Management Accounting Report: LSI Architects Case Study Analysis

VerifiedAdded on 2021/02/19

|16

|4279

|41

Report

AI Summary

This report delves into the intricacies of management accounting, focusing on LSI Architects (Design) Limited, a client of Equilibrium Asset Management. The assignment covers a range of topics, including management accounting systems like cost accounting, price optimization, and inventory management, along with their application and benefits. It explores various reporting methods and evaluates their integration within organizational processes. Furthermore, the report examines cost calculation techniques, such as marginal and absorption costing, and analyzes the application of different management accounting techniques. Planning tools used in budgetary control, including master budgets, are discussed, along with their advantages and disadvantages. The report also provides an interpretation of business activity data and concludes with an evaluation of how management accounting can contribute to sustainable organizational success. The report provides detailed calculations using different costing methods and explores how LSI Architects can use these tools to solve financial problems.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its systems which are essentially required...............................1

P2 Methods of management accounting reporting......................................................................2

M1 Benefits of systems used in management accounting with their application........................3

D1 Evaluation of management accounting systems and its reporting's integration within

organisational processes...............................................................................................................3

TASK 2............................................................................................................................................4

P3 Calculating cost by using appropriate techniques in cost analysis.........................................4

M2 Application of range of management accounting techniques...............................................7

D2 Interpretation of data of business activities............................................................................7

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of planning tools used in budgetary control.........................8

M3 Use of different planning tools and application of them in preparing and forecasting

budgets.......................................................................................................................................10

TASK 4..........................................................................................................................................10

P5 Comparison of application of management accounting system by different organisations to

respond financial problems........................................................................................................10

M4 The way in which management accounting can lead organisations to sustainable success12

D3 Use of planning tools in solving financial problems to lead organisation towards

sustainable success.....................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its systems which are essentially required...............................1

P2 Methods of management accounting reporting......................................................................2

M1 Benefits of systems used in management accounting with their application........................3

D1 Evaluation of management accounting systems and its reporting's integration within

organisational processes...............................................................................................................3

TASK 2............................................................................................................................................4

P3 Calculating cost by using appropriate techniques in cost analysis.........................................4

M2 Application of range of management accounting techniques...............................................7

D2 Interpretation of data of business activities............................................................................7

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of planning tools used in budgetary control.........................8

M3 Use of different planning tools and application of them in preparing and forecasting

budgets.......................................................................................................................................10

TASK 4..........................................................................................................................................10

P5 Comparison of application of management accounting system by different organisations to

respond financial problems........................................................................................................10

M4 The way in which management accounting can lead organisations to sustainable success12

D3 Use of planning tools in solving financial problems to lead organisation towards

sustainable success.....................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is a technique of keeping record of internal environment of the

organisation and it is also known as managerial accounting. With the help of it managers try to

analyse that the efforts which were made by them to reach predetermined goals are resulting

positively or negatively (Alyousef and Mickan, 2016). This report is based upon LSI Architects

(Design) Limited which is a client of Equilibrium Asset Management a medium sized financial

consultant established in United Kingdom. This assignment covers various topics such as

management accounting system and methods for their reporting, calculation of costs with the

help of different costing techniques and use of planning tools in management accounting. Along

with this, use of all the management accounting systems in respond to financial problems is also

covered under this project.

TASK 1

P1 Management accounting and its systems which are essentially required

Management accounting: The process which is used by managers of the business

entities to determine that organisation is performing well or not is known as management

accounting. There are various types of systems which are used by management of LSI

Architects (Design) Limited in order to execute business activities in appropriate manner.

Description of all of them is as follows:

Cost accounting system: It can be defined as a framework which is used by different

companies to determine cost of different products or services which are delivered to clients. In

LSI Architects managers are using this system to estimate accurate cost of different buildings

which are constructed according to requirements of customers. Essential requirements of it for

the organisation is that it helps to analyse up to date information regarding expenses which are

related to different operations (Azmitov and Korabelnikova, 2015).

Price optimisation system: It is a system which guides organisations to set best suitable

price for all the products or services which are sold to clients. Managers in LSI Architects

Limited are using it for the purpose of setting such rates for all its services so that higher profits

could be generated by fulfilling requirements of customers. Essential requirement of it for the

company is that it guides top level executives to make sure that they set optimum prices for all

facilities so that objectives such as profit maximisation and customer satisfaction could be met.

1

Management accounting is a technique of keeping record of internal environment of the

organisation and it is also known as managerial accounting. With the help of it managers try to

analyse that the efforts which were made by them to reach predetermined goals are resulting

positively or negatively (Alyousef and Mickan, 2016). This report is based upon LSI Architects

(Design) Limited which is a client of Equilibrium Asset Management a medium sized financial

consultant established in United Kingdom. This assignment covers various topics such as

management accounting system and methods for their reporting, calculation of costs with the

help of different costing techniques and use of planning tools in management accounting. Along

with this, use of all the management accounting systems in respond to financial problems is also

covered under this project.

TASK 1

P1 Management accounting and its systems which are essentially required

Management accounting: The process which is used by managers of the business

entities to determine that organisation is performing well or not is known as management

accounting. There are various types of systems which are used by management of LSI

Architects (Design) Limited in order to execute business activities in appropriate manner.

Description of all of them is as follows:

Cost accounting system: It can be defined as a framework which is used by different

companies to determine cost of different products or services which are delivered to clients. In

LSI Architects managers are using this system to estimate accurate cost of different buildings

which are constructed according to requirements of customers. Essential requirements of it for

the organisation is that it helps to analyse up to date information regarding expenses which are

related to different operations (Azmitov and Korabelnikova, 2015).

