Management Accounting Report: Techniques for Financial Success

VerifiedAdded on 2019/12/18

|9

|2031

|262

Report

AI Summary

This report delves into management accounting, focusing on cost analysis techniques like marginal and absorption costing. It examines budgetary control methods, comparing their advantages and disadvantages. The report uses Return on Capital Employed (ROCE) and operating profit margin to assess financial performance of UCK Furniture and its competitor, UCK Woodworks. It analyzes how management accounting systems aid companies in achieving success, emphasizing tools like budgetary control, project evaluation, standard costing, cost variances, and ratio analysis. The report concludes by highlighting the importance of these tools in enhancing efficiency and improving profitability for effective decision-making in the financial sector, with specific reference to the case study of UCK Furniture and UCK Woodworks.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Calculating costs using marginal and absorption costing.....................................................3

1.2 Applying range of management accounting techniques ......................................................4

1.3 Interpretation of the data.......................................................................................................4

TASK 2............................................................................................................................................5

2.1 Advantages and Disadvantages of different types of budgetary control...............................5

TASK 3............................................................................................................................................5

3.1 Comparing how organisations are adopting management accounting systems to respond to

financial problems.......................................................................................................................5

3.2 Analysing management accounting can help both the companies to achieve success..........6

3.3 Evaluating the planning tools used by the companies to reduce the financial problems......6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Calculating costs using marginal and absorption costing.....................................................3

1.2 Applying range of management accounting techniques ......................................................4

1.3 Interpretation of the data.......................................................................................................4

TASK 2............................................................................................................................................5

2.1 Advantages and Disadvantages of different types of budgetary control...............................5

TASK 3............................................................................................................................................5

3.1 Comparing how organisations are adopting management accounting systems to respond to

financial problems.......................................................................................................................5

3.2 Analysing management accounting can help both the companies to achieve success..........6

3.3 Evaluating the planning tools used by the companies to reduce the financial problems......6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Management accounting can be defined as per the Institute of Management Accounting

that it is a profession that deals with management decision-making, expertise in formulation and

implementation of strategies and assist management in planning and performance of

management. UCK Furniture is a well renowned company of UK which is engaged in a business

of manufacturing furniture products that is they manufacture in mainly two sectors which are

tables and drawers. This company is a well established firm having a huge turnover and popular

in the sector of satisfying customer to a great extent. This report specifies that UCK Furniture is

planning to start a training programme for new interns in September 2016.

