Management Accounting: Systems, Reporting, and Integration

29 Pages4421 Words90 Views

Added on 2022-12-26

About This Document

This document provides an overview of management accounting, including its systems, reporting methods, and integration within organizational processes. It discusses the essential requirements of management accounting systems, different methods of management accounting reporting, and the major benefits of these systems. The document also explores how management accounting is integrated within organizational processes and evaluates its importance. Additionally, it includes financial reporting examples and applies various management accounting techniques.

Management Accounting: Systems, Reporting, and Integration

Added on 2022-12-26

ShareRelated Documents

Management Accounting

INTRODUCTION

The terms management accounting is made up of two different terms: the management

and the accounting. This can be described as a mechanism that provides information tools to an

organization's managers to assist them in making decisions. It helps in managerial effectiveness

by presenting all relevant information and statistics to executives, enabling them to make

informed decisions and monitor all other aspects of the business (Ameen, Ahmed and Abd

Hafez, 2018). The study covers multiple tasks which covers different aspects of MA like systems

and reports of MA, key planning tools, ratio analysis and preparation of budget.

Section One

1.1 Management accounting and essential requirements of multiple forms of management

accounting systems:

Managerial accounting corresponds to vital practice of recognizing, assessing, interpreting,

evaluating and efficiently reporting key fiscal details about managerial personnel for pursuits of

enterprise objectives. This varies from the concept of financial accounting due to the fact the

meant motive of managerial accounting is to provide assistance to users inner to corporation in

developing well-informed commercial enterprise decisions. Managerial accounting comprises

multiple facets of accounting aimed toward improving the quality of records brought to

management regarding business operation metrics. Managerial accountants within enterprise use

information concerned with the costs and incomes form sales of products/services

(Abdusalomova, 2019).

MA system implies to effective mechanism which comprises activities or tasks that

contribute towards supply of key information for decision-making. Management accounting

system generally require use of both accounting as well as managerial data which help managing

personnel in decision making. Key importance of management accounting is in managerial

decision-making. Management accounting provide comprehensive details and facts which are

ultimately used by managers in developing management policies and creation of base for

decision making.

The terms management accounting is made up of two different terms: the management

and the accounting. This can be described as a mechanism that provides information tools to an

organization's managers to assist them in making decisions. It helps in managerial effectiveness

by presenting all relevant information and statistics to executives, enabling them to make

informed decisions and monitor all other aspects of the business (Ameen, Ahmed and Abd

Hafez, 2018). The study covers multiple tasks which covers different aspects of MA like systems

and reports of MA, key planning tools, ratio analysis and preparation of budget.

Section One

1.1 Management accounting and essential requirements of multiple forms of management

accounting systems:

Managerial accounting corresponds to vital practice of recognizing, assessing, interpreting,

evaluating and efficiently reporting key fiscal details about managerial personnel for pursuits of

enterprise objectives. This varies from the concept of financial accounting due to the fact the

meant motive of managerial accounting is to provide assistance to users inner to corporation in

developing well-informed commercial enterprise decisions. Managerial accounting comprises

multiple facets of accounting aimed toward improving the quality of records brought to

management regarding business operation metrics. Managerial accountants within enterprise use

information concerned with the costs and incomes form sales of products/services

(Abdusalomova, 2019).

MA system implies to effective mechanism which comprises activities or tasks that

contribute towards supply of key information for decision-making. Management accounting

system generally require use of both accounting as well as managerial data which help managing

personnel in decision making. Key importance of management accounting is in managerial

decision-making. Management accounting provide comprehensive details and facts which are

ultimately used by managers in developing management policies and creation of base for

decision making.

