Strategic Cost Management and Competitive Advantage

VerifiedAdded on 2020/07/22

|18

|5040

|56

AI Summary

This assignment focuses on various aspects of strategic cost management as a means to achieve competitive advantage in today's global business landscape. It includes studies on tailoring controls to strategies (Govindarajan & Shank, 2014), international comparisons of strategic management accounting practices (Guilding et al., 2016), and global supply chain risk management strategies (Manuj & Mentzer, 2015). Additionally, it covers the integration of management accounting with marketing for competitive advantage (Roslender & Hart, 2013) and the role of human resource management practices in gaining competitive advantage (Schuler & MacMillan, 2014). The assignment also delves into environmental technologies and competitive advantage (Shrivastava, 2015), knowledge management for competitive advantage (Silvi & Cuganesan, 2016), and the reflection of corporate strategy in manufacturing decisions (Wheelwright, 2013).

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT ACCOUNTING

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive summary

The report focuses on the management accounting system of the Pacific computers. Different

methods of the management accounting system are explained thoroughly. Account management

officer present a report about the negative issues of the organisation to geranial manager.

Management performs the market research by following the newspaper, text books, magazine

and so on. This helps the higher hierarchy to perform perfect strategy in order to raise the

recognition of the enterprise in global market. Systematic strategy prevents the chaotic behavior

from the enterprise.

2

The report focuses on the management accounting system of the Pacific computers. Different

methods of the management accounting system are explained thoroughly. Account management

officer present a report about the negative issues of the organisation to geranial manager.

Management performs the market research by following the newspaper, text books, magazine

and so on. This helps the higher hierarchy to perform perfect strategy in order to raise the

recognition of the enterprise in global market. Systematic strategy prevents the chaotic behavior

from the enterprise.

2

Table of Contents

Introduction......................................................................................................................................3

LO 1:................................................................................................................................................3

P1: Explanation of accounting system of management and the provision of key necessities of

various types of accounting systems of management......................................................................3

P2: Explanation of various methods utilized for management accounting.....................................6

P3.....................................................................................................................................................8

M2:...................................................................................................................................................9

D2:.................................................................................................................................................10

Reference list.................................................................................................................................11

3

Introduction......................................................................................................................................3

LO 1:................................................................................................................................................3

P1: Explanation of accounting system of management and the provision of key necessities of

various types of accounting systems of management......................................................................3

P2: Explanation of various methods utilized for management accounting.....................................6

P3.....................................................................................................................................................8

M2:...................................................................................................................................................9

D2:.................................................................................................................................................10

Reference list.................................................................................................................................11

3

To The General Manager

Pacific Computers

Introduction

Internal managerial systems of accounting are implemented to deliver information that the

management of the company can utilise to make better decisions in its business. These systems

are often utilised by plants of manufacturing to helping managing and costing the process of

manufacturing. IT systems generally utilise this type of system that helps them in billing of

insurance and other various in-house necessities. The primary objective of this system is to give

data to managers for making quality decisions. Internal managerial systems of accounting vary

from industry to industry in which they are utilised, that allows for reports and functionalities

particular to that specific industry.

LO 1:

P1: Explanation of accounting system of management and the provision of key

necessities of various types of accounting systems of management

According to Fisman et al. (2014, p.422),in managerial or management accounting, the provision

of information for accounting are utilised by managers, they utilise the provisions of information

of accounting for better informing themselves prior to matters of decision making in the

company, that aids their performance and management of functions of control.

4

Pacific Computers

Introduction

Internal managerial systems of accounting are implemented to deliver information that the

management of the company can utilise to make better decisions in its business. These systems

are often utilised by plants of manufacturing to helping managing and costing the process of

manufacturing. IT systems generally utilise this type of system that helps them in billing of

insurance and other various in-house necessities. The primary objective of this system is to give

data to managers for making quality decisions. Internal managerial systems of accounting vary

from industry to industry in which they are utilised, that allows for reports and functionalities

particular to that specific industry.

LO 1:

P1: Explanation of accounting system of management and the provision of key

necessities of various types of accounting systems of management

According to Fisman et al. (2014, p.422),in managerial or management accounting, the provision

of information for accounting are utilised by managers, they utilise the provisions of information

of accounting for better informing themselves prior to matters of decision making in the

company, that aids their performance and management of functions of control.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

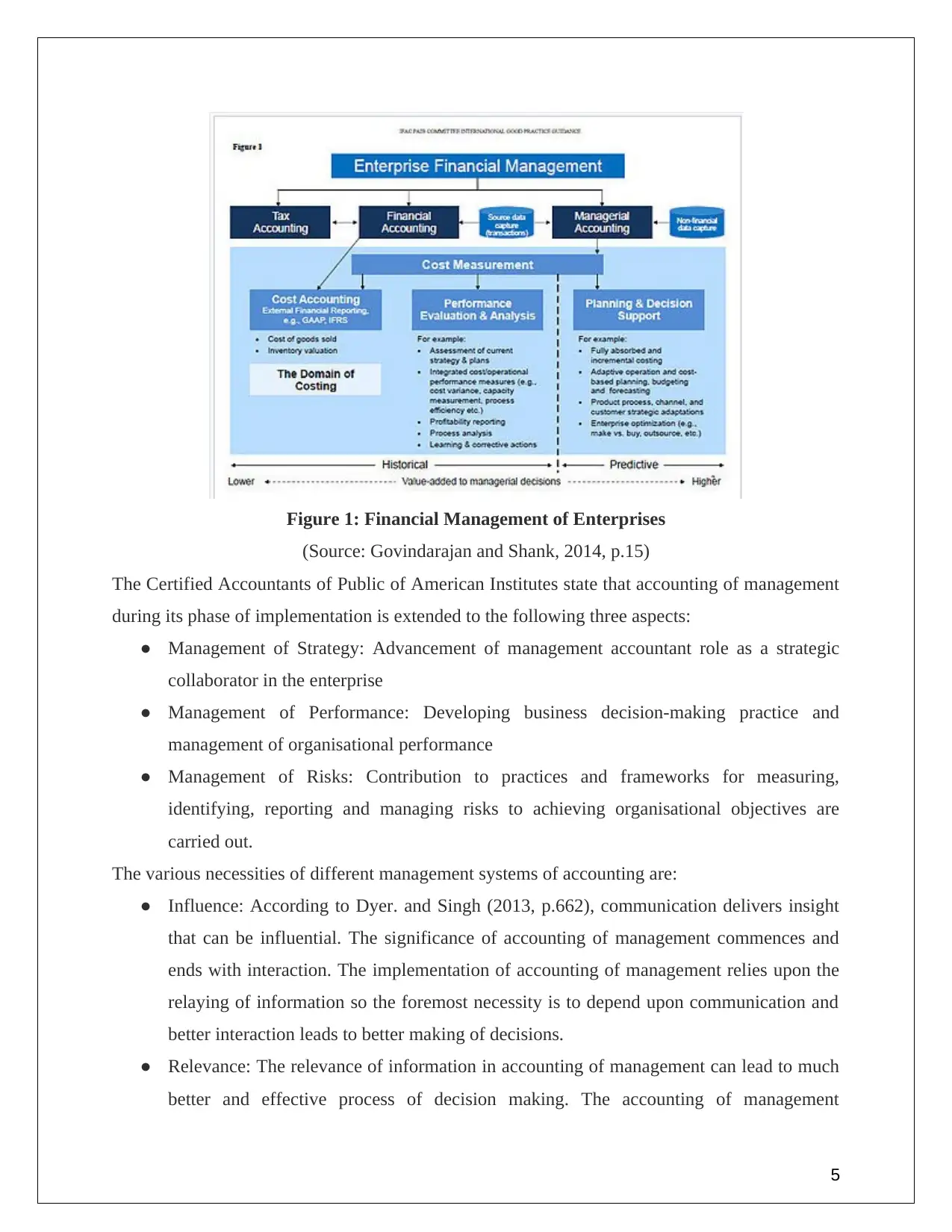

Figure 1: Financial Management of Enterprises

(Source: Govindarajan and Shank, 2014, p.15)

The Certified Accountants of Public of American Institutes state that accounting of management

during its phase of implementation is extended to the following three aspects:

● Management of Strategy: Advancement of management accountant role as a strategic

collaborator in the enterprise

● Management of Performance: Developing business decision-making practice and

management of organisational performance

● Management of Risks: Contribution to practices and frameworks for measuring,

identifying, reporting and managing risks to achieving organisational objectives are

carried out.