Price optimisation system: It is a system which guides organisations to set best suitable

price for all the products or services which are sold to clients. Managers in LSI Architects

Limited are using it for the purpose of setting such rates for all its services so that higher profits

could be generated by fulfilling requirements of customers. Essential requirement of it for the

company is that it guides top level executives to make sure that they set optimum prices for all

facilities so that objectives such as profit maximisation and customer satisfaction could be met.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system: It can be defined as a system which is used by

companies for different activities such as monitoring, evaluating and overseeing processes which

are conducted for management of stock used for business operations. In LSI Architects all the

managers are using it to keep track record of materiel which is used by the company to construct

buildings. Essential requirement of it for the organisation is that it guides management to be

aware of actual status of stock so that material could be ordered on right time (Boiral, 2016).

There are three different types of it which are as follows:

LIFO: In this method of inventory management recently received goods are used for

business operations, therefore it is called Last in First Out.

FIFO: While using this method of inventory management managers use earlier received

inventory for business execution, hence it is called First in First Out.

AVCO: In this method all the goods are used by organisation on the basis of their

average cost for business activities so it is called Average Cost Method of inventory

management.

From all the above described methods management in LSI Architects Limited are using

FIFO method to manage inventory. One of the main reason behind using it is no effect of

purchases at the end of the period on net income and cost of goods sold.

P2 Methods of management accounting reporting

Management accounting reporting: Managers follow specific procedures to prepare

management reports which is known as management accounting reporting. There are various

types of reports that are generated by managers in LSI Architects to analyse that business is able

to reach long term goals or not. All of them are described below in detail:

Performance report: In most of the business entities this type of report is generated by

managers for the purpose of analysing that operation and staff members are performing

appropriately or not. In LSI Architects Limited management generate it to monitor that

all the employees are working productively or not so that organisational goals could be

achieved. It is beneficial for the company because with the help of it decisions for the

betterment of enterprise could be formed if the performance of business is very low

(Campanale and Cinquini, 2016).

Inventory management report: It ca be defined as a report which covers detailed

information regarding goods which are utilised by organisations to perform all the

2

companies for different activities such as monitoring, evaluating and overseeing processes which

are conducted for management of stock used for business operations. In LSI Architects all the

managers are using it to keep track record of materiel which is used by the company to construct

buildings. Essential requirement of it for the organisation is that it guides management to be

aware of actual status of stock so that material could be ordered on right time (Boiral, 2016).

There are three different types of it which are as follows:

LIFO: In this method of inventory management recently received goods are used for

business operations, therefore it is called Last in First Out.

FIFO: While using this method of inventory management managers use earlier received

inventory for business execution, hence it is called First in First Out.

AVCO: In this method all the goods are used by organisation on the basis of their

average cost for business activities so it is called Average Cost Method of inventory

management.

From all the above described methods management in LSI Architects Limited are using

FIFO method to manage inventory. One of the main reason behind using it is no effect of

purchases at the end of the period on net income and cost of goods sold.

P2 Methods of management accounting reporting

Management accounting reporting: Managers follow specific procedures to prepare

management reports which is known as management accounting reporting. There are various

types of reports that are generated by managers in LSI Architects to analyse that business is able

to reach long term goals or not. All of them are described below in detail:

Performance report: In most of the business entities this type of report is generated by

managers for the purpose of analysing that operation and staff members are performing

appropriately or not. In LSI Architects Limited management generate it to monitor that

all the employees are working productively or not so that organisational goals could be

achieved. It is beneficial for the company because with the help of it decisions for the

betterment of enterprise could be formed if the performance of business is very low

(Campanale and Cinquini, 2016).

Inventory management report: It ca be defined as a report which covers detailed

information regarding goods which are utilised by organisations to perform all the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

operational activities. In LSI Architects Limited management create it to keep track

record of stock which is used to construct buildings. It is advantageous for the entity

because it can guides managers to check requirement of goods to fulfil needs of

customers.