1.2 Different methods of management accounting reporting:

Management accounting within a business context involves multiple systems which enable

organization to make effective decisions. In this regard following is detailed discussion about the

multiple systems of MA along with their crucial requirements, as follows:

Inventory management system: This system is dedicated towards recording of different kind of

inventories of an enterprise. Management should adopt this system for facilitating effective

management of inventories. In business, inventories directly affect business’s gross profitability,

thus it’s key task of management to manage their inventory items properly. This system

primarily requires use of detailed accurate and relevant information of inventories like WIP,

Finished goods, raw-materials etc. This system also requires use of method of inventory

valuation like FIFO, LIFO or average cost method (Allain, Lemaire and Lux, 2021). Here are

key features of these methods, as follows:

FIFO: Herein this approach, key assumption for valuing stock is that first bought stock-

items are sold first.

LIFO: As opposite to FIFO approach, this system assumed that last purchased stock are

sold first in a particular sequence.

Average Cost method: In this approach, simple average of all the inventories costs are

used to value stock.

Job costing System: Job costing system is cost-control mechanism that attributes production

costs to every product, allowing executives to keep tracking of expenses/costs. Manufacturing

costs are measured using work costing systems, which divide them into overheads, material

costs, including production overhead and measure them at product’s actual value. Job costing is

an efficacious technique for allocating cost of product as well as keep tracking of

order's expenditure, particularly when a company 's items are not comparable. To enhance cost

oversight and increase profitability, mostly businesses now use computer based job costing

processes. Main requirement within a business relating to job costing system is to proper

allocation of costs to each of the order received by a business. Job costing produces distinct

"buckets" of details for every job, which the cost accountant may analyze to decide whether this

should be attributed towards such job. There's a fair risk that costs would be wrongly attributed if

Management accounting within a business context involves multiple systems which enable

organization to make effective decisions. In this regard following is detailed discussion about the

multiple systems of MA along with their crucial requirements, as follows:

Inventory management system: This system is dedicated towards recording of different kind of

inventories of an enterprise. Management should adopt this system for facilitating effective

management of inventories. In business, inventories directly affect business’s gross profitability,

thus it’s key task of management to manage their inventory items properly. This system

primarily requires use of detailed accurate and relevant information of inventories like WIP,

Finished goods, raw-materials etc. This system also requires use of method of inventory

valuation like FIFO, LIFO or average cost method (Allain, Lemaire and Lux, 2021). Here are

key features of these methods, as follows:

FIFO: Herein this approach, key assumption for valuing stock is that first bought stock-

items are sold first.

LIFO: As opposite to FIFO approach, this system assumed that last purchased stock are

sold first in a particular sequence.

Average Cost method: In this approach, simple average of all the inventories costs are

used to value stock.

Job costing System: Job costing system is cost-control mechanism that attributes production

costs to every product, allowing executives to keep tracking of expenses/costs. Manufacturing

costs are measured using work costing systems, which divide them into overheads, material

costs, including production overhead and measure them at product’s actual value. Job costing is

an efficacious technique for allocating cost of product as well as keep tracking of

order's expenditure, particularly when a company 's items are not comparable. To enhance cost

oversight and increase profitability, mostly businesses now use computer based job costing

processes. Main requirement within a business relating to job costing system is to proper

allocation of costs to each of the order received by a business. Job costing produces distinct

"buckets" of details for every job, which the cost accountant may analyze to decide whether this

should be attributed towards such job. There's a fair risk that costs would be wrongly attributed if

there're a lot of different jobs under progress, but this costing system's design allows this highly

auditable (Abdusalomova, 2020).

