the organization. It is required

to prepare the budget to represent while borrowing the money on credit.

Disadvantages

Operational Budgeting- The Company estimated all the incomes and expenses that are rely on

the future estimation report for the given period of time.

Financial Budget- Financial budget is the process in which the assets, cash flow, incomes and

expenses are estimated that are used to managing the strategy (Cools, Stouthuysen, and Van den

Abbeele, 2017).

Advantage and Disadvantage of Budgeting

Advantages

Forecasting- Preparing budget not only supports the company to sustain the heavy expenses but

also helps to estimate the cost which will occur in the coming future. It is beneficial for the

organisation to forecast the cost in terms of saving the money.

Price setting- It has been seen that there are various budget reports that helps the organisation to

sustain the market position by setting the prices. The budget of the organisation is developed by

the company by analyzing the market condition such as by analyzing the competitor’s prices in

different parameters. The company analyses the different parameters such as fees, rates, and

prices. Set up prices in the process of budgeting helps to enjoy the competitive advantage in the

market (Arend, Zhao, Song, and Im, 2017).

Credit Procurement- There are various financial institutions that help the organisation in

monetary terms such as banks, suppliers, and the other lenders. These financial institutions

provide the money on credit by analyzing the financial situation of the organization. It is required

to prepare the budget to represent while borrowing the money on credit.

Disadvantages

MANAGEMENT ACCOUNTING 8

Blame for Outcomes- If a division does not receive the budget at the appropriate amount then

they blame to the other department budget in the monetary terms. It is observed that the conflicts

has been arises among the departments within the organization.

Time Consuming - It has been observed that the organisation prepare the budget by analyzing

the market condition and internal resources. The process of analyzing the market condition and

preparing the budget helps the organization but it consumes the high time.

Inaccurate estimation- It has been evaluated that the budget report is prepared as per the

expenses of different departments. It is observed that the estimated amounts of expenses are

inaccurate because sometimes departments require more money to invest that time budget report

will fail (Rajnoha, Štefko, Merková, and Dobrovič, 2016).

LO4- Comparison ways in which organizations could use management accounting to

respond to financial problems

Adoption of systems of management accounting in order to respond the financial problems

Benchmarking- It is a procedure of assessing the performance of products, processes, or

services with the other companies of the industry. It also helps the organization to analyses the

internal resources and capabilities for improvement (Castro, and Frazzon, 2017).

Key Benefits-

The process of Benchmarking is useful for the organisation in terms of profit and efficiency of

financial condition. The benefits are discussed below:

It helps to improve the employee understanding towards the cost structure

Blame for Outcomes- If a division does not receive the budget at the appropriate amount then

they blame to the other department budget in the monetary terms. It is observed that the conflicts

has been arises among the departments within the organization.

Time Consuming - It has been observed that the organisation prepare the budget by analyzing

the market condition and internal resources. The process of analyzing the market condition and

preparing the budget helps the organization but it consumes the high time.

Inaccurate estimation- It has been evaluated that the budget report is prepared as per the

expenses of different departments. It is observed that the estimated amounts of expenses are

inaccurate because sometimes departments require more money to invest that time budget report

will fail (Rajnoha, Štefko, Merková, and Dobrovič, 2016).

LO4- Comparison ways in which organizations could use management accounting to

respond to financial problems

Adoption of systems of management accounting in order to respond the financial problems

Benchmarking- It is a procedure of assessing the performance of products, processes, or

services with the other companies of the industry. It also helps the organization to analyses the

internal resources and capabilities for improvement (Castro, and Frazzon, 2017).

Key Benefits-

The process of Benchmarking is useful for the organisation in terms of profit and efficiency of

financial condition. The benefits are discussed below:

It helps to improve the employee understanding towards the cost structure

MANAGEMENT ACCOUNTING 9

It also encourages the team and builds the interest of becoming more competitive

It enhances the performance of organization by analyzing or evaluating the opportunities.

Key Performance Indicators

It is a kind of tool that used to evaluate the performance. KPIs help to estimate the success of the

organization or an activity of the business in which they perform the services. It has been seen

that the selecting the right KPIs depend upon an understanding of importance of activities of the

organisation (Uyar, and Kuzey, 2016).

Management Accounting Skills required

Planning and Reporting-It is required to evaluate the future, measure performance and report

financial results. Planning and reporting is prepared by the organization that helps to evaluate the

financial statements.

Decision Making- It is required to guide to take the decision, manage risk and the others. The

skill of management accountant is used by the organisation to take the decision for the

development.

Leadership- It is required to collaborate and inspire the team to attain the organizational goal. It

is essential for the management accounting to have leadership skills in order to encourage the

team.

Technology – The management accountant should have the knowledge of technology manage

and information system to enable the effective operations.

Skills help to solve the financial problems

It also encourages the team and builds the interest of becoming more competitive

It enhances the performance of organization by analyzing or evaluating the opportunities.

Key Performance Indicators

It is a kind of tool that used to evaluate the performance. KPIs help to estimate the success of the

organization or an activity of the business in which they perform the services. It has been seen

that the selecting the right KPIs depend upon an understanding of importance of activities of the

organisation (Uyar, and Kuzey, 2016).

Management Accounting Skills required

Planning and Reporting-It is required to evaluate the future, measure performance and report

financial results. Planning and reporting is prepared by the organization that helps to evaluate the

financial statements.

Decision Making- It is required to guide to take the decision, manage risk and the others. The

skill of management accountant is used by the organisation to take the decision for the

development.

Leadership- It is required to collaborate and inspire the team to attain the organizational goal. It

is essential for the management accounting to have leadership skills in order to encourage the

team.

Technology – The management accountant should have the knowledge of technology manage

and information system to enable the effective operations.

Skills help to solve the financial problems

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 10

Replacement -It has been seen that these skills helps the organisation to cut out the expenses or

implementing the changes to replace the large amount of expenses with the small amount of

expenses. Implementing the changes in the organisation helps to reduce the financial issues of

large expenses or enhancing the performance.

Expenses reduce- If a management accountant has the skills than he can reduce the expenses

because it helps to identify the areas that need some special attention. Budgeting report is the

process in which the organisation controls the expenses by estimating the cost for future. The

issue of facing heavy losses will be solved by reducing the expenses.

Increase spending Awareness- As discussed above, it has been seen that the leadership skill

helps to encourage the team in order to perform well in their services. Spreading awareness

among the team helps to reduce the cost of operating the business because team members invest

less amount to manufacture the product. It helps to prevent the organisation from the financial

problems by investing fewer amounts in operating activities.