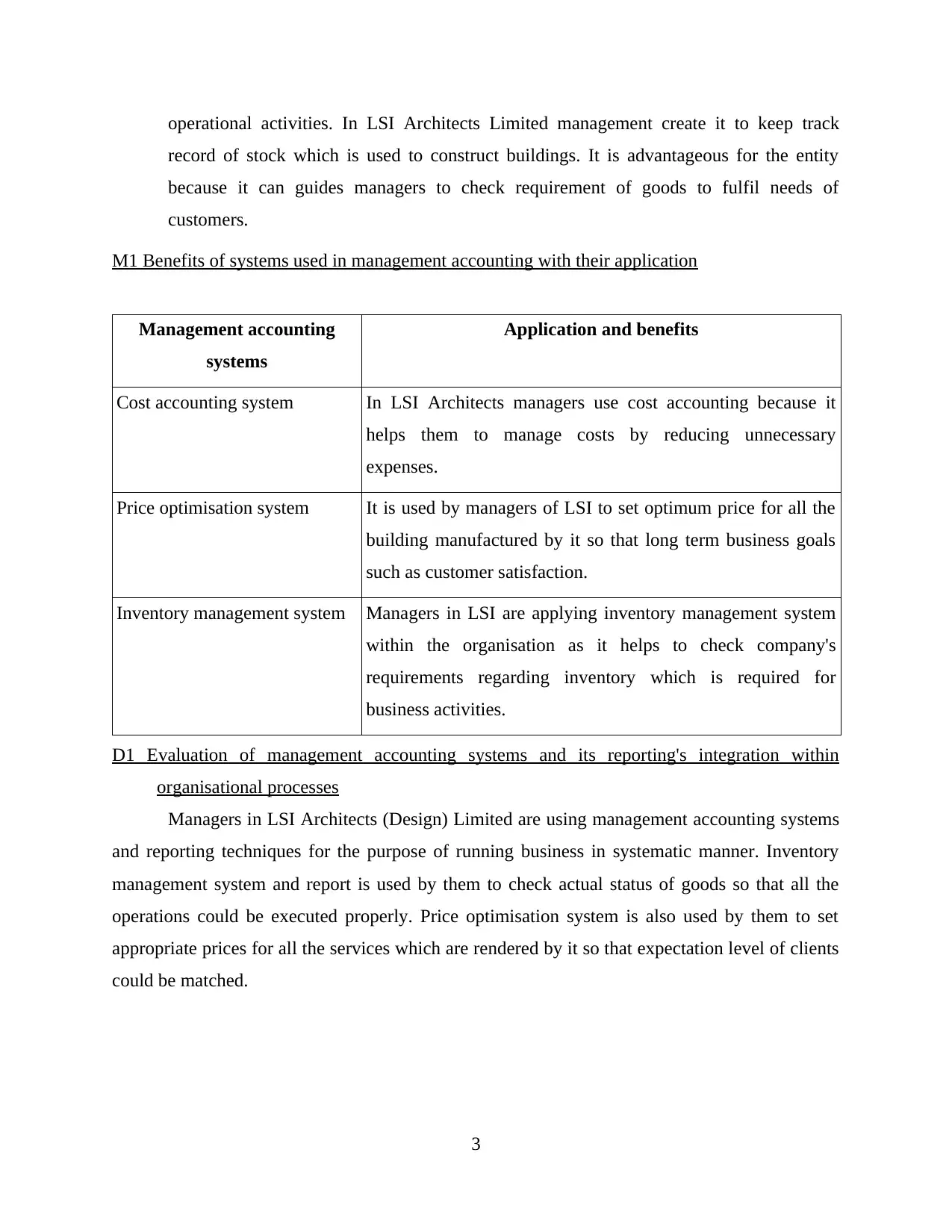

M1 Benefits of systems used in management accounting with their application

Management accounting

systems

Application and benefits

Cost accounting system In LSI Architects managers use cost accounting because it

helps them to manage costs by reducing unnecessary

expenses.

Price optimisation system It is used by managers of LSI to set optimum price for all the

building manufactured by it so that long term business goals

such as customer satisfaction.

Inventory management system Managers in LSI are applying inventory management system

within the organisation as it helps to check company's

requirements regarding inventory which is required for

business activities.

D1 Evaluation of management accounting systems and its reporting's integration within

organisational processes

Managers in LSI Architects (Design) Limited are using management accounting systems

and reporting techniques for the purpose of running business in systematic manner. Inventory

management system and report is used by them to check actual status of goods so that all the

operations could be executed properly. Price optimisation system is also used by them to set

appropriate prices for all the services which are rendered by it so that expectation level of clients

could be matched.

3

record of stock which is used to construct buildings. It is advantageous for the entity

because it can guides managers to check requirement of goods to fulfil needs of

customers.

M1 Benefits of systems used in management accounting with their application

Management accounting

systems

Application and benefits

Cost accounting system In LSI Architects managers use cost accounting because it

helps them to manage costs by reducing unnecessary

expenses.

Price optimisation system It is used by managers of LSI to set optimum price for all the

building manufactured by it so that long term business goals

such as customer satisfaction.

Inventory management system Managers in LSI are applying inventory management system

within the organisation as it helps to check company's

requirements regarding inventory which is required for

business activities.

D1 Evaluation of management accounting systems and its reporting's integration within

organisational processes

Managers in LSI Architects (Design) Limited are using management accounting systems

and reporting techniques for the purpose of running business in systematic manner. Inventory

management system and report is used by them to check actual status of goods so that all the

operations could be executed properly. Price optimisation system is also used by them to set

appropriate prices for all the services which are rendered by it so that expectation level of clients

could be matched.