The various necessities of different management systems of accounting are:

● Influence: According to Dyer. and Singh (2013, p.662), communication delivers insight

that can be influential. The significance of accounting of management commences and

ends with interaction. The implementation of accounting of management relies upon the

relaying of information so the foremost necessity is to depend upon communication and

better interaction leads to better making of decisions.

● Relevance: The relevance of information in accounting of management can lead to much

better and effective process of decision making. The accounting of management

5

(Source: Govindarajan and Shank, 2014, p.15)

The Certified Accountants of Public of American Institutes state that accounting of management

during its phase of implementation is extended to the following three aspects:

● Management of Strategy: Advancement of management accountant role as a strategic

collaborator in the enterprise

● Management of Performance: Developing business decision-making practice and

management of organisational performance

● Management of Risks: Contribution to practices and frameworks for measuring,

identifying, reporting and managing risks to achieving organisational objectives are

carried out.

The various necessities of different management systems of accounting are:

● Influence: According to Dyer. and Singh (2013, p.662), communication delivers insight

that can be influential. The significance of accounting of management commences and

ends with interaction. The implementation of accounting of management relies upon the

relaying of information so the foremost necessity is to depend upon communication and

better interaction leads to better making of decisions.

● Relevance: The relevance of information in accounting of management can lead to much

better and effective process of decision making. The accounting of management

5

comprises of various types of data with respect to Pacific Computers regardless of of it

being financial or not. The only aspect that is relevant to cultural and social aspects of the

company.

● Analysis: This necessity is also called value. Value impact is evaluated. Referring to

Schuler and Jackson (2017, p.212), management is helped by management accounting to

analyse the given information suitably so that better decision making can take place by

the management of the company. As a result, suitable analysis is mandatory for the

management of Pacific Computers. The information needs to be analysed by the

management of the organisation so that organisational environment can be understood

and better business decisions can be implemented.

● Trust: Trust is built by stewardship. This necessary element of financial accounting

systems on the execution of accountants of management is done so that persons are

accountable and ethical to Pacific Computers. Referring to Wheelwright (2013, p.62), an

accountant of management needs to be a loyal person for the analysis of information of

management accounting in apt ways. The trust of stakeholders needs to be considered by

the management accountants and should be accountable for improving the company via

better making of business decisions.

6

being financial or not. The only aspect that is relevant to cultural and social aspects of the

company.

● Analysis: This necessity is also called value. Value impact is evaluated. Referring to

Schuler and Jackson (2017, p.212), management is helped by management accounting to

analyse the given information suitably so that better decision making can take place by

the management of the company. As a result, suitable analysis is mandatory for the

management of Pacific Computers. The information needs to be analysed by the

management of the organisation so that organisational environment can be understood

and better business decisions can be implemented.

● Trust: Trust is built by stewardship. This necessary element of financial accounting

systems on the execution of accountants of management is done so that persons are

accountable and ethical to Pacific Computers. Referring to Wheelwright (2013, p.62), an

accountant of management needs to be a loyal person for the analysis of information of

management accounting in apt ways. The trust of stakeholders needs to be considered by

the management accountants and should be accountable for improving the company via

better making of business decisions.

6

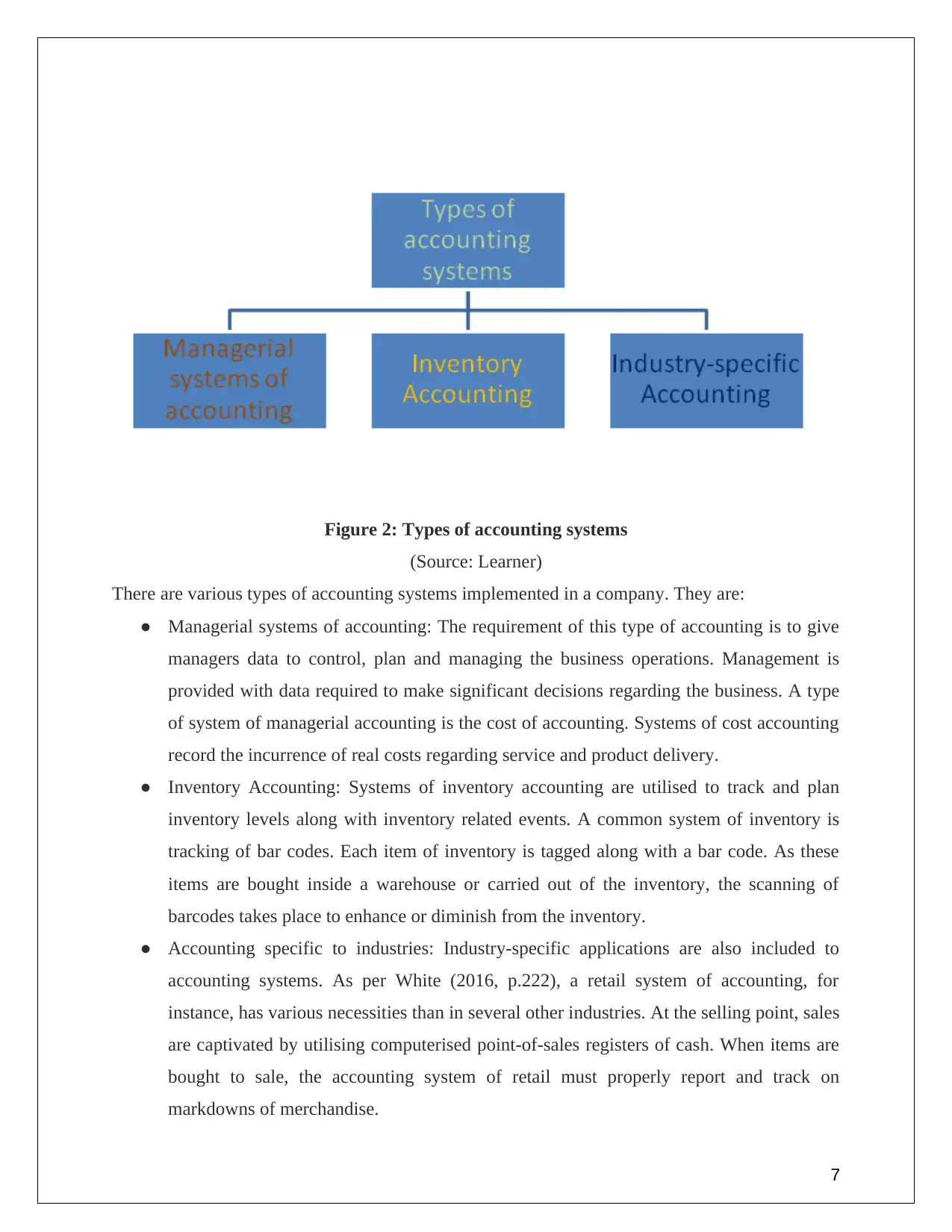

Figure 2: Types of accounting systems

(Source: Learner)

There are various types of accounting systems implemented in a company. They are:

● Managerial systems of accounting: The requirement of this type of accounting is to give

managers data to control, plan and managing the business operations. Management is

provided with data required to make significant decisions regarding the business. A type

of system of managerial accounting is the cost of accounting. Systems of cost accounting

record the incurrence of real costs regarding service and product delivery.