Creating plan or budget- It is observed that the creating plan or budget helps the organisation

to solve the financial problems. Generating a plan for spending the money for a month is the

smartest thing that helps to aware the departments to invest the money in an appropriate manner.

System of management accounting can lead organization to sustainable success in order to

respond to financial problems

The main purpose of management accounting is to offer the information to management in order

to take the appropriate decision towards the organisation. In the case of financial problems, it has

been seen that the organisation requires the information or the details from which they can use to

address the financial issues. Management accounting is the processes in which the different

Replacement -It has been seen that these skills helps the organisation to cut out the expenses or

implementing the changes to replace the large amount of expenses with the small amount of

expenses. Implementing the changes in the organisation helps to reduce the financial issues of

large expenses or enhancing the performance.

Expenses reduce- If a management accountant has the skills than he can reduce the expenses

because it helps to identify the areas that need some special attention. Budgeting report is the

process in which the organisation controls the expenses by estimating the cost for future. The

issue of facing heavy losses will be solved by reducing the expenses.

Increase spending Awareness- As discussed above, it has been seen that the leadership skill

helps to encourage the team in order to perform well in their services. Spreading awareness

among the team helps to reduce the cost of operating the business because team members invest

less amount to manufacture the product. It helps to prevent the organisation from the financial

problems by investing fewer amounts in operating activities.

Creating plan or budget- It is observed that the creating plan or budget helps the organisation

to solve the financial problems. Generating a plan for spending the money for a month is the

smartest thing that helps to aware the departments to invest the money in an appropriate manner.

System of management accounting can lead organization to sustainable success in order to

respond to financial problems

The main purpose of management accounting is to offer the information to management in order

to take the appropriate decision towards the organisation. In the case of financial problems, it has

been seen that the organisation requires the information or the details from which they can use to

address the financial issues. Management accounting is the processes in which the different

MANAGEMENT ACCOUNTING 11

reports are maintain to get the whole information or financial data of the organisation (Maas,

Schaltegger, and Crutzen, 2016). These reports help to gather the information that can be used by

the organisation to resolve the financial problems.

Nowadays, it is required for the organisations to develop the business strategies, models and

practices to overcome the challenges of social, environmental while creating the financial

success and developing the values of shareholders. The management report of the organisation

states that how numerous business units have disappeared into the valuable intelligences.

Management accounting report represents the business entities that have disappeared into the

appreciated intelligences and analysis in order to gain the accountability capabilities. It includes

the analysis of business environment or social factors that affects the development of the

organisation and its performance in financial terms (Groesser, and Jovy, 2016). The

organisations mainly face the issues just because of respondent and management that do not

consider the data or facts while taking the decision.

Forecasting the cash flows- Forecasting the cash flow helps to calculate the upcoming cash

surpluses or shortages. The information helps the organisation to take the right choices for future.

The various decisions can take the organisation by using or estimating the future cost of the cash

flows such as tax preparation, planning new equipment’s purchases or finding the financial areas

to secure the small business loan. Management accounting report helps to forecast the cash flow

as it gathered the all cash transactions. The organisation can also use the estimating information

for an upcoming business change or decision.

Management accounts reports are used in many ways to guide the companies to attain the

success:

reports are maintain to get the whole information or financial data of the organisation (Maas,

Schaltegger, and Crutzen, 2016). These reports help to gather the information that can be used by

the organisation to resolve the financial problems.

Nowadays, it is required for the organisations to develop the business strategies, models and

practices to overcome the challenges of social, environmental while creating the financial

success and developing the values of shareholders. The management report of the organisation

states that how numerous business units have disappeared into the valuable intelligences.

Management accounting report represents the business entities that have disappeared into the

appreciated intelligences and analysis in order to gain the accountability capabilities. It includes

the analysis of business environment or social factors that affects the development of the

organisation and its performance in financial terms (Groesser, and Jovy, 2016). The

organisations mainly face the issues just because of respondent and management that do not

consider the data or facts while taking the decision.

Forecasting the cash flows- Forecasting the cash flow helps to calculate the upcoming cash

surpluses or shortages. The information helps the organisation to take the right choices for future.

The various decisions can take the organisation by using or estimating the future cost of the cash

flows such as tax preparation, planning new equipment’s purchases or finding the financial areas

to secure the small business loan. Management accounting report helps to forecast the cash flow

as it gathered the all cash transactions. The organisation can also use the estimating information

for an upcoming business change or decision.

Management accounts reports are used in many ways to guide the companies to attain the

success:

MANAGEMENT ACCOUNTING 12

This report helps to elaborate the influence of these constancy issues in terms of strong

business.

The report helps to find environmental and social factors that affect the company

capability to make the value over time.

It helps the organisation to face the business challenges by developing the business

strategy, model, performance overview and licensing license.

It is utilizing the administrative accounting tools or techniques like life cycle cost, and

carbon footprint, natural resources gain and the others in order to assist the combining

matters in decision making procedure (Malmi, 2016).

This report helps to elaborate the influence of these constancy issues in terms of strong

business.

The report helps to find environmental and social factors that affect the company

capability to make the value over time.

It helps the organisation to face the business challenges by developing the business

strategy, model, performance overview and licensing license.

It is utilizing the administrative accounting tools or techniques like life cycle cost, and

carbon footprint, natural resources gain and the others in order to assist the combining

matters in decision making procedure (Malmi, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 13

References

Arend, R.J., Zhao, Y.L., Song, M. and Im, S. (2017) Strategic planning as a complex and

enabling managerial tool. Strategic Management Journal, 38(8), pp.1741-1752.

Argenti, J. (2018) Practical corporate planning. Routledge.

Babu, M.A. and Masum, M.H. (2019) Crucial Factors for the Implementation of Activity-Based

Costing System: A Comprehensive Study of Bangladesh. ABC Research Alert, 7(1).

Business Dictionary. (2018) Management accounting. [online] Available from:

http://www.businessdictionary.com/definition/management-accounting.html [Accessed

11/07/19].

Castro, V.F.D. and Frazzon, E.M. (2017) Benchmarking of best practices: an overview of the

academic literature. Benchmarking: an international journal, 24(3), pp.750-774.

Chenhall, R.H. and Moers, F. (2015) The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and society,

47, pp.1-13.

Cools, M., Stouthuysen, K. and Van den Abbeele, A. (2017) Management control for stimulating

different types of creativity: The role of budgets. Journal of Management Accounting Research,

29(3), pp.1-21.

Cooper, D.J., Ezzamel, M. and Qu, S.Q. (2017) Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research, 34(2), pp.991-1025.

Groesser, S.N. and Jovy, N. (2016) Business model analysis using computational modeling: A

strategy tool for exploration and decision-making. Journal of Management Control, 27(1),

pp.61-88.