3

TASK 2

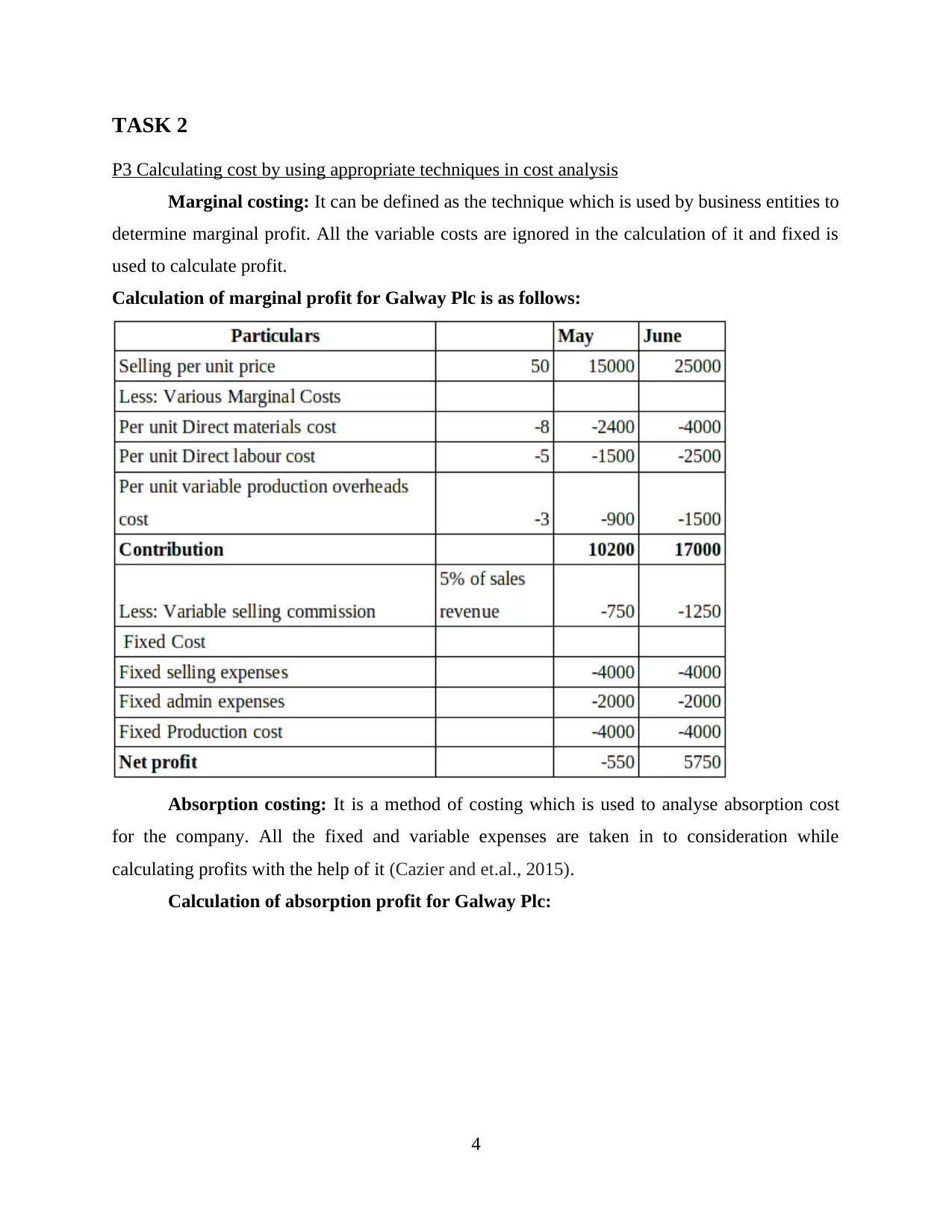

P3 Calculating cost by using appropriate techniques in cost analysis

Marginal costing: It can be defined as the technique which is used by business entities to

determine marginal profit. All the variable costs are ignored in the calculation of it and fixed is

used to calculate profit.

Calculation of marginal profit for Galway Plc is as follows:

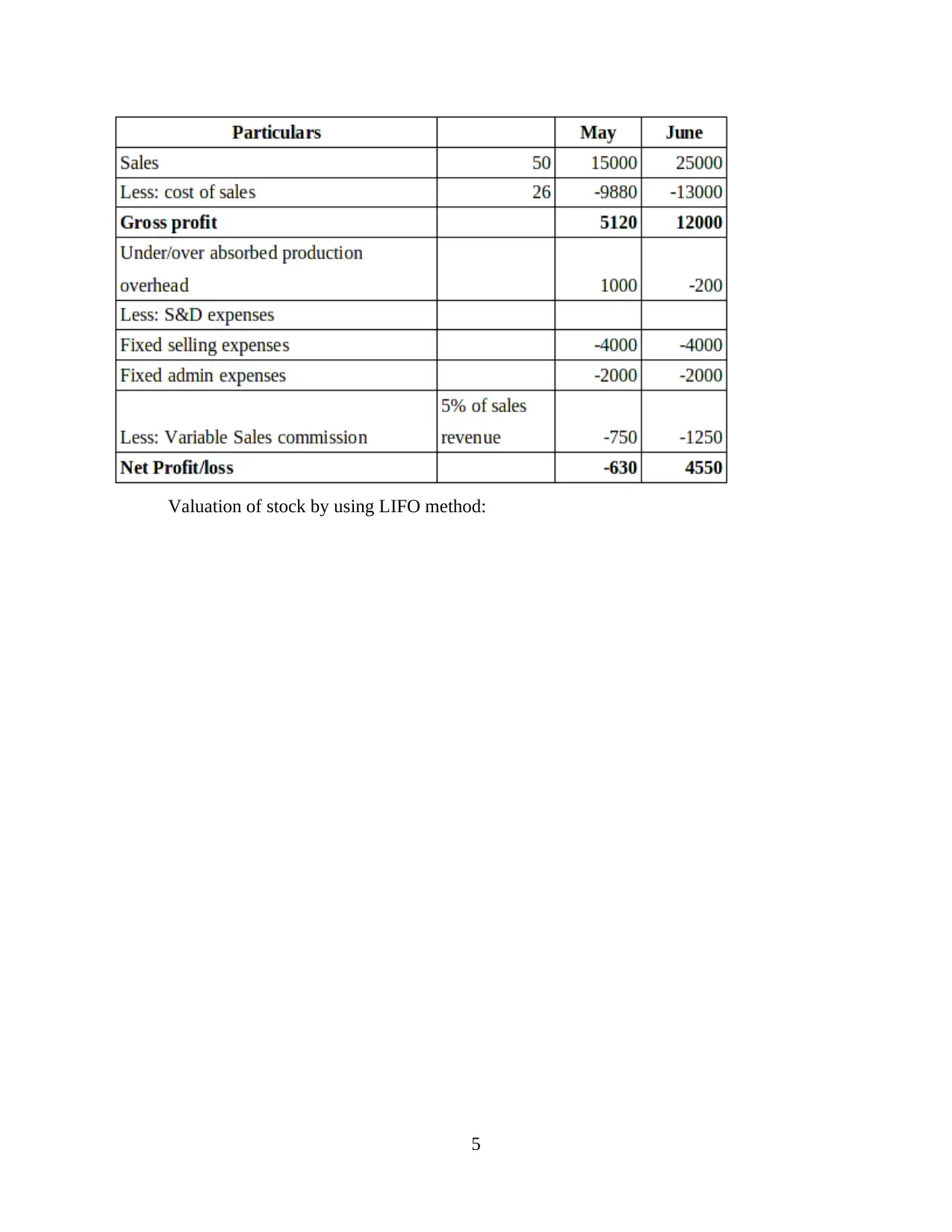

Absorption costing: It is a method of costing which is used to analyse absorption cost

for the company. All the fixed and variable expenses are taken in to consideration while

calculating profits with the help of it (Cazier and et.al., 2015).

Calculation of absorption profit for Galway Plc:

4

P3 Calculating cost by using appropriate techniques in cost analysis

Marginal costing: It can be defined as the technique which is used by business entities to

determine marginal profit. All the variable costs are ignored in the calculation of it and fixed is

used to calculate profit.

Calculation of marginal profit for Galway Plc is as follows:

Absorption costing: It is a method of costing which is used to analyse absorption cost

for the company. All the fixed and variable expenses are taken in to consideration while

calculating profits with the help of it (Cazier and et.al., 2015).

Calculation of absorption profit for Galway Plc:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