TASK 1

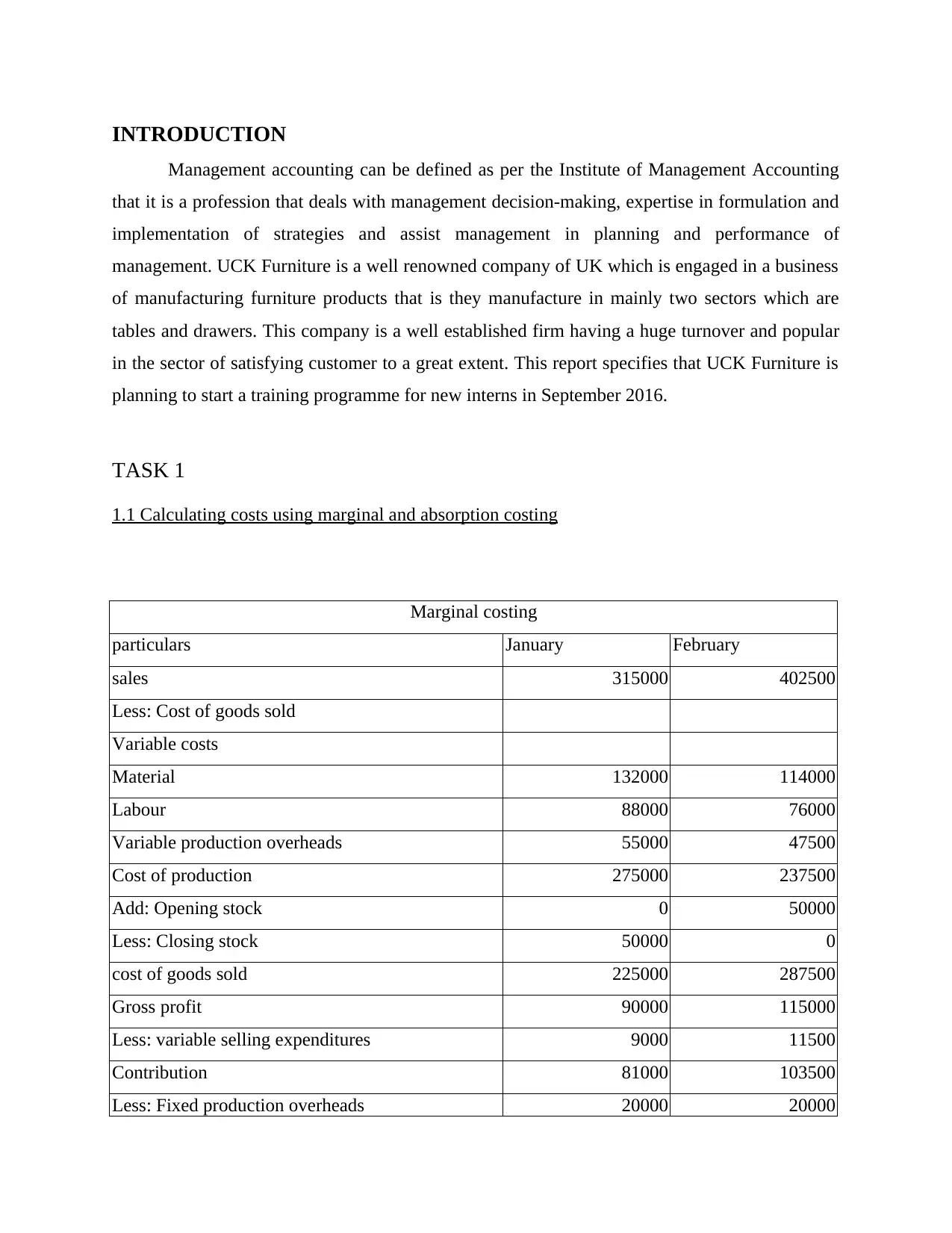

1.1 Calculating costs using marginal and absorption costing

Marginal costing

particulars January February

sales 315000 402500

Less: Cost of goods sold

Variable costs

Material 132000 114000

Labour 88000 76000

Variable production overheads 55000 47500

Cost of production 275000 237500

Add: Opening stock 0 50000

Less: Closing stock 50000 0

cost of goods sold 225000 287500

Gross profit 90000 115000

Less: variable selling expenditures 9000 11500

Contribution 81000 103500

Less: Fixed production overheads 20000 20000

Management accounting can be defined as per the Institute of Management Accounting

that it is a profession that deals with management decision-making, expertise in formulation and

implementation of strategies and assist management in planning and performance of

management. UCK Furniture is a well renowned company of UK which is engaged in a business

of manufacturing furniture products that is they manufacture in mainly two sectors which are

tables and drawers. This company is a well established firm having a huge turnover and popular

in the sector of satisfying customer to a great extent. This report specifies that UCK Furniture is

planning to start a training programme for new interns in September 2016.

TASK 1

1.1 Calculating costs using marginal and absorption costing

Marginal costing

particulars January February

sales 315000 402500

Less: Cost of goods sold

Variable costs

Material 132000 114000

Labour 88000 76000

Variable production overheads 55000 47500

Cost of production 275000 237500

Add: Opening stock 0 50000

Less: Closing stock 50000 0

cost of goods sold 225000 287500

Gross profit 90000 115000

Less: variable selling expenditures 9000 11500

Contribution 81000 103500

Less: Fixed production overheads 20000 20000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