Kaplan, R.S. and Atkinson, A.A. (2015) Advanced management accounting. PHI Learning.

References

Arend, R.J., Zhao, Y.L., Song, M. and Im, S. (2017) Strategic planning as a complex and

enabling managerial tool. Strategic Management Journal, 38(8), pp.1741-1752.

Argenti, J. (2018) Practical corporate planning. Routledge.

Babu, M.A. and Masum, M.H. (2019) Crucial Factors for the Implementation of Activity-Based

Costing System: A Comprehensive Study of Bangladesh. ABC Research Alert, 7(1).

Business Dictionary. (2018) Management accounting. [online] Available from:

http://www.businessdictionary.com/definition/management-accounting.html [Accessed

11/07/19].

Castro, V.F.D. and Frazzon, E.M. (2017) Benchmarking of best practices: an overview of the

academic literature. Benchmarking: an international journal, 24(3), pp.750-774.

Chenhall, R.H. and Moers, F. (2015) The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and society,

47, pp.1-13.

Cools, M., Stouthuysen, K. and Van den Abbeele, A. (2017) Management control for stimulating

different types of creativity: The role of budgets. Journal of Management Accounting Research,

29(3), pp.1-21.

Cooper, D.J., Ezzamel, M. and Qu, S.Q. (2017) Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research, 34(2), pp.991-1025.

Groesser, S.N. and Jovy, N. (2016) Business model analysis using computational modeling: A

strategy tool for exploration and decision-making. Journal of Management Control, 27(1),

pp.61-88.

Kaplan, R.S. and Atkinson, A.A. (2015) Advanced management accounting. PHI Learning.

MANAGEMENT ACCOUNTING 14

Labro, E. (2019) Costing Systems. Foundations and Trends® in Accounting, 13(3-4), pp.267-

404.

Maas, K., Schaltegger, S. and Crutzen, N. (2016) Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136, pp.237-

248.

Malmi, T. (2016) Managerialist studies in management accounting: 1990–2014. Management

Accounting Research, 31, pp.31-44.

Otley, D. (2016) The contingency theory of management accounting and control: 1980–2014.

Management accounting research, 31, pp.45-62.

Quattrone, P. (2016) Management accounting goes digital: Will the move make it wiser?.

Management Accounting Research, 31, pp.118-122.

Rajnoha, R., Štefko, R., Merková, M. and Dobrovič, J. (2016) Business intelligence as a key

information and knowledge tool for strategic business performance management. E+ M

Ekonomie a Management.

Schaltegger, S. and Burritt, R. (2017) Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Thomas, T.F. (2016) Motivating revisions of management accounting systems: An examination

of organizational goals and accounting feedback. Accounting, Organizations and Society, 53,

pp.1-16.

Uyar, A. and Kuzey, C. (2016) Does management accounting mediate the relationship between

cost system design and performance?. Advances in accounting, 35, pp.170-176.

Labro, E. (2019) Costing Systems. Foundations and Trends® in Accounting, 13(3-4), pp.267-

404.

Maas, K., Schaltegger, S. and Crutzen, N. (2016) Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136, pp.237-

248.

Malmi, T. (2016) Managerialist studies in management accounting: 1990–2014. Management

Accounting Research, 31, pp.31-44.

Otley, D. (2016) The contingency theory of management accounting and control: 1980–2014.

Management accounting research, 31, pp.45-62.

Quattrone, P. (2016) Management accounting goes digital: Will the move make it wiser?.

Management Accounting Research, 31, pp.118-122.

Rajnoha, R., Štefko, R., Merková, M. and Dobrovič, J. (2016) Business intelligence as a key

information and knowledge tool for strategic business performance management. E+ M

Ekonomie a Management.

Schaltegger, S. and Burritt, R. (2017) Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Thomas, T.F. (2016) Motivating revisions of management accounting systems: An examination

of organizational goals and accounting feedback. Accounting, Organizations and Society, 53,

pp.1-16.

Uyar, A. and Kuzey, C. (2016) Does management accounting mediate the relationship between

cost system design and performance?. Advances in accounting, 35, pp.170-176.