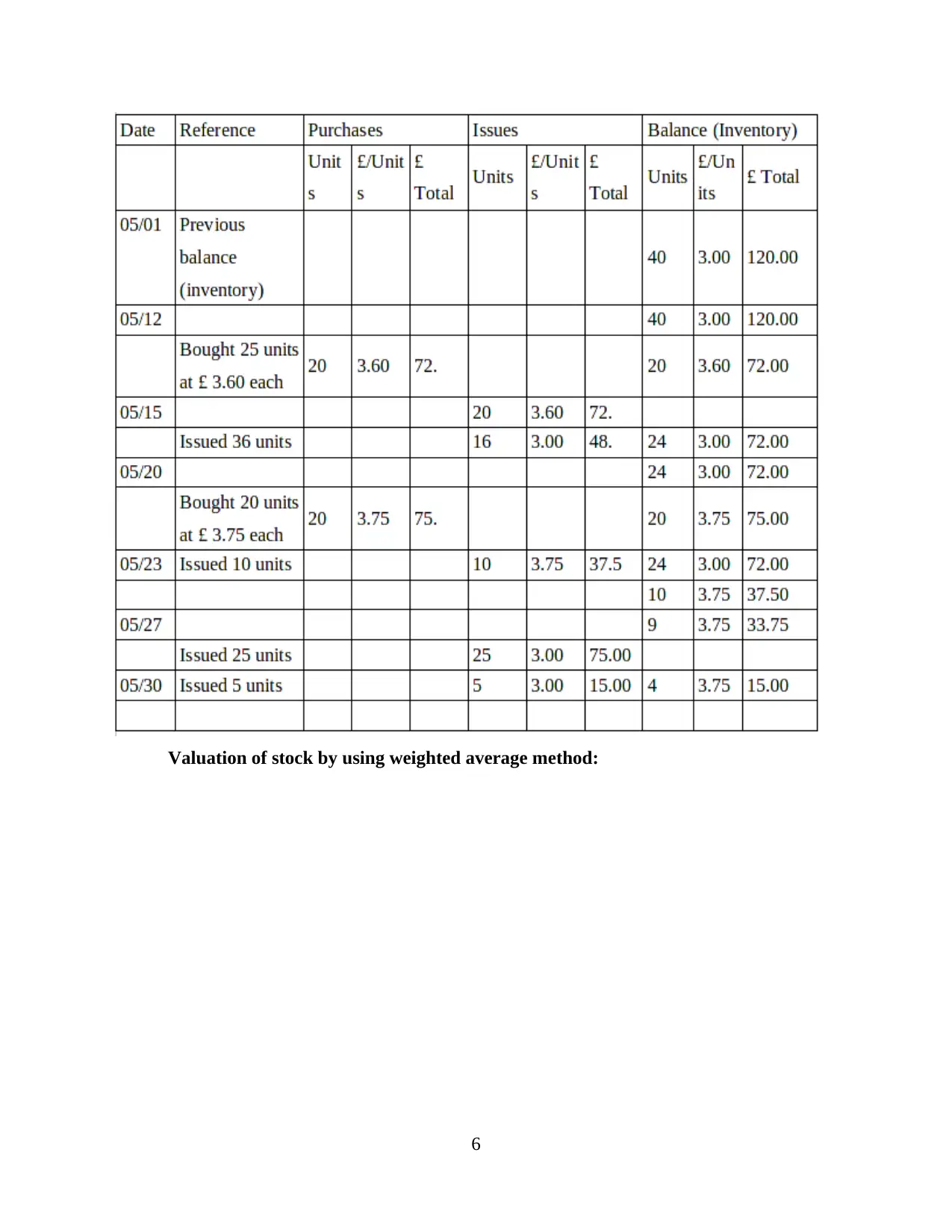

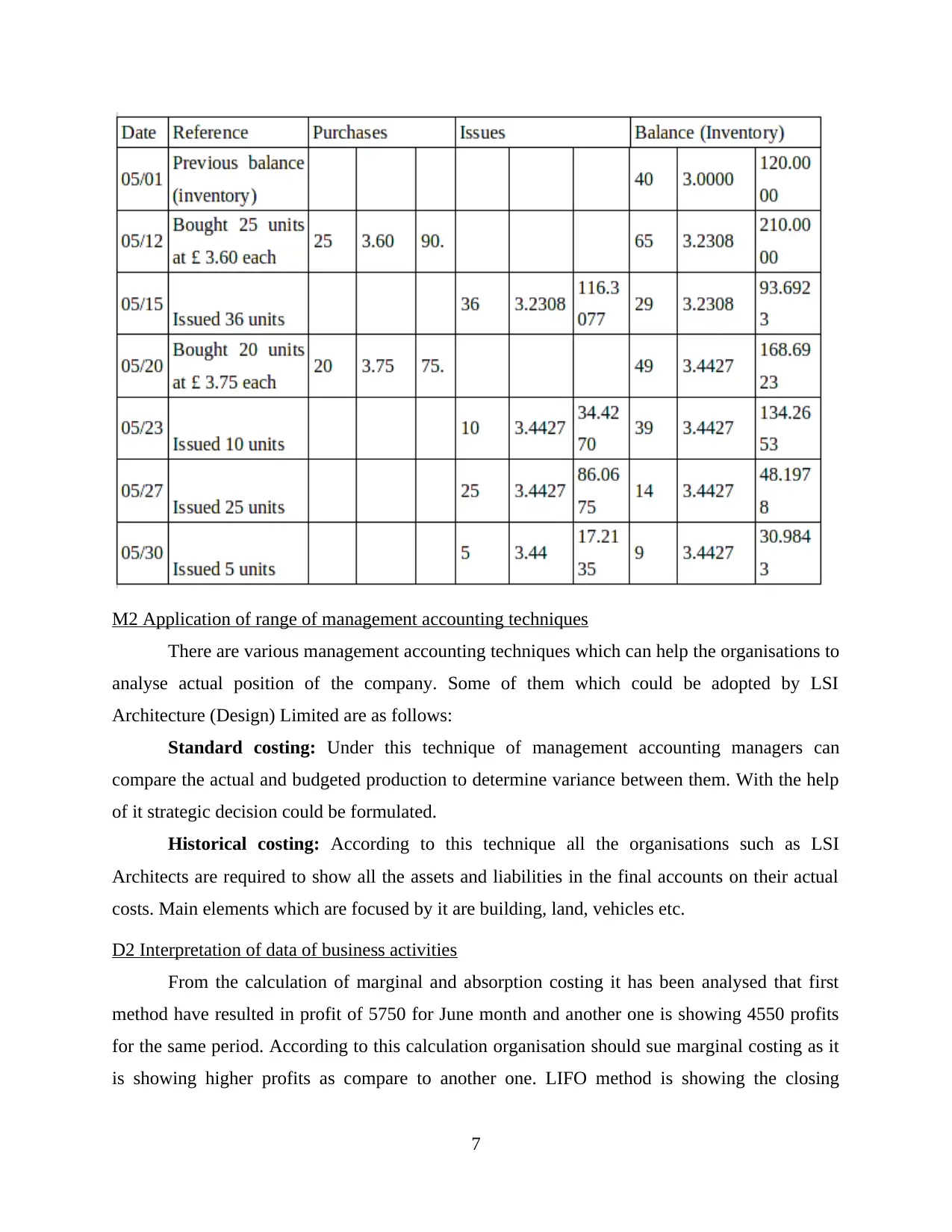

Valuation of stock by using LIFO method:

5

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Valuation of stock by using weighted average method:

6

6

M2 Application of range of management accounting techniques

There are various management accounting techniques which can help the organisations to

analyse actual position of the company. Some of them which could be adopted by LSI

Architecture (Design) Limited are as follows:

Standard costing: Under this technique of management accounting managers can

compare the actual and budgeted production to determine variance between them. With the help

of it strategic decision could be formulated.

Historical costing: According to this technique all the organisations such as LSI

Architects are required to show all the assets and liabilities in the final accounts on their actual

costs. Main elements which are focused by it are building, land, vehicles etc.

D2 Interpretation of data of business activities

From the calculation of marginal and absorption costing it has been analysed that first

method have resulted in profit of 5750 for June month and another one is showing 4550 profits

for the same period. According to this calculation organisation should sue marginal costing as it

is showing higher profits as compare to another one. LIFO method is showing the closing

7

There are various management accounting techniques which can help the organisations to

analyse actual position of the company. Some of them which could be adopted by LSI

Architecture (Design) Limited are as follows:

Standard costing: Under this technique of management accounting managers can

compare the actual and budgeted production to determine variance between them. With the help

of it strategic decision could be formulated.

Historical costing: According to this technique all the organisations such as LSI

Architects are required to show all the assets and liabilities in the final accounts on their actual

costs. Main elements which are focused by it are building, land, vehicles etc.