● Inventory Accounting: Systems of inventory accounting are utilised to track and plan

inventory levels along with inventory related events. A common system of inventory is

tracking of bar codes. Each item of inventory is tagged along with a bar code. As these

items are bought inside a warehouse or carried out of the inventory, the scanning of

barcodes takes place to enhance or diminish from the inventory.

● Accounting specific to industries: Industry-specific applications are also included to

accounting systems. As per White (2016, p.222), a retail system of accounting, for

instance, has various necessities than in several other industries. At the selling point, sales

are captivated by utilising computerised point-of-sales registers of cash. When items are

bought to sale, the accounting system of retail must properly report and track on

markdowns of merchandise.

7

(Source: Learner)

There are various types of accounting systems implemented in a company. They are:

● Managerial systems of accounting: The requirement of this type of accounting is to give

managers data to control, plan and managing the business operations. Management is

provided with data required to make significant decisions regarding the business. A type

of system of managerial accounting is the cost of accounting. Systems of cost accounting

record the incurrence of real costs regarding service and product delivery.

● Inventory Accounting: Systems of inventory accounting are utilised to track and plan

inventory levels along with inventory related events. A common system of inventory is

tracking of bar codes. Each item of inventory is tagged along with a bar code. As these

items are bought inside a warehouse or carried out of the inventory, the scanning of

barcodes takes place to enhance or diminish from the inventory.

● Accounting specific to industries: Industry-specific applications are also included to

accounting systems. As per White (2016, p.222), a retail system of accounting, for

instance, has various necessities than in several other industries. At the selling point, sales

are captivated by utilising computerised point-of-sales registers of cash. When items are

bought to sale, the accounting system of retail must properly report and track on

markdowns of merchandise.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

● Not-for-profit Accounting: Referring to Dierickx and Cool (2014, p.1506), this type of

accounting comprises of its own particular set of requirements for reporting. For instance,

funds are needed to be tracked so that designated donations for particular reasons are

spent properly.

P2: Explanation of various methods utilized for management accounting.

Various techniques of accounting of management include:

● Financial Planning: It is considered an act of advance decision-making process regarding

the necessary financial activities for the criterion of achieving its foremost goals. It

comprises of determining both short and long-term financial goals of Pacific Computers,

developing policies of finance and formulating the procedure to reach the objectives. The

significance of policies of finance cannot be highlighted to achieve maximum return on

the employed capital. According to Shukla and Clement (2017, p.121), the policies of

finance might relate to determine the capital amount that would be necessary, income

distribution and governing determination. In the utilisation of equity and debt

determination and capital of the best level of investment in different assets can be acted

as a guide.

● Analysis of statements of finance: The evaluation of the financial statements is

considered an attempt to determine the meaning and significance of the data of financial

statements so that a prediction might be formulated of prospects of earning in the future,

capability to pay the interest off along with debt maturities. It also includes of a policy

that is soundly dividend. Referring to Aladwani (2014, p.266), techniques implemented

in such analysis include trend analysis, comparative statements of finance, ratio analysis

and statements of cash funds flow.

● Accounting of Historical Costs: The Accounting of Historical Costs provides past

information to the organisational management with respect to cost of every job

department and process so that comparison can be carried out with standard costs.

● Standard Costing: The development of standard costs is defined by standard costing

under the most impactful conditions of operating, calculation, comparison of reality with

standard, variance analysis and in order to realise the purposes. As per Lascu (2014,

p.122), it would also include emphasise the responsibility along with taking remedial

8

accounting comprises of its own particular set of requirements for reporting. For instance,

funds are needed to be tracked so that designated donations for particular reasons are

spent properly.

P2: Explanation of various methods utilized for management accounting.

Various techniques of accounting of management include:

● Financial Planning: It is considered an act of advance decision-making process regarding

the necessary financial activities for the criterion of achieving its foremost goals. It

comprises of determining both short and long-term financial goals of Pacific Computers,

developing policies of finance and formulating the procedure to reach the objectives. The

significance of policies of finance cannot be highlighted to achieve maximum return on

the employed capital. According to Shukla and Clement (2017, p.121), the policies of

finance might relate to determine the capital amount that would be necessary, income

distribution and governing determination. In the utilisation of equity and debt

determination and capital of the best level of investment in different assets can be acted

as a guide.

● Analysis of statements of finance: The evaluation of the financial statements is

considered an attempt to determine the meaning and significance of the data of financial

statements so that a prediction might be formulated of prospects of earning in the future,

capability to pay the interest off along with debt maturities. It also includes of a policy

that is soundly dividend. Referring to Aladwani (2014, p.266), techniques implemented

in such analysis include trend analysis, comparative statements of finance, ratio analysis

and statements of cash funds flow.

● Accounting of Historical Costs: The Accounting of Historical Costs provides past

information to the organisational management with respect to cost of every job

department and process so that comparison can be carried out with standard costs.

● Standard Costing: The development of standard costs is defined by standard costing

under the most impactful conditions of operating, calculation, comparison of reality with

standard, variance analysis and in order to realise the purposes. As per Lascu (2014,

p.122), it would also include emphasise the responsibility along with taking remedial

8

actions. As a result, adverse situations might take place again. This field is important to

have control of costs.

● Control of Budget: The accountant of the management utilises the tool for budget control

for controlling and planning the different events of a business. The control of budget is

deemed as a significant technique of directing operations of business in a direction that is

desired, i.e. a satisfactory return is achieved on investment (Silv and Cuganesan, 2016,

p.314).

● Marginal Costing: The accountant of management utilises the methods of marginal

costing, break-even analysis and differential costing for controlling of costs, profit-

maximisation and decision-making.

● Statement of funds flow: The accountant of management utilises the methods of

statement of funds flow for analysing the modifications in the position of finance of an

enterprise between two different dates. It informs about the funds which are inflowing in

the business and how these are being substantial in the growth of the business.

● Statement of Cash Flow: A statement of funds flow that is based on decrease or increase

in the working capital would result in long range planning of finance. It might be highly

probable that sufficient capital of working as revealed by the statement of funds flow and

the organisation might still be unable to comply with its ongoing liabilities as and when

they are due to fall. It might be because of a gathering of inventories along with an

increase in debtors of trade.

● Making of business decisions: According to Ellram and Siferd (2015, p.55), when various

alternatives are there of executing a specific work, it turns out to be important to choose

the optimal solution out of all the alternatives. This decision is required on behalf of the

management. The accounting of management would help the management via the

methods of capital budgeting, marginal costing and differential costing to choose the

optimal solution would result in maximisation of profits of the business.

● Assessment of Accounting: The accountant of management, via Pacific Computers would

assure the preservation and assurance of the organisational capital. It takes into

consideration the influence of modifications regarding price of preparation of statements

of finance.

● LO2:

9

have control of costs.