MANAGEMENT ACCOUNTING 15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 16

Appendix

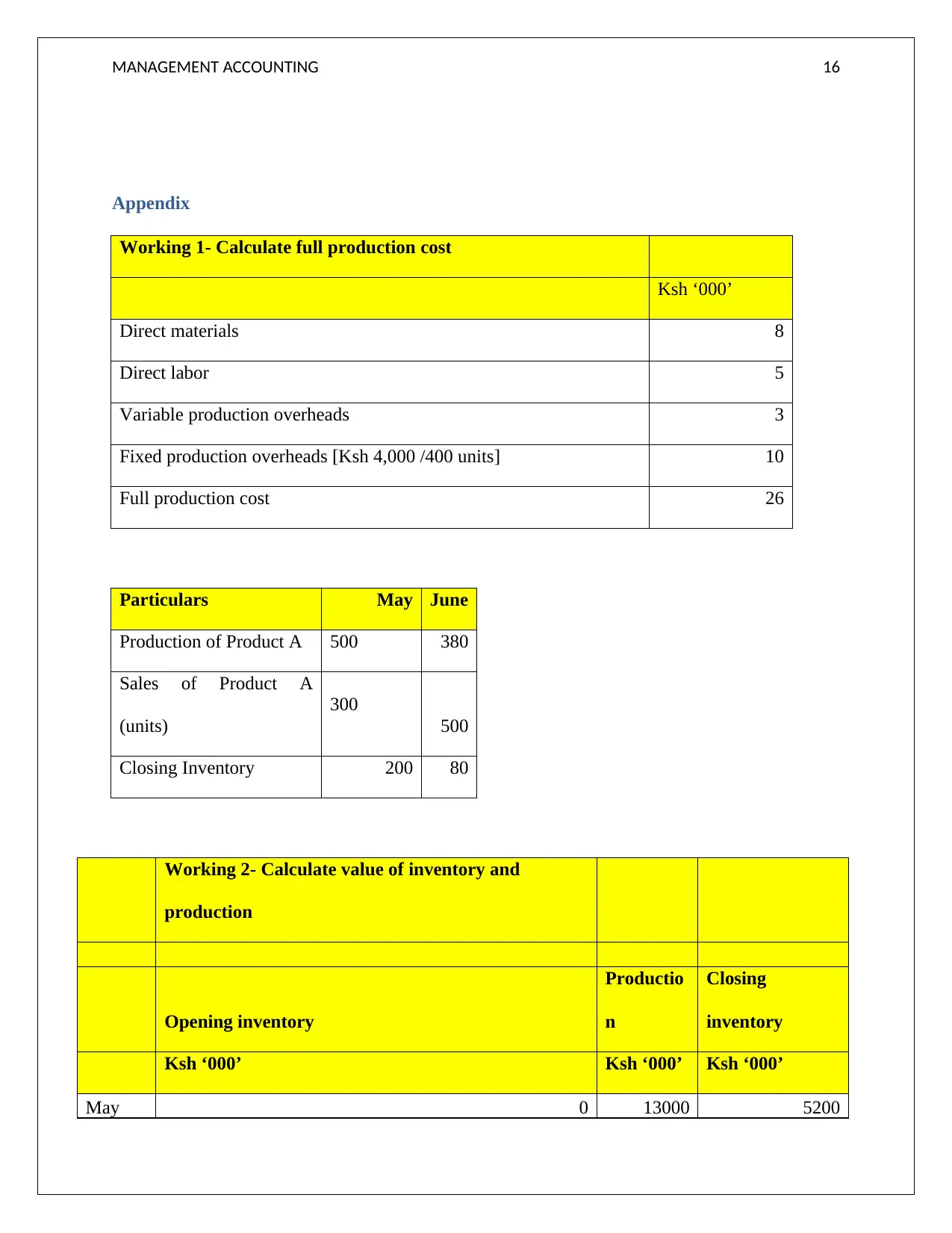

Working 1- Calculate full production cost

Ksh ‘000’

Direct materials 8

Direct labor 5

Variable production overheads 3

Fixed production overheads [Ksh 4,000 /400 units] 10

Full production cost 26

Particulars May June

Production of Product A 500 380

Sales of Product A

(units)

300

500

Closing Inventory 200 80

Working 2- Calculate value of inventory and

production

Opening inventory

Productio

n

Closing

inventory

Ksh ‘000’ Ksh ‘000’ Ksh ‘000’

May 0 13000 5200

Appendix

Working 1- Calculate full production cost

Ksh ‘000’

Direct materials 8

Direct labor 5

Variable production overheads 3

Fixed production overheads [Ksh 4,000 /400 units] 10

Full production cost 26

Particulars May June

Production of Product A 500 380

Sales of Product A

(units)

300

500

Closing Inventory 200 80

Working 2- Calculate value of inventory and

production

Opening inventory

Productio

n

Closing

inventory

Ksh ‘000’ Ksh ‘000’ Ksh ‘000’

May 0 13000 5200

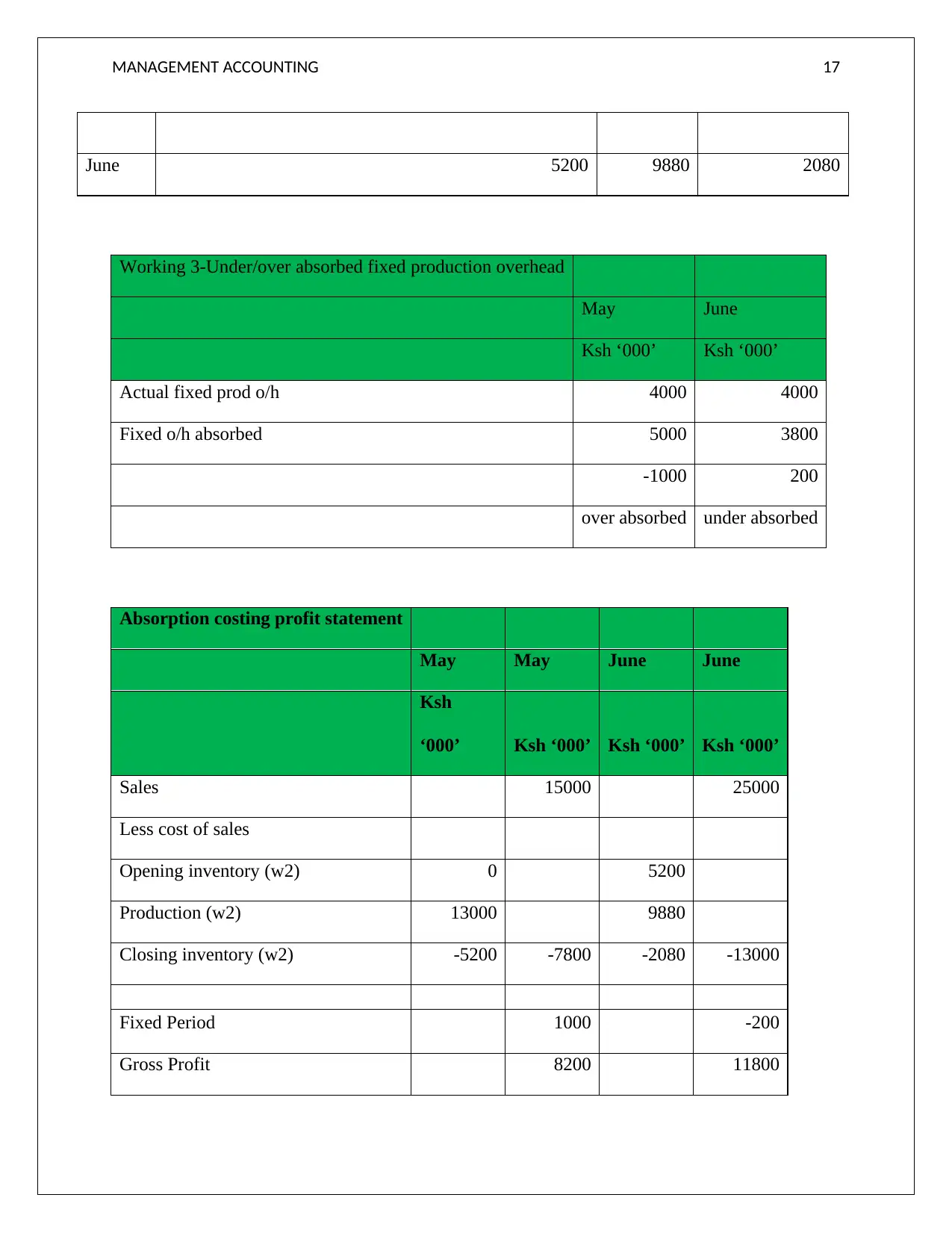

MANAGEMENT ACCOUNTING 17

June 5200 9880 2080

Working 3-Under/over absorbed fixed production overhead

May June

Ksh ‘000’ Ksh ‘000’

Actual fixed prod o/h 4000 4000

Fixed o/h absorbed 5000 3800

-1000 200

over absorbed under absorbed

Absorption costing profit statement

May May June June

Ksh

‘000’ Ksh ‘000’ Ksh ‘000’ Ksh ‘000’