D2 Interpretation of data of business activities

From the calculation of marginal and absorption costing it has been analysed that first

method have resulted in profit of 5750 for June month and another one is showing 4550 profits

for the same period. According to this calculation organisation should sue marginal costing as it

is showing higher profits as compare to another one. LIFO method is showing the closing

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

balance of 15 pounds and weighted average method is showing the balance of 30.98. from both

the methods organisation should use weighted average method as it shows that higher cost bas

compare to LIFO.

TASK 3

P4 Advantages and disadvantages of planning tools used in budgetary control

Budget: It is a type of financial plan which is formulated by management of

organisations for future activities in order to reduce possibility of challenges such as lack of

monetary resources. In LSI Architecture managers are formulating budgets to execute all the

operational activities appropriately so that predetermined objectives could be achieved. Main

purpose of creating budget is to forecasting future requirements of funds for business and then

arranging them to run the operational procedures smoothly (Guenther and et.al., 2015).

Budgetary control: It is a process in which management of entities set performance and

financial goals for business by comparing current and previous situations. It is highly required

for organisations such as LSI Architects because it helps to reduce spendings which are not

required for business. Two main types of planning tools are used in it which are described below

in detail:

Master Budget: It can be defined as a budget which is a summary of all the functional

budgets which are generated by an organisation in a specific time period. The process of

formulating it is very complex as it documents different elements such as predicts sales for

future, purchased, expenses which may take place in upcoming period and production levels. In

LSI Architects (Design) Limited managers create it to reduce burden of internal stakeholders to

check end number of budgets. They can analyse it and gather information of all the other

financial plans to determine actual position of the company (Kalkhouran and et.al., 2015). For

example, with the help of master budget managers in LSI Architects (Design) Limited can make

sure that the opening stock and budgeted production is equal to actual sales or not. Advantages

and disadvantages of it for LSI Architects (Design) Limited are as follows:

Advantages: Master budget helps managers and other stakeholders to gather brief

information of all the other budgets as it is the summary of them. It provides bird's eye view of

the business which is beneficial for all the members to check actual position of the company so

that strategic decisions for future could be formulated. It guides all the top level executives to

8

the methods organisation should use weighted average method as it shows that higher cost bas

compare to LIFO.

TASK 3

P4 Advantages and disadvantages of planning tools used in budgetary control

Budget: It is a type of financial plan which is formulated by management of

organisations for future activities in order to reduce possibility of challenges such as lack of

monetary resources. In LSI Architecture managers are formulating budgets to execute all the

operational activities appropriately so that predetermined objectives could be achieved. Main

purpose of creating budget is to forecasting future requirements of funds for business and then

arranging them to run the operational procedures smoothly (Guenther and et.al., 2015).

Budgetary control: It is a process in which management of entities set performance and

financial goals for business by comparing current and previous situations. It is highly required

for organisations such as LSI Architects because it helps to reduce spendings which are not

required for business. Two main types of planning tools are used in it which are described below

in detail:

Master Budget: It can be defined as a budget which is a summary of all the functional

budgets which are generated by an organisation in a specific time period. The process of

formulating it is very complex as it documents different elements such as predicts sales for

future, purchased, expenses which may take place in upcoming period and production levels. In

LSI Architects (Design) Limited managers create it to reduce burden of internal stakeholders to

check end number of budgets. They can analyse it and gather information of all the other

financial plans to determine actual position of the company (Kalkhouran and et.al., 2015). For

example, with the help of master budget managers in LSI Architects (Design) Limited can make

sure that the opening stock and budgeted production is equal to actual sales or not. Advantages

and disadvantages of it for LSI Architects (Design) Limited are as follows:

Advantages: Master budget helps managers and other stakeholders to gather brief

information of all the other budgets as it is the summary of them. It provides bird's eye view of

the business which is beneficial for all the members to check actual position of the company so

that strategic decisions for future could be formulated. It guides all the top level executives to

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

form master plans for betterment of business and reach long term business goals by providing

brief information of current status of business to stakeholders.

Disadvantages: As it is a combination of different budgets so it is not able to specify

causes of all the expenses due to brief information of all of them. It is very difficult to read and

update master budget because of complexities in the formulation process of it. All the budgets

including master budget are based upon estimations so it can create uncertainty for business. It is

based upon certain assumptions which may not prove right over the period.

Cash Budget: It can be defined as a budget which is generated to record all the cash

transactions so that actual liquidity of business could be estimated. Main purpose of creating it is

to determine that the organisation is generating sufficient amount to execute business activities

smoothly or not. In LSI Architects (Design) Limited management focuses on formulation of it as

it helps to determine the monetary funds which are going to be received in upcoming period in

future. The figures which are recorded in it includes collected revenues, all the expenses which

are paid, receipts from debtors etc. In other words it could be defined as a plan which reflects

future position of business (Leotta, Rizza and Ruggeri, 2017). All the expenses such as

depreciation which are not faced by companies in monetary terms are not recorded in this

budget. For example, different types of receipts such as cash receipts, payment received from

buyers, and payments such as salaries, wages, lean, interest etc. could be analysed with the help

of cash budget. Some of its advantages and disadvantages are as follows:

Advantages: While formulating cash budget all the debts are ignored which helps the

organisation to analyse actual receipts and payments. As it records only cash transactions so it

make the company more resourceful which helps to spend more money to execute business

activities in more systematic manner. With the help of cash budget potential deficit for LSI

Architects (Design) Limited could be identified quickly by managers. It facilitates small as well

as large enterprises to communicate their financial position with internal and external

stakeholders as it helps to determine cash balance at the end of financial year.