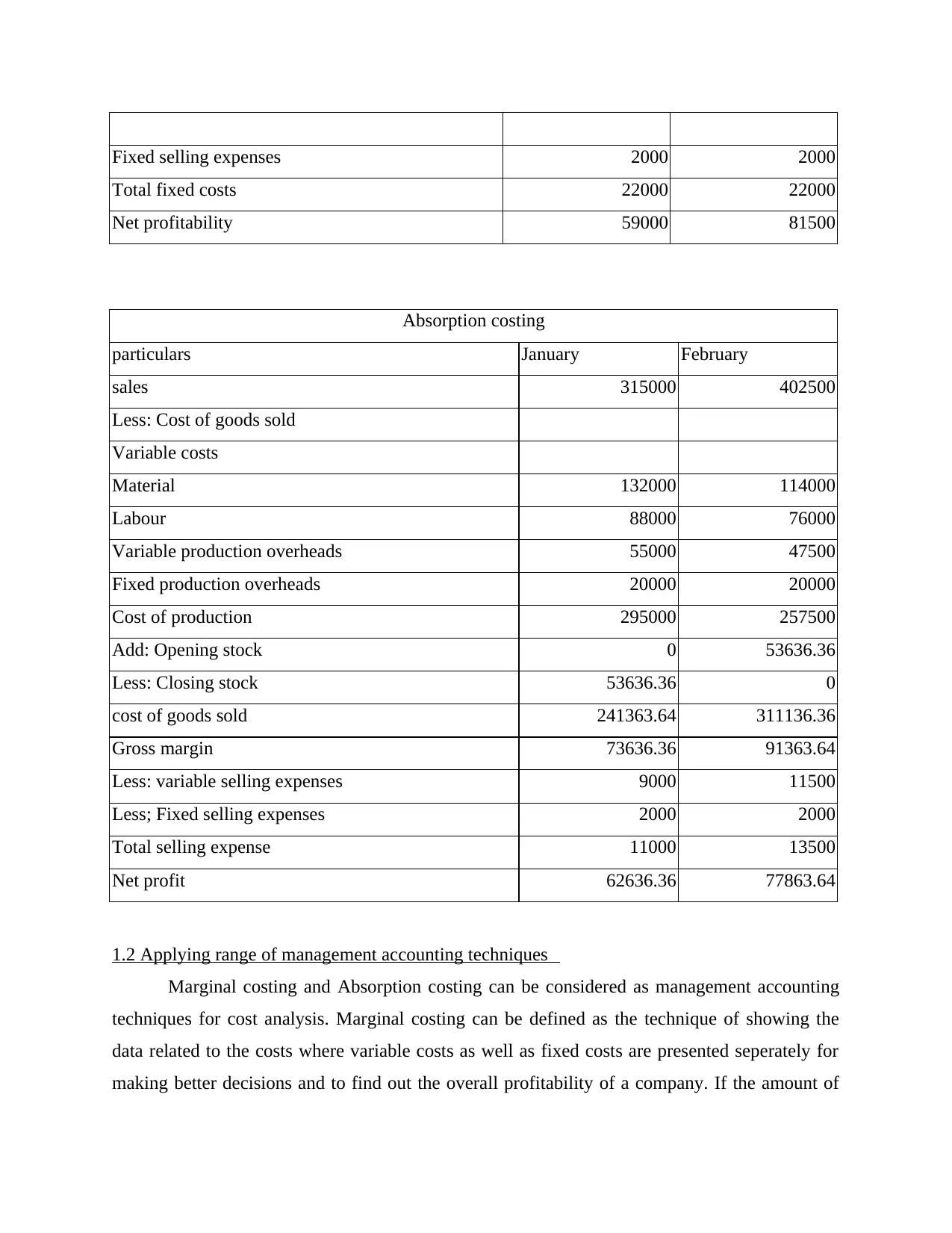

Fixed selling expenses 2000 2000

Total fixed costs 22000 22000

Net profitability 59000 81500

Absorption costing

particulars January February

sales 315000 402500

Less: Cost of goods sold

Variable costs

Material 132000 114000

Labour 88000 76000

Variable production overheads 55000 47500

Fixed production overheads 20000 20000

Cost of production 295000 257500

Add: Opening stock 0 53636.36

Less: Closing stock 53636.36 0

cost of goods sold 241363.64 311136.36

Gross margin 73636.36 91363.64

Less: variable selling expenses 9000 11500

Less; Fixed selling expenses 2000 2000

Total selling expense 11000 13500

Net profit 62636.36 77863.64

1.2 Applying range of management accounting techniques

Marginal costing and Absorption costing can be considered as management accounting

techniques for cost analysis. Marginal costing can be defined as the technique of showing the

data related to the costs where variable costs as well as fixed costs are presented seperately for

making better decisions and to find out the overall profitability of a company. If the amount of