Sales 15000 25000

Less cost of sales

Opening inventory (w2) 0 5200

Production (w2) 13000 9880

Closing inventory (w2) -5200 -7800 -2080 -13000

Fixed Period 1000 -200

Gross Profit 8200 11800

June 5200 9880 2080

Working 3-Under/over absorbed fixed production overhead

May June

Ksh ‘000’ Ksh ‘000’

Actual fixed prod o/h 4000 4000

Fixed o/h absorbed 5000 3800

-1000 200

over absorbed under absorbed

Absorption costing profit statement

May May June June

Ksh

‘000’ Ksh ‘000’ Ksh ‘000’ Ksh ‘000’

Sales 15000 25000

Less cost of sales

Opening inventory (w2) 0 5200

Production (w2) 13000 9880

Closing inventory (w2) -5200 -7800 -2080 -13000

Fixed Period 1000 -200

Gross Profit 8200 11800

MANAGEMENT ACCOUNTING 18

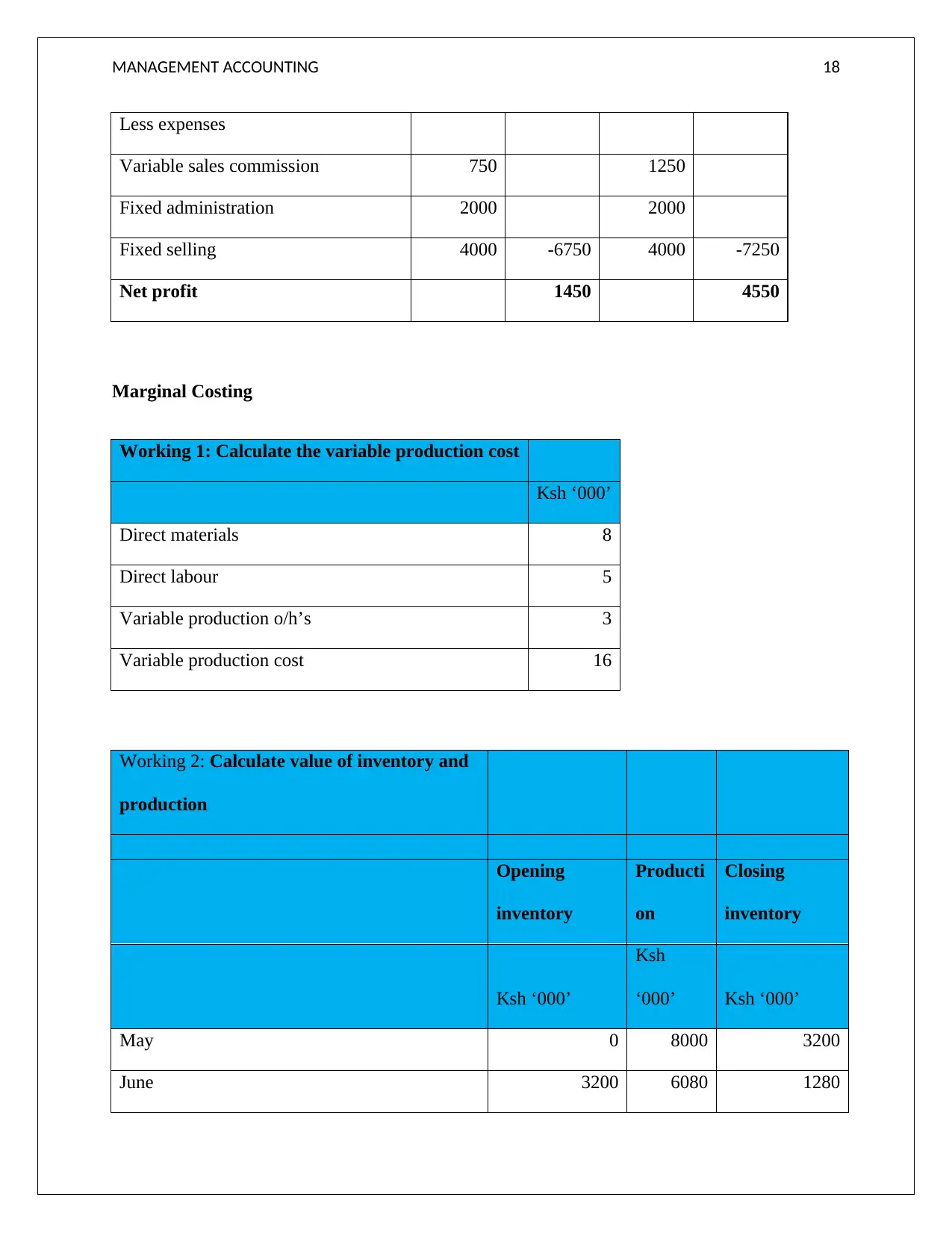

Less expenses

Variable sales commission 750 1250

Fixed administration 2000 2000

Fixed selling 4000 -6750 4000 -7250

Net profit 1450 4550

Marginal Costing

Working 1: Calculate the variable production cost

Ksh ‘000’

Direct materials 8

Direct labour 5

Variable production o/h’s 3

Variable production cost 16

Working 2: Calculate value of inventory and

production

Opening

inventory

Producti

on

Closing

inventory

Ksh ‘000’

Ksh

‘000’ Ksh ‘000’

May 0 8000 3200

June 3200 6080 1280

Less expenses

Variable sales commission 750 1250

Fixed administration 2000 2000

Fixed selling 4000 -6750 4000 -7250

Net profit 1450 4550

Marginal Costing

Working 1: Calculate the variable production cost

Ksh ‘000’

Direct materials 8

Direct labour 5

Variable production o/h’s 3

Variable production cost 16

Working 2: Calculate value of inventory and

production

Opening

inventory

Producti

on

Closing

inventory

Ksh ‘000’

Ksh

‘000’ Ksh ‘000’