Disadvantages: There is lack of flexibility in cash budget because if any modification is

made in any transaction then it is not possible to record it in the budget. It is based upon

estimations and it is not possible to trust them properly because it may get changed with time. It

could be manipulated by managers because they want that records should reflect position image

9

brief information of current status of business to stakeholders.

Disadvantages: As it is a combination of different budgets so it is not able to specify

causes of all the expenses due to brief information of all of them. It is very difficult to read and

update master budget because of complexities in the formulation process of it. All the budgets

including master budget are based upon estimations so it can create uncertainty for business. It is

based upon certain assumptions which may not prove right over the period.

Cash Budget: It can be defined as a budget which is generated to record all the cash

transactions so that actual liquidity of business could be estimated. Main purpose of creating it is

to determine that the organisation is generating sufficient amount to execute business activities

smoothly or not. In LSI Architects (Design) Limited management focuses on formulation of it as

it helps to determine the monetary funds which are going to be received in upcoming period in

future. The figures which are recorded in it includes collected revenues, all the expenses which

are paid, receipts from debtors etc. In other words it could be defined as a plan which reflects

future position of business (Leotta, Rizza and Ruggeri, 2017). All the expenses such as

depreciation which are not faced by companies in monetary terms are not recorded in this

budget. For example, different types of receipts such as cash receipts, payment received from

buyers, and payments such as salaries, wages, lean, interest etc. could be analysed with the help

of cash budget. Some of its advantages and disadvantages are as follows:

Advantages: While formulating cash budget all the debts are ignored which helps the

organisation to analyse actual receipts and payments. As it records only cash transactions so it

make the company more resourceful which helps to spend more money to execute business

activities in more systematic manner. With the help of cash budget potential deficit for LSI

Architects (Design) Limited could be identified quickly by managers. It facilitates small as well

as large enterprises to communicate their financial position with internal and external

stakeholders as it helps to determine cash balance at the end of financial year.

Disadvantages: There is lack of flexibility in cash budget because if any modification is

made in any transaction then it is not possible to record it in the budget. It is based upon

estimations and it is not possible to trust them properly because it may get changed with time. It

could be manipulated by managers because they want that records should reflect position image

9

of the company. In cash budget there is lack of non financial factors which creates barriers for

stakeholders to analyse contribution of them in organisational performance.

M3 Use of different planning tools and application of them in preparing and forecasting budgets

Different types of planning tools are used by managers of LSI Architects (Design)

Limited in order to prepare and forecast budget for the organisation. These are master and cash

budget. With the help of both of them management try to analyse actual situation of business and

then formulate strategic decisions for future. It helps them to be prepare to deal with

uncertainties which may take place in upcoming period and affect functionality of operations.

TASK 4

P5 Comparison of application of management accounting system by different organisations to

respond financial problems

Financial problems could be defined as such issues which are faced by companies due to

insufficient monetary resources. For all the companies such as LSI Architects (Design) Limited it

is very important to be aware of such situations which may create such types of challenges

(McLean, McGovern and Davie, 2015). All the finance related issues which are faced by the

organisation are as follows:

Improper money management system: When an organisation do not have experienced

and skilled staff members then they can make mistakes while recording funds in appropriate

accounts. This problem is also faced by LSI Architects (Design) Limited which creates financial

problem for it and affect the process of attainment of organisational goals.

Sudden expenses: Sometimes such expenses takes places which are not expected and

then companies have to spend money on them to reduce possibility of huge risks for business.

LSI Architects (Design) Limited is also dealing with this type of financial challenge which

results in lack of funds for future activities (McVay, Kennedy and Fullerton, 2016).

In order to identify both the above described problems managers in LSI Architects

(Design) Limited are using following techniques:

KPI (Key Performance Indicator): It is a type of technique which is used by business

entities to measure success or failure of different procedures which are conducted for attainment

of long term business goals. There are two main types of it which are financial and non financial

(KPI, 2019.).

10

stakeholders to analyse contribution of them in organisational performance.

M3 Use of different planning tools and application of them in preparing and forecasting budgets

Different types of planning tools are used by managers of LSI Architects (Design)

Limited in order to prepare and forecast budget for the organisation. These are master and cash

budget. With the help of both of them management try to analyse actual situation of business and

then formulate strategic decisions for future. It helps them to be prepare to deal with

uncertainties which may take place in upcoming period and affect functionality of operations.

TASK 4

P5 Comparison of application of management accounting system by different organisations to

respond financial problems

Financial problems could be defined as such issues which are faced by companies due to

insufficient monetary resources. For all the companies such as LSI Architects (Design) Limited it

is very important to be aware of such situations which may create such types of challenges

(McLean, McGovern and Davie, 2015). All the finance related issues which are faced by the

organisation are as follows:

Improper money management system: When an organisation do not have experienced

and skilled staff members then they can make mistakes while recording funds in appropriate

accounts. This problem is also faced by LSI Architects (Design) Limited which creates financial

problem for it and affect the process of attainment of organisational goals.

Sudden expenses: Sometimes such expenses takes places which are not expected and

then companies have to spend money on them to reduce possibility of huge risks for business.

LSI Architects (Design) Limited is also dealing with this type of financial challenge which

results in lack of funds for future activities (McVay, Kennedy and Fullerton, 2016).

In order to identify both the above described problems managers in LSI Architects

(Design) Limited are using following techniques:

KPI (Key Performance Indicator): It is a type of technique which is used by business

entities to measure success or failure of different procedures which are conducted for attainment

of long term business goals. There are two main types of it which are financial and non financial

(KPI, 2019.).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.