Total fixed costs 22000 22000

Net profitability 59000 81500

Absorption costing

particulars January February

sales 315000 402500

Less: Cost of goods sold

Variable costs

Material 132000 114000

Labour 88000 76000

Variable production overheads 55000 47500

Fixed production overheads 20000 20000

Cost of production 295000 257500

Add: Opening stock 0 53636.36

Less: Closing stock 53636.36 0

cost of goods sold 241363.64 311136.36

Gross margin 73636.36 91363.64

Less: variable selling expenses 9000 11500

Less; Fixed selling expenses 2000 2000

Total selling expense 11000 13500

Net profit 62636.36 77863.64

1.2 Applying range of management accounting techniques

Marginal costing and Absorption costing can be considered as management accounting

techniques for cost analysis. Marginal costing can be defined as the technique of showing the

data related to the costs where variable costs as well as fixed costs are presented seperately for

making better decisions and to find out the overall profitability of a company. If the amount of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sales fall in a given period then the profit will automatically fall by the same amount. Fixed

production overheads are not considered in marginal costing so as to avoid the effect of varying

charges on each unit(Azizi and et.al, 2010, June.)

Absorption costing considers fixed overheads that is it considers both direct as well as indirect

cost to assess the profitability of the company. All expenses associated with the manufacturing of

a product are included in the absorption costing.

1.3 Interpretation of the data

As per the above data, it can be interpreted that absorption costing includes fixed

overheads unlike marginal costing that's why there is a difference in the profitability of marginal

and absorption costing. Because of the adjustment of the fixed overheads in both the techniques,

there is a difference in the valuation of opening and closing stock of both the months. In

marginal costing s tock is valued at 50000 but in the absorption costing stock is valued at

53636.36 because of the fixed charges of 2000.

TASK 2

2.1 Advantages and Disadvantages of different types of budgetary control

Bottom-up budgeting:

This budget contains the better information as employees themselves set the budget as

well as it enables better communication between the departments. Its disadvantage is that

decision-making is sometimes bad as it is taken by less experienced managers.

Top-down budgeting:

this budgeting has a greater advantage of better control of managers as budget is mainly

set by the senior managers (Managerial Accounting, 2012). Its disadvantage is that there is no

communication between the departments and top managers doesn't listen to the employees

regarding any complaints.

Zero-based budgeting:

Zero based budgeting are considered to be flexible budgets that is whenever we want to

change anything in our budget in future it can be changed. But it has a shortcoming of resource

and time constraint. It takes a lot of time to be prepared which is a major drawback.

production overheads are not considered in marginal costing so as to avoid the effect of varying

charges on each unit(Azizi and et.al, 2010, June.)

Absorption costing considers fixed overheads that is it considers both direct as well as indirect

cost to assess the profitability of the company. All expenses associated with the manufacturing of

a product are included in the absorption costing.

1.3 Interpretation of the data

As per the above data, it can be interpreted that absorption costing includes fixed

overheads unlike marginal costing that's why there is a difference in the profitability of marginal

and absorption costing. Because of the adjustment of the fixed overheads in both the techniques,

there is a difference in the valuation of opening and closing stock of both the months. In

marginal costing s tock is valued at 50000 but in the absorption costing stock is valued at

53636.36 because of the fixed charges of 2000.

TASK 2

2.1 Advantages and Disadvantages of different types of budgetary control

Bottom-up budgeting:

This budget contains the better information as employees themselves set the budget as

well as it enables better communication between the departments. Its disadvantage is that

decision-making is sometimes bad as it is taken by less experienced managers.