● Control of Budget: The accountant of the management utilises the tool for budget control

for controlling and planning the different events of a business. The control of budget is

deemed as a significant technique of directing operations of business in a direction that is

desired, i.e. a satisfactory return is achieved on investment (Silv and Cuganesan, 2016,

p.314).

● Marginal Costing: The accountant of management utilises the methods of marginal

costing, break-even analysis and differential costing for controlling of costs, profit-

maximisation and decision-making.

● Statement of funds flow: The accountant of management utilises the methods of

statement of funds flow for analysing the modifications in the position of finance of an

enterprise between two different dates. It informs about the funds which are inflowing in

the business and how these are being substantial in the growth of the business.

● Statement of Cash Flow: A statement of funds flow that is based on decrease or increase

in the working capital would result in long range planning of finance. It might be highly

probable that sufficient capital of working as revealed by the statement of funds flow and

the organisation might still be unable to comply with its ongoing liabilities as and when

they are due to fall. It might be because of a gathering of inventories along with an

increase in debtors of trade.

● Making of business decisions: According to Ellram and Siferd (2015, p.55), when various

alternatives are there of executing a specific work, it turns out to be important to choose

the optimal solution out of all the alternatives. This decision is required on behalf of the

management. The accounting of management would help the management via the

methods of capital budgeting, marginal costing and differential costing to choose the

optimal solution would result in maximisation of profits of the business.

● Assessment of Accounting: The accountant of management, via Pacific Computers would

assure the preservation and assurance of the organisational capital. It takes into

consideration the influence of modifications regarding price of preparation of statements

of finance.

● LO2:

9

● P3: Calculation of costs by utilizing suitable techniques of analysis of costs of

absorption and marginal costing

● The cost which varies with decision is the decision analysis. Small variation in existing

practice of cost in the enterprise for limited period of time increase the recognition of

enterprise in global market. Fixed cost of products diminishes the identification of

enterprise among their recent users. Thus, the management team performs macro and

micro factors in order to compete with their products in recent market. The cost of the

product varies widely which attract customer and the higher hierarchy creates this

strategy for short term procedure. Flynn et al. (2015, p.660) commented that long term

strategy is created by the management team by following the policies of the government

and political conflicts. This helps the organisation to prevent chaotic behavior from the

organisation. Marginal costing help the Pacific Computers to easily distinguishes

between the variable and fixed cost. The marginal cost of the enterprise includes the

variable cost of it. The variable cost includes direct labor, direct expenses, and direct

material along with variable part of the overheads. The marginal cost combines the cost

of material, expense, direct labor and overheads.

● Mahoney and Pandian (2013, p.380) opined that marginal cost refers to marginal cost per

unit and total marginal cost of the enterprise’s department or operation or batch. This

marginal cost is the contribution approach along with direct costing. This cost is directly

proportional with the production volume of the organisation. It does not include any kind

of fixed cost criteria in the enterprise. Thus, the higher hierarchy performs their research

in order to create the short term strategy. Absorption costing includes all cost of the

production in the enterprise. The cost of production may be fixed or variable. This

absorption technique allocates the manufacturing cost, direct labor and materials costs.

Therefore, this absorption procedure is also known as the full costing method as it

includes the product costs of the Pacific Computers.

10

absorption and marginal costing

● The cost which varies with decision is the decision analysis. Small variation in existing

practice of cost in the enterprise for limited period of time increase the recognition of

enterprise in global market. Fixed cost of products diminishes the identification of

enterprise among their recent users. Thus, the management team performs macro and

micro factors in order to compete with their products in recent market. The cost of the

product varies widely which attract customer and the higher hierarchy creates this

strategy for short term procedure. Flynn et al. (2015, p.660) commented that long term

strategy is created by the management team by following the policies of the government

and political conflicts. This helps the organisation to prevent chaotic behavior from the

organisation. Marginal costing help the Pacific Computers to easily distinguishes

between the variable and fixed cost. The marginal cost of the enterprise includes the

variable cost of it. The variable cost includes direct labor, direct expenses, and direct

material along with variable part of the overheads. The marginal cost combines the cost

of material, expense, direct labor and overheads.

● Mahoney and Pandian (2013, p.380) opined that marginal cost refers to marginal cost per

unit and total marginal cost of the enterprise’s department or operation or batch. This

marginal cost is the contribution approach along with direct costing. This cost is directly

proportional with the production volume of the organisation. It does not include any kind

of fixed cost criteria in the enterprise. Thus, the higher hierarchy performs their research

in order to create the short term strategy. Absorption costing includes all cost of the

production in the enterprise. The cost of production may be fixed or variable. This

absorption technique allocates the manufacturing cost, direct labor and materials costs.

Therefore, this absorption procedure is also known as the full costing method as it

includes the product costs of the Pacific Computers.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

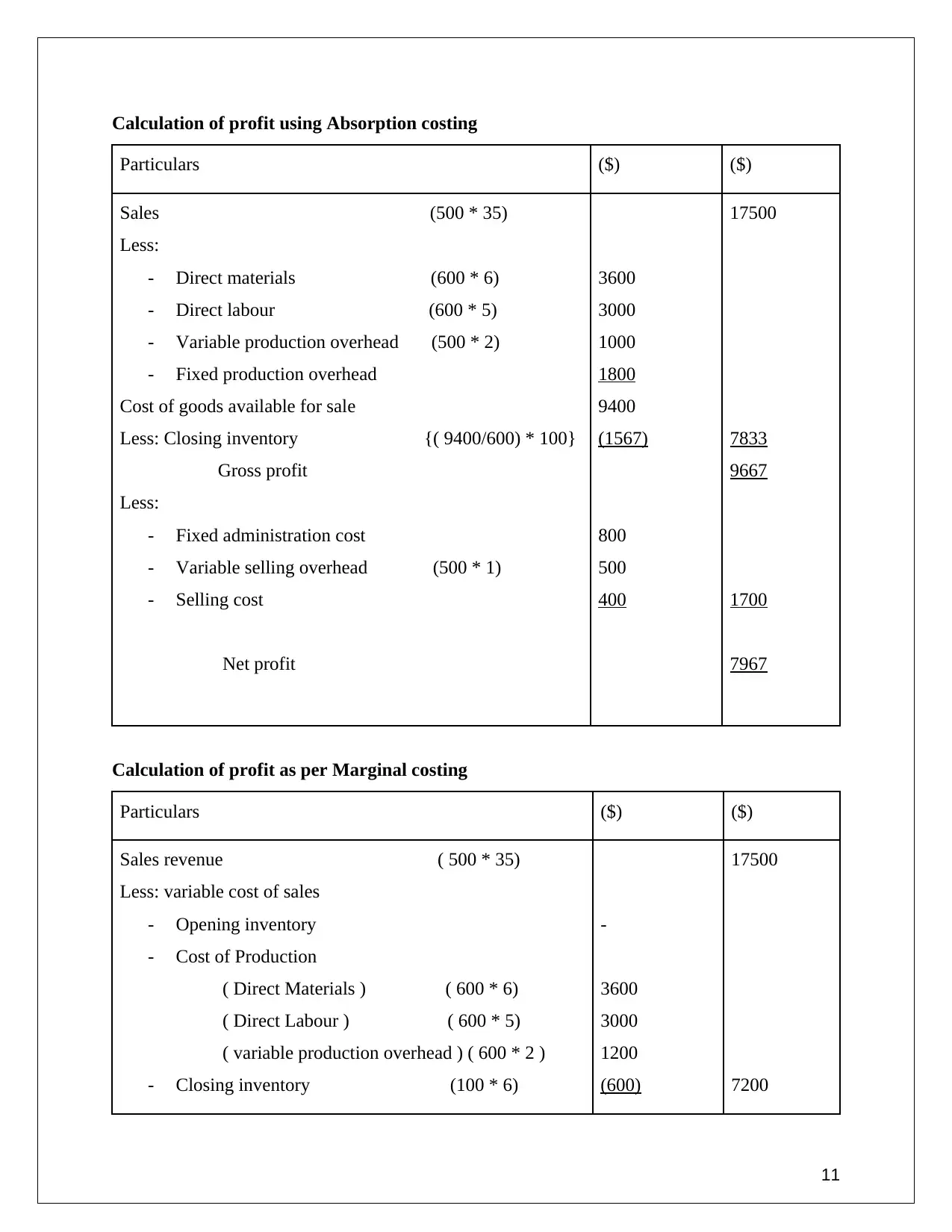

Calculation of profit using Absorption costing

Particulars ($) ($)