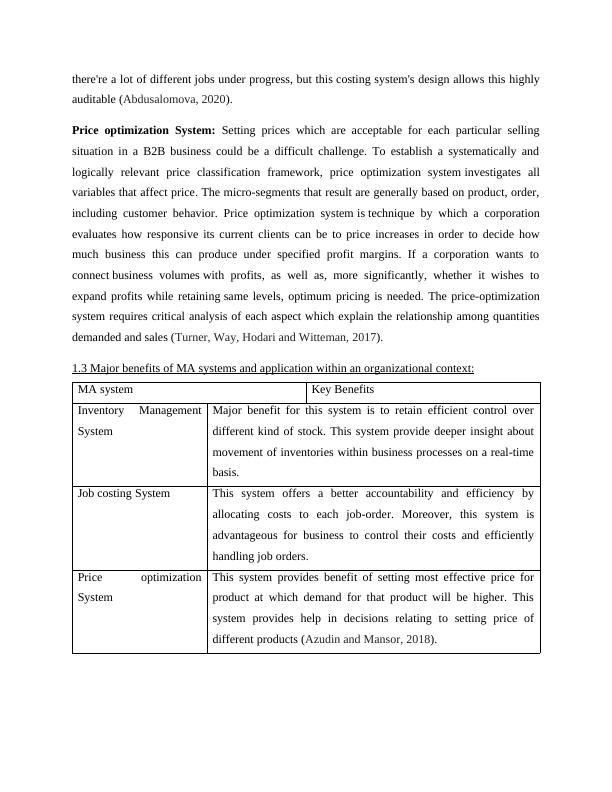

Price optimization System: Setting prices which are acceptable for each particular selling

situation in a B2B business could be a difficult challenge. To establish a systematically and

logically relevant price classification framework, price optimization system investigates all

variables that affect price. The micro-segments that result are generally based on product, order,

including customer behavior. Price optimization system is technique by which a corporation

evaluates how responsive its current clients can be to price increases in order to decide how

much business this can produce under specified profit margins. If a corporation wants to

connect business volumes with profits, as well as, more significantly, whether it wishes to

expand profits while retaining same levels, optimum pricing is needed. The price-optimization

system requires critical analysis of each aspect which explain the relationship among quantities

demanded and sales (Turner, Way, Hodari and Witteman, 2017).

1.3 Major benefits of MA systems and application within an organizational context:

MA system Key Benefits

Inventory Management

System

Major benefit for this system is to retain efficient control over

different kind of stock. This system provide deeper insight about

movement of inventories within business processes on a real-time

basis.

Job costing System This system offers a better accountability and efficiency by

allocating costs to each job-order. Moreover, this system is

advantageous for business to control their costs and efficiently

handling job orders.

Price optimization

System

This system provides benefit of setting most effective price for

product at which demand for that product will be higher. This

system provides help in decisions relating to setting price of

different products (Azudin and Mansor, 2018).

auditable (Abdusalomova, 2020).

Price optimization System: Setting prices which are acceptable for each particular selling

situation in a B2B business could be a difficult challenge. To establish a systematically and

logically relevant price classification framework, price optimization system investigates all

variables that affect price. The micro-segments that result are generally based on product, order,

including customer behavior. Price optimization system is technique by which a corporation

evaluates how responsive its current clients can be to price increases in order to decide how

much business this can produce under specified profit margins. If a corporation wants to

connect business volumes with profits, as well as, more significantly, whether it wishes to

expand profits while retaining same levels, optimum pricing is needed. The price-optimization

system requires critical analysis of each aspect which explain the relationship among quantities

demanded and sales (Turner, Way, Hodari and Witteman, 2017).

1.3 Major benefits of MA systems and application within an organizational context:

MA system Key Benefits

Inventory Management

System

Major benefit for this system is to retain efficient control over

different kind of stock. This system provide deeper insight about

movement of inventories within business processes on a real-time

basis.

Job costing System This system offers a better accountability and efficiency by

allocating costs to each job-order. Moreover, this system is

advantageous for business to control their costs and efficiently

handling job orders.

Price optimization

System

This system provides benefit of setting most effective price for

product at which demand for that product will be higher. This

system provides help in decisions relating to setting price of

different products (Azudin and Mansor, 2018).

1.4. Critical evaluation how MA systems and MA is integrated within organizational processes.

Along with Importance of different methods of reporting:

In a business, linkage between different processes and MA system is significant for

efficient adaption of overall managerial accounting framework. For instance, accounting and

processes provides key information for price-optimization system and job costing system. As

well as inventory storage and handling processes provide key data or information regarding

inventories for inventory management system. Thus integration of processes and MA system are

crucial for more productive decision making (Pedroso and Gomes, 2020).