Top-down budgeting:

this budgeting has a greater advantage of better control of managers as budget is mainly

set by the senior managers (Managerial Accounting, 2012). Its disadvantage is that there is no

communication between the departments and top managers doesn't listen to the employees

regarding any complaints.

Zero-based budgeting:

Zero based budgeting are considered to be flexible budgets that is whenever we want to

change anything in our budget in future it can be changed. But it has a shortcoming of resource

and time constraint. It takes a lot of time to be prepared which is a major drawback.

TASK 3

3.1 Comparing how organisations are adopting management accounting systems to respond to

financial problems

Return of capital employed(ROCE): Operating profit/ capital employed

UCK Furniture:

Design Division: 5890/23100 *100 = 25.5%

Gear Box Division: 3600/31930*100 = 11.27%

UCK Woodworks = 6955/81230*100= 8.56%

Operating Profit Margin: Operating income/ net sales

UCK Furniture:

Design Division: 5890/13000*100= 45.31%

Gear Box Division: 3600/24900*100= 14.46%

UCK Woodworks: 6955/15580*100= 44.64%

Interpretation:

As per the above calculations, UCK woodworks which is a competitor of UCK Furnitures has a

lower return on capital employed. Return on capital employed measures the profitability of the

organisation and helps in better decision making. Design Division of UCK Furniture has the

highest return on capital employed which is 25.5% followed by the Gear Box Division of UCK

Furniture. UCK woodworks has the lowest profitability so they have not adopted management

accounting systems in an efficient manner. But this is opposite in the operating profit margin as

UCK woodworks has the operating profit of 44.64%. Design division of UCK furniture has the

highest operating profit margin of around 45%. Gear Box Division of UCK Furniture has the

lowest operating profit margin. Therefore, Design Division of UCK furnitures has the highest

profitability and measures the highest performance.

3.2 Analysing management accounting can help both the companies to achieve success

Management accounting system helps the companies in achieving success as this system

provides financial expertise, skills and knowledge related to the management in order to ensure

efficiency and effectiveness. It is considered as an effective tool for decision making in the

company which helps the managers of the companies to strive for success. Costs related to each

department, expenditures etc. are estimated and budget is made accordingly which will help both

3.1 Comparing how organisations are adopting management accounting systems to respond to

financial problems

Return of capital employed(ROCE): Operating profit/ capital employed

UCK Furniture:

Design Division: 5890/23100 *100 = 25.5%

Gear Box Division: 3600/31930*100 = 11.27%

UCK Woodworks = 6955/81230*100= 8.56%

Operating Profit Margin: Operating income/ net sales

UCK Furniture:

Design Division: 5890/13000*100= 45.31%

Gear Box Division: 3600/24900*100= 14.46%

UCK Woodworks: 6955/15580*100= 44.64%

Interpretation:

As per the above calculations, UCK woodworks which is a competitor of UCK Furnitures has a

lower return on capital employed. Return on capital employed measures the profitability of the

organisation and helps in better decision making. Design Division of UCK Furniture has the

highest return on capital employed which is 25.5% followed by the Gear Box Division of UCK

Furniture. UCK woodworks has the lowest profitability so they have not adopted management

accounting systems in an efficient manner. But this is opposite in the operating profit margin as

UCK woodworks has the operating profit of 44.64%. Design division of UCK furniture has the

highest operating profit margin of around 45%. Gear Box Division of UCK Furniture has the

lowest operating profit margin. Therefore, Design Division of UCK furnitures has the highest

profitability and measures the highest performance.

3.2 Analysing management accounting can help both the companies to achieve success

Management accounting system helps the companies in achieving success as this system

provides financial expertise, skills and knowledge related to the management in order to ensure

efficiency and effectiveness. It is considered as an effective tool for decision making in the

company which helps the managers of the companies to strive for success. Costs related to each

department, expenditures etc. are estimated and budget is made accordingly which will help both

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the companies to survive in the market. Their actual costs should be compared to the standard

costs to maintain profitability(Macintosh and et.al, 2010)

UCK Furnitures and UCK woodworks both the companies adopt management accounting

systems to achieve success in the market. Management accounting system helps the companies

in improving liquidity in the organisation. UCK Furniture deals with two different divisions and

UCK woodwork is the competitor of the UCK furniture and both the companies adopt

management accounting systems then also UCK furniture is more profitable on the basis of the

financial tools used.