Sales (500 * 35)

Less:

- Direct materials (600 * 6)

- Direct labour (600 * 5)

- Variable production overhead (500 * 2)

- Fixed production overhead

Cost of goods available for sale

Less: Closing inventory {( 9400/600) * 100}

Gross profit

Less:

- Fixed administration cost

- Variable selling overhead (500 * 1)

- Selling cost

Net profit

3600

3000

1000

1800

9400

(1567)

800

500

400

17500

7833

9667

1700

7967

Calculation of profit as per Marginal costing

Particulars ($) ($)

Sales revenue ( 500 * 35)

Less: variable cost of sales

- Opening inventory

- Cost of Production

( Direct Materials ) ( 600 * 6)

( Direct Labour ) ( 600 * 5)

( variable production overhead ) ( 600 * 2 )

- Closing inventory (100 * 6)

-

3600

3000

1200

(600)

17500

7200

11

Particulars ($) ($)

Sales (500 * 35)

Less:

- Direct materials (600 * 6)

- Direct labour (600 * 5)

- Variable production overhead (500 * 2)

- Fixed production overhead

Cost of goods available for sale

Less: Closing inventory {( 9400/600) * 100}

Gross profit

Less:

- Fixed administration cost

- Variable selling overhead (500 * 1)

- Selling cost

Net profit

3600

3000

1000

1800

9400

(1567)

800

500

400

17500

7833

9667

1700

7967

Calculation of profit as per Marginal costing

Particulars ($) ($)

Sales revenue ( 500 * 35)

Less: variable cost of sales

- Opening inventory

- Cost of Production

( Direct Materials ) ( 600 * 6)

( Direct Labour ) ( 600 * 5)

( variable production overhead ) ( 600 * 2 )

- Closing inventory (100 * 6)

-

3600

3000

1200

(600)

17500

7200

11

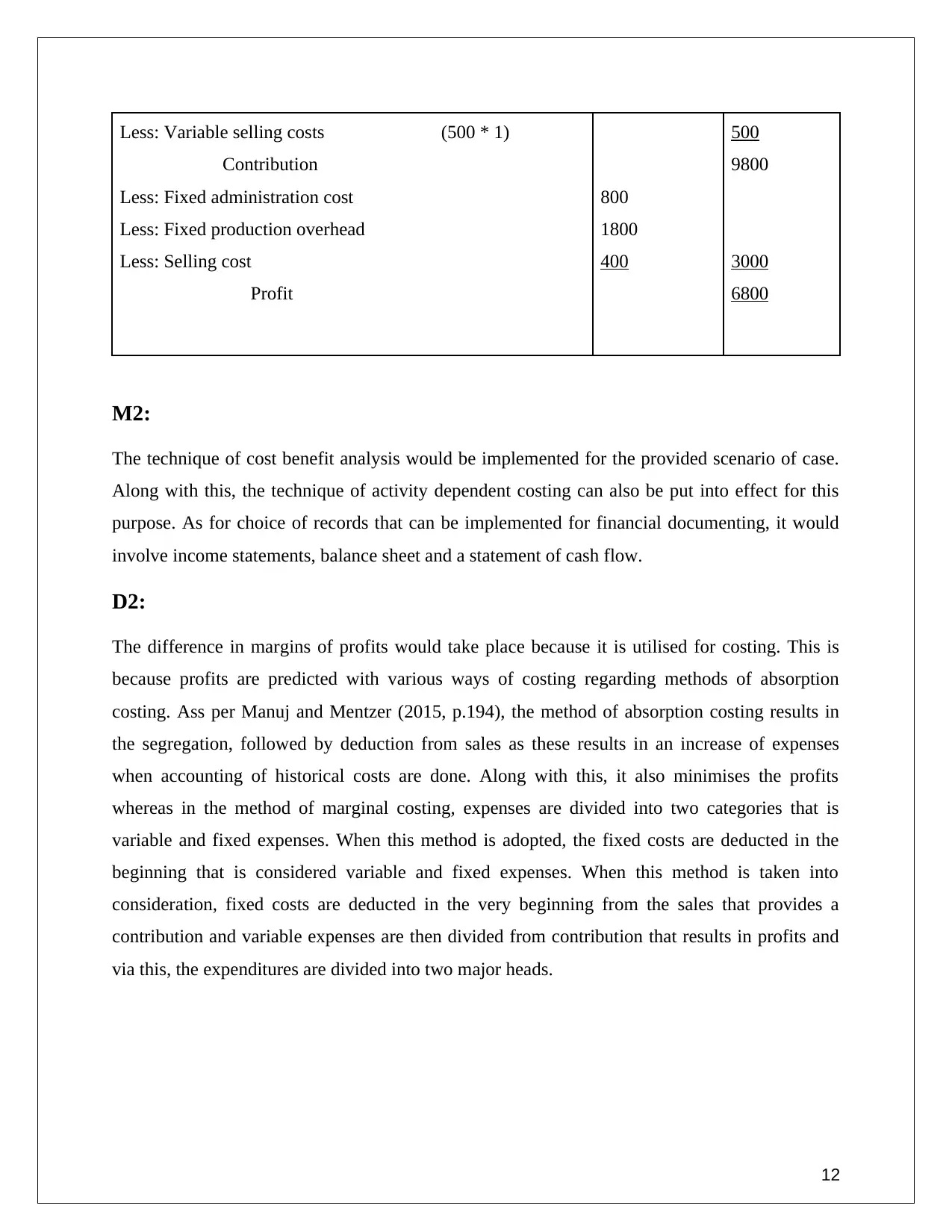

Less: Variable selling costs (500 * 1)

Contribution

Less: Fixed administration cost

Less: Fixed production overhead

Less: Selling cost

Profit

800

1800

400

500

9800

3000

6800

M2:

The technique of cost benefit analysis would be implemented for the provided scenario of case.

Along with this, the technique of activity dependent costing can also be put into effect for this

purpose. As for choice of records that can be implemented for financial documenting, it would

involve income statements, balance sheet and a statement of cash flow.

D2:

The difference in margins of profits would take place because it is utilised for costing. This is

because profits are predicted with various ways of costing regarding methods of absorption

costing. Ass per Manuj and Mentzer (2015, p.194), the method of absorption costing results in

the segregation, followed by deduction from sales as these results in an increase of expenses

when accounting of historical costs are done. Along with this, it also minimises the profits

whereas in the method of marginal costing, expenses are divided into two categories that is

variable and fixed expenses. When this method is adopted, the fixed costs are deducted in the

beginning that is considered variable and fixed expenses. When this method is taken into

consideration, fixed costs are deducted in the very beginning from the sales that provides a

contribution and variable expenses are then divided from contribution that results in profits and

via this, the expenditures are divided into two major heads.

