Management Accounting Budgeting Report and Financial Analysis

VerifiedAdded on 2020/05/16

|8

|1017

|333

Report

AI Summary

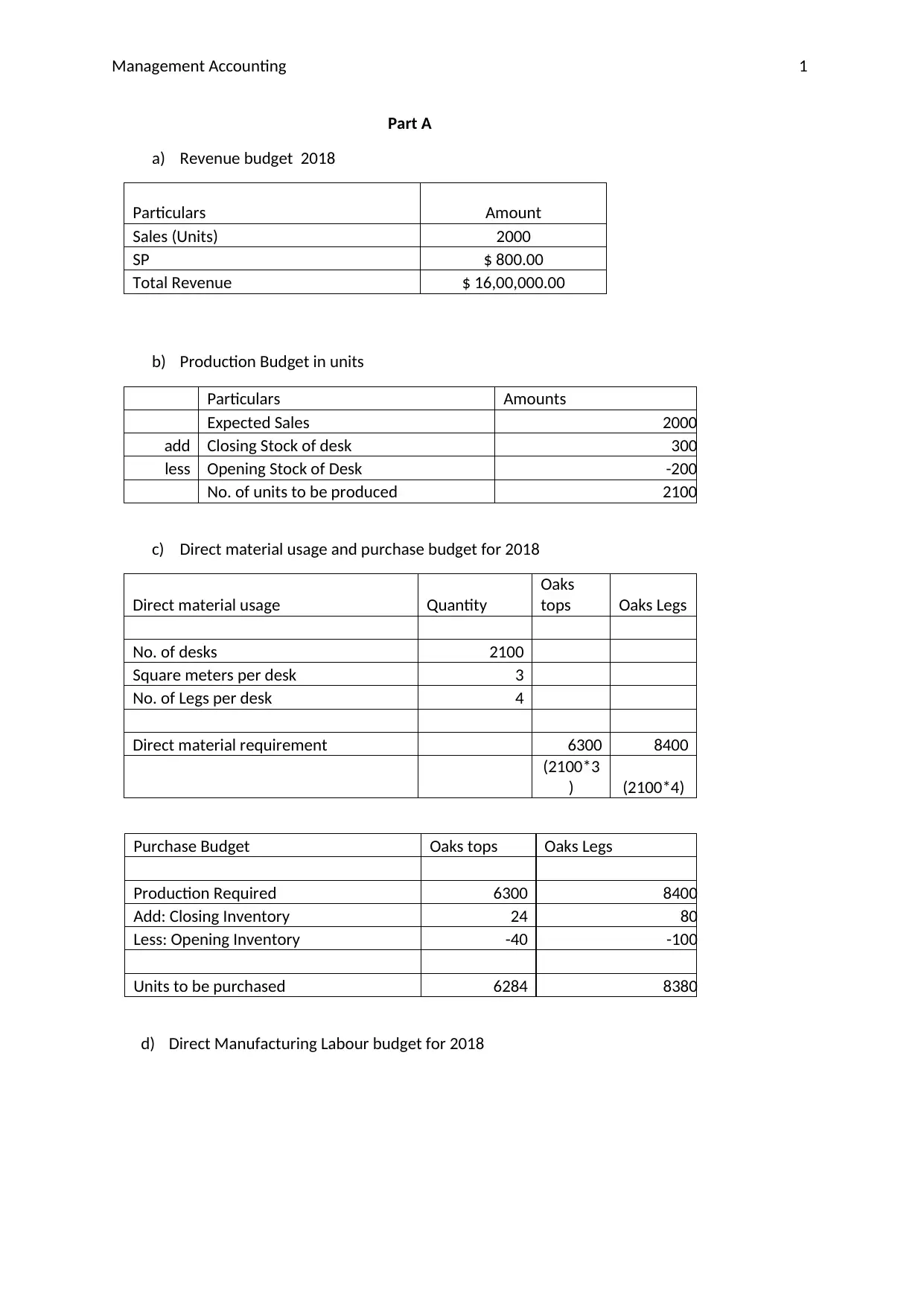

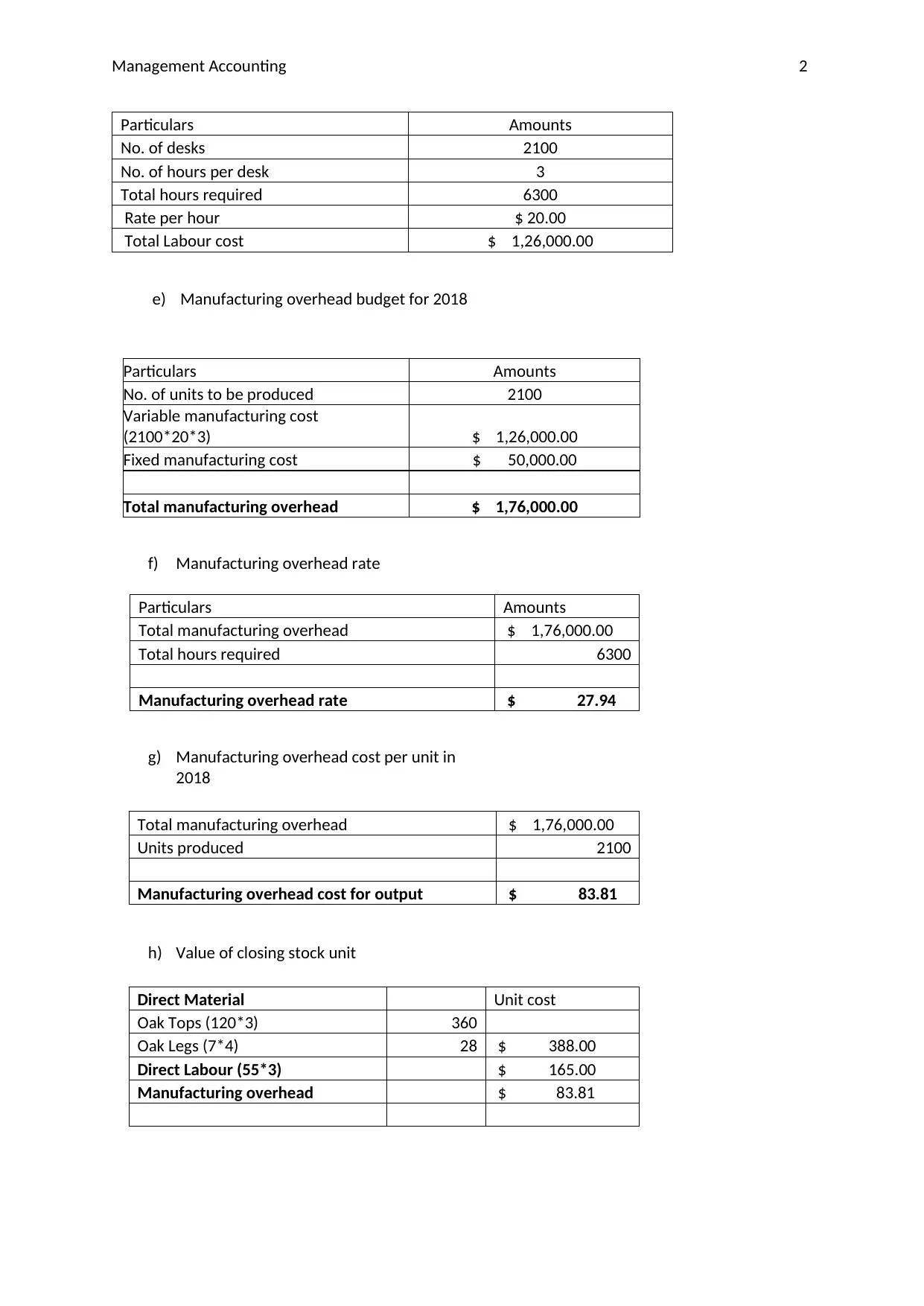

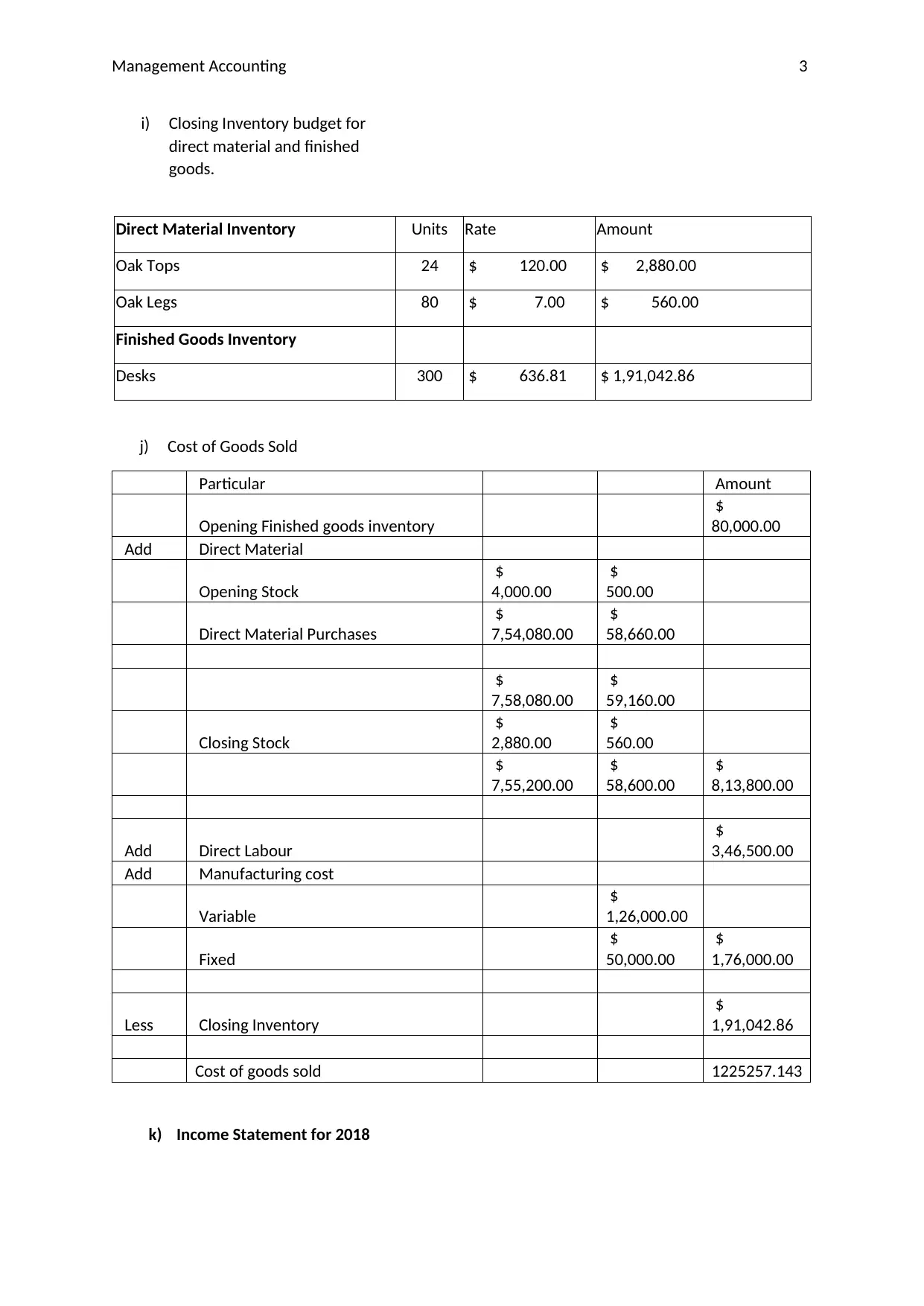

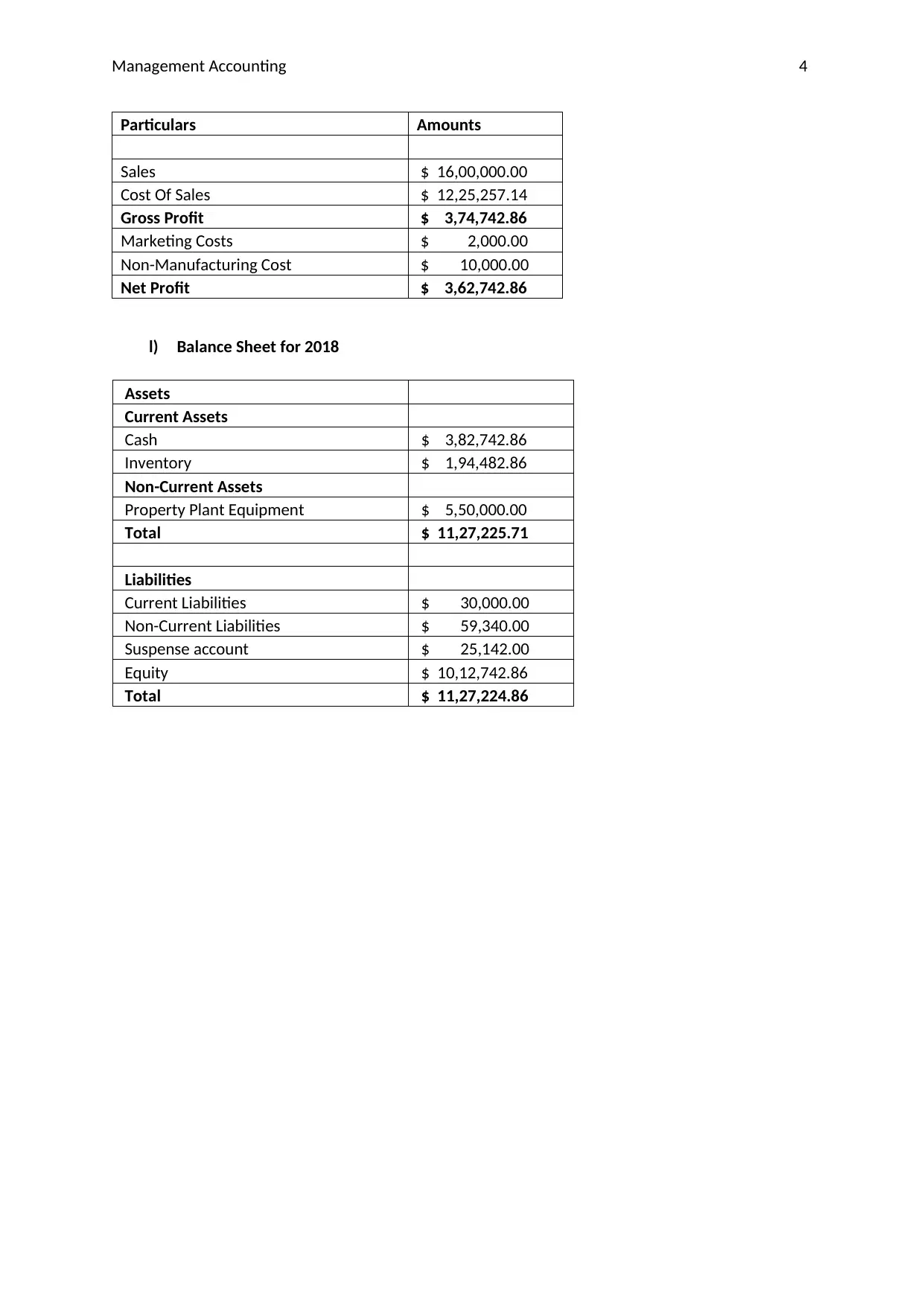

This report presents a detailed analysis of management accounting, focusing on budgeting for Exhibition Furniture. Part A includes the revenue, production, direct material usage and purchase, direct manufacturing labor, and manufacturing overhead budgets for 2018. It also covers the closing inventory budget, cost of goods sold, income statement, and balance sheet. Part B provides a memo to the manager, outlining strategies for cost reduction and increased profitability. These strategies include using machine-intensive production methods, increasing selling prices, reducing marketing costs through advertising, and optimizing inventory valuation and management. The report suggests implementing activity-based costing, just-in-time inventory maintenance, and determining the economic order quantity to enhance sales and overall financial performance. The analysis incorporates references to relevant management accounting literature.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.