Internal information through financial results is found in the management accounting

report. The reporting process is used to develop plans, make decisions, and evaluate the

organization's success. In order to maintain tracking of details, reports are produced on a constant

schedule. These reports play a major role in the corporation's critical decisions. Upper authorities

must keep a close focus on reports before making any more organization decisions. The

following part go through the various forms of reports which are produced in a corporation:

Account Receivable Aging Report: This form of report in MA is necessary whenever a

corporation's credit-based business is highly dependent on its scale and activities. Trade

receivables aging reports serve a significant part in this. This report analyzes debtors and breaks

down customers and unpaid balances into discrete time frames, enabling company administrators

to classify debtors and search for problems with the corporation's collection mechanism. If a

corporation identifies so many defaulters, this can need to adjust its debt collection mechanism

and tighten its credit norms as cash flows is necessary for business operations. It is normal for

companies to have bad-debts that must be written-off time to time. Conversely, since a

corporation cannot make this a routine, it's indeed prudent for it to be informed of its debtors

(Charifzadeh and Taschner, 2017).

Cost Report: Details regarding overall costs of goods produced within a business are reported in

this report. This form of report takes into consideration all costs linked to raw materials,

overheads, manpower, and processing costs, among other items. The overall cost is after which

divided by the number of goods manufactured in such unit. All of this information is outlined in

the article. The report helps company executives to consider costing of their goods as they are

being produced in contrast to retail prices. These profits are also assessed and projected, and

Along with Importance of different methods of reporting:

In a business, linkage between different processes and MA system is significant for

efficient adaption of overall managerial accounting framework. For instance, accounting and

processes provides key information for price-optimization system and job costing system. As

well as inventory storage and handling processes provide key data or information regarding

inventories for inventory management system. Thus integration of processes and MA system are

crucial for more productive decision making (Pedroso and Gomes, 2020).

Internal information through financial results is found in the management accounting

report. The reporting process is used to develop plans, make decisions, and evaluate the

organization's success. In order to maintain tracking of details, reports are produced on a constant

schedule. These reports play a major role in the corporation's critical decisions. Upper authorities

must keep a close focus on reports before making any more organization decisions. The

following part go through the various forms of reports which are produced in a corporation:

Account Receivable Aging Report: This form of report in MA is necessary whenever a

corporation's credit-based business is highly dependent on its scale and activities. Trade

receivables aging reports serve a significant part in this. This report analyzes debtors and breaks

down customers and unpaid balances into discrete time frames, enabling company administrators

to classify debtors and search for problems with the corporation's collection mechanism. If a

corporation identifies so many defaulters, this can need to adjust its debt collection mechanism

and tighten its credit norms as cash flows is necessary for business operations. It is normal for

companies to have bad-debts that must be written-off time to time. Conversely, since a

corporation cannot make this a routine, it's indeed prudent for it to be informed of its debtors

(Charifzadeh and Taschner, 2017).

Cost Report: Details regarding overall costs of goods produced within a business are reported in

this report. This form of report takes into consideration all costs linked to raw materials,

overheads, manpower, and processing costs, among other items. The overall cost is after which

divided by the number of goods manufactured in such unit. All of this information is outlined in

the article. The report helps company executives to consider costing of their goods as they are

being produced in contrast to retail prices. These profits are also assessed and projected, and

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Benefits and Drawbacks of Budgetary Control Planning Toolslg...

|19

|4262

|98

Benefits and drawbacks of budgetary control planning toolslg...

|20

|4642

|21

Principles and Practice of Management Accountinglg...

|22

|5460

|52

Management Accounting Assignment : Airdri Limitedlg...

|17

|5440

|91

Using FIFO Method for Inventory Accounting and Year-End Inventory Activitieslg...

|13

|1317

|277

INVENTORY METHODs.lg...

|8

|458

|25