12

Contribution

Less: Fixed administration cost

Less: Fixed production overhead

Less: Selling cost

Profit

800

1800

400

500

9800

3000

6800

M2:

The technique of cost benefit analysis would be implemented for the provided scenario of case.

Along with this, the technique of activity dependent costing can also be put into effect for this

purpose. As for choice of records that can be implemented for financial documenting, it would

involve income statements, balance sheet and a statement of cash flow.

D2:

The difference in margins of profits would take place because it is utilised for costing. This is

because profits are predicted with various ways of costing regarding methods of absorption

costing. Ass per Manuj and Mentzer (2015, p.194), the method of absorption costing results in

the segregation, followed by deduction from sales as these results in an increase of expenses

when accounting of historical costs are done. Along with this, it also minimises the profits

whereas in the method of marginal costing, expenses are divided into two categories that is

variable and fixed expenses. When this method is adopted, the fixed costs are deducted in the

beginning that is considered variable and fixed expenses. When this method is taken into

consideration, fixed costs are deducted in the very beginning from the sales that provides a

contribution and variable expenses are then divided from contribution that results in profits and

via this, the expenditures are divided into two major heads.

12

LO3:

P4: Explanation of benefits and issues of various categories of planning tools

Affinity diagram

This diagram helps the organisation to deal with the chaotic behavior of the organisation. Simons

(2013, p.143) mentioned that the management team of the enterprise perform several research

before creating and implementing any strategy in the enterprise. The higher hierarchy follows the

government rules and political parties’ policies and these prevent the organisation from

governmental penalties and raise their identification in global market. Issues of this diagram are

it too large in nature and full of complexity. This complex diagram is time consuming in nature

and diminishes the production quantity of Pacific Computers.

Interrelationship diagram (ID)

This diagram focuses on the cause and the effects relationship in the enterprise. The problem of

the enterprise is marked out and possible solution is written. It is future oriented in nature and

helps the organization to create a future strategy. The demerit of this diagram is it cannot handle

the present negative issues of the organisation. Thus, the management team cannot use this ID to

create their short term strategy.

Tree diagram

Barney (2016, p.665) stated that this diagram subdivided the negative and positive issues of the

organization into finer level details of the negative issues. These diagrams directly concentrate

on the individual issues of the organisation. The management teams perform their research and

modify the rules and policies of the organization by following the issues of the organisation. The

negative issues can be diminished easily and raise the organisation identification and profit

margin in recent market. The stakeholders can easily give their feedback about the service and

product quality of the enterprise. Higher hierarchy took all the necessary steps in order to

diminish the present issues of the organisation and raise their identification in present market.

Demerit of this diagram is the management team diminishes the negative issues of the

organisation by creating short term strategy. Higher hierarchy could not create the long term

strategy of the enterprise by following this diagram. Short term strategies help the enterprise to

tackle the current situation of the organisation and help it to maintain their recognition in global

13

P4: Explanation of benefits and issues of various categories of planning tools

Affinity diagram

This diagram helps the organisation to deal with the chaotic behavior of the organisation. Simons

(2013, p.143) mentioned that the management team of the enterprise perform several research

before creating and implementing any strategy in the enterprise. The higher hierarchy follows the

government rules and political parties’ policies and these prevent the organisation from

governmental penalties and raise their identification in global market. Issues of this diagram are

it too large in nature and full of complexity. This complex diagram is time consuming in nature

and diminishes the production quantity of Pacific Computers.

Interrelationship diagram (ID)

This diagram focuses on the cause and the effects relationship in the enterprise. The problem of

the enterprise is marked out and possible solution is written. It is future oriented in nature and

helps the organization to create a future strategy. The demerit of this diagram is it cannot handle

the present negative issues of the organisation. Thus, the management team cannot use this ID to

create their short term strategy.

Tree diagram

Barney (2016, p.665) stated that this diagram subdivided the negative and positive issues of the

organization into finer level details of the negative issues. These diagrams directly concentrate

on the individual issues of the organisation. The management teams perform their research and

modify the rules and policies of the organization by following the issues of the organisation. The

negative issues can be diminished easily and raise the organisation identification and profit

margin in recent market. The stakeholders can easily give their feedback about the service and

product quality of the enterprise. Higher hierarchy took all the necessary steps in order to

diminish the present issues of the organisation and raise their identification in present market.

Demerit of this diagram is the management team diminishes the negative issues of the

organisation by creating short term strategy. Higher hierarchy could not create the long term

strategy of the enterprise by following this diagram. Short term strategies help the enterprise to

tackle the current situation of the organisation and help it to maintain their recognition in global

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

market. Combination of technology and the organisation help the accounting officer to manage

the negative issues of the stakeholders easily.

Prioritization matrix

Oliver (2017, p.713) commented that the management team of organisation divided the negative

issues of the organisation according to its weighted criteria. It follows the combination of the

matrix and tree diagram in order to raise the identification of the enterprise in global market. The

creditor always creates a pressure to increase the production rate and the profit margin of Pacific

Computers. The management team can easily perform the cost benefits analysis, time

management strategy which includes the importance of urgency and so on. Cost benefit analysis

help the organisation to maintain their product demand in recent market. The demerit of this

diagram is the management team also cannot create the long term strategy and future strategy

cannot be prepared by following this diagram.

Quality table

Roslender and Hart (2013, p.270) demonstrated that this table focuses on the relationship

between the two or more elements in the enterprise. At each intersection the elements relation is

either present or absent. Thus, the management team can easily identify the strength and

weakness of the internal environment in the organisation. Thus, the higher hierarchies modify

their strategy along with rules and regulation in order to increase the discipline level of the

enterprise. The management accounting officer raise use news bulletins and magazines in order

to report the general manager to take the necessary steps to diminish the negative issues.

Publications of market research by the accounting officer help the general manager to manage

these negative issues of the organisation and increase their recognition and profit margin in the

recent market.

Activity network figure

This diagram helps the account manager to discuss the negative issues with the general manager

and mitigate the issues of the organisation. This decrement of negative issues increases their

identification in global markets. Bharadwaj et al. (2013, p.90) opined that the account officer

uses the long sequences of the task in order to manage the complex activities of the enterprise.

Thus, the general manager can modify the rules of the enterprise which diminishes the rate of the

negative issues from the organization. With the help if this diagram the higher hierarchy can set

schedule of different task in the enterprise. It also increases the interaction with the higher and

14

the negative issues of the stakeholders easily.

Prioritization matrix

Oliver (2017, p.713) commented that the management team of organisation divided the negative

issues of the organisation according to its weighted criteria. It follows the combination of the

matrix and tree diagram in order to raise the identification of the enterprise in global market. The

creditor always creates a pressure to increase the production rate and the profit margin of Pacific

Computers. The management team can easily perform the cost benefits analysis, time

management strategy which includes the importance of urgency and so on. Cost benefit analysis

help the organisation to maintain their product demand in recent market. The demerit of this

diagram is the management team also cannot create the long term strategy and future strategy

cannot be prepared by following this diagram.

Quality table

Roslender and Hart (2013, p.270) demonstrated that this table focuses on the relationship

between the two or more elements in the enterprise. At each intersection the elements relation is

either present or absent. Thus, the management team can easily identify the strength and

weakness of the internal environment in the organisation. Thus, the higher hierarchies modify

their strategy along with rules and regulation in order to increase the discipline level of the

enterprise. The management accounting officer raise use news bulletins and magazines in order

to report the general manager to take the necessary steps to diminish the negative issues.