May 0 8000 3200

June 3200 6080 1280

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 19

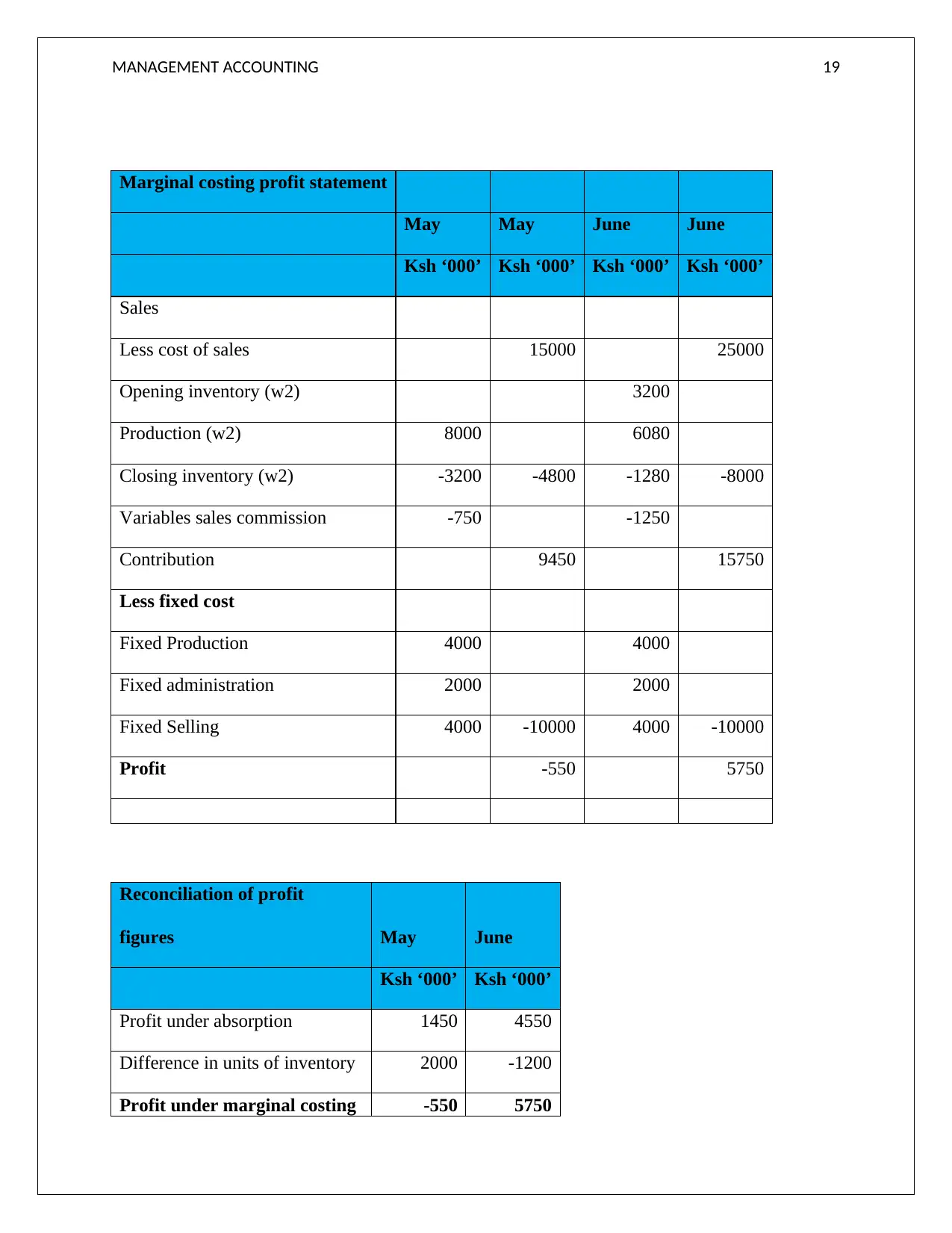

Marginal costing profit statement

May May June June

Ksh ‘000’ Ksh ‘000’ Ksh ‘000’ Ksh ‘000’

Sales

Less cost of sales 15000 25000

Opening inventory (w2) 3200

Production (w2) 8000 6080

Closing inventory (w2) -3200 -4800 -1280 -8000

Variables sales commission -750 -1250

Contribution 9450 15750

Less fixed cost

Fixed Production 4000 4000

Fixed administration 2000 2000

Fixed Selling 4000 -10000 4000 -10000

Profit -550 5750

Reconciliation of profit

figures May June

Ksh ‘000’ Ksh ‘000’

Profit under absorption 1450 4550

Difference in units of inventory 2000 -1200

Profit under marginal costing -550 5750

Marginal costing profit statement

May May June June

Ksh ‘000’ Ksh ‘000’ Ksh ‘000’ Ksh ‘000’

Sales

Less cost of sales 15000 25000

Opening inventory (w2) 3200

Production (w2) 8000 6080

Closing inventory (w2) -3200 -4800 -1280 -8000

Variables sales commission -750 -1250

Contribution 9450 15750

Less fixed cost

Fixed Production 4000 4000

Fixed administration 2000 2000

Fixed Selling 4000 -10000 4000 -10000

Profit -550 5750

Reconciliation of profit

figures May June

Ksh ‘000’ Ksh ‘000’