Management accounting system used by the companies also increases financial returns as

they are the best tool to be considered for decision making. This helps in achieving success for

the organisation as better decisions ultimately leads to success(Fullerton and et.al, 2013)

3.3 Evaluating the planning tools used by the companies to reduce the financial problems

Budgetary control:

This tool is used by the organisation in order to predict future requirements and these

future needs are arranged in such a manner so as to take decisions effectively. This technique is

used to analyse the performances of the business and all the budgets are prepared in a desired

manner. These standard costs are compared to the actual costs in order to analyse the profitability

of the company to achieve success.

Project Evaluation:

This tool is used by the management to assess the overall project efficiency. Its main

objective is to check the level of effectiveness as well as sustainability. Project should be

properly evaluated and checked by the manager so as to formulate policies and procedures to

achieve success.

Standard costing:

Standard costing is another important tool used by the companies in order to analyse

predetermined cost in the organisation. This cost is then compared with the actual costs incurred

in the manufacturing organisation like material, labour, overhead costs. Standard costing is used

to find out the reasons of the deviations(Cinquini and et.al, 2010.)

Cost Variances:

Cost variances helps the managers to correct and control the variations from the standard

costs. They act as a very useful tool in achieving success by analysing the variations. It helps

costs to maintain profitability(Macintosh and et.al, 2010)

UCK Furnitures and UCK woodworks both the companies adopt management accounting

systems to achieve success in the market. Management accounting system helps the companies

in improving liquidity in the organisation. UCK Furniture deals with two different divisions and

UCK woodwork is the competitor of the UCK furniture and both the companies adopt

management accounting systems then also UCK furniture is more profitable on the basis of the

financial tools used.

Management accounting system used by the companies also increases financial returns as

they are the best tool to be considered for decision making. This helps in achieving success for

the organisation as better decisions ultimately leads to success(Fullerton and et.al, 2013)

3.3 Evaluating the planning tools used by the companies to reduce the financial problems

Budgetary control:

This tool is used by the organisation in order to predict future requirements and these

future needs are arranged in such a manner so as to take decisions effectively. This technique is

used to analyse the performances of the business and all the budgets are prepared in a desired

manner. These standard costs are compared to the actual costs in order to analyse the profitability

of the company to achieve success.

Project Evaluation:

This tool is used by the management to assess the overall project efficiency. Its main

objective is to check the level of effectiveness as well as sustainability. Project should be

properly evaluated and checked by the manager so as to formulate policies and procedures to

achieve success.

Standard costing:

Standard costing is another important tool used by the companies in order to analyse

predetermined cost in the organisation. This cost is then compared with the actual costs incurred

in the manufacturing organisation like material, labour, overhead costs. Standard costing is used

to find out the reasons of the deviations(Cinquini and et.al, 2010.)

Cost Variances:

Cost variances helps the managers to correct and control the variations from the standard

costs. They act as a very useful tool in achieving success by analysing the variations. It helps

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial managers to detect the deviations by considering different types of variances like profit

volume variance, material cost variance, labour cost variance etc(Zimmerman and et.al, 2011.)

Ratio Analysis:

This tool is used by the management in order to carry out different functions of planning,

forecasting, evaluating and analysing the financial statements. It helps the managers in reducing

financial problems by estimating the sales and profit in advance and to meet different targets.

CONCLUSION

As per the current study on management accounting it considers the concept of

management accounting that why it is useful for the managers to achieve success in the

organisation and improve profitability. UCK furnitures has adopted various tools and techniques

for decision making. Standard costing, ratio analysis, cost of variance analysis, budgeting etc.

has been used to improve an efficiency. Management accounting systems have been adopted by

the organisations to reduce various costs, and to increase the financial returns.

volume variance, material cost variance, labour cost variance etc(Zimmerman and et.al, 2011.)