Publications of market research by the accounting officer help the general manager to manage

these negative issues of the organisation and increase their recognition and profit margin in the

recent market.

Activity network figure

This diagram helps the account manager to discuss the negative issues with the general manager

and mitigate the issues of the organisation. This decrement of negative issues increases their

identification in global markets. Bharadwaj et al. (2013, p.90) opined that the account officer

uses the long sequences of the task in order to manage the complex activities of the enterprise.

Thus, the general manager can modify the rules of the enterprise which diminishes the rate of the

negative issues from the organization. With the help if this diagram the higher hierarchy can set

schedule of different task in the enterprise. It also increases the interaction with the higher and

14

lower hierarchy. Performance level and creativity of the worker is also increased. Demerit of this

diagram is it doesn't help the enterprise to solve the external issues of the enterprise.

LO4:

P5: Comparison of organizations and why it should adopt management accounting

techniques

Factors that influence the organization to adopt the technique of management accounting are as

follows:

Financial rules of reporting

These reporting rules help the organisation to adopt the different technique of costing technique.

The variable costing, overhead costing, adsorption costs and so on are included in the budgetary

report of the enterprise. The journals and magazines help the organisation to tackle the negative

issues of the organisation. Production cost can be varied according to the need of the

organisation. The project managers manage the information of the magazines and journals in

order to create a perfect strategy. The advancement of technology helps it to increase their

interaction and communication between the stakeholders and the company. Strategy is created in

order to meet the recent trends of the customers and increase their profit margin.

Inventory management

Schuler and MacMillan (2014, p.250) stated that this management focuses on the risks and the

negative issues of the enterprise. The management teams follow the feedback of the stakeholders

and modify their strategy. They took help from the internal journals, magazines and other

gadgets in order to create the perfect strategy. Discussions with the higher and lower hierarchy

diminish the negative issues of the strategy and make it much more helpful for the organisation.

Economic orders technique help the enterprise to manage cost of the production in the enterprise.

This management helps the organisation to diminish the production costs and increase their

profit margin and identification in global market. Quality product and services raises the

customer satisfaction and raise their identification in recent market. Thus, Pacific Computers can

easily compete with other enterprise present in the recent market.

Strategy management of accounting

Shrivastava (2015, p.200) illustrated that this management focuses on the external factors of the

enterprise. The budget of the enterprise depends on the competitor's products, products demands

among recent users and so on. It helps the enterprise to increase the interaction with the suppliers

15

diagram is it doesn't help the enterprise to solve the external issues of the enterprise.

LO4:

P5: Comparison of organizations and why it should adopt management accounting

techniques

Factors that influence the organization to adopt the technique of management accounting are as

follows:

Financial rules of reporting

These reporting rules help the organisation to adopt the different technique of costing technique.

The variable costing, overhead costing, adsorption costs and so on are included in the budgetary

report of the enterprise. The journals and magazines help the organisation to tackle the negative

issues of the organisation. Production cost can be varied according to the need of the

organisation. The project managers manage the information of the magazines and journals in

order to create a perfect strategy. The advancement of technology helps it to increase their

interaction and communication between the stakeholders and the company. Strategy is created in

order to meet the recent trends of the customers and increase their profit margin.

Inventory management

Schuler and MacMillan (2014, p.250) stated that this management focuses on the risks and the

negative issues of the enterprise. The management teams follow the feedback of the stakeholders

and modify their strategy. They took help from the internal journals, magazines and other

gadgets in order to create the perfect strategy. Discussions with the higher and lower hierarchy

diminish the negative issues of the strategy and make it much more helpful for the organisation.

Economic orders technique help the enterprise to manage cost of the production in the enterprise.

This management helps the organisation to diminish the production costs and increase their

profit margin and identification in global market. Quality product and services raises the

customer satisfaction and raise their identification in recent market. Thus, Pacific Computers can

easily compete with other enterprise present in the recent market.

Strategy management of accounting

Shrivastava (2015, p.200) illustrated that this management focuses on the external factors of the

enterprise. The budget of the enterprise depends on the competitor's products, products demands

among recent users and so on. It helps the enterprise to increase the interaction with the suppliers

15

and consumers relationship. The target is set to the worker according to their experience and

conduct level by following the strategy. This management helps the organisation to raise their

identification, profit margin, workers performance.

Life cycle costing

Guilding et al. (2016, p.113) stated that this costing method track all the records of the products

and help the management team to perform the adequate research to improve their product

quality. The management team performs research which helps the enterprise to raise their

product quality and profit margin. Good product quality and the reasonable price attract more

customers to the products. The wages of the workers, production costs are also included in this

costing method. Thus, the life cycle method helps the enterprise to diminish the chaotic

behaviour from the enterprise and raises the disciplinary attitude in the enterprise. Discipline and

respect for each other in the organisation diminish the ego and grudges from the enterprise.

Benchmarking

The management teams perform industry analysis by the help of twitter, magazines, journals,

newspaper and so on in order to create a long term and systematic strategy. (2014, p.39)

mentioned that systematic strategy help the enterprise to increase their profit margin and

performance level of the workers. Good performance and creativity of the workers help the

organisation to increase their profit margin and identification in global market. Market analysis

helps the enterprise to compete with their competitors easily in the recent market.

Conclusion

Pacific computers use different management tools in order to control the negative issues of the

enterprise. The management team of the organisation performs market analysis in order to create

a perfect strategy. The modifications of the enterprise’s rules depend on the macro and micro

factors of the company. Constant research and notification of the strategy help the enterprise to

meet the recent trends of the organisation. Good interactions with the stakeholders help the

enterprise to raise their recognition in global market.

From

Management accounting officer

16

conduct level by following the strategy. This management helps the organisation to raise their

identification, profit margin, workers performance.

Life cycle costing

Guilding et al. (2016, p.113) stated that this costing method track all the records of the products

and help the management team to perform the adequate research to improve their product

quality. The management team performs research which helps the enterprise to raise their

product quality and profit margin. Good product quality and the reasonable price attract more

customers to the products. The wages of the workers, production costs are also included in this

costing method. Thus, the life cycle method helps the enterprise to diminish the chaotic

behaviour from the enterprise and raises the disciplinary attitude in the enterprise. Discipline and

respect for each other in the organisation diminish the ego and grudges from the enterprise.

Benchmarking

The management teams perform industry analysis by the help of twitter, magazines, journals,

newspaper and so on in order to create a long term and systematic strategy. (2014, p.39)

mentioned that systematic strategy help the enterprise to increase their profit margin and

performance level of the workers. Good performance and creativity of the workers help the

organisation to increase their profit margin and identification in global market. Market analysis

helps the enterprise to compete with their competitors easily in the recent market.

Conclusion

Pacific computers use different management tools in order to control the negative issues of the

enterprise. The management team of the organisation performs market analysis in order to create

a perfect strategy. The modifications of the enterprise’s rules depend on the macro and micro

factors of the company. Constant research and notification of the strategy help the enterprise to

meet the recent trends of the organisation. Good interactions with the stakeholders help the

enterprise to raise their recognition in global market.

From

Management accounting officer

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Reference list

Aladwani, A.M., (2014). Change management strategies for successful ERP implementation.

Business Process management journal, 7(3), pp.266-275.

Barney, J.B., (2016). Organizational culture: can it be a source of sustained competitive

advantage?. Academy of management review, 11(3), pp.656-665.

Bharadwaj, S.G., Varadarajan, P.R. and Fahy, J., (2013). Sustainable competitive advantage in

service industries: a conceptual model and research propositions. The Journal of Marketing,

12(8), pp.83-99.