Profit under absorption 1450 4550

Difference in units of inventory 2000 -1200

Profit under marginal costing -550 5750

MANAGEMENT ACCOUNTING 20

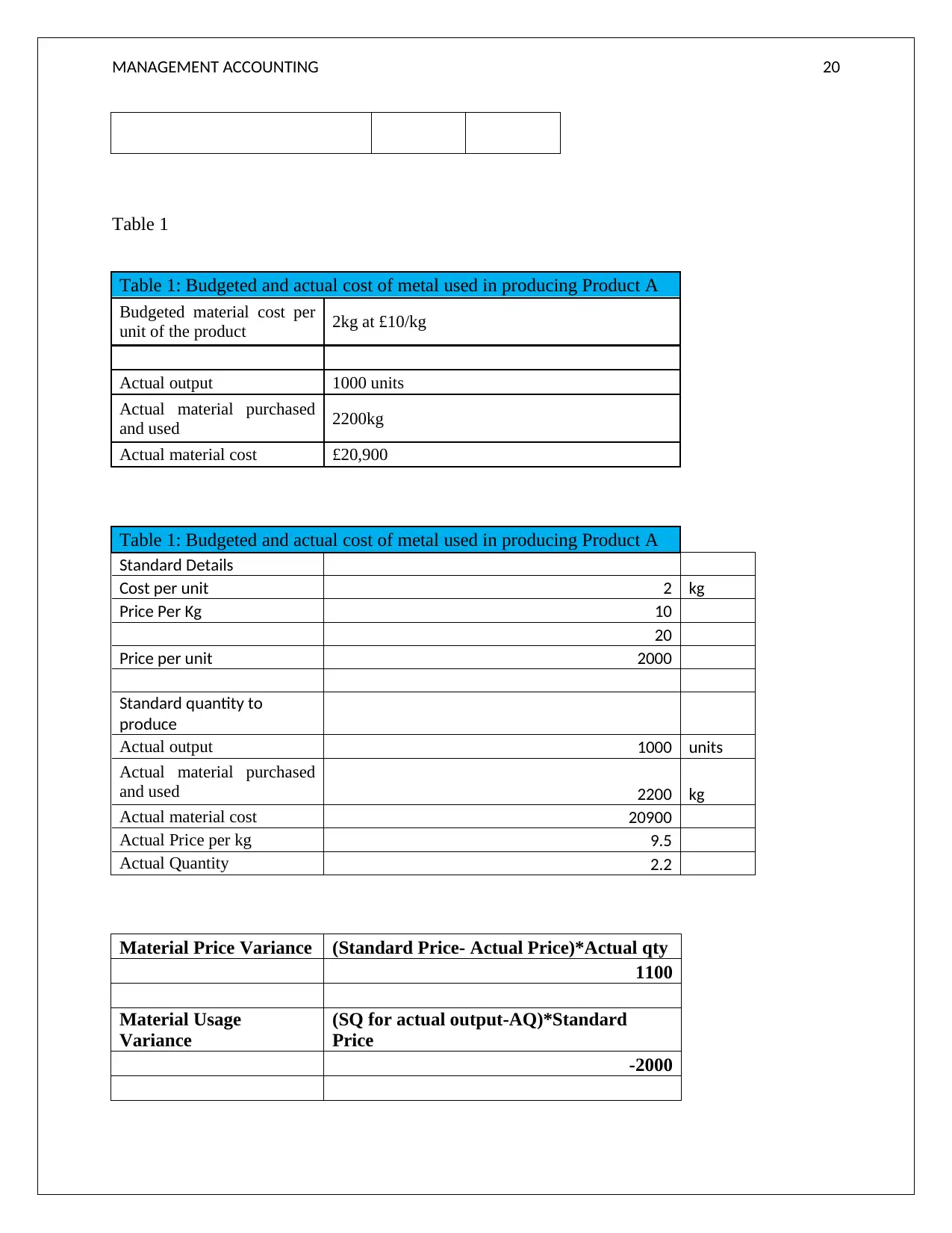

Table 1

Table 1: Budgeted and actual cost of metal used in producing Product A

Budgeted material cost per

unit of the product 2kg at £10/kg

Actual output 1000 units

Actual material purchased

and used 2200kg

Actual material cost £20,900

Table 1: Budgeted and actual cost of metal used in producing Product A

Standard Details

Cost per unit 2 kg

Price Per Kg 10

20

Price per unit 2000

Standard quantity to

produce

Actual output 1000 units

Actual material purchased

and used 2200 kg

Actual material cost 20900

Actual Price per kg 9.5

Actual Quantity 2.2

Material Price Variance (Standard Price- Actual Price)*Actual qty

1100

Material Usage

Variance

(SQ for actual output-AQ)*Standard

Price

-2000

Table 1

Table 1: Budgeted and actual cost of metal used in producing Product A

Budgeted material cost per

unit of the product 2kg at £10/kg

Actual output 1000 units

Actual material purchased

and used 2200kg

Actual material cost £20,900

Table 1: Budgeted and actual cost of metal used in producing Product A

Standard Details

Cost per unit 2 kg

Price Per Kg 10

20

Price per unit 2000

Standard quantity to

produce

Actual output 1000 units

Actual material purchased

and used 2200 kg

Actual material cost 20900

Actual Price per kg 9.5

Actual Quantity 2.2

Material Price Variance (Standard Price- Actual Price)*Actual qty

1100

Material Usage

Variance

(SQ for actual output-AQ)*Standard

Price

-2000

MANAGEMENT ACCOUNTING 21

Material Cost Variance

Standard cost for actual output- Actual

Cost

-900

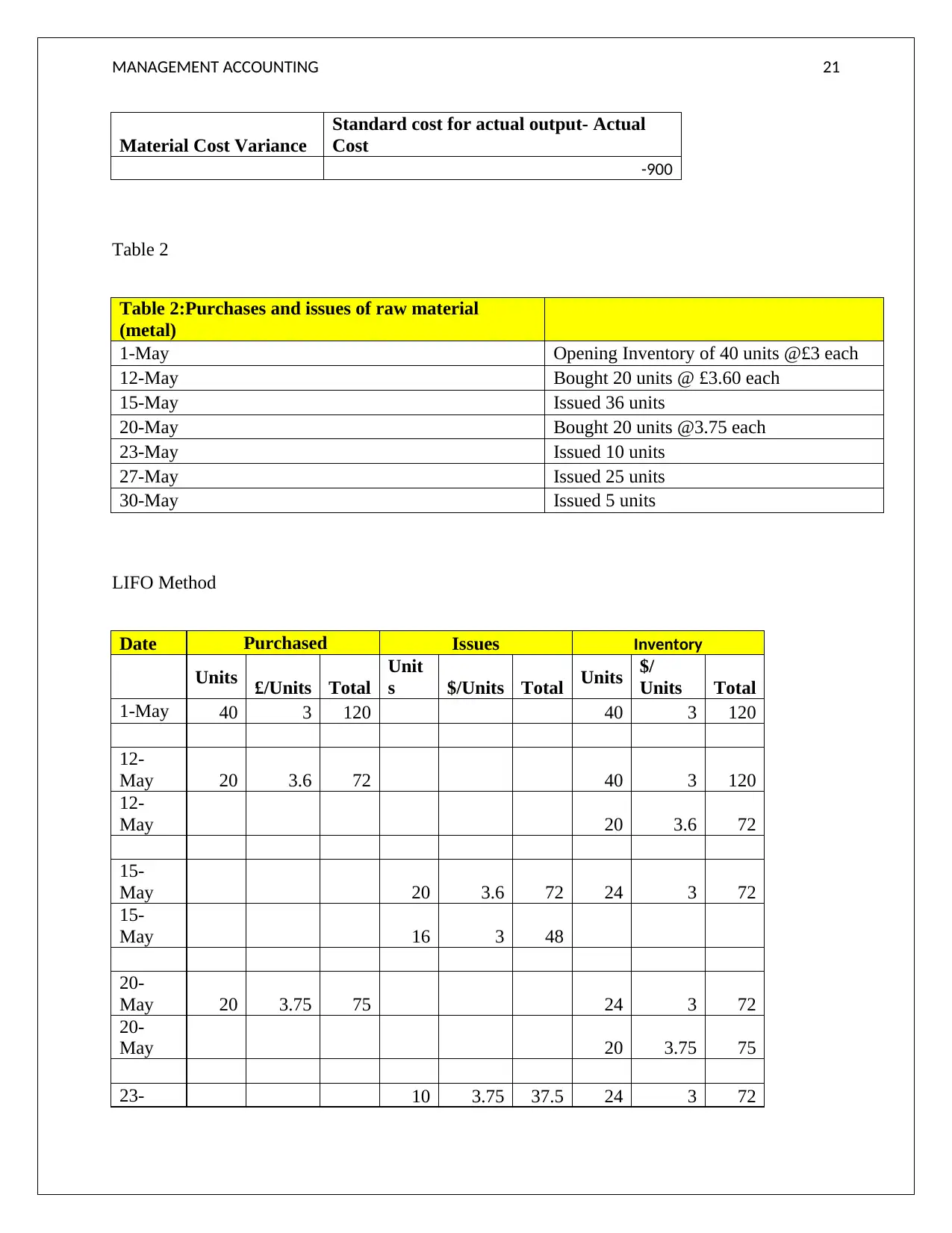

Table 2

Table 2:Purchases and issues of raw material

(metal)