Ratio Analysis:

This tool is used by the management in order to carry out different functions of planning,

forecasting, evaluating and analysing the financial statements. It helps the managers in reducing

financial problems by estimating the sales and profit in advance and to meet different targets.

CONCLUSION

As per the current study on management accounting it considers the concept of

management accounting that why it is useful for the managers to achieve success in the

organisation and improve profitability. UCK furnitures has adopted various tools and techniques

for decision making. Standard costing, ratio analysis, cost of variance analysis, budgeting etc.

has been used to improve an efficiency. Management accounting systems have been adopted by

the organisations to reduce various costs, and to increase the financial returns.

REFERENCES

Books and Journals

Ajibolade and et.al, 2010. MANAGEMENT ACCOUNTING SYSTEMS, PERCEIVED

ENVIRONMENTAL UNCERTAINTY AND COMPANIES'PERFORMANCE IN

NIGERIA.International Journal of Academic Research, 2(1).

Azizi and et.al., 2010, June. Energy-performance tradeoffs in processor architecture and circuit

design: a marginal cost analysis. In ACM SIGARCH Computer Architecture News (Vol. 38,

No. 3, pp. 26-36). ACM.

Cinquini and et.al., 2010. Strategic management accounting and business strategy: a loose

coupling?. Journal of Accounting & organizational change, 6(2), pp.228-259.

DRURY and et.al., 2013. Management and cost accounting. Springer.

Fullerton and et.al 2013. Management accounting and control practices in a lean manufacturing

environment.Accounting, Organizations and Society. 38(1), pp.50-71.

Gupta and et.al 2010. The implications of absorption cost accounting and production decisions

for future firm performance and valuation. Contemporary Accounting Research, 27(3),

pp.889-922.

Kaplan and et.al., 2015. Advanced management accounting. PHI Learning.

Macintosh and et.al., 2010. Management accounting and control systems: An organizational and

sociological approach. John Wiley & Sons.

Ward, K., 2012. Strategic management accounting. Routledge.

Zimmerman and et.al., 2011. Accounting for decision making and control. Issues in Accounting

Education, 26(1), pp.258-259.

Online

Managerial Accounting. 2012. [Online]. Available through:

<http://fisher.jsc.vsc.edu/manacct/wk23_ops_budgeting.html>. [Accessed on 9th May

2017].

Books and Journals

Ajibolade and et.al, 2010. MANAGEMENT ACCOUNTING SYSTEMS, PERCEIVED

ENVIRONMENTAL UNCERTAINTY AND COMPANIES'PERFORMANCE IN

NIGERIA.International Journal of Academic Research, 2(1).

Azizi and et.al., 2010, June. Energy-performance tradeoffs in processor architecture and circuit

design: a marginal cost analysis. In ACM SIGARCH Computer Architecture News (Vol. 38,

No. 3, pp. 26-36). ACM.

Cinquini and et.al., 2010. Strategic management accounting and business strategy: a loose

coupling?. Journal of Accounting & organizational change, 6(2), pp.228-259.

DRURY and et.al., 2013. Management and cost accounting. Springer.

Fullerton and et.al 2013. Management accounting and control practices in a lean manufacturing

environment.Accounting, Organizations and Society. 38(1), pp.50-71.

Gupta and et.al 2010. The implications of absorption cost accounting and production decisions

for future firm performance and valuation. Contemporary Accounting Research, 27(3),

pp.889-922.

Kaplan and et.al., 2015. Advanced management accounting. PHI Learning.

Macintosh and et.al., 2010. Management accounting and control systems: An organizational and

sociological approach. John Wiley & Sons.

Ward, K., 2012. Strategic management accounting. Routledge.

Zimmerman and et.al., 2011. Accounting for decision making and control. Issues in Accounting

Education, 26(1), pp.258-259.

Online

Managerial Accounting. 2012. [Online]. Available through:

<http://fisher.jsc.vsc.edu/manacct/wk23_ops_budgeting.html>. [Accessed on 9th May

2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.