Dierickx, I. and Cool, K., (2014). Asset stock accumulation and sustainability of competitive

advantage. Management science, 35(12), pp.1504-1511.

Dyer, J.H. and Singh, H., (2013). The relational view: Cooperative strategy and sources of

interorganizational competitive advantage. Academy of management review, 23(4), pp.660-679.

Ellram, L.M. and Siferd, S.P., (2015). Total cost of ownership: a key concept in strategic cost

management decisions. Journal of business logistics, 19(1), p.55.

Fisman, D.N., Reilly, D.T., Karchmer, A.W. and Goldie, S.J., (2014). Clinical effectiveness and

cost-effectiveness of 2 management strategies for infected total hip arthroplasty in the elderly.

Clinical Infectious Diseases, 32(3), pp.419-430.

Flynn, B.B., Schroeder, R.G. and Sakakibara, S., (2015). The impact of quality management

practices on performance and competitive advantage. Decision sciences, 26(5), pp.659-691.

Govindarajan, V. and Shank, J.K., (2014). Strategic cost management: tailoring controls to

strategies. Journal of Cost Management, 6(3), pp.14-25.

Guilding, C., Cravens, K.S. and Tayles, M., (2016). An international comparison of strategic

management accounting practices. Management Accounting Research, 11(1), pp.113-135.

Lascu, D.N., (2014). Total global strategy: Managing for worldwide competitive advantage.

Journal of Marketing, 58(3), p.121-125.

Mahoney, J.T. and Pandian, J.R., (2013). The resource‐based view within the conversation of

strategic management. Strategic management journal, 13(5), pp.363-380.

Manuj, I. and Mentzer, J.T., (2015). Global supply chain risk management strategies.

International Journal of Physical Distribution & Logistics Management, 38(3), pp.192-223.

17

Aladwani, A.M., (2014). Change management strategies for successful ERP implementation.

Business Process management journal, 7(3), pp.266-275.

Barney, J.B., (2016). Organizational culture: can it be a source of sustained competitive

advantage?. Academy of management review, 11(3), pp.656-665.

Bharadwaj, S.G., Varadarajan, P.R. and Fahy, J., (2013). Sustainable competitive advantage in

service industries: a conceptual model and research propositions. The Journal of Marketing,

12(8), pp.83-99.

Dierickx, I. and Cool, K., (2014). Asset stock accumulation and sustainability of competitive

advantage. Management science, 35(12), pp.1504-1511.

Dyer, J.H. and Singh, H., (2013). The relational view: Cooperative strategy and sources of

interorganizational competitive advantage. Academy of management review, 23(4), pp.660-679.

Ellram, L.M. and Siferd, S.P., (2015). Total cost of ownership: a key concept in strategic cost

management decisions. Journal of business logistics, 19(1), p.55.

Fisman, D.N., Reilly, D.T., Karchmer, A.W. and Goldie, S.J., (2014). Clinical effectiveness and

cost-effectiveness of 2 management strategies for infected total hip arthroplasty in the elderly.

Clinical Infectious Diseases, 32(3), pp.419-430.

Flynn, B.B., Schroeder, R.G. and Sakakibara, S., (2015). The impact of quality management

practices on performance and competitive advantage. Decision sciences, 26(5), pp.659-691.

Govindarajan, V. and Shank, J.K., (2014). Strategic cost management: tailoring controls to

strategies. Journal of Cost Management, 6(3), pp.14-25.

Guilding, C., Cravens, K.S. and Tayles, M., (2016). An international comparison of strategic

management accounting practices. Management Accounting Research, 11(1), pp.113-135.

Lascu, D.N., (2014). Total global strategy: Managing for worldwide competitive advantage.

Journal of Marketing, 58(3), p.121-125.

Mahoney, J.T. and Pandian, J.R., (2013). The resource‐based view within the conversation of

strategic management. Strategic management journal, 13(5), pp.363-380.

Manuj, I. and Mentzer, J.T., (2015). Global supply chain risk management strategies.

International Journal of Physical Distribution & Logistics Management, 38(3), pp.192-223.

17

Oliver, C., (2017). Sustainable competitive advantage: Combining institutional and resource-

based views. Strategic management journal, 12(9), pp.697-713.

Roslender, R. and Hart, S.J., (2013). Integrating management accounting and marketing in the

pursuit of competitive advantage: the case for strategic management accounting. Critical

Perspectives on Accounting, 13(2), pp.255-277.

Schuler, R.S. and Jackson, S.E., (2017). Linking competitive strategies with human resource

management practices. The Academy of Management Executive (1987-1989), pp.207-219.

Schuler, R.S. and MacMillan, I.C., (2014). Gaining competitive advantage through human

resource management practices. Human Resource Management, 23(3), pp.241-255.

Shank, J.K. and Govindarajan, V., (2014). Strategic cost analysis of technological investments.

Sloan Management Review, 34(1), p.39-45.

Shrivastava, P., (2015). Environmental technologies and competitive advantage. Strategic

management journal, 16(1), pp.183-200.

Shukla, R.K. and Clement, J., (2017). A comparative analysis of revenue and cost-management

strategies of not-for-profit and for-profit hospitals. Journal of Healthcare Management, 42(1),

pp.117-134.

Silvi, R. and Cuganesan, S., (2016). Investigating the management of knowledge for competitive

advantage: a strategic cost management perspective. Journal of intellectual capital, 7(3), pp.309-

323.

Simons, R., (2013). The role of management control systems in creating competitive advantage:

new perspectives. Accounting, organizations and society, 15(1-2), pp.127-143.

Wheelwright, S.C., (2013). Reflecting corporate strategy in manufacturing decisions. Business

horizons, 21(1), pp.57-66.

White, R.E., (2016). Generic business strategies, organizational context and performance: An

empirical investigation. Strategic Management Journal, 7(3), pp.217-231.

18

based views. Strategic management journal, 12(9), pp.697-713.

Roslender, R. and Hart, S.J., (2013). Integrating management accounting and marketing in the

pursuit of competitive advantage: the case for strategic management accounting. Critical

Perspectives on Accounting, 13(2), pp.255-277.

Schuler, R.S. and Jackson, S.E., (2017). Linking competitive strategies with human resource

management practices. The Academy of Management Executive (1987-1989), pp.207-219.

Schuler, R.S. and MacMillan, I.C., (2014). Gaining competitive advantage through human

resource management practices. Human Resource Management, 23(3), pp.241-255.

Shank, J.K. and Govindarajan, V., (2014). Strategic cost analysis of technological investments.

Sloan Management Review, 34(1), p.39-45.

Shrivastava, P., (2015). Environmental technologies and competitive advantage. Strategic

management journal, 16(1), pp.183-200.

Shukla, R.K. and Clement, J., (2017). A comparative analysis of revenue and cost-management

strategies of not-for-profit and for-profit hospitals. Journal of Healthcare Management, 42(1),

pp.117-134.

Silvi, R. and Cuganesan, S., (2016). Investigating the management of knowledge for competitive

advantage: a strategic cost management perspective. Journal of intellectual capital, 7(3), pp.309-

323.

Simons, R., (2013). The role of management control systems in creating competitive advantage:

new perspectives. Accounting, organizations and society, 15(1-2), pp.127-143.

Wheelwright, S.C., (2013). Reflecting corporate strategy in manufacturing decisions. Business

horizons, 21(1), pp.57-66.

White, R.E., (2016). Generic business strategies, organizational context and performance: An

empirical investigation. Strategic Management Journal, 7(3), pp.217-231.

18

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.