1-May Opening Inventory of 40 units @£3 each

12-May Bought 20 units @ £3.60 each

15-May Issued 36 units

20-May Bought 20 units @3.75 each

23-May Issued 10 units

27-May Issued 25 units

30-May Issued 5 units

LIFO Method

Date Purchased Issues Inventory

Units £/Units Total

Unit

s $/Units Total Units $/

Units Total

1-May 40 3 120 40 3 120

12-

May 20 3.6 72 40 3 120

12-

May 20 3.6 72

15-

May 20 3.6 72 24 3 72

15-

May 16 3 48

20-

May 20 3.75 75 24 3 72

20-

May 20 3.75 75

23- 10 3.75 37.5 24 3 72

Material Cost Variance

Standard cost for actual output- Actual

Cost

-900

Table 2

Table 2:Purchases and issues of raw material

(metal)

1-May Opening Inventory of 40 units @£3 each

12-May Bought 20 units @ £3.60 each

15-May Issued 36 units

20-May Bought 20 units @3.75 each

23-May Issued 10 units

27-May Issued 25 units

30-May Issued 5 units

LIFO Method

Date Purchased Issues Inventory

Units £/Units Total

Unit

s $/Units Total Units $/

Units Total

1-May 40 3 120 40 3 120

12-

May 20 3.6 72 40 3 120

12-

May 20 3.6 72

15-

May 20 3.6 72 24 3 72

15-

May 16 3 48

20-

May 20 3.75 75 24 3 72

20-

May 20 3.75 75

23- 10 3.75 37.5 24 3 72

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 22

May

23-

May 10 3.75 37.5

27-

May 10 3.75 37.5 9 3 27

27-

May 15 3 45

30-

May 5 3 15 4 3 12

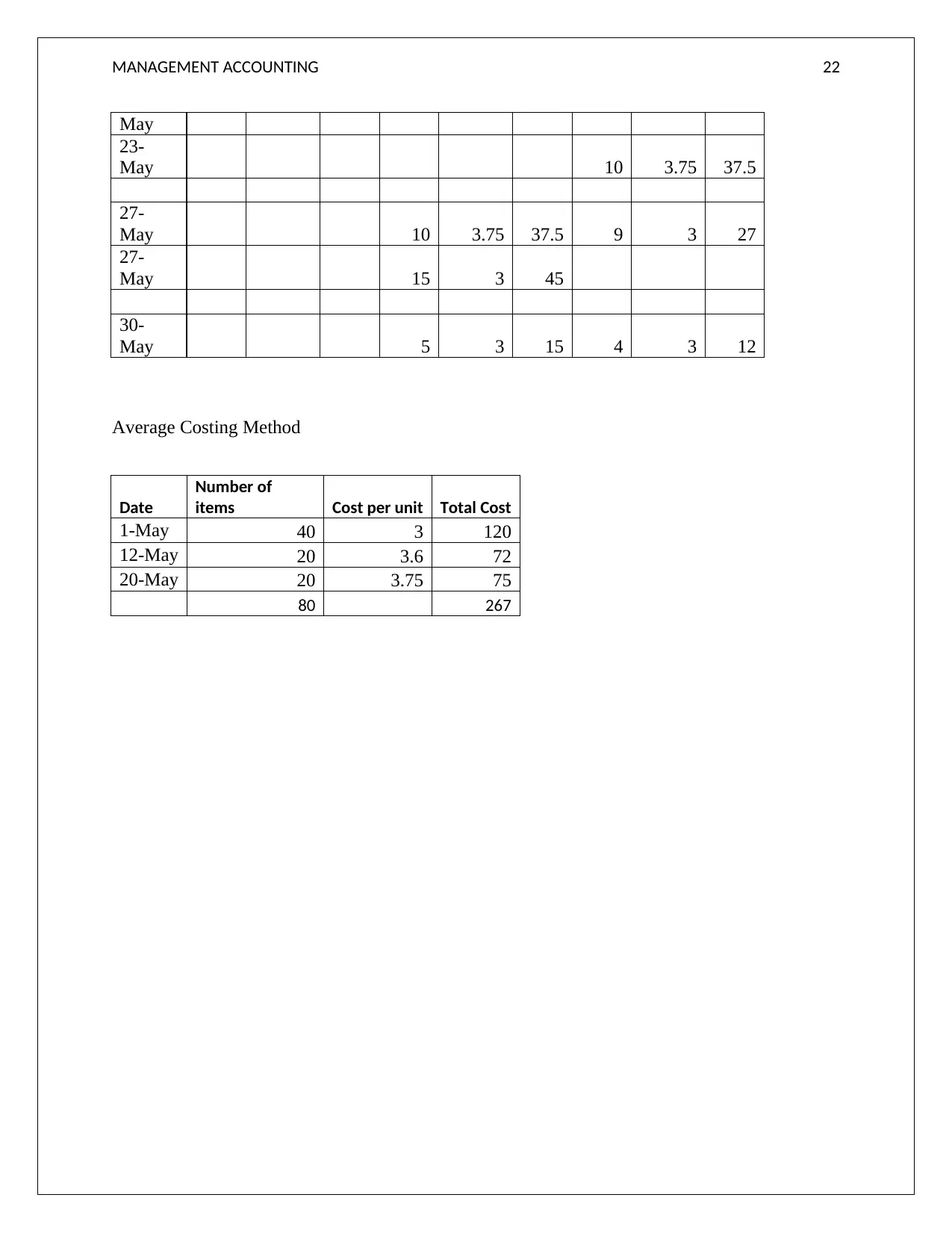

Average Costing Method

Date

Number of

items Cost per unit Total Cost

1-May 40 3 120

12-May 20 3.6 72

20-May 20 3.75 75

80 267

May

23-

May 10 3.75 37.5

27-

May 10 3.75 37.5 9 3 27

27-

May 15 3 45

30-

May 5 3 15 4 3 12

Average Costing Method

Date

Number of

items Cost per unit Total Cost

1-May 40 3 120

12-May 20 3.6 72

20-May 20 3.75 75

80 267

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.